BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on September 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

At 2 pm EST Today

By Staff Reporters

***

***

ABOUT THE FEDERAL OPEN MARKET COMMITTEE

The term “monetary policy” refers to the actions undertaken by a central bank, such as the Federal Reserve, to influence the availability and cost of money and credit to help promote national economic goals. The Federal Reserve Act of 1913 gave the Federal Reserve responsibility for setting monetary policy.

The Federal Reserve controls the three tools of monetary policy–open market operations, the discount rate, and reserve requirements. The Board of Governors of the Federal Reserve System is responsible for the discount rate and reserve requirements, and the Federal Open Market Committee is responsible for open market operations. Using the three tools, the Federal Reserve influences the demand for, and supply of, balances that depository institutions hold at Federal Reserve Banks and in this way alters the federal funds rate. The federal funds rate is the interest rate at which depository institutions lend balances at the Federal Reserve to other depository institutions overnight.

Changes in the federal funds rate trigger a chain of events that affect other short-term interest rates, foreign exchange rates, long-term interest rates, the amount of money and credit, and, ultimately, a range of economic variables, including employment, output, and prices of goods and services.

And so, the macroeconomic FOMC is kicking off at 2pm ET today, when the Fed will announce the first interest rate cut in over four years. But, financial watchers are split between two predictions: a standard 0.25% cut or a more aggressive one of 0.5% (investors are betting on the latter, while many analysts think the former).

Regardless of its size, today’s rate cut and subsequent ones are expected to make borrowing cheaper for consumers and businesses, with ripple effects throughout the economy.

Posted on September 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks were mixed yesterday as Wall Street waits for the Fed to cut interest rates tomorrow. The Dow Jones Industrial Average closed at a record high and the S&P 500 inched up. But the tech-heavy NASDAQ slipped, partly because Apple fell after analysts pointed out that demand for the iPhone 16 hasn’t equaled the kind of frenzy new models commanded in the past.

***

Boeing seeks to hoard its cash. While dealing with a strike by 30,000 unionized factory workers that has shut down production of its 737 planes and could cost the company $500 million a week, Boeing has instituted a hiring freeze and other money-saving measures.

Posted on September 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

It’s going to be a gloomy October for some 1,800 PwC employees. The Big Four firm has announced it’ll be laying off around 2.5% of its US unit’s workforce next month, the Wall Street Journal reported. About half of the job cuts will take place offshore. The cuts will occur mainly in PwC’s US advisory, products, and technology operations functions.

Alcoa climbed 6.09% on the news that it will sell its stake in a joint venture with Saudi Arabia Mining Co. to the tune of $1.1 billion in stock and cash.

Bausch + Lomb Corp popped 14.66% on a report from the Financial Times that the eyewear company is considering selling itself to get out from under a massive debt load.

Nuvalent soared 28.27% on impressive results from Phase 1 trials of its new cancer treatments.

What’s down

Apple fell 2.78% just a few days before its big iPhone 16 launch on Friday thanks to reports that demand for the new phone may be lower than anticipated.

Walgreens Boots Alliance sank 2.06% after it agreed to pay $106.8 million for charging the US government for prescriptions it never filled.

Yelp tumbled 3.03% thanks to Bank of America analysts initiating their coverage of the reviews website with a bearish “underperform” rating.

Trump Media & Technology Group gave up some of its recent gains, falling 3.84% only a few days after soaring on the news that former President Donald Trump won’t sell his shares of the company.

The S&P 500® index (SPX) added 7.07 points (0.13%) to 5,633.09; the Dow Jones Industrial Average® ($DJI) rose 228.30 points (0.55%) to 41,622.08; the NASDAQ Composite® ($COMP) dropped 91.84 points (–0.52%) to 17,592.13.

The 10-year Treasury note yield (TNX) fell about three basis points to 3.62%, a new 15-month closing low.

The BOE Volatility Index® (VIX) inched up to 16.99.

Stat: 2%. That’s how much the birth rate declined from 2022 to 2023. (CDC)

Quote: “Every year they choose not to act, they will be complicit.”—Christine McComas, a mother from Maryland whose daughter died after she was cyberbullied, on members of the House attempting to pass a bill to regulate social media for children (Politico)

Read: UK Prime Minister Keir Starmer said the National Health Service must “reform or die,” and laid out a 10-year plan to fix it. (Reuters)

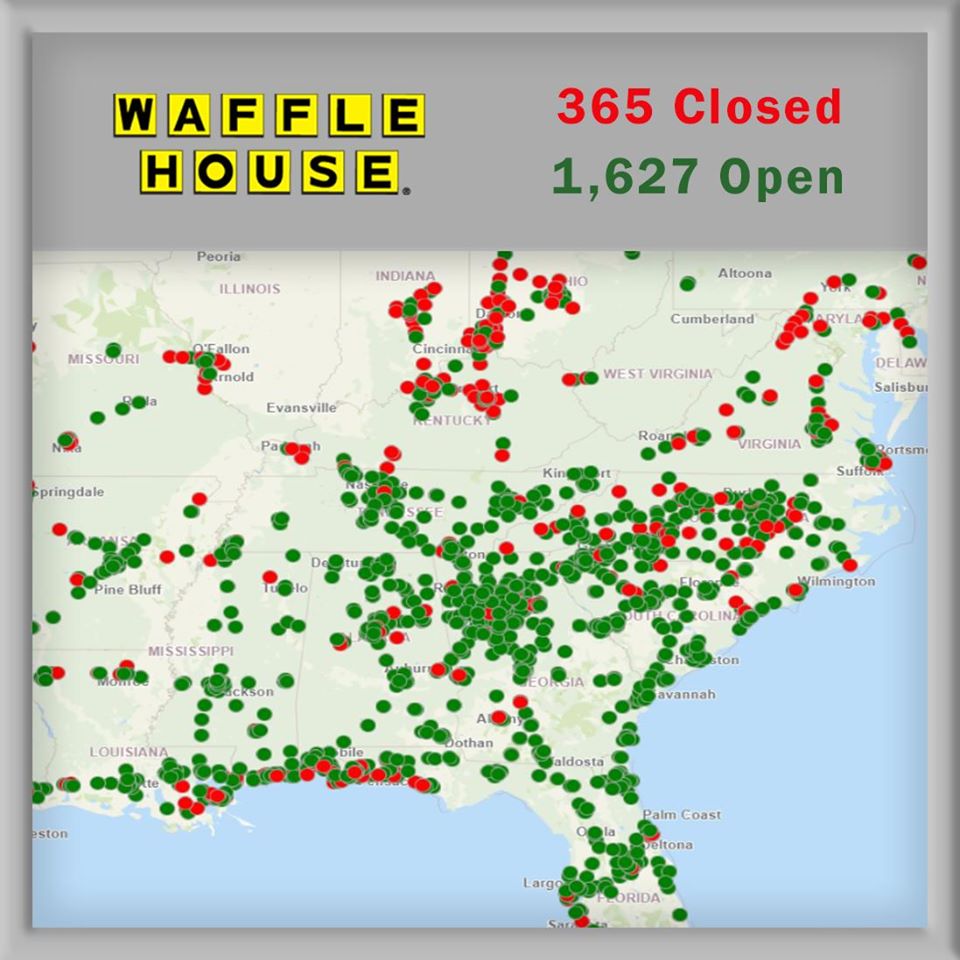

Walt Ehmer, the president and CEO of Waffle House and a member of the board of trustees for the Atlanta Police Foundation, has died at age 58, the foundation announced last Sunday; 2024. Ehmer joined Waffle House in 1992 and quickly rose to senior leadership, becoming president of the company in 2002, and later adding the titles of CEO and chairman, according to information from Georgia Tech University, his alma mater.

“His leadership, dedication and warmth touched the lives of many, both within the Waffle House family and beyond. He leaves behind a remarkable legacy,” Mayor Andre Dickens said in a news release.

415 Restaurants Closed in Georgia and Elsewhere in 2022

The Waffle House Index [WHI] is an informal metric named after the Waffle House restaurant chain, headquartered in Georgia, and used by the Federal Emergency Management Agency (FEMA) to determine the effect of a storm and the likely scale of assistance required for disaster recovery.

IOW: “If you get there and the Waffle House is closed? Well, that’s really bad”, according to Craig Fugate – Former Head of the Federal Emergency Management Agency [FEMA].

Posted on September 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

At the most general level, economists may define wealth as “the total of anything of value” that captures both the subjective nature of the idea and the idea that it is not a fixed or static concept. Various definitions and concepts of wealth have been asserted by various people in different contexts. Defining wealth can be a normative process with various ethical implications, since often wealth maximization is seen as a goal or is thought to be a normative principle of its own. A community, region or country that possesses an abundance of such possessions or resources to the benefit of the common good is known as wealthy.

