BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on February 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

The most recent numbers show that more than 45 million of us itemized deductions on our 1040s—claiming $1.2 trillion dollars’ worth of tax deductions. That’s right: $1,200,000,000,000! That same year, taxpayers who claimed the standard deduction accounted for $747 billion. Some of those who took the easy way out probably shortchanged themselves. (If you turned age 65 in 2021 or earlier, remember that you deserve a bigger standard deduction than younger folks.)

Here are our 10 most overlooked tax deductions. Claim them if you deserve them, and keep more money in your pocket. Good advice for all physicians, nurse and medical professionals, too.

1. State sales taxes

This write-off makes sense primarily for those who live in states that do not impose an income tax. Especially Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Here’s why this is a factor. You must choose between deducting state and local income taxes or state and local sales taxes. For most citizens of income-taxing-states, the state and local income tax deduction is usually the better deal.

For those of you in an income-tax free state, there are two ways to claim the sales tax deduction on your tax return. One, you can use the IRS tables provided for your state to determine what you can deduct. In addition, if you purchased a vehicle, boat, airplane, home or did major home renovations, you may be able to add the state sales tax you paid on these items to the amount shown in the IRS tables up to the limit for your state. Or two, you can you can keep track of all of the sales tax you paid throughout the year and use that.

The best way to see what you can deduct is to use the IRS’s Sales Tax Calculator for this. Keep in mind, the total of your itemized deductions for all of your state and local taxes is limited to $10,000 per year.

2. Reinvested dividends

This isn’t really a tax deduction, but it is a subtraction that can save you a lot of money. And it’s one that many taxpayers miss. If, like most investors, you have mutual fund dividends automatically invested in extra shares, remember that each reinvestment increases your “tax basis” in the stock or mutual fund. That, in turn, reduces the amount of taxable capital gain (or increases the tax-saving loss) when you sell your shares.

Forgetting to include the reinvested dividends in your cost basis—which you subtract from the proceeds of sale to determine your gain—means overpaying your taxes.

3. Out-of-pocket charitable contributions

It’s hard to overlook the big charitable gifts you made during the year by check or payroll deduction. But the little things add up, too, and you can write off out-of-pocket costs you incur while doing good deeds. Ingredients for casseroles you regularly prepare for a qualified nonprofit organization’s soup kitchen, for example, or the cost of stamps you buy for your school’s fundraiser count as a charitable contribution. If you drove your car for charity in 2021, remember to deduct 14 cents per mile.

4. Student loan interest paid by you or someone else

In the past, if parents or someone else paid back a medical school or other loan incurred by a student, no one got a tax break. To get a deduction, the law said that you had to be both liable for the debt and actually pay it yourself. But now there’s an exception. You may know that you might be eligible to take a deduction but even if someone else pays back the loan, the IRS treats it as though they gave you the money, and you then paid the debt. So, a student who’s not claimed as a dependent can qualify to deduct up to $2,500 of student loan interest paid by you or by someone else.

5. Moving expenses

While most taxpayers lost the ability to deduct moving expenses beginning in 2018, one main group of people who can still claim their moving expenses to the IRS. Who are they? Military personnel. If you’re an active duty military member who is relocating, you can still deduct these expenses —if you don’t receive reimbursement from the government for the move.

Also, as long as the move is permanent —and your relocation was ordered by the military — you don’t have to pay tax on qualified moving expense reimbursements. So start getting those receipts out now – because you can claim travel and lodging expenses for you and your family, moving household goods, and the costs for shipping your cars and your beloved pets! And that’s good news for the men and women we thank for bravely serving our country.

6. Child and Dependent Care Tax Credit

A tax credit is so much better than a tax deduction—it reduces your tax bill dollar for dollar. So missing one is even more painful than missing a deduction that simply reduces the amount of income that’s subject to tax.

But it’s easy to overlook the Child and Dependent Care Credit if you pay your child care bills through a reimbursement account at work. For 2020, the law allows you to run up to $5,000 of such expenses through a tax-favored reimbursement account at work. Up to $6,000 in care expenses can qualify for the credit, but the $5,000 from a tax favored account can’t be used. So if you run the maximum $5,000 through a plan at work but spend more for work-related child care, you can claim the credit on up to an extra $1,000. That would cut your tax bill by at least $200 using the minimum 20 percent of the expenses. The credit percentage goes up for lower income households.

