BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on April 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

If you need a reprieve to prevent the government from raiding your bank account, you’re not alone—the IRS expects 19 million people to file for an extensionthis year. The agency will automatically grant you a six-month extension, although it’s recommended you remit a payment by April 15th if you expect to owe money to avoid interest and penalties. The good news is you probably won’t have to fork over as much as Mark Cuban, who said he is sending the IRS $288 million today and is proud to pay his fair share.

The stock market is coming off its worst week of the year, and the road ahead is no less bumpy. A direct military confrontation between Iran and Israel has investors on edge about a wider regional war that threatens energy supplies. Amid the uncertainty, safe-haven assets are seeing major interest: The US dollar just had its best week in more than 18 months.

Questions – from doctors – like these remind me that the workings of the financial services industry which I tend to take for granted but can be confusing to people outside the field.

The following analogy may help to explain.

Orchestra Analogy

Think of an orchestra. The investment adviser is the equivalent of the director/conductor and the money managers are the instrumentalists. Each one is a specialist who plays a particular type of instrument, and it takes a variety of these specialists to make up the orchestra.

Specialists

The broad specialties are the types of instruments, such as strings, brass, winds, and percussion. These are the equivalent of fund managers who specialize in asset classes like equities, bonds, real estate, commodities, and absolute returns.

Sub-Specialists

Within each specialty are a variety of subspecialists. Winds, for example, include clarinets, oboes, and saxophones—which are further divided into alto, soprano, tenor, and bass. The brass section has French horns, trumpets, and trombones. The divisions and sub-divisions go on and on. Similarly, within the various asset classes are a great many mutual fund managers who specialize in narrower subcategories.

Conductor

The task of the orchestra conductor-director is to pick, not just the best musicians, but the best mix of musicians. A group with only trumpets or every subspecialty of percussion, no matter how skilled, isn’t an orchestra. Before auditioning a single musician, the director’s first task is to clarify the purpose of the ensemble being created. A different mix of instruments will be required for a symphony, a marching band, an intimate chamber group, or a dance band. It all depends on what the audience wants.

The conductor-director needs to weigh the various musicians’ abilities against their cost and their specific specialties against the needs of the orchestra. When the right mix of players has been chosen, the director needs to pick the appropriate music, assemble the group, and rehearse. The director’s talent, experience, and leadership skills all serve to help the right players produce the right sound for their audiences.

***

***

It takes similar coordination and skill to put together the right mix of asset classes and mutual fund managers to produce the best results for various clients, especially since there are some 17,000 mutual funds to choose from.

Fees

Just as both the orchestra director and the musicians are paid based on their skills and their work, both mutual fund managers and investment advisers are paid based on the assets they manage. Mutual fund managers earn 0.05% to 3.0%. Financial advisers earn 0.30% to 3.0%. An informed consumer could pay as low as 0.35% while an uninformed consumer could pay up to 6% a year, which would eat up most of the investment returns.

One essential responsibility for an adviser, then, is to choose mutual fund managers whose fees are low.

However, the cost of the mutual fund manager isn’t the be-all and end-all. One must also weigh performance, just as an orchestra director might pay more to get an outstanding musician who would add significant value to the performances.

Example:

For example, my firm’s overall average fee for mutual fund managers is 0.5%. We could get that as low as 0.1%, which might be impressive at first glance.

However, we would give up 0.25% to 1.00% of net return in some areas, resulting in poorer outcomes for the clients.

***

***

Assessment

Skilled direction of an orchestra is obviously more art than science. Skilled coordination of mutual fund managers is the same. Both require knowledge, integrity, and commitment to the quality of the final product.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

An attractive investment and a polished sales pitch can often hide the underlying costs of the investment, leading some medical professionals to give up a significant portion of the long-term growth of their assets to fees. Fees absolutely matter.

In a good market investors have a propensity to ignore them and in challenging markets they are scrutinized, but in the end no matter what type of market we are in fees do make a substantial difference in your long-term investment returns.

Assessing the Worth of the Investment

The first step in assessing the worth of the investment under consideration is figuring out what the fees actually are. If a medical professional is investing in a mutual fund, these costs are found in mutual fund company’s now obligatory “Fund Facts”.

This manuscript clearly outlines all the fees paid – including upfront fees (or commissions/loads), deferred sales charges, and any switching fees. Fund management expense ratios are also part of the overall cost of ownership. Trading costs within the mutual fund can also impact performance.

The List of Fees Keep Coming … and Coming!

Here is a list of the traditional fees from investing in a mutual fund:

Front end load: It is the commission charged to purchase the fund through a broker or financial advisor. The commission reduces the amount you have available to invest. Thus if you start with $100,000 to invest and the advisor charges a 5 percent front end load, you end up actually investing $95,000.

Deferred Sales Charge (DSC) or back end load: Charge imposed if you sell your position in the mutual fund within a pre-specified period of time (normally five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: These are costs charged by the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing.

Annual Administration Fee: Many mutual fund companies also charge an additional fee just for administering the account – usually under $150 per year. A 1 percent disparity in fees for a medical professional may not seem like a lot. But fees do make a considerable impact over a longer time period. [For example, a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the client pays a 2 percent operating fee. In comparison, if the investor opted for a fund that charges a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000! For many investors, this is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more fee savings over an elongated period of time].

***

[The Carousel of Fees]

Assessment

Fees and expenses can have significant impact on the performance of your investments. Always monitor the costs of an investment program to ensure that fees and expenses are reasonable for the services provided and are not consuming a disproportionate amount of the investment returns.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

“Worried about an IRS audit? Avoid what’s called a red flag. That’s something the IRS always looks for. For example, say you have some money left in your bank account after paying taxes. That’s a red flag.“

― Jay Leno

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Americans are saving less at their lowest pace in more than a year, and are apparently spending more than the growth of their incomes, according to an analysis by Wells Fargo that was shared with Newsweek.

In February, the personal savings rate hit 3.6 percent, “marking the lowest rate at which households saved in 14 months,” Wells Fargo economists noted in the Thursday report, adding that spending outpaced income growth for the month. The savings rate is higher than the below 3 percent level it fell to following the COVID-19 pandemic, but is nevertheless way down from the pre-pandemic rate of 6 percent.

The deadline for most people to file a 2023 tax return with the IRS is fast approaching; returns are due by 11:59 p.m., in your time zone, on Monday, April 15th today, with some exceptions. Taxpayers in Massachusetts and Maine have until April 17th to file and pay taxes because of the Patriots’ Day and Emancipation Day holidays. There are also extensions in some areas impacted by extreme weather. Individuals and businesses impacted by the October 7th attack on Israel have also been given an extension, the IRS announced. There are extensions for certain active-duty military members and citizens living abroad.

Nike announced plans to lay off around 1,600 employees, or about 2% of its global workforce, as part of a $2 billion cost-cutting strategy. CEO John Donahoe said performance has not been the best and took responsibility. Donahoe said, “This is a painful reality and not one that I take lightly.”

