BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on December 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko; MBA MEd

***

***

The 50/30/20 budgeting rule is a widely embraced personal finance strategy that offers a straightforward framework for managing income. This rule divides after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Its simplicity and flexibility make it an ideal starting point for individuals seeking financial stability and long-term growth.

🏠 50% for Needs

The first category, “needs,” encompasses essential expenses that are non-negotiable for daily living. These include housing costs (rent or mortgage), utilities, groceries, transportation, insurance, and minimum loan payments. The goal is to keep these necessities within half of one’s income to avoid financial strain. If needs exceed 50%, it may signal the need to reassess lifestyle choices—such as downsizing housing or reducing commuting costs—to maintain balance.

🎉 30% for Wants

“Wants” refer to discretionary spending—things that enhance life but aren’t essential. Dining out, entertainment, travel, hobbies, and luxury purchases fall into this category. This portion of the budget allows for enjoyment and personal fulfillment, which is crucial for mental well-being. However, distinguishing between wants and needs can be tricky. For example, a basic phone plan is a need, but the latest smartphone upgrade is a want. Practicing mindful spending helps ensure this category doesn’t encroach on essentials or savings.

💰 20% for Savings and Debt Repayment

The final 20% is allocated to financial growth and security. This includes building an emergency fund, contributing to retirement accounts, investing, and paying off debts beyond minimum payments. Prioritizing this category helps individuals prepare for unexpected expenses and achieve long-term goals like homeownership or early retirement. For those with high-interest debt, allocating more of this portion toward repayment can yield significant financial benefits over time.

📊 Benefits of the 50/30/20 Rule

One of the rule’s greatest strengths is its simplicity. Unlike complex budgeting systems that require meticulous tracking of every expense, the 50/30/20 rule offers a high-level view that’s easy to implement and maintain. It’s also adaptable—users can tweak percentages based on personal circumstances. For instance, someone aggressively saving for a home might shift to a 40/20/40 model temporarily.

Moreover, this rule promotes financial discipline without sacrificing enjoyment. By clearly defining boundaries for spending, it encourages intentional choices and reduces impulsive purchases. It also fosters a habit of saving, which is often overlooked in traditional budgeting approaches.

🧭 Conclusion

The 50/30/20 budgeting rule is a powerful tool for anyone seeking to take control of their finances. Its balanced approach ensures that essential needs are met, personal desires are fulfilled, and future goals are actively pursued. Whether you’re just starting your financial journey or looking to simplify your budget, this rule offers a clear, effective roadmap to financial wellness.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on December 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

🎄 Introduction

The holiday season has long been synonymous with heightened consumer spending, as families allocate budgets for gifts, travel, food, and entertainment. In 2025, however, this tradition is unfolding against a backdrop of inflation, rising living costs, and shifting consumer priorities. While spending remains robust in certain segments, the overall picture reveals a more complex and cautious approach to holiday consumption.

📊 Spending Trends

Overall increase in spending: According to KPMG, consumers expect to spend 4.6% more than last year, though this rise is largely attributed to higher prices rather than stronger financial positions.

Income disparities: Higher‑income households are driving most of the gains, while lower‑income families anticipate cutting back.

Decline in discretionary spending: Growth in discretionary purchases is minimal, with real buying power declining.

Generational differences: Younger generations, especially Gen Z, plan to reduce holiday spending, reflecting financial strain and shifting values.

Gift spending contraction: Average gift spending is expected to drop, signaling a move toward more practical or meaningful purchases.

🛍️ Shopping Behavior

Timing of purchases: Many consumers are delaying shopping, avoiding the traditional early‑season surge.

Digital vs. physical stores: Online shopping continues to grow, but physical stores remain critical for driving results.

Technology in discovery: Tools powered by artificial intelligence are reshaping holiday shopping, helping consumers find deals and products more efficiently.

Concentration of spending: A large share of gift purchases occurs between Thanksgiving and Cyber Monday, reflecting the importance of promotional events.

🎁 Shifts in Priorities

Focus on essentials: Consumers are prioritizing tangible goods and essentials over luxury or experiential items.

Value‑driven choices: Shoppers are seeking value and meaning, often opting for fewer but more thoughtful gifts.

Travel and self‑spending: Many households are allocating more budget for travel and personal indulgence, even as they cut back on gifts.

🌍 Broader Implications

Holiday spending trends highlight the tension between tradition and economic reality. Retailers face challenges in predicting demand, as consumer sentiment remains cautious. Marketing strategies are shifting toward digital platforms, social media, and personalized promotions. For policymakers and economists, these spending patterns serve as indicators of household confidence and broader economic health.

🎯 Conclusion

In summary, consumer spending during the holiday season is marked by uneven growth, generational shifts, and a stronger emphasis on essentials and value. While higher‑income households sustain overall spending levels, many others are scaling back, reflecting the pressures of inflation and rising costs. The season remains festive, but it is increasingly defined by careful budgeting, strategic shopping, and evolving consumer values.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

For generations, the prevailing belief in healthcare has been that physicians [MD, DO and DPM], with their high salaries and prestige, inevitably retire wealthier than nurses. Yet this assumption overlooks the financial realities of different nursing specialties and the long‑term impact of debt, lifestyle, and retirement planning. In fact, some Registered Nurses (RNs)—particularly Certified Registered Nurse Anesthetists (CRNAs), visiting nurses, and those who participate in structured pay programs like the Baylor plan—can retire richer than physicians. The reasons lie in the interplay of education costs, career flexibility, income potential, and disciplined financial planning.

Education Costs and Debt Burden

One of the most decisive factors shaping retirement wealth is the cost of education. Physicians often spend over a decade in training, including undergraduate studies, medical school, and residency. This path not only delays their earning years but also saddles them with substantial student debt. The median medical school debt in the United States exceeds $200,000, and many physicians spend years paying it down.

By contrast, RNs typically complete their training in two to four years, with advanced practice nurses such as CRNAs requiring graduate‑level education. Even so, their debt burden is far lighter, often less than half of what physicians carry. This difference means nurses can begin earning earlier, save for retirement sooner, and avoid the crushing interest payments that erode physicians’ wealth. A CRNA who starts practicing in their late twenties may already be investing in retirement accounts while a physician is still in residency earning a modest stipend.

Income Potential of Specialized Nurses

While physicians generally earn more annually than nurses, the gap is narrower in certain specialties. CRNAs, for example, are among the highest‑paid nursing professionals, with average salaries often exceeding $200,000 per year. This places them in direct competition with some physician specialties, especially primary care doctors, who may earn similar or even lower salaries.

Visiting nurses also benefit from unique financial advantages. Many work on flexible schedules, contract arrangements, or per‑visit compensation models. This allows them to maximize income while minimizing burnout. By avoiding the overhead costs of private practice and the administrative burdens physicians face, visiting nurses can channel more of their earnings directly into savings and investments.

When combined with lower debt and earlier career starts, these income streams can compound into significant retirement wealth.