What does wealth mean to you?

In a recent survey by Edelman Financial Engines, 57% of respondents said they’d feel wealthy if they had $1 million in the bank. But for many people, that’s not enough.

Among those with $500,000 and $3 million in assets, 53% said it would take over $3 million in the bank for them to feel wealthy, and 33% said it would take over $5 million. Given that these are amounts some people will never even come close to amassing in their lifetimes, it may be hard to wrap your head around these answers.

Posted on September 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

It’s the most wonderful time of the year – Survey Season! Beginning in late May each year, numerous industry normative benchmark physician production and compensation surveys begin publishing the most recent year’s reports. These healthcare and specialty specific surveys annually report specific types of physician compensation and productivity metrics across the country for various specialties and are widely used by hospitals, physician practices, and healthcare compensation and valuation experts, are often used for the determination of Fair Market Value (FMV) physician compensation for regulatory compliance purposes.

Additionally, the government has referenced and utilized industry normative benchmark compensation surveys (including those listed below) in reviewing and litigating physician compensation arrangements, indicating their reliance on this data as well. (Read more…)

Posted on September 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

On July 26, 2024, the U.S. Department of Justice (DOJ) filed a complaint in intervention against Murphy Medical Center, doing business as Erlanger Western Carolina Hospital, and Chattanooga-Hamilton County Hospital Authority, doing business as the Erlanger Health System and Erlanger Medical Center. The government’s complaint, filed in the U.S. District Court for the Western District of North Carolina, alleges that Erlanger violated the Stark Law, and subsequently submitted false claims to the Medicare program in violation of the False Claims Act (FCA).

Posted on September 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

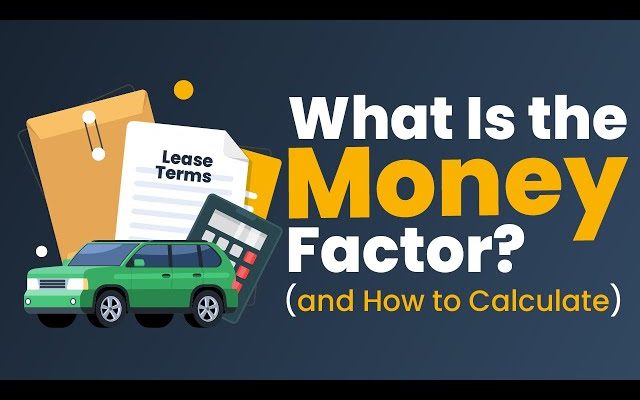

An increasingly common leasing scam is the money factor lie

The “money factor” in leasing is the financing cost of a monthly lease payment and is similar to an interest rate – and it’s important to know the difference. The money factor is a small decimal and should be shown as such, whereas the interest rate is a percentage. A deceitful sales person will count on you not knowing the difference.

For example, a interest rate of 2.5% is not the same as a factor of .0025 and when the latter is used to calculate your lease payment, he or she ends up overcharging you. As a result, you have to pay much more over the lease term without realizing it.

To calculate the money factor, use this formula: Money Factor = Lease Charge / (Capitalized Cost * Residual Value) * Lease Term. It’s important to note that the customer’s credit score determines the money factor. The higher your credit score is, the lower the money factor on the lease will be.

One way to calculate the money factor is by converting it to an APR. To do this, you multiply the money factor by 2,400. If a car dealer provides you with an interest rate, divide it by 2,400 to find the money factor.

In another example, if you are quoted a money factor of .003 on a loan, that would be (2,400x.003) 7.2%. If the car dealer quotes you an interest rate of 4.2%, you can divide it by 2,400 to find the money factor of .00175.

The money factor may be shown in an easier-to-read format, like 1.75 instead of .00175. This can often confuse customers because it appears to be a low interest rate. But don’t be fooled by a money factor presented as a factor of 1,000. Always be sure to ask if the number you are given is the APR or the money factor. If it’s the money factor, convert it to APR so that you can clearly see the interest rate.

Posted on September 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

It seems many of America’s millionaires are saving for retirement. Thanks largely to a stock market, the number of 401(k) millionaires hit a new record last quarter—rising 2.5% to 497,000, as per Fidelity. It was the third quarter in a row of growth for retirement savings, Quartzreports, and the average amount in retirement accounts hit $127,100.

But even those who have made it to the $1 million mark haven’t quite hit the figure most Americans think they need to retire comfortably. That’d be $1.46 million, according to the latest survey by Northwestern Mutual.

The decision to sell, buy or merge a medical practice, while often financially driven, and is inherently an emotional one for these impact investors who went into the profession largely because of a deep seated zeal to help others.

Still, beyond impact investing musings, there are other economic reasons for a practice valuation that include changes in ownership, determining insurance coverage for a practice buy-sell agreement or upon a physician-owner’s death, organic growth meter, establishing stock options, or bringing in a new partner; etc.

Practice appraisals are also used for legal reasons such as divorce, bankruptcy, breach of contract and minority shareholder complaints. In 2002, the Financial Accounting Standards Board (FASB) issued rules that required certain intangible assets to be valued, such as goodwill. This may be important for practices seeking start-up, service segmentation extensions, or operational funding. Some other reasons for a medical practice appraisal, and the considerations that go along with them, are discussed here.

Medical practice valuation may be required for estate planning purposes. For a decedent physician with a gross estate of more than current in-place tax limits, his or her assets must be reported at fair market value on an estate tax return. If lifetime gifts of a medial practice business interest are made, it is generally wise to obtain an appraisal and attach it to the gift tax return.

Note that when a “closely-held” level of value (in contrast to “freely traded,” “marketable,” or “publicly traded” level) is sought, the valuation consultant may need to make adjustments to the results. There are inherent risks relative to the liquidity of investments in closely held, non-public companies (e.g., medical group practice) that are not relevant to the investment in companies whose shares are publicly traded (freely-traded). Investors in closely-held companies do not have the ability to dispose of an invested interest quickly if the situation is called for, and this relative lack of liquidity of ownership in a closely held company is accompanied by risks and costs associated with the selling of an interest said company (i.e., locating a buyer, negotiation of terms, advisor/broker fees, risk of exposure to the market, etc.). Conversely, investors in the stock market are most often able to sell their interest in a publicly traded company within hours and receive cash proceeds in a few days. Accordingly, a discount may be applicable to the value of a closely held company due to the inherent illiquidity of the investment. Such a discount is commonly referred to as a “discount for lack of marketability.”

Discount for lack of marketability is typically discussed in three categories: (1) transactions involving restricted stock of publicly traded companies; (2) private transactions of companies prior to their initial public offering (IPO); and, (3) an analysis and comparison of the price to earnings (P/E) ratios of acquisitions of public and private companies respectively published in the “Mergerstat Review Study.”\

With a non-controlling interest, in which the holder cannot solely authorize and cannot solely prevent corporate actions (in contrast to a controlling interest), a “discount for lack of control,” (DLOC), may be appropriate. In contrast, a control premium may be applicable to a controlling interest. A control premium is an increase to the pro rata share of the value of the business that reflects the impact on value inherent in the management and financial power that can be exercised by the holders of a control interest of the business (usually the majority holders). Conversely, a discount for lack of control or minority discount is the reduction from the pro rata share of the value of the business as a whole that reflects the impact on value of the absence or diminution of control that can be exercised by the holders of a subject interest.

Several empirical studies have been done to attempt to quantify DLOC from its antithesis, control premiums. The studies include the Mergerstat Review, an annual series study of the premium paid by investors for controlling interest in publicly traded stock, and the Control Premium Study, a quarterly series study that compiles control premiums of publicly traded stocks by attempting to eliminate the possible distortion caused by speculation of a deal.

Buy-Sell Agreements

The ideal situation is for physician partners to put in place a buy-sell agreement when practice relationships are amicable. This establishes the terms for departure before they are required, and is akin to a prenuptial agreement in the marriage contract. Disagreements most often occur when a doctor leaves the group, often acrimoniously. Business operations of the practice decline, employee and partner morale suffers, feuding factions develop spilling over into the office, and the practice begins to implode creating a downward valuation spiral. And so, valuations should be done every 2-3 years, or as the economic circumstances of the practice change. Independence and credibility are provided, and emotional overtones are purged from the transaction.

Physician Partnership Disputes

Medical practice appraisals are often used in partnership disputes, such as breach-of-contract or departure issues. Obvious revenue declinations are not difficult to quantify. But, revenues may not immediately fall since certain Current Procedural Terminology [CPT®] code reimbursements may actually increase. Upon verification however, lost business may be camouflaged as the number of procedures performed, or number of patients decrease after partner departure.

