BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on May 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

It’s the first anniversary of the Medicaid unwinding for many states, a process that kicked off when federal rules that had kept people on Medicaid and the Children’s Health Insurance Program (CHIP) through the pandemic expired. And while states could redetermine eligibility again, things have “unwound” more than some experts predicted. Children were kicked off the rolls at higher rates than adults, according to a new study the Urban Institute released May 2. Twelve states—Montana, Iowa, South Dakota, Alabama, Idaho, Georgia, Texas, Arkansas, Oklahoma, Florida, Mississippi, Colorado—exceeded 100% of their total projections for disenrolling children.

The S&P 500® index (SPX) was little changed at 5,187.67; the Dow Jones Industrial Average gained 172.13 points (0.4%) to 39,056.39; the NASDAQ Composite® ($COMP) declined 29.80 points (0.2%) to 16,302.76.

The 10-year Treasury note yield (TNX) rose more than 3 basis points to 4.496%.

The CBOE Volatility Index® (VIX) fell 0.23 to 13.00.

Retail and real estate shares were among the weakest areas Wednesday, while banks and utilities were firm. Utility shares extended a nearly month-long rally, which may in part reflect greater expectations for Fed rate cuts. Lower interest rates can make utility shares with high dividend yields relative to Treasuries more appealing. The Dow Jones Utility Average ($DJU) rose 0.5% to end at its highest level since late July and is up 12% from a mid-April low.

And, Shopify’s value plunged by nearly $20 billion after the online payments company released a gloomy forecast for this quarter. It’s the latest pandemic darling to stumble: According to the Financial Times, the firms that skyrocketed during lockdowns have lost a collective $1.5 trillion in value since the end of 2020.

Steward Health Care System, the largest U.S. physician-owned hospital operator, is expected to file for chapter 11 bankruptcy as soon as Sunday, according to a WSJ report, which cited people familiar with the matter. Steward Health Care is the largest tenant of Medical Properties Trust (NYSE: MPW). Steward Health Care hired restructuring advisers to improve its liquidity and restore its balance sheet in January 2024.

Posted on May 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500 index rose 6.96 points (0.1%) to 5,187.70; the Dow Jones Industrial Average gained 31.99 points (0.1%) to 38,884.26; the NASDAQ Composite® ($COMP) eased 16.70 points (0.1%) to 16,332.56.

The 10-year Treasury note yield dropped more than 3 basis points to 4.457%.

The CBOE Volatility Index® (VIX) fell 0.26 to 13.23.

Interest-rate-sensitive sectors, such as real estate and utilities, were among the market’s strongest performers Tuesday. The Philadelphia Utility Index (UTY) rose 1.3%, its fifth straight daily gain, and hit its highest level in almost a year. The recent strength may in part reflect heightened expectations for lower interest rates, which may make utility shares with relatively high dividend yields compared to Treasuries more appealing. The utilities sector is also coming off a strong April, during which it was the only S&P 500 sector with a positive return, with chart patterns suggesting a bullish long-term momentum shift.

The semiconductor sector was among the weakest sectors Tuesday, partly behind a 1.7% drop in Nvidia (NVDA). The shares fell after billionaire investor Stanley Druckenmiller told CNBC he reduced his stake in the chipmaker in late March, saying that artificial intelligence may be a “little overhyped” for the short term.

***

Peloton is reportedly being circled by private equity firms for a potential buyout of the enfeebled fitness company.

The SEC is preparing to sue over Robinhood’s crypto business. Robinhood just revealed that it’s been notified that the SEC plans to bring an enforcement action against its crypto unit for alleged securities violations. But the online brokerage said it’s not sweating: “We firmly believe that the assets listed on our platform are not securities and we look forward to engaging with the SEC to make clear just how weak any case against Robinhood Crypto would be on both the facts and the law,” Dan Gallagher, Robinhood’s chief legal, compliance, and corporate affairs officer, wrote in a blog post. Such a notice doesn’t always mean a suit will follow, but crypto companies and the agency have been sparring for years over whether crypto tokens count as securities.

The Biden administration were quick to praise a new report that extends the lifespan of the Hospital Insurance Trust Fund, but the report renewed calls for increasing physician payments.

Amwell, a telehealth company, continues to struggle in the stock market, and both its bottom- and top-line results in the first quarter missed Street analysts’ estimates.

And … between the Change Healthcare cyberattack and Medicare Advantage headwinds, major insurers faced unique challenges in the first quarter.

Stat: 8.7%. That’s the level to which US consumers can expect the 30-year mortgage rate to rise over the next year, which marks a series high, according to a New York Federal Reserve survey (MarketWatch)

Posted on May 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Low-income communities often struggle to access healthcare services, but a new analysis of federally qualified health centers (FQHCs)—which provide quality care to patients regardless of ability to pay—has helped nail down one reason. When it comes to screening for certain cancers, these nonprofit community health centers have fallen far behind the national average, according to a study led by cancer center researchers at the University of Texas MD Anderson and the University of New Mexico.

Healthcare bankruptciessurged in 2023, and it turns out many of the companies that went under had one thing in common: private equity (PE) ownership. At least 21% of the 80 healthcare companies that filed for bankruptcy last year were PE-owned, according to a report from the nonprofit Private Equity Stakeholder Project (PESP).

Warren Buffett oncontemplated his own mortality at Berkshire’s meeting.Succession was the topic du jour at the Berkshire Hathaway shareholder meeting in Omaha last week. After his longtime business partner Charlie Munger died last year at 99, CEO Warren Buffett—who turns 94 in August—revealed his heir apparent, Greg Abel, will have the final say on investment decisions in his absence. Buffett ended his Q&A portion with the quip, “I not only hope you come next year. I hope I come next year.” Adding to the ominous vibes, Buffett said AI is a genie that “scares the hell out of me.”

The S&P 500 index climbed 52.95 points (1.0%) to 5,180.74; the Dow Jones Industrial Average gained 176.59 points (0.5%) to 38,852.27; the NASDAQ Composite advanced 192.92 points (1.2%) to 16,349.25.

The 10-year Treasury note yield (TNX) fell about 1 basis point to 4.491%.

The CBOE Volatility Index® (VIX) was little changed at 13.48.

Semiconductors were among the strongest performers Monday behind Micron Technology (MU), whose shares rallied 4.7% after Robert W. Baird upgraded the chipmaker to “outperform” from “neutral.” Micron Technology was the top gainer in the Philadelphia Semiconductor Index (SOX), which advanced 2.2% to near a four-week high.

Small-cap stocks also got out of the gate strong this week. The Russell 2000® Index (RUT) gained 1.2% to end at a four-week high but is still up just 1.7% for the year, while the S&P 500 has gained 8.6%.

Posted on May 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A cooling labor market raises hopes for a rate cut in the summer. The latest Labor Department data shows the US added 175,000 jobs in April, but much less than the 300,000 added in March and also less than economists expected. Meanwhile, the unemployment rate ticked up to 3.9% from 3.8% in March, and wages rose less than anticipated. All that bad news for us was music to the ears of investors who are holding out hope that the Federal Reserve might still cut interest rates this summer despite most recent economic data showing that inflation is sticking around.

Rate cuts appear to be back on the 2024 menu following Friday’s softer-than-expected jobs report, fueling gains for all three major stock indexes last week. With the report calming worries that inflation is ticking back up, investors now project a 50% likelihood that the Federal Reserve will reduce rates in September.