The Baylor plan, a structured pay program used by some hospitals, allows nurses to work full‑time hours compressed into fewer days—often weekends—while still receiving full‑time pay and benefits. This arrangement provides several financial advantages. First, it enables nurses to earn competitive wages while freeing up weekdays for additional work, education, or entrepreneurial ventures. Second, it reduces commuting and childcare costs, allowing more income to be saved. Third, the plan often includes robust retirement benefits, such as employer‑matched contributions to 401(k) or pension programs.

Nurses who consistently participate in such structured pay plans can accumulate substantial nest eggs, often surpassing physicians who delay retirement savings due to debt repayment or lifestyle inflation. The Baylor plan highlights the importance of systematic investing: by automating contributions and focusing on long‑term growth, nurses can harness the power of compound interest. A nurse who invests steadily for 35 years may accumulate more wealth than a physician who begins saving late and inconsistently, despite earning a higher salary.

Lifestyle and Work‑Life Balance

Another overlooked factor is lifestyle. Physicians often face grueling schedules, high stress, and the temptation to maintain expensive lifestyles commensurate with their social status. Luxury homes, cars, and vacations can erode their financial base. Nurses, while not immune to lifestyle inflation, often maintain more modest spending habits.

Visiting nurses, in particular, enjoy flexibility that allows them to balance work with personal life. This reduces burnout and healthcare costs while enabling consistent employment into later years. By living within their means and prioritizing savings, nurses can accumulate wealth steadily without the financial pitfalls that sometimes accompany physician lifestyles.

Retirement Wealth Beyond Salary

Retirement wealth is not solely determined by annual income. It is shaped by debt management, savings discipline, investment strategies, and lifestyle choices. Nurses who leverage high‑paying specialties like anesthesia, flexible arrangements like visiting nursing, and structured programs like the Baylor plan can outperform physicians in these areas.

Consider two professionals: a physician earning $250,000 annually but burdened by $200,000 in debt and high living expenses, and a CRNA earning $200,000 with minimal debt and disciplined savings. Over decades, the CRNA may accumulate more net wealth, retire earlier, and enjoy greater financial security.

Conclusion

The assumption that physicians always retire richer than nurses is outdated. While physicians command higher salaries, their delayed earnings, heavy debt, and lifestyle pressures often undermine long‑term wealth. Nurses, particularly CRNAs, visiting nurses, and those who participate in structured pay programs like the Baylor plan, can retire wealthier by combining lower debt, earlier savings, competitive incomes, and disciplined financial planning.

Ultimately, retirement wealth is not about prestige but about strategy. Nurses who recognize this truth and act accordingly may find themselves enjoying more financial freedom than the very physicians they once assisted.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Money is a powerful tool. It can provide security, open opportunities, and help build a fulfilling life. Yet, when mismanaged, it can quickly become a source of stress and regret. Understanding the worst ways to use money is essential for anyone who wants to avoid financial pitfalls and build lasting stability.

1. Impulse Spending

One of the most damaging habits is spending without thought. Buying items on impulse—whether it’s clothes, gadgets, or luxury goods—often leads to regret and wasted resources. These purchases rarely align with long‑term goals and can drain savings meant for emergencies or investments.

2. High‑Interest Debt

Credit cards and payday loans can trap people in cycles of debt. Paying 20% or more in interest means that even small purchases balloon into massive financial burdens. Using debt irresponsibly is one of the fastest ways to erode wealth.

3. Ignoring Savings and Investments

Failing to save for the future is another critical mistake. Without an emergency fund, unexpected expenses like medical bills or car repairs can derail financial stability. Similarly, neglecting investments means missing out on compound growth that builds wealth over time.

4. Chasing Get‑Rich‑Quick Schemes

From pyramid schemes to speculative “hot tips,” chasing unrealistic returns is a recipe for disaster. These schemes prey on greed and impatience, often leaving participants with nothing but losses. Sustainable wealth comes from patience and discipline, not shortcuts.

5. Overspending on Status

Many people waste money trying to impress others—buying luxury cars, designer clothes, or extravagant experiences they cannot afford. This pursuit of status often leads to debt and financial insecurity, while providing only fleeting satisfaction.

6. Neglecting Insurance

Skipping health, auto, or home insurance to save money may seem smart in the short term, but it can be catastrophic when disaster strikes. Without protection, one accident or emergency can wipe out years of savings.

7. Failing to Budget

Living without a plan is like sailing without a map. Without a budget, it’s easy to overspend, miss bills, or fail to allocate money toward goals. Budgeting is not restrictive—it’s empowering, because it ensures money is used intentionally.

8. Ignoring Education and Skills

Spending money without investing in personal growth is another hidden mistake. Education, training, and skill development often yield lifelong returns. Neglecting these opportunities can limit earning potential and financial independence.

Conclusion

The worst things to do with money often stem from short‑term thinking, lack of discipline, or the desire for instant gratification. Impulse spending, high‑interest debt, chasing schemes, and neglecting savings all undermine financial health. By avoiding these traps and focusing on budgeting, investing wisely, and protecting against risks, money can serve as a foundation for security and freedom rather than a source of stress.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Life Cycle Hypothesis (LCH) is a foundational theory in economics and personal finance that explains how individuals plan their consumption and savings behavior over the course of their lives. Developed in the 1950s by economists Franco Modigliani and Richard Brumberg, the LCH posits that people aim to smooth their consumption throughout their lifetime, regardless of fluctuations in income. This theory has had a profound impact on how economists, financial planners, and policymakers understand saving patterns, retirement planning, and fiscal policy.

At its core, the LCH assumes that individuals are forward-looking and rational. They anticipate changes in income—such as those caused by retirement, unemployment, or career progression—and adjust their saving and spending accordingly. During high-income periods, typically in mid-career, individuals save more to prepare for low-income phases, such as retirement. Conversely, in early adulthood and old age, when income is lower, individuals are expected to dissave, or spend from their accumulated savings.

One of the key insights of the LCH is that consumption is not directly tied to current income but rather to expected lifetime income. This means that temporary changes in income should not significantly affect consumption patterns, as individuals base their spending decisions on long-term expectations. For example, a young professional may take out a loan to buy a car, anticipating higher future earnings that will allow them to repay the debt without drastically altering their lifestyle.

The LCH also provides a framework for understanding the role of pensions, social security, and other retirement savings mechanisms. By recognizing that individuals need to save during their working years to maintain consumption levels in retirement, the theory supports the development of policies that encourage long-term savings and financial literacy. It also helps explain why some people may under-save or over-consume if they misjudge their future income or lack access to financial planning resources.

Despite its elegance, the Life Cycle Hypothesis has faced criticism and refinement. Behavioral economists argue that individuals are not always rational and may struggle with self-control, procrastination, or lack of financial knowledge. These limitations have led to the development of the Behavioral Life Cycle Hypothesis, which incorporates psychological factors such as mental accounting and framing effects. Moreover, empirical studies have shown that many people do not smooth consumption as predicted, often due to liquidity constraints, uncertainty, or cultural influences.

