BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on March 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

RETIREMENT PLANNING

By Staff Reporters

***

***

A PEP is a defined contribution plan, such as a 401(k), in which multiple employers can participate. When employers join a PEP, they delegate their named fiduciary role to a third-party pooled plan provider (PPP). PEP fiduciary oversight falls on the PPP rather than the employer. And although each PPP may set its own eligibility requirements, businesses joining a PEP benefit plan needn’t operate in the same industry or geographical area.

PEP plans provide viable 401(k) alternatives for small business owners who may otherwise struggle to compete for talent against large organizations with comprehensive benefits packages.

Other advantages include: Less in-house administration: The PPP assumes responsibility for much of the plan administration, handling all plan documentation, governmental filings and ongoing compliance. Employee payroll deductions are left to the employer, but these can be efficiently managed with the help of a payroll service provider that integrates payroll and benefits.

Tax credits can help offset PEP start-up costs. For the first three years of participation, employers may be eligible for a tax credit of $5,000 annually, with an additional $500 available to those who set up automatic enrollment. Under Secure Act 2.0, an additional credit of up to $1,000 per employee for eligible employer contributions may apply to employers with up to 50 employees for the preceding taxable year. This credit phases out from 51 to 100 employees.

Businesses participating in single-employer retirement plans (SEP) must independently communicate and coordinate with their record-keeper, custodian, investment advisor, trustee and auditor. With PEP, all these tasks and services are bundled into one, saving employers time and money.

Despite its advantages, a PEP does have some drawbacks, particularly when compared to an SEP. Unlike a PEP, an SEP gives employers more of the following:

Flexibility: Employers can customize the design of their plan to meet their retirement goals and the needs of their employees.

Control: Employers are not dependent on the actions or decisions of others and can access information and resolve problems directly without the need of a third party.

Choice: Employers have the unilateral freedom to choose a different service provider, move their plan or negotiate better pricing if they are unsatisfied with the cost or quality of service.

The giant accounting firm Grant Thornton LLP is laying off 200 people, its second round of layoffs in the past six months and an indication that the major players in the professional consulting, accounting and advisory business are preparing for an economic slowdown that could squeeze profits across corporate America.

***

Statistics: 7.4%. That’s the percentage drop in students who graduated with a degree in accounting in the 2021–2022 school year than the year before. Low starting salaries, heavy workloads, and uncertainty around AI are driving the exodus of students from choosing accounting degrees. (the Wall Street Journal).

Running a business involves a constant learning curve. And that applies whether you’re a rookie entrepreneur just starting out with a great idea for a new business or a more established small business owner with a quickly growing business that needs to expand. You should always be learning as a business owner, no matter where you are in your career—there’s always a new tool to master, new problems to solve, and new vocabulary to understand.

In order to not get totally overwhelmed, it’s helpful to take things one segment at a time. For instance, feeling confident when discussing the business’s financial needs should be a priority for every small business owner. After all, you represent the heart and soul of your business in the marketplace. So knowing the “language” of business finance is an integral part of your job as the owner.

The good news is that you don’t have to be an accountant or a financial planner to negotiate in the world of business finance. Here are some business terms and finance terms that will help you find your way to successful small business funding. https://www.youtube.com/embed/0kD4X2fgxGs

Business and Finance Terms to Know

From accounting, to business loans, to general business financial operations, here’s the ultimate list to all the business finance terms and definitions you need to know:

1. Accounts Payable

Accounts payable is a business finance 101 term. This represents your small business’s obligations to pay debts owed to lenders, suppliers, and creditors. Sometimes referred to as A/P or AP for short, accounts payable can be short or long term depending upon the type of credit provided to the business by the lender.

2. Accounts Receivable

Also known as A/R (or AR, good guess), accounts receivables is another business finance 101 term that means the money owed to your small business by others for goods or services rendered. These accounts are labeled as assets because they represent a legal obligation for the customer to pay you cash for their short-term debt.

3. Accrual Basis

The accrual basis of accounting is an accounting method of recording income when it’s actually earned and expenses when they actually occur. Accrual basis accounting is the most common approach used by larger businesses to record and maintain financial transactions.

4. Accruals

A business finance term and definition referring to expenses that have been incurred but haven’t yet been recorded in the business books. Wages and payroll taxes are common examples.

5. Asset

This business finance key term is anything that has value—whether tangible or intangible—and is owned by the business is considered an asset. Typical items listed as business assets are cash on hand, accounts receivable, buildings, equipment, inventory, and anything else that can be turned into cash.

6. Balance Sheet

Along with three other reports relating to the financial health of your small business, the balance sheet is essential information that gives a “snapshot” of the company’s net worth at any given time. The report is a summary of the business assets and liabilities.

7. Bookkeeping

A method of accounting that involves the timely recording of all financial transactions for the business.

8. Capital

Refers to the overall wealth of a business as demonstrated by its cash accounts, assets, and investments. Often called “fixed capital,” it refers to the long-term worth of the business. Capital can be tangible, like durable goods, buildings, and equipment, or intangible such as intellectual property.

9. Working Capital

Not to be confused with fixed capital, working capital is another business finance 101 term. It consists of the financial resources necessary for maintaining the day-to-day operation of the business. Working capital, by definition, is the business’s cash on hand or instruments that you can convert to cash quickly.

10. Cash Flow

Every business needs cash to operate. The business finance term and definition cash flow refers to the amount of operating cash that “flows” through the business and affects the business’s liquidity. Cash flow reports reflect activity for a specified period of time, usually one accounting period or one month. Maintaining tight control of cash flow is especially important if your small business is new, since ready cash can be limited until the business begins to grow and produce more working capital.

11. Cash Flow Projections

Future business decisions will depend on your educated cash flow projections. To plan ahead for upcoming expenditures and working capital, you need to depend on previous cash flow patterns. These patterns will give you a comprehensive look at how and when you receive and spend your cash. This info is the key to unlock informed, accurate cash flow projections.

12. Depreciation

The value of any asset can be said to depreciate when it loses some of that value in increments over time. Depreciation occurs due to wear and tear. Various methods of depreciation are used by businesses to decrease the recorded value of assets.

13. Fixed Asset

A tangible, long-term asset used for the business and not expected to be sold or otherwise converted into cash during the current or upcoming fiscal year is called a fixed asset. Fixed assets are items like furniture, computer equipment, equipment, and real estate.

14. Gross Profit

This business finance term and definition can be calculated as total sales (income) less the costs (expenses) directly related to those sales. Raw materials, manufacturing expenses, labor costs, marketing, and transportation of goods are all included in expenses.

15. Income Statement

Here is one of the four most important reports lenders and investors want to see when evaluating the viability of your small business. It is also called a profit and loss statement, and it addresses the business’s bottom line, reporting how much the business has earned and spent over a given period of time. The result will be either a net gain or a net loss.

16. Intangible Asset

A business asset that is non-physical is considered intangible. These assets can be items like patents, goodwill, and intellectual property.

17. Liability

This business finance key term is a legal obligation to repay or otherwise settle a debt. Liabilities are considered either current (payable within one year or less) or long-term (payable after one year) and are listed on a business’s balance sheet. A business’s accounts payable, wages, taxes, and accrued expenses are all considered liabilities.

18. Liquidity

Liquidity is an indicator of how quickly an asset can be turned into cash for full market value. The more liquid your assets, the more financial flexibility you have.

19. Profit & Loss Statement

See “Income Statement” above.

20. Statement of Cash Flow

One of the important documents required by lenders and investors that shows a summary of the actual collection of revenue and payment of expenses for your business. The statement of cash flow should reflect activity in the areas of operating, investing, and financing and should be an integral part of your financial statement package.

21. Statement of Shareholders’ Equity

If you have chosen to fund your small business with equity financing and you have established shares and shareholders as part of the controlling interests, you are obligated to provide a financial report that shows changes in the equity section of your balance sheet.

