BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

If you’ve ever listened to an early morning financial news broadcast, you’ve heard a reference to “futures” and how they affect the stock market before it opens. Physicians Investors follow the futures because it provides an indication of where stocks are headed at the opening bell. One of the most widely followed futures is the Dow Futures, whose underlying value is based on the Dow Jones Industrial Average, an index of 30 major U.S. companies.

***

***

DEFINITION: After the markets close at 4 pm New York time, implied open prices of the Dow Jones Industrial Average, S&P 500 Index, and NASDAQ, which fluctuate from minute to minute, can be calculated.

Considering the DJIA as an example, the basis of calculating implied open is the price of a “DJX index option futures contract “.

Posted on October 5, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

FORPHYSICIAN INVESTORS

By David Belk MD

Health Insurance Company Financial Index

Below is a listing of the Nine largest for-profit health insurance Companies. The Annual financial statements are linked to the year for each Company and a four page summary report is linked to the name of the health insurance company at the top of the listing.

The relevant pages in each financial statement I used to prepare my summaries are listed next to each year’s statement. Aetna and Coventry’s summaries are combined because they merged in 2012. Health Net also Merged with Centene in 2016 leaving only seven major health insurance companies.

A decentralized autonomous organization (DAO), sometimes called a decentralized autonomous corporation (DAC), is an organization represented by rules encoded as a computer program that is transparent, controlled by the organization members and not influenced by a central government. A DAO’s financial transaction record and program rules are maintained on a blockchain. The precise legal status of this type of business organization is unclear.

A well-known example, intended for venture capital funding, was The DAO, which launched with $150 million in crowdfunding in June 2016, and was nearly immediately hacked and drained of US$50 million in cryptocurrency. The hack was reversed in the following weeks, and the money restored, via a hard fork of the Ethereum blockchain: the Ethereum miners and clients switched to the new fork.

A Ponzi scheme (/ˈpɒnzi/, Italian: [ˈpontsi]) is a form of fraud that lures investors and pays profits to earlier investors with funds from more recent investors. Recall Bernie Madoff.

The scheme leads victims to believe that profits are coming from legitimate business activity (e.g., product sales or successful investments), and they remain unaware that other investors are the source of funds. A Ponzi scheme can maintain the illusion of a sustainable business as long as new investors contribute new funds, and as long as most of the investors do not demand full repayment and still believe in the non-existent assets they are purported to own.

A pyramid scheme is a business model that recruits members via a promise of payments or services for enrolling others into the scheme, rather than supplying investments or sale of products. As recruiting multiplies, recruiting becomes quickly impossible, and most members are unable to profit; as such, pyramid schemes are unsustainable and often illegal.

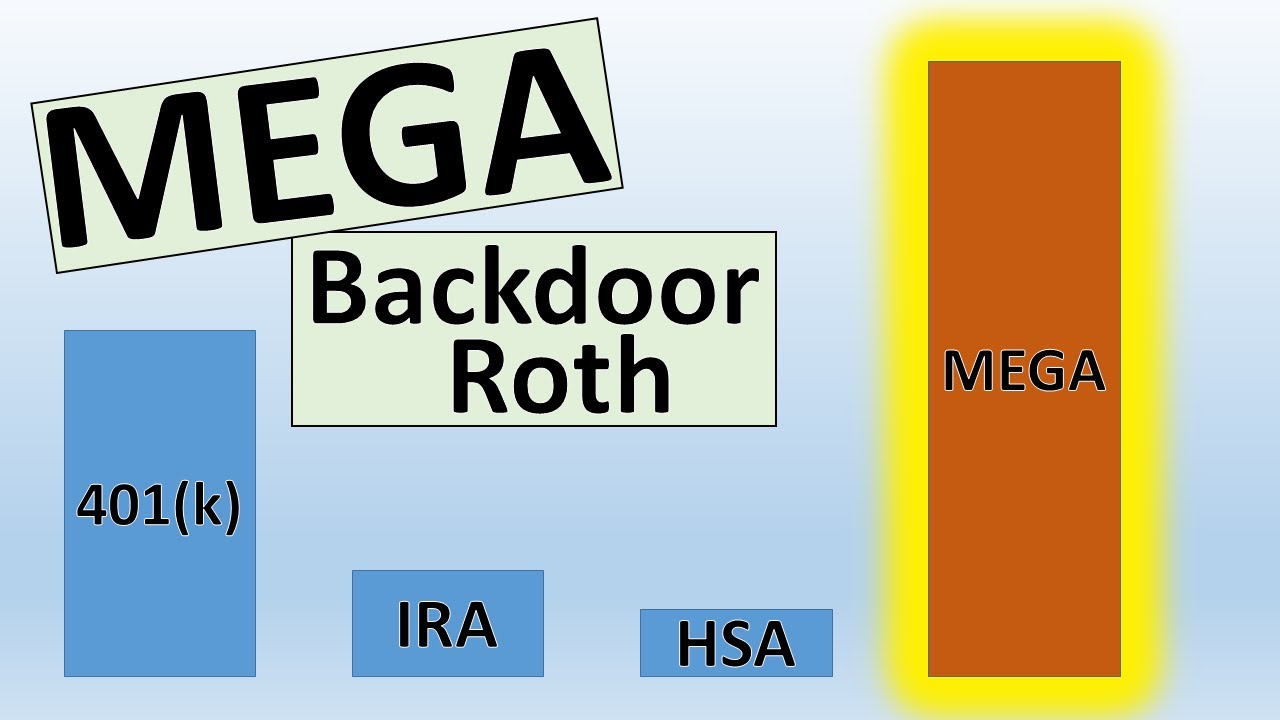

If you’re a physician looking to get ahead on planning for retirement, you’re likely familiar with individual retirement accounts, or IRAs. An IRA is a tax-advantaged vehicle that helps you grow your retirement savings. Roth IRAs are particularly attractive, because you don’t pay taxes on withdrawals in retirement.