Coinbase is benefiting from the hype around new bitcoin ETFs. The crypto exchange reported a $1.2 billion quarterly profit last week, and net revenue rose by 115%.

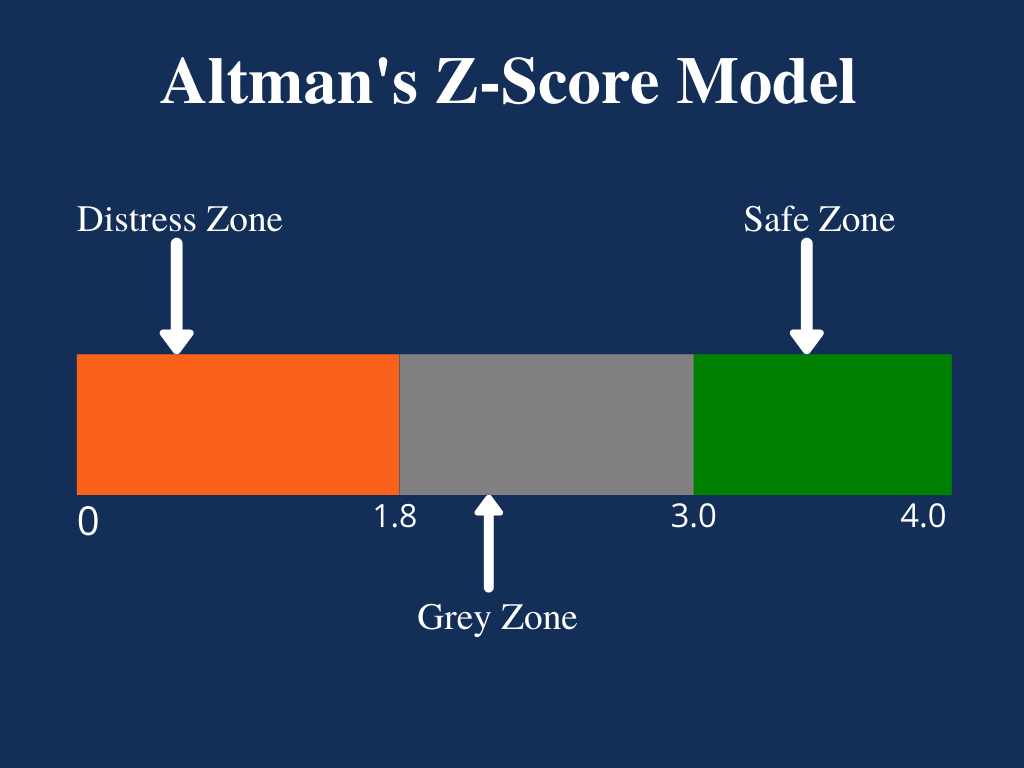

The Zeta Model is a mathematical model that estimates the chances of a public company going bankrupt within a two-year time period. The number produced by the model is referred to as the company’s Z-score (or zeta score) and is considered to be a reasonably accurate predictor of future bankruptcy.

The model was published in 1968 by New York University professor of finance Edward I. Altman. The resulting Z-score uses multiple corporate income and balance sheet values to measure the financial health of a company.

Posted on May 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Starbucks – The coffee company known for consistently outperforming itself reported less-than-spectacular earnings this week, sending its stock plunging 12% on Tuesday evening last week on the news—nearly as much as when the company shut all its doors during Covid 19. For the first time since 2020, US same-store sales declined, falling 3% alongside a 7% decrease in foot traffic. Meanwhile, revenue fell 1.8% to $8.56 billion as sales in China—the chain’s second-biggest market—declined 11%, and Starbucks lowered its sales outlook for the year.

Educators have long pushed back against distraction machines (aka phones), with 77% of schools banning them in the classroom as of 2020, according to a National Center for Education Statistics survey. School time still overlaps with screen time: 97% of students are on their phones during school hours, according to a study by Common Sense Media, a nonprofit that informs parents about technology. While much of students’ phone use might be at lunch or recess, teachers complain that kids aren’t waiting for the bell to take a discreet peek at their screens.

Creatine may counteract sleep deprivation. The dietary supplement all over your Instagram feed might one day help workers who have to do a lot on small amounts of sleep, like ER staff, first responders, and anyone sharing a house with a baby.

Posted on May 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500 index rose 63.59 points (1.3%) to 5,127.79, up 0.6% for the week; the Dow Jones Industrial Average® ($DJI) gained 450.02 points (1.2%) to 38,675.68, up 1.1% for the week; the NASDAQ Composite surged 315.37 points (2.0%) to 16,156.33, up 1.4% for the week.

The 10-year Treasury note yield (TNX) fell about 7 basis points to 4.50%, down about 16 basis points for the week.

The CBOE Volatility Index® (VIX) fell 1.19 to 13.49.

Technology shares were among the strongest performers Friday behind a 6% rally in shares of Apple (AAPL), which late Thursday reported stronger-than-expected quarterly results and said it will repurchase $110 billion in shares. Amgen (AMGN) soared nearly 12%, leading Dow gainers after the biotechnology company beat earnings expectations.

In other markets, WTI Crude Oil futures (/CL) extended a week-long slump to end just above $78 per barrel, the lowest since mid-March. Crude futures dropped almost 7% this week, partly reflecting rising U.S. supplies and signs of slower fuel demand.

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Job growth slowed and unemployment ticked higher last month, marking a break from a string of data showing surprising strength in the labor market.

U.S. employers added a seasonally adjusted 175,00 jobs in April, the Labor Department reported on Friday. That was far less than in March, when gains exceeded 300,000, and also below what economists had expected. The unemployment rate ticked up to 3.9% from March’s 3.8%.

According to the WSJ, wages also rose less than anticipated, increasing 3.9% from a year earlier after rising 4.1% in March.

Friday’s report today is sure to stir immediate debate among economists and investors about whether the labor market is merely cooling in a welcome fashion or starting to show more serious strains under the pressure of higher interest rates.

Treasury yields, which largely reflect investors’ expectations for short-term rates set by the Federal Reserve, fell after the report. The yield on the benchmark 10-year U.S. Treasury note was 4.471% in recent trading, according to Tradeweb, down from 4.569% Thursday.

Stock futures climbed, suggesting investors were pleased with the data, which could increase optimism about the outlook for inflation.

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Yesterday, sales of Wegovy more than doubled last quarter, and at least 25,000 people are starting to take it in the US per week. It also posted a $3.65 billion net profit and increased its sales outlook for 2024. But its stock Novo Nordisk still dropped yesterday.

***

iPhone sales are down but Apple share buybacks are up. Apple managed to keep investors happy, sending its stock shooting up after-hours yesterday, despite selling fewer iPhones last quarter. Sales of the signature phone dipped 10% year over year, and revenue fell 4.3% to $90.8 billion. But Apple also announced $110 billion in share buybacks, the largest in the company’s history, per CNBC. And sales in China, which has been a sore spot, came in at $16.4 billion, less than a year earlier but more than analysts had predicted.

***

Stocks rose yesterday as investors digested Jerome Powell’s recent comments and decided they only had to fear fear itself—and not interest rate hikes. Investors changed into the fast lane to buy Carvana after the used car sales site reported its best earnings ever Wednesday evening.

***

Stat: 16%. That’s the percentage by which CVS stocks plummeted Wednesday after the company reported earnings below expectations and cut its annual outlook, according to (CNBC).