Physicians getting divorced should get a practice appraisal, and either side may hire the appraiser, although occasionally the court will order an expert to provide a neutral valuation. Such valuations should be done in light of both court discovery rules and IRS requirements for closely held businesses. Generally, this requires the consideration of eight elements:

• Practice specialty and operating history

• Economic and healthcare industry condition

• Estimates of practice risks and future returns

• Book value and financial condition of the practice

• Practice future earning capacity

• Physician bonuses, dividends and distributions

• Intangible assets

• Comparable practice sales

Sometimes, the non-physician spouse may even desire a lifestyle analysis to evaluate the potential for under reported income, by a forensic accountant, or appraiser. A family law judge is often the final arbiter of different valuations, and because of varying state laws there may be 50 different nuances of what the practice is really worth.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, urls and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Crowdfunding is a popular way to raise money online. People often use crowdfunding to fund raise for a business, for charity, or for gifts. It’s important to know that money raised through crowdfunding may be taxable.

Do you have to pay taxes on the money you receive from GoFundMe, etc?

Generally, you will not owe taxes on donated funds you receive from a crowdfunding platform. The IRS considers the money received from GoFundMe to be a gift instead of income, so it is typically not taxable. A gift is any transfer of cash or property you make to an individual without receiving full consideration in return, according to the IRS. People who donate money to GoFundMe to help pay for medical expenses are typically doing it out of generosity and do not expect anything in return.

Some money raised through crowdfunding may NOT be considered a gift.

Under federal tax law, gross income includes all income from any source, unless it’s excluded from gross income by law. In most cases, gifts aren’t included in the gross income of the person receiving the gift. Here’s what people involved in crowdfunding should know:

If a crowdfunding organizer is raising money on behalf of others, the money may not be included in the organizer’s gross income, as long as the organizer gives the money to the person for whom they organized the crowdfunding campaign.

If people donate to a crowdfunding campaign out of generosity and without expecting anything in return, the donations are gifts. Therefore, they will not be included in the gross income of the person for whom the campaign was organized.

However, not all contributions to crowdfunding campaigns are gifts and may be taxable.

When employers give to crowdfunding campaigns for an employee, those contributions are generally included in the employee’s gross income.

Taxpayers may want to consult a trusted tax pro for information and advice regarding how to treat amounts received from crowdfunding campaigns.

Posted on August 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Remember NFTs? This is an excellent history of OpenSea, the largest NFT marketplace, and all the chaos within its walls.

***

***

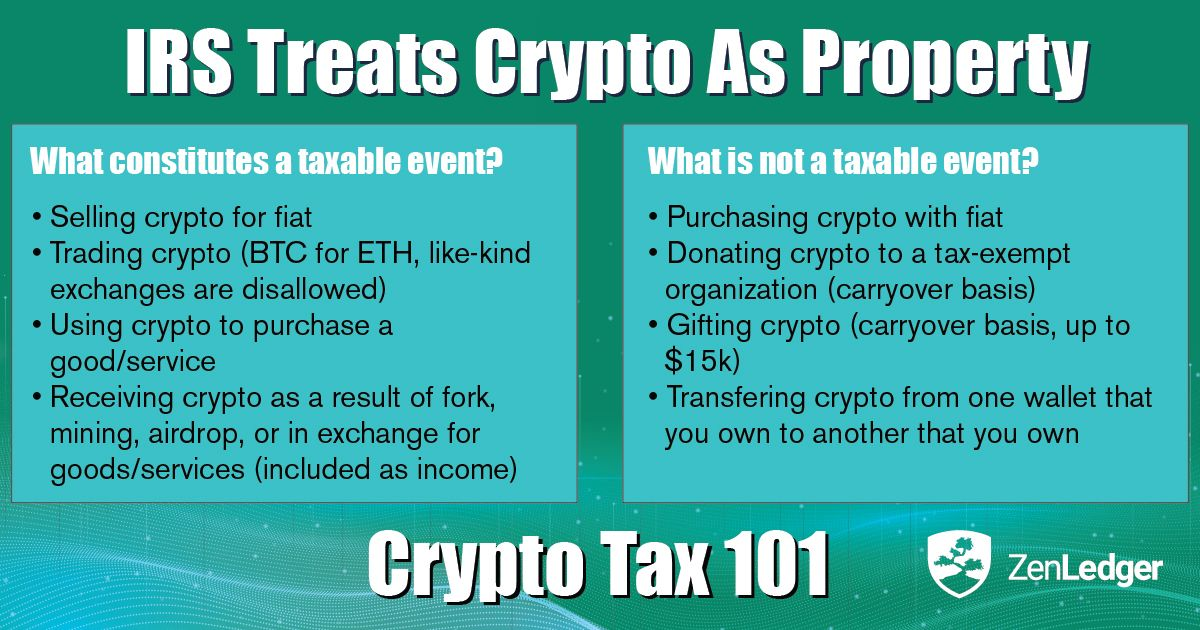

You have to report your crypto and NFT transactions to the IRS

While not technically new, for 2024. the IRS is making a more concerted effort to track cryptocurrency sales and trades. Whenever you sell or trade your crypto or purchase an item with crypto, you trigger a taxable event. Currently, crypto is taxed like property, making it subject to short- or long-term capital gains taxes. This also means you can report any crypto losses to help offset any gains. Since 2022 saw a drastic drop and rise in the value of cryptocurrencies like bitcoin and ethereum, if you sold or traded your crypto at a loss, you may be able to reduce your tax bill by reporting your capital loss. The same goes for NFTs.

And though the IRS will flag any unreported crypto gains, if you don’t report a loss that can lower your tax burden, the IRS won’t adjust your return on your behalf. “If you leave it off, it stays off. “Tax deductible losses from your virtual currency activity do have real consequences on your tax return, and can save you real dollars.

So we always tell people, if you’ve got something that you don’t fully understand, you certainly should seek out guidance from a trained experienced tax professional.”

Posted on August 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: Consumer confidence index (CCI) is a standardized confidence indicator providing an indication of future developments of households’ consumption and saving.

The index is based upon answers regarding household’s expected financial situation, their sentiment about the general economic situation, unemployment and capability of savings. An indicator above 100 signals a boost in the consumers’ confidence towards the future economic situation, as a consequence of which they are less prone to save, and more inclined to spend money on major purchases in the next 12 months. Values below 100 indicate a pessimistic attitude towards future developments in the economy, possibly resulting in a tendency to save more and consume less.

The decline in inflation and the expectation of an imminent interest rate cut have Americans feeling better about the economy than they have in a while, according to the latest update of the Conference Board’s consumer confidence index [CCI].

On the other hand, consumers are worried about the softening labor market. While the unemployment rate remains below historical standards at 4.3%, it has increased for four straight months—likely enough to convince J. Powell and the Federal Reserve to cut rates in September.

Posted on August 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Nvidia will drop its Q2 numbers on Wednesday. Investors will also look for an update from CEO Jensen Huang about reported delays in production of the company’s highly anticipated new Blackwell chips.

Andersen, the US unit of Andersen Global, is considering an IPO in 2025, the Wall Street Journal reported. Andersen Global, an association of consulting firms, was formed in the wake of the 2002 collapse of Big Five accounting firm Arthur Andersen. The parent company has more than 17,000 employees worldwide and earned around $1.9 billion in revenue last year.

Kroger gained 1.6% as the antitrust trial began over its plan to merge with rival Albertsons in a $25 billion deal.

XPeng ADRs (American Depositary Receipts) spiked 7.90% on news that the Chinese EV maker’s CEO bought more than 2 million of the company’s shares. Those ADRs are still down nearly 50% this year. Here’s what an ADR is, by the way.

What’s down

Nvidia (-2.25%), Super Micro Computer (-8.27%), and Broadcom (-4.05%) stunk up the joint today. Investors are biting their nails ahead of Nvidia’s earnings report on Wednesday.

Uber dropped 2.30% on a day it was hit with a record $324 million fine by the Dutch data protection regulator for violating EU personal data rules.

Intel plopped 2% after CNBC reported on Friday that the chipmaker has hired advisors to help defend the castle against activist investors.

The SPX dropped 17.77 points (–0.32%) to 5,616.84; the Dow Jones Industrial Average® ($DJI) rose 65.44 points (0.16%) to 41,240.52; the NASDAQ Composite®($COMP) fell 152.02 points (–0.85%) to 17.725.77.

The 10-year Treasury note yield (TNX) inched up about one basis point to nearly 3.82%.

The CBOE Volatility Index® (VIX) edged up to 16.09 but remains below its historic average.

Americans can receive free Covid-19 tests through the mail beginning next month.

