BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Required Minimum Distributions (RMDs) are mandatory withdrawals from certain retirement accounts that begin at age 73, designed to ensure the IRS collects taxes on previously tax-deferred savings.

Required Minimum Distributions (RMDs) are a critical component of retirement planning in the United States. They represent the minimum amount that retirees must withdraw annually from specific tax-deferred retirement accounts, such as traditional IRAs, 401(k)s, and other qualified plans, once they reach a certain age. As of 2025, individuals must begin taking RMDs at age 73, a change implemented by the SECURE 2.0 Act for those born between 1951 and 1959.

The rationale behind RMDs is rooted in tax policy. Contributions to tax-deferred accounts are made with pre-tax dollars, allowing investments to grow without immediate tax consequences. However, the IRS eventually wants its share. RMDs ensure that retirees begin paying taxes on these funds, preventing indefinite tax deferral. The amount of each RMD is calculated using the account balance at the end of the previous year and a life expectancy factor provided by IRS tables.

Failing to take an RMD can result in steep penalties. Historically, the penalty was 50% of the amount not withdrawn, but recent changes have reduced this to 25%, and potentially 10% if corrected promptly. These penalties underscore the importance of understanding and complying with RMD rules.

Not all retirement accounts are subject to RMDs. Roth IRAs are exempt during the original account holder’s lifetime, and under the SECURE 2.0 Act, Roth 401(k) and Roth 403(b) accounts are also exempt from RMDs while the original owner is alive. However, beneficiaries of these accounts may still face RMD requirements.

***

***

Strategically managing RMDs can help retirees minimize tax impacts and optimize their retirement income. For example, retirees might consider withdrawing more than the minimum in years with lower income to reduce future RMD amounts. Others may choose to convert traditional IRA funds to Roth IRAs before reaching RMD age, thereby reducing future taxable distributions. Additionally, using RMDs to fund charitable donations through Qualified Charitable Distributions (QCDs) can satisfy the RMD requirement while excluding the amount from taxable income.

Timing is also crucial. The first RMD must be taken by April 1 of the year following the year the individual turns 73. Subsequent RMDs must be taken by December 31 each year. Delaying the first RMD can result in two withdrawals in one year, potentially increasing taxable income and affecting Medicare premiums or tax brackets.

In conclusion, RMDs are more than just a tax obligation—they are a planning opportunity. Understanding the rules, calculating the correct amount, and integrating RMDs into a broader retirement strategy can help retirees maintain financial stability and reduce unnecessary tax burdens.

As regulations evolve, staying informed and consulting with financial professionals is essential to make the most of retirement savings.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Retirement planning has evolved significantly over the past several decades, with employers and employees seeking solutions that balance security, flexibility, and predictability. Among the various retirement plan options available today, cash balance plans stand out as a hybrid design that combines features of both traditional defined benefit pensions and defined contribution plans. Their unique structure makes them an attractive choice for employers aiming to provide meaningful retirement benefits while maintaining financial predictability.

At their core, cash balance plans are a type of defined benefit plan. Unlike traditional pensions, which promise retirees a monthly income based on years of service and final salary, cash balance plans define the benefit in terms of a hypothetical account balance. Each participant’s account grows annually through two components: a “pay credit” and an “interest credit.” The pay credit is typically a percentage of the employee’s salary or a flat dollar amount, while the interest credit is either a fixed rate or tied to an index such as U.S. Treasury yields. Although the account is hypothetical—meaning the funds are not actually segregated for each employee—the structure provides participants with a clear, understandable statement of their retirement benefit.

One of the primary advantages of cash balance plans is their transparency. Employees can easily track the growth of their account balance, much like they would with a 401(k). This clarity helps workers better understand the value of their retirement benefits and fosters a sense of ownership. Additionally, cash balance plans are portable: when employees leave a company, they can roll over the vested balance into an IRA or another qualified plan, ensuring continuity in retirement savings.

***

***

From the employer’s perspective, cash balance plans offer several benefits as well. Traditional pensions often create unpredictable liabilities, as they depend on factors such as longevity and investment performance. Cash balance plans, by contrast, provide more predictable costs because the employer commits to specific pay and interest credits. This predictability makes them easier to manage and budget for, particularly in industries where workforce mobility is high. Moreover, cash balance plans can be designed to reward long-term employees while still appealing to younger workers who value portability.

Despite these advantages, cash balance plans are not without challenges. Because they are defined benefit plans, employers bear the investment risk and must ensure the plan is adequately funded. Regulatory requirements, including nondiscrimination testing and funding rules, add complexity and administrative costs. Additionally, while cash balance plans are generally more equitable across generations of workers, transitions from traditional pensions to cash balance designs have sometimes sparked controversy, particularly among older employees who may perceive a reduction in benefits.

In recent years, cash balance plans have gained popularity among professional firms, such as law practices and medical groups, as well as small businesses seeking tax-efficient retirement solutions. These plans allow owners and highly compensated employees to accumulate larger retirement savings than would be possible under defined contribution limits, while still providing benefits to rank-and-file workers. As such, they serve as a valuable tool for both talent retention and financial planning.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

After a lifetime of hard work practicing medicine and saving, you’re at the retirement finish line. Instead of a paycheck, you’re relying on your nest egg and investment income to cover the bills. Picking the right investments is even more important, as you won’t have much chance to recover as a retired MD, DO, DPM or DDS.

“You made it to the top of the mountain through a systematic approach and are trying to make your way down safely,” says retirement planner John Gillet John Gillet in Hollywood, Fla. “Why throw all caution to the wind and try something different now?”