Nevertheless, the LCH remains a powerful tool for analyzing financial behavior across different stages of life. It has influenced retirement planning strategies, tax policy, and the design of financial products. By emphasizing the importance of long-term planning and the intertemporal nature of financial decisions, the Life Cycle Hypothesis continues to shape how individuals and institutions approach economic well-being.

In conclusion, the Life Cycle Hypothesis offers a compelling lens through which to view personal finance. While it may not capture every nuance of human behavior, its emphasis on lifetime income and consumption smoothing provides a valuable foundation for understanding and improving financial decision-making.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Turning 50 with little to no savings can be daunting, especially for a doctor who has spent decades in a demanding profession. Yet, all is not lost. With strategic planning, discipline, and a willingness to adapt, a broke 50-year-old physician can still build a solid retirement foundation by age 65.

First, it’s essential to confront the financial reality. This means calculating current income, expenses, debts, and any assets, however small. A clear picture allows for realistic goal-setting. The target should be to save aggressively—ideally 30–50% of income—over the next 15 years. While this may seem steep, doctors often have above-average earning potential, even in their later years, which can be leveraged.

Next, lifestyle adjustments are crucial. Downsizing housing, eliminating unnecessary expenses, and avoiding new debt can free up significant cash flow. If possible, relocating to a lower-cost area or refinancing existing loans can also help. Every dollar saved should be redirected into retirement accounts such as a 401(k), IRA, or a solo 401(k) if self-employed. Catch-up contributions for those over 50 allow for higher annual deposits, which can accelerate growth.

Investing wisely is non-negotiable. A diversified portfolio with a mix of stocks, bonds, and alternative assets can provide both growth and stability. Working with a fiduciary financial advisor ensures that investments align with retirement goals and risk tolerance. Time is limited, so the focus should be on maximizing returns without taking reckless risks.

Increasing income is another powerful lever. Many doctors can boost earnings through side gigs like telemedicine, consulting, teaching, or locum tenens work. These flexible options can add tens of thousands annually without requiring a full career shift. Additionally, monetizing expertise—writing, speaking, or creating online courses—can generate passive income streams.

Debt reduction must be prioritized. High-interest loans, especially credit card debt, can erode savings potential. Paying off these balances aggressively while avoiding new liabilities is key. For student loans, exploring forgiveness programs or refinancing options may offer relief.

Finally, mindset matters. Retirement at 65 doesn’t have to mean complete cessation of work. It can mean transitioning to part-time roles, passion projects, or advisory positions that provide income and fulfillment. The goal is financial independence, not necessarily total inactivity.

In conclusion, while starting late is challenging, a broke 50-year-old doctor can still retire comfortably at 65. It requires a blend of financial discipline, income optimization, smart investing, and lifestyle changes. With focus and determination, the next 15 years can be transformative—turning a precarious situation into a secure and dignified retirement.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

What Medical School Didn’t Teach Doctors About Money

Medical school is designed to mold students into competent, compassionate physicians. It teaches anatomy, pathology, pharmacology, and clinical skills with precision and rigor. Yet, despite the depth of medical knowledge imparted, one critical area is often overlooked: financial literacy. For many doctors, the transition from student to professional comes with a steep learning curve—not in medicine, but in money. From managing debt to understanding taxes, investing, and retirement planning, medical school leaves a financial education gap that can have long-term consequences.

The Debt Dilemma

One of the most glaring omissions in medical education is how to manage student loan debt. The average medical student graduates with over $200,000 in debt, yet few are taught how to navigate repayment options, interest accrual, or loan forgiveness programs. Many doctors enter residency with little understanding of income-driven repayment plans or Public Service Loan Forgiveness (PSLF), missing opportunities to reduce their financial burden. Without guidance, some make costly mistakes—such as refinancing federal loans prematurely or choosing repayment plans that don’t align with their career trajectory.

Income ≠ Wealth

Medical students often assume that a high salary will automatically lead to financial security. While physicians do earn more than most professionals, income alone doesn’t guarantee wealth. Medical school rarely addresses the importance of budgeting, saving, and investing. As a result, many doctors fall into the “HENRY” trap—High Earner, Not Rich Yet. They spend lavishly, assuming their income will always cover expenses, only to find themselves living paycheck to paycheck. Without a solid financial foundation, even high earners can struggle to build net worth.

***

***

Taxes and Business Skills

Doctors are also unprepared for the complexities of taxes. Whether employed by a hospital or running a private practice, physicians face unique tax challenges. Medical school doesn’t teach how to track deductible expenses, optimize retirement contributions, or navigate self-employment taxes. For those who open their own clinics, the lack of business education is even more pronounced. Understanding profit margins, payroll, insurance billing, and compliance regulations is essential—but rarely covered in medical training.

Investing and Retirement Planning

Another blind spot is investing. Medical students are rarely taught the basics of compound interest, asset allocation, or retirement accounts. Many don’t know the difference between a Roth IRA and a traditional 401(k), or how to evaluate mutual funds and index funds. This lack of knowledge delays retirement planning and can lead to missed opportunities for long-term growth. Some doctors rely on financial advisors without understanding the fees or conflicts of interest involved, putting their wealth at risk.

Insurance and Risk Management

Medical school also fails to educate students on insurance—life, disability, malpractice, and health. Doctors need robust coverage to protect their income and assets, but many don’t know how to evaluate policies or understand terms like “own occupation” or “elimination period.” Inadequate coverage can leave physicians vulnerable to financial disaster in the event of illness, injury, or litigation.

Emotional and Behavioral Finance

Beyond technical knowledge, medical school overlooks the emotional side of money. Physicians often face pressure to maintain a certain lifestyle, especially after years of sacrifice. The desire to “catch up” can lead to impulsive spending, luxury purchases, and financial stress. Without tools to manage money mindset and behavioral habits, doctors may struggle with guilt, anxiety, or burnout related to finances.

The Case for Financial Education

Fortunately, awareness of this gap is growing. Organizations like Medics’ Money and podcasts such as “Docs Outside the Box” are working to fill the void by offering financial education tailored to physicians.

These resources cover everything from budgeting and debt management to investing and entrepreneurship. Some medical schools are beginning to incorporate financial literacy into their curricula, but progress is slow and inconsistent.

Conclusion

Medical school equips doctors to save lives, but it doesn’t prepare them to secure their own financial future. The lack of financial education leaves many physicians vulnerable to debt, poor investment decisions, and lifestyle inflation. To thrive both professionally and personally, doctors must seek out financial knowledge beyond the classroom. Whether through self-study, mentorship, or professional guidance, understanding money is as essential as understanding medicine. After all, financial health is a cornerstone of overall well-being—and every doctor deserves to master both.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Turning 65 is often seen as the gateway to retirement—a time to slow down, reflect, and enjoy the fruits of decades of labor. But for some, including doctors who may have faced financial setbacks, poor planning, or unexpected life events, reaching this milestone without financial security can be deeply unsettling. The image of a broke 65-year-old doctor may seem paradoxical, given the profession’s reputation for high earnings. Yet, reality paints a more nuanced picture. Fortunately, even in the face of financial hardship, retirement is not a closed door—it’s a challenge that can be met with creativity, resilience, and strategic planning.