22. Annual Percentage Rate

The business finance term and definition APR represents the yearly real cost of a loan including all interest and fees. The total amount of interest to be paid is based on the original amount loaned, or the principal, and is represented in percentage form. When shopping for the right loan for your small business, you should know the APR for the loan in question. This figure can be very helpful in comparing one financial tool with another since it represents the actual cost of borrowing.

23. Appraisal

Just like your real estate appraisal when buying a house, an appraisal is a professional opinion of market value. When closing a loan for your small business, you will probably need one or more of the three types of appraisals: real estate, equipment, and business value.

24. Balloon Loan

A loan that is structured so that the small business owner makes regular repayments on a predetermined schedule and one much larger payment, or balloon payment, at the end. These can be attractive to new businesses because the payments are smaller at the outset when the business is more likely to be facing strict financial constraints. However, be sure that your business will be capable of making that last balloon payment since it will be a large one.

25. Bankruptcy

This federal law is used as a tool for businesses or individuals who are having severe financial challenges. It provides a plan for reduction and repayment of debts over time or an opportunity to completely eliminate the majority of the outstanding debts. Turning to bankruptcy should be given careful thought because it will have a negative effect on the business credit score.

26. Bootstrapping

Using your own money to finance the start-up and growth of your small business. Think of it as being your own investor. Once the business is up and running successfully, the business finance term and definition bootstrapping refers to the use of profits earned to reinvest in the business.

27. Business Credit Report

Just like you have a personal credit report that lenders look at to determine risk factors for making personal loans, businesses also generate credit reports. These are maintained by credit bureaus that record information about a business’s financial history.

Items like how large the company is, how long has it been in business, amount and type of credit issued to the business, how credit has been managed, and any legal filings (i.e., bankruptcy) are all questions addressed by the business credit report. Lenders, investors, and insurance companies use these reports to evaluate risk exposure and financial health of a business.

28. Business Credit Score

A business credit score is calculated based on the information found in the business credit report. Using a specialized algorithm, business credit scoring companies take into account all the information found on your credit report and give your small business a credit score. Also called a commercial credit score, this number is used by various lenders and suppliers to evaluate your creditworthiness.

29. Collateral

Any asset that you pledge as security for a loan instrument is called collateral. Lenders often require collateral as a way to make sure they won’t lose money if your business defaults on the loan. When you pledge an asset for collateral, it becomes subject to seizure by the lender if you fail to meet the requirements of the loan documents.

30. Credit Limit

When a lender offers a business line of credit it usually comes with a credit limit, or a maximum amount that you can use at any given time. It is said that you reach your credit limit or “max out” your credit when you borrow up to or exceed that number. A business line of credit can be especially useful if your business is seasonal or if the income is extremely unpredictable. It is one of the fastest ways to access cash for emergencies.

31. Debt Consolidation

If your small business has several loans with various payments, you might want to consider a business debt consolidation loan. It is a process that lets you combine multiple loans into a single loan. The advantages are possibly reducing the interest rates on the borrowed funds as well as lowering the total amount you repay each month. Businesses use this tool to help improve cash flow.

32. Debt Service Coverage Ratio

The business finance term and definition debt service coverage ratio (DSCR) is the ratio of cash your small business has available for paying or servicing its debt. Debt payments include making principal and interest payments on the loan you are requesting. Generally speaking, if your DSCR is above 1, your business has enough income to meet its debt requirements.

33. Debt Financing

When you borrow money from a lender and agree to repay the principal with interest in regular payments for a specified period of time, you’re using debt financing. Traditionally, it has been the most common form of funding for small businesses.

Debt financing can include borrowing from banks, business credit cards, lines of credit, personal loans, merchant cash advances, and invoice financing. This method creates a debt that must be repaid but lets you maintain sole control of your business.

34. Equity Financing

The act of using investor funds in exchange for a piece or ”share” of your business is another way to raise capital. These funds can come from friends, family, angel investors, or venture capitalists.

Before deciding to use equity financing to raise the cash necessary for your business, decide how much control you are willing to share when it comes to decision-making and philosophy. Some investors will also want voting rights.

35. FICO Score

A FICO score is another type of credit score used by potential lenders for evaluating the wisdom of entering a contract with you and your business. FICO scores comprise a substantial part of the credit report that lenders use to assess credit risk. It was created by the Fair Isaac Corporation, hence the name FICO.

36. Financial Statements

An integral part of the loan application process is furnishing information that shows your business is a good credit risk. The standard financial statement packet includes four main reports: the income statement, the balance sheet, the statement of cash flow, and the statement of shareholders’ equity, if you have shareholders.

Lenders and investors want to see that your business is well-balanced with assets and liabilities, has positive cash flow, and will have capital to make expected repayments.

37. Fixed Interest Rate

The interest rate on a loan that is established in the beginning and does not change for the lifetime of the loan is said to be fixed. Loans with fixed interest rates are appealing to small business owners because the repayment amounts are consistent and easier to budget for in the future.

38. Floating Interest Rate

In contrast to the business finance term and definition fixed rate, the floating interest rate will change with market fluctuations. Also referred to as variable rates or adjustable rates, these amounts may often start out lower than the fixed rate percentages. This makes them more appealing in the short term if the market is trending down.

39. Guarantor

When starting a new small business, lenders might want you to provide a guarantor. This is an individual who guarantees to cover the balance owed on a debt if you or your business cannot meet the repayment obligation.

40. Interest Rate

All loans and other lending instruments are assigned the business finance key term interest rates. This is a percentage of the principal amount charged by the lender for the use of its money. Interest rates represent the current cost of borrowing.

41. Invoice Factoring or Financing

If your business has a significant amount of open invoices outstanding, you may contact a factoring company and have them purchase the invoices at a discount. By raising capital this way, there is no debt, and the factoring company assumes the financial responsibility for collecting the invoice debts.

42. Lien

This business finance term and definition is a creditor’s legal claim to the collateral pledged as security for a loan is called a lien.

43. Line of Credit

A lender may offer you an unsecured amount of funds available for your business to draw on when capital is needed. This line of credit is considered a short-term funding option, with a maximum amount available. This pre-approved pool of money is appealing because it gives you quick access to the cash.

44. Loan-to-Value

The LTV comparison is a ratio of the fair-market value of an asset compared to the amount of the loan that will fund it. This is another important number for lenders who need to know if the value of the asset will cover the loan repayment if your business defaults and fails to pay.

45. Long-Term Debt

Any loan product with a total repayment schedule lasting longer than one year is considered a long-term debt.

46. Merchant Cash Advance

A merchant may offer a funding method through a loan based on the business’s monthly sales volume. Repayment is made with a percentage of the daily or weekly sales. These tend to be short-term loans and are one of the costliest ways to fund your small business.

47. Microloan

Microloans are loans made through nonprofit, community-based organizations and they are most often for amounts under $50,000.

48. Personal Guarantee

If you’re seeking financing for a very new business and don’t have a high value asset to offer as collateral, you may be asked by the lender to sign a statement of personal guarantee. In effect, this statement affirms that you as an individual will act as guarantor for the business’s debt, making you personally liable for the balance of the loan even in the event that your business fails.

49. Principal

Any loan instrument is made of three parts—the principal, the interest, and the fees. The principal is a business finance key term and is the original amount that is borrowed or the outstanding balance to be repaid less interest. It is used to calculate the total interest and fees charged.

50. Revolving Line of Credit

This business finance term and definition is a funding option is similar to a standard line of credit. However, the agreement is to lend a specific amount of money, and once that sum is repaid, it can be borrowed again.

51. Secured Loan

Many lenders will require some form of security when loaning money. When this happens, this business finance term and definition is a secured loan. The asset being used as collateral for the loan is said to be “securing” the loan. In the event that your small business defaults on the loan, the lender can then claim the collateral and use its fair-market value to offset the unpaid balance.

52. Term Loan

These are debt financing tools used to raise needed funds for your small business. Term loans provide the business with a lump sum of cash up front in exchange for a promise to repay the principal and interest at specified intervals over a set period of time. These are typically longer term, one-time loans for start-up expenses or costs for established business expansion.

