DR. DAVID E. MARCINKO MBA

http://www.CertifiedMedicalPlanner.org

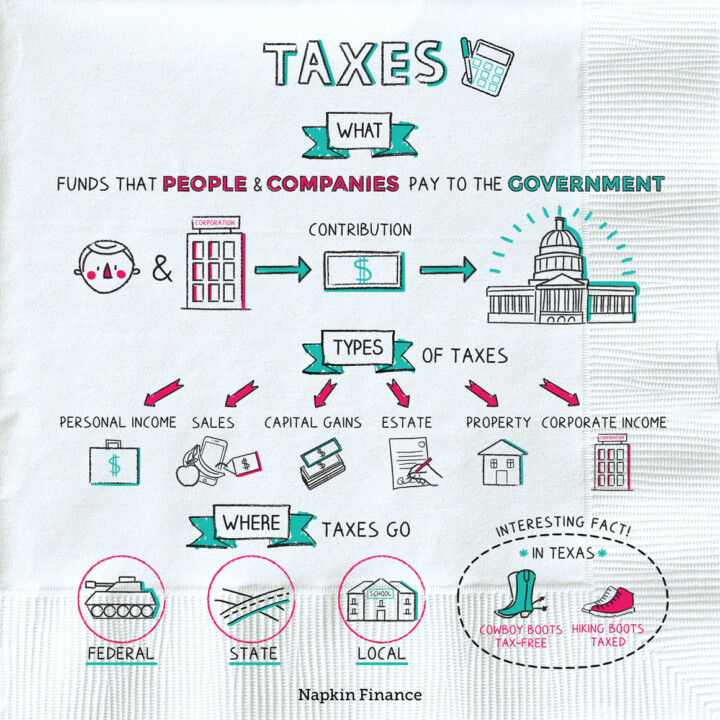

eTax Savings Strategies

[By Ana Vassallo] AND [Dr. David E. Marcinko MBA]

Managed Care Organizations (MCOs) that accept capitated risk contracts face a potentially significant tax burden for Incurred but Not Reported (IBNR) claims. It is not uncommon that IBNR claims at the end of a reporting period equal one to two months premiums for MCOs under a fee-for-service model. The Internal Revenue Service (IRS) has taken a very strong position relative to the deductibility of these claims by saying that an MCO cannot deduct such losses if they are based on estimates.

Incurred But Not Reported [IBNR] Claims

IBNR is a term that refers to the costs associated with a medical service that has been provided, but for which the carrier has not yet received a claim. The carrier to account for estimated liability based on studies of prior lags in claim submission records IBNR reserves. In capitated contracts, MCOs are responsible for IBNR claims of their enrollees (Kennedy, 1).

For example, if an enrollee is treated in an emergency room, a plan may not know it is liable for this care for at least 30-60 days. Well-run plans devote considerable attention to accurately estimating such claims because a plan can look healthy based on claims submitted and be financially unhealthy if IBNR claims experience is increasing substantially but is unknown.

Why a Problem for HMO’s/MCOs

Section 809(d)(1) of the Code provides that, for purposes of determining the gain and loss from operations, a insurance company shall be allowed a deduction for all claims and benefits accrued, and all losses incurred (whether or not ascertained), during the taxable year on insurance and annuity contracts. Section 1.809-5(a) (1) of the Income Tax Regulations provides that the term “losses incurred (whether or not ascertained)” includes a reasonable estimate of the amount of the losses (based upon the facts in each case and the company’s experiences with similar cases) incurred but not reported by the end of the taxable year as well as losses reported but where the amount thereof cannot be ascertained by the end of the year. By taking into account for its prior years only the reported losses but not the unreported losses, the taxpayer has established a consistent pattern of treating a material item as a deduction. The effect of the taxpayer’s claim for the first time of a deduction for an estimate of losses incurred but unreported under section 809(d)(1) of the Code, was to change the timing for taking the deduction for the incurred but unreported losses.

Due to the taxpayer consistently deducting losses incurred in the taxable year in which reported, a change in the time for deducting losses incurred under section 809(d)(1) is a change in the method of accounting for such losses to which the provisions of section 446(e) apply (IRS, 14-30).

In order to qualify for an insurance company under the current IRS regulations, the MCO must have the following criteria (Kongstvedt, 235-256):

· At least 50% of the MCO must come from insurance related activities.

· The MCO must have an insurance company license.

If an MCO did not have these two criteria, the IRS will not deem the manage care company as an eligible insurance company. Therefore, the MCO would not be able to file for IBNRs with the IRS.

How MCOs/HMOs Intensify IBRN Claims

There is a high degree of uncertainty inherent in the estimates of ultimate losses underlying the liability for unpaid claims. The only reason the IRS would not allow an MCO to deduct IBNR because the financial statements is based on an estimate (IRS, 134-155).

Except through the insurance company exclusion IRS does not allow any taxpayer to deduct losses based on estimates. There has been some precedence set that the IRS will accept an amount for incurred but not reported claims if the amount is supported by valid receipts of claims that the company has in-house prior to the filing of the tax return.

There has been some controversy as to how long of a period of reporting time the IRS will allow you to include in those estimates. There are ranges from 3-6 months to file a claim (IRS, 137). The process by which these reserves are established requires reliance upon estimates based on known facts and on interpretations of circumstances, including the business’ experience with similar cases and historical trends involving claim payment patterns, claim payments, pending levels of unpaid claims and product mix, as well as other factors including court decisions, economic conditions and public attitudes.