Posted on August 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

Demand for a variety of healthcare services – including those provided by hospitals – is likely to increase significantly in the near future, primarily as a result of the changing demographics of the U.S. population, most notably the growth in the number of Americans over the age of 65. Indeed, a Health Affairs study found that population aging alone will create approximately 0.74% annual growth in the demand for inpatient hospital services. While hospital consolidation is leading to operational efficiency for hospitals in providing services to an increasing number of patients, the federal government’s intensifying focus on anti-competitive behaviors in healthcare may hinder traditional consolidation efforts going forward.

This second installment in a five-part series on the valuation of hospitals reviews the competitive environment in which hospitals operate. (Read more...)

Posted on August 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS COMMON STOCK “PAR” VALUE?

DEFINITION:

For common stock, the value on the books of the corporation. It has little to do with market value or even the original price of shares at first issuance. The difference between par and the price at first issuance is carried on the books of a corporation as “paid-in capital” or “capital surplus.”

Par value for preferred stocks is also liquidating value and the value on which dividends (expressed as a percentage) are paid, generally $100 per share.

Financial ratio analysis typically involves the calculation of ratios that are financial and operational measures representative of the financial status of a clinic or medical practice enterprise. These ratios are evaluated in terms of their relative comparison to generally established industry norms, which may be expressed as positive or negative trends for that industry sector. The ratios selected may function as several different measures of operating performance or financial condition of the subject entity.

Common types of financial indicators that are measured by ratio analysis include:

Liquidity. Liquidity ratios measure the ability of an organization to meet cash obligations as they become due, i.e., to support operational goals. Ratios above the industry mean generally indicate that the organization is in an advantageous position to better support immediate goals. The current ratio, which quantifies the relationship between assets and liabilities, is an indicator of an organization’s ability to meet short-term obligations. Managers use this measure to determine how quickly assets are converted into cash.

Activity. Activity ratios, also called efficiency ratios, indicate how efficiently the organization utilizes its resources or assets, including cash, accounts receivable, salaries, inventory, property, plant, and equipment. Lower ratios may indicate an inefficient use of those assets.

Leverage.Leverage ratios, measured as the ratio of long-term debt to net fixed assets, are used to illustrate the proportion of funds, or capital, provided by shareholders (owners) and creditors to aid analysts in assessing the appropriateness of an organization’s current level of debt. When this ratio falls equal to or below the industry norm, the organization is typically not considered to be at significant risk.

Profitability. Indicates the overall net effect of managerial efficiency of the enterprise. To determine the profitability of the enterprise for bench marking purposes, the analyst should first review and make adjustments to the owner(s) compensation, if appropriate. Adjustments for the market value of the “replacement cost” of the professional services provided by the owner are particularly important in the valuation of professional medical practices for the purpose of arriving at an ”economic level” of profit.

The selection of financial ratios for analysis and comparison to the organization’s performance requires careful attention to the homogeneity of data. Bench marking of intra-organizational data (i.e., internal bench marking) typically proves to be less variable across several different measurement periods.

However, the use of data from external facilities for comparison may introduce variation in measurement methodology and procedure. In the latter case, use of a standard chart of accounts for the organization or recasting the organization’s data to a standard format can effectively facilitate an appropriate comparison of the organization’s operating performance and financial status data to survey results.

In Part 1, we discussed how to establish fair market value (FMV) for a medical practice in the article, “Establish Your Practice’s Fair Market Value.” This time, we’ll review important terms and conditions for the sale acquisition and transaction.

Unfortunately, as a general rule, medical practice worth is presently deteriorating. A good medical practice is no longer a good business necessarily, and selling doctors can no longer automatically expect to extract a premium sale price. Nevertheless, appraising your medical practice on a periodic basis can play a key role in obtaining maximum value for it.

Competent practice valuation specialists typically charge a retainer to cover out-of-pocket expenses. Fees should not be based on a percentage of practice value, and may take 30-45 days to complete. Flat fees should be the norm because a sliding scale or percentage fee may be biased toward over-valuation in a declining marketplace. Fees range from $7,500-$50,000 for the small to large medical practice or clinic.

Expect to pay a retainer and sign a formal, professional engagement letter. Seek an unbiased and independent viewpoint. Buyer and sellers should each have their own independent appraisal done, using similar statistics, accounting measures, and economic assumptions.

At the Institute of Medical Business Advisors, Inc www.MedicalBusinessAdvisors.com we use three engagement levels that vary in intensity, purpose, and cost:

1. A comprehensive valuation provides an unambiguous value range. It is supported by most all procedures that valuators deem relevant, with mandatory onsite review. This gold standard is suitable for contentious situations. A written “opinion of value” is applicable for litigation support activities like depositions and trial. It is also useful for external reporting to bankers, investors, the public, Internal Revenue Service (IRS), etc.

2. A limited valuation lacks additional suggested Uniform Standards of Professional Appraisal Practice (USPAP) procedures. It is considered to be an “agreed upon engagement,” when the client is the only user. For example, it may be used when updating a buy/sell agreement, or when putting together a practice buy-in for a valued associate. This limited valuation would not be for external purposes, so no onsite visit is necessary and a formal opinion of value is not rendered.

3. An ad-hoc valuation is a low level engagement that provides a gross non-specific approximation of value based on limited parameters or concerns involved parties. Neither a written report nor an opinion of value is rendered. It is often used periodically as an internal organic growth/decline gauge.

Structure Sales Transactions and Acquisitions

When the practice price has been determined and agreed on, the actual sales deal can be structured in a couple of ways:

(1) Stock Purchase v. Asset Purchase

In an asset transaction, the buyer will receive a tax amortization benefit associated with the intangible value of the business. This tax amortization represents a non-cash expense benefiting the buyer. In this case, the present value of those future tax benefits is added to the business enterprise value.

(2) Corporate Transactions

Typical private deals in the past involved some multiple (ratio) of earning before income taxes (EBIT)—usually a combination of cash, restricted stock, notes receivable, and possibly assumption of liabilities. For some physician hospital organizations, and public deals, the receipt of common stock can increase the practice price by as much as 40-50 percent (to accept the corresponding business risk, in lieu of cash).

Complete the Deal

The deal structure will vary depending on whether the likely buyer is a private practitioner, health system or a corporate partner. Some key issues to consider in the “art of the deal” include:

Working capital (in or out?): Including working capital in the transaction will increase the sale price.

Stock vs. asset transaction: Structuring the deal as an asset purchase will increase practice value due to the tax amortization benefits received by the buyer for intangible assets of the practice.

Common stock premium: The total sale price can be significantly higher than a cash equivalent price for accepting the risk and relative illiquidity of common stock as part of the payment.

Physician compensation: If your goal is to maximize practice value, take home a lower salary to increase practice sale price. The reverse is also true.

Understand Private Deal Structure

Assuming a practice sale is a private transaction, deal negotiations are based on the following pricing methodologies:

Seller financing: Many transactions involve an earn-out arrangement where the buyer puts money down and pays the balance under a formula based on future revenues, or gives the seller a promissory note under similar terms. Seller financing decreases a buyer’s risks (the longer the terms, the lower the risk). Longer terms demand premiums, while shorter terms demand discounts. Premiums that buyers pay for a typical seller-financed practice are usually more than what you would expect from a simple time value of money calculation, as a result of buyer risk reduction from paying over time, rather than up front with a bank loan or all cash. Remember to obtain a life insurance policy on the buyer.

Down payment: The greater the down payment for acquisition of a medical practice, the greater the risk is to the buyer. Consequently, sellers who will take less money up front can command a higher than average price for their practice, while sellers who want more down usually receive less in the end.

Taxation: Tax consequences can have a major impact on the price of a medical practice. For instance, a seller who obtains the majority of the sales price as capital gains can often afford to sell for a much lower price and still pocket as much or more than if the sales price were paid as ordinary income. Value attributed to the seller’s patient list, medical records, name brand, good will, and files qualifies for capital gains treatment. Value paid for the selling doctor’s continuing assistance after the sale and value attributed to a non-compete agreement are taxed at ordinary income. A buyer willing to allocate more for items with capital gains treatment, or a seller willing to take more in ordinary income, can frequently negotiate a better price. This is the essence of economically prudent practice transition planning.

Sidestep Common Buyer Blunders

Here are 10 blunders to avoid, as a buyer:

1. Believing the selling doctor’s attestations. Always verify data through an independent appraisal.

2. Wanting to change the culture of the practice. Be careful: Patients may not adjust quickly to change.

3. Using all available cash without keeping a reserve for potential contingencies.

4. Creating a conflict with the seller by recognizing a weakness and continually focusing on it for a bargain price.

5. Failing to realize that managed care plan contracts can be lost quickly or may not be always transferable.

6. Suffering from analysis paralysis. Money cannot be made by continually checking out a medical practice, only by actually running one.

7. Not appreciating the uniqueness of each practice, and using inaccurate “rules of thumb” from the golden age of medicine.