53. Unsecured Loans

Loans that are not backed by collateral are called unsecured loans. These types of loans represent a higher risk for the lender, so you can expect to pay higher interest rates and have shorter repayment time frames. Credit cards are an excellent example of unsecured loans that are a good option for small business funding when combined with other financing options.

54. Articles of Incorporation

This is legal documentation of the business’s creation, including name, type of business, and type of business structure or incorporation. This paperwork is one of the first tasks you will complete when you officially start your business. Once submitted, your articles of incorporation are kept on file with the appropriate governmental agencies.

55. Business Plan

Here is your tool for demonstrating how you want to establish your small business and how you plan to grow it into good financial health. When writing a business plan, it should include financial, operational, and marketing goals as well as how you plan to get there. The more specific you are with your business plan, the better prepared you will be in the long run.

56. Employer Identification Number (EIN) Certificate

In order to be more easily identified by the Internal Revenue Service, every business entity is assigned a unique number called an EIN. When you start your small business, an EIN will be assigned and mailed to the business address. This number never changes, and you will be asked to furnish it for many reasons.

57. Franchise Agreement

For a small business entrepreneur, entering into a franchise agreement with a larger company can be a way to enter the marketplace. The agreement made between you and the larger company gives you the right to operate as a satellite of the larger company in a certain territory for a given period of time. This lets you, the business owner, take advantage of a brand name that’s already familiar in the marketplace and a process or operation that has already been tested.

58. Net Worth

This business finance term and definition is an expression of your business’s total value, as determined by your total current assets less the total liabilities currently owed by the business. With your business’s most recent balance sheet in hand, you can calculate the net worth using a simple formula: Assets – Liabilities = Net Worth.

59. Retained Earnings

Just like it sounds, this term represents any profits earned that are retained in the business. This can also be referred to as bootstrapping.

60. Tax Lien

If your business fails to pay taxes owed to the designated government entity, namely the IRS, you may find your assets seized by the claim of a tax lien. The government can not only seize your assets for liquidation to resolve the tax debt, but they can also charge you penalties on the amount you owe.

Don’t Be Overwhelmed by Health Economics, Business and Finance Terms

As a small business owner, physicians are required to wear many different hats—often including that of chief financial officer or bookkeeper. Before you let yourself get intimidated by all the business terms and definitions, just remember that knowledge is power.

You can serve your small practice business, clinic, out-patient center or hospital most effectively by becoming familiar with terms used in business and finance and how they will affect your financial health. Armed with a basic understanding of business finance key terms, you will be prepared to face the financial challenges that go along with being a modern doctor, today!

Posted on February 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Nike is planning to restructure and lay off 2% of its staff, more than 1,500 people, as consumers pull back on spending.

***

If the total U.S. debt were divided by every household in the country, each household would get about $252,000, according to a September tweet from The Kobeissi Letter.

And, Jerome Powell, the Chair of the Federal Reserve, shared his concerns regarding the fiscal direction of the United States during a “60 Minutes” interview with Scott Pelley.

Powell said, “The U.S. is on an unsustainable fiscal path,” emphasizing that the growth of the national debt is outstripping the growth of the economy.

Despite the convenience of avoiding probate, a TOD account does not inherently provide tax benefits or protections against estate or inheritance taxes.

Upon your death, estate taxes may apply if the total value of your estate exceeds the federal exemption threshold, which is $13.61 million in 2024. Most people won’t come anywhere close to this level. However, a handful of states do impose inheritance taxes, which are paid by beneficiaries, though these exemption amounts are also generously high.

For capital gains, beneficiaries get a step-up in basis to the fair market value of the assets at the date of your death, which can provide significant tax benefits if the assets have appreciated in value.

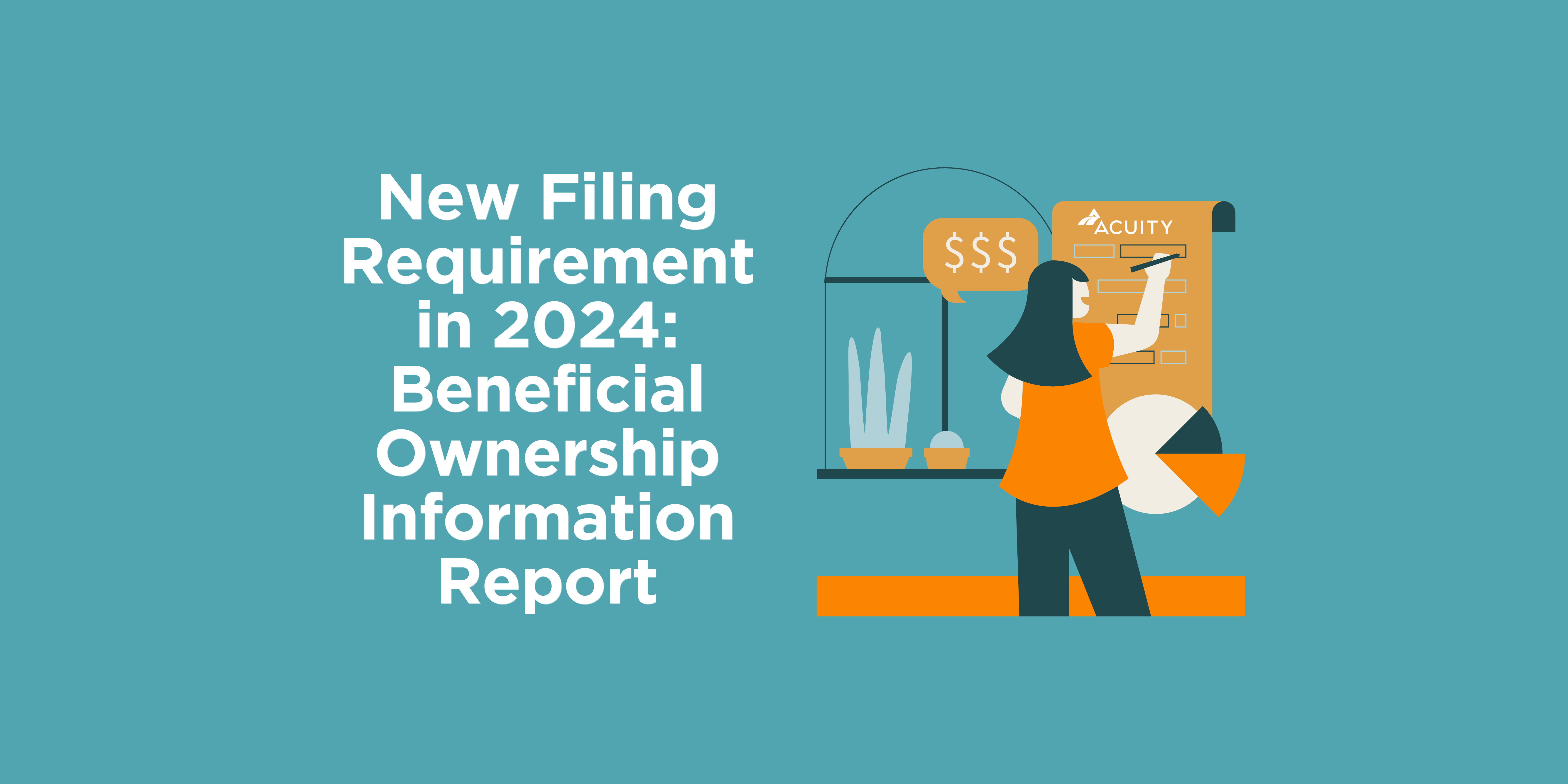

Posted on February 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Beneficial Ownership Information Report

IMPORTANT FOR DOCTORS, CONSULTANTS AND ADVISORS

By Staff Reporters

***

***

The BOI E-Filing System supports the electronic filing of the Beneficial Ownership Information Report (BOIR) under the Corporate Transparency Act (CTA). The CTA requires certain types of U.S. and foreign entities to report beneficial ownership information to the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury.