There has been no clear indication from the IRS that it will accept an accrual for these losses and entities. Therefore, companies deducting such losses may eventually find themselves in a position where the IRS may challenge the relating deductibility of those losses.

Evaluating IBNRs from a New Present Value Perspective

The best measure of whether or not a stream of future cash flows actually adds value to the organization is the net present value (NPV). The best decision rule for NPV to accept or reject a decision problem is if the NPV is greater than zero, the project adds value to the organization. Although – if the NPV is exactly zero it neither adds nor subtracts value from the organization (McLean 193). In either case, the project is acceptable. In addition, if the NPV is less than zero, the project subtracts value from the organization and should not be undertaken (McLean, 193).

The provision for unpaid claims represents an estimate of the total cost of outstanding claims to the year-end date. Included in the estimate are reported claims, claims incurred but not reported and an estimate of adjustment expenses to be incurred on these claims. The losses are necessarily subject to uncertainty and are selected from a range of possible outcomes (Veal, 11). During the life of the claim, adjustments to the losses are made as additional information becomes available. The change in outstanding losses plus paid losses is reported as claims incurred in the current period.

All but the smallest organizations have predictable and unpredictable losses. It is important mentally to separate the two since predictable losses are not risks but normal business expenses. Risk is the degree to which losses vary from the expected. If losses average $85,000 per year but could be as much as $20 million, the risk is $20 million minus $85,000. The $85,000 figure represents reasonably predictable losses (Veal, 12).

IBNR Challenges and Solutions

While I was unable to find an actual amount of the cost of the penalties that can be incurred, the IRS is able to impose penalty fees under Section 4958 of the IRS code (IRS, 255). While penalties differ depending on individual bases, MCOs will be penalizing for any misconduct either by IRS Codes or Court Jurisdiction.

It is prudent that MCOs ensure their organization that they will not incur a financial “meltdown”. They further need to ensure IBNR is funded for period of at least 2-3 months. In some states, the state laws make the MCO financially responsible to pay the providers for a second time if the intermediary fails to pay or becomes insolvent (Cagle, 1).

Paid losses, paid expenses and net premiums are usually deductible; reserves for incurred-but-unpaid losses generally are not, unless the taxpaying entity is an insurance company. Consequently, if a corporation has a high effective tax rate and concedes that it cannot deduct self-insured loss reserves, some of its more cost-effective options may be a paid-loss retro (if state rules are not too restrictive), a compensating balance plan, or the formation of a pool or industry captive. Even these plans may be subject to IRS challenge. To qualify as a tax-deductible expense, a premium or other payment must satisfy two criteria (Cagle, 2):

- There must be transfer of risk: an insurance risk. This differs from investment risk, but there is no authoritative definition of “risk transfer” other than various court decisions (primarily Helvering v. Le Gierse, 312 US 531 — U.S. Supreme Court 1941).

- There must be both risk shifting and risk distribution. “Risk shifting” means that one party shifts the risk of loss to another, generally not in the same corporate family. “Risk distribution” means that the party assuming the risk distributes the potential liability, in part, among others.

The deductibility of an insurance expense may also be questioned if it is contingent upon a future happening, such as a loss payment, right to a dividend or other credit, or possible forgiveness of future loans or notes (Cagle, 3). This may seem a broad statement, but the Cost Accounting Standards Board states in its Standards for Accounting for Insurance Expense that any expense which is recoverable if there are no losses shall be accounted as a deposit, not an expense. This is essentially the IRS position (IRS, 145).

Assessment

While there are a few solutions to this matter, the IRS is making sure that MCOs will be penalized if MCOs improperly handle IBNRs. It is also important for organizations to understand the MCO’s policies regarding IBNR reserves and their contractual obligations. And, while the IRS has set limitations for MCOs to file their IBNR claims, MCOs have the major responsibility of allocating these IBNR claims appropriately. There are severe penalties for not properly filing the IBNR claims appropriately. However, there is several tax saving strategies to help MCOs properly file their IBNR claims with the IRS. It imperative that MCO executives and accounting manager consult an expert to properly plan an ethical strategy that will help them build a stable business that is trustworthy and reliable.

Bibliography

1. Cagle, Jason, Esq., Interview, June 8, 2004, interview performed by Ana Vassallo.

2. McLean, Robert A., Net Profit Value, Pages 193-194, 2nd Edition, Thomson/Delmar Learning, Financial Management in Heath Care Organization, 2003.

3. Patient-Physician Network, Managed Care Glossary, Printed 6/11/04 http:/www.drppg.com/managed_care.asp.

4. Internal Revenue Services, IRS.Gov, Printed 6/12/04, http://www.irs.gov/

5. Internal Revenue Services, Revenue Ruling, Printed 6/11/04, http://www.taxlinks.com/rulings/1079/revrul179-21.thm

6. Kongstvedt, Peter R., Managed Care – What It Is and How it Works, Pages 235-256, Jones and Bartlett Publishers, 2003.

7. Veale, Tom, The Return of Captives in the Hard Market, Tristar Risk Management Aug. 22, 2002, San Diego RIMS.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Filed under: Accounting, Healthcare Finance, Insurance Matters, Practice Management, Research & Development, Taxation | Tagged: Ana Vassallo, HMO, IBNR, IBNR claims, IRS, Managed Care, MCO, NPV | 2 Comments »