But – Here’s where the major stock market benchmarks ended Thursday:

The S&P 500® index (SPX) rose 45.81 points (0.9%) to 5,064.20; the Dow Jones Industrial Average® ($DJI) added 322.37 points (0.9%) to 38,225.66; the NASDAQ Composite® ($COMP) surged 235.48 points (1.5%) to 15,840.96.

The 10-year Treasury note yield (TNX) dropped about 1 basis point to 4.583%.

The CBOE Volatility Index® (VIX) fell 0.71 to 14.68.

Transportation shares helped lead the market higher after C.H. Robinson (CHRW) reported stronger-than-expected quarterly results, sending the freight logistics and trucking company’s stock up 12%. The Dow Jones Transportation Average ($DJT) jumped 2.5%. Semiconductors were also strong after Qualcomm (QCOM) advanced 9.7% in the wake of the chip maker’s better-than-expected earnings.

Apple (AAPL) shares advanced 2.2% ahead of the company’s quarterly earnings report scheduled after Thursday’s close.

In other markets, WTI Crude Oil (/CL) futures bounced back to end with a slight gain after earlier dropping to a seven-week low under $78.50 per barrel.

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd CMP

***

***

Medicare [Dis] Advantage Plans [Medicare Part C] commenced in 2003 or so and I have railed against them since then. First, for their low physician payments. And then as a patient advocate for the last decade. And, today, for both reasons. As a doctor and independent health insurance agent myself, believe me when I speak thusly.

Now, while Medicare Advantage plans are undoubtedly not the right choice for everyone, insurance companies still say there are some folks who will get exactly what they need from the plans and at a moderate price.

Nevertheless, Ernesto Jaboneta, the IT Director of California-based Medicare insurance agency Agent Pitstop, acknowledged there are many predatory salespeople who will jump to have you join a plan that doesn’t end up helping you in the long run. Still, there are precautions you can take to make falling into this trap less likely.

“The first thing anyone can do is invite along a family member or trusted friend to any appointments with an insurance agent,” Jaboneta told Newsweek. “Don’t feel pressured to decide right away.”

Before you commit to anything, you should compare plans and find out if your doctors will remain in your network. And if you’re unsure about some of the information you received from an insurance agent, you can also call 1-800-MEDICARE for more assistance.

Jaboneta also said there’s a big difference between captive insurance agents and independent agents, as well, and seniors should take note of this.

“A captive agent is an insurance agent who works directly for an insurance carrier,” Jaboneta said. “They have no incentive to compare options outside their own company, which is different than an independent agent who can compare all the options available. In many cases, when a beneficiary calls into an insurance company to find information, they will be talked into enrolling.”

The open enrollment period lasts from October 15th to December 8th, but there’s another enrollment period from January 1st to March 31st for anyone unhappy with their Medicare Advantage plan who wants to switch or revert to Medicare.

INVESTING UPDATE: Managed-care companies are reporting that seniors on Medicare Advantage Part C plans used far more medical services than expected in the final months of 2023. The announcements have sparked two separate selloffs over the past week: The first came January 12th, when UnitedHealth Group announced its fourth-quarter earnings. The second came after Humana just laid out preliminary fourth-quarter results, and said the high utilization trends would have a material impact on its 2024 performance “if current trends continue.”

Humana said it would be ending some plans and cutting benefits for patients in 2025 as it hopes to boost its financial performance. Altogether, 6 million Americans are insured through Humana’s Medicare Advantage.

Posted on May 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX) fell 17.30 points (0.3%) to 5,018.39; the Dow Jones Industrial Average® ($DJI) gained 87.37 points (0.2%) to 37,903.29; the NASDAQ Composite® ($COMP) lost 52.34 points (0.3%) to 15,605.48.

The 10-year Treasury note yield (TNX) dropped more than 5 basis points to 4.63%.

The CBOE Volatility Index® (VIX) decreased 0.28 to 15.37.

Banks and other financial shares led the market’s afternoon upswing, reflecting renewed optimism over the outlook for interest rates. The KBW Regional Bank Index (KRX) jumped 2.4% and posted its first gain in five days. Biotechnology and communication services were also strong.

Energy shares were among the weakest performers as WTI Crude Oil (/CL) futures extended a week-long nosedive and dropped under $80 per barrel for the first time since mid-March. Crude futures sank over 3% after the Energy Information Administration reported U.S. oil inventories surged 1.6% last week.

Among top companies, Amazon (AMZN) gained 2.2% after reporting stronger-than-expected earnings and revenue late Tuesday. Starbucks (SBUX) tumbled 16% following unexpectedly soft quarterly results. Apple (AAPL) eased 0.6% ahead of its quarterly results, expected after Thursday’s close.

Speaking of stock companies, however big you think UnitedHealth is, it’s bigger than that. For example:

With a market cap of nearly $450 billion, it’s the fourth-largest company in the US by revenue this year, beating out Alphabet and Microsoft.

The company is eyeing a $24.7 billion profit in 2024.

One analyst estimated that more than 5% of US GDP flows through UnitedHealth’s systems daily.

And so, lawmakers in Washington are prepared to grill UnitedHealth CEO Andrew Witty in two congressional hearings today, months after a cyberattack on a subsidiary of the healthcare giant, Change Healthcare, rattled the industry and left pharmacies, doctors, and hospitals in the dark. Change processes roughly half of all Americans’ medical claims. Congress wants Witty to clarify how UnitedHealth handled the breach of patient data. But beyond that, it wants to investigate whether the company—the nation’s largest private health insurer—has grown too big and taken on too much risk.

Retailer Walmart announced plans Tuesday to shutter its network of 51 health clinics in five states, along with its telehealth business. The impending closures signify that Walmart is scuttling its initial plans to expand the services, citing escalating operation costs and “challenging reimbursement environment,” the company said in a news release.

Finally – Happy Women’s Health Month! Women and people assigned female at birth are disproportionately affected by a range of health conditions, including autoimmune diseases, chronic pain, and dementia. The month of May is intended to raise awareness of these disparities and educate women on steps they can take to improve their health, such as getting annual breast exams. For all our woman-identifying readers, take some time to prioritize your health this month!

Posted on May 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

May Day is a European festival of ancient origins marking the beginning of summer, usually celebrated on 1 May, around halfway between the Northern Hemisphere’s Spring equinox and June solstice. Festivities may also be held the night before, known as May Eve. Traditions often include gathering wildflowers and green branches, weaving floral garlands, crowning a May Queen and setting up a Maypole, May Tree or May Bush, around which people dance. Bonfires are also part of the festival in some regions.

***

Here’s where the major benchmarks ended:

The S&P 500 index fell 80.48 points (1.6%) to 5,035.69; the Dow Jones Industrial Average® ($DJI) lost 570.17 points (1.5%) to 37,815.92, down 5% for the month; the NASDAQ Composite declined 325.26 points (2.0%) to 15,657.82.

The 10-year Treasury note yield jumped more than 7 basis points to 4.682%.

The CBOE Volatility Index® (VIX) rose 0.98 to 15.65.

Energy shares were among the weakest performers Tuesday, behind a drop in WTI Crude Oil (/CL) futures, which fell a third consecutive session and briefly dropped under $81 per barrel. The Philadelphia Oil Service Index (OSX) tumbled 4.5% to a seven-week low. The small-cap Russell 2000® Index (RUT) shed 2.1% and ended with a loss of 7.1% for the month.