8. Not realizing that practice worth and goodwill value have plummeted lately and continue to decline in most parts of the country.

9. Not understanding that practice brokers may play both sides of the buy/sell equation for profit. Brokers usually are not obligated to disclose conflicts of interest, are not fiduciaries, and do not provide testimony as a court-approved expert witness.

10. Not hiring an appraisal professional who will testify in court, if need be, using the IRS-approved USPAP methods of valuation. Always assume that the appraisal will be contested (many times, it is).

After pricing and contracting due diligence has been performed, the next step in the medical practice sale process—as Donald Trump might say—is just good, old-fashioned negotiation.

Cimasi, R.J., A.P. Sharamitaro, T.A. Zigrang, L.A.Haynes. Valuation of Hospitals in a Changing Reimbursement and Regulatory Environment. Edited by David E. Marcinko. Healthcare Organizations: Financial Management Strategies. Specialty Technical Publishers, 2008.

Marcinko, D.E. “Getting it Right: How much is a plastic surgery practice really worth?” Plastic Surgery Practice, August 2006.

Marcinko, D.E., H.R. Hetico. The Business of Medical Practice (3rd ed). Springer Publishing,New York,N.Y., 2011.

Marcinko, D.E. and H.R. Hetico. Risk Management and Insurance Planning for Physicians and Advisors. Jones and Bartlett Publishers, Sudbury, Mass., 2007.

Marcinko, D.E. and H.R. Hetico. Financial Planning for Physicians and Advisors. Jones and Bartlett Publishers, Sudbury, Mass., 2007.

Marcinko, D.E. and H.R. Hetico. Dictionary of Health Insurance and Managed Care. Springer Publishers, New York, N.Y., 2007.

Marcinko, D.E. and H.R. Hetico. Dictionary of Health Economics and Finance. Springer Publishers,New York,N.Y., 2007.

There are a Myriad of Reasons for Obtaining a Medical Practice Valuation and Appraisal Engagement:

Outright selling-buying

Partnership and Associate buy-in / buy-out

Mergers and Acquisitions

Organic growth tracking

Hospital integrations

Private and public reporting

Financing and Venture Capital

Estate and tax planning

Our Capability

We have the ability to provide extensive analysis of value components in healthcare practices and provide appraisals based on business, economic, and market conditions. This involves detailed examination of financials and clinical data in the context of numerous factors including medical specialty, physician supply and demand, payer mix, regulatory environment, regional dynamics, and risk premium.

Posted on August 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Later this week, central bankers will meet in the shadow of the Tetons for the Jackson Hole Symposium, an annual retreat for global economic officials to talk monetary policy.

The main event: Federal Reserve Chairman Jerome Powell’s keynote speech on Friday, which investors hope will clarify the timing and pace of interest rate cuts.

Posted on August 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Free Market Medical Association

*** DEFINITION: Direct Primary Care (DPC) is an innovative alternative payment model improving access to high functioning healthcare with a simple, flat, affordable membership fee. No fee-for-service payments. No third party billing. The defining element of DPC is an enduring and trusting relationship between a patient and his or her primary care provider. Patients have extraordinary access to a physician of their choice, often for as little as $70 per month, and physicians are accountable first and foremost their patients. DPC is embraced by health policymakers on the left and right and creates happy patients and happy doctors all over the country!

Posted on August 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The FDA declined to approve MDMA as a PTSD treatment, which would have been a big step forward for psychedelics use in mental health care, saying further study is needed. But the agency did approve a nasal spray to treat severe allergic reactions as an alternative to shots like EpiPen.

Stellantis will lay off 2,450 factory workers this year as it phases out an older version of its Ram pickup truck.

Scams via Zelle, the payment service you turn to when you run out of wedding gift ideas, are the subject of an ongoing inquiry by the Consumer Financial Protection Bureau (CFPB), the Wall Street Journal reported this week. Zelle was founded in 2017 by seven of the biggest US banks to compete with peer-to-peer payment apps like Venmo and Cash App. It outgrew its rivals but became a magnet for scams, which customers typically don’t get reimbursed for.

Posted on August 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On July 10, 2024, the Centers for Medicare & Medicaid Services (CMS) released its proposed Medicare Physician Fee Schedule (MPFS) for calendar year (CY) 2025.

In addition to the agency’s suggested cut to physician payments, the proposed rule also announced new covered services. According to CMS, the proposed rule “reflect[s] a broader Administration-wide strategy to create a more equitable health care system that results in better accessibility, quality, affordability, empowerment, and innovation for all Medicare beneficiaries.” (Read more…)

Posted on August 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

FTX was ordered to pay $12.7 billion to customers. All customers will recoup their deposits that were locked when the crypto exchange went under in 2022, the Commodity Futures Trading Commission just said last Thursday.

Take-Two Interactive Software surged 4.35% after it beat earnings estimates last quarter, but no word yet on how its Gearbox acquisition is helping its bottom line, nor when GTA 6 is going to be released.

Expedia traveled 10.21% higher due to an earnings beat, with the company sidestepping a consumer spending slowdown quite nicely.

What’s down

e.l.f. Beauty tanked 14.46% despite beating earnings estimates and guiding for a better fiscal year than expected, as investors worry about tough competition.

Capri Holdings slid 4.86% as the company founded by Michael Kors faces slowing sales from cash-strapped consumers.

The S&P 500® index (SPX) rose 25 points (0.5%) to 5,344.16, ending the week little changed; the Dow Jones Industrial Average® ($DJI) rose 51 points (0.1%) to 39,497.54 to end the week down about 0.6%; the NASDAQ Composite® ($COMP) ended 85 points higher (0.5%) at 16,745.30, leaving it about 0.2% lower for the week.

The 10-year Treasury note yield (TNX) dropped five basis points to 3.944%.

The Cboe Volatility Index (VIX) declined three points (13%) to 20.7.

Google and Meta teamed up to target teens with ads for Instagram on YouTube, going against Google’s own rules, the Financial Times reported.

Posted on August 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A carry trade is a tactic in which an investor borrows a currency with lower interest rates and invests the proceeds in a higher-yielding asset, often in a different market with higher interest rates.

Over the past few years, many funds were using this strategy by buying US equities or selling US bonds with money borrowed from the yen because of the huge disparity in interest rates between the US and Japan. Japan kept the yen cheap on purpose because its economy is primarily export-driven, and the low price of Japanese products kept exports thriving. And the dollar, as the dominant global currency, has remained impressively strong through thick and thin.

This was all fun and profits, until Japan raised interest rates for the first time in 17 years last week. Suddenly, the yen wasn’t as cheap as it once was. And at the exact same time, the US is expected to cut interest rates in September, which means the dollar would become less valuable, completely throwing this international carry trade out of balance

Posted on August 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

By Staff Reporters

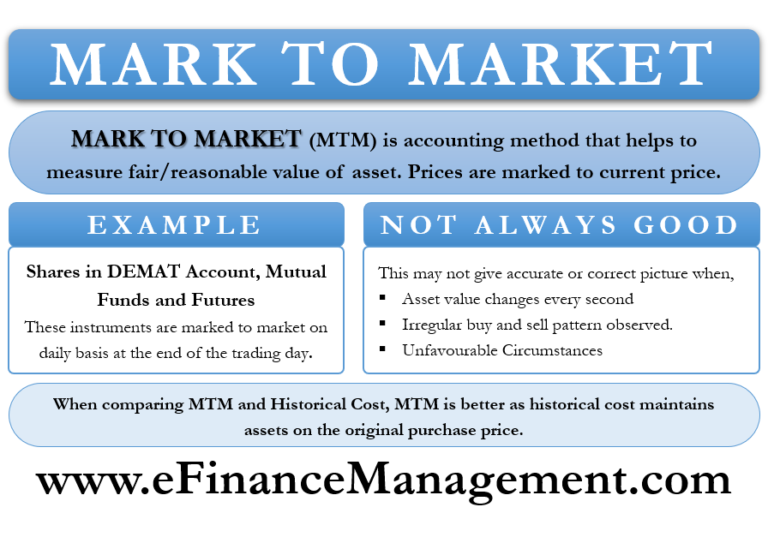

According to Wikipeida, Mark-to-market (MTM or M2M) or fair value accounting is accounting for the “fair value” of an asset or liability based on the current market price, or the price for similar assets and liabilities, or based on another objectively assessed “fair” value.[1] Fair value accounting has been a part of Generally Accepted Accounting Principles (GAAP) in the United States since the early 1990s. Failure to use it is viewed as the cause of the Orange County Bankruptcy,[2][3] even though its use is considered to be one of the reasons for the Enron scandal and the eventual bankruptcy of the company, as well as the closure of the accounting firm Arthur Andersen.[4]

Mark-to-market accounting can change values on the balance sheet as market conditions change. In contrast, historical cost accounting, based on the past transactions, is simpler, more stable, and easier to perform, but does not represent current market value. It summarizes past transactions instead. Mark-to-market accounting can become volatile if market prices fluctuate greatly or change unpredictably. Buyers and sellers may claim a number of specific instances when this is the case, including inability to value the future income and expenses both accurately and collectively, often due to unreliable information, or over-optimistic or over-pessimistic expectations of cash flow and earnings.[5]

Stock brokers allow their clients to access credit via margin accounts. These accounts allow clients to borrow funds to buy securities. Therefore, the amount of funds available is more than the value of cash (or equivalents). The credit is provided by charging a rate of interest and requiring a certain amount of collateral, in a similar way that banks provide loans. Even though the value of securities (stocks or other financial instruments such as options) fluctuates in the market, the value of accounts is not computed in real time. Marking-to-market is performed typically at the end of the trading day, and if the account value decreases below a given threshold (typically a ratio predefined by the broker), the broker issues a margin call that requires the client to deposit more funds or liquidate the account.