***

***

Definitions

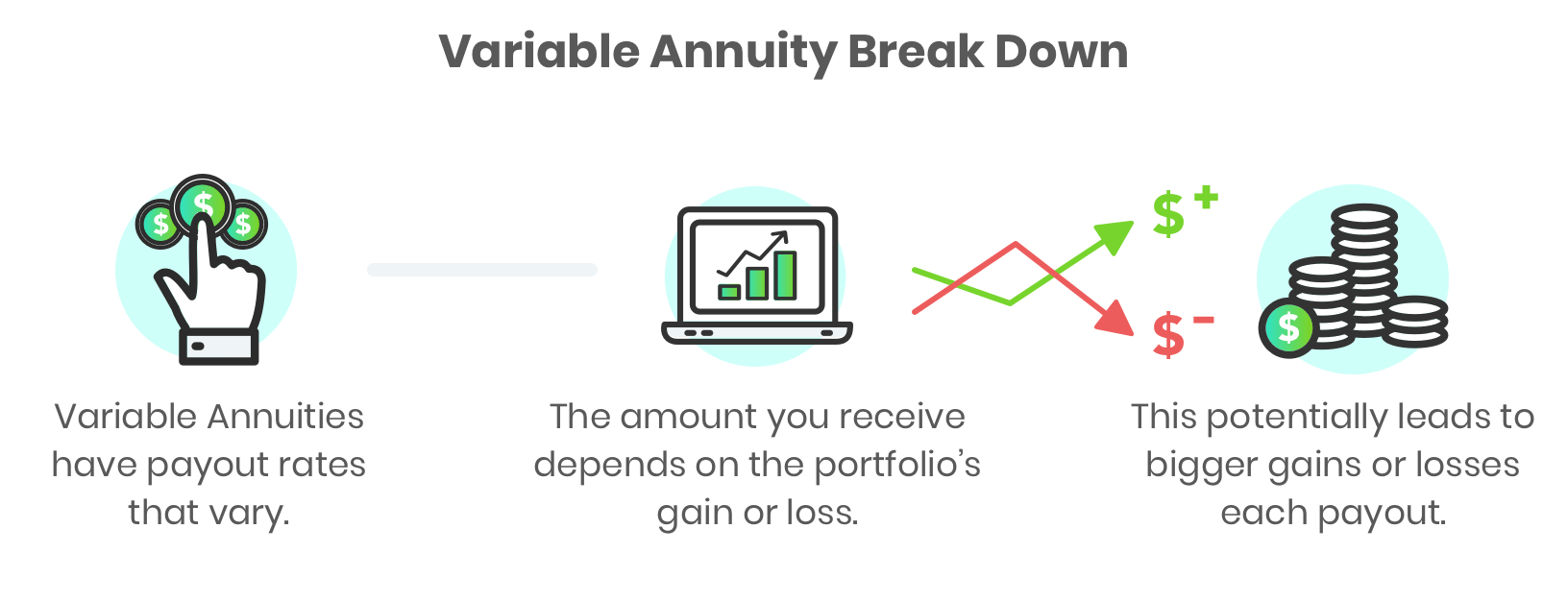

An annuity is an insurance contract designed to grow your money and then repay it as income. There are different versions. An immediate annuity turns your lump sum into future guaranteed income payments, like your own personal pension. They are simple to understand with no or small fees.

Fixed annuities pay a guaranteed interest rate over a set period to grow your money, like 5% a year for five years. These options could make sense as part of a retirement plan.

A variable annuity, on the other hand, invests your savings in mutual funds. While you can buy riders that guarantee a minimum income, you’ll be paying very much for it. “All in, the annual fees can be 3% or more of your balance,” says Jeff Bailey, an advisor from Nashville. “That’s a huge withdrawal rate from your portfolio versus investing on your own.”

The variable annuity will lock up your money for years. If you cancel early, you owe a surrender charge that could start at 7% or more of your annuity balance before gradually going down as time goes by. “Clients believe they can walk away with their contract value, but that’s often not true,” says Bailey.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Yourmedical practice. Your personal goals. Your financial plan. Our experienced confirmation guide.

***

***

When you know exactly where you are today, have a vision of where you want to be tomorrow, and have trusted counsel at your side, you have already achieved so much success. Marcinko Associates works to keep you at that level of confidence every day. We use a comprehensive economic process to uncover what’s most important to you and then develop a financial strategy that gives you the highest probability of achieving your monetary goals.

We assess, plan, and opine for your success

To accurately see where you are today, chart a strategic path to your goals and help you make the most informed decisions to keep you on financial track, our key services for physicians and high net worth medical clients include:

Investment Portfolio Review

Fee, Charge and Cost Review

Comprehensive Financial Planning

Insurance Reviews

Estate Planning

Investment and Asset Management Second Opinions

We take a deep dive into your financial retirement plans

Physicians and dental employers now have options for how to design and deliver retirement benefits and we can help you make the best choice for your healthcare business. Our services for retirement plans include:

Fee, Charges & Fiduciary Review

Portfolio Analysis

Single Employer Retirement Plan Advisory

Retirement Plans Risk Analysis

Capital Funding and Financing

Business Planning and Practice Valuations

Career Development

and more!

We take a broad and balanced look at your financial life life

We coordinate our recommendations with your other advisors, including attorneys, accountants, insurance professionals and others, to ensure each decision is consistent with your goals and overall strategy. For example, through our partnerships we offer physician colleagues deeper expanded advisory services, like:

There’s an aspect to retirement that many physicians do not plan for … the transition from work and practice to retirement. Your work has been an important part of your life. That’s why the emotional adjustments of retirement may be some of the most difficult ones.

For example, what would you like to do in retirement? Your retirement vision will be unique to you. You are retiring to something not from something that you envisioned. When you have more time, you would like to do more traveling, play golf or visit more often, family and friends. Would you relocate closer to your kids? Learn a new art or take a new class? Fund your grandchildren’s education? Do you have philanthropic goals? Perhaps you would like to help your church, school or favorite charity? If your net worth is above certain limits, it would be wise to take a serious look at these goals. With proper planning, there might be some tax benefits too. Then you have to figure how much each goal is going to cost you.

If you have a list of retirement goals, you need to prioritize which goal is most important. You can rate them on a scale of 1 to 10; 10 being the most important. Then, you can differentiate between wants and needs. Needs are things that are absolutely necessary for you to retire; while wants are things that still allow retirement but would just be nice to have.

Recent studies indicate there are three phases in retirement, each with a different spending pattern [Richard Greenberg CFP®, Gardena CA, personal communication]. The three phases are:

The Early Retirement Years. There is a pent-up demand to take advantage of all the free time retirement affords. You can travel to exotic places, buy an RV and explore forty-nine states, go on month-long sailing vacations. It’s possible during these years that after-tax expenses increase during these initial years, especially if the mortgage hasn’t been paid off yet. Usually the early years last about ten years until most retirees are in their 70’s.

Middle Years. People decide to slow down on the exploration. This is when people start simplifying their life. They may sell their house and downsize to a condo or townhouse. They may relocate to an area they discovered during their travels, or to an area close to family and friends, to an area with a warm climate or to an area with low or no state taxes. People also do their most important estate planning during these years. They are concerned about leaving a legacy, taking care of their children and grandchildren and fulfilling charitable intent. This a time when people spend more time in the local area. They may start taking extension or college classes. They spend more time volunteering at various non-profits and helping out older and less healthy retirees. People often spend less during these years. This period starts when a retiree is in his or her mid to late 70’s and can last up to 20 years, usually to mid to late-80’s.

Late Years. This is when you may need assistance in our daily activities. You may receive care at home, in a nursing home or an assisted care facility. Most of the care options are very expensive. It’s possible that these years might be more expensive than your pre-retirement expenses. This is especially true if both spouses need some sort of assisted care. This period usually starts when the retiree is their 80’s; however they can sometimes start in the middle to the late 70’s.