But, it was a better day for Mounjaro maker Eli Lilly, which climbed nearly 6% after its popular weight loss drugs pushed it to raise its 2024 forecast.

A class-action complaint was filed against MultiPlan and major payers like UnitedHealth Group and CVS Health’s Aetna, arguing payers’ claims data was being used to generate low reimbursement rates.

Posted on April 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

It’ll be a big week for hot takes on the US economy, after the Federal Reserve meeting Tuesday and Wednesday and the April jobs report dropping Friday. Because inflation has been sticking around, the FOMC is expected to hold interest rates steady at this meeting and for the foreseeable future. On the jobs front, economists are projecting another strong month for employment growth.

In 2022, with bipartisan support, Congress passed the CHIPS and Science Act, an ambitious plan to juice domestic manufacturing of a product vital to national security: semiconductors. Two years later, the government has doled out more than half of the CHIPS Act’s $39 billion in incentives. According to the Financial Times …

Chip companies and their suppliers have announced US investments of $327 billion over the next 10 years, per the Semiconductor Industry Association.

Construction of manufacturing facilities for computing and electronics devices has jumped 15x, government data shows.

By 2030, the US will likely produce around 20% of the world’s most advanced chips, according to USCommerce Secretary Gina Raimondo. Right now, it’s making 0%.

The proposed factories are massive and could transform regional economies. Micron, which received $6.1 billion in federal grants last week, plans to invest $100 billion in a manufacturing campus near Syracuse.

The S&P 500® index (SPX) rose 16.21 points (0.3%) to 5,116.17, its highest close in over two weeks; the Dow Jones Industrial Average® ($DJI) gained 146.43 points (0.4%) to 38,386.09, the NASDAQ Composite® ($COMP) advanced 55.18 points (0.4%) to 15,983.08.

The 10-year Treasury note yield (TNX) fell more than 5 basis points to 4.616%.

The CBOE Volatility Index® (VIX) declined 0.36 to 14.67.

Communication services shares were among the market’s weakest performers Monday, reversing last Friday’s upswing as Alphabet (GOOGL) dropped more than 3% and Meta Platforms (META) lost 2.4%. Banks and retailers were also soft. The Philadelphia Semiconductor Index (SOX) climbed for the sixth-straight day and ended near a three-week high even though its biggest member, Nvidia (NVDA), ended little changed.

In other markets, the U.S. Dollar Index ($DXY) faded from early gains but is still up about 1% in April, driven by expectations domestic rates will remain high. “The U.S. dollar’s strength continues to reflect the relative strength of the economy and the wide interest rate differentials between the United States and other major developed markets,” Schwab Center for Financial Research analysts said in a report.

Despite last week’s strength, the S&P 500 index and the NASAQ Composite are still down 2.6% and 2.4%, respectively, for April and on track to break five-month winning streaks.

Humana expects to exit Medicare Advantage (MA) markets in 2025, company executives told investors. The company reported its first quarter earnings April 24th. Humana posted $741 million in net income in the first quarter of 2024, beating investor expectations, but pulled its 2025 earnings guidance.

Posted on April 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A SPECIAL REPORT

By Vitaliy N. Katsenelson CFA

***

Uber’s business is doing extremely well. It has reached escape velocity – the company’s expenses have grown at a slow rate while its revenues are growing at 22% a year. This caused profit margins to expand and earnings and free cash flows to skyrocket. Our investment in Uber was based on the assumption that its services would become a utility – just like water and electricity. The company’s name is synonymous with ride sharing.

I must confess that the biggest risk to our investment in Uber is me. Yes, you read that right. Uber has an incredible growth runway. It is not just going after ride sharing and food delivery, where it still has plenty of room to grow, it is also making serious inroads into the grocery market. It has terrific management that is putting a lot of daylight between Uber and its competitors.

Posted on April 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Republic First Bank. The FDIC said regulators seized the troubled Philadelphia-based bank and agreed to sell it to Fulton Bank. While news of a regional bank failure might take you back to March 2023 when Silicon Valley Bank bit the dust, Republic First was much smaller than SVB (and much smaller than the similarly named First Republic, which ultimately got absorbed by JPMorgan Chase as regional banks struggled). And, because there’s already a buyer, there are no lingering questions about the safety of deposits.

So, while the first bank failure of the year is a sign that regional banks are still in a bad way, it’s unlikely to spur a larger crisis.

It is critical for physician executives to understand and to measure the total cost of hospital capital. Lack of understanding and appreciation of the total cost of capital is widespread, particularly among not-for-profit hospital and physician executives. The capital structure includes long-term debt and equity; total capital is the sum of these two, and, each of these components has cost associated with it.

For the long-term debt portion, this cost is explicit—it is the interest rate plus associated costs of placement and servicing. For the equity portion, the cost is not explicit and is widely misunderstood. In many cases, hospital capital structures include significant amounts of equity that has accumulated over many years of favorable operations.

Far too many executives wrongly attribute zero cost to the equity portion of their capital structure. Although it is correct that generally accepted accounting principles continue to assign a zero cost to equity, there is opportunity cost associated with equity that needs to be considered. This cost is the opportunity available to utilize that capital in alternative ways.

***

***

In general, the cost attributed to equity is the return expected by the equity markets on hospital equity. This can be observed by evaluating the equity prices of hospital companies whose equity is traded on public stock exchanges. Usually, the equity prices will imply cost of equity in the range of 10%–14%. Almost always, the cost of equity implied by hospital equity prices traded on public stock exchanges will substantially exceed the cost of long-term debt. Thus, while many hospital executives will view the cost of equity to be substantially less than the cost of debt (i.e., to be zero) in nearly all cases, the appropriate cost of equity will be substantially greater than the cost of debt.

Hospitals need to measure their weighted average cost of capital (WACC). WACC is the cost of long-term debt multiplied by the ratio of long-term debt to total capital plus the cost of equity multiplied by the ratio of equity to total capital (where total capital is the sum of long-term debt and equity).

WACC is then used as the basis for capital charges associated with all capital investments. Capital investments should be expected to generate positive returns after applying this capital charge based on the WACC. Capital investments that do not generate returns exceeding the WACC consume enterprise value; those that generate returns exceeding WACC increase enterprise value. Therefore, physician and hospital executives need to be rewarded for increasing enterprise value.

Some of the pioneers of behavioral finance are Drs. Kahneman, Twersky and Thaler. This short introduction to the subject is based on John Nofsinger’s little book entitled “Psychology of Investing” an excellent quick read for all medical professionals or anyone who is interested in learning more about behavioral finance.

Rational Decisions?

Much of modern finance is built on the assumption that investors “make rational decisions” and “are unbiased in their predictions about the future”, however this is not always the case.

Cognitive errors come from (1) prospect theory (people feel good/bad about gain/loss of $500, but not twice as good/bad about a gain/loss of $1,000; they feel worse about a $500 loss than feel good about a $500 gain); (2) mental accounting (meaning that people tend to create separate buckets which they examine individually), (3) Self-deception (e.g. overconfidence), (4) heuristic simplification (shortcuts) and (4) mood can affect ability to reach a logical conclusion.

John Nofsinger’s Book

The following are some of the major chapter headings in Nofsinger’s book, and represent some of the key behavioral finance concepts.