There’s one problem: you can’t contribute to a Roth IRA directly if you make above a certain income. A backdoor IRA, though, can solve your problem by allowing you to convert a traditional IRA into a Roth.

Here’s how it works:

First, place your contribution in a traditional IRA—which has no income limits.

Then, move the money into a Roth IRA using a Roth conversion.

But make sure you understand the tax consequences before using this strategy.

The mega backdoor Roth allows you to put up to $38,500 in a Roth IRA or Roth 401(k) in 2021, on top of the regular contribution limits for those accounts. If you have a Roth 401(k) at work (and the plan allows for the mega option as described below), generally you can choose whether the final destination of your mega contributions is the Roth 401(k) or a Roth IRA. If your employer offers only a traditional 401(k), then your mega contributions would end up in a Roth IRA.

Here’s a quick summary of what you need to have in place for the ideal mega backdoor Roth strategy:

A 401(k) plan that allows “after-tax contributions.” After-tax contributions are a separate bucket of money from your traditional and Roth 401(k) contributions. About 43% of 401(k) plans allow after-tax contributions, according to a 2017 survey of large and midsize employers by consulting firm Willis Towers Watson.

Your employer offers either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan. If you’re not sure, ask your human resources department or plan administrator.

You’ve got money left over to save, even after maxing out your regular 401(k) and Roth IRA contributions.

Do your children have income-generating assets in a custodial account?

If so, be sure you understand the so-called kiddie tax.

This law was passed to discourage wealthier individuals from transferring assets to their children to take advantage of their lower tax rates. The kiddie tax has seen many iterations but current rules tax a minor child’s unearned income—including capital gains distributions, dividends, and interest income—at the parents’ tax rate if it exceeds the annual limit ($2,200 in 2021).

The tax applies to dependent children under the age of 18 at the end of the tax year (or full-time students younger than 24) and works like this:

The first $1,100 of unearned income is covered by the kiddie tax’s standard deduction, so it isn’t taxed.

The next $1,100 is taxed at the child’s marginal tax rate.

Anything above $2,200 is taxed at the parents’ marginal tax rate.

So – If your child also has earned income, say from a summer job or legitimate work in your medical office or practice, the rules become more complicated.

