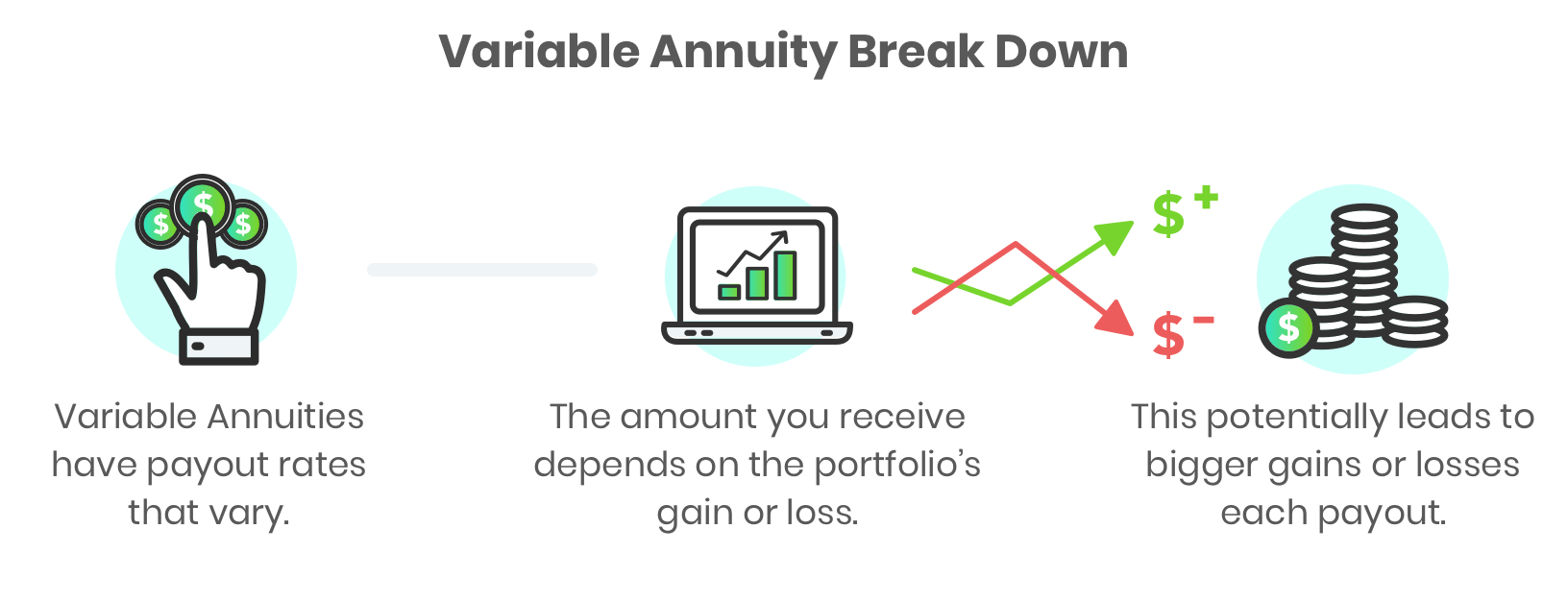

BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BASIC DEFINITIONS

By Dr. David Edward Marcinko MBA MEd

***

***

A financial warrant is similar to an option, but it is typically issued directly by a company rather than traded on an exchange. Warrants allow holders to purchase shares of the issuing company at a fixed price, known as the exercise price, within a specified time frame. Unlike options, which are standardized and traded on secondary markets, warrants are often attached to bonds or preferred stock as a “sweetener” to make those securities more attractive to investors.

🔑 Key Features of Warrants

Right, not obligation: Investors can choose whether to exercise the warrant depending on market conditions.

Longer maturity: Warrants often have longer lifespans than options, sometimes lasting several years.

Issued by companies: They are a direct financing tool, unlike exchange-traded options.

Dilution effect: When exercised, new shares are created, which can dilute existing shareholders’ equity.

📊 Types of Warrants

Equity warrants: Allow purchase of common stock at a set price.

Bond warrants: Sometimes attached to debt instruments, giving bondholders the right to buy equity.

Detachable vs. non-detachable: Detachable warrants can be traded separately from the bond or preferred share they were issued with, while non-detachable ones remain tied.

Exotic warrants: Some markets offer specialized versions, such as knock-out warrants or mini-futures, which add complexity and leverage.

💼 Uses in Corporate Finance

Companies issue warrants for several reasons:

Capital raising: Warrants encourage investors to buy bonds or preferred shares, providing immediate funding.

Employee incentives: Similar to stock options, warrants can reward employees with potential future equity.

Strategic deals: Warrants may be used in mergers or acquisitions to align interests between parties.

⚖️ Benefits and Risks

Benefits:

Provide leverage, allowing investors to control more shares with less capital.

Offer long-term exposure to a company’s growth potential.

Can enhance returns if the underlying stock price rises above the exercise price.

Risks:

Warrants may expire worthless if the stock price never exceeds the exercise price.

Dilution reduces the value of existing shares when warrants are exercised.

Higher volatility compared to traditional equity investments.

📌 Conclusion

Financial warrants occupy a unique space between corporate finance and speculative investing. They serve as capital-raising tools for companies and leveraged opportunities for investors, but they also carry risks of dilution and expiration without value. Understanding their mechanics, types, and strategic uses is essential for anyone navigating modern financial markets.

In essence, warrants are a bridge between debt and equity, offering flexibility to issuers and optionality to investors. Their role in corporate finance highlights the innovative ways companies structure securities to balance risk, reward, and capital needs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

An Overview

Introduction In the world of finance, the distinction between recourse and non-recourse loans is critical. Non-recourse financing refers to loans in which the lender’s rights are limited strictly to the collateral pledged for the loan. If the borrower defaults, the lender cannot pursue the borrower’s personal assets or income beyond the collateral. This structure makes non-recourse loans particularly attractive to borrowers who want to protect their broader financial portfolio, though it comes with trade-offs such as higher interest rates and stricter eligibility requirements.

Definition and Core Features

A non-recourse loan is secured by collateral, typically real estate or high-value assets. Unlike recourse loans, where lenders can seize collateral and pursue additional assets if the collateral does not cover the debt, non-recourse loans restrict recovery to the collateral alone.

Key features include:

Collateral-based repayment: Only the pledged asset can be seized.

Borrower protection: Other personal or business assets remain untouched.

Higher lender risk: Because recovery is limited, lenders face greater exposure.

Higher interest rates: To offset risk, lenders often charge more.

Applications in Real Estate and Project Financing

Non-recourse financing is most common in commercial real estate and large-scale projects. For example, developers building shopping centers or office towers often rely on non-recourse loans because repayment depends on future rental income once the project is complete. Similarly, infrastructure projects with long lead times—such as energy plants or toll roads—use non-recourse financing to align repayment with project revenues.