Overconfidence leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

Pride and Regret leads to: (1) disposition effect (not only selling winners and holding on to the losers, but selling winners too soon- confirming how smart I was, and losers to late- not admitting a bad call, even though selling losers increases one’s wealth due to the tax benefits), (2) reference points (the point from where one measures gains or losses is not necessarily the purchase price, but may perhaps be the most recent 52 week high and it is most likely changing continuously- clearly such a reference point will affect investor’s judgment by perhaps holding on to “loser” too long when in fact it was a winner.)

Considering the Past in decisions about the future, when future outcomes are independent of the past lead to a whole slew of more bad decisions, such as: (1) house money effect (willing to increase the level of risk taken after recent winnings- i.e. playing with house’s money), (2) risk aversion or snake-bite effect (becoming more risk averse after losing money), (3) trying to break-even (at times people will increase their willing to take higher risk to try to recover their losses- e.g. double or nothing), (4) endowment or status quo effect (often people are only prepared to sell something they own for more than they would be willing to buy it- i.e. for investments people tend to do nothing, just hold on to investments they already have) (5) memory and decision making ( decisions are affected by how long ago did the pain/pleasure occur or what was the sequence of pain and pleasure), (6) cognitive dissonance (people avoid important decisions or ignore negative information because of pain associated with circumstances).

Mental Accounting is the act of bucketizing investments and then reviewing the performance of the individual buckets separately (e.g. investing at low savings rate while paying high credit card interest rates).

Examples of mental accounting are: (1) matching costs to benefits (wanting to pay for vacation before taking it and getting paid for work after it was done, even though from perspective of time value of money the opposite should be preferred0, (2) aversion to debt (don’t like long-term debt for short-term benefit), (3) sunk-cost effect (illogically considering non-recoverable costs when making forward-going decisions). In investing, treating buckets separately and ignoring interaction (correlations) induces people not to sell losers (even though they get tax benefits), prevent them from investing in the stock market because it is too risky in isolation (however much less so when looked at as part of the complete portfolio including other asset classes and labor income and occupied real estate), thus they “do not maximize the return for a given level of risk taken).

In building portfolios, assets included should not be chosen on basis of risk and return only, but also correlation; even otherwise well educated individuals make the mistake of assuming that adding a risky asset to a portfolio will increase the overall risk, when in fact the opposite will occur depending on the correlation of the asset to be added with the portfolio (i.e. people misjudge or disregard interactions between buckets, which are key determinants of risk).

This can lead to: (1) building behavioral portfolios (i.e. safety, income, get rich, etc type sub-portfolios, resulting in goal diversification rather than asset diversification), (2) naïve diversification (when aiming for 50:50 stock:bond allocation implementing this as 50:50 in both tax-deferred (401(k)/RRSP) accounts and taxable accounts, rather than placing the bonds in the tax-deferred and stocks in taxable accounts respectively for tax advantages), (3) naïve diversification in retirement accounts (if five investment options are offered then investing 1/5th in each, thus getting an inappropriate level of diversification or no diversification depending on the available choices; or being too heavily invested in one’s employer’s stock).

Representativenes may lead investors to confusing a good company with a good investment (good company may already be overpriced in the market; extrapolating past returns or momentum investing), and familiarity to over-investment in one’s own employer (perhaps inappropriate as when stock tanks one’s job may also be at risk) or industry or country thus not having a properly diversified portfolio.

Emotions can affect investment decisions: mood/feelings/optimism will affect decision to buy or sell risky or conservative assets, even though the mood resulted from matters unrelated to investment. Social interactions such as friends/coworkers/clubs and the media (e.g. CNBC) can lead to herding effects like over (under) valuation.

Financial Strategies

Nofsinger finishes with a final chapter which includes strategies for:

(i) beating the biases: (1) Understand the biases, (2) define your investment objectives, (3) have quantitative investment criteria, i.e. understand why you are buying a specific investor (or even better invest in a passive fashion), (4) diversify among asset classes and within asset classes (and don’t over invest in your employer’s stock), and (5) control your investment environment (check on stock monthly, trade only monthly and review progress toward goals annually).

(ii) using biases for the good: (1) set new employee defaults for retirement plans to being enrolled, (2) get employees to commit some percent of future raises to automatically go toward retirement (save-more-tomorrow).

Assessment

Buy the book (you can get used copies through Amazon). As indicated it is a quick read and occasionally you may even want to re-read it to insure you avoid the biases or use them for the good. Also, the book has long list of references for those inclined to delve into the subject more deeply.

You might even ask “How does all this Behavioral Finance coexist with Efficient Market theory?” and that’s a great question that I’ll leave for another time.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500 index gained 51.54 points (1.0%) to 5,099.96, up 2.7% for the week; the Dow Jones Industrial Average® ($DJI) increased 153.86 points (0.4%) to 38,239.66, up 0.7% for the week; the NASDAQ Composite jumped 316.14 points (2.0%) to 15,927.90, up 4.2% for the week.

The 10-year Treasury note yield (TNX) lost about 4 basis points to 4.665%.

The CBOE Volatility Index® (VIX) fell 0.34 to 15.03.

Alphabet’s rally helped communication services reverse Thursday’s downturn, which was driven by disappointing quarterly results from Meta Platforms (META). The S&P 500 Communication Services index ($SP500#50) surged 4.7% Friday and ended the week with a 2.7% gain. Semiconductor shares were also strong, led by a 6% gain in Nvidia (NVDA). The Russell 2000® Index (RUT) added 1.1% Friday and posted a 2.8% advance for the week.

In other markets, WTI Crude Oil (/CL) futures rose slightly Friday, ending around $83.65 per barrel and shutting down a three-week losing streak.

Midi Health, a health clinic geared toward women in midlife, raised $60 million in Series B funding to expand its network to 150 clinicians by the end of the year, among other efforts. (MobiHealthNews)

“We’re fooling ourselves if we think that’s cheap or can be done less expensively.”—Carmela Coyle, president and CEO of the California Hospital Association, on hospital finances and cutting costs (AP)

The federal government implemented new staffing rules to improve patient care, but most nursing homes won’t be able to meet that demand. (KFF Health News/NPR)

The Biden administration is considering a change that would downgrade cannabis from a Schedule I drug to a Schedule III drug this year. The reclassification would have major effects on the business of cannabis, but for that to happen, the Drug Enforcement Agency needs proof of medical effectiveness.

Posted on April 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

New GDP numbers out yesterday show a worrying combo of stubborn inflation + waning growth that dampens hopes for a potential interest rate cut. Per the latest data from the Bureau of Economic Analysis, the first quarter of 2024 was a confounding one:

GDP increased at a 1.6% annualized rate, far below projections of 2.4% and notably down from 3.4% at the end of 2023.

While slow growth would typically signal that the Fed could cut rates, another metric complicates matters: Consumer prices (excluding volatile categories), a solid indicator of inflation, shot up to a much higher than anticipated 3.7%.

***

Meta reported record Q1 revenue yesterday, but it was overshadowed by the billions of dollars the company is spending in its efforts to win the Artificial Intelligence race and make the Metaverse happen. Investors were unhappy with the company’s forecast that its spending will rise by $10 billion dollars to support Artificial Intelligence development, sending Meta’s stock price down 15% after hours.

Here’s where the major benchmarks ended:

The S&P 500 index fell 23.21 points (0.5%) to 5,048.42; the Dow Jones Industrial Average lost 375.12 points (1.0%) to 38,085.80; the NASDAQ Composite® ($COMP) shed 100.99 points (0.6%) to 15,611.76.

