BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

+ Plus / – Minus Two Weeks

Stock market crashes have long been associated with the fall season, particularly October, which has earned a reputation as a month of financial turmoil. While crashes can occur at any time, the clustering of several historic downturns in autumn has led many investors to believe that markets are more vulnerable during this period.

Historical Patterns of Fall Crashes

Some of the most devastating collapses in financial history have taken place in the fall. The Wall Street Crash of 1929 began in late October and marked the start of the Great Depression. In October 1987, markets experienced “Black Monday,” when the Dow Jones Industrial Average plunged more than 20% in a single day. More recently, the global financial crisis of 2008 saw some of its steepest declines in September and October. These events have cemented autumn’s reputation as a season of heightened risk.

Why the Fall Is Riskier

Several factors contribute to the perception that fall is a dangerous time for markets:

Investor psychology: The memory of past crashes in October can heighten anxiety, making traders more prone to panic selling.

Fiscal cycles: Many institutional investors close their books at the end of September, leading to portfolio adjustments and sell-offs in October.

Economic data releases: Key reports on employment, corporate earnings, and government budgets often arrive in the fall, influencing sentiment.

Global events: Political and economic developments frequently coincide with autumn months, adding uncertainty.

Statistical Evidence and Skepticism

Despite the historical examples, statistical studies suggest that crashes are not inherently more likely in October than in other months. Market downturns are rare events, and their clustering in autumn may be more coincidence than causation. Crashes have also occurred outside the fall, such as the bursting of the dot-com bubble in spring 2000 and the COVID-19 crash in March 2020. This suggests that the so-called “October Effect” may be more psychological than empirical.

Lessons for Investors

Whether or not fall crashes are statistically more likely, the historical record offers important lessons:

Diversify investments to reduce vulnerability to sudden downturns.

Avoid panic selling, since many crashes are followed by rapid recoveries.

Prepare for volatility, as autumn often brings heightened uncertainty.

Conclusion

Stock market crashes are not guaranteed to happen in the fall, but history has made October synonymous with financial turmoil. The clustering of major downturns during this season has created a psychological bias that influences investor behavior. Whether coincidence or pattern, the lesson is clear: autumn is a time when vigilance, discipline, and preparation are especially important for market participants.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

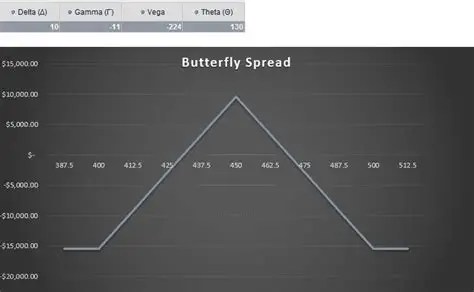

Investing in Butterfly Spreads

Options trading provides investors with a wide range of strategies to suit different market conditions. One of the more refined approaches is the butterfly spread, a strategy designed to profit from stability in the price of an underlying asset. It combines multiple option contracts at different strike prices to create a position with limited risk and limited reward. The name comes from the shape of its profit-and-loss diagram, which resembles the wings of a butterfly.

Structure of the Strategy

A typical butterfly spread involves four options contracts with three strike prices. In a long call butterfly spread, the investor buys one call at a lower strike, sells two calls at a middle strike, and buys one call at a higher strike. This creates a payoff that peaks if the underlying asset closes at the middle strike price. Losses are capped at the initial premium paid, while profits are capped at the difference between the strikes minus the premium.

Variations of Butterfly Spreads

Butterfly spreads can be built with calls, puts, or a mix of both:

Long Call Butterfly: Profits if the asset stays near the middle strike.

Long Put Butterfly: Similar structure but using puts.

Iron Butterfly: Combines calls and puts, selling an at-the-money straddle and buying protective wings.

Reverse Iron Butterfly: Designed to benefit from sharp price movements and volatility.

Each variation adapts to different market expectations, but all share the principle of balancing risk and reward.

Benefits of Butterfly Spreads

Defined Risk: The maximum loss is known upfront.

Cost Efficiency: Requires less capital than outright buying options.

Neutral Outlook: Works best when the investor expects little price movement.

Flexibility: Can be tailored to different market conditions with calls, puts, or combinations.

Drawbacks and Risks

Limited Profit Potential: Gains are capped, which may not appeal to aggressive traders.

Dependence on Timing: The strategy works only if the asset closes near the middle strike at expiration.

Complexity: Requires careful planning of strike prices and expiration dates.

Example in Practice

Suppose a stock trades at $100, and the investor expects it to remain near that level. They could set up a butterfly spread with strikes at $95, $100, and $105. If the stock closes at $100, the strategy delivers maximum profit. If the stock moves significantly away from $100, the investor’s loss is limited to the premium paid. This makes the butterfly spread particularly useful in calm, low-volatility markets.

Conclusion

The butterfly spread is a disciplined options strategy that thrives in stable markets. It offers a balance between risk control and profit potential, making it attractive to traders who prefer structured outcomes. While the rewards are capped, the defined risk and cost efficiency make butterfly spreads a valuable tool for investors who anticipate minimal price movement and want to manage their exposure carefully.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Retirement planning has evolved significantly over the past several decades, with employers and employees seeking solutions that balance security, flexibility, and predictability. Among the various retirement plan options available today, cash balance plans stand out as a hybrid design that combines features of both traditional defined benefit pensions and defined contribution plans. Their unique structure makes them an attractive choice for employers aiming to provide meaningful retirement benefits while maintaining financial predictability.

At their core, cash balance plans are a type of defined benefit plan. Unlike traditional pensions, which promise retirees a monthly income based on years of service and final salary, cash balance plans define the benefit in terms of a hypothetical account balance. Each participant’s account grows annually through two components: a “pay credit” and an “interest credit.” The pay credit is typically a percentage of the employee’s salary or a flat dollar amount, while the interest credit is either a fixed rate or tied to an index such as U.S. Treasury yields. Although the account is hypothetical—meaning the funds are not actually segregated for each employee—the structure provides participants with a clear, understandable statement of their retirement benefit.

One of the primary advantages of cash balance plans is their transparency. Employees can easily track the growth of their account balance, much like they would with a 401(k). This clarity helps workers better understand the value of their retirement benefits and fosters a sense of ownership. Additionally, cash balance plans are portable: when employees leave a company, they can roll over the vested balance into an IRA or another qualified plan, ensuring continuity in retirement savings.