Stellantis is the world’s fourth-largest automaker by sales, behind Toyota, Volkswagen Group, and Hyundai Motor Group. The company designs, manufactures, and sells automobiles bearing its 14 brands: Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS, Fiat, Jeep, Lancia, Maserati, Opel, Peugeot, Ram, and Vauxhall. Their headquarters is located in Amsterdam, and they have over 300,000 employees in 130 countries.

***

The Biden administration wants to make changes to private Medicare insurance plans that officials say will help seniors find plans that best suit their needs, promote access to behavioral health care and increase use of extra benefits such as fitness and dental plans. “We want to ensure that taxpayer dollars actually provide meaningful benefits to enrollees,” said Health and Human Services Secretary Xavier Becerra. If finalized, the proposed rules rolled out Monday could also give seniors faster access to some lower-cost drugs. Administration officials said the changes, which are subject to a 60-day comment period, build on recent steps taken to address what they called confusing or misleading advertisements for Medicare Advantage [Part C] plans. Just over half of those eligible for Medicare get coverage through a private insurance plan rather than traditional, government-run Medicare.

***

Healthcare varies substantially by state based on dozens of factors. The same is valid for cities. Some of this is due to the availability of medical facilities. Some have to do with health habits. Some have to do with incomes and poverty levels. People who live in poor states, based on income, almost always have unhealthy populations. A new study from Renew Bariatrics shows the “Healthiest (and Unhealthiest) States in the US—2024 Rankings,” and reviews alcohol use, diabetes, drug overdoses, mental health, isolation, tobacco use, exercise, and the presence of heart disease, obesity, and cancer. These, taken together, create an index from 0 to 100, with 100 being the worst possible score. These are the most expensive states to live in.

Posted on April 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

DEFINITION: Tax season is the period of time, generally between January 1st and April 15th of each year, when individual taxpayers prepare to report their taxable income to the federal government and, in most cases, to the government of the state in which they live.

Some Year-End Preparation for the Upcoming Tax Filing Season

The filing season for 2023 tax returns us now upon us. A little advance preparation can prevent stressful tax time surprises for doctors and all medical professionals. Here are some important steps you can take now to set yourself up for worry-free tax filing:

Do one last withholding checkup. Time is running out to adjust your paycheck withholding to make sure you have paid enough tax throughout 2023. You can use the online IRS Withholding Estimator tool to make sure your numbers are on track.

If your name changed in 2023, report the change to the Social Security Administration as soon as possible, preferably before the end of the year.

Locate your bank account information, including both your account number and the bank routing number, so you can receive your tax refund by direct deposit.

Watch for year-end income statements, especially in late January and early February. These statements may include W-2 forms, along with 1099-NEC, 1099-MISC, 1099-INT, 1099-G and other 1099 forms. Note that some of these forms may come by mail, while others may be sent to you electronically. Keep all of the forms together and organized.

Organize records for tax deductions and credits. These records may include Form 1095-A (Health Insurance Marketplace Statement), tuition statements (Form 1098-T), medical bills, mortgage interest statements, and home energy improvement or clean vehicle receipts or invoices.

Waiting until the last minute to try to assemble these documents can lead to missing the filing deadline, so start early.

Posted on April 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Medial Office Equipment Interest Rate Costs

Dr. David E. Marcinko; MBA, MEd, CMP™

[Publisher in Chief]

Physicians, administrators and healthcare entrepreneurs are aware of the compounding effect of interest.However, since interest is deductible as a medical office business expense, many seem to forget about it despite the fact that it must be continually paid until the asset is either purchased or otherwise disposed.

So, what are the various types of interest rates important to the medical practitioner and commodity – money?

[1] Simple Interest

Simple interest is merely the pro rata interest on a loan or deposit and represents the most basic interest rate type.

For example, for every $100 Dr. Bill borrows at 12 percent annual interest, he pays twelve dollars per year. The interest is calculated by multiplying the principal or original amount, by the interest rate in decimal form (100 x .12).

[2] Add-On Interest

Add on interest immediately attaches the annual interest amount, to the principal amount, at the beginning of the payment period. Payments are then made according to the number of years required.

The following formula is useful:

Add-on-Interest minus Payment = Total Interest on Balance/Number of Payments

For example, if Dr. William Needy borrows $10,000 at 8 percent add-on interest, he will repay $10,000 plus $ 800 ($10,000 x 8%) or $10,800, divided by twelve months, for a total of $900 per month, since $ 900/month x 12 months equals $10,800.

[3] Discounted Interest

When using the discounted interest method, the interest amount is deducted from the principal right up front. Notice that this is the opposite of add-on-interest that is applied up front.

For example, if Dr. Bill borrows the same $ 10,000 at a discounted interest rate of 8 percent, he will only receive a $9,200 loan, since $10,000 – $800 is $9,200.

Obviously, the discount method is the most expense way to borrow money.

[4] Annual Percentage Rate

Most financial institutions advertise an annual percentage rates (APR) for loans, deposits and investments. The APR is the periodic interest rate multiplied by the number of periods a year. If the APR is 12 percent, and interest is compounded monthly, you receive (or pay) 1 percent of your balance each month, and the balance shifts with each compounding.

For example, if Dr. Bill deposits $ 100 dollars at 12 percent APR compounded monthly, he receives $ 1 interest the first month (1% of $100), $1.10 the second month (1% of $101), and so forth. If compounding is daily, the interest accumulates at the rate of 1/365 of the APR each day.

Unless interest is compounded annually, the APR will be lower than the effective annual interest rate, discussed below.

[5] Effective Interest Rate

It is important to differentiate between the effective interest rate and the APR, which is often the most prominent figure in advertisements for medical business equipment, consumer goods and financial services (loans, annuities, IRAs, CDs, investment analysis, college funding or retirement planning). Although the APR is the periodic interest rate multiplied by the number of periods per year, the effective annual interest rate is the periodic rate, compounded.

In our case, if the APR is 12 percent, compounded monthly, the monthly interest rate is 1 percent and the effective annual rate is the monthly rate compounded for 12 periods.

Therefore, if your calculation is for a single year, you can treat the effective rate as simple interest. If you deposit (or borrow) $1,000 at 12 percent APR, the effective rate is 12.68 percent, and interest for the first year is about $126.80 (12.68% of $1,000).

For longer periods, you can use the effective interest rate as the periodic interest rate, compounded annually.

[a] “Rule of 72” (Double your Money)

The number of periods required to double a lump sum of money can be quickly estimated by using what is known as the “Rule of 72”. To get the number of periods, usually years, just divide 72 by the periodic interest rate, expressed as a whole number (not a decimal).

For example, if the annual interest rate is 10 percent, it will take about 7.2 years (72/10) to double any lump cache of money. Conversely, you can also calculate the interest rate required to double your money in a given period by dividing 72 by the term.

Thus, to double your money in ten years, you need to earn about 7.2 percent annual interest (72/10) = 7.2%).