***

***

[A] Planning issues – early career

Most retirement lifestyle issues do not have to be addressed at this point. Keeping a healthy, balanced lifestyle will help to ensure a more productive retirement. This is the time to focus on the financial aspects of retirement planning.

[B] Planning issues – mid career

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement

[C] Planning issues – late career

Three to five years before you retire, start making the transition from work to retirement.

Try out different hobbies;

Find activities that will give you a purpose in retirement;

Establish friendships outside of the office or hospital;

Discuss retirement plans with your spouse.

If you plan to relocate to a new place, it is important to rent a place in that area and stay for few months and see if you like it. Making a drastic change like relocating and then finding you don’t like the new town or state might be very costly mistake. The key is to gradually make the transition.

For physicians, like most folks, retirement is the stage in life when one chooses to leave the workforce and live off sources of income or savings that do not require active work. The age at which a person retires, their lifestyle during retirement, and the way they fund that lifestyle, will vary from one person to the next, depending on individual preferences and financial planning. Usually it is age 65.

Some doctors may opt for early retirement to enjoy their hobbies and travel, while others may continue working part-time to stay engaged and supplement their income. Effective retirement planning often involves a combination of savings, investments, and possibly pension benefits to ensure a comfortable and secure post-work life.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial planning and investment decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just a few weeks ago.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Assessment

QUESTION: How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.” In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Yes, you can contribute to both a Roth IRA and a 401(k), provided you don’t exceed annual contribution limits for each account.

Determining whether to contribute to a Roth IRA, 401(k), or both can be an important step in planning for your retirement. Here are the key differences, including tax advantages, employer contributions, and investment options.

Eligibility requirements are the first consideration when contributing to a Roth IRA and a 401(k). For Roth IRA contributions, your eligibility is determined by your income. Specifically, if your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute to a Roth IRA may be reduced or eliminated. However, there are no income limits for contributing to a 401(k), making it accessible to anyone with earned income.

IRS rules do allow for contributions to both a Roth IRA and a 401(k), provided you adhere to the annual contribution limits for each account.

This means you can take advantage of the higher contribution limits of a 401(k) while also benefiting from the tax-free growth of a Roth IRA. This dual approach can be a strategy for maximizing your retirement savings. The advantages to contributing to both accounts present some key benefits, such as:

Tax diversification in retirement, allowing for better management of taxable income.

Potential reduction of overall tax burden.

Maximization of savings potential by taking full advantage of the benefits each account offers.3

Balancing contributions between a Roth IRA and a 401(k) requires careful planning. You might start by contributing enough to your 401(k) to receive the full employer match, which is essentially free money, if your employer offers this. Once you’ve secured the match, consider maxing out your Roth IRA contributions, if you’re eligible.

Life planning and behavioral finance as proposed for physicians and integrated by the Institute of Medical Business Advisors Inc., is unique in that it emanates from a holistic union of personal financial planning, human physiology and medical practice management, solely for the healthcare space. Unlike pure life planning, pure financial planning, or pure management theory, it is both a quantitative and qualitative “hard and soft” science, with an ambitious economic, psychological and managerial niche value proposition never before proposed and codified, while still representing an evolving philosophy. Its’ first-mover practitioners are called Certified Medical Planners™.

Financial Life Planning is an approach to financial planning that places the history, transitions, goals, and principles of the client at the center of the planning process. For the financial advisor or planner, the life of the client becomes the axis around which financial planning develops and evolves.

Financial Life Planning is about coming to the right answers by asking the right questions. This involves broadening the conversation beyond investment selection and asset management to exploring life issues as they relate to money.

Financial Life Planning is a process that helps advisors move their practice from financial transaction thinking, to life transition thinking. The first step is aimed to help clients “see” the connection between their financial lives and the challenges and opportunities inherent in each life transition.

But, for informed physicians, life planning’s quasi-professional and informal approach to the largely isolate disciplines of financial planning and medical practice management is inadequate. Today’s practice environment is incredibly complex, as compressed economic stress from HMOs managed care, financial insecurity from insurance companies, ACOs and VBC, Washington DC and Wall Street; liability fears from attorneys, criminal scrutiny from government agencies, and IT mischief from malicious electronic medical record [eMR] hackers. And economic bench marking from hospital employers; lost confidence from patients; and the Patient Protection and Affordable Care Act [PP-ACA] more than a decade ago. All promote “burnout” and converge to inspire a robust new financial planning approach for physicians and most all medical professionals.

The iMBA Inc., approach to financial planning, as championed by the Certified Medical Planner™ professional certification designation program, integrates the traditional concepts of financial life planning, with the increasing complex business concepts of medical practice management. The former topics are presented in this textbook, the later in our recent companion text: The Business of Medical Practice [Transformational Health 2.0 Skills for Doctors].

***

***

For example, views of medical practice, personal lifestyle, investing and retirement, both what they are and how they may look in the future, are rapidly changing as the retail mentality of medicine is replaced with a wholesale and governmental philosophy. Or, how views on maximizing current practice income might be more profitably sacrificed for the potential of greater wealth upon eventual practice sale and disposition.

Or, how the ultimate fear represented by Yale University economist Robert J. Shiller, in The New Financial Order: Risk in the 21st Century, warns that the risk for choosing the wrong profession or specialty, might render physicians obsolete by technological changes, managed care systems or fiscally unsound demographics. OR, if a medical degree is even needed for future physicians?

Say, what medical license?

Dr. Shirley Svorny, chair of the economics department at California State University, Northridge, holds a PhD in economics from UCLA. She is an expert on the regulation of health care professionals who participated in health policy summits organized by Cato and the Texas Public Policy Foundation. She argues that medical licensure not only fails to protect patients from incompetent physicians, but, by raising barriers to entry, makes health care more expensive and less accessible. Institutional oversight and a sophisticated network of private accrediting and certification organizations, all motivated by the need to protect reputations and avoid legal liability, offer whatever consumer protections exist today.

Yet, the opportunity to revise the future at any age through personal re-engineering, exists for all of us, and allows a joint exploration of the meaning and purpose in life. To allow this deeper and more realistic approach, the informed transformation advisor and the doctor client, must build relationships based on trust, greater self-knowledge and true medical business management and personal financial planning acumen.

[A] The iMBA Philosophy

As you read this ME-P website, we hope you will embrace the opportunity to receive the focused and best thinking of some very smart people. Hopefully, along the way you will self-saturate with concrete information that proves valuable in your own medical practice and personal money journey. Maybe, you will even learn something that is so valuable and so powerful, that future reflection will reveal it to be of critical importance to your life. The contributing authors certainly hope so.