This structure allows borrowers to undertake ambitious projects without risking personal bankruptcy if the venture fails. It also encourages investment in sectors where upfront costs are high and returns are delayed.

Comparison with Recourse Loans

The difference between recourse and non-recourse loans lies in risk allocation:

Recourse loans: Lenders can seize collateral and pursue other assets. These loans are lower risk for lenders and typically carry lower interest rates.

Non-recourse loans: Lenders are limited to collateral. Borrowers gain protection, but lenders demand higher rates and stricter terms.

This trade-off means non-recourse loans are less common and usually reserved for borrowers with strong creditworthiness or projects with predictable revenue streams.

Advantages of Non-Recourse Financing

Risk limitation for borrowers: Protects personal wealth and other business assets.

Encourages investment: Makes large-scale, high-risk projects feasible.

Predictable liability: Borrowers know their maximum exposure is limited to collateral.

Disadvantages and Risks

Higher costs: Interest rates and fees are higher due to lender risk.

Strict eligibility: Only borrowers with strong financial standing or valuable collateral qualify.

Collateral dependency: If the collateral loses value, lenders face significant losses.

Bad boy carve-outs: Certain clauses allow lenders to pursue borrowers if fraud, misrepresentation, or intentional misconduct occurs.

Legal and Financial Implications

Non-recourse financing is shaped by legal frameworks that define lender rights. In many jurisdictions, lenders cannot pursue deficiency judgments beyond collateral. However, exceptions exist through “bad boy carve-outs,” which hold borrowers personally liable for misconduct such as misappropriation of funds or environmental violations.

Conclusion

Non-recourse financing is a powerful tool in modern finance, particularly for commercial real estate and infrastructure projects. By limiting borrower liability to collateral, it enables ambitious ventures while protecting personal assets. However, this protection comes at the cost of higher interest rates, stricter eligibility, and potential carve-outs that reintroduce personal liability. Ultimately, non-recourse loans represent a balance between borrower protection and lender risk, shaping the way large-scale projects are funded and developed.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

The Financial Industry Regulatory Authority (FINRA) is a cornerstone of the U.S. financial system, serving as a self-regulatory organization that oversees brokerage firms and their registered representatives. Established in 2007 through the consolidation of the National Association of Securities Dealers (NASD) and the regulatory arm of the New York Stock Exchange, FINRA plays a critical role in maintaining market integrity, protecting investors, and ensuring that the securities industry operates fairly and transparently.

Origins and Mission

FINRA’s creation was driven by the need for a unified regulatory body that could streamline oversight of broker-dealers. Its mission is straightforward yet vital: to safeguard investors and promote market integrity. Unlike government agencies such as the Securities and Exchange Commission (SEC), FINRA is a non-governmental organization, but it operates under the SEC’s supervision. This unique structure allows FINRA to act with agility while still being accountable to federal oversight.

Core Responsibilities

FINRA’s responsibilities are broad and multifaceted.

Licensing and Registration: FINRA ensures that brokers and brokerage firms meet professional standards before they can operate. This includes administering qualification exams such as the Series 7 and Series 63.

Rulemaking and Enforcement: FINRA develops rules that govern broker-dealer conduct and enforces them through disciplinary actions when violations occur.

Market Surveillance: FINRA monitors trading activity across U.S. markets to detect fraud, manipulation, or other irregularities.

Investor Education: Through initiatives like BrokerCheck, FINRA provides investors with tools to research brokers and firms, empowering them to make informed decisions.

Each of these functions contributes to a safer and more transparent marketplace.

Protecting Investors

Investor protection lies at the heart of FINRA’s mission. By enforcing ethical standards and monitoring trading practices, FINRA reduces the risk of misconduct such as insider trading, excessive risk-taking, or misleading investment advice. Its arbitration and mediation services also provide investors with avenues to resolve disputes with brokers outside of lengthy court proceedings. This combination of proactive regulation and accessible dispute resolution strengthens public trust in financial markets.

Challenges and Criticisms

Like any regulatory body, FINRA faces challenges. Critics argue that as a self-regulatory organization, it may be too close to the industry it oversees, raising concerns about conflicts of interest. Others question whether its penalties are sufficient to deter misconduct. Additionally, the rapid evolution of financial technology, cryptocurrency markets, and complex trading algorithms presents new regulatory hurdles. FINRA must continually adapt its rules and surveillance systems to keep pace with innovation.

Impact on the Financial System

Despite these challenges, FINRA’s impact is undeniable. By maintaining standards of conduct and transparency, it helps ensure that capital markets remain efficient and trustworthy. Investors, from individuals saving for retirement to institutions managing billions, rely on FINRA’s oversight to protect their interests. Broker-dealers, meanwhile, benefit from clear rules that create a level playing field and reduce systemic risk.

Conclusion

In summary, FINRA is an essential pillar of the U.S. financial regulatory framework. Its blend of licensing, rulemaking, enforcement, and investor education fosters confidence in the securities industry. While it must continue to evolve in response to technological and market changes, its mission remains constant: protecting investors and promoting integrity. Without FINRA’s presence, the risk of misconduct and instability in financial markets would be far greater. As the financial landscape grows more complex, FINRA’s role will only become more critical in ensuring that markets remain fair, transparent, and resilient.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

In the realm of finance and investment, the pursuit of profit is inseparable from the presence of risk. Every investor, whether an individual or an institution, must grapple with the reality that higher returns often come with greater uncertainty. To evaluate investments effectively, it is not enough to look at raw returns alone. Instead, one must consider how much risk was undertaken to achieve those returns. This balance is captured by the concept of the risk-adjusted rate of return, a cornerstone of modern portfolio theory and investment analysis.

The risk-adjusted rate of return measures the profitability of an investment relative to the risk assumed. Unlike simple return calculations, which only show the percentage gain or loss, risk-adjusted metrics incorporate volatility and other forms of uncertainty. For example, two investments may both yield a 10% annual return, but if one is highly volatile and the other is stable, the stable investment is more attractive when viewed through a risk-adjusted lens. This approach ensures that investors are not misled by high returns that are achieved through excessive risk-taking.

Several tools have been developed to calculate risk-adjusted returns. The Sharpe Ratio is among the most widely used. It measures excess return per unit of risk, with risk defined as the standard deviation of returns. A higher Sharpe Ratio indicates that an investment is delivering better returns for the level of risk taken. Another measure, the Treynor Ratio, evaluates returns relative to systematic risk, using beta as the risk measure. The Sortino Ratio refines the Sharpe Ratio by focusing only on downside volatility, thereby distinguishing between harmful risk and general fluctuations. Each of these metrics provides a different perspective, but all share the same goal: to assess whether the reward justifies the risk.