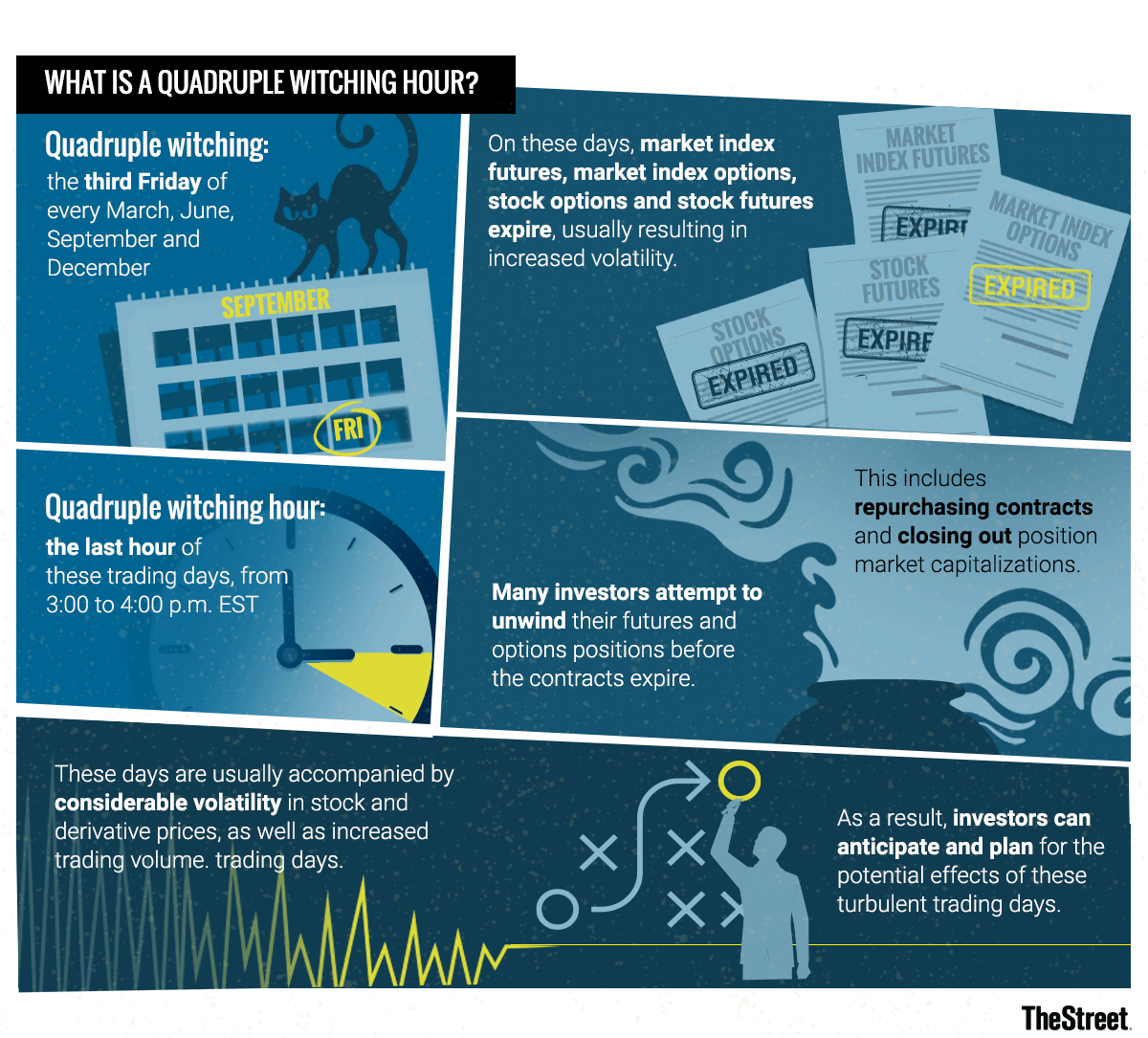

Markets: While yesterday was somewhat of a snoozefest on Wall Street, today should be more interesting. In a quarterly event known as “quadruple witching,” stock options, index options, stock futures, and index futures all expire on the same day, which can produce fireworks.

The phrase quadruple witching brings to mind stories that begin, “It was a dark and stormy night…” or folkloric visions of witches flying chaotically on broomsticks across the brightness of a moon.

In the context of investing, quadruple witching also refers to possible chaos but chaos in the financial markets. Such chaos can erupt due to four different types of contracts on financial assets expiring on the same day. The quadruple witching hour is the last hour of the trading session on that day. The question is whether investors can make abnormally robust profits on quadruple witching days due to market fluctuations.

What Is Quadruple Witching?

Quadruple witching refers to four days during the calendar year when the contracts on four different kinds of financial assets expire. The days are the third Friday of March, June, September and December. The assets on which the contracts expire on that day are stock options, single stock futures, stock index futures and stock index options. Options contracts also expire monthly. Futures contracts expire quarterly.

Because all four types of contracts expire on the same day, the quadruple witching day usually sees a heavier volume of trading. This is why the reference to chaos is made about this witching day. Market volume is increased partly due to offsetting trades that are made automatically. Volume on quadruple witching days has increased roughly two-thirds of the time since 2005.

Recent Quadruple Witching Expiration Day

On June 18, 2021, a quadruple witching day, a near-record volume of single-stock equity options was set to expire at the end of the day in the amount of $818 billion. As a result, a near-record of single stock open interest of about $3 trillion stood on June 18, 2021. Open interest refers to how many contracts are open during any given point during the day. It is an important metric for traders to watch since a large amount of open interest can move the value of the underlying stock.

Taking a distribution from a tax qualified retirement plan, such as a 401(k), prior to age 59 1/2 is generally subject to a 10 percent early withdrawal tax penalty.

However, the IRS rule of 55 may allow you to receive a distribution after attaining age 55 (and before age 59 1/2 ) without triggering the early penalty if your plan provides for such distributions.

The distribution would still be subject to an income tax withholding rate of 20 percent, however. (If it turns out that 20 percent is more than you owe based on your total taxable income, you will get a refund after filing your yearly tax return.)

Posted on September 16, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ByBertalan Meskó, MDPhD

Elizabeth Holmes has no idea how much damage she has done with Theranos. As I often wrote, for digital technologies to gain ground and become part of our everyday lives, we need not only technological solutions but a cultural paradigm shift. Holmes rolled a massive rock in front of it.

Similarly, Facebook’s data privacy practices do not increase people’s confidence in the company’s products. All the scandals that have surrounded the social network could backfire when Facebook wants to step into healthcare – and this is exactly what we wrote about in our latest article, Is There A Place For Facebook In Healthcare? In it, we looked at what Facebook currently does in medicine and evaluated whether those are viable ways to follow in the future.

Take care, Berci Bertalan Meskó, MDPhD The Medical Futurist

An IRA in which distributions continue after the primary beneficiary’s death.

For an IRA to be inherited, the primary beneficiary must have already been receiving the required minimum distribution; the distributions either continue or are re-calculated based upon the secondary beneficiary’s life expectancy.

If the secondary beneficiary is the widow(er) of the primary beneficiary, she/he may roll over the inherited IRA into her/his own IRA without penalty.

The saver’s credit is a tax credit that’s intended to promote retirement savings among low- and moderate-income workers. It can reduce an eligible taxpayer’s federal income taxes when they save in a qualified retirement plan. It may be especially useful to medical students, nurses, interns, residents and fellows.

****

***

In 2021, the maximum credit is worth $1,000 for individuals and $2,000 for married couples filing jointly, although it phases out for higher earners. To qualify for the credit, individuals must have an adjusted gross income of $32,500 or less. The income threshold for married couples is $65,000.

Because the credit is non-refundable, eligible taxpayers are able to use it to effectively reduce their tax bill to zero – but it cannot provide them with a tax refund.

Posted on September 9, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ALERT FOR PHYSICIANS AND ALL INVESTORS

***

1. You can trade actively in a Roth IRA

Some physician investors may be concerned that they can’t actively trade in a Roth IRA. But there’s no rule from the IRS that says you can’t do so. So you won’t get in legal trouble if you do.

But there may be some extra fees if you trade certain kinds of investments. For example, while brokers won’t charge you if you trade in and out of stocks and most ETFs on a short-term basis, many mutual fund companies will charge you an early redemption fee if you sell the fund. This fee is usually assessed only if you’ve owned the fund for fewer than 30 days.