[b] “Rule of 78”

According to this method, interest is front end loaded like a home mortgage, or office condominium, to discourage prepayment of a loan and consequently preserve the lender’s profit. In other words, it is a method of calculating installment loan interest rebates.

The number 78 comes from an approved method of accelerated tax depreciation, known as the “Sum of the Years Digits” (SOYD) method (i.e., 12 + 11 + 10 + 9 . . . = 78). This fact is important because, throughout the period of a loan, even though the payments are all the same, the portions that are interest and principal are very different.

Using this method for a one year loan shows that, in the first payment, 15.38 percent of the interest due is paid off, and by the sixth month, 73.08 percent of the interest is paid off. This means, that if a physician makes a one year equipment loan with a total interest charge of $ 100 and pays the loan off in full with the sixth payments, he or she will not get an interest rebate of $ 50, but only $ 26.92, since $ 73.08 of the interest has already been prepaid.

Most ethical lenders use simple interest rates for loan rebates, and the Rule of 78 is unfair according to many authorities.

[c] “Rule of 116”

A derivative of the Rule of 72 is the Rule of 116. This determines the number of years it takes for a principal amount to be tripled and is calculated by dividing the annual interest rate into 116.

The Rules of 72 and 78 are very handy for figuring the amount of interest payments made or growth of funds invested. They can also be used in reverse to calculate at what rate of interest money must be invested to double or triple in a certain number of years.

[6] Medical Equipment Payback Cost Analysis

The payback period, expressed in years, is the length of time that it takes for the medical equipment investment to recoup its initial cost out of the cash receipts it generates. The basic premise is that the quicker the cost of an investment can be recovered, the better the investment is. It is most often used when considering equipment whose useful life is short and unpredictable.

When the same cash flow occurs every year, the formula is as follows:

Investment Required / Net Annual Cash Inflow = Payback Period

Thus, in today’s tightening medical reimbursement atmosphere, practice cost control and expense reduction is the easiest method to increase medical office profitability. Keeping the cost of the commodity money in the form of interest rate charges, as low as possible, will assist in this endeavor

Assessment

And so, how have these rules affected your medical office borrowing costs; if at all? Does these principles apply to the medical student loan crisis, today?

Posted on April 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Essay on the Eight-Hundred Pound Gorilla in the Medical Treatment Room

By Dr. David E. Marcinko MBA MEd CMP

[Editor-in-Chief]

According to economist Austin Frakt PhD, and others, there is a school of thought that says Congress is incapable of controlling costs in the Medicare and Medicaid System [CMS].

And, then there is the reality known by all practicing medical professionals regardless of specialty orientation or degree designation. That is to say, CMS really can control healthcare costs and with great ferocity and efficiency, and to non-public sectors as well …. PARADOXICAL?

On Getting What You Wish For

Blogger Ezra Klein opines that one of the dirty little secrets of the health-care system is that Medicare has done a much better job controlling costs than private health insurers.

Of course, we doctors know that the real problem is that Medicare seemingly [think Seinfeld’s character George Costanza] controls costs all too well; but not really. It is just that CMS pays doctors too little and thus it appears costs are controlled. What really is happening is that physician fees are being reduced carte’ blanche.

Nevertheless, and regardless of semantics, CMS will never control costs much more efficiently than private insurance companies or doctors will simply abandon Medicare for related payment models like direct reimbursement or concierge medicine. This is happening right now. Physicians, osteopaths and podiatrists etc, are opting out of Medicare in increasingly large numbers. In a world where there’s only Medicare and Medicare to control costs, doctors can either take the pay cut or stop seeing patients, and stop being doctors. “Taking what they are given – because they’re working for a livin.”

So sorry that this seems like a forehead-palm moment for Ezra, but not for healthcare practitioners or the ME-P!

Too Much Demand Elsewhere

And, as we see from other countries, many young bright folks want to be doctors, even if being a doctor doesn’t make one particularly wealthy [high demand and high eventual supply produces lower provider costs in the long term?]. Think medical tourism.

Not so much the case anymore in this country [lower demand and lower eventual supply produces higher reimbursement costs to the doctor survivors in the very long term?].

Our Domestic World

But, we are not elsewhere. In fact, in our present domestic healthcare ecosystem, when Medicare decides to control costs, many doctors can simply stop accepting Medicare patients, and the politicians will lose their jobs. One political party then declares that Medicare is rationing and will hurt senior citizens. The other party capitulates and pays MDs more [SGR]. Then, the federal budget looks bad as it does now. The circle is complete when one party asserts that Medicare actually can’t contain costs but the private insurance companies will. It all fails, in an unending circular Boolean-like loop of illogic.

Listen Up!

So, listen up AARP, politicians, CMS and seniors as I admonish you to be careful what you wish for [medical cost controls]. It might just come true. As Ezra rightly says; rinse, repeat – rinse, repeat – ad nausea. You simply can’t have it both ways. You either choose to spend less and offend certain cohorts, or spend more and offend different factions. Either way, you’re going to piss someone off. A good healthcare reimbursement system would try to make that decision rationally [a-politically]. But, at least it would make an economics driven decision; wouldn’t it?

Assessment

Is CMS really the eight hundred pound cost-controlled gorilla in the increasingly large Medicare treatment room? Why or why not? Now, relative to the ACA of 2010, please read: The Case for Public Plan Choice in National Health Reform [Key to Cost Control and Quality Coverage], by Jacob S. Hacker, PhD. Link:Jacob Hacker Public Plan Choice

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Do we have a Medicare cost control efficiency paradox? Or, are the economists just reveling in the publication banal? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed: And, credible sponsors and like-minded advertisers are always welcomed.

Posted on April 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST– Today’sNewsletter

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

NEW YORK (Reuters) -The U.S. accounting watchdog on Wednesday said it has hit KPMG Netherlands with a $25 million civil penalty, a record for the regulator, in response to “egregious” and widespread exam cheating at the foreign affiliate of the major audit firm.

As millions of Americans approach age 66, they face the inevitable question, is it time to retire? The physician population is aging alongside the general population—more than 40% of physicians in the U.S. will be 65 years or older within the next decade. In the case of surgeons, there is little guidance on how to best ensure their competency throughout their career and at the same time maintain patient safety while preserving mature physician dignity.

It is a scenario playing out nationwide. From Oregon to Pennsylvania, hundreds of communities have in recent years either stopped adding fluoride to their water supplies or voted to prevent its addition. Supporters of such bans argue that people should be given the freedom of choice. The broad availability of over-the-counter dental products containing the mineral makes it no longer necessary to add to public water supplies, they say. The Centers for Disease Control and Prevention says that while store-bought products reduce tooth decay, the greatest protection comes when they are used in combination with water fluoridation.

More health systems are going to be opting out of Medicare Advantage (MA) plans, George Hill, a managing director at Deutsche Bank in Boston, predicted Monday at a “Wall Street Comes to Washington” webinar hosted by the Brookings Institution. “I think you’re going to see more large provider organizations threaten to opt out of networks, particularly as it relates to MA,” Hill said, adding that there are a number of reasons for this. “Prior authorizations are the problem, claims denials are a huge problem, delayed payments and rates are the problem — barriers in access to care in all varieties are the problem.”