This notice is given under the Privacy Act of 1974 (Privacy Act) and the Paperwork Reduction Act of 1995 (Paperwork Reduction Act). The Privacy Act and Paperwork Reduction Act require that FinCEN inform persons of the following when requesting and collecting information in connection with this collection of information.

This collection of information is authorized under 31 U.S.C. 5336 and 31 C.F.R. 1010.380. The principal purpose of this collection of information is to generate a database of information that is highly useful in facilitating national security, intelligence, and law enforcement activities, as well as compliance with anti-money laundering, countering the financing of terrorism, and customer due diligence requirements under applicable law. Pursuant to 31 U.S.C. 5336 and 31 C.F.R. 1010.380, reporting companies and certain other persons must provide specified information. The provision of that information is mandatory and failure to provide that information may result in criminal and civil penalties. The provision of information for the purpose of requesting a FinCEN Identifier is voluntary; however, failure to provide such information may result in the denial of such a request.

Generally, the information within this collection of information may be shared as a “routine use” with other government agencies and financial institutions that meet certain criteria under applicable law. The complete list of routine uses of the information is set forth in the relevant Privacy Act system of record notice available at https://www.federalregister.gov/documents/2023/09/13/2023-19814/privacy-act-of-1974-system-of-records.

According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a valid OMB control number. The valid OMB control number for this information collection is 1506-0076. It expires on November 30, 2026.

The estimated average burden associated with this collection of information from reporting companies is 90 to 650 minutes per respondent for reporting companies with simple or complex beneficial ownership structures, respectively. The estimated average burden associated with reporting companies updating information previously provided is 40 to 170 minutes per respondent for reporting companies with simple or complex beneficial ownership structures, respectively. The estimated average burden associated with this collection of information from individuals applying for FinCEN identifiers is 20 minutes per applicant. The estimated average burden associated with individuals who have obtained FinCEN identifiers updating information previously provided is 10 minutes per individual.

***

***

Comments regarding the accuracy of this burden estimate, and suggestions for reducing the burden should be directed to the Financial Crimes Enforcement Network, P. O. Box 39, Vienna, VA 22183, Attn: Policy Division.

I’m a late career entry and 55 year old burned out doctor who wants out. Can I retire in 2 years with a pension of $6,100 a month (net). I have $825,000 in my 401(k) and 457 plan and a mortgage of $95,000 at 5.30%. I am not planning to move and will retire in place.

SOME THOUGHTS AND ANSWERS?

Congratulations on you solid retirement fund on top of a pending pension.

The first step you should take is to create a detailed budget for your retirement years. Consider expected living costs, healthcare expenses, travel and any other major expenses. Many folks make the mistake of setting up a monthly budget, but keep out significant milestones that are often costly, such as paying for a child’s college education or wedding.

Next, you should figure out your plan for housing. Mortgage payments, upkeep and taxes are important considerations. There was no mention of mortgage equity.

Another factor to take into account is state and Federal tax projections. If the 401(k) funds are all pre-tax dollars, any distributions will be taxable and there may be penalties if funds are withdrawn prior to 59 ½ years old. That will impact your retirement plan if you’re preparing to retire at 57-58.

It also sounds like you haven’t taken into account your Social Security allowance. It’s possible that your pension is one that comes with a government pension offset which would explain why you didn’t include it. On the other hand, maybe you’re thinking it’s far out enough that it doesn’t factor into your calculations?

Finally, you may want to look for a fee-only financial advisor that is paid directly by the client and doesn’t receive commissions for recommending financial products. So, advice is less biased. And get a fiduciary advisor which means they are required to put your best interests ahead of their own.

Also, someone with medical niche specificity. Good Luck!

***

NOTE: This is not an offer to buy or sell any security or interest. All investing involves risk, including loss of principal. Working with an adviser may come with potential downsides such as payment of fees (which will reduce returns). There are no guarantees that working with an adviser will yield positive returns. The existence of a fiduciary duty does not prevent the rise of potential conflicts of interest.

Posted on January 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

The stock markets were closed yesterday for MLK Day. But, with everyone there talking about AI, one stock to watch is Nvidia, which has continued to climb this year after soaring nearly 240% last year.

***

***

The Internal Revenue Service (IRS) has announced plans to launch a pilot plan, Direct File, providing a free method for U.S. workers to file their federal taxes. This new system aims to allow taxpayers to submit their federal tax returns at no cost through an in-house filing system. This development presents a significant challenge to tax preparation firms like TurboTax.

***

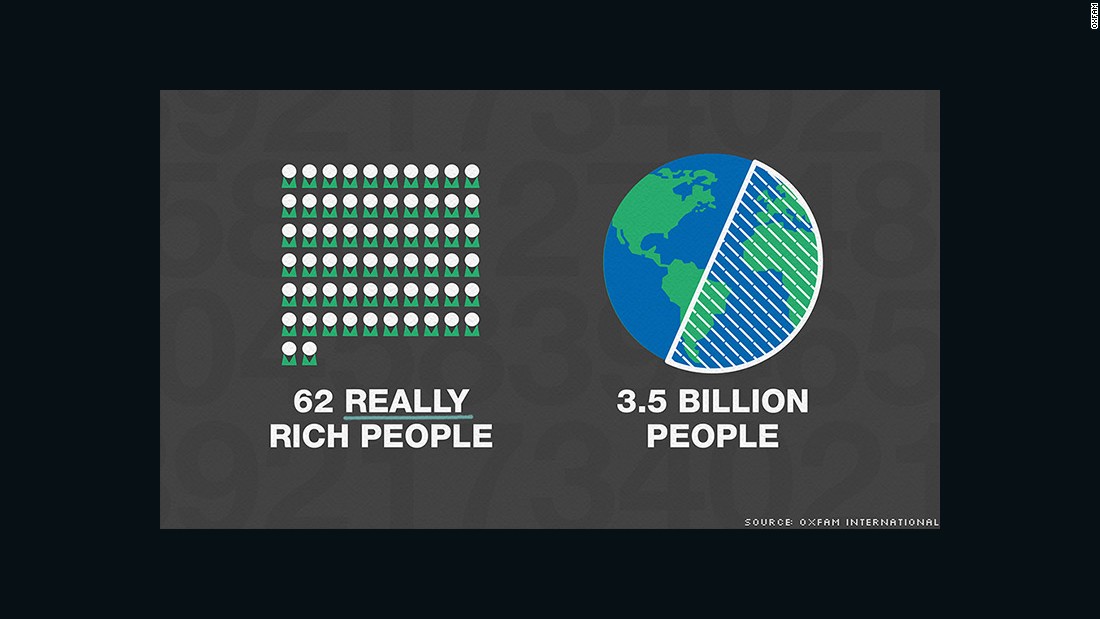

And, despite the IRS, it’s never a bad time to be rich. The world’s five richest people have more than doubled their wealth since 2020, according to Oxfam. Tesla’s Elon Musk, LVMH’s Bernard Arnault, Amazon’s Jeff Bezos, Oracle’s Larry Ellison, and Berkshire Hathaway’s Warren Buffett together had $405 billion in March 2020 compared to $869 billion as of November 2023, the charity group found.

Oxfam predicts that if things continue as they are, the world will see its first trillionaire within the next 10 years—though the anti-poverty group also noted that almost 5 billion people have become poorer over roughly the same period.

Posted on December 27, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

GOODBYE FORM 1099-Ks

By Staff Reporters

***

***

The IRS just said it is again delaying the implementation of a 2021 law that requires payment platforms such as Venmo, Paypal or Cash App to send tax forms called 1099-Ks to anyone who received more than $600 in the current tax year.

It’s the second consecutive year the IRS has delayed enacting the new regulation, after the tax agency last year pushed off the new law until 2023. On Tuesday, the IRS said it will push the regulation back another year “to reduce taxpayer confusion” after hearing from taxpayers, tax professionals and payment processors.

Posted on December 23, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Annual Gift Tax Exclusion Increased

Currently, you can give any number of people up to $17,000 each in a single year without taxation. For 2024, this will be increased to $18,000. For married couples, $36,000 will be available to be given to beneficiaries, tax-free, beginning next year.