The importance of risk-adjusted returns extends beyond individual securities to entire portfolios. Portfolio managers use these metrics to compare strategies, evaluate asset allocations, and determine whether their investment approach aligns with client objectives. For instance, a hedge fund may report impressive raw returns, but if those returns are accompanied by extreme volatility, its risk-adjusted performance may be inferior to that of a conservative mutual fund. By incorporating risk-adjusted measures, investors can make more informed decisions and build portfolios that reflect their risk tolerance and long-term goals.

Risk-adjusted returns also play a vital role in distinguishing skill from luck in investment management. A manager who consistently delivers high risk-adjusted returns demonstrates genuine expertise in navigating markets. Conversely, a manager who achieves high raw returns through excessive risk-taking may simply be gambling with investor capital. This distinction is critical for institutions and individuals alike, as it ensures that performance evaluations are grounded in sustainability rather than short-term speculation.

Of course, risk-adjusted metrics are not without limitations. They often rely on historical data, which may not accurately predict future outcomes. Market conditions can change rapidly, and past volatility may not reflect future risks. Additionally, different metrics may yield conflicting results, complicating the decision-making process. Despite these challenges, risk-adjusted returns remain indispensable because they encourage investors to look beyond superficial gains and consider the broader context of risk management.

In conclusion, the risk-adjusted rate of return is a fundamental concept in investment analysis. By integrating both risk and reward into a single measure, it empowers investors to evaluate opportunities more effectively, compare diverse assets, and build resilient portfolios. While no metric is flawless, the emphasis on risk-adjusted performance ensures that investment decisions are not driven solely by the pursuit of high returns but by the pursuit of sustainable, well-balanced growth. In a financial landscape defined by uncertainty, the ability to measure success in terms of both profit and prudence is what ultimately separates wise investing from reckless speculation.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

Money supply measures—M0, M1, M2, and M3—are essential tools used by economists and policymakers to assess liquidity, guide monetary policy, and understand economic health. Each measure reflects a different level of liquidity and plays a unique role in financial analysis.

The money supply refers to the total amount of monetary assets available in an economy at a specific time. It includes various forms of money, ranging from physical currency to more liquid financial instruments. To better understand and manage economic activity, central banks and economists categorize money into different measures based on liquidity: M0, M1, M2, and M3.

M0, also known as the monetary base or base money, includes all physical currency in circulation—coins and paper money—plus reserves held by commercial banks at the central bank. It represents the most liquid form of money and is directly controlled by the central bank through tools like open market operations and reserve requirements.

M1 builds on M0 by adding demand deposits (checking accounts) and other liquid deposits that can be quickly converted into cash. It includes:

Physical currency held by the public

Traveler’s checks

Demand deposits at commercial banks

M1 is a key indicator of immediate spending power in the economy. A rapid increase in M1 can signal rising consumer activity, while a decline may indicate tightening liquidity.

M2 expands further by including near-money assets—those that are not as liquid as M1 but can be converted into cash relatively easily. M2 includes:

All components of M1

Savings deposits

Money market securities

Certificates of deposit (under $100,000)

M2 is widely used by economists and the Federal Reserve to gauge intermediate-term economic trends. It reflects both spending and saving behavior, making it a critical tool for forecasting inflation and guiding interest rate decisions.

M3, though no longer published by the Federal Reserve since 2006, includes M2 plus large time deposits, institutional money market funds, and other larger liquid assets. M3 provides a broader view of the money supply, especially useful for analyzing long-term investment trends and credit expansion. Some countries, like the UK and India, still track M3 for macroeconomic planning.

These measures are not just academic—they have real-world implications. For instance, during the COVID-19 pandemic, the U.S. saw a historic surge in M2 due to stimulus payments and quantitative easing. This expansion raised concerns about future inflation, which materialized in subsequent years. Monitoring money supply helps central banks adjust monetary policy to maintain price stability and support economic growth.

In conclusion, money supply measures offer a layered view of liquidity in the economy, from the most liquid (M0) to broader aggregates (M3).

Understanding these categories helps policymakers, investors, and businesses anticipate economic shifts, manage inflation, and make informed financial decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Risk arbitrage, often referred to as merger arbitrage, is a specialized investment strategy that seeks to exploit pricing inefficiencies arising during corporate mergers, acquisitions, or other restructuring events. Unlike traditional arbitrage, which involves risk-free profit opportunities from price discrepancies across markets, risk arbitrage carries inherent uncertainty because it depends on the successful completion of corporate transactions. Despite its name, it is not risk-free; rather, it is a calculated approach to profiting from the probability of deal closure.

At its core, risk arbitrage involves buying the stock of a company being acquired and, in some cases, shorting the stock of the acquiring company. For example, if Company A announces it will acquire Company B at $50 per share, but Company B’s stock trades at $47, arbitrageurs may purchase shares of Company B, betting that the deal will close and the stock will rise to the agreed acquisition price. The $3 difference represents the potential arbitrage profit. However, this spread exists precisely because of uncertainty: regulatory approval, financing challenges, shareholder resistance, or unforeseen market conditions could derail the transaction, leaving arbitrageurs exposed to losses.

The practice of risk arbitrage has a long history in Wall Street. It gained prominence in the mid-20th century, particularly during the wave of conglomerate mergers in the 1960s and leveraged buyouts in the 1980s. Hedge funds and specialized arbitrage desks at investment banks became key players, using sophisticated models to assess the likelihood of deal completion. Today, risk arbitrage remains a central strategy for event-driven funds, which focus on corporate actions as catalysts for investment opportunities.

One of the defining features of risk arbitrage is its reliance on probability analysis. Investors must evaluate not only the financial terms of the deal but also the legal, regulatory, and political environment. For instance, antitrust regulators may block a merger if it reduces competition, or foreign investment committees may intervene in cross-border acquisitions. Arbitrageurs often assign probabilities to deal completion and calculate expected returns accordingly. A deal with high regulatory risk may offer a wider spread, but the probability of failure tempers the attractiveness of the trade.

Risk arbitrage also plays an important role in market efficiency. By narrowing the spread between target company stock prices and acquisition offers, arbitrageurs help align market prices with expected outcomes. Their activity provides liquidity to shareholders of target firms and signals market confidence—or skepticism—about deal success. In this sense, arbitrageurs act as informal referees of corporate transactions, reflecting collective judgment about feasibility.

Nevertheless, risk arbitrage is not without controversy. Critics argue that it can encourage speculative behavior and amplify volatility around merger announcements. Moreover, when deals collapse, arbitrageurs can suffer significant losses, as seen in high-profile failed mergers. The strategy requires not only financial acumen but also resilience in managing downside risk.