The 10-year Treasury note yield (TNX) rose about 5 basis points to 4.704%.

The CBOE Volatility Index® (VIX) fell 0.64 to 15.33.

Communication services shares were the weakest S&P 500 sector Thursday behind the plunge in Meta Platforms. Late Wednesday, the Facebook parent provided lighter-than-expected second-quarter revenue guidance, while CEO Mark Zuckerberg discussed spending in currently unprofitable pursuits such as artificial intelligence (AI) and mixed reality. Meta’s first-quarter earnings and revenue both came above analysts ‘ estimates, however.

Meta’s slump helped send the S&P 500 Communication Services index ($SP500#50) down 4%. Banks were also particularly soft amid concern that persistently high interest rates may compress lender margins. Semiconductor and transportation shares were among the few pockets of strength.

But, Alphabet, Microsoft, and Snap reported Q1 earnings yesterday, and were generally good. Alphabet issued its first-ever dividend and authorized $70 billion in stock buybacks, after it beat Wall Street’s revenue expectations. Microsoft also beat revenue forecasts on the strength of its cloud services. And Snap shares soared after it topped estimates and impressed investors with its 422 million global daily active users. It was a much-needed boost for the sector after Meta spooked the market with how much it’s spending on AI.

Posted on April 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Microsoft is looking at a broader AI future than just OpenAI

Microsoft has been at the forefront of the AI revolution through its $13 billion stake in the ChatGPT-maker, but recently it showed it’s also making other Artificial Intelligence bets, announcing it will pursue several partnerships and is investing $2.1 billion in French startup Mistral AI. Mistral’s tech will be available to Microsoft Azure users.

And then Microsoft President Brad Smithtold Axios that OpenAI CEO Sam Altman is “brilliant”, but …… Read Axios Story.

Perhaps even to counter Mark Zuckerbergs META Platform.

Posted on April 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Big Artificial Intelligence Spending Boosts Meta’s Cost Structure!

Meta [Facebook, FB] reported record Q1 revenue yesterday, but it was overshadowed by the billions the company is spending in its efforts to win the AI race and to try to make the metaverse happen. Investors were displeased with the company’s forecast that its spending will rise by $10 billion to support AI development, sending Meta’s stock price down 15% after hours.

Now, the metaverse is a vision of a virtual reality where people can socialize, work, play, and explore in immersive digital spaces.

But CEO Mark Zuckerberg urged them to keep the faith, saying, “We’ve historically seen a lot of volatility in our stock during this phase of our product playbook.”

Posted on April 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

An uptick in corporate dealmaking fueled investment banking growth at the four largest US banks—JPMorgan Chase, Bank of America, Wells Fargo, and Citibank—as well as at Goldman Sachs and Morgan Stanley. The result was “one of [investment banking’s] best quarters” since the Fed began hiking rates in 2022, the Wall Street Journal reported. Their earnings releases over the last week either matched or beat the consensus forecasts for revenue and earnings per share, according to the WSJ.

“It’s clear that we’re in the early stages of a reopening of the capital markets,” Goldman Sachs CEO David Solomon said in an earnings call last Monday. Goldman reported that growth in its investment banking and trading pushed its net income up 28% year over year, beating analyst expectations. Solomon said he expects more M&A activity will keep boosting the demand for debt underwriting at Goldman, which saw a 32% Year over Year jump in internet-banking revenue.

Solomon’s sunny outlook was beclouded the next day by Fed Chair Jerome Powell. The Fed had hoped inflation reports would show it could cut rates soon without overheating the economy, but instead inflation has continued to tick up.

As a young adult, what could you spend money on that would be a wise investment in your financial future? A home? Medical school education? A money management class?

Well, all of these may be good ideas, but there’s something else you can buy that could make an even greater difference in your long-term financial health: counseling.

Behavioral Finance

What does psychological counseling have to do with money? Sometimes; a lot!

For example, I was recently interviewed by a reporter for an article about money disorders. The conversation reminded me just how many problems can result from dysfunctional money beliefs and behaviors. Money disorders can impair people’s functioning and disrupt their lives just as significantly as disorders like alcoholism or other addictions.

Some common money disorders include the following:

Compulsive Spending is a consuming focus on spending. It can include buying things you can’t afford as well as shopping where no money is actually spent

Financial Enabling is a codependent attempt to help others that actually does more harm than good. A pattern of bailing kids out financially is a good example.

Hoarding is compulsively buying and storing things that you don’t need or will never use.

Financial Infidelity is keeping money secrets (such as spending, saving, or investment mistakes) from your partner because you would be ashamed to have them find out.

Financial Incest is inappropriate sharing of worries or financial details in ways that violate the boundaries between children and adults.

Workaholism, especially medical professionals, is a consuming focus on work or earning to a point of damaging your relationships.

Under-spending is frugality taken to extremes, such as inadequate spending on health care, nutrition, shelter, or clothing even when you can afford them.

Not about Money

How many of the above “disorders” are you guilty of?

All these disorders have one thing in common: fundamentally, they aren’t about the money. A given pattern of behavior around money can be someone’s unconscious response to emotional pain, in the same way addiction or anger might be.

For that particular person, the money behavior may just happen to be the medicator that works to cope with deep emotional stress. While one person may find relief in alcohol or drugs and another may find it in work, someone else might use shopping or hoarding as a way to feel better and function in the world.

An Addiction?

Just like addictions, however, money disorders only relieve pain for a short time. In the long term, they only cause more pain. The result is an escalating cycle of destructive behavior that has many negative consequences, including financial ones.

Rag Mags

To see how emotional health and financial health are linked, all you have to do is read a celebrity magazine or look around at the people you know. I’ve seen high-earning doctors and other medical professionals who have a negative self-worth because they can’t control their spending. We all know people who bounce from one financial mess to another, never seeming to learn from their money mistakes. Some very capable and intelligent doctors struggle financially and in their careers because of emotional issues that have nothing directly to do with money.

Counseling

Counseling to resolve emotional issues may seem to be a low-priority expense that comes far down the list after basic needs like housing, food, and transportation. Yet for anyone who struggles to overcome destructive patterns of behavior—even those that aren’t directly about money—counseling can pay off in very real monetary ways.

Assessment

Emotionally healthy and confident people make better choices about relationships, careers, and other major aspects of their lives. They also make better choices about money. This is why counseling is more than an investment in your emotional health. It can also make a measurable difference in your financial health.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Posted on April 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Otherwise known as “National Prescription Drug Take Back Day,” National Drug Take Back Day on April 25th is sponsored by the Drug Enforcement Agency. Its goal is to keep the public aware of the dangers of prescription drug use and misuse. Many Americans don’t know how to safely dispose of the prescription drugs that have been sitting in the medicine cabinet past their prime. Using these expired drugs, or using someone else’s, is dangerous and puts both the public and the environment at risk.

Spotify made money in Q1. According to Morning Brew, the streaming music giant grew its revenue last quarter by 20% to $3.8 billion on a record $180 million in profit, it announced yesterday. The smash report comes after Spotify cut costs last year, which included laying off more than a quarter of its workforce. The company also raised prices in 2023 for the first time in a decade as it further expanded beyond music into audio books and other categories. Spotify shares soared ~11% following the news.