At the Institute of Medical Business Advisors, and thru the Certified Medical Planner™ program, we suggest that such an epiphany can be realized only if you have extraordinary clarity regarding your personal, economic and [financial advisory or medical] practice goals, your money, and your relationship with it. Money is, after only, no more or less than what we make of it.

Ultimately, your relationship with it, and to others, is the most important component of how well it will serve you.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

An annuity is a contract between you and an insurance company. When you purchase an annuity, you make a lump-sum contribution or a series of contributions, generally each month. In return, the insurance company makes periodic payments to you beginning immediately or at a pre-determined date in the future. These periodic payments may last for a finite period, such as 20 years, or an indefinite period, such as until both you and your spouse are deceased. Annuities may also include a death benefit that will pay your beneficiary a specified minimum amount, such as the total amount of your contributions.

The growth of earnings in your annuity is typically tax-deferred; this could be beneficial as you may be in a lower tax bracket when you begin taking distributions from the annuity.

Warning: A word of caution: Annuities are intended as long-term investments. If you withdraw your money early from an annuity, you may pay substantial surrender charges to the insurance company as well as tax penalties to the IRS and state.

***

***

There are three basic types of annuities — fixed, indexed, and variable

1. With a fixed annuity, the insurance company agrees to pay you no less than a specified (fixed) rate of interest during the time that your account is growing. The insurance company also agrees that the periodic payments will be a specified (fixed) amount per dollar in your account.

2. With an indexed annuity, your return is based on changes in an index, such as the S&P. Indexed annuity contracts also state that the contract value will be no less than a specified minimum, regardless of index performance.

3. A variable annuity allows you to choose from among a range of different investment options, typically mutual funds. The rate of return and the amount of the periodic payments you eventually receive will vary depending on the performance of the investment options you select.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Beneficiary designations can provide a relatively easy way to transfer an account or insurance policy upon your death. However, if you’re not careful, missing or outdated beneficiary designations can easily cause your estate plan to go awry.

Where you can find them

Here’s a sampling of where you’ll find beneficiary designations:

In several states, so-called “lady bird” deeds for real estate

***

***

10 tips about beneficiary designations

Because beneficiary designations are so important, keep these things in mind in your estate planning:

Remember to name beneficiaries. If you don’t name a beneficiary, one of the following could occur:

The account or policy may have to go through probate. This process often results in unnecessary delays, additional costs, and unfavorable income tax treatment.

The agreement that controls the account or policy may provide for “default” beneficiaries. This could be helpful, but it’s possible the default beneficiaries may not be whom you intended.

Name both primary and contingent beneficiaries. It’s a good practice to name a “back up” or contingent beneficiary in case the primary beneficiary dies before you. Depending on your situation, you may have only a primary beneficiary. In that case, consider whether it may make sense to name a charity (or charities) as the contingent beneficiary.

Update for life events. Review your beneficiary designations regularly and update them as needed based on major life events, such as births, deaths, marriages, and divorces.

Read the instructions. Beneficiary designation forms are not all alike. Don’t just fill in names — be sure to read the form carefully. If necessary, you can draft your own customized beneficiary designation, but you should do this only with the guidance of an experienced attorney or tax advisor.

Coordinate with your will and trust. Whenever you change your will or trust, be sure to talk with your attorney about your beneficiary designations. Because these designations operate independently of your other estate planning documents, it’s important to understand how the different parts of your plan work as a whole.

Think twice before naming individual beneficiaries for particular assets. For example, you may establish three accounts of equal value initially and name a different child as beneficiary of each account. Over the years, the accounts may grow or be depleted unevenly, so the three children end up receiving different amounts — which is not what you originally intended.

Avoid naming your estate as beneficiary. If you designate a beneficiary on your 401(k), for example, it won’t have to go through probate court to be distributed to the beneficiary. If you name your estate as beneficiary, the account will have to go through probate. For IRAs and qualified retirement plans, there may also be unfavorable income tax consequences.

Use caution when naming a trust as beneficiary. Consult your attorney or CPA before naming a trust as beneficiary for IRAs, qualified retirement plans, or annuities. There are situations where it makes sense to name a trust — for example if:

Your beneficiaries are minor children

You’re in a second marriage

You want to control access to funds

Be aware of tax consequences. Many assets that transfer by beneficiary designation come with special tax consequences. It’s helpful to work with an experienced tax advisor to help provide planning ideas for your particular situation.

Use disclaimers when necessary — but be careful. Sometimes a beneficiary may actually want to decline (disclaim) assets on which they’re designated as beneficiary. Keep in mind that disclaimers involve complex legal and tax issues and require careful consultation with your attorney and CPA.

An alternative investment is a financial asset that does not fall into one of the conventional investment categories. Conventional categories include stocks, bonds, and cash. Alternative investments can include private equity or venture capital, hedge funds, managed futures, art and antiques, commodities, and derivatives contracts. Real estate is also often classified as an alternative investment.

QUESTION: But what about a medical, podiatric or dental practice?

***

***

AnAlternate Asset Class Surrogate?

A medical practice is much like an alternative investment [AI], or alternate asset class in, two respects.

First, it provides the work environment that generates personal income which has been considered generous, to date.

Second, it has inherent appreciation and sales value that can be part of an exit (retirement) or succession planning transfer strategy.

Conclusion

So, unlike the emerging thought that offers Social Security payments as a surrogate for an asset classes; or a federally insured AAA bond – a medical practice might also be considered by some folks as an asset class within a well diversified modern investment portfolio.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

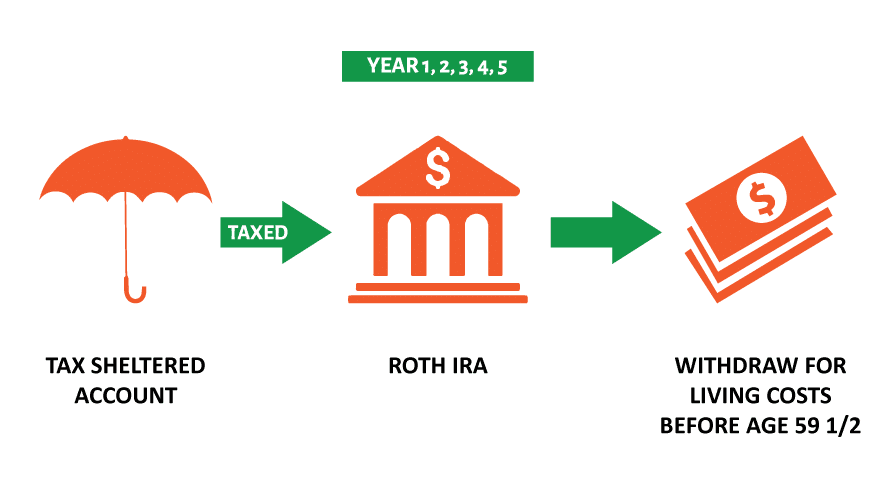

Why would a doctor consider a Roth IRA conversion?