***

***

From the employer’s perspective, cash balance plans offer several benefits as well. Traditional pensions often create unpredictable liabilities, as they depend on factors such as longevity and investment performance. Cash balance plans, by contrast, provide more predictable costs because the employer commits to specific pay and interest credits. This predictability makes them easier to manage and budget for, particularly in industries where workforce mobility is high. Moreover, cash balance plans can be designed to reward long-term employees while still appealing to younger workers who value portability.

Despite these advantages, cash balance plans are not without challenges. Because they are defined benefit plans, employers bear the investment risk and must ensure the plan is adequately funded. Regulatory requirements, including nondiscrimination testing and funding rules, add complexity and administrative costs. Additionally, while cash balance plans are generally more equitable across generations of workers, transitions from traditional pensions to cash balance designs have sometimes sparked controversy, particularly among older employees who may perceive a reduction in benefits.

In recent years, cash balance plans have gained popularity among professional firms, such as law practices and medical groups, as well as small businesses seeking tax-efficient retirement solutions. These plans allow owners and highly compensated employees to accumulate larger retirement savings than would be possible under defined contribution limits, while still providing benefits to rank-and-file workers. As such, they serve as a valuable tool for both talent retention and financial planning.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

American Depository Receipts Defined

In the modern era of globalization, financial instruments that connect investors across borders have become indispensable. Among these, American Depository Receipts (ADRs) stand out as a powerful mechanism that allows U.S. investors to participate in foreign equity markets without the complexities of international trading. ADRs not only simplify access to global companies but also enhance the ability of foreign corporations to raise capital in the United States. This essay explores the origins, structure, regulatory frameworks, benefits, risks, and real-world examples of ADRs, highlighting their role in the integration of global finance.

Historical Development

The concept of ADRs emerged in 1927 when J.P. Morgan introduced the first ADR for the British retailer Selfridges. At the time, American investors faced significant hurdles in purchasing foreign shares, including currency conversion, unfamiliar trading practices, and regulatory differences. ADRs solved these problems by creating a U.S.-based certificate that represented ownership in foreign shares, denominated in dollars, and traded on American exchanges.

Over the decades, ADRs expanded rapidly, especially during the post-World War II era when globalization accelerated. By the late 20th century, ADRs had become a mainstream tool for accessing international equities, with companies from Europe, Asia, and Latin America increasingly using them to tap into U.S. capital markets.

Structure and Mechanics

An ADR is issued by a U.S. depositary bank, which holds the underlying shares of a foreign company in custody. Each ADR corresponds to a specific number of shares—sometimes one, sometimes multiple, or even a fraction. Investors buy and sell ADRs in U.S. dollars, and dividends are paid in dollars as well, eliminating the need for currency conversion.

Key structural features include:

Depositary Banks: Institutions such as J.P. Morgan, Citibank, and Bank of New York Mellon act as custodians and issuers of ADRs.

ADR Ratios: The number of foreign shares represented by one ADR can vary, allowing flexibility in pricing.

Trading Platforms: ADRs can be listed on major exchanges like the NYSE or NASDAQ, or traded over-the-counter.

Regulatory Framework

ADRs are subject to U.S. securities regulations, which vary depending on the level of ADR issued:

Level I ADRs: Traded over-the-counter, requiring minimal disclosure. They are primarily used for visibility rather than fundraising.

Level II ADRs: Listed on U.S. exchanges, requiring compliance with SEC reporting standards, including reconciliation of financial statements to U.S. GAAP or IFRS.

Level III ADRs: Allow foreign companies to raise capital directly in U.S. markets through public offerings. These require the highest level of regulatory compliance, including registration with the SEC and adherence to corporate governance standards.

This tiered system ensures that investors receive appropriate levels of transparency while giving foreign companies flexibility in their approach to U.S. markets.

Benefits for Investors

ADRs offer numerous advantages to American investors:

Convenience: Investors can buy shares in foreign companies without dealing with foreign exchanges or currencies.

Diversification: ADRs provide access to global firms across industries, enhancing portfolio diversification.

Transparency: ADRs listed on U.S. exchanges must comply with SEC regulations, ensuring reliable financial reporting.

Liquidity: ADRs trade on familiar platforms, making them easily accessible to retail and institutional investors alike.

Benefits for Companies

Foreign corporations also benefit significantly from ADRs:

Access to Capital: ADRs open the door to the world’s largest pool of investors.

Global Visibility: Listing in the U.S. enhances reputation and credibility.

Improved Liquidity: Shares become more widely traded, increasing market efficiency.

Investor Base Diversification: Companies can attract both domestic and international investors, reducing reliance on local markets.

Risks and Challenges

Despite their advantages, ADRs carry certain risks:

Currency Risk: ADR values are tied to foreign shares denominated in local currencies, making them vulnerable to exchange rate fluctuations.

Political and Economic Risk: Instability in the issuing company’s home country can affect performance.

Taxation: Dividends may be subject to foreign withholding taxes before conversion to U.S. dollars.

Regulatory Differences: Even with SEC oversight, differences in accounting standards and corporate governance can pose challenges.

Case Studies

1. Alibaba Group (China) Alibaba’s ADRs, listed on the NYSE in 2014, marked one of the largest IPOs in history, raising $25 billion. This demonstrated the power of ADRs to connect Chinese companies with American investors, despite regulatory complexities between the two countries.

2. Toyota Motor Corporation (Japan) Toyota’s ADRs have long provided U.S. investors with access to one of the world’s largest automakers. By listing ADRs, Toyota expanded its investor base and strengthened its global presence.

3. Royal Dutch Shell (Netherlands/UK) Shell’s ADRs illustrate how multinational corporations use ADRs to maintain visibility in U.S. markets while managing complex cross-border structures.

The Role of ADRs in Global Finance

ADRs embody the globalization of capital markets. They facilitate cross-border investment, enhance market efficiency, and foster economic integration. For investors, ADRs represent a gateway to international diversification. For companies, they provide access to the deepest capital markets in the world.

Conclusion

American Depositary Receipts are more than just financial instruments; they are symbols of global interconnectedness. By bridging the gap between U.S. investors and foreign companies, ADRs have reshaped the landscape of international finance. They balance convenience with exposure to global risks, offering both opportunities and challenges. As globalization continues to evolve, ADRs will remain a vital tool for investors and corporations alike, reinforcing their role as a cornerstone of modern capital markets.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Role of Volatility Indices in Financial Markets

Volatility is often described as the pulse of financial markets, reflecting the collective emotions of investors as they respond to uncertainty, risk, and opportunity. Among the many tools designed to measure this phenomenon, the CBOE Volatility Index, or VIX, stands out as the most widely recognized. Dubbed the “fear gauge,” the VIX captures market expectations of near-term volatility in the S&P 500, derived from options pricing. Its movements often mirror investor sentiment: rising sharply during periods of crisis and falling when confidence returns. Yet, the VIX is not alone. A family of volatility indices exists across global markets, each offering unique insights into sector-specific or regional risk.