When it comes to purchasing a medical practice, there are a variety of factors that one must consider in evaluating the worth of the practice. Assessing the value of a practice is fraught with potential landmines if one does not go into the process with a strong understanding of some key principles to medical practice valuation.

According to the Dictionary of Health Economics and Finance, practice valuation is the “formal process of determining the worth of healthcare or other medical business entity at a specific point in time and the act or process of determining fair market value.” Fair market value is defined as “ … the price at which a willing buyer will buy and a willing seller will sell an asset in an open free market with full disclosure.”

The Internal Revenue Service (IRS) Revenue Ruling 59-60 clearly states that fair market value “is essentially a future prophecy and must be based on facts available at the required date of appraisal.”

Unfortunately, one cannot directly observe the value of a medical practice as there are a number of underlying issues. Obviously, the buyer and seller are pursuing opposite objectives, and this reality is not necessarily conducive to facilitating clarity on those issues.

Accordingly, let us consider a few mistakes that are commonly made by physicians who are considering the purchase of a medical practice.

A Guide To The Myths And Realities Of Medical Practice Valuation

• Valuations are material representations providing a range of transferable worth. • Valuations are reproducible estimates based on economic assumptions. • Valuations are not “back of the envelope multiples” using specious benchmarks. • Valuations are defensible and should be “signed off” by the completing firm attesting to origination guidelines and in accordance with the Uniform Standards of Professional Appraisal Practice (USPAP) and IRS formats as needed. • Financial accounting value (book value) is not fair market value. • Professional valuators represent only one party. The buyer or seller-owner is the client. • Unbiased valuators do not provide financing or equity participation schemes.

Knowing The Distinctions Among Engagement Types

The Institute of Medical Business Advisors uses three levels that approximate engagement types for the industry. These levels are comprehensive valuation, limited valuation and ad-hoc valuation.

A comprehensive valuation is an extensive service designed to provide an unambiguous opinion of the value range. It is supported by all procedures that valuators deem relevant with mandatory onsite review. This gold standard is suitable for contentious situations like divorce, partnership dissolution, estate planning and gifting, etc. The written opinion of value is applicable for litigation support activities like depositions and trial. It is also useful for external reporting to bankers, investors, the public and IRS, etc.

A limited valuation lacks additional suggested USPAP procedures. It is considered to be an “agreed upon procedure,” which is used in circumstances in which the client is the only user. For example, one may use the limited valuation when updating a buy-sell agreement or when putting together a practice buy-in for a valued associate. This limited valuation would not be for external purposes. No onsite visit is needed. A formal opinion of value is not rendered.

An ad-hoc valuation is a low level engagement that provides a gross and non-specific approximation of value based on limited limited parameters or concerns by involved parties. Neither a written report nor an opinion of value is rendered. The ad-hoc valuation is often used periodically as an internal organic growth/decline gauge.

Are You Following Industry Standards And Rules?

Specifically, when it comes to USPAP transactions involving physician practices, the following points are implied by the industry and the IRS.

• Discounted cash flow analysis is the most relevant income approach and must be done on an “after-tax” basis. It generally produces a higher value but is costly, detail-oriented and time consuming. • Project practice collections based on reasonable assumptions for the practice and market, etc. • Physician compensation is based on market rates consistent with age, experience and productivity. • Majority (control) premiums and minority (lack of control) discounts are also to be considered. A majority premium is the amount paid to gain enough ownership to set policies, direct operations and make decisions for the practice. A minority discount for partial ownership does not allow this power. Thus, majority ownership is valuated higher than minority ownership purchase.

What About Personal Goodwill And Practice Goodwill?

Goodwill represents the difference between practice purchase price and the value of the net assets. Personal goodwill results from the charisma, skills and reputation of a specific doctor. These attributes accrue solely to the individual, are not transferable and cannot be sold. Personal goodwill has little or no economic value.

Transferable medical practice goodwill has value, may be transferred and is defined as the unidentified residual attributes that contribute to the propensity of patients and managed care contracts (and their revenue streams) to return in the future.

However, bear in mind that the Goodwill Registry, an older source used to determine the average percentage of revenue contributed to practice goodwill, has sparse to no podiatry input, may be dated for some specialties and leads to abnormally high values.

In addition to various multiple factors, one must also appreciate the impact of a changing environment and practice transfer in a local market, which can augment or blunt goodwill value. It is also important to determine whether patients or HMOs return because of true goodwill or are mandated to do so by contractual obligations.

Now to further confuse the issue, how each kind of goodwill is allocated in situations like divorce depends on state law. For example, some courts weigh in on the apportionment of both kinds of goodwill, other courts exclude both kinds of goodwill and other courts pursue a case-by-case approach.

Understanding ‘Excess Earnings Capitalization’ And Compensation Issues

Another way to determine goodwill value is through “excess earnings capitalization.” This economic method looks at the difference between salary and what you would have to pay a comparable doctor replacement.

As an example, when you subtract the numbers and divide the result by 20 percent, an important percentage referred to as the capitalization rate emerges. The final number gives a dollar value for practice goodwill. Courts seem to prefer this method in divorce situations because it tends to reflect a practice’s current value.

Regardless of the practice business model, physician compensation is inversely related to practice value. In other words, the more a doctor takes home in above average salary, the less the practice is generally worth and vice versa.

Emphasize Practice Specifics Over Benchmarks And Formulas

In the stable economic past, physicians may have used industry benchmarks as quick and inexpensive substitutes for professionally prepared valuations. However, this practice can be fraught with peril if challenged. The courts seem to frown on this simplistic and dated methodology. Moreover, generic benchmark formulas assume a financial statement reporting standard that just does not exist with contemporary professional valuations.

Therefore, almost every competitive issue that impacts value should be addressed with each practice engagement. This includes but is not limited to:

• contemporary dislocations by third parties, Medicare and commercial payers; • retail clinics and changes in supply/ demand and specialty trends; • the rise of ambulatory surgery centers, walk-in clinics and specialty hospitals; • outsourced care and medical tourism; • alterations in resource based-relative value units, ambulatory payment classifications (APCs), diagnosis-related groups (DRGs) and newer Medicare-severity diagnosis-related groups (MS-DRGs); and • the Medicare Modernization Act, HIPAA, OSHA, the EEOC and other regulations.

One must also consider the impact of current employee trends to high-deductible health care plans and private concierge medicine. Another consideration is employer shifts away from defined benefits plans to defined contribution plans.

Aggregating Or ‘Normalizing’ Financial Information: What You Should Know

In addition to possibly conducting employee interviews, one must gather appropriate financial information in order to properly value a practice. As a starting point, interested physician buyers should be able to see the following information for the most recent three-year period.

It is especially important to eliminate one-time, non-recurring practice expenses. These are adjusted for excessive or below normal expenses on the profit and loss statement. Such “normalization” can produce a big surprise for benchmark proponents and formula-driven advocates when a selling doctor runs personal expenditures through the practice that a buyer or court would not consider legitimate. Of course, one is less likely to encounter such shenanigans when the valuation is conducted according to professional USPAP and IRS style guidelines.

For example, we recall one doctor who painted his home and wrote it off as a valid business expense. Deleting other major expenses such as country club memberships make a practice look more profitable. This is good news if you are selling it. It is bad news if you are getting a divorce.

Conversely, you may have to defend legitimate business expenses that an appraiser may seek to normalize. For example, doctors may pay for a vehicle through their practice. If they use the vehicle to travel between multiple offices and hospitals, the expense may be legitimate.

Also realize that the appraiser may also add expenses that have not been incurred. For example, the appraiser may add an office manager’s salary if your spouse is in that role for free. This produces a lower appraised value and is common in small podiatry practices. Honorarium is another example that does not figure into value calculations.