Understanding the Situation

Before exploring solutions, it’s important to understand how a physician might arrive at retirement age without adequate savings. Medical school debt, late career starts, divorce, health issues, poor investment decisions, or supporting family members can all contribute. Some doctors work in lower-paying specialties or underserved areas, sacrificing income for impact. Others may have lived beyond their means, assuming their high salary would always be enough. Regardless of the cause, the key is to shift focus from regret to action.

Traditional retirement—ceasing work entirely—is not the only option. For a broke 65-year-old doctor, retirement may mean transitioning to a less demanding role, reducing hours, or shifting to a new field. The goal is to create a sustainable lifestyle that balances income, purpose, and well-being.

Leveraging Medical Expertise

Even if full-time clinical practice is no longer viable, a physician’s knowledge remains valuable. Here are several ways to continue earning while easing into retirement:

Telemedicine: Remote consultations are in high demand, especially in primary care, psychiatry, and chronic disease management. Telemedicine offers flexibility, reduced overhead, and the ability to work from home.

Locum Tenens: Temporary assignments can fill staffing gaps in hospitals and clinics. These roles often pay well and allow for travel or seasonal work.

Medical Writing and Reviewing: Physicians can write for journals, websites, or pharmaceutical companies. Peer reviewing, editing, and content creation are viable options.

Teaching and Mentoring: Medical schools, nursing programs, and residency programs need experienced educators. Adjunct teaching or mentoring can be fulfilling and financially helpful.

Consulting: Doctors can advise healthcare startups, legal teams, or insurance companies. Their insights are valuable in product development, litigation, and policy.

Exploring Non-Clinical Opportunities

Some physicians may wish to pivot entirely. Transferable skills—critical thinking, communication, leadership—open doors in other industries:

Health Coaching or Life Coaching: With certification, doctors can guide clients in wellness, stress management, or career transitions.

Entrepreneurship: Starting a small business, such as a tutoring service, online course, or specialty clinic, can generate income and autonomy.

Real Estate or Investing: With careful planning, investing in rental properties or learning about the stock market can create passive income.

Maximizing Government and Community Resources

At 65, individuals become eligible for Medicare, which can significantly reduce healthcare costs. Additionally, Social Security benefits may be available, depending on work history. While delaying benefits until age 70 increases monthly payments, some may need to claim earlier to meet immediate needs.

***

***

Other resources include:

Supplemental Security Income (SSI): For those with limited income and assets.

SNAP (food assistance) and LIHEAP (energy assistance): These programs help cover basic living expenses.

Community Organizations: Nonprofits and religious groups often provide support with housing, transportation, and social engagement.

Downsizing and Budgeting

Reducing expenses is a powerful way to stretch limited resources. Consider:

Relocating: Moving to a lower-cost area or state with favorable tax policies can reduce housing and living expenses.

Selling Assets: A large home, unused vehicle, or collectibles may be converted into cash.

Shared Housing: Living with family, roommates, or in co-housing communities can cut costs and reduce isolation.

Minimalist Living: Prioritizing needs over wants and embracing simplicity can lead to financial and emotional freedom.

Creating a realistic budget is essential. Track income and expenses, eliminate unnecessary costs, and prioritize essentials. Free budgeting tools and financial counseling services can help.

Financial stress can take a toll on mental health. It’s important to cultivate resilience and maintain a sense of purpose. Strategies include:

Staying Active: Physical activity improves mood and health. Walking, yoga, or swimming are low-cost options.

Volunteering: Giving back can provide structure, community, and fulfillment.

Learning New Skills: Online courses, hobbies, or certifications can reignite passion and open new doors.

Building a Support Network: Friends, family, and peer groups offer emotional support and practical advice.

Planning for the Future

Even at 65, it’s not too late to plan. Consider:

Debt Management: Negotiate payment plans, consolidate loans, or seek professional help.

Estate Planning: Create a will, designate healthcare proxies, and organize important documents.

Insurance Review: Ensure adequate coverage for health, life, and long-term care.

Financial Advising: A fee-only advisor can help create a sustainable plan without selling products.

Embracing a New Chapter

Retirement is not a destination—it’s a transition. For a broke 65-year-old doctor, it may not look like the glossy brochures, but it can still be rich in meaning. By leveraging experience, reducing expenses, accessing resources, and nurturing well-being, retirement becomes a journey of reinvention.In many ways, doctors are uniquely equipped for this challenge. They’ve faced long hours, high stakes, and complex problems. That same grit and adaptability can guide them through financial hardship and into a fulfilling retirement.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Investing may seem complicated, but today there are many ways for the newly minted physician [MD, DO, DPM, DMD or DDS] to begin, even with minimal knowledge and only a small amount to invest. Starting as soon as possible will help you get closer to the retirement you deserve.

***

Why is investing important?

Investing often feels like a luxury reserved for the already wealthy physician. Many of us find it difficult to think about investing for the future when there are so many things we need that money for right now; medical school loans, auto, home and children; etc. But, at some point, we’re going to want to stop working and enjoy retirement. And simply put, retirement is expensive.

Most calculations advise that you aim for enough savings to give you 70% to 80% of your pre-retirement income for 20 years or more. Depending on your goals for retirement, that means you could need between $500,000 and $1 million in savings by the time you retire. That may not sound attainable, but with the power of compounding growth, it’s not as hard to achieve as you think. The key is starting as soon as possible and making smart choices.

The short answer is “now,” no matter what your age. Due to the way the gains in investments can compound, the earlier you start the better. Money invested in your 20s could very easily grow over 20 times before you retire, without you having to do much.That is powerful. Even if you’re in your 50s or older, you can still make significant progress toward meeting your goals in retirement.

How much should you invest per month?

Most financial experts say you should invest 10% to 15% of your annual income for retirement. That’s the goal, but you don’t have to get there immediately. Whatever you can start investing today is going to help you down the road.

So, if 10% to 15% is too much right now, start small and build toward that goal over time. You can actually start investing with $5 if you want. And you should. Some investment products require a minimum investment, but there are plenty that don’t, and a lot of online brokerage accounts can be started for free.

The best investments for you are going to depend on your age, goals, and strategy. The important thing is to get started. You’ll learn as you go. If you have questions, a dedicated DIYer or investment advisor can help give you the guidance and options you need.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Sometimes debt is a necessary tool in building wealth

Using debt to build wealth might seem counterintuitive. After all, when you calculate your wealth, you look at what you own (assets) and subtract what you owe (debts and liabilities) to determine what your net worth (wealth) is.

It’s easy to oversimplify that debt is bad and is harmful to your wealth. Because some debt is really harmful, like credit cards, automobile, debt gets lumped into the category of “bad.”

But some types of debt can be useful and sometimes necessary to create wealth; home, education, business, etc. For folks that don’t readily have access to large sums of cash or capital, debt may be the tool that allows them to expand.