2. Any gains are tax-free – forever

The ability to avoid taxes on your investments is an incredible benefit. You’ll be able to escape – perfectly legally – taxes on dividends and capital gains. Not surprisingly, this superpower makes the Roth IRA very popular, but to enjoy its benefits, you must abide by a few rules.

The Roth IRA limits you to a $6,000 maximum annual contribution (for 2021), and you won’t be able to withdraw earnings from the account until retirement age (59 1/2) or later and after owning the account for at least five years. However, you can withdraw your contributions to the account without being taxed at any time, but you won’t be able to replace those contributions later.

Many traders use margin in their accounts. With a margin loan, the broker extends you capital to invest beyond what you actually own. It’s a useful tool, especially if you’re trading frequently. Unfortunately, margin loans are not available in IRA accounts.

For frequent traders the ability to trade on margin is not just about magnifying your returns. It’s also about having the ability to sell a position and immediately buy another. In a cash account (like a Roth IRA), you have to wait for a transaction to settle, and that takes a couple days. In the meantime you’re unable to trade with that money even though it’s credited to your account.

PLUS A FOURTH RULE

4. You don’t get to deduct losses

If you’re trading in a taxable brokerage account, you’ll get a tax write-off if you make a losing investment. Some investors even make sure they’re getting the largest write-off they can using a process called tax-loss harvesting. They scoop up that benefit and then even repurchase the stock or fund later (after 30 days) if they think it’s poised to rise in the future.

But if you’re trading in a Roth IRA, you won’t get the ability to write off losses. Changes to the tax code in 2017 eliminated the ability to claim any benefit from losses in an IRA account.

Posted on September 8, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

QUICK DEFINITION – INVESTING BASICS

MUTUAL COMPANY: A company that has no capital stock or stockholders. Rather, it is owned by its policy-owners and managed by a board of directors chosen by the policy-owners.

Any earnings, in addition to those necessary for the operation of the company and contingency reserves, are returned to the policy-owners in the form of policy dividends.

STOCK COMPANY: A joint-stock company is a business entity in which shares of the company’s stock can be bought and sold by shareholders.

Each shareholder owns company stock in proportion, evidenced by their shares (certificates of ownership). Shareholders are able to transfer their shares to others without any effects to the continued existence of the company.

Posted on August 25, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

In this episode, DWealthMuse host, Dara Albright, and guest Jeff Ross, CIO of Vailshire Capital Management, discuss why bitcoin may just be that once-in-a-species asset class that saves the planet from economic and, yes, even environmental ruin.

Thisepisode is loaded with so many great insights including:

Why Jeff believes bitcoin’s investment risk has evaporated;

How bitcoin fits into Warren Buffet’s investment thesis;

Two characteristics bitcoin skeptics share: a lack of understanding and deep ties to the traditional banking system;

Why bitcoin is a dishonest politician’s worst nightmare;

Why every modern retirement portfolio should have bitcoin exposure;

Why regulatory scrutiny may be turning away from bitcoin and heading straight towards ethereum and altcoins;

How bitcoin could solve the world’s energy problems;

Why we may be nearing the end of the Keynesian economic experiment;

How bitcoin forces an honest unit of accounting by governments;

Why fiat is destined to self-destruct while bitcoin is designed to appreciate in time;

Whether bitcoin can reach a new all-time high by Jeff’s August 29th birthday and cross 100,000 by Dara’s December 24th birthday?

Use National Financial Awareness Day to your Advantage

Aug. 14th is National Financial Awareness Day. Financial awareness is about more than just understanding the basics on how money works. It’s also about evaluating your own budget, savings and investments to make sure your finances are working for your needs.

So if it’s been a while since your last financial “check up,” National Financial Awareness Day can be the extra push you’ve needed to finally take a look under the hood.

In 2020, at the request of the U.S. House Committee on Ways and Means (the Committee), the Medicare Payment Advisory Commission (MedPAC) began investigating the role that private equity (PE) plays in healthcare provided to Medicare beneficiaries.

In its June 2021 “Report to the Congress on Medicare and the Health Care Delivery System,” MedPAC included for the first time a chapter on PE’s effect on Medicare, wherein it discussed the findings and observations from its investigation and answered a number of questions posed by the Committee. This Health Capital Topics article will analyze MedPAC’s answers to those questions, review its investigation of PE’s role in healthcare, and summarize reactions from stakeholders.(Read more…)

–The Private Equity Firm Offers an Up Front Lump Sum of Money and Administrative Services Such as Billing and Collections for the Practice.

–In Return, the Doctors in the Practice Agree to Have 30-40% of All Future Revenue Go to the Private Equity Firm.

The Up Front Lump Sum Can Be Equal to as Much as 10 – 20 Years of Income for a Physician.

The Older Doctors in the Practice Who Are Usually the Partners Frequently Take This Deal, Resulting in the Younger Partners Making Less Take-Home Pay.

Implication for Employers:

Private Equity Firms Create Larger Group Practices to Have Better Negotiating Leverage with Commercial Insurance Carriers and Obtain Higher Fee-for-Service Reimbursement.

Overall Healthcare Costs for Physician Services Go Up, While the Take-Home Pay for Doctors Goes Down… and the Private Equity Firm Keeps the Difference.

NOTE: The Older Doctors Who Are Paid the Lump Sum Are Still Required to Stay at the Practice for a Certain Number of Years After the Transaction.

Posted on July 10, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Dr. David Edward Marcinko is Speaking Up

Dr. David Edward Marcinko MBA CMP® enjoys personal coaching and public speaking and gives as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These have included lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

His talks tend to be engaging, iconoclastic, and humorous. His most popular presentations include a diverse variety of topics and typically include those in all iMBA, Inc’s textbooks, handbooks, white-papers and most topics covered on this blog.