In conclusion, risk arbitrage is a sophisticated investment strategy that blends financial analysis with legal and regulatory insight. While it offers opportunities for profit, it demands careful risk management and a deep understanding of corporate dynamics. Far from being risk-free, it is a calculated gamble on the successful execution of complex transactions. For investors willing to navigate uncertainty, risk arbitrage remains a compelling, though challenging, avenue in modern financial markets.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

A Special Purpose Acquisition Company (SPAC) is a corporate entity created solely to raise capital through an initial public offering (IPO) with the intention of merging with or acquiring an existing private company. Unlike traditional firms, SPACs have no commercial operations at the time of their IPO. They exist as shell companies, holding investor funds in trust until a suitable target is identified. This unique structure has earned them the nickname “blank check companies.”

How SPACs Work

The lifecycle of a SPAC typically unfolds in three stages:

Formation and IPO: Sponsors—often experienced investors or industry executives—form the SPAC and take it public, raising funds from investors.

Target Search: The SPAC has a limited time frame, usually 18–24 months, to identify and negotiate with a private company to merge with.

De-SPAC Transaction: Once a merger is completed, the private company effectively becomes public, bypassing the traditional IPO process.

This process allows private firms to access public markets more quickly and with fewer regulatory hurdles compared to conventional IPOs.

Advantages of SPACs

SPACs gained traction because they offered several benefits:

Speed and Certainty: Traditional IPOs can be lengthy and uncertain, while SPACs provide a faster route to public markets.

Flexibility in Valuation: Unlike IPOs, SPACs can negotiate valuations directly with target companies.

Access to Expertise: Sponsors often bring industry knowledge and networks that can help the acquired company grow.

Investor Opportunity: Investors can participate early, with the option to redeem shares if they dislike the proposed merger.

Risks and Criticisms

Despite their appeal, SPACs are not without controversy:

Sponsor Incentives: Sponsors typically receive a significant stake (often 20%) at a low cost, which can misalign their interests with ordinary investors.

Uncertain Targets: Investors commit funds without knowing which company will be acquired, creating risk.

Performance Concerns: Studies show that many SPACs underperform after completing mergers, with share prices often declining.

Regulatory Scrutiny: Authorities have warned investors to carefully evaluate SPACs, especially regarding projections of future performance, which are less restricted than in IPOs.

Historical Context and Trends

SPACs first appeared in the 1990s but remained niche until the early 2020s, when they experienced a boom. In 2020 and 2021, hundreds of SPAC IPOs raised billions of dollars, fueled by market liquidity and investor enthusiasm. High-profile deals, such as DraftKings and Virgin Galactic, brought attention to the model. However, by the mid-2020s, enthusiasm cooled due to poor post-merger performance and tighter regulations.

Conclusion

SPACs represent a fascinating innovation in financial markets, offering an alternative to traditional IPOs. Their advantages in speed, flexibility, and access to capital made them attractive during periods of market optimism. Yet, their risks—misaligned incentives, uncertain outcomes, and regulatory challenges—have tempered investor enthusiasm. While SPACs are unlikely to disappear entirely, their future will depend on whether they can evolve into a more transparent and sustainable mechanism for taking companies public.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

+ Plus / – Minus Two Weeks

Stock market crashes have long been associated with the fall season, particularly October, which has earned a reputation as a month of financial turmoil. While crashes can occur at any time, the clustering of several historic downturns in autumn has led many investors to believe that markets are more vulnerable during this period.

Historical Patterns of Fall Crashes

Some of the most devastating collapses in financial history have taken place in the fall. The Wall Street Crash of 1929 began in late October and marked the start of the Great Depression. In October 1987, markets experienced “Black Monday,” when the Dow Jones Industrial Average plunged more than 20% in a single day. More recently, the global financial crisis of 2008 saw some of its steepest declines in September and October. These events have cemented autumn’s reputation as a season of heightened risk.

Why the Fall Is Riskier

Several factors contribute to the perception that fall is a dangerous time for markets:

Investor psychology: The memory of past crashes in October can heighten anxiety, making traders more prone to panic selling.

Fiscal cycles: Many institutional investors close their books at the end of September, leading to portfolio adjustments and sell-offs in October.

Economic data releases: Key reports on employment, corporate earnings, and government budgets often arrive in the fall, influencing sentiment.

Global events: Political and economic developments frequently coincide with autumn months, adding uncertainty.

Statistical Evidence and Skepticism

Despite the historical examples, statistical studies suggest that crashes are not inherently more likely in October than in other months. Market downturns are rare events, and their clustering in autumn may be more coincidence than causation. Crashes have also occurred outside the fall, such as the bursting of the dot-com bubble in spring 2000 and the COVID-19 crash in March 2020. This suggests that the so-called “October Effect” may be more psychological than empirical.

Lessons for Investors

Whether or not fall crashes are statistically more likely, the historical record offers important lessons:

Diversify investments to reduce vulnerability to sudden downturns.

Avoid panic selling, since many crashes are followed by rapid recoveries.

Prepare for volatility, as autumn often brings heightened uncertainty.

Conclusion

Stock market crashes are not guaranteed to happen in the fall, but history has made October synonymous with financial turmoil. The clustering of major downturns during this season has created a psychological bias that influences investor behavior. Whether coincidence or pattern, the lesson is clear: autumn is a time when vigilance, discipline, and preparation are especially important for market participants.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

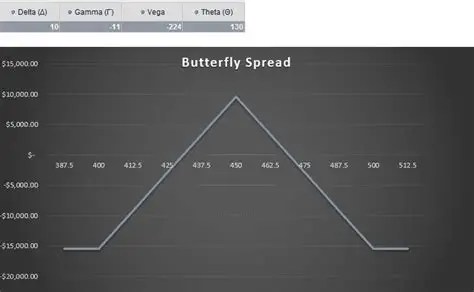

Investing in Butterfly Spreads

Options trading provides investors with a wide range of strategies to suit different market conditions. One of the more refined approaches is the butterfly spread, a strategy designed to profit from stability in the price of an underlying asset. It combines multiple option contracts at different strike prices to create a position with limited risk and limited reward. The name comes from the shape of its profit-and-loss diagram, which resembles the wings of a butterfly.

Structure of the Strategy

A typical butterfly spread involves four options contracts with three strike prices. In a long call butterfly spread, the investor buys one call at a lower strike, sells two calls at a middle strike, and buys one call at a higher strike. This creates a payoff that peaks if the underlying asset closes at the middle strike price. Losses are capped at the initial premium paid, while profits are capped at the difference between the strikes minus the premium.

Variations of Butterfly Spreads

Butterfly spreads can be built with calls, puts, or a mix of both:

Long Call Butterfly: Profits if the asset stays near the middle strike.

Long Put Butterfly: Similar structure but using puts.

Iron Butterfly: Combines calls and puts, selling an at-the-money straddle and buying protective wings.

Reverse Iron Butterfly: Designed to benefit from sharp price movements and volatility.

Each variation adapts to different market expectations, but all share the principle of balancing risk and reward.

Benefits of Butterfly Spreads

Defined Risk: The maximum loss is known upfront.

Cost Efficiency: Requires less capital than outright buying options.