By Staff Reporters

***

***

A Roth conversion involves transferring funds from a traditional retirement account—such as a 401(k), 403(b), or individual retirement account (IRA) funded with pre-tax dollars—into a Roth IRA.

The biggest benefit lies in the tax treatment of the converted funds. Once the funds are in the Roth IRA, future growth of those assets is tax-free. Withdrawals in retirement are also tax-free, assuming they meet certain criteria. As with any strategy, there are important considerations to keep in mind.

When you convert funds to a Roth IRA, the amount converted is taxable income in that tax year. For example, if you convert $100,000 from a traditional IRA to a Roth IRA, that $100,000 will be added to your taxable income in the conversion year.

Converting large amounts can result in a significant tax bill and may push you into a higher tax bracket. Even so, using retirement funds to pay taxes may make sense for those looking to convert large IRAs to reduce their future required minimum distributions (RMDs).

The timing of your Roth conversion matters too. Generally, it’s a good idea to convert when your income is lower—for example, after you’ve retired and before you begin drawing Social Security. You may also choose to convert over the course of several years to spread out the tax impacts. But if you can get comfortable with these considerations, a Roth conversion can provide you with benefits beyond tax-free growth and withdrawals.

Some of these benefits are:

Tax diversification. Having both traditional and Roth accounts allows you to manage your tax liability in retirement. For example, if your income in a given year is higher than expected, you can withdraw from the Roth IRA without increasing your taxable income.

No RMDs. Traditional IRAs and 401(k)s require you to begin taking RMDs at age 73. Roth IRAs have no RMD requirement during your lifetime. With a Roth account, you have more control over your retirement withdrawals and can leave the funds to grow for your heirs.

Benefits for heirs. Roth IRAs can be passed on to beneficiaries, who can inherit the account income tax-free. This means your heirs can enjoy the tax-free growth and withdrawals if the Roth IRA has been held for five years or more—a significant advantage, especially if your beneficiaries are in a higher tax bracket.

Posted on April 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA CPHQ CMP™

***

***

Finally … Fiduciary second investing and financial planning opinions right here!

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and financially personalized

Rendered by a pre-screened financial consultant for doctors and medical professionals

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-financial advisor telephone or e-mail portal that connects independent financial professionals to doctors, nurses or healthcare executives desiring affordable and unbiased financial planning advice.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Human Resources, Retirement Planning and Employee Benefits. To assist our medical professional and healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

QUESTION:Can I invest my Individual Retirement Account [IRA] in a Hedge Fund?

This is up to the manager, but there is no legal restriction on a hedge fund accepting individual retirement account (IRA) assets. IRA accounts are not well suited for funds that make extensive use of leverage, however. In such cases, the fund is likely to generate significant amounts of unrelated business taxable income (UBTI) – profits of the fund attributable to the use of leverage. The holder of an IRA account must pay taxes on UBTI, even if the UBTI was generated in an IRA account.

But, today’s hedge funds may or may not use leverage. Many hedge funds are not hedged at all, but rather are just specialized versions of regular long stock portfolios. If such funds do not use much leverage, IRA investors will not encounter much difficulty with UBTI and should not hesitate in considering these funds.

In considering whether to accept IRA money, hedge fund managers must consider several factors. If the only type of retirement money accepted by the hedge funds is IRA money, then the manager has no limit on how much retirement money the fund can accept. If, however, there are other types of retirement money invested in the fund, such as pension funds, IRA money will be counted towards a total of 25 percent of fund assets that can be invested in retirement accounts before the fund becomes subject to the Employment Retirement Income Security Act of 1974 (ERISA). Funds subject to ERISA regulations face a heavy administrative burden and more restrictions than most fund managers like.

Finally, IRA distributions from a hedge fund are subject to the standard 20 percent withholding unless the funds are directly rolled over to other qualified plans.

Merger risk arbitrage, while a subset of a larger strategy called event-driven arbitrage, represents a sufficient portion of the market-neutral universe to warrant separate discussion.

Merger arbitrage earned a bad reputation in the 1980s when Ivan Boesky and others like him came to regard insider trading as a valid investment strategy. That notwithstanding, merger arbitrage is a respected strategy and when executed properly, can be highly profitable. It bets on the outcomes of mergers, takeovers and other corporate events involving two stocks which may become one.

Example:

A classic example is acquisition of SDL Inc. (SDLI) by JDS Uniphase Corp (JDSU). On July 10, 2010 JDSU announced its intent to acquire SDLI by offering to exchange 3.8 shares of its own shares for one share of SDLI. At that time, the JDSU shares traded at $101 and SDLI at $320.5. It was apparent that there was almost 20 percent profit to be realized if the deal went through (3.8 JDSU shares at $101 are worth $383 while SDLI was worth just $320.5).

This apparent mispricing reflected the market’s expectation about the deal’s outcome. Since the deal was subject to the approval of the U.S. Justice Department and shareholders, there was some doubt about its successful completion.

Risk arbitrageurs who did their homework and properly estimated the probability of success bought shares of SDLI and simultaneously sold short shares of JDSU on a 3.8 to 1 ratio, thus locking in the future profit. Convergence took place about eight months later, in February 2011, when the deal was finally approved and the two stocks began trading at exact parity, eliminating the mis-pricing and allowing arbitrageurs to realize a profit.

***

***

Hedge Fund Research defines the strategy as follows:

Merger Arbitrage,also known as risk arbitrage, involves investing in securities of companies that are the subject of some form of extraordinary corporate transaction, including acquisition or merger proposals, exchange offers, cash tender offers and leveraged buy-outs. These transactions will generally involve the exchange of securities for cash, other securities or a combination of cash and other securities. Typically, a manager purchases the stock of a company being acquired or merging with another company, and sells short the stock of the acquiring company. A manager engaged in merger arbitrage transactions will derive profit (or loss) by realizing the price differential between the price of the securities purchased and the value ultimately realized when the deal is consummated. The success of this strategy usually is dependent upon the proposed merger, tender offer or exchange offer being consummated.