A “MEME” stock isn’t as easily defined as a growth or value stock, so to give it a definitive categorization would be inappropriate. Nor would actually categorizing it alongside growth and value stocks. They won’t be found in textbooks anytime soon, but to overlook their impact could potentially be an expensive oversight.

Posted on June 23, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

OVER HEARD IN THE DOCTOR’S LOUNGE

The financial planner is a like juggler, trying to keep a variety of balls simultaneously in the air. Each aspect of practice becomes critical, just as action is needed.

Some of the activities of operating a successful financial planning practice generally attract more attention than others, such as marketing and advertising, closing engagements, and office administration. Because product review, selection and implementation are often related to advisor compensation, they attract a great deal of the financial juggler’s concentration.

But, the heart of financial planning, niche advice, often receives little attention. Not because it is unimportant, it just doesn’t seem immediately and predictably urgent. Here, that ball does not seem to be dropping so rapidly.

However, retaining clients and receiving referrals from other professionals is very dependent on the quality of the advice delivered. And, the first line of protection from practitioner liability exposure is to not deliver incorrect or incomplete advice.

But, where does the financial advisor turn for ideas and organized research in the healthcare sector?

There are varying opinions on how much of your total income should go toward savings and retirement goals each month. Moreover, the answer is likely to vary, depending on your full financial profile.

But if you’re looking for some basic KISS guidelines, consider applying the 50-30-20 rule, a budgeting method that allocates 50% of your income to essentials, like rent and bills, 30% to discretionary spending and 20% to savings.

Posted on June 17, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Dr. David E. Marcinko is at your Service

Dr. David Edward Marcinko MBA CMP® enjoys personal coaching and public speaking and gives as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These have included lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

His talks tend to be engaging, iconoclastic, and humorous. His most popular presentations include a diverse variety of topics and typically include those in all iMBA, Inc’s textbooks, handbooks, white-papers and most topics covered on this blog.

Posted on June 12, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

A YOUNG PHYSICIAN INQUIRES ABOUT NON-PUBLIC COMPANY SHARES AND VESTING?

***

***

QUESTION: I am a physician and work for a startup healthcare IT company with shares in a non-public company that vests over time. What does that mean, and will the shares only be worth something if we go public or are acquired?

–Shelly from Boston, MA

****

ANSWER: In most cases, startups dangle equity compensation over employees like a just-out-of-reach cupcake in front of a treadmill. Vesting means some condition needs to be met before you fully own your shares, whether it’s staying at the company for a period of time, reaching a target valuation, or both.

Once your shares have fully vested, you’d think you can finally cash in. But that’s not always the case. It’s a hassle to sell private company shares because there are far fewer buyers compared to selling shares in a publicly traded company.

If you want to sell your stake before the company goes public, you can ask the execs at your company to buy back your shares. If they say no—and they might, because once they let one employee sell, it’s hard to turn down others—you need another buyer, like an outside investor.

There are eBay-like marketplaces for selling private company shares, but it’s not like posting a picture of your old iPod and offering free shipping. You can only sell to accredited investors (aka hedge funds and other rich folks), and your company needs to authorize the sale.

It’s way easier to sell your shares if and when your company goes public or is acquired by another company.

BOOK-VALUE: Cost of capital assets minus accumulated depreciation for a healthcare [corporation], or other organization.

The net asset value of a [healthcare] companies common stock. This is calculated by dividing the net tangible assets of the company (minus the par value of any preferred stock the company has) by the number of common shares outstanding.

****

PAR VALUE: For common stock, the value on the books of the corporation. It has little to do with market value or even the original price of shares at first issuance.

The difference between par and the price at first issuance is carried on the books of a corporation as “paid-in capital” or “capital surplus.”

To keep up with the ever-changing healthcare industrial complex, we must learn new definitions and re-learn old terminology in order to correctly apply it to practice. By aggregating the most up-to-date abbreviations, acronyms, definitions and terms, the Health DictionarySeries offers a wealth of information to help understand the ever-changing terms-of-art in healthcare today.

Each 10,000 item handbook is essential for doctors, nurses, benefits managers, financial advisors/planners, and insurance agents, CPAs, and administrators; as well as graduate and under graduate students and professors. Our goal to for each dictionary to be designated as a Doody’s Core Title.

Dictionary of Health Insurance and Managed Care

With more than 10,000 definitions, 4,000 abbreviations and acronyms, and a 3,000 item oeuvre of resources, readings, and nomenclature derivatives, this dictionary covers the Medicare, managed care and Medicaid, private insurance, Veteran’s Administration and PP-ACA language of the entire health and long-term care insurance sector.

Dictionary of Health Economics and Finance

Health economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, mathematics, the actuarial sciences, stochastics and statistics, salary reimbursements, physician payments, compensation and forecasting are all commingled arenas.

Dictionary of Health Information Technology Security

There is a myth that all healthcare stakeholders understand the meaning of information technology jargon. In truth, the vernacular of contemporary systems is unique, and often misused or misunderstood. Moreover, emerging Heath Information Technology (HIT) thru the HITECG initiatives; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert in a position of maximum uncertainty and minimum productivity.