A Financial Self Discovery Questionnairefor Medical Professionals

For understanding your relationship with money, it is important to be aware of yourself in the contexts of culture, family, value systems and experience. These questions will help you. This is a process of self-discovery. To fully benefit from this exploration, please address them in writing. You will simply not get the full value from it if you just breeze through and give mental answers. While it is recommended that you first answer these questions by yourself, many people relate that they have enjoyed the experience of sharing them with others who are important to them.

As you answer these questions, be conscious of your feelings, actually describing them in writing as part of your process.

Childhood

What is your first memory of money?

What is your happiest moment with Money? Your most unhappy?

Name the miscellaneous money messages you received as a child.

How were you confronted with the knowledge of differing economic circumstances among people, that there were people “richer” than you and people “poorer” than you?

Cultural heritage

What is your cultural heritage and how has it interfaced with money?

To the best of your knowledge, how has it been impacted by the money forces? Be specific.

To the best of your knowledge, does this circumstance have any motive related to Money?

Speculate about the manners in which your forebears’ money decisions continue to affect you today?

Family

How is/was the subject of money addressed by your church or the religious traditions of your forebears?

What happened to your parents or grandparents during the Depression?

How did your family communicate about money?

How? Be as specific as you can be, but remember that we are more concerned about impacts upon you than historical veracity.

When did your family migrate to America (or its current location)?

What else do you know about your family’s economic circumstances historically?

Your parents

How did your mother and father address money?

How did they differ in their money attitudes?

How did they address money in their relationship?

Did they argue or maintain strict silence?

How do you feel about that today?

Please do your best to answer the same questions regarding your life or business partner(s) and their parents.

Childhood: Revisited

How did you relate to money as a child? Did you feel “poor” or “rich”? Relatively? Or, absolutely? Why?

Were you anxious about money? Did you receive an allowance? If so, describe amounts and responsibilities.

Did you have household responsibilities?

Did you get paid regardless of performance?

Did you work for money?

If not, please describe your thoughts and feelings about that.

***

***

Same questions, as a teenager, young adult, older adult.

Credit

When did you first acquire something on credit?

When did you first acquire a credit card?

What did it represent to you when you first held it in your hands?

Describe your feelings about credit.

Do you have trouble living within your means?

Do you have debt?

Adulthood

Have your attitudes shifted during your adult life? Describe.

Why did you choose your personal path? a) Would you do it again? b) Describe your feelings about credit.

Adult attitudes

Are you money motivated? If so, please explain why? If not, why not? How do you feel about your present financial situation? Are you financially fearful or resentful? How do you feel about that?

Will you inherit money? How does that make you feel?

If you are well off today, how do you feel about the money situations of others? If you feel poor, same question.

How do you feel about begging? Welfare? If you are well off today, why are you working?

Do you worry about your financial future?

Are you generous or stingy? Do you treat? Do you tip?

Do you give more than you receive or the reverse? Would others agree?

Could you ask a close relative for a business loan? For rent/grocery money?

Could you subsidize a non-related friend? How would you feel if that friend bought something you deemed frivolous?

Do you judge others by how you perceive they deal with their Money? Do you feel guilty about your prosperity? Are your siblings prosperous?

What part does money play in your spiritual life?

Do you “live” your Money values?

Conclusion

There may be other questions that would be useful to you. Others may occur to you as you progress in your life’s journey. The point is to know your personal money issues and their ramifications for your life, work, and personal mission.

This will be a “work-in-process” with answers both complex and incomplete. Don’t worry.

Just incorporate fine-tuning into your life’s process.

A paradox is a statement or situation that seems contradictory but actually makes sense when you think about it more deeply. It challenges logic and often reveals a hidden truth.

FLEXIBLY DOGMATIC PARADOX

The Flexibly Dogmatic Paradox suggests that no matter how sensible your financial planning, investing or wealth management process is there will be uncomfortably long periods when it looks broken. And process is the best way of ensuring you keep standing for something because if you don’t stand for something, you’ll fall for anything. This is why, when assessing an investment fund, focus 50% on the manager’s character and 50% on their process. Everything else is detail. There are few guarantees in investing, but the fact that markets will batter you emotionally is one of them.

Example: During volatile times, the temptation to abandon the process is strong. But that’s why it’s there. Process is what forces one fund manager to keep buying unbroken companies when everyone else thinks they’re bust, and another to keep faith with a top-quality company when the mob says it’s too expensive The best fund managers dogmatically stick to their process when it’s out of favor. Then, when it returns to favor, the elastic pings back: they recapture lost ground surprisingly fast. However, every rule has an exception. And spotting the exceptions to their process is something the true greats have a knack for buying and selling.

***

***

Example: In 2007, US value manager Bill Miller had the makings of an investment legend, but the financial crisis wrecked all that. His process told him to double down into falling share prices, which had worked well for years. But it doesn’t work if the companies go bust, which many of his financial stocks did in 2008.

The fact is that no matter how good it is, a process operated without human judgment is just an algorithm. The best fund managers and financial prospectors and sales men/women know this.

They stick dogmatically to their process but somehow remain flexible enough to spot the occasions when it’s about to drive them into a brick wall.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