The importance of volatility indices lies in their ability to quantify uncertainty. Traditional measures such as historical volatility look backward, analyzing past price fluctuations. In contrast, indices like the VIX are forward-looking, reflecting implied volatility based on options markets. This distinction makes them invaluable for traders, portfolio managers, and policymakers. For example, a sudden spike in the VIX often signals heightened fear, prompting investors to hedge positions or reduce exposure to equities. Conversely, a low VIX suggests complacency, though it can also precede unexpected shocks.

Beyond the VIX, other indices provide complementary perspectives. The VXN tracks volatility in the Nasdaq-100, often dominated by technology stocks. Because the tech sector is highly sensitive to innovation cycles and regulatory changes, the VXN can diverge significantly from the VIX, highlighting sector-specific risks. Similarly, the RVX measures volatility in the Russell 2000, offering a window into small-cap stocks that are more vulnerable to domestic economic conditions. Internationally, indices such as the VSTOXX in Europe and India VIX extend this framework globally, allowing investors to compare risk sentiment across regions. Together, these indices form a mosaic of market psychology, enabling a more nuanced understanding of global financial stability.

Volatility indices also play a crucial role in risk management. Derivatives linked to these indices, such as futures and exchange-traded products, allow investors to hedge against sudden downturns. For instance, during the 2008 financial crisis, demand for VIX futures surged as investors sought protection from extreme market swings. More recently, volatility products have become popular among retail traders, though their complexity and tendency to lose value over time make them risky for long-term holding.

Critics argue that volatility indices can be misleading. A low VIX does not guarantee stability, and a high VIX does not always signal disaster. Moreover, the rise of volatility-linked products has occasionally amplified market stress, as seen during the “Volmageddon” event of February 2018, when inverse volatility ETFs collapsed. These episodes underscore the need for caution: volatility indices are powerful tools, but they must be used with a clear understanding of their limitations.

In conclusion, volatility indices such as the VIX serve as vital instruments for gauging investor sentiment and managing risk. They provide a forward-looking measure of uncertainty, complementing traditional metrics and offering insights across sectors and regions. While not infallible, their role in modern finance is undeniable.

For traders, analysts, and policymakers alike, these indices are more than numbers on a screen—they are reflections of the market’s collective psyche, guiding decisions in times of both calm and crisis.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Silver occupies a distinctive position within the realm of investment assets, functioning simultaneously as a precious metal and an industrial commodity. This dual nature imbues silver with characteristics that make it a valuable component of a diversified portfolio, offering both defensive qualities and growth potential. While its volatility necessitates careful consideration, silver’s unique attributes warrant attention from investors seeking balance between risk mitigation and opportunity.

Silver as a Hybrid Asset

Unlike gold, which is primarily regarded as a store of value, silver derives a substantial portion of its demand from industrial applications. It is indispensable in sectors such as electronics, renewable energy, and medical technology, with photovoltaic cells in solar panels representing a particularly significant driver of consumption. This industrial utility ensures that silver’s price is influenced not only by macroeconomic uncertainty but also by technological innovation and global manufacturing trends. Consequently, silver provides investors with exposure to both traditional safe-haven dynamics and cyclical industrial growth.

Accessibility and Cost Efficiency

Silver’s affordability relative to gold enhances its appeal to a broad spectrum of investors. Physical silver, in the form of coins and bars, allows individuals with modest capital to participate in the precious metals market. Moreover, financial instruments such as exchange-traded funds (ETFs) and mining equities provide liquid and scalable avenues for investment. This accessibility ensures that silver can serve as an entry point into alternative assets, particularly for those seeking to hedge against inflation without committing substantial resources.

Inflation Hedge and Currency Protection

Historically, silver has demonstrated resilience during periods of inflation and currency depreciation. As fiat currencies lose purchasing power, tangible assets such as silver tend to appreciate, preserving wealth for investors. Although gold is often considered the primary hedge, silver’s similar properties, combined with its lower cost, render it a practical complement. In times of geopolitical instability or monetary expansion, silver can function as a safeguard against systemic risks.

Volatility and Associated Risks

Despite its advantages, silver is characterized by pronounced price volatility. Its smaller market size relative to gold renders it more susceptible to speculative trading and abrupt shifts in investor sentiment. Furthermore, fluctuations in industrial demand can amplify short-term price movements. While this volatility can generate significant returns, it also exposes investors to heightened risk. Accordingly, silver is best employed as a long-term holding within a diversified portfolio rather than as a vehicle for short-term speculation.

Portfolio Diversification and Investment Vehicles

Incorporating silver into a portfolio enhances diversification by introducing an asset class with low correlation to equities and fixed income securities. This non-correlation reduces overall portfolio risk and provides stability during market downturns. Investors may access silver through several channels: physical bullion for tangible ownership, ETFs for liquidity, mining stocks for leveraged exposure, and futures contracts for advanced strategies. Each vehicle entails distinct risk-reward profiles, enabling investors to tailor their approach according to objectives and tolerance.

Conclusion

Silver’s dual identity as both a precious metal and an industrial commodity distinguishes it from other investment assets. Its affordability, inflation-hedging capacity, and diversification benefits make it a compelling addition to portfolios. While volatility requires prudent management, silver’s potential to balance defensive and growth-oriented strategies underscores its enduring relevance in contemporary investment practice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

The velocity of money is a fundamental concept in macroeconomics that measures how quickly money circulates through the economy. It reflects the frequency with which a unit of currency is used to purchase goods and services within a given time period. This metric is crucial for understanding economic activity, inflation, and the effectiveness of monetary policy.

At its core, the velocity of money is calculated using the formula:

This equation shows how many times money turns over in the economy to support a given level of economic output. For example, if the GDP is $20 trillion and the money supply (say, M2) is $10 trillion, the velocity is 2—meaning each dollar is used twice in a year to purchase goods and services.

There are different measures of money supply used in this calculation, most commonly M1 and M2. M1 includes the most liquid forms of money, such as cash and checking deposits, while M2 includes M1 plus savings accounts and other near-money assets. The choice of which measure to use depends on the context and the specific economic analysis being conducted.