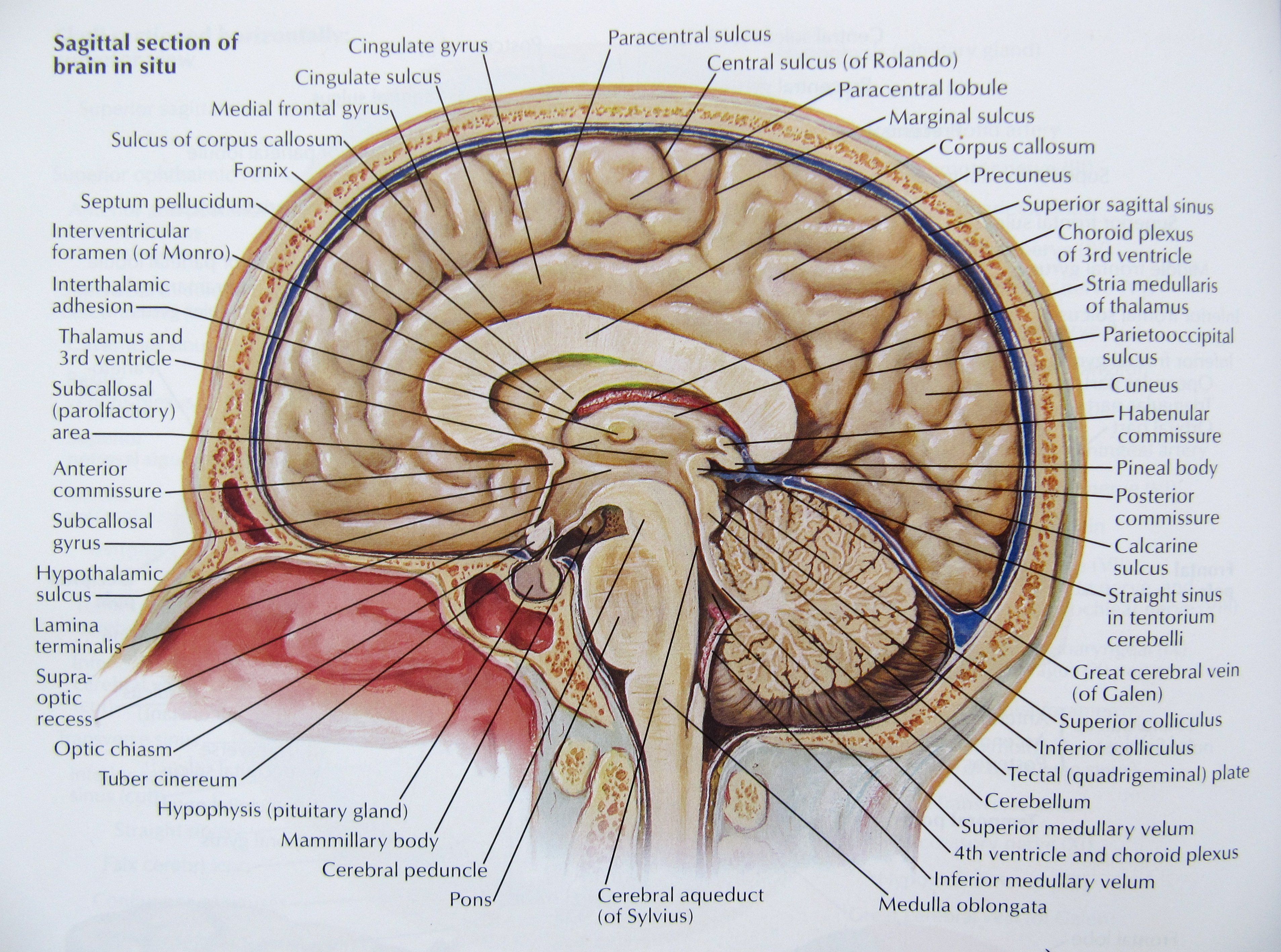

I am not a neurologist, psychologist, or psychiatrist. But, it is well known that emotional and behavioral change involves the human nervous system. And, there are two parts of the nervous system that are especially significant for holistic financial advisor; the first is the limbic system and the second is the autonomic nervous system.

According to Dr. C. George Boerre of Shippensburg University of Pennsylvania, this is known as the emotional nervous system.

1. The Limbic System

The limbic system is a set of structures that lies on both sides of the thalamus, just under the cerebrum. It includes the hypothalamus, the hippocampus, the amygdala, and nearby areas. It is primarily responsible for emotions, memories and recollection.

Hypothalamus

The small hypothalamus is located just below the thalamus on both sides of the third ventricle (areas within the cerebrum filled with cerebrospinal fluid that connect to spinal fluid). It sits inside both tracts of the optic nerve, and just above the pituitary gland.

The hypothalamus is mainly concerned with homeostasis or the process of returning to some “set point.” It works like a thermostat: When the room gets too cold, the thermostat conveys that information to the furnace and turns it on. As the room warms up and the temperature rises, it sends turns off the furnace. The hypothalamus is responsible for regulating hunger, thirst, response to pain, levels of pleasure, sexual satisfaction, anger and aggressive behavior, and more. It also regulates the functioning of the autonomic nervous system, which means it regulates functions like pulse, blood pressure, breathing, and arousal in response to emotional circumstances. In a recent discovery, the protein leptin is released by fat cells with over-eating. The hypothalamus senses leptin levels in the bloodstream and responds by decreasing appetite. So, it seems that some people might have a gene mutation which produces leptin, and can’t tell the hypothalamus that it is satiated. The hypothalamus sends instructions to the rest of the body in two ways. The first is to the autonomic nervous system. This allows the hypothalamus to have ultimate control of things like blood pressure, heart rate, breathing, digestion, sweating, and all the sympathetic and parasympathetic functions.