Lifetime Gift Tax Exemption

Additionally, the IRS has announced that the lifetime estate and gift tax exemption will increase to $13.61 million in 2024. If a gift exceeds the annual limit ($17,000 this year, $18,000 in 2024), that does not automatically prompt a gift tax. The difference is simply taken from the person’s lifetime exemption limit and no taxes are owed.

Americans who owe back taxes will be given an incentive to pay up after the Internal Revenue Service it would waive nearly $1 billion in late-payment penalties. Roughly 4.6 million individual taxpayers who owe for tax years 2020 and 2021 will be eligible for the penalty relief. The IRS is extending the olive branch because it stopped sending out many collection letters during the pandemic. It hoped the letter halt would help struggling taxpayers and reduce its backlog. The long absence of these computer-generated letters had big consequences for taxpayers. Americans’ debt on unpaid back taxes had been growing with interest and penalties, and many were likely in the dark about just how much they owed.

Here is where the major benchmarks ended:

Here’s where the major benchmarks ended:

The S&P 500 index was up 27.81 points (0.6%) at 4,768.37; the Dow Jones Industrial Average was up 251.90 points (0.7%) at 37,557.92; the NASDAQ Composite® (COMP) was up 98.03 points (0.7%) at 15,003.22.

The 10-year Treasury note yield (TNX) was down about 3 basis points at 3.924%.

The CBOE® Volatility Index (VIX) was down 0.03 at 12.53.

Energy shares extended an early week rally behind a continued rebound in WTI Crude Oil futures (/CL), which rose for a fifth straight day and ended near a three-week high above $74 per barrel.

Banks and retailers were also particularly firm. The S&P 500 Retail Select Industry Index (SPSIRE) surged over 2% and ended at its highest level in over 10 months.

And, Tuesday’s big winner was Affirm, whose shares skyrocketed 15% after the buy now, pay later company announced it’s expanding its Walmart partnership to include the retailer’s self-checkout kiosks.

The IRS Quietly Changed the Rules on Children’s Inheritance

The IRS just issued Revenue Ruling 2023-2, which had a substantial impact on estate planning, particularly where an irrevocable trust is involved.

In the last decade or so, more families have begun utilizing irrevocable trusts to protect their assets from spend-down in order to qualify for government benefits, such as Medicaid and VA Aid and Attendance. Prior to the issuance of this ruling, it was unclear whether assets passing to beneficiaries through an irrevocable trust would receive a step-up in basis, thereby eliminating any capital gains taxes that would otherwise be owed.

Historically, assets that are disposed of during an individual’s lifetime are subject to capital gains taxes on the increase in value of that asset over time. The amount of capital gains owed is determined largely by the difference between the value at the time of purchase and the value at the time of transfer.

Delta Dental of California data breach exposed info of 7 million people

“Delta Dental of California and its affiliates are warning almost seven million patients that they suffered a data breach after personal data was exposed in a MOVEit Transfer software breach.Delta Dental of California provides 24 months of free credit monitoring and identity theft protection services to impacted patients to mitigate the risk of their exposed data.”

Posted on December 17, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: Section 179 of the U.S. IRS code is an immediate expense deduction that business owners can take for purchases of depreciating business equipment instead of capitalizing and depreciating the asset over a period of time. The Section 179 deduction can be taken if the piece of equipment is purchased or financed and the full amount of the purchase price is eligible for the deduction.

Not understanding parameters – Eligible property and annual limits

Medical practices may make mistakes by not fully understanding which types of property qualify for a Section 179 deduction. Section 179 is applicable only to assets used for business purposes. Failing to allocate assets properly can lead to improper deductions.

Eligible property for Section 179 may include:

Equipment, X-Ray, computers, fax machines, telephones, and other business property

Furniture and fixtures

Off-the-shelf-software that is used for business operations

Improvements to real-estate such as roofs, heating, ventilation, and air-conditioning.

Section 179 limits are updated annually, so it is important for doctors and practice owners to be aware of these limits and to plan accordingly.

Source: Natalie Westfall, Physicians Practice [12/4/23]

Posted on December 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: Income is the money you receive in exchange for your labor or products. Income may have different definitions depending on the context—for example, taxation, financial accounting, or economic analysis. For most people, income is their total earnings in the form of wages and salaries, the return on their investments, pension distributions, and other receipts. For businesses, income is the revenue from selling services, products, and any interest and dividends received with respect to their cash accounts and reserves related to the business. Economists have different definitions of income and different ways of measuring it, from focusing on earnings, savings, consumption, production, public finance, capital investment or other topics … Maybe?

WASHINGTON (Reuters) – The U.S. Supreme Court is set on Tuesday to consider a challenge to the legality of a tax targeting owners of foreign corporations that could undermine efforts at imposing a wealth tax on the very rich in a case that has already sparked controversy over a call for Justice Samuel Alito to recuse.

The justices are due to hear arguments in an appeal by Charles and Kathleen Moore – a retired couple from Redmond, Washington couple – of a lower court’s decision rejecting their challenge to the tax on foreign company earnings, even though those profits had not been distributed.

The one-time “mandatory repatriation tax” (MRT), which applied to taxpayers owning at least 10% of certain foreign corporations, was part of a 2017 Republican-backed tax bill signed into law by former President Donald Trump.

At issue in the case is whether this levy on unrealized gains is allowed under the U.S. Constitution’s 16th Amendment, which enabled Congress to “collect taxes on incomes.” The Moores, backed by the Competitive Enterprise Institute and other conservative and business groups, contend that “income” means only those gains that are realized through payment to the taxpayer, not a mere increase in the value of property.

SCOTUS will hear the “quadrillion-dollar” question?

Kicking off the Supreme Court this week will hear oral arguments today for a case that could upend the US tax code.

In Moore v. United States, the justices will be asked to decide whether the federal government can tax certain “unrealized gains”—assets that have yet to be sold.

Wall Street is gearing up for rate cuts. Yep! Twenty months after the Federal Reserve began a historic campaign against inflation, investors now believe there is a much greater chance that the central bank will cut rates in just four months than raise them again in the foreseeable future.

Interest-rate futures indicated last week a roughly 60% chance the Fed will lower rates by a quarter-of-a-percentage point by its May 2024 policy meeting, up from 29% at the end of October, according to CME Group data. The same data has pointed to four cuts by the end of the year. And, investors, battered by the Fed’s efforts to slow the economy, have reacted by driving the S&P 500 up nearly 9% this month. That is despite the wagers reflecting different possible paths for the economy, not all of them favorable for stocks.

Of course, investors look ahead to the release this week of key US inflation data that could provide a guide for the Federal Reserve’s plans for interest rates going into the new year.

The S&P 500 Index was down 8.91 points (0.2%) at 4,550.43; theDow Jones Industrial Average® (DJI) was down 56.68 points (0.2%) at 35,333.47; the NASDAQ Composite® was down 9.83 points (0.1%) at 14,241.02.

The 10-year Treasury note yield (TNX) was down about 10 basis points at 4.387%.

CBOE Volatility Index® (VIX) was up 0.23 at 12.69.

Transportation shares were among the weakest performers Monday, and energy was also soft behind a drop in crude oil futures. Weakness in many retail stocks suggested some concern over consumer spending given high interest rates and slower job growth. The S&P Retail Select Index (SPSIRE) fell 0.6% but is still up 8.2% for the month. Consumer discretionary and real estate shares were among the few gainers.

Posted on November 24, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Elevated mortgage rates are set to keep sellers of previously owned homes out of the market heading into next year, but sales will “bottom out” in early 2024, Fannie Mae said this week, before a rebound the following year.

Mortgage rates hovered near 8 percent as recently as October, the highest level it has hit since the turn of the millennium, which has scared used homeowners from selling their homes as many prefer to stay in lower rates secured in years past. This “lock in effect,” as Fannie Mae analysts describe it, has added to a depleted supply of homes available for buyers and helped push up prices.