The latest budget update from the nonpartisan Congressional Budget Office (CBO) found that the federal government has spent more on paying interest on the national debt than on the military in fiscal year 2024. The CBO’s budget report for March showed that the U.S. has spent $412 billion on military programs at the Department of Defense through the first half of FY-2024, according to preliminary figures from CBO and the Treasury Department.

Consumer price increases remained high last month, boosted by gas, rents, and car insurance, the government said Wednesday in a report that will likely give pause to the Federal Reserve as it weighs when and by how much to cut interest rates this year. Prices outside the volatile food and energy categories rose 0.4% from February to March, the same accelerated pace as in the previous month. Measured from a year earlier, these core prices were up 3.8%, unchanged from the year-over-year rise in February. The Fed closely tracks core prices because they tend to provide a good read of where inflation is headed.

Here’s where the major benchmarks ended:

The S&P 500® index (SPX) dropped 49.27 points (1.0%) to 5,160.64; the Dow Jones Industrial Average lost 422.16 points (1.1%) to 38,461.51; the NASDAQ Composite® ($COMP) fell 136.28 points (0.8%) to 16,170.36.

The 10-year Treasury note yield (TNX) soared more than 18 basis points to 4.548%.

The CBOE Volatility Index® (VIX) jumped 0.82 to 15.80.

Interest-rate-sensitive sectors like banks, real estate, and utilities led Wednesday’s decliners. The KBW Regional Bank Index (KRX) tumbled 5% to its lowest point since late November. The small-cap Russell 2000® Index (RUT) lost 2.5%. Energy shares were among the few gainers as WTI Crude Oil (/CL) futures rebounded after three-straight losing sessions.

In other markets, the U.S. dollar index (DXY) jumped 1% to a five-month high amid expectations interest rates will remain elevated.

Posted on April 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Physicians Received $12 Billion from Drug & Device Makers in Less Than 10 Years

A review of the federal Open Payments database found that the pharmaceutical and medical device industry paid physicians $12.1 billion over nearly a decade. Almost two thirds of eligible physicians — 826,313 doctors — received a payment from a drug or device maker from 2013 to 2022, according to a study published online in JAMA on March 28th. Overall, the median payment was $48 per physician.

Orthopedists received the largest amount of payments in aggregate, $1.3 billion, followed by neurologists and psychiatrists at $1.2 billion, and cardiologists at $1.29 billion. To find out what any physician was paid, click here.

In a recent survey by Edelman Financial Engines, 57% of respondents said they’d feel wealthy if they had $1 million in the bank. But for many people, like doctors, that may not be enough.

Among those with $500,000 and $3 million in assets, 53% said it would take over $3 million in the bank for them to feel wealthy, and 33% said it would take over $5 million. Given that these are amounts some people will never even come close to amassing in their lifetimes, it may be hard to wrap your head around these answers.

Posted on April 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Since 2013 – Americans believe they now need $1.46 million to retire in style

***

***

The new magic number for retirement, found in a study by Northwestern Mutual, is 15% higher than what people thought they needed last year—and 53% higher than the amount people in 2020 pictured themselves needing to feel comfortable leaving the workforce to sit on a beach in Florida.

In fact, it’s also more than most people have socked away: On average, US adults have $88,400 saved for retirement.

Posted on April 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Intel revealed that its semiconductor-making unit lost $7 billion last year. The news sent the company’s stock down.

And, Amazon is laying off hundreds of employees from its cloud computing division, including the team overseeing its cashierless tech (and not just the Just Walk Out feature it’s pulling from stores), as well as people sales and marketing roles.

Posted on April 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

On March 5th, 2024, the Department of Justice’s (DOJ’s) Antitrust Division, the Federal Trade Commission (FTC), and the Department of Health and Human Services (HHS), announced the launch of a multi-agency inquiry – in the form of a request for information (RFI) and public workshop – focusing on the increasing control of private equity (PE) and other corporations over the healthcare industry.

This Health Capital Topics article discusses the agencies recent actions and how it appears to be in line with the government’s recent moves to crack down on anti-competitive actions in healthcare. (Read more…)

Posted on April 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On March 9th, 2024, President Biden signed into law a $460 billion spending package to continue funding the federal government for the remainder of the 2024 fiscal year. Contained within the spending package was legislation to cut in half the 2024 Medicare physician payment update of approximately -3.4%.

This Health Capital Topics article discusses the payment update, other healthcare provisions contained in the bipartisan spending bills, and responses from stakeholders. (Read more…)

Managerial and medical cost accounting is not governed by generally accepted accounting principles (GAAP) as promoted by the Financial Accounting Standards Board (FASB) for CPAs. Rather, a healthcare organization costing expert may be a Certified Cost Accountant (CCA) or Certified Managerial Accountant (CMA) designated by the Cost Accounting Standards Board (CASB), an independent board within the Office of Management and Budget’s (OMB) Office of Federal Procurement Policy (OFPP).

The Cost Accounting Standards Board

CASB consists of five members, including the OFPP Administrator who serves as chairman and four members with experience in government contract cost accounting (two from the federal government, one from industry, and one from the accounting profession). The Board has the exclusive authority to make, promulgate, and amend cost accounting standards and interpretations designed to achieve uniformity and consistency in the cost accounting practices governing the measurement, assignment, and allocation of costs to contracts with the United States.

Codified at 48 CFR

CASB’s regulations are codified at 48 CFR, Chapter 99. The standards are mandatory for use by all executive agencies and by contractors and subcontractors in estimating, accumulating, and reporting costs in connection with pricing and administration of, and settlement of disputes concerning, all negotiated prime contract and subcontract procurement with the United States in excess of $500,000. The rules and regulations of the CASB appear in the federal acquisition regulations.

North American Industry Classification System (NAICS) codes are used to categorize data for the federal government. In acquisition they are particularly critical for size standards. The NAICS codes are revised every five years by the Census Bureau. As of October 1, 2007, the federal acquisition community began using the 2007 version of the NAICS codes at www.census.gov/epcd/www/naics.html

Cost Accounting Standards

Healthcare organizations and consultants are obligated to comply with the following cost accounting standards (CAS) promulgated by federal agencies:

CAS 501 requires consistency in estimating, accumulating, and reporting costs.

CAS 502 requires consistency in allocating costs incurred for the same purpose.

CAS 505 requires proper treatment of unallowable costs.

CAS 506 requires consistency in the periods used for cost accounting.

The requirements of these standards are different from those of traditional financial accounting, which are concerned with providing static historical information to creditors, shareholders, and those outside the public or private healthcare organization.