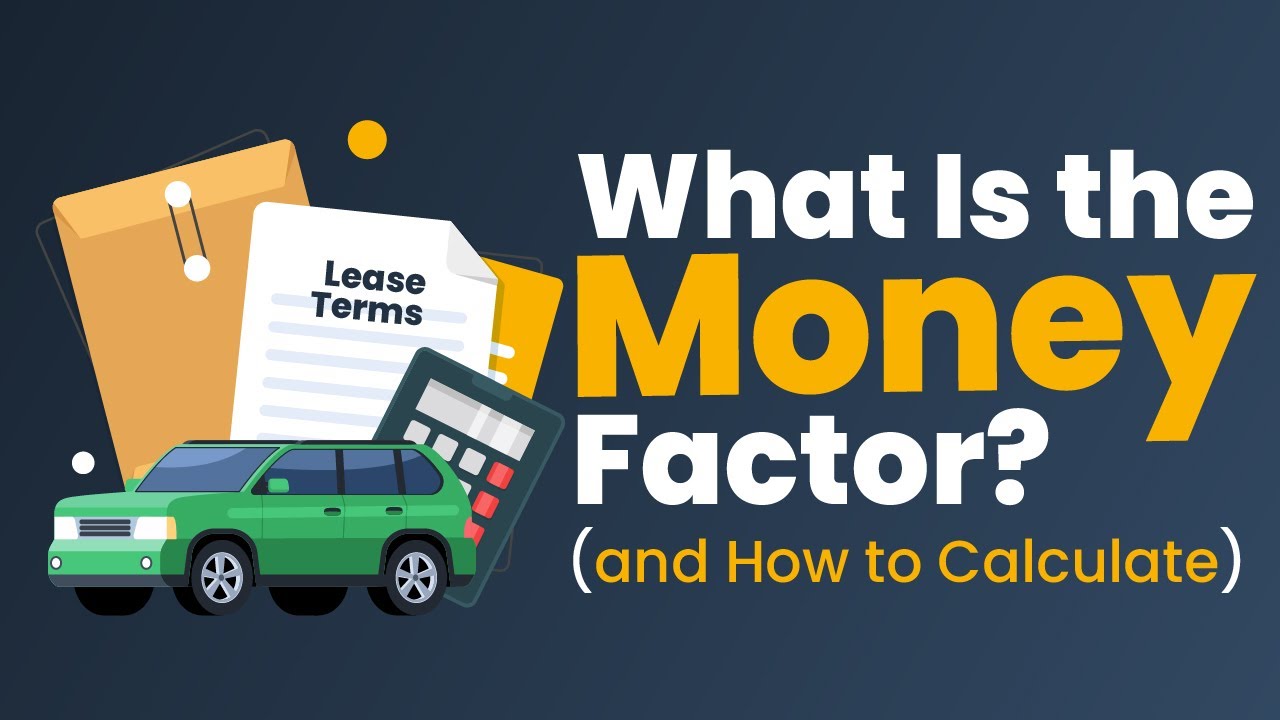

The so-called money factor (abbreviated as MF on invoices) is a number in a decimal form that dealers use to calculate the APR of a car lease. It’s a major part of your monthly payment and dealers are known to jack up the money factor to pad their profits.

Most doctors don’t ask to see it because they’re not aware of it or don’t know how to calculate it. Ask to see the money factor, then multiply it by 2,400.

For example, if the money factor is .00150, you multiply it by 2,400 to get 3.6%. If that’s higher than the prevailing rate, you have room to talk them down.

How to reduce it

So how do you get a good interest rate when you lease a vehicle? The same way you do when borrowing for any other reason, whether it’s buying a home or applying for a personal loan: by having good credit. This may reduce your interest rate because you’ll represent a lower risk to a lender.

A high residual value on the car could also help you get a better interest rate. A higher residual value means you’d have lower monthly payments because there would be less depreciation on the vehicle. Since interest is applied to your monthly payment, a lower monthly payment would equate to reduced interest charges.

The money factor is one of the many numbers you may want to learn about when leasing a car. It’s one of the transactional costs that come with leasing, and allows dealers and finance companies to make a profit on every lease they execute. As a consumer, it’s a smart idea to learn the financial implications of this number and how it’ll affect your overall costs over the course of a multi-year lease.

***

***

If the interest rate is too high, you may need to shop around for a better rate, negotiate with the dealer or lender to lower the money factor, or consider leasing another vehicle that’s more in line with your budget. Either way, make sure you explore all your financial options before taking a car off the lot.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A psychological paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given.

This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention and/or persuade them to action, sales and closing statements. But paradoxes for the financial sector can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

One good psychological paradox example is The Paradox of Thrift which suggests that while saving money is generally considered a prudent financial behavior, excessive saving during times of economic downturn can actually hinder economic recovery. When consumers collectively reduce their spending and increase their savings, it creates a decrease in aggregate demand. This reduction in demand can lead to lower production levels, job losses, and ultimately a decline in economic output. In other words, what may be individually rational behavior (financial saving) can have negative consequences for the overall economy.

The following paradoxical contradictions will help financial advisors guide clients to close more sales to the benefit of both.

____

In the intricate world of finance sales, advisors are often at the crossroads of various paradoxes that challenge client decision-making. While the journey towards financial security involves calculated strategies, it’s the nuanced understanding of paradoxes that can help the advisor close more sales.

____

But, what seems trueabout money often turns out to be false, according to colleague Finance Professor John Goodell, PhD from the University Akron:

The more we try to trade our way to profits, the less likely we are to profit.

The more boring an investment—think index funds—the more exciting the long-run performance will probably be.

The more exciting an investment—name your latest Wall Street concoction, Special Purpose Acquisition Company [SPAC] or anything crypto—the less exciting the long-term results typically are.

The only certainty is uncertainty and the only constant is change. Today’s market decline will eventually become a bull market, and today’s market leaders will eventually yield to other stocks.

Big market trends play a huge role in investment results, and yet trying to time macroeconomic cycles or guess which market sectors will outperform is a fool’s errand. Many big market rotations are set in motion by something wholly unanticipated, like a virus pandemic or a war.

To be happy when wealthy, we also need to be happy with far less money. The fact is, above a relatively modest income level, no amount of extra money will change our level of happiness. More money might even make us miserable, as many lottery winners have discovered.

The more we hate an investing trait—or any trait for that matter—the more likely it is that we’re resisting seeing that trait in ourselves. It’s what Carl Jung MD called the Shadowof Undesirable Personality Aspects that we hide from ourselves. Do prospects get irritated listening to your unsolicited financial advice? There’s a good chance that you often give unsolicited financial advice but don’t like to admit it.

The more we learn about investing, the more we realize we don’t know anything. We should just buy index funds and instead spend our time worrying about stuff we can actually control.

The more an investor is convinced he’s right, the more likely he is to be wrong. Short sellers, in particular, are likely to succumb to this paradoxical trap.

The more options we have, the less satisfied we’ll be with each one. This is the Paradox of Choice; revised. Anyone who has spent hours “optimizing” his or her portfolio knows this all too well. Its close cousin is information overload, another frustration paradox when investing.

The more afraid we are of losing money, the more likely we are to take unwitting risks that lose us money. Sitting in cash seems wise during market selloffs. But the truth is, none of us can reliably time the market. Pull up any chart of the stock market over any period longer than a decade and you’ll see that the riskiest decision is sitting in cash, which gets destroyed by inflation.

The more we think about our investments and look at our financial accounts, the more likely we are to damage our results by buying high because of greed and selling low because of fear. It can pay to look away.

ASSESSMENT

How should you respond to these financial paradoxes? As you plan for your own financial future, as well as your own client prospecting endeavors, embrace the concept of “loosely held views.”

In other words, make financial and client acquisitions plans, but continuously update your views, question your assumptions and paradoxes and rethink your priorities. Years of experience with clients certainly support the futility of trying to help them change their financial behavior by telling them what they “should” know or do.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological paradoxes to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2016.

Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York. 2006

Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2015.

Most individual physician portfolios are simply a list of stocks. Doctors with such lists usually know the cost of each position and when they acquired it. It is not unusual to find inherited low cost stocks in the account that have been held for many years.

When you inherit securities, a new cost basis is established (the price of the stock on the date of death or six months later—the executor of the estate makes this determination). Even though there would be no capital gain liability if the stock were sold immediately after date of death, most people simply don’t do anything, just hold the stock. Of course taxes should be considered when selling securities but the investment merit should be the overriding factor.

***

***

Doctor and Accountant Opinions

In a personal communication, Mr. L. Eddie Dutton, CPA said, “First make an investment decision and if it fits into the tax plan, so much the better. Doctors often wonder where they will get the money to pay the taxes. I say to get it from the sale of the appreciated stock and cry all the way to the bank with your profit.”