***

Here’s where the major benchmarks ended:

The S&P 500 index® (SPX) rose 1.08 points (0.02%) to 5,071.63; the Dow Jones Industrial Average® ($DJI) fell 42.77 points (0.1%) to 38,460.92; the NASDAQ Composite® ($COMP) added 16.11 points (0.1%) to 15,712.75.

The 10-year Treasury note yield rose more than 4 basis points to 4.644%.

The CBOE Volatility Index® (VIX) rose 0.28 to 15.97.

Transportation shares were among the market’s weakest performers Wednesday behind a drop of more than 10% in Old Dominion Freight Line (ODFL), which reported lighter-than-expected quarterly revenue. The shipper’s nosedive helped send the Dow Jones Transportation Average ($DJT) down 2.3%. Consumer staples, semiconductors, and utilities posted moderate advances. The Dow Jones Utility Index ($DJU) gained for the sixth straight day and ended at a three-and-a-half-month high.

***

The National Association of Realtors’ $418 million settlement over an alleged conspiracy to inflate commissions received preliminary approval yesterday. It’s a new world order: Sellers won’t have to pay buyers’ agents anymore. There’s been talk of a metaphorical death of real estate agents, or a mass extinction; the jury is still out, but RE/MAX cofounder and chairman Dave Liniger doesn’t seem too concerned.

The Labor Department announced it has finalized its Retirement Security Rule, which aims to protect American workers who are saving for retirement and relying on advice from fiduciaries for it. The new rule will update the definition of an investment advice fiduciary under the Employee Retirement Income Security Act and the Internal Revenue Code.

Clinicians don’t always get it right, and their mistakes can be costly: Studies show misdiagnoses lead to roughly 800,000 patient deaths or permanent disabilities each year in the US and cost the healthcare system an estimated $20 billion annually. Cleveland Clinic is using telehealth to try to combat misdiagnoses via its virtual second opinions program, which has saved an average of $8,705 per patient by avoiding unnecessary treatments, according to an analysis released in March.

Posted on April 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Tesla’s pivotal earnings call yesterday had the vibes of an undergrad at office hours begging for extra credit after failing every assignment all semester. The automaker whiffed on revenue targets, even after tempering expectations.

And, forthe first time since 2020, the EV-maker’s quarterly revenue dropped, falling to $21.3 billion, compared with $23.3 billion from the same period a year ago (analysts were expecting about $22b). Tesla’s profits sunk to a six-year low. The company said earlier this month that it only delivered 386,810 cars in the first quarter, down 8.5% from the same time in 2023.

On the bright side according to Morning Brew, despite the earnings miss, Tesla’s stock went up in after-hours trading, likely because the company vowed to accelerate the launch of more affordable models. It announced it was working on integrating ride-hailing technology into its app in a bid to take on Uber, and that the growth of its energy storage business is set to outpace that of its auto business this year.

That signal came amid broader concern that Tesla would move away from its traditional car making roots in favor of a business model focused on autonomous driving, robotics and AI-related technologies. It triggered an after-hours jump in Tesla stock that was cemented by a shareholder-friendly conference call from Chief Executive Elon Musk.

“I think we’ll have higher sales this year than last year,” Musk told investors, even as the group reiterated its forecast for “notably lower” vehicle deliveries for the current year.

Posted on April 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: 740. That’s how many employees Nike will lay off at its Oregon HQ before the end of June. In February, Nike CEO John Donahoe informed employees of the company’s plan to reduce 2% of its workforce, which would mean around 1,600 employees in total. (USA Today)

Let’s say you leave your job at any time during or after the calendar year you turn 55 (or age 50 if you’re a public safety employee with a government defined-benefit plan). Under a little-known separation-of-service provision, often referred to as the “rule of 55,” you may be able take distributions (though some plans may allow only one lump-sum withdrawal) from your 401(k), 403(b), or other qualified retirement planfree of the usual 10% early-withdrawal penalties. However, be aware that you’ll still owe ordinary income taxes on the amount distributed. This exception applies only to the plan (including any consolidated accounts) that you were contributing to when you separated from service. It does not extend to IRAs.

The S&P 500 index rose 59.95 points (1.2%) to 5,070.55; the Dow Jones Industrial Average gained 263.71 points (0.7%) to 38,503.69; the NASDAQ Composite® ($COMP) surged 245.33 points (1.6%) to 15,696.64.

The 10-year Treasury note yield (TNX) decreased about 2 basis points to 4.602%.

The CBOE Volatility Index® (VIX) fell 1.25 to 15.69.

Similar to Monday, chipmakers were among the market’s strongest areas, carrying the Philadelphia Semiconductor Index (SOX) to a 2.2% advance. Retailers and communication services shares were also strong. The Dow Jones Utility Index ($DJU) gained for the fifth straight day and ended at its highest level in over three months. The Russell 2000® Index (RUT) surged nearly 2%.

Posted on April 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Busy earnings week will focus on the Magnificent Seven

Big Tech is leading the stock-market rout, but in the coming days, it has the opportunity to turn things around. Magnificent Seven members Microsoft, Meta, Alphabet, and Tesla are among the 178 S&P 500 companies scheduled to report their earnings this jam-packed week.

Other blue-chip stocks reporting include GM, Boeing, IBM, and PepsiCo.

Posted on April 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The March Consumer Price Index, which the Bureau of Labor Statistics released last week, revealed that core inflation hit 3.8% Year over Year in March, rising for the first time in 12 months. That’s moving in the wrong direction for the Fed, whose goal is to bring inflation down to 2%.

The S&P 500 index rose 43.37 points (0.9%) to 5,010.60; the Dow Jones Industrial Average® ($DJI) gained 253.58 points (0.7%) to 38,239.98; the NASDAQ Composite advanced 169.30 points (1.1%) to 15,451.31.

The 10-year Treasury note yield (TNX) was little changed at 4.617%.

The CBOE Volatility Index® (VIX) fell 1.41 to 16.39.

Chipmaker strength lifted the Philadelphia Semiconductor Index (SOX) up 1.7% Monday, partially reclaiming last week’s 9.2% tumble. Banking shares were also among the strongest sectors, while the Russell 2000® Index (RUT) advanced 1%. WTI crude futures earlier dropped to just a few cents above $82 per barrel, the lowest intraday price since late March.

“Telemedicine has a lot of potential to bridge barriers and make it convenient for people to access healthcare. But it’s limited by lack of tools. Your doctor can’t reach through the computer screen.”—Akshaya Anand, co-founder of Korion Health, on the startup’s efforts to create an electronic stethoscope for clinicians to record heart and lung movement (Maryland Today)

Posted on April 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A SPECIAL REPORT

(In case you missed it)

***

By Vitaliy Katsenelson CFA

***

I am going to share with you excerpts from a research paper I wrote in 2018 about Tesla and electrical vehicles (EVs), which I have turned into a small book for reader convenience (it is available for free, here). I want to share these essays with you today because we are at a pivotal moment for traditional carmakers, and these essays, which I have not updated, present an important thinking framework about the industry.

It is easier to convince shareholders and the board of directors to invest money into new factories when the demand for EVs is growing, even if you are losing money per vehicle. At least there is hope that once you get to scale and perfect new technology, the losses will turn into profits.

However, when the demand for electrical vehicles stutters and your inventory of EVs starts piling up – which is exactly what is happening right now – investing in EVs becomes very difficult (I wrote about it here).