Of course, normalization is a sophisticated and time intensive process. However, the expert earns his or her professional fee, and defends the resulting valuation range when challenged.

Keys To Selecting The Right Valuator Professional

The most important credentials to look for are fiduciary level experience, specificity and independence. Some doctors mistakenly turn to those who may have never appraised a practice before. Just because an appraiser has initials behind his or her name, it does not mean he or she understands the peculiarities of medical specialties. Agents, brokers, solicitors and other intermediaries are not fiduciaries.

Physicians looking to assess a practice for possible sale/purchase should only select an independent health economist, who will be your advocate under Securities Exchange Commission (SEC), IRS or other relevant managerial accounting guidelines.

Moreover, be very wary if the valuation is not done in an independent manner or, worse, performed for both parties simultaneously.

Essential Insights On Professional Fees And What You Can Expect

Of course, it is almost impossible to answer concerns regarding fees without specific information. The cost of a valuation can range from $0 to $50,000 for an onsite team of experts for behemoth practices and ambulatory surgery centers. Keep in mind that in most cases you want to ensure the value determination will stand up to IRS scrutiny so the $0 rule of thumb approach is not an option.

However, most reputable firms use a blended fee schedule of fixed and hourly rates (plus expenses). Internists should expect to spend approximately $5,000 to $10,000 for an average sized practice and a limited appraisal that is completely suitable for most internal activities.

External appraisals or poorly aggregated financial information, onsite reviews and litigation support services incur additional costs. However, most doctors find the money well spent. Expect to pay a retainer and sign a formal professional engagement letter.

Finally, once the practice price is agreed upon, sales contract terms and agreements present a plethora of financing challenges for both parties to consider. For example, one must negotiate bank loans (if they are even available), payment rates and length, personal promissory guarantees, down payment offsets, earn-out arrangements and Uniform Commercial Codes.

Final Notes

Do not be surprised if a sales broker does not consider the aforementioned issues as the modern health era emerges. Most agent-appraisers are predominantly concerned with earning commissions by working both transaction parties and may not represent your best interests. Also be aware that they are usually not obliged to disclose conflicts of interest and do not provide testimony as a court approved expert witness.

However, it is a fait accompli that medical practice worth is presently deteriorating. As the population ages and third-party reimbursements plummet, doctors are commoditized and traditional retail medicine is replaced by more efficient wholesale business models like workplace health clinics. The subprime mortgage default fiasco, credit freeze, potential tax reform law expiration, the ACA, VBC, capitation payments and the political specter of a nationalized healthcare system only add fuel to the macroeconomic fires of uncertainty. Do not forget the corona pandemic.

As a result, a good medical practice is no longer good business necessarily and retiring doctors can no longer automatically expect to extract premium sales prices. Moreover, uninformed young physicians should not be goaded to overpay.

Statistics: 7.4%. That’s the percentage drop in students who graduated with a degree in accounting in the 2021–2022 school year than the year before. Low starting salaries, heavy workloads, and uncertainty around AI are driving the exodus of students from choosing accounting degrees. (the Wall Street Journal).

Posted on August 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What it is – How it works?

[By staff reporters]

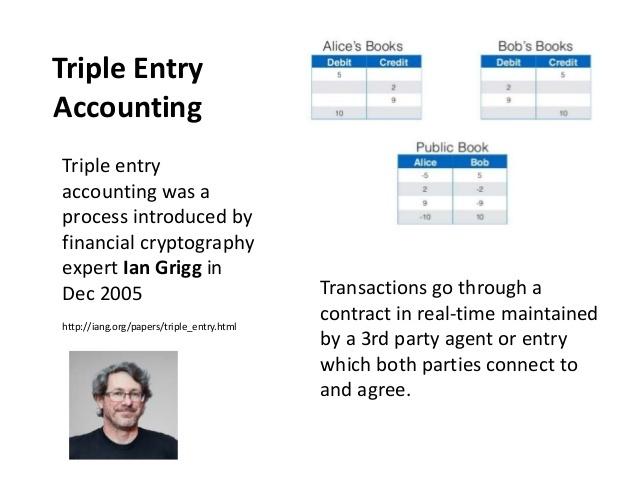

The term “Triple Entry Accounting,” was first used by Ian Grigg, financial cryptographer, and described in his paper published in 2005, three years before the emergence of Bitcoin and its underlying Blockchain protocol.

Here is the original historical article on “Triple Entry Accounting” by Grigg:

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on August 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Jerome Powell says September rate cut could be “on the table”

By Staff Reporters

***

***

Jerome Powell isn’t known for being direct, but he made an exception yesterday, saying an interest rate cut could come “as soon as the next meeting” in September after the FOMC kept rates steady at the two-decade high they’ve been at since last July.

“We’re getting closer to the point at which it’ll be appropriate to reduce our policy rate,” he said. “But we’re not quite at that point.”

It’s a change from Powell’s other recent statements, which were hazier on the timing, though he did say the decision to cut rates still depends on inflation continuing to cool.

Posted on July 31, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What it is – How it works

SMART CONTRACTS

[By Staff Reporters]

Wolfram Alpha is an online mathematical search engine launched in March 2009 and developed by Stephen Wolfram. It seeks to answer factual queries directly by computing the answer from structured data, rather than providing a list of web pages that might contain the answer.

In this way, WA differs from traditional semantic search engines, which index a large number of answers and then try to match the question to one. Wolfram Alpha has many parallels with Cyc, a project aimed since the 1980s at developing a common-sense inference engine. Wolfram Alpha is built on Wolfram’s earlier flagship product, Mathematica, which encompasses computer algebra, symbolic and numerical computation, visualization, and statistics capabilities.

With Mathematica running in the background, WA is suited to answer mathematical questions. The answer usually presents a human-readable solution.

Wolfram Alpha is written in about 5 million lines of Mathematica (using webMathematica and gridMathematica) code and runs on 10,000 CPUs. As well as being a web site, Wolfram Alpha provides an API (for a fee) that delivers computational answers to other applications. One such application is the Bing search engine.

Capabilities

As an example, one can input the name of a website, and it will return relevant information about the site, including its location, site rank, number of visitors and more. The database currently includes hundreds of datasets, including current and historical weather, drug data, star charts, currency conversion, and many others. The datasets have been accumulated over approximately two years, and are expected to continue to grow. The range of questions that can be answered is also expected to grow with the expansion of the datasets.

Wolfram Alpha is ideal for use by all readers and subscribers of the ME-P. It may be used by doctors, nurses, financial advisors and insurance agents, economists, mathematicians, editors, and publishers, teachers and students of all academic levels. The graphical nature of output is particularly helpful.

Assessment

Wolfram Alpha has received mixed reviews, to date. Advocates point to its potential, some even stating that how it determines output result is more important than current usefulness.

And so, your thoughts and comments on this ME-P are appreciated. Give Wolfram Alpha a click, listen to the audio-cast, and tell us what you think. Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Posted on July 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

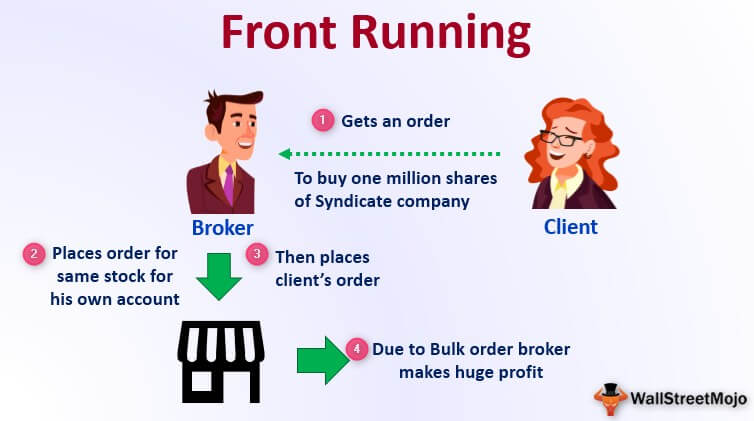

According to Wikipedia, front running, also known as tailgating, is the practice of entering into an equity (stock) trade, option, futures contract, derivative, or security-based swap to capitalize on advance, nonpublic knowledge of a large (“block”) pending transaction that will influence the price of the underlying security. In essence, it means the practice of engaging in a personal or proprietary securities transaction in advance of a transaction in the same security for a client’s account.

Front running is considered a form of market manipulation in many markets. Cases typically involve individual brokers or brokerage firms trading stock in and out of undisclosed, unmonitored accounts of relatives or confederates. Institutional and individual investors may also commit a front running violation when they are privy to inside information.

A front running firm either buys for its own account before filling customer buy orders that drive up the price, or sells for its own account before filling customer sell orders that drive down the price. Front running is prohibited since the front-runner profits come from nonpublic information, at the expense of its own customers, the block trade, or the public market.