The velocity of money is influenced by several factors:

Consumer and business confidence: When people feel optimistic about the economy, they are more likely to spend rather than save, increasing velocity.

Interest rates: Higher interest rates can encourage saving and reduce spending, lowering velocity. Conversely, lower rates can stimulate borrowing and spending.

Inflation expectations: If people expect prices to rise, they may spend more quickly, increasing velocity.

Technological and structural changes: Innovations in digital payments and shifts in consumer behavior can also affect how quickly money moves.

Historically, the velocity of money has fluctuated with economic cycles. During periods of economic expansion, velocity tends to rise as spending increases. In contrast, during recessions or periods of uncertainty, velocity often falls as consumers and businesses hold onto cash. For instance, during the 2008 financial crisis and the early stages of the COVID-19 pandemic, velocity dropped sharply due to reduced consumer spending and increased saving.

In recent years, the U.S. has experienced persistently low velocity, even amid significant increases in the money supply. This phenomenon has puzzled economists and raised questions about the effectiveness of monetary policy. Despite aggressive stimulus measures, much of the new money has remained in savings or financial markets rather than circulating through the real economy.

Understanding the velocity of money is essential for policymakers. A low velocity may signal weak demand and justify expansionary fiscal or monetary policies. Conversely, a high velocity could indicate overheating and the need for tightening measures to prevent inflation.

In conclusion, the velocity of money is a dynamic indicator of economic vitality. It helps economists and central banks assess the flow of money, the strength of demand, and the potential for inflation.

While often overlooked by the public, it plays a vital role in shaping economic policy and understanding the broader health of the economy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

For generations, the prevailing belief in healthcare has been that physicians [MD, DO and DPM], with their high salaries and prestige, inevitably retire wealthier than nurses. Yet this assumption overlooks the financial realities of different nursing specialties and the long‑term impact of debt, lifestyle, and retirement planning. In fact, some Registered Nurses (RNs)—particularly Certified Registered Nurse Anesthetists (CRNAs), visiting nurses, and those who participate in structured pay programs like the Baylor plan—can retire richer than physicians. The reasons lie in the interplay of education costs, career flexibility, income potential, and disciplined financial planning.

Education Costs and Debt Burden

One of the most decisive factors shaping retirement wealth is the cost of education. Physicians often spend over a decade in training, including undergraduate studies, medical school, and residency. This path not only delays their earning years but also saddles them with substantial student debt. The median medical school debt in the United States exceeds $200,000, and many physicians spend years paying it down.

By contrast, RNs typically complete their training in two to four years, with advanced practice nurses such as CRNAs requiring graduate‑level education. Even so, their debt burden is far lighter, often less than half of what physicians carry. This difference means nurses can begin earning earlier, save for retirement sooner, and avoid the crushing interest payments that erode physicians’ wealth. A CRNA who starts practicing in their late twenties may already be investing in retirement accounts while a physician is still in residency earning a modest stipend.

Income Potential of Specialized Nurses

While physicians generally earn more annually than nurses, the gap is narrower in certain specialties. CRNAs, for example, are among the highest‑paid nursing professionals, with average salaries often exceeding $200,000 per year. This places them in direct competition with some physician specialties, especially primary care doctors, who may earn similar or even lower salaries.

Visiting nurses also benefit from unique financial advantages. Many work on flexible schedules, contract arrangements, or per‑visit compensation models. This allows them to maximize income while minimizing burnout. By avoiding the overhead costs of private practice and the administrative burdens physicians face, visiting nurses can channel more of their earnings directly into savings and investments.

When combined with lower debt and earlier career starts, these income streams can compound into significant retirement wealth.

The Baylor plan, a structured pay program used by some hospitals, allows nurses to work full‑time hours compressed into fewer days—often weekends—while still receiving full‑time pay and benefits. This arrangement provides several financial advantages. First, it enables nurses to earn competitive wages while freeing up weekdays for additional work, education, or entrepreneurial ventures. Second, it reduces commuting and childcare costs, allowing more income to be saved. Third, the plan often includes robust retirement benefits, such as employer‑matched contributions to 401(k) or pension programs.

Nurses who consistently participate in such structured pay plans can accumulate substantial nest eggs, often surpassing physicians who delay retirement savings due to debt repayment or lifestyle inflation. The Baylor plan highlights the importance of systematic investing: by automating contributions and focusing on long‑term growth, nurses can harness the power of compound interest. A nurse who invests steadily for 35 years may accumulate more wealth than a physician who begins saving late and inconsistently, despite earning a higher salary.

Lifestyle and Work‑Life Balance

Another overlooked factor is lifestyle. Physicians often face grueling schedules, high stress, and the temptation to maintain expensive lifestyles commensurate with their social status. Luxury homes, cars, and vacations can erode their financial base. Nurses, while not immune to lifestyle inflation, often maintain more modest spending habits.

Visiting nurses, in particular, enjoy flexibility that allows them to balance work with personal life. This reduces burnout and healthcare costs while enabling consistent employment into later years. By living within their means and prioritizing savings, nurses can accumulate wealth steadily without the financial pitfalls that sometimes accompany physician lifestyles.

Retirement Wealth Beyond Salary

Retirement wealth is not solely determined by annual income. It is shaped by debt management, savings discipline, investment strategies, and lifestyle choices. Nurses who leverage high‑paying specialties like anesthesia, flexible arrangements like visiting nursing, and structured programs like the Baylor plan can outperform physicians in these areas.

Consider two professionals: a physician earning $250,000 annually but burdened by $200,000 in debt and high living expenses, and a CRNA earning $200,000 with minimal debt and disciplined savings. Over decades, the CRNA may accumulate more net wealth, retire earlier, and enjoy greater financial security.

Conclusion

The assumption that physicians always retire richer than nurses is outdated. While physicians command higher salaries, their delayed earnings, heavy debt, and lifestyle pressures often undermine long‑term wealth. Nurses, particularly CRNAs, visiting nurses, and those who participate in structured pay programs like the Baylor plan, can retire wealthier by combining lower debt, earlier savings, competitive incomes, and disciplined financial planning.

Ultimately, retirement wealth is not about prestige but about strategy. Nurses who recognize this truth and act accordingly may find themselves enjoying more financial freedom than the very physicians they once assisted.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Physicians are increasingly facing car repossessions in 2025 due to rising debt, high vehicle prices, and economic pressures that are reshaping the financial landscape for medical professionals.