Assessment

Functionally, most healthcare organizations also contain cost centers, which have no revenue budgets or mission to earn revenues for the organization. Examples include human resources, administration, housekeeping, nursing, and the like. These are known as responsibility centers with budgeting constraints but no earnings. Furthermore, shadow cost centers include certain non-cash or cash expenses, such as amortization, depreciation and utilities, and rent. These non-centralized shadow centers are cost allocated for budgeting purposes and must be treated as costs http://www.CertifiedMedicalPlanner.org

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Types of Checks

A cashier’s check is a check drawn from the bank’s own funds, not yours, and signed by a cashier or teller. Unlike a regular check, the bank, not the check writer, guarantees payment of a cashier’s check. A cashier’s check can also be called an official check.

A certified check is a personal check that the payer’s bank has certified to be legitimate and has earmarked the funds for the check. It’s a type of “official” payment. People often confuse certified checks with cashier’s checks. … Then, the bank prints a check against the funds they are holding.

A money order is a method of paying for something with cash using a check from a third party. You pay for the money order, and the third party issues you a check that you can give or send to someone. This person deposits the money order in their bank account or exchanges it for cash at a business or post office.

A bank draft is a negotiable instrument where payment is guaranteed by the issuing bank. Banks verify and withdraw funds from the requester’s account and deposit them into an internal account to cover the amount of the draft. A seller may require a bank draft when they have no relationship with the buyer.

Posted on March 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: The stock market kicked off its short trading week down as some investors questioned the enthusiasm around the Fed’s recent assurances that it’s still planning three rate cuts this year.

But Digital World Acquisition Corporation roared as the shell company that’s merging with Donald Trump’s Truth Social and will begin trading under its new ticker, DJT, today.

Digital World Acquisition Corp. (Nasdaq: DWAC) is a special purpose acquisition company formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses.

Posted on March 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Financial hardship has led dozens of operators of senior facilities to file for bankruptcy over the past three years, with 13 companies filing petitions in 2021, 12 debtors filing in 2022 and 15 more in 2023, according to Gibbins Advisors.

***

***

Notable Chapter 11 filings over the past year have included Evangelical Retirement Homes of Greater Chicago, which filed Chapter 11 in the U.S. Bankruptcy Court for the Northern District of Illinois in June 2023 to sell its assets at auction. Also, Windsor Terrace Health, an operator of 32 nursing homes in California and three in Arizona, filed its petition in the U.S. Bankruptcy Court for the Central District of California in August 2023 listing $1 million to $10 million in assets and liabilities and unable to pay its debts.

More recently, Magnolia Senior Living, an operator of four facilities in Georgia, filed for Chapter 11 protection on March. 19 in the U.S. Bankruptcy Court for the Northern District of Georgia.

***

The Great Recession of 2008 had a lot of downsides: People lost homes, jobs, and retirement savings, had their careers derailed, and were forced to learn what the heck synthetic collateralized debt obligations are. But according to recent research, it also made people in the US live longer.

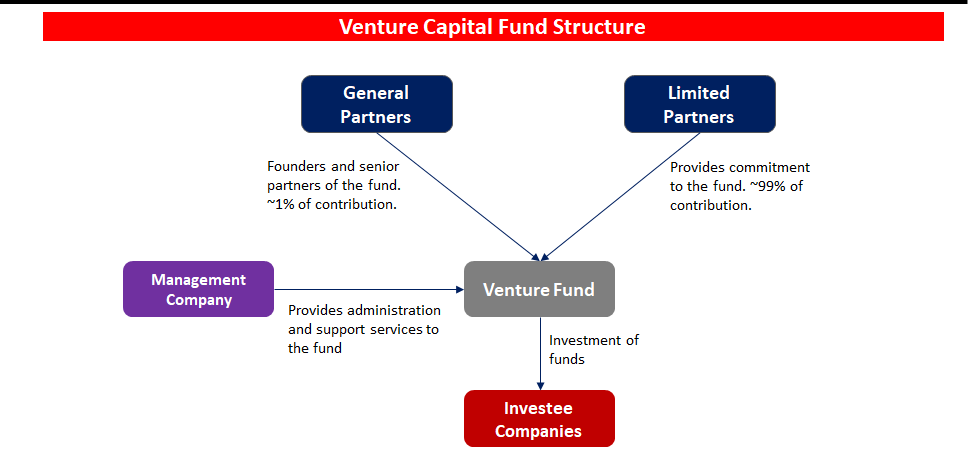

Venture capital funding in the digital health space cooled a bit in 2022 following a red-hot 2021. Overall, digital health companies raised $15.3 billion last year, down from the $29.1 billion raised in 2021—but still above the $14.1 billion raised in 2020, according to Rock Health a seed fund that supports digital health startups.

Nevertheless, analysts predict VC investors and bankers will still put a good amount of money into digital health in 2024 and 2025, especially in alternative care, drug development, health information technology technology, EMRs and software that reduces physician workload.

Of course. an essential first part of attracting VC interest and money is the crafting and presentation of your formal business plan [“elevator pitch”]; as well as the needed technical and managerial experience. This is crucial for success and exactly where we can assist.

Posted on March 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On December 26, 2023, a study published in the Journal of the American Medical Association (JAMA) found concerning changes in patient outcomes and hospital adverse events associated with private equity (PE) acquisition and ownership of hospitals. Over the past ten years, PE firms have set their sights on hospitals as a lucrative investment opportunity, spending nearly $1 trillion to finance healthcare acquisitions, and purchasing more than 200 hospitals from non-PE owners.

Posted on March 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

As tax season kicks off, the Internal Revenue Service is warning taxpayers and administrators of health spending plans that personal expenses for general health and wellness are not legally considered medical expenses, as it fears some may be misled.

In a press release published Wednesday, the IRS reminded individuals filing their taxes that medical expenses for areas such as weight loss are not deductible or reimbursable under health flexible spending arrangements, health savings accounts, health reimbursement arrangements or medical savings accounts, and that they should beware of companies suggesting otherwise.

“Legitimate medical expenses have an important place in the tax law that allows for reimbursements,” said Danny Werfel, the IRS commissioner, in a statement. “But taxpayers should be careful to follow the rules amid some aggressive marketing that suggests personal expenditures on things like food for weight loss qualify for reimbursement when they don’t qualify as medical expenses.”

According to the IRS, while some companies claim that a doctor’s note based on self-reported health information is enough to qualify a non-medical nutritional, wellness or exercise program as a reimbursable medical expense, that’s not the case. Legally, such a note does not back a targeted diagnosis-specific activity or treatment that would qualify as a medical expense, but simply a personal expense. Cite: Newsweek Giulia Carbonaro

Posted on March 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Key inflation data incoming: February’s consumer price index report on Tuesday will provide fresh data to help the Fed decide when to lower interest rates. Last week, Chair Jerome Powell said he needed “just a bit more evidence” that inflation was coming back down to normal levels before reducing rates, though “we’re not far from it,” he acknowledged.

Posted on March 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stat: 125,000+. That’s how many high-income people the IRS is targeting for not filing their taxes. The IRS started sending letters last week to folks with over $400,000 in income who haven’t filed between 2017 and 2022 (Journal of Accountancy)

The S&P 500 index fell 6.13 points (0.1%) to 5,130.95; the Dow Jones Industrial Average lost 97.55 points (0.3%) to 38,989.83; the NASDAQ Composite declined 67.43 points (0.4%) to 16,207.51.