Citron Research founder Andrew Left is used to being the one calling out fraud, but federal prosecutors and the SEC claimed he’s the one pulling a financial fast one. The government alleges that Left committed securities fraud by using his appearances on television and his social media accounts to make misleading statements that manipulated the market—and reaped $16 million in profit for doing so.

Left declined to comment to news outlets, but his lawyer told the Wall Street Journal that the government’s cases were “based on a defective theory” and targeted Left for sharing his opinions.

Posted on July 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What’s the difference between an IPO, a special purpose acquisition company (SPAC), and a direct listing?

[By staff reporters]

IPOs are a 6–12 month journey where a company works with investment banks and underwriters, who buy a bunch of shares and then sell them to investors in the public market during the actual IPO. Early investors are able to liquidate their shares, and the company raises new funds.

Direct listings skip the underwriting hullabaloo. But without that stability guarantee, direct listings can result in a more volatile opening. Some companies, like Coinbase, find that it’s worth it to keep their hard-earned money out of bankers’ hands.

SPACs, aka “blank-check companies,” offer yet another alternative path to public markets. A SPAC is a shell company that raises money through the traditional IPO process, then merges with a private company and takes it public.

Posted on July 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd CMP

I grew up in SE inner city Baltimore, Maryland and played stick ball in the parking lot of JHU medical school. And so, I was gratified to learn that it is about to get a lot cheaper—for many students at Johns Hopkins University, at least.

Thanks Mike Bloomberg. Be like Mike!

***

***

The former New York mayor, entrepreneur, and 1964 John Hopkins alum Michael Bloomberg donated $1 billion to the university, according to Bloomberg Philanthropies and the university in a recent announcement. Starting this fall, tuition will be free for students coming from households that earn less than $300,000 annually, and the gift will also cover living expenses and other fees for students from families with less than $175,000 in annual income.

Financial access to medical school is a challenge for many students: The median debt for the class of 2023 is $200,000, according to the Association of American Medical Colleges. This cost can discourage students from attending medical school at a time when the US needs more physicians; the association predicted that there will be a physician shortage of up to 86,000 doctors nationwide by 2036.

Posted on July 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

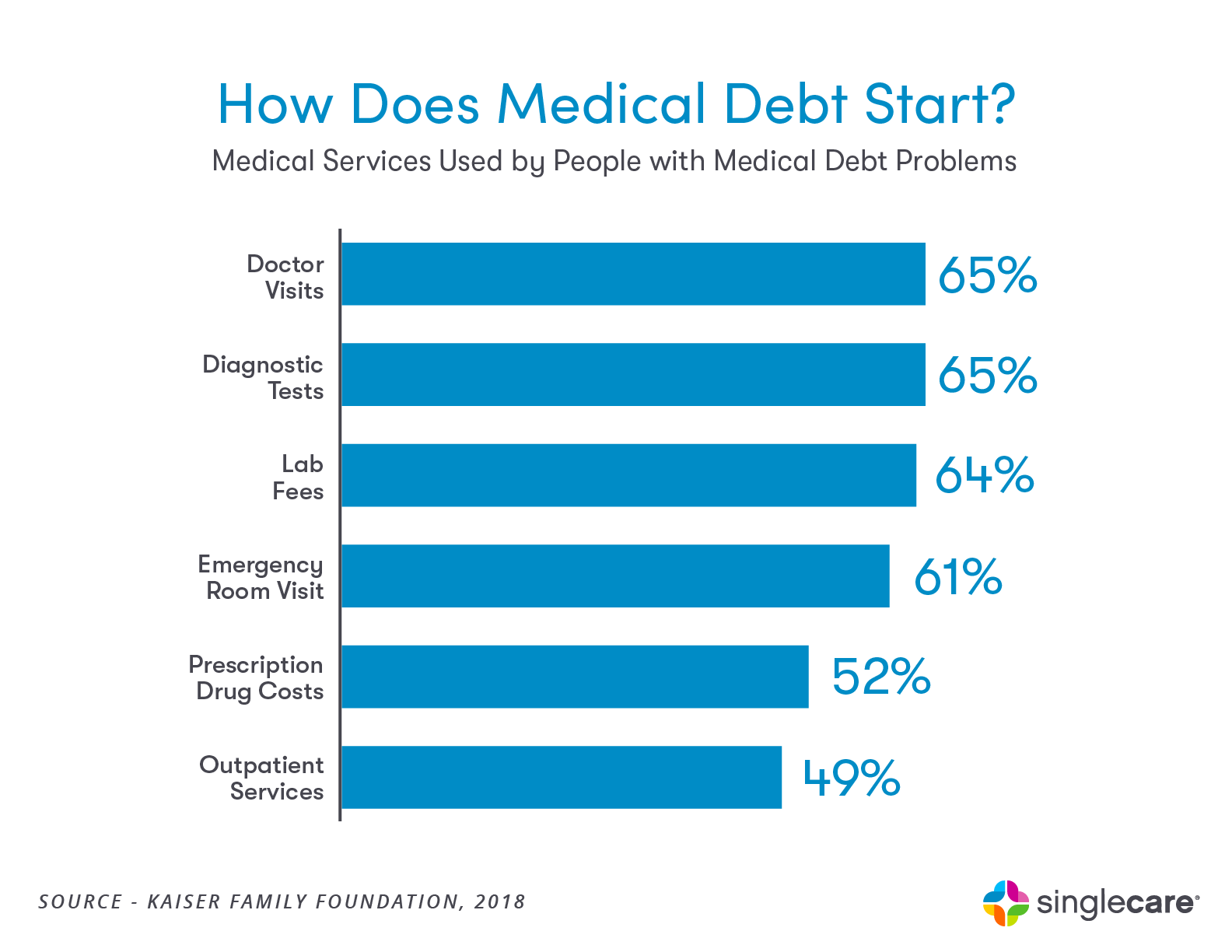

Report underscores ongoing concerns about accuracy of collections data, particularly with respect to medical debt

By Staff Reporters

***

***

According to Gabriella Cruz-Martinez, tens of millions of debt collections disappeared from Americans’ credit reports during the pandemic, a new government watchdog report found, but overdue medical bills remain a big strain on many households nationwide. The total number of debt collections on credit reports dropped by 33% from 261 million in 2018 to 175 million in 2022, according to the Consumer Financial Protection Bureau, while the share of consumers with a debt collection on their credit report shrunk by 20%.

Medical debt collections also dropped by 17.9% during that time, but still made up 57% of all collection accounts on credit reports, far more than other types of debt combined — including credit cards, utilities, and rent accounts. Despite the reduction in collections, the CFPB noted that the results underscore ongoing concerns that current medical billing and collection practices can lack transparency, often hurting the credit scores and financial health of those most vulnerable.

“Our analysis of credit reports provides yet another indicator that, due to a strong labor market and emergency programs during the pandemic, household financial distress reduced over the last two years,” Rohit Chopra, CFPB director said in a statement. “However, false and inaccurate medical debt on credit reports continues to drag on household financial health.”

Posted on July 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

INFLATION EASING

By Staff Reporters

***

***

For the first time since May 2020, the average cost of goods and services in the US made like a remote worker with wanderlust and dipped last month, the Labor Department just reported in July 2024, bolstering confidence that inflation is easing.

Carried by softening gas and rent prices, the consumer price index (CPI) decreased 0.1% in June, beating economists’ forecasts of a 0.1% monthly increase.

That dip brought down the annual CPI, which also beat expectations, to record a 3% year over year gain in June—a one-year price growth low and a rate last seen in early 2021.

Average gas prices fell 3.8% in June, after dropping 3.6% in May.

Shelter prices, which account for about one-third of the CPI, only rose 0.2% in June as rents cooled. It was the category’s smallest monthly rise in three years.

Posted on July 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

On the Self-Employment Tax

By Perry D’Alessio CPA

A sole proprietor is an individual business owner [medical practice] physician-executive whose business [practice] is accounted for on a separate schedule of the owner’s individual income tax return.

Typically, owners filing their business returns via the use of Schedule C of Form 1040 have the lowest level of reporting requirements and also (in general) do the poorest job of keeping good records of business activity.

There is only one level of tax for the sole proprietor. The net profit (or loss) from the Schedule C business is reported on page one of Form 1040 and is combined with all of the other income items reported to arrive at gross income.

Different from interest and dividend income, or investment income that is typically considered passive in nature, self-employment income is income considered to be generated by ones’ own actions.

Self Employment Tax

There is “Self Employment” tax to be paid on virtually all self-employment income reported in the tax return. Many sole proprietors get into trouble because they neglect to take this tax into account when estimating their tax liability for the year and this tax is significant as noted below.

How SET Works