Retreating to what you know, what has worked for almost a century, what doesn’t generate huge losses with every vehicle sold, and what your current workforce is trained for, and comfortable producing, seems like a natural decision. The decisions traditional carmakers will make over the next year or two will be very important for what their future looks like a decade or two from now.

Posted on April 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A group of 15 financial officers representing 13 states issued a warning to Bank of America over its alleged practices of “politicized de-banking” targeting conservatives. In a letter to Bank of America CEO Brian Moynihan, the officials said the bank’s practices threaten its own financial health and reputation with customers while simultaneously harming the U.S. economy and Americans’ civil liberties. They pointed to examples of Bank of America shuttering the accounts belonging to Christian groups and leaders and joining a net-zero climate alliance in addition to its poor viewpoint diversity rating.

Texas and Missouri will soon have about two dozen Walmart health centers, the retail giant announced this month, adding to its 50-site roster. The company plans to open eight clinics in the Houston metro area, 10 sites in the Dallas-Fort Worth area, and four facilities in Kansas City by the end of 2024, Modern Healthcare reported.

Hospitals reported the strongest quarter of mergers and acquisitions since 2020, according to consulting firm Kaufman Hall. Four of the 20 announced transactions in the first quarter of 2024 were “megamergers” and brought in $12 billion in revenue in that time period, per the firm’s analysis. The era of consolidation is here.

The S&P 500 index fell 43.89 points (0.9%) to 4,967.23, down 3% for the week; the Dow Jones Industrial Average gained 211.02 points (0.6%) to 37,986.40, little changed for the week; the NASDAQ Composite lost 319.49 points (2.1%) to 15,282.01, down 5.5% for the week.

The 10-year Treasury note yield (TNX) dropped more than 2 basis points to 4.623%, still up about 10 basis points for the week.

The CBOE Volatility Index® (VIX) rose 0.71 to 18.71.

Nvidia (NVDA) plunged 10% to lead the chip sector lower, sending the Philadelphia Semiconductor Index (SOX) down 4.1% to a two-and-a-half-month low. Communication Services shares were also among the weakest sectors, fueled by Netflix weakness. There were several pockets of strength, however. Banking shares posted firm gains Friday behind stronger-than-expected quarterly results from some regional lenders. Utilities also advanced.

The S&P 500 has fallen 5.5% from a record close March 28, more than halfway to the 10% threshold that’s traditionally viewed as a correction. The NASDAQ Composite is down 7.1% from a record close on April 11th.

Posted on April 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

If the practice makes a reasonable effort to collect from a patient who is experiencing financial hardship (e.g., job loss due to COVID-19), providers may be able to offer a discount (e.g., settle for 70% of the amount owed) without violating Stark Law, says Reed Tinsley, CPA, healthcare consultant in Houston, Texas. “But remember that just because even if someone doesn’t have a job, they could still have money,” he adds. “There are a lot of people out there with big savings accounts.”

Source: Lisa A. Eramo, MA, Keith A. Reynolds, Physicians Practice [4/3/24]

23andMe cofounder and CEO Anne Wojcicki wants to take the once-hot DNA company private. 23andMe said a Special Committee would evaluate the proposal in light of other options. The company’s valuation has tumbled since its stock market debut in 2021. The struggling DNA company once valued in the billions — was essentially worthless as of Wednesday.

But,shares soared Thursday less than three years after it began selling shares. Wojcicki told board members she is proposing to acquire the company in a potential go-private transaction, according to a filing with the Securities and Exchange Commission.

The S&P 500 index fell 11.09 points (0.2%) to 5,011.12; the Dow Jones Industrial Average® ($DJI) rose 22.07 points (0.1%) to 37,775.38; the NASDAQ Composite lost 81.88 points (0.5%) to 15,601.50.

The 10-year Treasury note yield (TNX) gained almost 5 basis points to 4.633%.

The CBOE Volatility Index® (VIX) dropped 0.22 to 17.99.

Weakness in chip maker shares pushed the Philadelphia Semiconductor Index (SOX) down 1.7% to a two-month low. Biotechnology and consumer discretionary shares were also among the weakest sectors. Energy companies eroded as WTI Crude Oil (/CL) futures dropped for a third straight trading day and closed at a three-week low.

The S&P 500 is on track for its third consecutive weekly decline, its weakest stretch since September, while the NASDAQ Composite appears headed for a fourth straight weekly slide.

You’ve got a sense of your ideal retirement age. And you’ve probably made certain plans based on that timeline. But what if you’re forced to retire sooner than you expect? Aging baby-boomers, corporate medicine, the medical practice great resignation and/or the pandemic, etc?

Early retirement is nothing new, but it’s clear how much the COVID-19 pandemic has affected an aging workforce. Whether due to downsizing, objections to vaccine mandates, concerns about exposure risks, other health issues, or the desire for more leisure time, the retired general population grew by 3.5 million over the past two years—compared to an annual average of 1 million between 2008 and 2019—according to the Pew Research Center.1 At the same time, a survey conducted by the National Institute on Retirement Security revealed that more than half of Americans are concerned that the COVID-19 pandemic has impacted their ability to achieve a secure retirement.2

***

***

There’s no need to panic, but those numbers make one thing clear, says Rob Williams, managing director of financial planning, retirement income, and wealth management for the Schwab Center for Financial Research. Flexible and personalized financial planning that addresses how you’d cope if you had to retire early can help you make the best use of all your resources.

So – Here are six steps to follow. We’ll use as an example a person who’s seeing if they could retire five years early, but the steps remain the same regardless of your individual time frame.

Step 1: Think strategically about pension and Social Security benefits

For most retirees, Social Security and (to a lesser degree) pensions are the two primary sources of regular income in retirement. You usually can collect these payments early—at age 62 for Social Security and sometimes as early as age 55 with a pension. However, taking benefits early will mean that you get smaller monthly benefits for the rest of your life. That can matter to your bottom line, even if you expect Social Security to be merely the icing on your retirement cake.

On the Social Security website, you can find a projection of what your benefits would be if you were pushed to claim them several years early. But if you’re part of a two-income couple, you may want to make an appointment at a Social Security office or with a financial professional to weigh the potential options.

For example, when you die, your spouse is eligible to receive your monthly benefit if it’s higher than his or her own. But if you claim your benefits early, thus receiving a reduced amount, you’re likewise limiting your spouse’s potential survivor benefit.

If you have a pension, your employer’s pension administrator can help estimate your monthly pension payments at various ages. Once you have these estimates, you’ll have a good idea of how much monthly income you can count on at any given point in time.

***

Step 2: Pressure-test your 401(k)

In addition to weighing different strategies to maximize your Social Security and/or pension, evaluate how much income you could potentially derive from your personal retirement savings—and there’s a silver lining here if you’re forced to retire early.

Rule of 55

Let’s say you leave your job at any time during or after the calendar year you turn 55 (or age 50 if you’re a public safety employee with a government defined-benefit plan). Under a little-known separation-of-service provision, often referred to as the “rule of 55,” you may be able take distributions (though some plans may allow only one lump-sum withdrawal) from your 401(k), 403(b), or other qualified retirement plan free of the usual 10% early-withdrawal penalties. However, be aware that you’ll still owe ordinary income taxes on the amount distributed.

This exception applies only to the plan (including any consolidated accounts) that you were contributing to when you separated from service. It does not extend to IRAs.

4% rule