Traditionally viewed as financially secure, doctors are now among the growing number of Americans struggling to keep up with auto loan payments. The surge in car repossessions—expected to reach a record 10.5 million assignments by the end of 2025—has not spared the medical community. While physicians often earn higher-than-average incomes, they also carry significant financial burdens, including student loan debt, practice overhead, and personal expenses. These pressures are being amplified by macroeconomic forces such as inflation, high interest rates, and stagnant reimbursement rates.

One of the key contributors to this trend is the soaring cost of vehicles. In 2025, the average price of a new car in the U.S. surpassed $50,000, a dramatic increase from just a decade ago. For physicians who rely on vehicles for commuting between hospitals, clinics, and private practices, owning a reliable car is not a luxury—it’s a necessity. However, the combination of high sticker prices and elevated interest rates—averaging 7.3% for used cars and 11.5% for new cars—has made financing increasingly difficult.

***

***

Even high-income professionals are not immune to the broader auto loan crisis. Subprime auto loan delinquencies reached 6.6% in early 2025, the highest rate in over 30 years.While physicians typically fall into the prime or super-prime credit categories, many are still affected by cash flow disruptions, especially those in private practice or rural areas where patient volumes and insurance reimbursements have declined. Additionally, younger doctors with substantial student debt may find themselves overleveraged, making it harder to keep up with car payments.

The emotional and professional toll of a car repossession can be significant. Beyond the embarrassment and logistical challenges, losing a vehicle can disrupt a physician’s ability to provide care, attend emergencies, or maintain a consistent work schedule. This can lead to further income loss, creating a vicious cycle of financial instability.

To combat this trend, some physicians are turning to financial advisors to restructure their debt, refinance auto loans, or downsize to more affordable vehicles. Others are advocating for systemic reforms, such as student loan forgiveness, higher Medicare reimbursements, and better financial literacy training during medical education.

In conclusion, the rise in car repossessions among doctors is a stark reminder that no profession is immune to economic volatility. As the cost of living continues to climb and financial pressures mount, even those in traditionally stable careers must adapt to protect their assets and livelihoods.

Addressing this issue requires both individual financial planning and broader policy changes to ensure that physicians can continue to serve their communities without the looming threat of personal financial collapse.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Say’s Law, named after the French economist Jean‑Baptiste Say, is a foundational idea in classical economics. Often summarized as “supply creates its own demand,” the law suggests that the act of producing goods and services inherently generates the income necessary to purchase them. This principle shaped economic thought throughout the 19th century and continues to influence debates about markets, government intervention, and the causes of economic crises.

Origins and Meaning Jean‑Baptiste Say introduced his law in the early 1800s in his Treatise on Political Economy. He argued that production is the source of demand: when producers create goods, they pay wages, rents, and profits, which in turn become purchasing power. In this view, general overproduction is impossible because every supply of goods corresponds to an equivalent demand. If imbalances occur, they are temporary and limited to specific sectors, not the economy as a whole.

Core Principles Say’s Law rests on several assumptions:

Markets are self‑correcting: Any surplus in one area leads to adjustments in prices and production.

Money is neutral: It serves only as a medium of exchange, not as a driver of demand.

Production drives prosperity: Economic growth depends on increasing output, not stimulating consumption.

No long‑term unemployment: Since supply creates demand, workers displaced in one industry will eventually find employment elsewhere.

These ideas aligned with classical economists’ belief in minimal government intervention and the efficiency of free markets.

Influence on Classical Economics Say’s Law became a cornerstone of classical economics, reinforcing the belief that recessions or depressions were temporary and self‑correcting. Economists like David Ricardo and John Stuart Mill adopted versions of the law, using it to argue against policies aimed at stimulating demand. The law supported laissez‑faire approaches, suggesting that governments should avoid interfering with markets, as production itself would ensure economic balance.

Criticism and Keynesian Revolution Say’s Law faced its greatest challenge during the Great Depression of the 1930s. Widespread unemployment and idle factories contradicted the idea that supply automatically generates demand. John Maynard Keynes famously rejected Say’s Law in his General Theory of Employment, Interest, and Money (1936). Keynes argued that demand, not supply, drives economic activity. He showed that insufficient aggregate demand could lead to prolonged recessions, requiring government intervention through fiscal and monetary policies.

Keynes’s critique marked a turning point in economics. While Say’s Law emphasized production, Keynesian economics highlighted consumption and demand management. This shift reshaped economic policy, leading to active government roles in stabilizing economies.

Modern Perspectives Today, Say’s Law is not accepted in its original form, but elements of it remain relevant. Supply‑side economists, for example, argue that policies encouraging production—such as tax cuts and deregulation—can stimulate growth. In contrast, Keynesians stress the importance of demand management. The debate reflects a broader tension in economics: whether prosperity depends more on producing goods or ensuring people have the means and willingness to buy them.

Conclusion: Say’s Law was a bold attempt to explain the self‑sustaining nature of markets. While its claim that “supply creates its own demand” proved too simplistic in the face of modern economic realities, it remains a vital part of the history of economic thought. The controversy surrounding Say’s Law highlights the evolving nature of economics, where theories are tested against real‑world crises and adapted to new circumstances. Even today, discussions of supply‑side versus demand‑side policies echo the enduring influence of Say’s original insight.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The singularity promises to revolutionize medicine by accelerating diagnostics, treatment, and longevity—but it also demands ethical vigilance and systemic transformation.

The concept of the technological singularity refers to a hypothetical future moment when artificial intelligence (AI) surpasses human intelligence, triggering exponential advances in technology. In medicine, this could mark a turning point where AI-driven systems outperform human clinicians in diagnosis, treatment planning, and even biomedical research. While the singularity remains speculative, its implications for healthcare are profound and multifaceted.

One of the most promising impacts is in diagnostics and precision medicine. AI systems trained on vast datasets of medical images, genetic profiles, and patient histories could detect diseases earlier and more accurately than human doctors. For example, algorithms already outperform radiologists in identifying certain cancers from imaging scans. As we approach the singularity, these systems may evolve into autonomous diagnostic agents capable of real-time analysis and personalized recommendations, tailored to each patient’s unique biology.

Another transformative area is drug discovery and development. Traditional pharmaceutical research is slow and costly, often taking over a decade to bring a new drug to market. AI could dramatically shorten this timeline by simulating molecular interactions, predicting therapeutic targets, and optimizing clinical trial designs. With superintelligent systems, the pace of innovation could accelerate to the point where treatments for currently incurable diseases—like Alzheimer’s or certain cancers—become feasible within months.