Posted on November 23, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

***

Thanksgiving is a trading holiday. Both the New York Stock Exchange and the Nasdaq are closed. Black Friday, one of the biggest shopping days of the year, is a half day for the stock market. Both stock exchanges close at 1:00 p.m. ET, with eligible options trading until 1:15 p.m. Normal trading hours resume on the Monday after Thanksgiving, also known as Cyber Monday, when many online retailers host major sales.

***

***

Thanks to plummeting prices at the pump, US drivers will save a collective $1.2 billion this Thanksgiving travel period, and day, compared to last year, according to GasBuddy. The average price per gallon is down nearly 46 cents from a year ago, and more than 50,000 stations now show gas prices at $2.99/gallon or less.

***

Narrow traffic lanes are safer than wide ones. Researchers at Johns Hopkins analyzed more than 1,000 streets in seven major cities across the US and found that narrower roads mitigated traffic collisions in certain conditions. The study did not find a significant difference between roads 9-feet wide and those 10- or 11-feet wide, but it did conclude that traffic accidents increase 1.5x when a road widens from 9 feet to 12 feet. Traffic fatalities are the leading cause of death for Americans aged 1–54.

***

Walgreens will close most of its pharmacies and stores on Thanksgiving Day for the first time in the company’s history, executives said last Thursday. The move to close more than 8,700 stores for the federal holiday comes as some Walgreens workers staged a three-day walkout this fall to push for improved working conditions and increased staffing numbers, Reuters reported.

***

***

Here is where the major benchmarks ended on Wednesday:

The S&P 500 Index was up 18.43 points (0.4%) at 4,556.62, near a four-month high close; the Dow Jones Industrial Average®(DJI) was up 184.74 points (0.5%) at 35,273.03; the NASDAQ Composite was up 65.88 points (0.5%) at 14,265.86.

The 10-year Treasury note yield (TNX) was down about 1 basis point at 4.41%, after earlier dropping to a two-month low under 4.37%.

CBOE Volatility Index (VIX) was down 0.50 at 12.85.

Communications services and technology were among the strongest performers Wednesday. Food and beverage companies were also firm. Energy shares were among the weakest performers Wednesday behind a drop of over 1% in WTI Crude Oil futures (/CL). ), which fell following reports OPEC delayed a weekend meeting until November 30th, a possible reflection of cartel members struggling to reach consensus over production cuts. WTI crude ended just under $77 a barrel, down 19% from a 2023 high above $95 in late October.

Posted on November 12, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

The Institute of Medical Business Advisors is a leading national scope provider of healthcare economics, finance, investing, managerial accounting, policy, management and business administration education and medical practice management textbooks, reports, hand-books, dictionaries, journals, white-papers, fair-market valuations [FMV] and legal advisory opinions using multi-platform and traditional seminars and channels of knowledge distribution. iMBA helps the nation’s financial, healthcare and education professionals make decisive improvements in their direction and performance by empowering them through unbiased information, consultants and proprietary tools, books, templates and B-school styled case models.A virtuous “win-win” situation for all concerned.

The firm serves universities, medical, business, graduate and nursing schools; physicians, dentists, attorneys and legal societies – accountants, financial service providers, stock brokers, RIAs, wealth and hedge fund managers – emerging entities, hospitals, clinics, outpatient centers, CXOs and their BODs – the press, media and related academic entities.

Posted on November 8, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

US credit card balances have jumped to a record $1.08 trillion, according to the New York Federal Reserve.

Nevertheless, Stocks rose for the seventh straight day on Tuesday, giving the NASDAQ and S&P 500 their longest winning streaks since 2021. The surge was fueled by a rally in Big Tech and a growing consensus that the Federal Reserve Bank is done raising interest rates. Chief among the tech revelers was Microsoft, which finished the day at an all-time high amid strong demand for its cloud computing services.

Kaiser Permanente continues to rebound from a rough 2022 and pulled in $239 million in net income in Q3. That marks a dramatic turnaround from the $1.5 billion net loss the integrated system had seen a year prior.

Finally, family physicians utilizing value-based payment (VBP) models reported burnout relief in a study from EHR company Elation Health and the American Academy of Family Physicians.Burnout among providers decreased once practices passed a threshold of 75% financial investment in VBP models.

Posted on November 3, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Even though the Federal Reserve announced its interest rate decision yesterday, Jerome Powell wasn’t the government official investors were most anxious to hear from.

Instead, he was upstaged by Treasury Secretary Janet Yellen, who gave an update on the size of upcoming bond auctions. Although many were concerned about the US selling new debt into a market where interest rates are high and demand for bonds has flagged (pushing yields way up), the market liked what she had to say.

Yellenexplained that the government would focus on shorter-term notes rather than longer-term ones, which prompted a rally for 10 and 30 year bonds.

Hospital and health system deal activity is finally starting to rebound following a pandemic-era plunge, according to consulting firm Kaufman Hall, but hospitals are increasingly citing “financial distress” as the reason behind the deals.

In more than a third of the 18 hospitals and health systems deals made in Q3 2023—including mergers and acquisitions (M&A) and partnerships—at least one party cited financial distress as the impetus for the transaction. That figure is “well above historical benchmarks,” according to the firm.

“Hospitals and health systems have been under extreme financial pressure since 2022, when median operating margins remained in negative territory for the full year,” Kaufmann Hall analysts wrote in an October 12 report. “These challenges are reflected in the 39% percent of announced transactions in Q3 in which a party has cited, or publicly available information has enabled Kaufman Hall to infer, an element of financial distress as a transaction driver.”

Posted on October 18, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The IRS recently announced some welcome news for higher-income workers with 401-k[s] and similar retirement plans. The agency delayed implementing a new rule that would have required catch-up contributions made by people earning over $145,000 to be directed into an after-tax Roth account.

The S&P 500 Index was down 0.43 point at 4,373.20; the Dow Jones Industrial Average was up 13.11 points at 33,997.65; the NASDAQ Composite (COMP) was down 34.24 points (0.3%) at 13,533.75.

The 10-year Treasury note yield was up about 13 basis points at 4.84%.

CBOE’s Volatility Index (VIX) was up 0.68 at 17.89.

Technology shares were among the market’s weakest performers Tuesday, with the Philadelphia Semiconductor Index (SOX) dropping more than 1%. Banks and retailers did better.

The KBW Regional Banking Index (KRX) rose 2% to end near a four-week high. Small-cap stocks were also higher, with the Russell 2000 Index (RUT) gaining more than 1%.

Posted on October 9, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

The Institute of Medical Business Advisors is a leading national scope provider of healthcare economics, finance, investing, managerial accounting, policy, management and business administration education and medical practice management textbooks, reports, hand-books, dictionaries, journals, white-papers, fair-market valuations [FMV] and legal advisory opinions using multi-platform and traditional seminars and channels of knowledge distribution. iMBA helps the nation’s financial, healthcare and education professionals make decisive improvements in their direction and performance by empowering them through unbiased information, consultants and proprietary tools, books, templates and B-school styled case models.A virtuous “win-win” situation for all concerned.

The firm serves universities, medical, business, graduate and nursing schools; physicians, dentists, attorneys and legal societies – accountants, financial service providers, stock brokers, RIAs, wealth and hedge fund managers – emerging entities, hospitals, clinics, outpatient centers, CXOs and their BODs – the press, media and related academic entities.

Posted on October 9, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Be alert and ready for the S&P 500 to crash by 50%, house prices to slide, and a recession to strike, Jeremy Grantham says.

***

***

***

It has been a difficult couple of years for BlackRock, the world’s biggest money manager. The firm is still enormously profitable, though it has recently taken some big hits because of its promotion of ESG investments.

Under a new proposal from the Post Office, the cost of a First Class stamp would rise to $.68 from $.66. The price was increased from $.63 to $.66 in July. Last January, the price rose from $.60 to $.63. If the new plan is accepted, First Class mail prices will rise 13% over the period.