However, there are big changes for 2021, The American Rescue Plan signed into law on March 11, 2021 brought significant changes to the amount and way that the child and dependent care tax credit can be claimed only for tax year 2021. The new law not only increases the credit, but also the amount of taxpayers that will benefit from the credit’s highest rate and it also makes it fully refundable. This means that, unlike previous years, you can still get the credit even if you don’t owe taxes. Changes to the Child and Dependent Care Credit that apply only for tax year 2021 (the taxes you file in 2022) include:

The highest credit percentage increased from 35% to 50% of qualifying expenses

Qualifying child and dependent care expenses increased from $3,000 to $8,000 for one qualifying person and from $6,000 to $16,000 for two or more qualifying individuals

The adjusted gross income (AGI) level at which the credit percentage is reduced is increased from $15,000 to $125,000

For example, prior to the 2021 tax year, a taxpayer with one qualifying person, $3,000 in qualifying expenses and an AGI of $60,000 would qualify for a nonrefundable credit of approximately $600 (20% x $3,000). By contrast, under the new law for tax year 2021 only, a taxpayer with the same circumstances can potentially claim a refundable credit of approximately $1,500 (50% x $3,000).

Also for tax year 2021, the maximum amount that can be contributed to a dependent care flexible spending account and the amount of tax-free employer-provided dependent care benefits is increased from $5,000 to $10,500.

7. Earned Income Tax Credit (EITC)

Millions of lower-income people take this credit every year. However, 25% of taxpayers who are eligible for the Earned Income Tax Credit fail to claim it, according to the IRS. Some people miss out on the credit because the rules can be complicated. Others simply aren’t aware that they qualify.

The EITC is a refundable tax credit—not a deduction— with maximum amounts for different filing statuses ranging from $1,502 to $6,728 for 2021. The credit is designed to supplement wages for low-to-moderate income workers. But the credit doesn’t just apply to lower income people. Tens of millions of individuals and families previously classified as “middle class”—including many medical colleagues and white-collar workers—are now considered “low income” because they:

lost a job

took a pay cut

or worked fewer hours during the year

The exact refund you receive depends on your income, marital status and family size. To get a refund from the EITC you must file a tax return, even if you don’t owe any taxes. Moreover, if you were eligible to claim the credit in the past but didn’t, you can file any time during the year to claim an EITC refund for up to three previous tax years.

8. State tax you paid last spring

Did you owe taxes when you filed your 2020 state tax return in 2021? Then remember to include that amount with your state tax itemized deduction on your 2021 return, along with state income taxes withheld from your paychecks or paid via quarterly estimated payments. Beginning in 2018, the deduction for state and local taxes is limited to a maximum of $10,000 per year.

9. Refinancing mortgage points

When you buy a house, you often get to deduct points paid to obtain your mortgage all at one time. When you refinance a mortgage, however, you have to deduct the points over the life of the loan. That means you can deduct 1/30th of the points a year if it’s a 30-year mortgage—that’s $33 a year for each $1,000 of points you paid. Doesn’t seem like much, but why throw it away?

Also, in the year you pay off the loan—because you sell the house or refinance again—you get to deduct all the points not yet deducted, unless you refinance with the same lender.

10. Jury pay paid to employer

Some employers continue to pay employees’ full salary while they are doing their civic duty, but ask that they turn over their jury fees to the company. The only problem is that the IRS demands that you report those fees as taxable income. If you give the money to your employer you have a right to deduct the amount so you aren’t taxed on money that simply passes through your hands.

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it is?

By Staff Reporters

***

Some doctors and other taxpayers may receive IRS Letter 6475, which references the third Economic Impact Payment. While most recipients eligible for this stimulus check have already received their money in full, some taxpayers might now be eligible or entitled to more money based on their 2021 tax information by claiming a Recovery Rebate Credit on their upcoming tax return. Those people will need this form to confirm how much of the third stimulus check they already received from the government, if they received any at all. Learn more here.

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Stock Markets: S&P 500, DJIA and NASDAQ booked their 4th straight day of gains with technology shares in focus.