Neutral Outlook: Works best when the investor expects little price movement.

Flexibility: Can be tailored to different market conditions with calls, puts, or combinations.

Drawbacks and Risks

Limited Profit Potential: Gains are capped, which may not appeal to aggressive traders.

Dependence on Timing: The strategy works only if the asset closes near the middle strike at expiration.

Complexity: Requires careful planning of strike prices and expiration dates.

Example in Practice

Suppose a stock trades at $100, and the investor expects it to remain near that level. They could set up a butterfly spread with strikes at $95, $100, and $105. If the stock closes at $100, the strategy delivers maximum profit. If the stock moves significantly away from $100, the investor’s loss is limited to the premium paid. This makes the butterfly spread particularly useful in calm, low-volatility markets.

Conclusion

The butterfly spread is a disciplined options strategy that thrives in stable markets. It offers a balance between risk control and profit potential, making it attractive to traders who prefer structured outcomes. While the rewards are capped, the defined risk and cost efficiency make butterfly spreads a valuable tool for investors who anticipate minimal price movement and want to manage their exposure carefully.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

American Depository Receipts Defined

In the modern era of globalization, financial instruments that connect investors across borders have become indispensable. Among these, American Depository Receipts (ADRs) stand out as a powerful mechanism that allows U.S. investors to participate in foreign equity markets without the complexities of international trading. ADRs not only simplify access to global companies but also enhance the ability of foreign corporations to raise capital in the United States. This essay explores the origins, structure, regulatory frameworks, benefits, risks, and real-world examples of ADRs, highlighting their role in the integration of global finance.

Historical Development

The concept of ADRs emerged in 1927 when J.P. Morgan introduced the first ADR for the British retailer Selfridges. At the time, American investors faced significant hurdles in purchasing foreign shares, including currency conversion, unfamiliar trading practices, and regulatory differences. ADRs solved these problems by creating a U.S.-based certificate that represented ownership in foreign shares, denominated in dollars, and traded on American exchanges.

Over the decades, ADRs expanded rapidly, especially during the post-World War II era when globalization accelerated. By the late 20th century, ADRs had become a mainstream tool for accessing international equities, with companies from Europe, Asia, and Latin America increasingly using them to tap into U.S. capital markets.

Structure and Mechanics

An ADR is issued by a U.S. depositary bank, which holds the underlying shares of a foreign company in custody. Each ADR corresponds to a specific number of shares—sometimes one, sometimes multiple, or even a fraction. Investors buy and sell ADRs in U.S. dollars, and dividends are paid in dollars as well, eliminating the need for currency conversion.

Key structural features include:

Depositary Banks: Institutions such as J.P. Morgan, Citibank, and Bank of New York Mellon act as custodians and issuers of ADRs.

ADR Ratios: The number of foreign shares represented by one ADR can vary, allowing flexibility in pricing.

Trading Platforms: ADRs can be listed on major exchanges like the NYSE or NASDAQ, or traded over-the-counter.

Regulatory Framework

ADRs are subject to U.S. securities regulations, which vary depending on the level of ADR issued:

Level I ADRs: Traded over-the-counter, requiring minimal disclosure. They are primarily used for visibility rather than fundraising.

Level II ADRs: Listed on U.S. exchanges, requiring compliance with SEC reporting standards, including reconciliation of financial statements to U.S. GAAP or IFRS.

Level III ADRs: Allow foreign companies to raise capital directly in U.S. markets through public offerings. These require the highest level of regulatory compliance, including registration with the SEC and adherence to corporate governance standards.

This tiered system ensures that investors receive appropriate levels of transparency while giving foreign companies flexibility in their approach to U.S. markets.

Benefits for Investors

ADRs offer numerous advantages to American investors:

Convenience: Investors can buy shares in foreign companies without dealing with foreign exchanges or currencies.

Diversification: ADRs provide access to global firms across industries, enhancing portfolio diversification.

Transparency: ADRs listed on U.S. exchanges must comply with SEC regulations, ensuring reliable financial reporting.

Liquidity: ADRs trade on familiar platforms, making them easily accessible to retail and institutional investors alike.

Benefits for Companies

Foreign corporations also benefit significantly from ADRs:

Access to Capital: ADRs open the door to the world’s largest pool of investors.

Global Visibility: Listing in the U.S. enhances reputation and credibility.

Improved Liquidity: Shares become more widely traded, increasing market efficiency.

Investor Base Diversification: Companies can attract both domestic and international investors, reducing reliance on local markets.

Risks and Challenges

Despite their advantages, ADRs carry certain risks:

Currency Risk: ADR values are tied to foreign shares denominated in local currencies, making them vulnerable to exchange rate fluctuations.

Political and Economic Risk: Instability in the issuing company’s home country can affect performance.

Taxation: Dividends may be subject to foreign withholding taxes before conversion to U.S. dollars.

Regulatory Differences: Even with SEC oversight, differences in accounting standards and corporate governance can pose challenges.

Case Studies

1. Alibaba Group (China) Alibaba’s ADRs, listed on the NYSE in 2014, marked one of the largest IPOs in history, raising $25 billion. This demonstrated the power of ADRs to connect Chinese companies with American investors, despite regulatory complexities between the two countries.

2. Toyota Motor Corporation (Japan) Toyota’s ADRs have long provided U.S. investors with access to one of the world’s largest automakers. By listing ADRs, Toyota expanded its investor base and strengthened its global presence.

3. Royal Dutch Shell (Netherlands/UK) Shell’s ADRs illustrate how multinational corporations use ADRs to maintain visibility in U.S. markets while managing complex cross-border structures.

The Role of ADRs in Global Finance

ADRs embody the globalization of capital markets. They facilitate cross-border investment, enhance market efficiency, and foster economic integration. For investors, ADRs represent a gateway to international diversification. For companies, they provide access to the deepest capital markets in the world.

Conclusion

American Depositary Receipts are more than just financial instruments; they are symbols of global interconnectedness. By bridging the gap between U.S. investors and foreign companies, ADRs have reshaped the landscape of international finance. They balance convenience with exposure to global risks, offering both opportunities and challenges. As globalization continues to evolve, ADRs will remain a vital tool for investors and corporations alike, reinforcing their role as a cornerstone of modern capital markets.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Role of Volatility Indices in Financial Markets

Volatility is often described as the pulse of financial markets, reflecting the collective emotions of investors as they respond to uncertainty, risk, and opportunity. Among the many tools designed to measure this phenomenon, the CBOE Volatility Index, or VIX, stands out as the most widely recognized. Dubbed the “fear gauge,” the VIX captures market expectations of near-term volatility in the S&P 500, derived from options pricing. Its movements often mirror investor sentiment: rising sharply during periods of crisis and falling when confidence returns. Yet, the VIX is not alone. A family of volatility indices exists across global markets, each offering unique insights into sector-specific or regional risk.