As a new physician investor, it’s important to know the distinctions between like measurements because the market allows firms to advertise their numbers in ways not otherwise regulated. Often companies will publicize their numbers using either GAAP or non-GAAP measures. GAAP, or generally accepted accounting principles, outlines rules and conventions for reporting financial information. It is a means to standardize financial statements and ensure consistency in reporting.

When a company publicizes its earnings and includes non-GAAP figures, it means it wants to provide investors with an arguably more accurate depiction of the company’s health (for instance, by removing one-time items to smooth out earnings). However, the further a company deviates from GAAP standards, the more room is allocated for some creative accounting and manipulation.

When looking at a company that is publishing non-GAAP numbers, new physician investors should be wary of these pro forma statements, because they may differ greatly from what GAAP deems acceptable.

GAAP is set forth in 10 primary principles, as follows:

Principle of consistency: This principle ensures that consistent standards are followed in financial reporting from period to period.

Principle of permanent methods: Closely related to the previous principle is that of consistent procedures and practices being applied in accounting and financial reporting to allow comparison.

Principle of non-compensation: This principle states that all aspects of an organization’s performance, whether positive or negative, are to be reported. In other words, it should not compensate (offset) a debt with an asset.

Principle of prudence: All reporting of financial data is to be factual, reasonable, and not speculative.

Principle of regularity: This principle means that all accountants are to consistently abide by the GAAP.

Principle of sincerity: Accountants should perform and report with basic honesty and accuracy.

Principle of good faith: Similar to the previous principle, this principle asserts that anyone involved in financial reporting is expected to be acting honestly and in good faith.

Principle of materiality: All financial reporting should clearly disclose the organization’s genuine financial position.

Principle of continuity: This principle states that all asset valuations in financial reporting are based on the assumption that the business or other entity will continue to operate going forward.

Principle of periodicity: This principle refers to entities abiding by commonly accepted financial reporting periods, such as quarterly or annually.

Earnings before interest, taxes, depreciation, and amortization

A company’s earnings before interest, taxes, depreciation, and amortization is an accounting measure calculated using a company’s earnings, before interest expenses, taxes, depreciation, and amortization are subtracted, as a proxy for a company’s current operating profitability. Though often shown on an income statement, it is not considered part of the Generally Accepted Accounting Principles by the SEC.

Posted on October 3, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On September 18, 2023, the Journal of the American Medical Association (JAMA) published a study comparing online hospital pricing and pricing given over the telephone for shoppable hospital services. Hospitals in the U.S. are required to post pricing online for specified services, but it was unknown whether or not hospitals quoted the same prices to telephone callers as they posted online.

This Health Capital Topics article will discuss the topic of price discrepancy and the difficulties with cost comparison. (Read more…)

Posted on October 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

The stock markets ended Q3 last week with a whimper despite new data showing that the Fed’s favorite CPI inflation measure cooled in August. September was the worst month of the year for the S&P 500 and the NASDAQ. But Blue Apron soared on the news that it’s being bought by Wonder Group, a food delivery startup helmed by a former Walmart exec.

America’s debt today stands at $33 trillion, a figure some politicians, finance mavens and everyday citizens find astonishingly high.

***

Carmot Therapeutics, which is developing drugs for diabetes and weight-loss, is reportedly mulling an IPO or possible sale to a large pharmaceutical company at a valuation of at least $1B. The biotech company has two injectable GLP-1 drug candidates in Phase 2 development for type 1 and type 2 diabetes, according to the company’s website.

Carmot enlisted JP Morgan and Bank of America as underwriters on an IPO, which could come as early as this year if market conditions are favorable. The company has also received “takeover interest” from large drug makers at a valuation of over $1B, according to a Bloomberg report. Carmot had a post-money valuation of $1.25B following a $150M funding round in May, Bloomberg added.

Posted on October 1, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

CPI: Here’s a breakdown of how different aisles and departments rose over the past 12 months:

Cereals and bakery: increase 6%

Meats, poultry, fish, and eggs: unchanged

Remaining products (ranging from dairy to beverages): increase 0.3% to 4.8%

Food in general is up 4.3%

Food away from home: increase 6.8%

Used cars and trucks fell 1.2% year-over-year, but new cars and trucks rose 0.3%. Those may not seem like much, but a new car still costs an average of more than $48,000 — as of May 2023 only three models were available in the U.S. market for $20,000 or less.

Transportation similarly rose 10.3% over the same period but shelter, which rose 7.3%, “was the largest factor in the monthly increase in the index for all items less food and energy,” according to the August CPI.

Not to put a damper on your Sunday morning (the relentless rain is already doing that to the North East USA), but the government still appears headed for a shutdown. Among the immediate impacts: Many federal employees will be furloughed, the IRS will stop picking up your calls, you won’t be able to get married in DC courts, and most national parks—and their social media handles—will go dark.

And even more rain as New York City was hit with its heaviest rain in decades, which flooded roads and subway stations and delayed air travel. Both the mayor and New York’s governor declared states of emergency as images of the waterlogged city filled social media.

***

It appears that Mark Zuckerberg’s new “Threads” social media platform is struggling with a massive decline. The social media platform called “Threads” was launched by Facebook (now called Meta). The platform is essentially a clone of Elon Musk’s Twitter, which is now called X. Threads struggling to maintain momentum and gain new users.

Among major social platforms, Threads is reportedly only ahead of Tumblr in the race for user acquisition. Forecasts by Insider Intelligence predict a U.S. user base of 23.7 million for Threads in 2023. The company reportedly anticipated 56.1 million U.S. users. In comparison, X has roughly 528.3 million monthly users.

Short-term goals (less than 12 months) require liquidity or short-term assets. These assets include cash, checking and saving accounts, certificates of deposit, and money market accounts. These accounts have two things in common. The principal is guaranteed from risk of loss, and pay a very low interest rate. As an investment, they are considered substandard and one would only keep what is actually needed for liquidity purposes in these accounts.

[B] Long-Term Assets

Longer-term assets (more than 12 months) include real estate, mutual funds, retirement plans, stocks, and life insurance cash value policies. Bonds may also be an appropriate long-term investment asset for a number of reasons, for example, if you are seeking a regular and reliable stream of income or if you have no immediate need for the amount of the principal invested. Bonds also can be used to diversify your portfolio and reducing the overall risk that is inherent in stock investments.

[C] Short-Term Liabilities

Short-term liabilities (less than 12 months) include credit card debt, utility bills, and auto loans or leasing. When a young doctor leaves residency and starts practice, the foremost concern is student debt. This is an unsecured debt that is not backed by any collateral, except a promise to pay. There are recourses that an unsecured creditor can take to recoup the bad debt. Usually, if the unsecured creditor is successful obtaining a judgment, it can force wages to be garnished, and the Department of Education can withhold up to ten percent of a wages without first initiating a lawsuit, if in default. It is also probable that young medical professionals have been holding at least one credit card since their sophomore year in college. Credit card companies consider college student the most lucrative target market and medical students hold their first card for an average of fifteen years. There are several other types of other unsecured debt, including department store cards, professional fees, medical and dental bills, alimony, child support, rent; utility bills, personal loans from relatives, and health club dues, to name a few.

[D] Long-Term Liabilities

A secured debt, on the other hand, is debt that is pledged by a specific property. This is a collateralized loan. Generally, the purchased item is pledged with the proceeds of the loan. This would include long-term liabilities (more than 12 months) such as a mortgage, home equity loan, or a car loan. Although the creditor has the ability to take possession of your property in order to recover a bad debt, it is done very rarely. A creditor is more interested in recovering money. Sometimes, when borrowing money, there may be a requirement to pledge assets that are owned prior to the loan.

For example, a personal loan from a finance company requires that you pledge all personal property such as your car, furniture, and equipment. The same property may become subject to a judicial lien if you are sued and a judgment is made against you. In this case, you would not be able to sell or pledge these assets until the judgment is satisfied.

A common example of a lien would be from unpaid federal, state or local taxes. Doctors can be found personally liable for unpaid payroll taxes of employees in their professional corporations. Be aware that some assets and liabilities defy short or long-term definition. When this happens, simply be consistent in your comparison of financial statements, over time.