And, Facebook rattled investors by posting a rare profit decline, driven by the company’s heavy spending on its vision for a so-called Metaverse while simultaneously confronting advertising challenges on its existing services. The company, formerly known as Facebook, posted net income of nearly $10.3 billion in the final three months of last year, a decline 8% from the same period in the prior year and below Wall Street analysts’ projections. For Meta, the disappointing earnings add to its challenges. It’s in the middle of a number of regulatory fights and also looking to justify its strategic shift to bet on an immersive internet known as the metaverse. Meanwhile, other platforms like TikTok and YouTube are gaining ground with younger users.

Several other social media companies also fell hard after the bell, including Twitter, Pinterest and Spotify, which also released disappointing results. And PayPal fell hard, too!

IRS: The Internal Revenue Service is adding about 1,200 employees to its rolls to help the agency navigate what will likely be one of the most challenging tax filing seasons in years.

Mike Milken: Is headed to the latest power base for U.S. financiers and politicians: South Florida. The income tax-free, palm tree-lined oasis is where New York’s ultra-wealthy have long decamped for the winter, but are increasingly making their permanent home. The 75-year-old billionaire kicks off the first Milken Institute South Florida Dialogues on Friday. The six-day preliminary agenda of island and mansion hopping has Ken Griffin talking national security in South Beach, and Sonia and Paul Tudor Jones hosting tennis matches at their oceanfront Palm Beach estate Casa Apava. The format is similar to the dialogues he’s presented in the Hamptons for years.

Posted on February 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

The IRS Tax Letter 6419 has been sent out to families who received the Child Tax Credit in 2021 and it explains how the advance tax credit will affect your filing this year. This may be of special importance to young physicians, nurses and all younger medical professionals.

Posted on February 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

Tax planning can be quite a tedious process, but there are benefits for all seniors to make it less taxing. And senor medical professionals should take particular note:

Free Advice: IRS-certified volunteers will help older taxpayers with tax return preparation and electronic filing between January 1st and April 15th each year.

No Withdrawal Penalties: Anyone aged 59 years or over can withdraw money from an IRA, without incurring the common 10% tax.

Catch-Up Contributions: Healthcare Workers aged 50 or older can defer income tax on an extra $6,500 or a total of $26,000 if contributed to a 401(k) plan, resulting in a tax savings of $6,240 for an older worker in the 24% tax bracket.

Additional IRA Contribution: Workers age 50 and older can contribute an additional $1,000 to an IRA, or a total of $7,000 in 2020.

Posted on January 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

For those those senior healthcare professionals that like to get out of town, vacation, or visit the grandchildren, be sure to always ask for discounts from the various travel providers. This is especially true for all travelers age 55 years and over. Here are a few we know about … for you to consider post pandemic:

American Airlines: There are various senior discounts that apply to various trips. Call to find out which are available.

Amtrak: Senior pricing is available for most Amtrak locations. This ranges from 10 to 15 percent off.

Alaska Airlines: Seniors can save a significant amount with discount plane tickets. However, discounts vary from one time frame to the next. Most commonly, seniors can save 10 percent.

Southwest Airlines: Seniors over 65 who are traveling with Southwest Airlines may be eligible for Senior Fares. These are available online and for international and domestic travel. You can also purchase Senior Fares through a customer service representative at the airline or a travel agency. You will need to arrive early at the gate to be able to prove your age in order to be checked in for your flight.

United Airlines: United offers discounted prices for flights for seniors over 65. Seniors need to select the Over 65 category when purchasing tickets online or with a customer service agent. Discounts vary depending on the flight and location.

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

Posted on January 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

FOR PHYSICIANS AND ALL OF US!

Br. Dr. David E. Marcinko MBA

By Staff Reporters

***

It’s been announced that January 24th 2022 is the official start of the tax filing season. This means it’s that time of year again to buy some pricey tax software and prepare your return on your own, hire a tax prep pro, CPA, or take advantage of the Free File Program from the IRS.

A Capital Gain [CG] occurs when you sell something for more than you spent to acquire it. This happens with investments, but it also applies to personal property, such as a car. Every physician and taxpayer should understand these basic facts about capital gains taxes.