When a tender or exchange offer or a proposal for a merger is publicly announced, the offer price or the value of the securities of the acquiring company to be received is typically greater than the current market price of the securities of the target company. Normally, the stock of an acquisition target appreciates while the acquiring company’s stock decreases in value. If a manager determines that it is probable that the transaction will be consummated, it may purchase shares of the target company and in most instances, sell short the stock of the acquiring company. Managers may employ the use of equity options as a low-risk alternative to the outright purchase or sale of common stock. Many managers will hedge against market risk by purchasing S&P put options or put option spreads.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

Achieving your financial, wealth and medical practice management goals is important, but handling everything on your own can be overwhelming. That’s where we come in. At D. E. Marcinko & Associates, our team of dual degree experienced physician advisors and medical consultants is here to guide you every step of the way. We believe in providing unbiased, high-quality financial and business advice.

For example, we offer a one-time written financial plan with oral evaluation for a flat fee with no ongoing sales or assets under management fees or commissions. Together, we can create a personalized financial plan tailored to your unique goals, empowering you to make confident, informed decisions as you navigate your financial future.

Other Services Include:

Estate Planning We have a network of qualified legal professionals that we can refer you to for state specific estate planning needs.

Tax Strategy We can work alongside your CPA for tax planning purposes. If needed, we can refer you to a qualified tax professional.

Investment Analysis If you have investments, we review your accounts to make sure they are aligned with your long-term goals.

401-k Allocations We evaluate your 401(k) allocations and provide recommendations that align with your goals.

Education Savings We help you explore the various ways to plan and save for education expenses.

Insurance & Risk Management We assess your insurance coverage to ensure it adequately protects you against potential risks; as well as evaluate and provide expert litigation witnesses, as needed.

Medical Practice Management We evaluate your current or potential medical practice to determine value and/or private equity offers or physician practice management formats [PPMC] for new, mid-career or retiring physicians, nurses and dentists.

D. E. Marcinko & Associates is unique and fully committed to all phases of a medical professionals personal and business life cycle. We are at your service 24/7: Email MarcinkoAdvisors@outlook.com

With the PP-ACA, increased compliance regulations and higher tax rates impending from the Biden administration – not to mention the corona pandemic, venture capital based healthcare corporations and telehealth – physicians are more concerned about their retirement and retirement planning than ever before; and with good reason. After payroll taxes, dividend taxes, limited itemized deductions, the new 3.8% surtax on net investment income and an extra 0.9% Medicare tax, for every dollar earned by a high earning physician, almost 50 cents can go to taxes!

Introduction

Retirement planning is not about cherry picking the best stocks, ETFs or mutual funds or how to beat the short term fluctuations in the market. It’s a disciplined long term strategy based on scientific evidence and a prudent process. You increase the probability of success by following this process and monitoring on a regular basis to make sure you are on track.

General Surveys

According to a survey from the Employee Benefit Research Institute [EBRI] and Greenwald & Associates; nearly half of workers without a retirement plan were not at all confident in their financial security, compared to 11 percent for those who participated in a plan, according to the 2014 Retirement Confidence Survey (RCS).

In addition, 35 percent of workers have not saved any money for retirement, while only 57 percent are actively saving for retirement. Thirty-six percent of workers said the total value of their savings and investments—not including the value of their home and defined benefit plan—was less than $1,000, up from 29 percent in the 2013 survey. But, when adjusted for those without a formal retirement plan, 73 percent have saved less than $1,000.

Debt is also a concern, with 20 percent of workers saying they have a major problem with debt. Thirty-eight percent indicate they have a minor problem with debt. And, only 44 percent of workers said they or their spouse have tried to calculate how much money they’ll need to save for retirement. But, those who have done the calculation tend to save more.

The biggest shift in the 24 years has been the number of workers who plan to work later in life. In 1991, 84 percent of workers indicated they plan to retire by age 65, versus only 9 percent who planned to work until at least age 70. In 2014, 50 percent plan on retiring by age 65; with 22 percent planning to work until they reach 70.

Physician Statistics

Now, compare and contrast the above to these statistics according to a 2018 survey of physicians on financial preparedness by American Medical Association [AMA] Insurance. The statistics are still alarming:

The top personal financial concern for all physicians is having enough money to retire.

Only 6% of physicians consider themselves ahead of schedule in retirement preparedness.

Nearly half feel they were behind

41% of physicians average less than $500,000 in retirement savings.

Nearly 70% of physicians don’t have a long term care plan.

Only half of US physicians have a completed estate plan including an updated will and Medical directives.

Thoughts to Ponder

And so, to help make your golden years comfortable and worry free, here are ten important retirement questions for all physicians to consider:

How much money do you need to retire?

What is your retirement cash flow?

What is your retirement vision?

How to stay on retirement track?

How to maximize retirement plan contributions such as 401(k) or 403(b)?

How to maximize retirement income from retirement plans?

What are some other retirement plan savings options?

What is your retirement plan and investing style?

What is the role of social security in retirement planning?

How to integrate retirement with estate planning?

The opinion of a competent Certified Medical Planner® can assist.

ASSESSMENT: Your thoughts, comments and input are appreciated.

Posted on November 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Internal Revenue Service (IRS) ruled that employees at an unnamed company can designate a portion of their employer match to student debt repayments or health reimbursement accounts, in addition to their traditional 401(k).

Warren Buffett’s Midas touch gave a boost to Domino’sPizza and PoolCorp. after Berkshire Hathaway announced it has bought shares of both companies. Domino’s popped to start the day but dropped 1.27%, while Pool climbed just 0.54%.

Palantir is jumping ship, moving from the NYSE to the Nasdaq. Shareholders liked the move, pushing the stock up 11.14%.

Bloom Energy…bloomed 59.19% on the news that the renewable energy company reached an agreement to provide utility company American Electric Power with 1 gigawatt worth of fuel cells.

STOCKS DOWN

What Buffett giveth, Buffett taketh away: Apple sank on the news that Berkshire Hathaway has sold shares of the company, and almost completely eliminated its position in UltaBeauty. Apple fell 1.41%, while Ulta Beauty dropped 4.60%.

Shareholders were expecting the worst from Chinese online retailer Alibaba, and although the company actually beat earnings forecasts, it wasn’t enough—shares still sank 2.20%.

Applied Materials tumbled 9.20% after beating both top and bottom line expectations, but shareholders balked at the slowdown in several key businesses.

Here’s where the major stock market benchmarks ended:

The SPX fell 78.55 points (–1.32%) to 5,870.62 to end the week down 2.08%; the Dow Jones Industrial Average® ($DJI) lost 305.87 points (–0.70%) to 43,444.99 to end the week down 1.24%; and the NASDAQ Composite®($COMP) decreased 427.52 points (–2.24%) to 18,680.12 to end the week down 3.15%.

The 10-year Treasury note yield rose one basis point to 4.43% but added 12 basis points for the week. Shorter-term yields rose less.

The CBOE Volatility Index® (VIX) climbed sharply to 16.11 as stocks fell.