The importance of volatility indices lies in their ability to quantify uncertainty. Traditional measures such as historical volatility look backward, analyzing past price fluctuations. In contrast, indices like the VIX are forward-looking, reflecting implied volatility based on options markets. This distinction makes them invaluable for traders, portfolio managers, and policymakers. For example, a sudden spike in the VIX often signals heightened fear, prompting investors to hedge positions or reduce exposure to equities. Conversely, a low VIX suggests complacency, though it can also precede unexpected shocks.

Beyond the VIX, other indices provide complementary perspectives. The VXN tracks volatility in the Nasdaq-100, often dominated by technology stocks. Because the tech sector is highly sensitive to innovation cycles and regulatory changes, the VXN can diverge significantly from the VIX, highlighting sector-specific risks. Similarly, the RVX measures volatility in the Russell 2000, offering a window into small-cap stocks that are more vulnerable to domestic economic conditions. Internationally, indices such as the VSTOXX in Europe and India VIX extend this framework globally, allowing investors to compare risk sentiment across regions. Together, these indices form a mosaic of market psychology, enabling a more nuanced understanding of global financial stability.

Volatility indices also play a crucial role in risk management. Derivatives linked to these indices, such as futures and exchange-traded products, allow investors to hedge against sudden downturns. For instance, during the 2008 financial crisis, demand for VIX futures surged as investors sought protection from extreme market swings. More recently, volatility products have become popular among retail traders, though their complexity and tendency to lose value over time make them risky for long-term holding.

Critics argue that volatility indices can be misleading. A low VIX does not guarantee stability, and a high VIX does not always signal disaster. Moreover, the rise of volatility-linked products has occasionally amplified market stress, as seen during the “Volmageddon” event of February 2018, when inverse volatility ETFs collapsed. These episodes underscore the need for caution: volatility indices are powerful tools, but they must be used with a clear understanding of their limitations.

In conclusion, volatility indices such as the VIX serve as vital instruments for gauging investor sentiment and managing risk. They provide a forward-looking measure of uncertainty, complementing traditional metrics and offering insights across sectors and regions. While not infallible, their role in modern finance is undeniable.

For traders, analysts, and policymakers alike, these indices are more than numbers on a screen—they are reflections of the market’s collective psyche, guiding decisions in times of both calm and crisis.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Silver occupies a distinctive position within the realm of investment assets, functioning simultaneously as a precious metal and an industrial commodity. This dual nature imbues silver with characteristics that make it a valuable component of a diversified portfolio, offering both defensive qualities and growth potential. While its volatility necessitates careful consideration, silver’s unique attributes warrant attention from investors seeking balance between risk mitigation and opportunity.

Silver as a Hybrid Asset

Unlike gold, which is primarily regarded as a store of value, silver derives a substantial portion of its demand from industrial applications. It is indispensable in sectors such as electronics, renewable energy, and medical technology, with photovoltaic cells in solar panels representing a particularly significant driver of consumption. This industrial utility ensures that silver’s price is influenced not only by macroeconomic uncertainty but also by technological innovation and global manufacturing trends. Consequently, silver provides investors with exposure to both traditional safe-haven dynamics and cyclical industrial growth.

Accessibility and Cost Efficiency

Silver’s affordability relative to gold enhances its appeal to a broad spectrum of investors. Physical silver, in the form of coins and bars, allows individuals with modest capital to participate in the precious metals market. Moreover, financial instruments such as exchange-traded funds (ETFs) and mining equities provide liquid and scalable avenues for investment. This accessibility ensures that silver can serve as an entry point into alternative assets, particularly for those seeking to hedge against inflation without committing substantial resources.

Inflation Hedge and Currency Protection

Historically, silver has demonstrated resilience during periods of inflation and currency depreciation. As fiat currencies lose purchasing power, tangible assets such as silver tend to appreciate, preserving wealth for investors. Although gold is often considered the primary hedge, silver’s similar properties, combined with its lower cost, render it a practical complement. In times of geopolitical instability or monetary expansion, silver can function as a safeguard against systemic risks.

Volatility and Associated Risks

Despite its advantages, silver is characterized by pronounced price volatility. Its smaller market size relative to gold renders it more susceptible to speculative trading and abrupt shifts in investor sentiment. Furthermore, fluctuations in industrial demand can amplify short-term price movements. While this volatility can generate significant returns, it also exposes investors to heightened risk. Accordingly, silver is best employed as a long-term holding within a diversified portfolio rather than as a vehicle for short-term speculation.

Portfolio Diversification and Investment Vehicles

Incorporating silver into a portfolio enhances diversification by introducing an asset class with low correlation to equities and fixed income securities. This non-correlation reduces overall portfolio risk and provides stability during market downturns. Investors may access silver through several channels: physical bullion for tangible ownership, ETFs for liquidity, mining stocks for leveraged exposure, and futures contracts for advanced strategies. Each vehicle entails distinct risk-reward profiles, enabling investors to tailor their approach according to objectives and tolerance.

Conclusion

Silver’s dual identity as both a precious metal and an industrial commodity distinguishes it from other investment assets. Its affordability, inflation-hedging capacity, and diversification benefits make it a compelling addition to portfolios. While volatility requires prudent management, silver’s potential to balance defensive and growth-oriented strategies underscores its enduring relevance in contemporary investment practice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

The velocity of money is a fundamental concept in macroeconomics that measures how quickly money circulates through the economy. It reflects the frequency with which a unit of currency is used to purchase goods and services within a given time period. This metric is crucial for understanding economic activity, inflation, and the effectiveness of monetary policy.

At its core, the velocity of money is calculated using the formula:

This equation shows how many times money turns over in the economy to support a given level of economic output. For example, if the GDP is $20 trillion and the money supply (say, M2) is $10 trillion, the velocity is 2—meaning each dollar is used twice in a year to purchase goods and services.

There are different measures of money supply used in this calculation, most commonly M1 and M2. M1 includes the most liquid forms of money, such as cash and checking deposits, while M2 includes M1 plus savings accounts and other near-money assets. The choice of which measure to use depends on the context and the specific economic analysis being conducted.

The velocity of money is influenced by several factors:

Consumer and business confidence: When people feel optimistic about the economy, they are more likely to spend rather than save, increasing velocity.

Interest rates: Higher interest rates can encourage saving and reduce spending, lowering velocity. Conversely, lower rates can stimulate borrowing and spending.

Inflation expectations: If people expect prices to rise, they may spend more quickly, increasing velocity.

Technological and structural changes: Innovations in digital payments and shifts in consumer behavior can also affect how quickly money moves.

Historically, the velocity of money has fluctuated with economic cycles. During periods of economic expansion, velocity tends to rise as spending increases. In contrast, during recessions or periods of uncertainty, velocity often falls as consumers and businesses hold onto cash. For instance, during the 2008 financial crisis and the early stages of the COVID-19 pandemic, velocity dropped sharply due to reduced consumer spending and increased saving.