Capital gains aren’t just for doctors or rich people

Anyone who sells a capital asset should know that capital gains tax may apply. And as the Internal Revenue Service points out, just about everything you own qualifies as a capital asset. That’s the case whether you bought it as an investment, such as stocks or property, or for personal use, such as a car or a big-screen TV.

If you sell something for more than your “basis” in the item, then the difference is a capital gain, and you’ll need to report that gain on your taxes. Your basis is usually what you paid for the item. It includes not only the price of the item, but any other costs you had to pay to acquire it, including:

Sales taxes, excise taxes and other taxes and fees

Shipping and handling costs

Installation and setup charges

In addition, money spent on improvements that increase the value of the asset—such as a new addition to a building—can be added to your basis. Depreciation of an asset can reduce your basis.

In most cases, your home is exempt

The single biggest asset many people have is their home, and depending on the real estate market, a homeowner might realize a huge capital gain on a sale. The good news is that the tax code allows you to exclude some or all of such a gain from capital gains tax, as long as you meet three conditions:

You owned the home for a total of at least two years in the five-year period before the sale.

You used the home as your primary residence for a total of at least two years in that same five-year period.

You haven’t excluded the gain from another home sale in the two-year period before the sale.

If you meet these conditions, you can exclude up to $250,000 of your gain if you’re single, $500,000 if you’re married filing jointly.

Length of ownership matters

If you sell an asset after owning it for more than a year, any gain you have is a “long-term” capital gain. If you sell an asset you’ve owned for a year or less, though, it’s a “short-term” capital gain. How much your gain is taxed depends on how long you owned the asset before selling.

The tax bite from short-term gains is significantly larger than that from long-term gains – typically 10-20% higher.

This difference in tax treatment is one of the advantages a “buy-and-hold” investment strategy has over a strategy that involves frequent buying and selling, as in day trading.

People in the lowest tax brackets usually don’t have to pay any tax on long-term capital gains. The difference between short and long term, then, can literally be the difference between taxes and no taxes.

Capital losses can offset capital gains

As anyone with much investment experience can tell you, things don’t always go up in value. They go down, too. If you sell something for less than its basis, you have a capital loss. Capital losses from investments—but not from the sale of personal property—can be used to offset capital gains.

If you have $50,000 in long-term gains from the sale of one stock, but $20,000 in long-term losses from the sale of another, then you may only be taxed on $30,000 worth of long-term capital gains.

$50,000 – $20,000 = $30,000 long-term capital gains

If capital losses exceed capital gains, you may be able to use the loss to offset up to $3,000 of other income. If you have more than $3,000 in excess capital losses, the amount over $3,000 can be carried forward to future years to offset capital gains or income in those years.

Business income isn’t a capital gain

If you operate a business that buys and sells items, your gains from such sales will be considered—and taxed as—business income rather than capital gains.

For example, many people buy items at antique stores and garage sales and then resell them in online auctions. Do this in a businesslike manner and with the intention of making a profit, and the IRS will view it as a business.

The money you pay out for items is a business expense.

The money you receive is business revenue.

The difference between them is business income, subject to employment taxes.

Whether you have stock, bonds, ETFs, cryptocurrency, rental property income or other investments, this info is vital to increase your tax knowledge and understanding all while doing your taxes.

Posted on January 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Stock Markets: The S&P is off to its worst start to a year since 2016. The NASDAQ is in a correction. And the week ahead features a busy earnings slate and a Federal Reserve meeting.

CovisPandemic: Tony Dr. Fauci said he is “confident as you can be” that the Omicron wave in the US will peak by mid-February. In a growing number of states, that peak has already come and gone and cases are plunging in states like New York and Florida. Other states, such as Oklahoma, Idaho, and Wyoming, are still reporting an uptick in new Covid cases.

Crypto-Currency: Crypto investors, meanwhile, wish they got the weekend off like stock traders, because bitcoin, ethereum, and other digital tokens continued to sink.

Federal Reserve: Federal Reserve officials will get together on Tuesday and Wednesday against the backdrop of quaking markets. Investors will want to hear an update on Chair Jerome Powell’s views on inflation. This Fed meeting will likely be the last before an anticipated interest rate hike in March. And, a blizzard of companies will report including nearly half of the Dow’s 30 giants (American Express, 3M, IBM, and more) and tech heavyweights such as Apple, Microsoft, and Tesla.