The 10-year Treasury note yield (TNX) rose about 4 basis points to 4.219%.

The CBOE Volatility Index® (VIX) increased 0.38 to 13.49.

Ongoing strength in chip makers propelled a 1.1% advance in the Philadelphia Semiconductor Index (SOX), which posted a record high for the third-straight trading day. Banks were also among the strongest performers. Small-cap shares eased, with the Russell 2000® Index (RUT) ending with a marginal loss after rising earlier to a two-year high.

As fellow doctors, we understand better than most the more complex financial challenges physicians can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

And you may be misled by unscrupulous “advisors”.

For example:

Question: Do you know the difference between a “Fee-Only” and a “Fee-Based financial advisor? Not knowing may cost you tens of thousands of dollars, or more, in excessive advisory fees.

Posted on March 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

RETIREMENT PLANNING

By Staff Reporters

***

***

A PEP is a defined contribution plan, such as a 401(k), in which multiple employers can participate. When employers join a PEP, they delegate their named fiduciary role to a third-party pooled plan provider (PPP). PEP fiduciary oversight falls on the PPP rather than the employer. And although each PPP may set its own eligibility requirements, businesses joining a PEP benefit plan needn’t operate in the same industry or geographical area.

PEP plans provide viable 401(k) alternatives for small business owners who may otherwise struggle to compete for talent against large organizations with comprehensive benefits packages.

Other advantages include: Less in-house administration: The PPP assumes responsibility for much of the plan administration, handling all plan documentation, governmental filings and ongoing compliance. Employee payroll deductions are left to the employer, but these can be efficiently managed with the help of a payroll service provider that integrates payroll and benefits.

Tax credits can help offset PEP start-up costs. For the first three years of participation, employers may be eligible for a tax credit of $5,000 annually, with an additional $500 available to those who set up automatic enrollment. Under Secure Act 2.0, an additional credit of up to $1,000 per employee for eligible employer contributions may apply to employers with up to 50 employees for the preceding taxable year. This credit phases out from 51 to 100 employees.

Businesses participating in single-employer retirement plans (SEP) must independently communicate and coordinate with their record-keeper, custodian, investment advisor, trustee and auditor. With PEP, all these tasks and services are bundled into one, saving employers time and money.

Despite its advantages, a PEP does have some drawbacks, particularly when compared to an SEP. Unlike a PEP, an SEP gives employers more of the following:

Flexibility: Employers can customize the design of their plan to meet their retirement goals and the needs of their employees.

Control: Employers are not dependent on the actions or decisions of others and can access information and resolve problems directly without the need of a third party.

Choice: Employers have the unilateral freedom to choose a different service provider, move their plan or negotiate better pricing if they are unsatisfied with the cost or quality of service.

Posted on February 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Pay for Performance Initiatives

[By Staff Writers]

Of course, consumer directed healthcare trends and fee transparency increasingly mandate physician economic accountability, such as in the P4P initiatives, but CMS may also begin profiling physicians and targeting those it deems inefficient sometime next year, as well.

In May 2007, Herbert Kuhn, acting deputy administrator of CMS, told a House subcommittee that the agency will have the data and computer capacity available to do tracking as soon as mid-2008.

To monitor efficiency, CMS would compare levels of tests physicians order for certain types of patients to tests ordered by other doctors who achieve similar outcomes. The agency would then contact the physicians whose testing patterns seem to be out of line. No doubt, the effects on private pay-for-performance [P4P] initiatives is obvious. Kuhn told the subcommittee that his largest concern was figuring out how to use the data to help physicians grow more efficient.

Assessment

To date, the agency hasn’t established plans to link efficiency measures with reimbursement changes. If it wants to do so, Congress would probably have to enact new legislation, according to several policymakers.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on February 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

OBTUSE METER?

By Staff Reporters

***

What is Delta?

FINANCE: Delta is a risk sensitivity measure used in assessing derivatives. It is one of the many measures that are denoted by a Greek letter. The series of risk measures that use such letters are fittingly referred to as the Greeks. They are often also called risk measures, hedge parameters, or risk sensitivities.

ACCOUNTING: Delta is the ratio of the change in price of an option to the change in price of the underlying asset. Also called the hedge ratio; For a call option on a stock, a delta of 0.50 means that for every $1.00 that the stock goes up, the option price rises by $0.50.

Posted on February 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

You can’t stop Nvidia and AI? The tech stock continued its post-earnings explosion yesterday, skyrocketing 16% and taking the entire stock market along with it. All three major indexes increased, with the S&P 500 notching another record high, as investors rode the surging waves.

***

***

Nvidia’s Q4 and full-year 2023 earnings smashed records, all but ensuring AI hype will continue for the foreseeable future. The chipmaker reported Q4 revenue of $22.1 billion, up 265% from Q4 2022, and a diluted EPS of $4.93, up 33% from last quarter and a whopping 765% from this time last year. (And, no, Lyft, those aren’t typos.)

“Accelerated computing and generative AI have hit the tipping point,” Nvidia’s founder and CEO Jensen Huang crowed in a press release. “Demand is surging worldwide across companies, industries, and nations.”

Nvidia’s made itself inescapable merely by virtue of being so big. Last week, it became the nation’s third-largest company, reaching a market cap of $1.83 trillion. It’s driven about a third of the NASDAQ 100’s gains this past year, according to Fast Company. That being the case, Nvidia’s performance can serve as a litmus test for the stock market itself.

Posted on February 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Big tech companies are continuing to pour cash into artificial intelligence at a breakneck pace. And based Bion the earnings update Wednesday from Nvidia, much of it is going to that chip maker. “This last year, we’ve seen generative AI really becoming a whole new application space, a whole new way of doing computing,” Jensen Huang, Nvidia’s co-founder and chief executive, said Wednesday. “A whole new industry is being formed, and that’s driving our growth.”

Pharmacies across the country are reporting delays to prescription orders due to a cyberattack against one of the nation’s largest health-care technology companies. Change Healthcare, a company handling orders and patient payments throughout the U.S., first noticed the “cyber security issue” affecting its networks Wednesday morning on the East Coast.

Here’s where the major benchmarks ended:

The S&P 500 index rose 105.23 points (2.1%) to 5,087.03; the Dow Jones Industrial Average gained 456.87 points (1.2%) to 39,069.11; the NASDAQ Composite rallied 460.75 points (3%) to 16,041.62.

The 10-year Treasury note yield (TNX) was little changed at 4.323%.

The CBOE Volatility Index® (VIX) fell 0.84 to 14.50.

Nvidia sparked a 5% rally in the Philadelphia Semiconductor Index (SOX) and a 3% gain in the NASDQ-100®(NDX), both of which ended at all-time highs. Consumer discretionary shares were also among the strongest sectors Thursday. The small-cap Russell 2000® Index (RUT) rose 1% and halted a three-day slide.