The singularity also opens doors to radical longevity and human enhancement. Advances in nanotechnology, genomics, and regenerative medicine may converge to extend human lifespan significantly. AI could help decode the aging process, identify biomarkers of cellular decline, and engineer interventions that slow or reverse it. Some theorists even envision a future where aging is treated as a curable condition, and mortality becomes a choice rather than a biological inevitability.

However, these breakthroughs come with serious ethical and societal challenges. Data privacy, algorithmic bias, and access inequality are critical concerns. If singularity-level AI is controlled by a few corporations or governments, it could exacerbate global health disparities. Moreover, the replacement of human clinicians with machines raises questions about empathy, trust, and accountability in care. Who is responsible when an AI makes a life-altering mistake?

To navigate this future responsibly, medicine must embrace interdisciplinary collaboration. Ethicists, technologists, clinicians, and policymakers must work together to ensure that AI systems are transparent, equitable, and aligned with human values. Regulatory frameworks must evolve to keep pace with innovation, and medical education must prepare practitioners to work alongside intelligent machines.

In conclusion, the singularity represents both a promise and a peril for medicine. It offers unprecedented opportunities to enhance human health, but also demands careful stewardship to avoid unintended consequences.

As we edge closer to this horizon, the challenge will be not just technological, but deeply human: to harness intelligence beyond our own in service of healing, compassion, and justice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

The Series 63 exam — the Uniform Securities State Law Examination — is a North American Securities Administrators Association (NASAA) exam administered by FINRA.

The exam consists of 60 scored questions and 5 unscored questions. Candidates have 75 minutes to complete the exam. In order for a candidate to pass the Series 63 exam, they must correctly answer at least 43 of the 60 scored questions.

Money is a powerful tool. It can provide security, open opportunities, and help build a fulfilling life. Yet, when mismanaged, it can quickly become a source of stress and regret. Understanding the worst ways to use money is essential for anyone who wants to avoid financial pitfalls and build lasting stability.

1. Impulse Spending

One of the most damaging habits is spending without thought. Buying items on impulse—whether it’s clothes, gadgets, or luxury goods—often leads to regret and wasted resources. These purchases rarely align with long‑term goals and can drain savings meant for emergencies or investments.

2. High‑Interest Debt

Credit cards and payday loans can trap people in cycles of debt. Paying 20% or more in interest means that even small purchases balloon into massive financial burdens. Using debt irresponsibly is one of the fastest ways to erode wealth.

3. Ignoring Savings and Investments

Failing to save for the future is another critical mistake. Without an emergency fund, unexpected expenses like medical bills or car repairs can derail financial stability. Similarly, neglecting investments means missing out on compound growth that builds wealth over time.

4. Chasing Get‑Rich‑Quick Schemes

From pyramid schemes to speculative “hot tips,” chasing unrealistic returns is a recipe for disaster. These schemes prey on greed and impatience, often leaving participants with nothing but losses. Sustainable wealth comes from patience and discipline, not shortcuts.

5. Overspending on Status

Many people waste money trying to impress others—buying luxury cars, designer clothes, or extravagant experiences they cannot afford. This pursuit of status often leads to debt and financial insecurity, while providing only fleeting satisfaction.

6. Neglecting Insurance

Skipping health, auto, or home insurance to save money may seem smart in the short term, but it can be catastrophic when disaster strikes. Without protection, one accident or emergency can wipe out years of savings.

7. Failing to Budget

Living without a plan is like sailing without a map. Without a budget, it’s easy to overspend, miss bills, or fail to allocate money toward goals. Budgeting is not restrictive—it’s empowering, because it ensures money is used intentionally.

8. Ignoring Education and Skills

Spending money without investing in personal growth is another hidden mistake. Education, training, and skill development often yield lifelong returns. Neglecting these opportunities can limit earning potential and financial independence.

Conclusion

The worst things to do with money often stem from short‑term thinking, lack of discipline, or the desire for instant gratification. Impulse spending, high‑interest debt, chasing schemes, and neglecting savings all undermine financial health. By avoiding these traps and focusing on budgeting, investing wisely, and protecting against risks, money can serve as a foundation for security and freedom rather than a source of stress.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

In the competitive world of financial services, attracting and retaining clients is a constant challenge. To stand out, many financial advisors employ strategic marketing tactics known as “loss leaders”—free or discounted services designed to showcase value and build trust. These offerings serve as entry points for potential clients, allowing advisors to demonstrate expertise and initiate long-term relationships.

One of the most common loss leaders is the free initial consultation. This no-obligation meeting gives prospective clients a chance to discuss their financial goals, ask questions, and get a feel for the advisor’s approach. For the advisor, it’s an opportunity to assess the client’s needs and present tailored solutions. While no revenue is generated from this meeting, it often leads to paid engagements once the client feels confident in the advisor’s capabilities.

Another popular tactic is offering a complimentary financial plan or portfolio review. These services provide tangible insights into a client’s current financial situation and suggest improvements. By delivering real value upfront, advisors build credibility and demonstrate their analytical skills. Clients who receive actionable advice are more likely to continue working with the advisor on a paid basis.

Educational content also plays a key role in loss leader strategy. Advisors frequently host free webinars, workshops, or seminars on topics like retirement planning, tax strategies, or investment basics. These events not only educate attendees but also position the advisor as a thought leader. Attendees often leave with a better understanding of their financial needs and a desire to seek personalized guidance.

In the digital realm, advisors may offer free tools and assessments on their websites. These include retirement readiness calculators, risk tolerance quizzes, and budgeting templates. Such tools engage users and provide personalized feedback, creating a natural segue into one-on-one consultations. Additionally, offering free newsletters or eBooks helps advisors stay top-of-mind while delivering ongoing value.

Some advisors go further by waiving fees for introductory services, such as account setup or the first few months of investment management. This lowers the barrier to entry and encourages hesitant clients to try the service. Once clients experience the benefits, they’re more likely to commit long-term.

Loss leaders are not limited to high-net-worth individuals. Advisors targeting younger or less affluent clients may offer free debt management plans or budgeting assistance. These services address immediate concerns and build loyalty among clients who may become more profitable as their financial situations improve.

Ultimately, loss leaders are about building relationships. By offering something of value without immediate compensation, financial advisors demonstrate their commitment to helping clients succeed. This fosters trust, encourages engagement, and often leads to lasting partnerships. In a field where reputation and reliability are paramount, loss leaders serve as powerful tools for growth and differentiation.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Diworsification is a term coined by Peter Lynch to describe when investors over‑diversify their portfolios, adding too many holdings and ultimately reducing returns instead of improving them.