Dr. Ernest Duty MD, a very successful private investor advises “Ask yourself this question: If you had the money instead of the stock, would you buy the stock? If your answer is ‘Yes’ then, hold on to the stock but if you say ‘No, I wouldn’t buy that stock today’ then, sell it” [personal communication].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: E-MAILCONTACT: MarcinkoAdvisors@outlook.com

Several years ago a group of highly trusted and deeply experienced financial advisors, insurance service professionals and estate planners noted that far too many of their mature retiring physician clients, using traditional stock brokers, management consultants and financial advisors, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse related relationship was noted, and dubbed the “Doctor Effect.” In others words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning and medical practice management, continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, dinners and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization confirmed the industry culture which seemed to be:

Bread for the advisor – Crumbs for the client!

And so, Marcinko Associates formed a cadre’ of technology focused and highly educated multi-degreed doctors, nurses, financial advisors, attorneys, accountants, psychologists and educational visionaries who decided there must be a better way for their healthcare colleagues to receive financial planning advice, products and related advisory services within a culture of fiduciary responsibility.

We trust you agree with this specific niche knowledge, and collegial consulting philosophy, as illustrated thru our firm and these two books.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

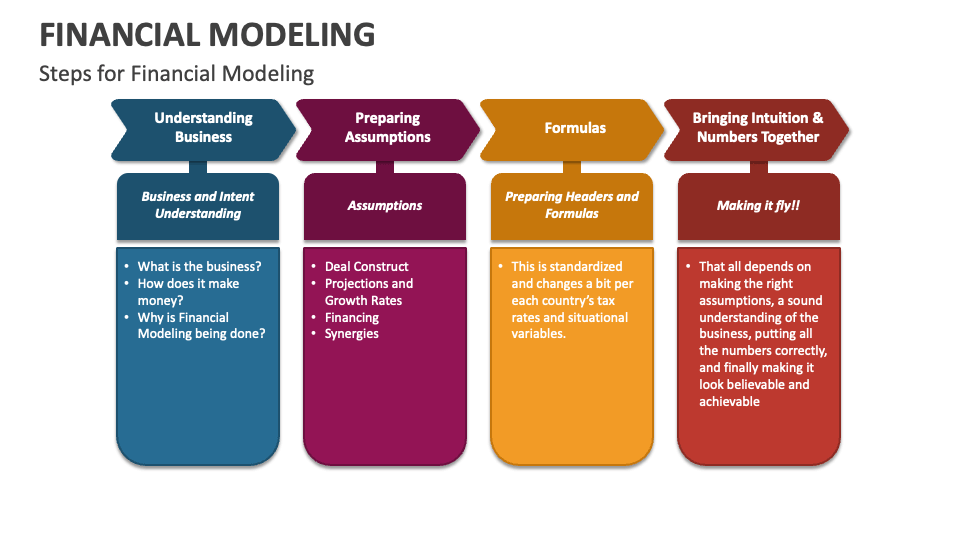

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.

What-If Analysis: Ever daydream about what would happen if you took that leap of faith with your business? This tool allows you to explore various scenarios without risking a dime. It’s like trying on outfits in a virtual dressing room before making a purchase.

Leveraged Buyout (LBO) Model: This is a bit like orchestrating a heist, but legally. It’s about acquiring a company using borrowed money, with plans to pay off the debts with the company’s own cash flows. High stakes, high rewards.

Mergers and Acquisitions (M&A) Model: Picture two puzzle pieces coming together. This model evaluates how combining companies can create a new, more valuable entity. It’s the corporate version of a matchmaker.

Three Statement Model: The holy trinity of financial modeling, linking the income statement, balance sheet, and cash flow statement. It’s like weaving a tapestry where each thread is crucial to the overall picture.

Capital Asset Pricing Model (CAPM): A formula that calculates the expected return on an investment, considering its risk compared to the market. It’s like choosing the best roller coaster in the park, balancing thrill and safety.

Cash Flow Forecasting: This is your financial weather forecast, predicting the cash flow climate of your business. It helps you plan for sunny days and save for the rainy ones.

Cost of Capital: The price of financing your business, whether through debt or equity. It’s like the interest rate on your growth engine, pushing you to maximize every dollar invested.

Debt Schedule: A timeline of your business’s debts, showing when and how much you owe. It’s your roadmap to becoming debt-free, one milestone at a time.

Equity Valuation: Determining the value of a company’s shares. It’s like assessing the worth of a rare gemstone, ensuring investors pay a fair price for a piece of the treasure.

Financial Leverage: Using debt to amplify returns on investment. It’s like using a lever to lift a heavy object, increasing force but also risk.

Forecast Model: A crystal ball for your finances, projecting future performance based on past and present data. It’s your guide through the financial wilderness, helping you navigate with confidence.

Operating Model: A detailed blueprint of how a business generates value, mapping out operational activities and their financial impact. It’s like laying out the inner workings of a clock, ensuring every gear turns smoothly.

Revenue Growth Model: This tracks potential increases in sales over time, charting a course for expansion. It’s like plotting your ascent up a mountain, anticipating the effort required to reach the summit.

Dying Broke. It’s a goal for those retirees who embrace the idea of spending their hard-earned wealth during their lifetimes. Their aim is to enjoy the fruits of their labor while they can and spend the last penny just as they take their last breath. The concept feels both pragmatic and poetic.

But here’s the twist: While the concept may conjure images of lavish spending sprees and exotic vacations, that’s rarely what I see in practice. Many of my clients who identify as Die Brokers aren’t recklessly burning through their wealth. In fact, the opposite is often true.

This is because their approach to spending and giving is shaped by a lifetime of frugal money scripts that are incredibly hard to shake. Many Boomers grew up with financial uncertainty, learning to save and sacrifice to protect themselves and their families. Even after decades of financial success, those habits don’t just disappear. The idea of “spending down” their wealth, even intentionally, feels unnatural and irresponsible. There is an internal tug-of-war between their stated desire to enjoy their wealth and their deeply rooted fear of running out.

This paradox can significantly affect retirees’ financial planning. While Die Brokers may express a strong commitment to living fully, their money behavior often reveals a need for reassurance that their money will last for their lifetime.

For many Boomers, including myself, those frugal money scripts have served us well for decades. They’ve provided financial stability and peace of mind. But in this stage of life, they can also hold us back from experiencing the freedom we’ve worked so hard to achieve—especially in the time we have left when we can still physically enjoy it. The challenge is finding balance, honoring the values that got us here while allowing ourselves permission to live fully.

Here are four ways to start turning those old money scripts into permission to spend and give intentionally:

Reframe wealth as a tool rather than a safety net. Recognize that money is about opportunity as well as security. Spending with intention can bring joy and meaning, whether it’s funding a family trip, supporting a cause, or splurging on a bucket list item.

Work with your financial advisor to analyze your retirement spending and the probability of running out of money. The amount they suggest you can spend may surprise you—it’s often far higher than your frugal money scripts would lead you to believe.

Experiment with incremental giving. If parting with your wealth feels daunting, start small. Gift modest amounts to family, friends, or charities and notice how it feels. Seeing the immediate impact of your generosity can help ease the transition and loosen the grip of those old money scripts.