Tax Season: The income tax filing season opens today and government officials warn it could be bumpy due to a depleted IRS. The Treasury says to file early, file online, and request your refund via direct deposit to avoid the severe headaches.

On November 30, 2021, the U.S. Supreme Court heard oral arguments regarding the challenges arising from the cuts made by the Centers of Medicare & Medicaid Services (CMS) to the 340B Drug Pricing Program.

The 340B Drug Pricing Program allows hospitals and clinics that treat low-income, medically underserved patients to purchase certain “specified covered outpatient drugs” at discounted prices (applying a ceiling to what drug manufacturers may charge certain healthcare facilities) – 25% to 50% of what providers would typically pay – and then receive reimbursement pursuant to the rates set forth in the Outpatient Prospective Payment System (OPPS) at the same rate as all other providers. (Read more…)

Here are eight things to keep in mind as you prepare to file your 2021 taxes.

1. Income tax brackets have shifted a bit

There are still seven tax rates, but the income ranges (tax brackets) for each rate have shifted slightly to account for inflation. For 2021, the following rates and income ranges apply:

Tax rate

Taxable income brackets:Single filers

Taxable income brackets:Married couples filing jointly (and qualifying widows or widowers)

10%

$0 to $9,950

$0 to $19,900

12%

$9,951 to $40,525

$19,901 to $81,050

22%

$40,526 to $86,375

$81,051 to $172,750

24%

$86,376 to $164,925

$172,751 to $329,850

32%

$164,926 to $209,425

$329,851 to $418,850

35%

$209,426 to $523,600

$418,851 to $628,300

37%

$523,601 or more

$628,301 or more

Source: Internal Revenue Service

2. The standard deduction has increased slightly

After an inflation adjustment, the 2021 standard deduction has increased slightly to $12,550 for single filers and married couples filing separately and $18,800 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction has risen to $25,100.

3. Itemized deductions remain the same

For most filers, taking the higher standard deduction is more practical and saves the hassle of keeping track of receipts. But if you have enough tax-deductible expenses, you might benefit from itemizing.

The following rules for itemized deductions haven’t changed much for 2021, but they’re still worth pointing out.

State and local taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is capped at $10,000.

Mortgage interest deduction: The mortgage interest deduction is limited to $750,000 of indebtedness. But people who had $1,000,000 of home mortgage debt before December 16, 2017, will still be able to deduct the interest on that loan.

Medical expenses: Only medical expenses that exceed 7.5% of adjusted gross income (AGI) can be deducted in 2021.

Charitable donations: The cash donation limit of 100% of AGI remains in place for 2021, if donations were made to operating charities.1

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

4. IRA and 401(k) contribution limits remain the same

The traditional IRA and Roth contribution limits in 2021 remain the same as in 2020. Individuals can contribute up to $6,000 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution. If you’re able to max out your IRA, consider doing so—you may qualify to deduct some or all of your contribution.

The 2021 contribution limit for 401(k) accounts also stays at $19,500. If you’re age 50 or older, you qualify to make an additional $6,500 catch-up contribution as well.

5. You can save a bit more in your health savings account (HSA)

For 2021, the max you can contribute into an HSA is $3,600 for an individual (up $50 from 2020) and $7,200 for a family (up $100). People age 55 and older can contribute an extra $1,000 catch-up contribution.

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (which usually has lower premiums as well). Learn more about the benefits of an HSA.

6. The Child Tax Credit has been expanded

For 2021, the American Rescue Plan Act (ARPA) has temporarily modified the Child Tax Credit requirements and amounts for household incomes below $75,000 for single filers and $150,000 for married filing jointly.

First, the ARPA has raised the age limit for dependents from 16 to 17. In addition, the child tax credit has increased from $2,000 to $3,000 for children age 6 through 17 and up to $3,600 for children under 6. If your income exceeded the above limits but was below $200,000 for single filers or $400,000 for joint filers, you’ll receive the standard child tax credit of $2,000 per child.

The IRS began sending monthly advance Child Tax Credit payments to eligible families in July and sent its last advance in December. If your dependent didn’t qualify for the child tax credit, you may still qualify for up to $500 of tax credits under the “credit for other dependents” (see IRS Publication 972 for more details). Tax credits, which reduce the tax you owe dollar for dollar, are generally better than deductions, which reduce your taxable income.