The problems at storied bond manager Western Asset Management keep growing. Clients have pulled about $55 billion from Wamco, as the division is known, since mid-August, representing about 15% of its assets. Franklin Templeton, its 77-year-old parent company and one of the largest asset managers in the U.S., recently reported its steepest quarterly outflows on record.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

A paradox is a logic and self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

***

And so, as we plan for our financial future thru a New Year Resolution for 2025, it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

According to Adam Grossman, here are seven [7] of the paradoxes that can bedevil financial decision-making, clients and financial advisors, alike:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds. More:https://tinyurl.com/285vftx4

There’s the paradox that the stock market may appear over valued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as the recent 2024 election results attest.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

401(k) vs. pension: There’s pros and cons to both. While pension plans guarantee a steady income stream, payments sometimes aren’t indexed by inflation, which can erode their value over time. On the flip side, 401(k)s are subject to market fluctuations and require financial literacy.

Medical Executive-Post Publisher-in-Chief, Dr. David Edward Marcinko MBA CMP™, and financial planner Paul Larson CFP™, were interviewed by Sharon Fitzgerald for Medical News, Inc. Here is a reprint of that interview.

Doctors Squeezed from both Ends

Physicians today “are getting squeezed from both ends” when it comes to their finances, according Paul Larson, president of Larson Financial Group. On one end, collections and reimbursements are down; on the other end, taxes are up. That’s why financial planning, including a far-sighted strategy for retirement, is a necessity.

Larson Speaks

“We help these doctors function like a CEO and help them quarterback their plan,” said Larson, a Certified Financial Planner™ whose company serves thousands of physicians and dentists exclusively. Headquartered in St. Louis, Larson Financial boasts 19 locations.

Larson launched his company after working with a few physicians and recognizing that these clients face unique financial challenges and yet have exceptional opportunities, as well.

What makes medical practitioners unique? One thing, Larson said, is because they start their jobs much later in life than most people. Physicians wrap up residency or fellowship, on average, at the age of 32 or even older. “The delayed start really changes how much money they need to be saving to accomplish these goals like retirement or college for their kids,” he said.

Another thing that puts physicians in a unique category is that most begin their careers with a student-loan debt of $175,000 or more. Larson said that there’s “an emotional component” to debt, and many physicians want to wipe that slate clean before they begin retirement saving.

Larson also said doctors are unique because they are a lawsuit target – and he wasn’t talking about medical malpractice suits. “You can amass wealth as a doctor, get sued in five years and then lose everything that you worked so hard to save,” he said. He shared the story of a client who was in a fender-bender and got out of his car wearing his white lab coat. “It was bad,” Larson said, and the suit has dogged the client for years.

The Three Mistake of Retirement Planning

Larson said he consistently sees physicians making three mistakes that may put a comfortable retirement at risk.

The first is assuming that funding a retirement plan, such as a 401(k), is sufficient. It’s not. “There’s no way possible for you to save enough money that way to get to that goal,” he said. That’s primarily due to limits imposed by the Internal Revenue Service, which allows a maximum contribution of $49,000 annually if self-employed and just $16,500 annually until the age of 50. He recommends that physicians throughout their career sock away 20 percent of gross income in vehicles outside of their retirement plan.

The second common mistake is making investments that are inefficient from a tax perspective. In particular, real estate or bond investments in a taxable account prompt capital gains with each dividend, and that’s no way to make money, he said.

The third mistake, and it’s a big one, is paying too much to have their money managed. A stockbroker, for example, takes a fee for buying mutual funds and then the likes of Fidelity or Janus tacks on an internal fee as well. “It’s like driving a boat with an anchor hanging off the back,” Larson said.

Marcinko Speaks

Dr. David E. Marcinko MBA MEd CPHQ, a physician and [former] certified financial planner] and founder of the more specific program for physician-focused fiduciary financial advisors and consultants www.CertifiedMedicalPlanner.org, sees another common mistake that wreaks havoc with a physician’s retirement plans – divorce.

He said clients come to him “looking to invest in the next Google or Facebook, and yet they will get divorced two or three times, and they’ll be whacked 50 percent of their net income each time. It just doesn’t make sense.”

Marcinko practiced medicine for 16 years until about 10 years ago, when he sold his practice and ambulatory surgical center to a public company, re-schooled and retired. Then, his second career in financial planning and investment advising began. “I’m a doctor who went to business school about 20 years ago, before it was in fashion. Much to my mother’s chagrin, by the way,” he quipped. Marcinko has written 27 books about practice management, hospital administration and business, physician finances, risk management, retirement planning and practice succession. He’s the founder of the Georgia-based Institute of Medical Business Advisors Inc.

Succession Planning for Doctors

Succession planning, Marcinko said, ideally should begin five years before retirement – and even earlier if possible. When assisting a client with succession, Marcinko examines two to three years of financial statements, balance sheets, cash-flow statements, statements of earnings, and profit and loss statements, yet he said “the $50,000 question” remains: How does a doctor find someone suited to take over his or her life’s work? “We are pretty much dead-set against the practice broker, the third-party intermediary, and are highly in favor of the one-on-one mentor philosophy,” Marcinko explained.

“There is more than enough opportunity to befriend or mentor several medical students or interns or residents or fellows that you might feel akin to, and then develop that relationship over the years.” He said third-party brokers “are like real-estate agents, they want to make the sale”; thus, they aren’t as concerned with finding a match that will ensure a smooth transition.

The only problem with the mentoring strategy, Marcinko acknowledged, is that mentoring takes time, and that’s a commodity most physicians have too little of. Nonetheless, succession is too important not to invest the time necessary to ensure it goes off without a hitch.

Times are different today because the economy doesn’t allow physicians to gradually bow out of a practice. “My overhead doesn’t go down if I go part-time. SO, if I want to sell my practice for a premium price, I need to keep the numbers up,” he noted.

Assessment

Dr. Marcinko’s retirement investment advice – and it’s the advice he gives to anyone – is to invest 15-20 percent of your income in an Vanguard indexed mutual fund or diversified ETF for the next 30-50 years. “We all want to make it more complicated than it really is, don’t we?” he said.

QUESTION: What makes a physician moving toward retirement different from most others employees or professionals? Marcinko’s answer was simple: “They probably had a better shot in life to have a successful retirement, and if they don’t make it, shame on them. That’s the difference.”

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Understanding the Impending Retirement-Planning Crisis

[By Somnath Basu PhD, MBA]

A serious retirement-planning crisis is looming in the US with many Baby Boomer physicians, and others, having already spent a portion of their nest egg and undermining any hope for a comfortable lifestyle unless they continue to work. Notwithstanding medical professionals, look no further than an annual “retirement confidence” survey conducted by the Employee Benefit Research Institute and Mathew Greenwald & Associates in each of the past 17 years. Nearly two in five of working Americans responding to the latest survey indicated that they have taken no action in the face of reductions in their employer-provided retirement benefits.