According to Joe Mazzola, director of trading and education at Schwab, Nvidia had a “profound effect” at both the sector and index level, partly reflecting its market value, which is nearing $2 trillion. Nvidia is now the third largest company behind Microsoft (MSFT) and Apple (AAPL).

Managed care insurers have profited handsomely from Medicare Advantage plans, scoring billions in annual profits. They credit this financial wizardry to their use of sophisticated data analytics, preventative care, cost optimization, provider networks, evidence and value-based care and risk mitigation strategies. However, doctors, hospitals, and medical providers assert something else.

In fact, Medicare Advantage plans have been making headlines in 2024, but not in a positive light, at least for health insurance companies. Medicare is a government-sponsored health insurance benefit; generally for retired people aged 65 and older.

For most, the money for Medicare Part B medical insurance or Part C Medicare Advantage plans is withdrawn directly from Social Security benefits monthly, coupled with a relatively small monthly payment from the patient. Nearly half of the Medicare population is enrolled in Part C Medicare Advantage plans.

***

***

However, there have been rumblings in the medical sector between medical providers and medical insurers coming to a head. So, where do you stand?

The giant accounting firm Grant Thornton LLP is laying off 200 people, its second round of layoffs in the past six months and an indication that the major players in the professional consulting, accounting and advisory business are preparing for an economic slowdown that could squeeze profits across corporate America.

***

Statistics: 7.4%. That’s the percentage drop in students who graduated with a degree in accounting in the 2021–2022 school year than the year before. Low starting salaries, heavy workloads, and uncertainty around AI are driving the exodus of students from choosing accounting degrees. (the Wall Street Journal).

Informational essays of most current interest to healthcare professionals. Check back periodically for practical updates. Our catalogue library of major books, texts, case models and dictionaries is suggested for additional financial, economic, business and medical practice management information and education.

Posted on February 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Get ’em … While They are Hot!

By Ann Miller RN MHA

[ME-P Executive Director]

Just click on the book icon to order; get any one or all three! You’ll be glad you did.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Running a business involves a constant learning curve. And that applies whether you’re a rookie entrepreneur just starting out with a great idea for a new business or a more established small business owner with a quickly growing business that needs to expand. You should always be learning as a business owner, no matter where you are in your career—there’s always a new tool to master, new problems to solve, and new vocabulary to understand.

In order to not get totally overwhelmed, it’s helpful to take things one segment at a time. For instance, feeling confident when discussing the business’s financial needs should be a priority for every small business owner. After all, you represent the heart and soul of your business in the marketplace. So knowing the “language” of business finance is an integral part of your job as the owner.

The good news is that you don’t have to be an accountant or a financial planner to negotiate in the world of business finance. Here are some business terms and finance terms that will help you find your way to successful small business funding. https://www.youtube.com/embed/0kD4X2fgxGs

Business and Finance Terms to Know

From accounting, to business loans, to general business financial operations, here’s the ultimate list to all the business finance terms and definitions you need to know:

1. Accounts Payable

Accounts payable is a business finance 101 term. This represents your small business’s obligations to pay debts owed to lenders, suppliers, and creditors. Sometimes referred to as A/P or AP for short, accounts payable can be short or long term depending upon the type of credit provided to the business by the lender.

2. Accounts Receivable

Also known as A/R (or AR, good guess), accounts receivables is another business finance 101 term that means the money owed to your small business by others for goods or services rendered. These accounts are labeled as assets because they represent a legal obligation for the customer to pay you cash for their short-term debt.

3. Accrual Basis

The accrual basis of accounting is an accounting method of recording income when it’s actually earned and expenses when they actually occur. Accrual basis accounting is the most common approach used by larger businesses to record and maintain financial transactions.

4. Accruals

A business finance term and definition referring to expenses that have been incurred but haven’t yet been recorded in the business books. Wages and payroll taxes are common examples.

5. Asset

This business finance key term is anything that has value—whether tangible or intangible—and is owned by the business is considered an asset. Typical items listed as business assets are cash on hand, accounts receivable, buildings, equipment, inventory, and anything else that can be turned into cash.

6. Balance Sheet

Along with three other reports relating to the financial health of your small business, the balance sheet is essential information that gives a “snapshot” of the company’s net worth at any given time. The report is a summary of the business assets and liabilities.

7. Bookkeeping

A method of accounting that involves the timely recording of all financial transactions for the business.

8. Capital

Refers to the overall wealth of a business as demonstrated by its cash accounts, assets, and investments. Often called “fixed capital,” it refers to the long-term worth of the business. Capital can be tangible, like durable goods, buildings, and equipment, or intangible such as intellectual property.

9. Working Capital

Not to be confused with fixed capital, working capital is another business finance 101 term. It consists of the financial resources necessary for maintaining the day-to-day operation of the business. Working capital, by definition, is the business’s cash on hand or instruments that you can convert to cash quickly.

10. Cash Flow

Every business needs cash to operate. The business finance term and definition cash flow refers to the amount of operating cash that “flows” through the business and affects the business’s liquidity. Cash flow reports reflect activity for a specified period of time, usually one accounting period or one month. Maintaining tight control of cash flow is especially important if your small business is new, since ready cash can be limited until the business begins to grow and produce more working capital.

11. Cash Flow Projections

Future business decisions will depend on your educated cash flow projections. To plan ahead for upcoming expenditures and working capital, you need to depend on previous cash flow patterns. These patterns will give you a comprehensive look at how and when you receive and spend your cash. This info is the key to unlock informed, accurate cash flow projections.

12. Depreciation

The value of any asset can be said to depreciate when it loses some of that value in increments over time. Depreciation occurs due to wear and tear. Various methods of depreciation are used by businesses to decrease the recorded value of assets.

13. Fixed Asset

A tangible, long-term asset used for the business and not expected to be sold or otherwise converted into cash during the current or upcoming fiscal year is called a fixed asset. Fixed assets are items like furniture, computer equipment, equipment, and real estate.

14. Gross Profit

This business finance term and definition can be calculated as total sales (income) less the costs (expenses) directly related to those sales. Raw materials, manufacturing expenses, labor costs, marketing, and transportation of goods are all included in expenses.

15. Income Statement

Here is one of the four most important reports lenders and investors want to see when evaluating the viability of your small business. It is also called a profit and loss statement, and it addresses the business’s bottom line, reporting how much the business has earned and spent over a given period of time. The result will be either a net gain or a net loss.

16. Intangible Asset

A business asset that is non-physical is considered intangible. These assets can be items like patents, goodwill, and intellectual property.

17. Liability

This business finance key term is a legal obligation to repay or otherwise settle a debt. Liabilities are considered either current (payable within one year or less) or long-term (payable after one year) and are listed on a business’s balance sheet. A business’s accounts payable, wages, taxes, and accrued expenses are all considered liabilities.

18. Liquidity

Liquidity is an indicator of how quickly an asset can be turned into cash for full market value. The more liquid your assets, the more financial flexibility you have.

19. Profit & Loss Statement

See “Income Statement” above.