[E] Personal Physician Net Worth

Once the value of all personal assets and liabilities is known, net worth can be determined with the following formula: Net worth = assets minus liabilities. Obviously, higher is better. In The Millionaire Next Door, Thomas H. Stanley, PhD, and William H. Danko give the following benchmark for net worth accumulation. Although conservative for physicians of a past generation, it may be more applicable in the future because of current managed care environment.

Here is the guide: Multiple your age by your annual pre-tax income from all sources – except inheritances – and divide by ten.

Real-Life Medical Example:As an HMO pediatrician, Dr. Curtis earned $ 60,000 last year. So, if she is 35, her net worth should be at least $ 210,000.

How do you get to that point? In a word, consume less, save more and watch the student loans. Stanley and Danko found that the typical millionaire set aside 15 percent of earned income annually and has enough invested to survive 10 years, at current income levels if he stopped working. Now, if Dr. Curtis lost her job tomorrow, how long could she pay herself the same salary?

[F] Common Liability Management Mistakes

A common liability management mistake is not recognizing when you are heading for trouble. If doctors are paying only the minimum payments on credit card debt, while continuing to charge purchases at a rate faster than the pay-down, trouble is brewing. If you don’t categorize your debt, you could find yourself paying down non-priority debt while ignoring priority debt.

A priority debt is one that is essential or subject to serious consequences, if not paid. Examples include rent, mortgage payments, utility bills, child support, car payments, unpaid taxes, and other secured debt. If in one month, a doctor had to choose between paying his accounting bill or his rent, it would be essential to pay the rent.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Several years ago a group of highly trusted and deeply experienced financial services professionals and estate planners noted that far too many of their mature physician clients, using traditional stock brokers, management consultants and financial advisors, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse relationship was noted, and dubbed the “Doctor Effect.” In others words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning and medical practice management, continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization was a confirmation of the industry culture which seemed to be: Bread for the advisor – Crumbs for the client!

And so, at D.E. Marcinko & Associates, our informed cadre’ of technology focused and highly educated doctors, nurses, financial advisors, attorneys, accountants, psychologists and educational visionaries decided there must be a better way for healthcare colleagues to receive financial planning advice, products and related management services within a culture of fiduciary responsibility.

We trust you agree with this ME Inc, and Certified Medical Planner™ consulting philosophy, as illustrated on our website.

Posted on September 18, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

For the third straight year, US incomes fell, according to new Census Bureau data. In 2022, the median household income fell to $74,580, adjusted for inflation. That’s a 2.3% decline from 2021’s median estimate of $76,330, according to the Census Bureau. And the latest figures mark a 4.7% drop from a 2019 peak of $78,250.

Meanwhile, earnings for both part-time and full-time workers fell 2.2% between 2021 and 2022. For full-time, year-round workers, median earnings dropped 1.3% in 2022.

One small bright spot: The Gini index, a measure of income inequality, modestly improved. The income gap between high- and low-income households decreased by 1.2% between 2021 and 2022, marking the first annual decrease since 2007.

In all, though, the latest Census data provides a snapshot of American households’ economic troubles, and the abundance of cash-strapped workers has created new challenges for CFOs.

Posted on September 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Yesterday was the first day of trade group America’s Health Insurance Plans 2023 Consumer Experience & Digital Health Forum, a two-day conference focused on emerging digital health innovations and how they’re changing the consumer experience of the US healthcare system.

According to Bankrate’s extensive research, the average cost of auto insurance in the U.S. is $2,014 per year. Minimum coverage, on the other hand, has an average annual cost of $622. However, car insurance is like a fingerprint. Although your circumstances may seem similar, your personalized rating factors will cause your premium to vary from that of friends, family and the national average. Still, knowing the average cost of car insurance might give you the information you need to ensure you’re not overpaying for this necessary financial protection.

***

The average cost of new cars is now well over $48,000—up almost $6,000 from two years ago and about $10,000 from September 2020, according to Kelley Blue Book.

Posted on September 13, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

REMINDER

***

***

Starting in 2026, high-income earners over the age of 50 who make more than $145,000 can no longer make catch-up contributions to regular 401(k)s. Instead, those catch-ups will head to Roth accounts. That carries significant tax implications.

Here is where the major benchmarks ended yesterday:

The S&P 500® Index (SPX) was down 25.56 points (0.6%) at 4,461.90; the Dow Jones Industrial Average (DJIA) was down 17.73 points at 34,645.99; the NASDAQ Composite was down 144.28 points (1.0%) at 13,773.61.

The 10-year Treasury note yield (TNX) was down about 2 basis points at 4.272%.

CBOE’s Volatility Index (VIX) was up 0.42 at 14.22.

While tech was the weakest performing sector Tuesday, consumer discretionary and communication services shares were also lower. Energy shares led sector gainers Tuesday as oil prices continued to rise.

The Philadelphia Oil Service Index (OSX) gained more than 2% and ended at its highest level since April 2019. WTI crude futures, the U.S. benchmark, extended gains to near $90 a barrel after OPEC, in a report, slightly increased its forecasts for global consumption in 2023 and 2024.

Posted on September 9, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The IRS just announced that it is launching an effort to aggressively pursue 1,600 millionaires and 75 large business partnerships that owe hundreds of millions of dollars in past due taxes. IRS Commissioner Daniel Werfel said that with a boost in federal funding and the help of artificial intelligence tools, the agency has new means of targeting wealthy people who have “cut corners” on their taxes.

“If you pay your taxes on time it should be particularly frustrating when you see that wealthy filers are not,” Werfel told reporters in a call previewing the announcement. He said 1,600 millionaires who owe at least $250,000 each in back taxes and 75 large business partnerships that have assets of roughly $10 billion on average are targeted for the new “compliance efforts.”

Werfel said a massive hiring effort and AI research tools developed by IRS employees and contractors are playing a big role in identifying wealthy tax dodgers. The agency is making an effort to showcase positive results from its burst of new funding under President Joe Biden’s Democratic administration as Republicans in Congress look to claw back some of that money.

“New tools are helping us see patterns and trends that we could not see before, and as a result, we have higher confidence on where to look and find where large partnerships are shielding income,” he said.

***

Here is where the major benchmarks ended:

The S&P 500 Index was up 6 points (0.1%) at 4,457.49, down 1.3% for the week; the Dow Jones Industrial Average (DJIA) was up 76 points (0.2%) at 34,576.59, down 0.8% for the week; the NASDAQ Composite was up 13 points (0.1%) at 13,761.53, down 1.9% for the week.

The 10-year Treasury note yield (TNX) remained unchanged at 4.26%.

CBOE’s Volatility Index (VIX) was down 0.56 at 13.84.

Energy shares were among the market’s strongest performers this week on expectations the recent rally in crude oil prices to 10-month highs will boost profits. The Philadelphia Oil Service index (OSX) has gained 5% so far this month and ended Friday at its highest level since April 2019. Utilities and regional banks were also firm.

Retail and transportation sectors were among the weakest performers, and small-cap stocks also took pressure, with the Russell 2000 (RUT) down 3.7% for the week.

Posted on August 27, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to the Institute of Taxation and Economic Policy (ITEP), more than one in four dollars of wealth in the U.S. is held by a small fraction of households with a net worth of over $30 million.

ITEP suggested a nationwide tax of 2% on wealth over $30 million could have raised nearly $415 billion if it were in effect, and a similar tax applying only to wealth in excess of $1 billion could have raised $62 billion. This would only affect 1 in 400 households — or 0.25% of the population

Posted on August 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

AUGUST 21st

By Dr. David Edward Marcinko MBACMP

***

It’s National Report Upcoding Fraud Day, an initiative started in 2017 to support whistleblowers of Medicare fraud, which costs the US billions of dollars each year. If you need any encouragement to report suspected healthcare fraud (like upcoding or inflated Medicare reimbursement claims), here’s your chance.