The second way the hypothalamus controls things is via the pituitary gland. It is neurally and chemically connected to the pituitary, which in turn pumps hormones called releasing factors into the bloodstream. The pituitary is the so-called “master gland” as these hormones are vitally important in regulating growth and metabolism.

Hippocampus

The hippocampus consists of two “horns” that curve back from the amygdala. It is important in converting things “in your mind” at the moment (short-term memory) into things that are remembered for the long run (long-term memory). If the hippocampus is damaged, a patient cannot build new memories and lives in a strange world where everything they experience just fades away; even while older memories from the time before the damage are untouched! Most patients who suffer from this kind of brain damage are eventually institutionalized.

Amygdala

The amygdalas are two almond-shaped masses of neurons on either side of the thalamus at the lower end of the hippocampus. When it is stimulated electrically, animals respond with aggression. And, if the amygdala is removed, animals get very tame and no longer respond to anger that would have caused rage before. The animals also become indifferent to stimuli that would have otherwise have caused fear and sexual responses.

Related Anatomic Areas

Besides the hypothalamus, hippocampus, and amygdala, there are other areas in the structures near to the limbic system that are intimately connected to it:

The cingulate gyrus is the part of the cerebrum that lies closest to the limbic system, just above the corpus collosum. It provides a pathway from the thalamus to the hippocampus, is responsible for focusing attention on emotionally significant events, and for associating memories to smells and to pain.

The ventral tegmental area of the brain stem (just below the thalamus) consists of dopamine pathways responsible for pleasure. People with damage here tend to have difficulty getting pleasure in life, and often turn to alcohol, drugs, sweets, and gambling.

The basal ganglia (including the caudate nucleus, the putamen, the globus pallidus, and the substantia nigra) lie over to the sides of the limbic system, and are connected with the cortex above them. They are responsible for repetitive behaviors, reward experiences, and focusing attention.

The prefrontal cortex, which is the part of the frontal lobe which lies in front of the motor area, is also closely linked to the limbic system. Besides apparently being involved in thinking about the future, making plans, and taking action, it also appears to be involved in the same dopamine pathways as the ventral tegmental area, and plays a part in pleasure and addiction.

2. The Autonomic Nervous System

The second part of the nervous system to have a particularly powerful part to play in our emotional life is the autonomic nervous system.

The autonomic nervous system is composed of two parts, which function primarily in opposition to each other. The first is the sympathetic nervous system, which starts in the spinal cord and travels to a variety of areas of the body. Its function appears to be preparing the body for the kinds of vigorous activities associated with “fight or flight,” that is, with running from danger or with preparing for violence. Activation of the sympathetic nervous system has the following effects:

dilates the pupils and opens the eyelids,

stimulates the sweat glands and dilates the blood vessels in large muscles,

constricts the blood vessels in the rest of the body,

increases the heart rate and opens up the bronchial tubes of the lungs, and

inhibits the secretions in the digestive system.

One of its most important effects is causing the adrenal glands (which sit on top of the kidneys) to release epinephrine (adrenalin) into the blood stream. Epinephrine is a powerful hormone that causes various parts of the body to respond in much the same way as the sympathetic nervous system. Being in the blood stream, it takes a bit longer to stop its effects, and may take some time to calm down again

The sympathetic nervous system also takes in information, mostly concerning pain from internal organs. Because the nerves that carry information about organ pain often travel along the same paths that carry information about pain from more surface areas of the body, the information sometimes get confused. This is called referred pain, and the best known example is the pain in the left shoulder and arm when having a heart attack.

The other part of the autonomic nervous system is called the parasympathetic nervoussystem. It has its roots in the brainstem and in the spinal cord of the lower back. Its function is to bring the body back from the emergency status that the sympathetic nervous system puts it into.

Some of the details of parasympathetic arousal include some of the following:.

pupil constriction and activation of the salivary glands,

stimulating the secretions of the stomach and activity of the intestines,

stimulating secretions in the lungs and constricting the bronchial tubes, and;

decreases heart rate.

The parasympathetic nervous system also has some sensory abilities: It receives information about blood pressure, levels of carbon dioxide in the blood, etc.

There is actually another part of the autonomic nervous system that is not mentioned too often: the enteric nervous system. It is a complex of nerves that regulate the activity of the stomach.

For example, if you get sick to your stomach with a new financial advisory client – or feel nervous butterflies with your first patient encounter as a doctor- you can blame the enteric nervous system.

What I see in my accounting practice is that significant accumulation in younger physician portfolio growth is not happening as it once did. This is partially because confidence in the equity markets is still not what it was; but that doctors are also looking for better solutions to support their reduced incomes.

For example, I see older doctors with about 25 percent of their wealth in the market, and even in retirement years, do not rely much on that accumulation to live on. Of this 25 percent, about 80 percent is in their retirement plan, as tax breaks for funding are just too good to ignore.

What I do see is that about 50 percent of senior physician wealth is in rental real estate, both in a private residence that has a rental component, and mixed-use properties. It is this that provides a good portion of income in retirement.

So; could I add dialog about real estate as a long term solution for retirement?

Yes, as I believe a real estate concentration in the amount of 5 percent is optimal for a diversified portfolio, but in a very passive way through mutual or index funds that are invested in real estate holdings and not directly owning properties.

Today, as an option, we have the ability to take pension plan assets and transfer marketable securities for rental property to be held inside the plan collecting rents instead of dividends.

Real estate holdings never vary very much, tend to go up modestly, and have preferential tax treatment due to depreciation of the property against income.

The Bidentax plan includes the following payroll tax, individual income tax, and estate and gift tax changes.