Consumption Equals Happiness?

The population is constantly told that consumption equals happiness. At the same time they are not being asked to understand about the implications of borrowing to fund for such consumption. Before we can expect to effect a change in the ensuing pattern of a vicious cycle, the population mass must have a clear understanding of the difference between needs (e.g., retiring with peace of mind) and desires (e.g., cruises or living the high life).

Negative Savings Rate

When savings first dipped into negative territory during the Great Depression in 1932 and 1933, people didn’t have enough to eat, whereas there has been no such urgency to raid nest eggs since the repeat of this performance in 2005 when the rate fell to minus 0.5 percent. Our grandparents were shining stars in the way they worked hard to build this country’s infrastructure and manufacturing sector, saved every red cent they could get their hands on and created affluence on a mass scale. Today we’re able to enjoy the fruit of their labor. But, somehow their values were lost on future generations.

Changing American Culture

Many of the nation’s top engineers and scientists now hail from China, India and other Asian countries as American culture has undergone a dramatic change to the point where jocks and cheerleaders are more valued than computer geeks and science nerds in our schools. We inherited so much affluence that it made us lazy as a society. The seeds of our destruction have been sown, but it’s up to our politicians, educators and other leaders, including financial advisors, to help reverse this disturbing pattern before it’s too late.

Many people fall into the trap of rushing through dinner and unwinding in front of the TV where a big part of the problem lies in slick and subtle, and hard to resist, primetime advertising and marketing messages (prime time for subtle messages) that seduce viewers into purchasing luxury cars or flying to far-flung resorts where they can sip umbrella-clad cocktails alongside affluent vacationers.

Americans in Debt

A recent wave of foreclosures has put Americans deeper in debt, with the sub-prime crisis exposing despicable predatory lending practices. But, research has shown the wreckage also could be found strewn across in the mid-prime and prime markets as middle-class borrowers struggled to pay adjustable rate mortgages. High hopes have been pinned on the stock market helping people crawl out from this crisis just like when the real estate market had softened the blow when the tech-bubble burst at the turn of this century. So far, this has happened, to an extent. But, if the stock market starts reeling again, then it will spell even bigger trouble. Add to this the international trade imbalance, which implies foreign governmental funding of our conspicuous consumption, and which comes with high interest rates that need to be paid to the lenders, again to such countries as China, India and other emerging economies, and a bigger, worse picture emerges.

Personal Bankruptcies

Personal bankruptcies have an even more devastating effect on an individual’s ability to plan for the future, particularly since the laws pertaining to this area were toughened to a point where reckless spenders will need to muster fiscal and financial discipline as never before. The doomsday scenario is that children now run the risk of inheriting debt instead of wealth, and it’s unconscionable to think future generations would have a standard of living that’s worse than their parents or grandparents.

Assessment

The true grit associated with being an American is to rise up in the face of adversity – a frontier spirit that drew me this remarkable country. We’ve weathered numerous storms and can do it again. But, it requires a serious commitment to stopping mindless consumption of goods and services, as well as understanding there’s a difference between basic needs and pie-in-the-sky desires.

NOTE: Dr. Somnath Basu is a Professor of Finance at California Lutheran University and the Director of its California Institute of Finance. He is also the creator of the innovative AgeBander technology www.agebander.com for planning retirement needs.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A retirement nest egg of $2.5 million can likely produce an annual income of $100,000 for as long as you are likely to live. This is using the 4% withdrawal rate many financial advisors consider standard. After starting with the first withdrawal of 4% of the total, the annual withdrawal will adjust for inflation. For example, if inflation runs at the target 2% rate of federal policymakers, during retirement the retiree will withdraw:

$100,000

in the first year

$102,000

in the second year

$104,040

in the third year and so on …

According to this model and conventional wisdom, a 4% withdrawal rate will allow a portfolio to last for at least 30 years. This would permit a 65-year-old retiree to maintain consistent purchasing power until age 95 and beyond.

For most retirees, this will likely be adequate to maintain a satisfying standard of living. Only about 3% of 2,000 retirees surveyed by the Employee Benefit Research Institute in 2022 spent $7,000 or more per month, equivalent to $84,000 in annual spending.

This model does not include a number of other factors. For instance, nearly all retirees are eligible for Social Security. For 2023, the maximum monthly Social Security benefit for people who claim benefits at full retirement age is $3,627. That’s equal to more than half the spending of the top 3% of retirees surveyed by EBRI. And, like the standard withdrawal rate, Social Security benefits are indexed to inflation.

5 Variables for Retiring With $2.5 Million at Age 65

While $2.5 million could seem like enough to retire at 65, many factors could change the outlook.

1. Unexpected Healthcare Costs

The Fidelity Retiree Health Care Cost Estimate suggests an average 65-year-old couple could need (approximate, after taxes):

This assumes both spouses are enrolled in traditional Medicare, which between Medicare Part A and Part B covers expenses such as hospital stays, doctor visits and services, physical therapy, lab tests and more, and in Medicare Part D, which covers prescription drugs.

This figure does not include long-term care (“custodial care”), most dental care, eye exams and more, so your estimated healthcare costs in retirement could be considerably more.

2. Inflation

Inflation can powerfully influence retirees’ financial well-being. When inflation occurs, it reduces the purchasing power of money withdrawn from your retirement account. You can increase withdrawals to maintain purchasing power, but this risks more quickly depleting your savings.

3. Market Downturns

Inflation isn’t the only cause of market downturns. Business cycles and financial crises can exaggerate normal fluctuations in stock market valuations. If you’re selling investments to generate income for living expenses, you may want to sell more if valuations are down.

4. Longevity

While living a long life is positive, you could outlive the money you’ve saved for retirement. Many financial planners use life expectancy to age 95 or 100 when developing plans for funding retirement.

The Social Security Administration says an average 65-year-old male can live to age 83, while the average woman can live to age 86. However, people in their 80s and 90s also generally reduce their spending, with the exception of healthcare costs.

5. Estate Planning

Retiring at 65 with $2.5 million likely involved generating high income and savings, so there’s a chance you could have assets to pass on. With estate planning, adding members of your family as beneficiaries for homes you paid off with a mortgage may have long-term positives.

You may also want to think about any additional income streams. For example, if you own a medical practice or business, you may want to add your family as a beneficiary so they can decide to keep the business running or sell it.

You’ve got a sense of your ideal retirement age. And you’ve probably made certain plans based on that timeline. But what if you’re forced to retire sooner than you expect? Aging baby-boomers, corporate medicine, the medical practice great resignation and/or the pandemic, etc?