In recent years, the U.S. has experienced persistently low velocity, even amid significant increases in the money supply. This phenomenon has puzzled economists and raised questions about the effectiveness of monetary policy. Despite aggressive stimulus measures, much of the new money has remained in savings or financial markets rather than circulating through the real economy.

Understanding the velocity of money is essential for policymakers. A low velocity may signal weak demand and justify expansionary fiscal or monetary policies. Conversely, a high velocity could indicate overheating and the need for tightening measures to prevent inflation.

In conclusion, the velocity of money is a dynamic indicator of economic vitality. It helps economists and central banks assess the flow of money, the strength of demand, and the potential for inflation.

While often overlooked by the public, it plays a vital role in shaping economic policy and understanding the broader health of the economy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

For generations, the prevailing belief in healthcare has been that physicians [MD, DO and DPM], with their high salaries and prestige, inevitably retire wealthier than nurses. Yet this assumption overlooks the financial realities of different nursing specialties and the long‑term impact of debt, lifestyle, and retirement planning. In fact, some Registered Nurses (RNs)—particularly Certified Registered Nurse Anesthetists (CRNAs), visiting nurses, and those who participate in structured pay programs like the Baylor plan—can retire richer than physicians. The reasons lie in the interplay of education costs, career flexibility, income potential, and disciplined financial planning.

Education Costs and Debt Burden

One of the most decisive factors shaping retirement wealth is the cost of education. Physicians often spend over a decade in training, including undergraduate studies, medical school, and residency. This path not only delays their earning years but also saddles them with substantial student debt. The median medical school debt in the United States exceeds $200,000, and many physicians spend years paying it down.

By contrast, RNs typically complete their training in two to four years, with advanced practice nurses such as CRNAs requiring graduate‑level education. Even so, their debt burden is far lighter, often less than half of what physicians carry. This difference means nurses can begin earning earlier, save for retirement sooner, and avoid the crushing interest payments that erode physicians’ wealth. A CRNA who starts practicing in their late twenties may already be investing in retirement accounts while a physician is still in residency earning a modest stipend.

Income Potential of Specialized Nurses

While physicians generally earn more annually than nurses, the gap is narrower in certain specialties. CRNAs, for example, are among the highest‑paid nursing professionals, with average salaries often exceeding $200,000 per year. This places them in direct competition with some physician specialties, especially primary care doctors, who may earn similar or even lower salaries.

Visiting nurses also benefit from unique financial advantages. Many work on flexible schedules, contract arrangements, or per‑visit compensation models. This allows them to maximize income while minimizing burnout. By avoiding the overhead costs of private practice and the administrative burdens physicians face, visiting nurses can channel more of their earnings directly into savings and investments.

When combined with lower debt and earlier career starts, these income streams can compound into significant retirement wealth.

The Baylor plan, a structured pay program used by some hospitals, allows nurses to work full‑time hours compressed into fewer days—often weekends—while still receiving full‑time pay and benefits. This arrangement provides several financial advantages. First, it enables nurses to earn competitive wages while freeing up weekdays for additional work, education, or entrepreneurial ventures. Second, it reduces commuting and childcare costs, allowing more income to be saved. Third, the plan often includes robust retirement benefits, such as employer‑matched contributions to 401(k) or pension programs.

Nurses who consistently participate in such structured pay plans can accumulate substantial nest eggs, often surpassing physicians who delay retirement savings due to debt repayment or lifestyle inflation. The Baylor plan highlights the importance of systematic investing: by automating contributions and focusing on long‑term growth, nurses can harness the power of compound interest. A nurse who invests steadily for 35 years may accumulate more wealth than a physician who begins saving late and inconsistently, despite earning a higher salary.

Lifestyle and Work‑Life Balance

Another overlooked factor is lifestyle. Physicians often face grueling schedules, high stress, and the temptation to maintain expensive lifestyles commensurate with their social status. Luxury homes, cars, and vacations can erode their financial base. Nurses, while not immune to lifestyle inflation, often maintain more modest spending habits.

Visiting nurses, in particular, enjoy flexibility that allows them to balance work with personal life. This reduces burnout and healthcare costs while enabling consistent employment into later years. By living within their means and prioritizing savings, nurses can accumulate wealth steadily without the financial pitfalls that sometimes accompany physician lifestyles.

Retirement Wealth Beyond Salary

Retirement wealth is not solely determined by annual income. It is shaped by debt management, savings discipline, investment strategies, and lifestyle choices. Nurses who leverage high‑paying specialties like anesthesia, flexible arrangements like visiting nursing, and structured programs like the Baylor plan can outperform physicians in these areas.

Consider two professionals: a physician earning $250,000 annually but burdened by $200,000 in debt and high living expenses, and a CRNA earning $200,000 with minimal debt and disciplined savings. Over decades, the CRNA may accumulate more net wealth, retire earlier, and enjoy greater financial security.

Conclusion

The assumption that physicians always retire richer than nurses is outdated. While physicians command higher salaries, their delayed earnings, heavy debt, and lifestyle pressures often undermine long‑term wealth. Nurses, particularly CRNAs, visiting nurses, and those who participate in structured pay programs like the Baylor plan, can retire wealthier by combining lower debt, earlier savings, competitive incomes, and disciplined financial planning.

Ultimately, retirement wealth is not about prestige but about strategy. Nurses who recognize this truth and act accordingly may find themselves enjoying more financial freedom than the very physicians they once assisted.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Say’s Law, named after the French economist Jean‑Baptiste Say, is a foundational idea in classical economics. Often summarized as “supply creates its own demand,” the law suggests that the act of producing goods and services inherently generates the income necessary to purchase them. This principle shaped economic thought throughout the 19th century and continues to influence debates about markets, government intervention, and the causes of economic crises.

Origins and Meaning Jean‑Baptiste Say introduced his law in the early 1800s in his Treatise on Political Economy. He argued that production is the source of demand: when producers create goods, they pay wages, rents, and profits, which in turn become purchasing power. In this view, general overproduction is impossible because every supply of goods corresponds to an equivalent demand. If imbalances occur, they are temporary and limited to specific sectors, not the economy as a whole.

Core Principles Say’s Law rests on several assumptions:

Markets are self‑correcting: Any surplus in one area leads to adjustments in prices and production.

Money is neutral: It serves only as a medium of exchange, not as a driver of demand.

Production drives prosperity: Economic growth depends on increasing output, not stimulating consumption.

No long‑term unemployment: Since supply creates demand, workers displaced in one industry will eventually find employment elsewhere.

These ideas aligned with classical economists’ belief in minimal government intervention and the efficiency of free markets.