It imposes a 12.4 percent Old-Age, Survivors, and Disability Insurance (Social Security) payroll tax on income earned above $400,000, evenly split between employers and employees.

DEFINITION: A fiduciary is a person who holds a legal or ethical relationship of trust with one or more other parties (person or group of persons).

Typically, a fiduciary prudently takes care of money or other assets for another person. One party, for example, a corporate trust company or the trust department of a bank, acts in a fiduciary capacity to another party, who, for example, has entrusted funds to the fiduciary for safekeeping or investment. Likewise, financial advisers, financial planners, and asset managers, including managers of pension plans, endowments, and other tax-exempt assets, are considered fiduciaries under applicable statutes and laws.

In a fiduciary relationship, one person, in a position of vulnerability, justifiably vests confidence, good faith, reliance, and trust in another whose aid, advice, or protection is sought in some matter. In such a relation good conscience requires the fiduciary to act at all times for the sole benefit and interest of the one who trusts.

I, the undersigned, ___________________________ (“financial advisor”), pledge to always put the best interests of _______________________________ (“client”) first, no matter what.

As such, I will disclose in writing the following material facts and any conflicts of interest (actual and/or perceived) that may arise in our business relationship:

All commission, fees, loads, and expenses, in advance, client will pay as a result of my advice and recommendations;

All commission and commissions I receive as a result of my advice and recommendations;

The maximum fee discount allowed by my firm and the largest fee discount I give to other customers;

The fee discount client is receiving;

Any recruitment bonuses and other recruitment compensation I have or will receive from my firm;

Fees I paid to others for the referral of client to me;

Fees I have or will receive for referring client to any third-parties; and

Any other financial conflicts of interest that could reasonably compromise the impartiality of my advice and recommendations.

Alpha: The measure of the amount of a stock’s expected return that is not related to the stock’s sensitivity to market volatility. It measures the residual non-market influences that contribute to a securities risk unique to each security.

Alpha uses beta as a measure of risk, a benchmark and a risk free rate of return (usually T-bills) to compare actual performance with expected performance.

For example, a fund with a beta of .80 in a market that rises 10% is expected to rise 8%. If the risk-free return is 3%, the alpha would be –.6%, calculated as follows:

Posted on May 10, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

A PODCAST PRESENTATIONON THE C.C.P.

By Vitaliy Katsenelson, CFA

EDITOR’S NOTE: Over the last six months, my value investing management colleague Vitaliy Katsenelson has skewed his IMA’s portfolios more towards defense companies.

–Dr. David Edward Marcinko MBA CMP®

WHY THE SHIFT?

The world appears less safe today than at any time since the Berlin Wall came down. Fast-forward two decades from then to now, and we find a drastically different world.

For example, China’s large Long March 5b rocket has fallen to Earth mostly as expected, much to the chagrin of critics. And some suggest the country is gearing up for “World War III” after Congress passed a multi-billion dollar defense Bill on Friday which President Donald Trump had previously vetoed.

Posted on May 7, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

The Dramatic Rise in the Stock Market Over the Last 10 Years Has Caused Institutional Investors Like Pension Funds to Re-balance to Private Equity

By Eric Bricker MD

A Typical Pension Fund Portfolio Will Be 51% Bonds, 28% Equities, 6% Real Estate, 5% Private Equity, 4% Other and 6% Cash. As a Result of Rebalancing Money Out of Skyrocketing Equities, Private Equity Funding Has Doubled to Over $1.2 Trillion in the Last 10 Years.

Specifically in Healthcare, Private Equity Investment in Providers (i.e. Physician Groups, Surgery Centers, Imaging Centers, etc.) Doubled to $30 Billion in Just ONE YEAR. The Private Equity Investment on the Payor Side of Healthcare PALES in Comparison at Only $1 Billion. The Majority of These Private Equity Investments Plan on Making Money By INCREASING Healthcare Costs in a Fee-for-Service Payment Environment.

Healthcare Costs Don’t Rise By Accident. They Rise Because Specific People Make Specific Plans to Increase Costs to Earn a Return on Their Investment.

NOTE: Colleagues at Health Capital Consultants (HCC) represent a team of qualified, experienced and certified healthcare valuation professionals with specific healthcare industry focus; along with in-depth understanding and extensive experience of the healthcare market on a local, regional and national basis; and strong dedication to in-depth research and analysis.

DEFINITION: A member of a securities exchange with the essential function of maintaining a fair and orderly market, insofar as reasonably practicable, in the stocks in which he is registered as a specialist. To do this, s/he must buy and sell for his own account and risk, to a reasonable degree, when there is a temporary disparity between supply and demand. In order to equalize trends, he must buy or sell counter to the direction of the market. DHEF:https://lnkd.in/dqdbWM9 FOREWORD: https://lnkd.in/ecwZWxu

At all times the specialist must put his customer’s interest before his own. All specialists are registered with the exchange, but are not employees of that exchange. Your thoughts are appreciated.

![DR. DAVID EDWARD MARCINKO FACFAS MBA CFP MBBS [Hon] [Executive Summary] - PDF Free Download](https://educationdocbox.com/docs-images/75/71938560/images/8-1.jpg)

:strip_icc():format(webp)/what-is-the-rule-of-55-2894280-v1-fa6b42c5a8f647e8aa5776a550c121a5-1fc39bd85b914af9b2682601f2cefdf6.png)

:max_bytes(150000):strip_icc():format(webp)/the-50-30-20-rule-of-thumb-453922-final-5b61ec23c9e77c007be919e1-5ecfc51b09864e289b0ee3fa0d52422f.png)

***

***

{kind=link}