Diversification has long been heralded as one of the cornerstones of sound investing. By spreading capital across different asset classes, industries, and geographies, investors can reduce risk and protect themselves against the volatility of individual securities. Yet, as with many strategies, there exists a point where the benefits diminish and the practice becomes counterproductive. This phenomenon, known as diworsification, was popularized by legendary investor Peter Lynch to describe the tendency of investors and corporations to dilute their strengths by expanding too broadly.

At its core, diworsification occurs when the pursuit of safety leads to excessive complexity. For individual investors, this often manifests in portfolios bloated with dozens or even hundreds of stocks, mutual funds, or exchange‑traded funds. While the intention is to minimize risk, the result is frequently a portfolio that mirrors the market index but with higher costs and less focus. Instead of achieving superior returns, the investor ends up with average performance weighed down by management fees, trading expenses, and the difficulty of monitoring so many positions. In essence, the investor has sacrificed the potential for meaningful gains in exchange for a false sense of security.

Corporations are not immune to this trap. In the corporate world, diworsification describes the tendency of firms to expand into unrelated businesses, diluting their competitive advantage. A company that excels in consumer electronics, for example, may attempt to branch into unrelated industries such as food services or real estate. Without the expertise, synergies, or strategic fit, these ventures often fail to deliver value, distracting management and eroding shareholder wealth. History is replete with examples of conglomerates that grew too large, too fast, only to later divest their non‑core businesses in recognition of the inefficiencies created.

The dangers of diworsification are not merely theoretical. They highlight the importance of discipline in both investing and corporate strategy. For investors, the lesson is clear: diversification should be purposeful, not indiscriminate. A well‑constructed portfolio might include a mix of equities, bonds, and alternative assets, but each holding should serve a specific role—whether it is growth, income, or risk mitigation. Beyond a certain point, adding more securities does not reduce risk meaningfully; instead, it complicates decision‑making and reduces the chance of outperforming the market.

Similarly, for corporations, strategic focus is paramount. Expansion should be guided by core competencies and long‑term vision rather than the allure of short‑term growth. Firms that resist the temptation to chase every opportunity are better positioned to strengthen their brand, innovate within their domain, and deliver sustainable value to shareholders.

In conclusion, diworsification serves as a cautionary tale against the excesses of diversification. While spreading risk is essential, overdoing it can undermine performance and clarity. Both investors and corporations must strike a balance between breadth and focus, ensuring that every addition to a portfolio or business strategy enhances rather than dilutes overall strength. In other words, “diversification means you will always have to say you’re sorry.”

True wisdom lies not in owning everything, but in owning the right things.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The NASDAQ, short for the National Association of Securities Dealers Automated Quotations, is one of the largest and most influential stock exchanges in the world. Founded in 1971, it was the first electronic stock market, revolutionizing how securities were traded by replacing traditional floor-based systems with computerized trading platforms. This innovation made transactions faster, more transparent, and accessible to a broader range of investors.

Unlike the New York Stock Exchange (NYSE), which historically operated through physical trading floors, the NASDAQ is entirely virtual. It connects buyers and sellers through a sophisticated network of computers, allowing for rapid execution of trades. This digital-first approach has made it particularly attractive to technology companies and growth-oriented firms, earning it a reputation as the go-to exchange for innovative and high-tech businesses.

Companies Listed on the NASDAQ The NASDAQ is home to some of the most prominent and influential companies in the world. Giants like Apple, Microsoft, Amazon, Google (Alphabet), Meta (formerly Facebook), and Tesla all trade on the NASDAQ. These companies are part of the NASDAQ-100, an index that tracks the performance of the 100 largest non-financial companies listed on the exchange. The NASDAQ Composite Index, which includes over 3,000 stocks, provides a broader snapshot of the market’s overall health and direction.

How It Works The NASDAQ operates as a dealer’s market, meaning transactions are facilitated by market makers—firms that stand ready to buy or sell securities at publicly quoted prices. These market makers help maintain liquidity and ensure that trades can be executed efficiently. Prices are determined by supply and demand, and the electronic nature of the exchange allows for real-time updates and high-speed trading.

Significance in the Global Economy The NASDAQ plays a vital role in the global financial system. It provides companies with access to capital by allowing them to issue shares to the public, and it offers investors a platform to buy and sell those shares. The performance of the NASDAQ is often seen as a barometer for the health of the technology sector and, more broadly, the innovation economy. When the NASDAQ rises, it typically signals investor confidence in growth and future earnings; when it falls, it may reflect concerns about economic stability or company performance.

Global Reach and Influence Though based in the United States, the NASDAQ’s influence extends worldwide. Many international companies choose to list on the NASDAQ to gain exposure to U.S. investors and benefit from the prestige associated with being part of a leading global exchange. Its technological infrastructure and regulatory standards make it a model for other exchanges around the world.

In summary, the NASDAQ is more than just a stock exchange—it’s a symbol of innovation, speed, and global connectivity. Its pioneering approach to electronic trading has reshaped the financial landscape, and its roster of companies continues to drive technological progress and economic growth across the globe.

The 3-5-7 Rule is a trading strategy that helps investors manage risk and maximize gains by setting clear limits on losses and targets for profits. It’s a simple yet powerful framework for disciplined decision-making.

In the volatile world of trading, success often hinges not just on identifying opportunities but on managing risk with precision. The 3-5-7 Rule is a widely respected risk management strategy designed to help traders protect their capital while pursuing consistent returns. This rule provides a structured approach to trading by setting specific thresholds for risk exposure and profit expectations.

At its core, the 3-5-7 Rule breaks down into three key components:

3% Risk Per Trade: Traders should never risk more than 3% of their total account value on a single trade. This limit ensures that even if a trade goes against them, the loss is manageable and doesn’t jeopardize their overall portfolio.

5% Total Exposure Across All Positions: The rule advises that total exposure across all open positions should not exceed 5% of the account value. This prevents over-leveraging and reduces the impact of correlated losses during market downturns.

7% Profit Target: For every trade, the goal is to achieve a profit that is at least 7% greater than the potential loss. This risk-to-reward ratio helps ensure that even with a lower win rate, traders can remain profitable over time.

The beauty of the 3-5-7 Rule lies in its simplicity and adaptability. It can be applied across various asset classes—stocks, forex, crypto—and suits both beginners and seasoned traders. By enforcing discipline, it helps traders avoid emotional decisions, such as chasing losses or holding onto losing positions too long. Moreover, this rule encourages thoughtful position sizing. Traders must calculate their entry and exit points carefully, factoring in stop-loss levels and account size. This analytical approach fosters better trade planning and reduces impulsive behavior.