7. The alternative minimum tax (AMT) exemption has gone up

Until the AMT exemption enacted by the Tax Cuts and Jobs Act expires in 2025, the AMT will continue to affect mostly households with incomes over $500,000. Still, the AMT has investment implications for some high earners.

For 2021, the AMT exemptions are $73,600 for single filers and $114,600 for married taxpayers filing jointly. The phase-out thresholds are $1,047,200 for married taxpayers filing a joint return and $523,600 for all other taxpayers.

8. The estate tax exemption is even higher

The estate and gift tax exemption, which is indexed to inflation, has risen to $11.7 million for 2021. But the now-higher exemption is set to expire at the end of 2025, meaning it could be essentially cut in half at that time if Congress doesn’t act.

The annual gift exclusion, which allows you to give money to your loved ones each year without incurring any tax liability or using up any of your lifetime estate and gift tax exemption, stays at $15,000 per recipient.

Don’t get caught off guard

As you prepare to file your taxes for 2021, here are a few additional items to consider.

If you’re not retired, the 10% early withdrawal penalty that was waived for retirement account distributions in 2020 has been reinstated for 2021.

If you’re age 72 or older, make sure you’ve taken your required minimum distribution (RMD) from your retirement accounts or else you face a 50% penalty on any undistributed funds (unless it’s your first RMD, in which case, you can wait until April 1, 2022).

If you haven’t contributed to your retirement accounts already, now is the time. Review your earnings for the year and take advantage of any deductions that can lower your tax bill. Also, keep an eye on Washington for any last-minute tax changes that could affect your return before you file. Tax season will be here before you know it, and it’s never too early to start preparing.

1Operating charities, or qualifying public charities, are defined by Internal Revenue Code section 170(b)(1)(A). You can use the Tax Exempt Organization Search tool on IRS.gov to check an organization’s eligibility.

Posted on January 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Spike in Hospitals Suing Patients for Unpaid Medical Bills

• Lawsuits over unpaid bills for hospitals rose by 37% in Wisconsin from 2001 to 18. • Wage garnishments from the lawsuits rose 27% in that time period. • 5% of hospitals account for 25% of lawsuits. Nonprofit hospitals and critical access hospitals are more likely to sue patients, according to the study. • There were 1.86 lawsuits per 1,000 Black residents in 2018, compared to 1.32 per 1,000 white residents.

Posted on January 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

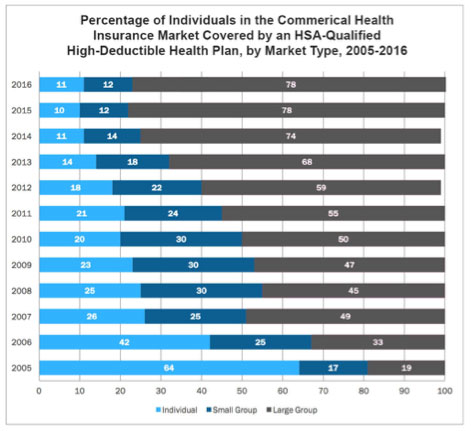

In the United States, a high-deductible health plan is a health insurance plan with lower premiums and higher deductibles than a traditional health plan. It is intended to incentivize consumer-driven healthcare. Being covered by an HDHP is also a requirement for having a health savings account. Some HDHP plans also offer additional “wellness” benefits, provided before a deductible is paid.

High-deductible health plans are a form of catastrophic coverage, intended to cover for catastrophic illnesses. Adoption rates of HDHPs have been growing since their inception in 2004, not only with increasing employer options, but also increasing government options. As of 2016, HDHPs represented 29% of the total covered workers in the United States; however, the impact of such benefit design is not widely understood.

***

% Covered Employees Enrolled in Account-Based CDHP’s

Posted on January 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

INFLATION – Did we say [Health Care] Inflation?

****

***

Why? Inflation, which is the rate of price increases over time, affects all of us on a personal level. We pay electric bills, go grocery shopping, decorate our houses, buy cars—and this year all of those things got more expensive. Especially health care.

