A “Need-to-Know” Glossary for all Medical Professionals

http://www.HealthDictionarySeries.org

[ME-P Staff Writers]

ADV: A two-part form filed by investment advisors who register with the Securities and Exchange Commission (SEC), as required under the Investment Advisers Act. ADV Part II information must be provided to potential investors and made available to current investors.

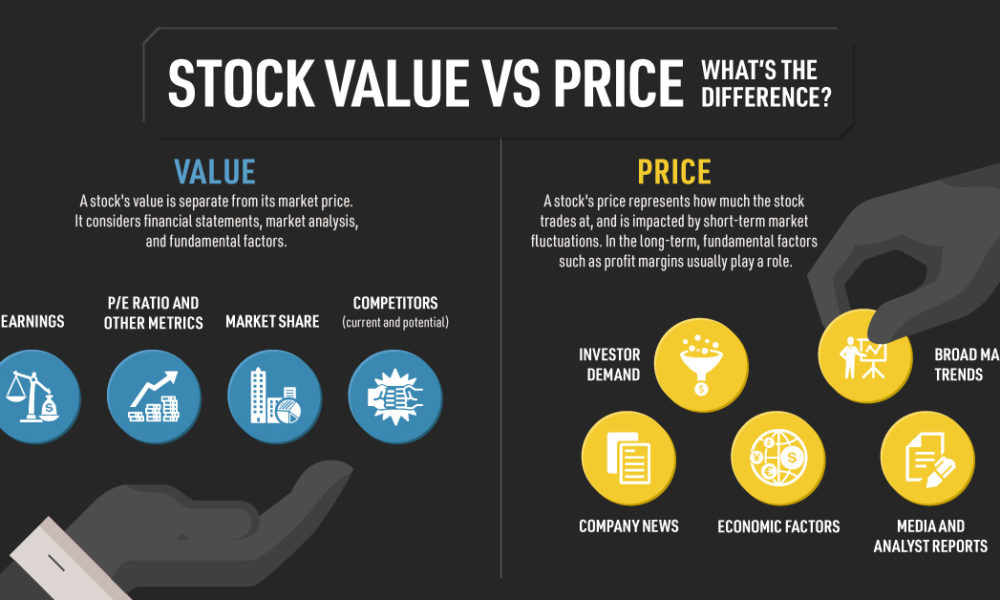

Alpha: A measure of the amount of a portfolio’s expected return that is not related to the portfolio’s sensitivity to market volatility. A benchmark that uses beta as a measure of risk, a benchmark and a risk free rate of return (usually T-bills) to compare actual performance with expected performance.

For example, a fund with a beta of .80 in a market that rises 10% is expected to rise 8%.

If the risk-free return is 3%, the alpha would be –.6%, calculated as follows: (Fund return – Risk-free return) – (Beta x Excess return) = Alpha (8% – 3%) – [.8 × (10% – 3%)] = (–) .6%

Note: A positive alpha indicates out-performance while a negative alpha means underperformance.

Asset allocation: Strategic asset allocation refers to the long-term targets for allocation of a percentage of a portfolio among different asset classes. In contrast, tactical asset allocation refers to short-term targets.

Average maturity: The average weighted maturity of the bonds in a portfolio providing an indication of interest rate risk.

Benchmark: An index, managed portfolio, or fund used to compare performance characteristics with the targeted portfolio or fund.

Beta: A statistically computed measure of the portfolio’s relationship to changes in market value. If, compared to the S&P 500, a fund has a beta of .80; it is expected to underperform a rising market by 20% and outperform a falling market by 20%.

Bond: Publicly traded debt instruments that are issued by governments and corporations. The issuer agrees to pay a fixed amount of interest over a specified time period and to repay the principal at maturity.

Closed-end mutual fund: An investment company that registers shares in accordance with SEC regulations and is traded in securities markets at prices determined by investments.

Diversification: Buying a number of different investment vehicles to protect against default of a single vehicle, thereby reducing the risk of the portfolio.

Duration: A more technical calculation of interest rate risk exposure that uses the present value of expected cash flows to be returned to the bond holder over the term of the bond.

Fundamental analysis: An analysis of a company’s stock that focuses on the economic environment, the industry the company is in, and the company’s financial situation and operating results.

Mutual fund: A regulated investment company that manages a portfolio of securities for its shareholders.

Net asset value (NAV): The value of fund assets fewer liabilities divided by outstanding shares.

Open-end mutual fund: An investment company that invests money in accordance with specific objectives on behalf of investors. Fund assets expand or contract based on investment performance, new investments and redemptions.

Portfolio manager: The person(s) who is/are responsible for managing the portfolio in accordance with the objectives dictated by an investor or a fund’s prospectus.

Prospectus: A disclosure document filed with the SEC and made available to prospective and current investors. The prospectus covers sales charges, expenses, investment objectives and restrictions, management fees, financial highlights, and other information.

R-squared (R2): Relationship of a fund or portfolio’s performance to a benchmark index.

For example, a fund R-squared of .5 means only 50% of its return is explained by the index. Other factors are responsible for the balance of performance.

SEC yield: A standardized calculation of yield over a 30-day period, sometimes quoted as the “30-day yield.” It takes into account yield-to-maturity rather than current dividends.

Standard deviation: A statistic that looks at a series of returns and expresses the average deviation from the mean return.

Statement of additional information: A disclosure document filed with the SEC that supplements the prospectus. It is made available to investors upon request.

Technical analysis: An analysis that focuses on trends in financial markets generally.

For example, a technical analyst may view an entire industry’s group of stocks to be declining. Although the analyst may be correct about the group of stocks as a whole, there may be exceptions represented by specific, individual companies.

Total return: The combination of investment return from income, such as dividends and interest, and appreciation or depreciation in the value of the investment (Income returns plus capital return.)

Turnover: Under SEC rules, a figure computed that indicates how often securities in the portfolio are bought and sold. For example, if turnover is 100% over a one-year period, the securities (on average) were replaced once.

12b-1 fee: The maximum annual fee payable from fund assets for distribution and sales costs as allowed by the SEC.

MORE: Glossary Terms Ap 3

https://www.amazon.com/Comprehensive-Financial-Planning-Strategies-Advisors/dp/1482240289/ref=sr_1_1?ie=UTF8&qid=1418580820&sr=8-1&keywords=david+marcinko

Filed under: Glossary Terms, Investing | Leave a comment »