Another advantage is its scalability. As a trader’s account grows, the percentages remain constant, but the dollar amounts adjust accordingly. This keeps the strategy relevant and effective regardless of portfolio size. In practice, the 3-5-7 Rule acts as a safety net. It doesn’t guarantee profits, but it significantly reduces the likelihood of catastrophic losses. It also promotes consistency, which is crucial for long-term success in trading.

In conclusion, the 3-5-7 Rule is more than just a guideline—it’s a mindset. It teaches traders to respect risk, plan strategically, and aim for favorable outcomes.

By adhering to this rule, traders can navigate the unpredictable markets with greater confidence and control.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Historian Cyril Parkinson’s wrote in his book Parkinson’s Law,

“The time spent on any item of the agenda will be in inverse proportion to the sum [of money] involved.”

EXAMPLE: Parkinson described a fictional finance committee with three tasks: approval of a $10 million nuclear reactor, $400 for an employee bike shed, and $20 for employee refreshments in the break room.

The committee approves the $10 million nuclear reactor immediately, because the number is too big to contextualize, alternatives are too daunting to consider, and no one on the committee is an expert in nuclear power.

Bike Shed Effect: The bike shed gets considerably more debate. Committee members argue whether a bike rack would suffice and whether a shed should be wood or aluminum, because they have some experience working with those materials at home.

Employee refreshments take up two-thirds of the debate, because everyone has a strong opinion on what’s the best coffee, the best cookies, the best chips, etc.

Absurd: The world is filled with these absurdities. In personal finance, Ramit Sethi recently said we should stop asking $3 questions (should I buy coffee?) and ask more $30,000 questions (should I buy a smaller home?). Most people don’t, because it’s hard and intimidating. In any given moment the easiest way to deal with a big problem is to ignore it and fill your time thinking about a smaller one.

***

***

Assessment: Your thoughts and comments related to the post Corona Virus Pandemic, meetings and time management and psychology are appreciated.

High-frequency trading (HFT) is a form of algorithmic trading that uses powerful computers and complex programs to execute thousands of trades in fractions of a second. It has transformed modern financial markets by increasing speed, liquidity, and efficiency—but also raised concerns about fairness and stability.

High-frequency trading emerged in the early 2000s as technological advances allowed financial firms to process market data and execute trades faster than ever before. HFT firms use sophisticated algorithms to analyze multiple markets and identify short-term opportunities. These trades are often held for mere seconds or milliseconds, and profits are made by exploiting tiny price discrepancies across assets or exchanges.

One of the defining features of HFT is its reliance on speed. Firms invest heavily in infrastructure—such as co-location services near exchange servers and fiber-optic cables—to gain microsecond advantages over competitors. This race for speed has led to a technological arms race, where milliseconds can mean millions in profit.

HFT contributes significantly to market liquidity, meaning it helps ensure that buyers and sellers can transact quickly at stable prices. By constantly placing and updating orders, HFT firms narrow bid-ask spreads and reduce transaction costs for other market participants. This has made markets more efficient and accessible, especially for retail investors.

However, HFT is not without controversy. Critics argue that it creates an uneven playing field, where firms with access to advanced technology and capital can dominate markets. Concerns about market manipulation—such as quote stuffing (flooding the market with orders to slow competitors) or spoofing (placing fake orders to move prices)—have led to increased regulatory scrutiny.

The 2010 Flash Crash is often cited as a cautionary example of HFT’s potential risks. During this event, the Dow Jones Industrial Average plunged nearly 1,000 points in minutes before rebounding. Investigations revealed that automated trading systems, including HFT algorithms, contributed to the sudden loss of liquidity and extreme volatility.

Regulators have responded by implementing safeguards such as circuit breakers, which pause trading during extreme price movements, and requiring firms to register and disclose their trading strategies. The Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) continue to monitor HFT’s impact on market integrity.

Despite its challenges, HFT remains a dominant force in global finance. It accounts for a significant portion of trading volume in equities, futures, and foreign exchange markets. Many institutional investors rely on HFT strategies to manage large portfolios and hedge risks.

In conclusion, high-frequency trading represents both the promise and peril of technological innovation in finance. While it enhances market efficiency and liquidity, it also introduces new risks and ethical dilemmas.

As markets evolve, balancing innovation with fairness and stability will be essential to ensuring that HFT serves the broader interests of investors and the economy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on November 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

The Sraffa–Hayek debate stands as a pivotal moment in the history of economic thought, highlighting deep philosophical and methodological differences between two influential schools: the Austrian School, represented by Friedrich Hayek, and the neo-Ricardian or Cambridge School, represented by Piero Sraffa. Taking place primarily in the 1930s, this intellectual exchange centered on the nature of capital, the role of equilibrium, and the validity of marginalist theory.

Friedrich Hayek, a staunch advocate of Austrian economics, had developed a theory of business cycles rooted in the mis allocation of capital due to artificially low interest rates. In his framework, interest rates serve as signals that coordinate inter temporal production decisions. When central banks distort these signals, they cause over investment in capital-intensive industries, leading to unsustainable booms followed by inevitable busts. Hayek’s theory was grounded in a time-structured view of capital, emphasizing the importance of temporal coordination in production.

Piero Sraffa, a Cambridge economist and close associate of John Maynard Keynes, challenged Hayek’s assumptions in a 1932 review of Hayek’s book Prices and Production. Sraffa’s critique was both technical and philosophical. He questioned the coherence of Hayek’s notion of a uniform natural rate of interest in a complex economy with heterogeneous capital goods. Sraffa argued that in such an economy, there could be multiple natural rates of interest, making it impossible to define a single rate that equilibrates savings and investment across all sectors.

Moreover, Sraffa criticized the Austrian reliance on equilibrium analysis in a world characterized by uncertainty and institutional complexity. He contended that Hayek’s model was overly abstract and detached from real-world dynamics. This critique foreshadowed Sraffa’s later work, Production of Commodities by Means of Commodities (1960), which laid the foundation for the neo-Ricardian critique of marginalist economics. In that work, Sraffa demonstrated that prices and distribution could be determined without recourse to subjective utility or marginal productivity, challenging the core of neoclassical theory.

The debate had far-reaching implications. For the Austrian School, it exposed vulnerabilities in their capital theory and prompted refinements in their approach to intertemporal coordination. For the broader economics profession, Sraffa’s critique contributed to a growing skepticism about the internal consistency of marginalist value theory, influencing the Cambridge capital controversies of the 1950s and 1960s.