20. Statement of Cash Flow

One of the important documents required by lenders and investors that shows a summary of the actual collection of revenue and payment of expenses for your business. The statement of cash flow should reflect activity in the areas of operating, investing, and financing and should be an integral part of your financial statement package.

21. Statement of Shareholders’ Equity

If you have chosen to fund your small business with equity financing and you have established shares and shareholders as part of the controlling interests, you are obligated to provide a financial report that shows changes in the equity section of your balance sheet.

22. Annual Percentage Rate

The business finance term and definition APR represents the yearly real cost of a loan including all interest and fees. The total amount of interest to be paid is based on the original amount loaned, or the principal, and is represented in percentage form. When shopping for the right loan for your small business, you should know the APR for the loan in question. This figure can be very helpful in comparing one financial tool with another since it represents the actual cost of borrowing.

23. Appraisal

Just like your real estate appraisal when buying a house, an appraisal is a professional opinion of market value. When closing a loan for your small business, you will probably need one or more of the three types of appraisals: real estate, equipment, and business value.

24. Balloon Loan

A loan that is structured so that the small business owner makes regular repayments on a predetermined schedule and one much larger payment, or balloon payment, at the end. These can be attractive to new businesses because the payments are smaller at the outset when the business is more likely to be facing strict financial constraints. However, be sure that your business will be capable of making that last balloon payment since it will be a large one.

25. Bankruptcy

This federal law is used as a tool for businesses or individuals who are having severe financial challenges. It provides a plan for reduction and repayment of debts over time or an opportunity to completely eliminate the majority of the outstanding debts. Turning to bankruptcy should be given careful thought because it will have a negative effect on the business credit score.

26. Bootstrapping

Using your own money to finance the start-up and growth of your small business. Think of it as being your own investor. Once the business is up and running successfully, the business finance term and definition bootstrapping refers to the use of profits earned to reinvest in the business.

27. Business Credit Report

Just like you have a personal credit report that lenders look at to determine risk factors for making personal loans, businesses also generate credit reports. These are maintained by credit bureaus that record information about a business’s financial history.

Items like how large the company is, how long has it been in business, amount and type of credit issued to the business, how credit has been managed, and any legal filings (i.e., bankruptcy) are all questions addressed by the business credit report. Lenders, investors, and insurance companies use these reports to evaluate risk exposure and financial health of a business.

28. Business Credit Score

A business credit score is calculated based on the information found in the business credit report. Using a specialized algorithm, business credit scoring companies take into account all the information found on your credit report and give your small business a credit score. Also called a commercial credit score, this number is used by various lenders and suppliers to evaluate your creditworthiness.

29. Collateral

Any asset that you pledge as security for a loan instrument is called collateral. Lenders often require collateral as a way to make sure they won’t lose money if your business defaults on the loan. When you pledge an asset for collateral, it becomes subject to seizure by the lender if you fail to meet the requirements of the loan documents.

30. Credit Limit

When a lender offers a business line of credit it usually comes with a credit limit, or a maximum amount that you can use at any given time. It is said that you reach your credit limit or “max out” your credit when you borrow up to or exceed that number. A business line of credit can be especially useful if your business is seasonal or if the income is extremely unpredictable. It is one of the fastest ways to access cash for emergencies.

31. Debt Consolidation

If your small business has several loans with various payments, you might want to consider a business debt consolidation loan. It is a process that lets you combine multiple loans into a single loan. The advantages are possibly reducing the interest rates on the borrowed funds as well as lowering the total amount you repay each month. Businesses use this tool to help improve cash flow.

32. Debt Service Coverage Ratio

The business finance term and definition debt service coverage ratio (DSCR) is the ratio of cash your small business has available for paying or servicing its debt. Debt payments include making principal and interest payments on the loan you are requesting. Generally speaking, if your DSCR is above 1, your business has enough income to meet its debt requirements.

33. Debt Financing

When you borrow money from a lender and agree to repay the principal with interest in regular payments for a specified period of time, you’re using debt financing. Traditionally, it has been the most common form of funding for small businesses.

Debt financing can include borrowing from banks, business credit cards, lines of credit, personal loans, merchant cash advances, and invoice financing. This method creates a debt that must be repaid but lets you maintain sole control of your business.

34. Equity Financing

The act of using investor funds in exchange for a piece or ”share” of your business is another way to raise capital. These funds can come from friends, family, angel investors, or venture capitalists.

Before deciding to use equity financing to raise the cash necessary for your business, decide how much control you are willing to share when it comes to decision-making and philosophy. Some investors will also want voting rights.

35. FICO Score

A FICO score is another type of credit score used by potential lenders for evaluating the wisdom of entering a contract with you and your business. FICO scores comprise a substantial part of the credit report that lenders use to assess credit risk. It was created by the Fair Isaac Corporation, hence the name FICO.

36. Financial Statements

An integral part of the loan application process is furnishing information that shows your business is a good credit risk. The standard financial statement packet includes four main reports: the income statement, the balance sheet, the statement of cash flow, and the statement of shareholders’ equity, if you have shareholders.

Lenders and investors want to see that your business is well-balanced with assets and liabilities, has positive cash flow, and will have capital to make expected repayments.

37. Fixed Interest Rate

The interest rate on a loan that is established in the beginning and does not change for the lifetime of the loan is said to be fixed. Loans with fixed interest rates are appealing to small business owners because the repayment amounts are consistent and easier to budget for in the future.

38. Floating Interest Rate

In contrast to the business finance term and definition fixed rate, the floating interest rate will change with market fluctuations. Also referred to as variable rates or adjustable rates, these amounts may often start out lower than the fixed rate percentages. This makes them more appealing in the short term if the market is trending down.

39. Guarantor

When starting a new small business, lenders might want you to provide a guarantor. This is an individual who guarantees to cover the balance owed on a debt if you or your business cannot meet the repayment obligation.

40. Interest Rate

All loans and other lending instruments are assigned the business finance key term interest rates. This is a percentage of the principal amount charged by the lender for the use of its money. Interest rates represent the current cost of borrowing.

41. Invoice Factoring or Financing

If your business has a significant amount of open invoices outstanding, you may contact a factoring company and have them purchase the invoices at a discount. By raising capital this way, there is no debt, and the factoring company assumes the financial responsibility for collecting the invoice debts.

42. Lien

This business finance term and definition is a creditor’s legal claim to the collateral pledged as security for a loan is called a lien.

43. Line of Credit

A lender may offer you an unsecured amount of funds available for your business to draw on when capital is needed. This line of credit is considered a short-term funding option, with a maximum amount available. This pre-approved pool of money is appealing because it gives you quick access to the cash.

44. Loan-to-Value

The LTV comparison is a ratio of the fair-market value of an asset compared to the amount of the loan that will fund it. This is another important number for lenders who need to know if the value of the asset will cover the loan repayment if your business defaults and fails to pay.

45. Long-Term Debt

Any loan product with a total repayment schedule lasting longer than one year is considered a long-term debt.

46. Merchant Cash Advance