Influence on Classical Economics Say’s Law became a cornerstone of classical economics, reinforcing the belief that recessions or depressions were temporary and self‑correcting. Economists like David Ricardo and John Stuart Mill adopted versions of the law, using it to argue against policies aimed at stimulating demand. The law supported laissez‑faire approaches, suggesting that governments should avoid interfering with markets, as production itself would ensure economic balance.

Criticism and Keynesian Revolution Say’s Law faced its greatest challenge during the Great Depression of the 1930s. Widespread unemployment and idle factories contradicted the idea that supply automatically generates demand. John Maynard Keynes famously rejected Say’s Law in his General Theory of Employment, Interest, and Money (1936). Keynes argued that demand, not supply, drives economic activity. He showed that insufficient aggregate demand could lead to prolonged recessions, requiring government intervention through fiscal and monetary policies.

Keynes’s critique marked a turning point in economics. While Say’s Law emphasized production, Keynesian economics highlighted consumption and demand management. This shift reshaped economic policy, leading to active government roles in stabilizing economies.

Modern Perspectives Today, Say’s Law is not accepted in its original form, but elements of it remain relevant. Supply‑side economists, for example, argue that policies encouraging production—such as tax cuts and deregulation—can stimulate growth. In contrast, Keynesians stress the importance of demand management. The debate reflects a broader tension in economics: whether prosperity depends more on producing goods or ensuring people have the means and willingness to buy them.

Conclusion: Say’s Law was a bold attempt to explain the self‑sustaining nature of markets. While its claim that “supply creates its own demand” proved too simplistic in the face of modern economic realities, it remains a vital part of the history of economic thought. The controversy surrounding Say’s Law highlights the evolving nature of economics, where theories are tested against real‑world crises and adapted to new circumstances. Even today, discussions of supply‑side versus demand‑side policies echo the enduring influence of Say’s original insight.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The singularity promises to revolutionize medicine by accelerating diagnostics, treatment, and longevity—but it also demands ethical vigilance and systemic transformation.

The concept of the technological singularity refers to a hypothetical future moment when artificial intelligence (AI) surpasses human intelligence, triggering exponential advances in technology. In medicine, this could mark a turning point where AI-driven systems outperform human clinicians in diagnosis, treatment planning, and even biomedical research. While the singularity remains speculative, its implications for healthcare are profound and multifaceted.

One of the most promising impacts is in diagnostics and precision medicine. AI systems trained on vast datasets of medical images, genetic profiles, and patient histories could detect diseases earlier and more accurately than human doctors. For example, algorithms already outperform radiologists in identifying certain cancers from imaging scans. As we approach the singularity, these systems may evolve into autonomous diagnostic agents capable of real-time analysis and personalized recommendations, tailored to each patient’s unique biology.

Another transformative area is drug discovery and development. Traditional pharmaceutical research is slow and costly, often taking over a decade to bring a new drug to market. AI could dramatically shorten this timeline by simulating molecular interactions, predicting therapeutic targets, and optimizing clinical trial designs. With superintelligent systems, the pace of innovation could accelerate to the point where treatments for currently incurable diseases—like Alzheimer’s or certain cancers—become feasible within months.

The singularity also opens doors to radical longevity and human enhancement. Advances in nanotechnology, genomics, and regenerative medicine may converge to extend human lifespan significantly. AI could help decode the aging process, identify biomarkers of cellular decline, and engineer interventions that slow or reverse it. Some theorists even envision a future where aging is treated as a curable condition, and mortality becomes a choice rather than a biological inevitability.

However, these breakthroughs come with serious ethical and societal challenges. Data privacy, algorithmic bias, and access inequality are critical concerns. If singularity-level AI is controlled by a few corporations or governments, it could exacerbate global health disparities. Moreover, the replacement of human clinicians with machines raises questions about empathy, trust, and accountability in care. Who is responsible when an AI makes a life-altering mistake?

To navigate this future responsibly, medicine must embrace interdisciplinary collaboration. Ethicists, technologists, clinicians, and policymakers must work together to ensure that AI systems are transparent, equitable, and aligned with human values. Regulatory frameworks must evolve to keep pace with innovation, and medical education must prepare practitioners to work alongside intelligent machines.

In conclusion, the singularity represents both a promise and a peril for medicine. It offers unprecedented opportunities to enhance human health, but also demands careful stewardship to avoid unintended consequences.

As we edge closer to this horizon, the challenge will be not just technological, but deeply human: to harness intelligence beyond our own in service of healing, compassion, and justice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Money is a powerful tool. It can provide security, open opportunities, and help build a fulfilling life. Yet, when mismanaged, it can quickly become a source of stress and regret. Understanding the worst ways to use money is essential for anyone who wants to avoid financial pitfalls and build lasting stability.

1. Impulse Spending

One of the most damaging habits is spending without thought. Buying items on impulse—whether it’s clothes, gadgets, or luxury goods—often leads to regret and wasted resources. These purchases rarely align with long‑term goals and can drain savings meant for emergencies or investments.

2. High‑Interest Debt

Credit cards and payday loans can trap people in cycles of debt. Paying 20% or more in interest means that even small purchases balloon into massive financial burdens. Using debt irresponsibly is one of the fastest ways to erode wealth.

3. Ignoring Savings and Investments

Failing to save for the future is another critical mistake. Without an emergency fund, unexpected expenses like medical bills or car repairs can derail financial stability. Similarly, neglecting investments means missing out on compound growth that builds wealth over time.

4. Chasing Get‑Rich‑Quick Schemes

From pyramid schemes to speculative “hot tips,” chasing unrealistic returns is a recipe for disaster. These schemes prey on greed and impatience, often leaving participants with nothing but losses. Sustainable wealth comes from patience and discipline, not shortcuts.

5. Overspending on Status

Many people waste money trying to impress others—buying luxury cars, designer clothes, or extravagant experiences they cannot afford. This pursuit of status often leads to debt and financial insecurity, while providing only fleeting satisfaction.

6. Neglecting Insurance

Skipping health, auto, or home insurance to save money may seem smart in the short term, but it can be catastrophic when disaster strikes. Without protection, one accident or emergency can wipe out years of savings.

7. Failing to Budget

Living without a plan is like sailing without a map. Without a budget, it’s easy to overspend, miss bills, or fail to allocate money toward goals. Budgeting is not restrictive—it’s empowering, because it ensures money is used intentionally.

8. Ignoring Education and Skills

Spending money without investing in personal growth is another hidden mistake. Education, training, and skill development often yield lifelong returns. Neglecting these opportunities can limit earning potential and financial independence.

Conclusion

The worst things to do with money often stem from short‑term thinking, lack of discipline, or the desire for instant gratification. Impulse spending, high‑interest debt, chasing schemes, and neglecting savings all undermine financial health. By avoiding these traps and focusing on budgeting, investing wisely, and protecting against risks, money can serve as a foundation for security and freedom rather than a source of stress.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***