Set intentional spending goals instead of vaguely aiming to “enjoy your wealth.” Identify specific ways you want to use your money to enhance your life or the lives of others. Having a clear plan can turn spending into a meaningful act rather than an exercise in guilt.

For many of us, the Die Broke mentality is not about recklessness or extravagance. It’s about learning to let go. Despite our bold talk of spending down to the last penny, most of us will likely leave behind more than we planned. And maybe that’s just fine—especially for our kids and grand kids. Perhaps being a Die Broker is really about giving ourselves permission to live with intention, to savor what we’ve built, and to enjoy living to the fullest the rich life our frugality has helped provide.

It has been said that most ordinary people should have at least three to six months of living expenses (not including taxes) in a cash-equivalent reserve fund that is easily accessible (i.e., liquid). The amount needed for a one-month reserve is equal to the amount of expenses for the month, rather than the amount of monthly income. This is because during no-income months there is no income tax.

However, the situation might not be the same for physicians in today’s harsh economic climate.

The New Realities

Now, some physician-focused financial advisors, financial planners and Certified Medical Planners™ suggest even more reserve fund savings; up to two years. That’s because many factors come into play when determining how much a particular doctor’s family should have.

For example:

Does the family have one income or two? If the doctor is in a dual-income family with stable incomes and they live on a single income, the need for a liquid reserve is less.

How stable is the doctor’s income source? If a sole provider with an unstable income who spends all of the income each month, the need for a liquid cash reserve is high.

Does the doctor own the practice, work in a clinic, medical group, hospital or healthcare system? In other words – employee (less control) or employer (more control).

What is the doctor’s medical specialty and how has managed care penetrated his locale, or affected her focus? What about a DO, DDS/DMD or DPM, etc.

How does the family use its income each month; does it have a saver, spender, or investor mentality?

Does the family anticipate the possibility of large expenses occurring in the future (medical practice start-up costs or practice purchase; children, medical school student debts; auto or home loans; and/or liability suits, etc)?

Pan physician lifestyle?

The Past

In the ancient past, a doctor may have opted for a nine-twelve month reserve if the need for security was high – and a six-to-nine month reserve if the need for security was low. But today, even more may be needed. How about 15-18 months, or more? Perhaps even 24 months!

So, the following questions may be helpful in determining the amount of reserve needed by the physician:

1. How long would it take you to find another job in your medical specialty if you suddenly found yourself unemployed – same for your spouse?

2. Would you have to relocate – same for your spouse?

3. How much do you spend each month on fixed or discretionary expenses and would you be willing to lower your monthly expenses if you were unemployed?

Assessment

Once the amount of reserve is determined, the doctor should use the appropriate investment vehicles for the funds.

At minimum, the reserve should be invested in a money market fund. For larger reserves, an ultra-short-term bond fund might be appropriate for amounts over three-six months. While even larger reserves might be kept in a short term bond fund depending on interest rates and trends.

So, what do the initials M.D. really mean? … More Dough!

How much reserve do you have and where is it stashed?

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

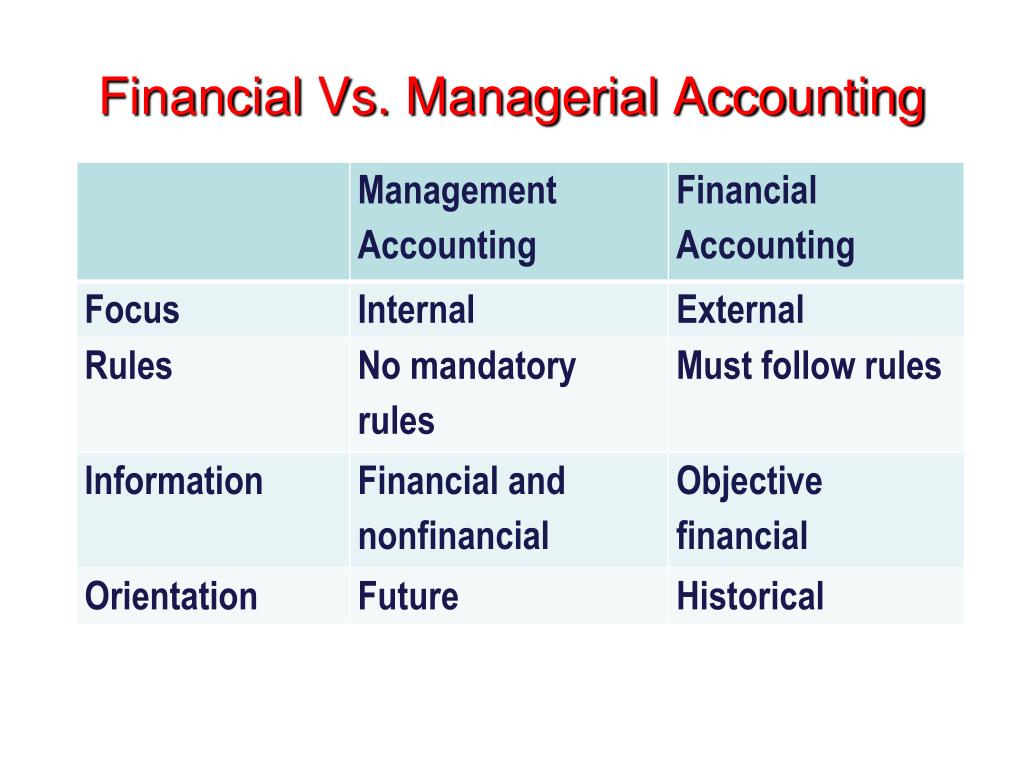

Financial accounting and managerial accounting are two distinct branches of the accounting field, each serving different purposes and stakeholders. Financial accounting focuses on creating external reports that provide a snapshot of a company’s financial health for investors, regulators, and other outside parties. Managerial accounting, meanwhile, is an internal process aimed at aiding managers in making informed business decisions.

Objectives of Financial Accounting

Financial accounting is primarily concerned with the preparation and presentation of financial statements, which include the balance sheet, income statement, and cash flow statement. These documents are meticulously crafted to reflect the company’s financial performance over a specific period, providing insights into its profitability, liquidity, and solvency. The objective is to offer a clear, standardized view of the financial state of the company, ensuring that external entities have a reliable basis for evaluating the company’s economic activities.

The process of financial accounting also involves the meticulous recording of all financial transactions. This is achieved through the double-entry bookkeeping system, where each transaction is recorded in at least two accounts, ensuring that the accounting equation remains balanced. This systematic approach provides accuracy and accountability, which are paramount in financial reporting. CPA = Certified Public Accountant.

Objectives of Managerial Accounting

Managerial accounting is designed to meet the information needs of the individuals who manage organizations. Unlike financial accounting, which provides a historical record of an organization’s financial performance, managerial accounting focuses on future-oriented reports. These reports assist in planning, controlling, and decision-making processes that guide the day-to-day, short-term, and long-term operations.