Thanks to a nefarious mix of soaring demand for goods and snarled supply chains, US consumer prices jumped the most in 39 years in November, and the 6.8% inflation rate marked the sixth straight month inflation grew by 5% or more. Producer prices, which can eventually trickle down to individuals, also increased at their fastest pace on record last month.

Of course, some inflation is good for the economy when wages keep up with rising prices (the Fed aims for a 2% inflation rate over time). But, so far in the pandemic, that hasn’t happened. While many Americans have gotten a raise in 2021, wage gains haven’t been sufficient to offset inflation, resulting in the erosion of purchasing power—especially for folks on a more or less fixed income.

Where do we go from here?

After months of claiming inflation was “transitory,” the Fed has dropped that term and adopted a more hawkish monetary policy to tamp down surging prices. The central bank is winding down its bond-buying stimulus program faster than originally planned, and also plans to hike interest rates three times in 2022.

In its inflation-fighting efforts, the Fed isn’t alone on the front lines. The Bank of England became the first major central bank to raise interest rates during the pandemic in order to combat the biggest annual jump in consumer prices in 10 years. Russia has raised rates seven times this year. Mexico, Chile, Costa Rica, Pakistan, and Hungary are among other countries which are tightening monetary policy to combat higher prices.

Looking ahead…as if economic policymakers needed another inflation curveball, Omicron has taken the mound. Central banks generally don’t expect the new variant to significantly dent economic growth, but they do think it may prolong inflation by exacerbating the supply–demand imbalance that fueled higher prices in the first place.

On December 2, 2021, the U.S. Department of Justice (DOJ) announced that it had entered into an $18.2 million settlement with Flower Mound Hospital, a 91-bed hospital located northwest of Dallas, to resolve claims that the hospital had violated the Stark Law, the Anti-Kickback Statute (AKS), and the False Claims Act (FCA) by making improper inducements to referring physicians. This Health Capital Topics article will review the facts underlying the settlement. (Read more…)

Posted on December 12, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Doctors Must Understand the Tax Man

By Staff Reporters

***

Mutual-fund physician and other investors with holdings in taxable accounts need to prepare for a tax hit on distributed gains — even if they reinvest the distributions. They can offset some or all of the gains (and taxes) if they’ve sold positions at a loss.

Physicians and people who own mutual funds in tax-sheltered accounts such as 401(k)s or individual retirement accounts and are reinvesting the distributions, on the other hand, don’t have to worry. In those accounts, taxes only count when investors sell holdings in retirement, and those who have funds in qualified Roth IRAs won’t have to pay even then.

When President Joe Biden was elected in 2020, there was much anticipation and speculation regarding what his election would mean for the U.S. healthcare industry in the coming years.

As an ardent supporter of the Patient Protection and Affordable Care Act (ACA) who campaigned on offering a public insurance option similar to Medicare, many in the healthcare industry assumed that the Biden Administration would be a strong proponent of continuing the shift to value-based care, which shift was largely spurred by his predecessor and former boss, Barack Obama, with the passage of the ACA. (Read more…)

Posted on December 7, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

A Curated Report

By Staff Reporters

***

The marriage penalty has faded in recent years, particularly after the 2017 Republican tax cuts that targeted high incomes. But the singles penalty remains — the tax code is still written to benefit people in 1950s middle-class marriages who own their homes. That’s not great for the millions of households who are shouldering other cost burdens around single life.

Progressive tax codes are intended, at least theoretically, to ensure equitable distribution of the costs of maintaining civilization. They should (again, theoretically) be readjusted when a certain group begins to shoulder a disproportionate amount of that burden — like, for instance, single or divorced people. That’s not what’s happened, not for couples with two earners and not for the growing number of single or solo households. The reality of how people live and who works has changed. The policy has not kept pace.

The same principle holds true for Social Security, which was created first and foremost as a means of protecting the elderly from living out their final years in the literal poorhouse. The idea was simple: You and your employers pay in part of your salary now, and when you retire, you have enough to survive.

As noted in the first installment of this five-part series, internal medicine is the largest specialty among physicians and an understanding of the various environments in which these physicians operate is crucial in determining their numerous value drivers.

In particular, healthcare reimbursement, the process by which private health insurers and government agencies pay for the services of healthcare providers (including internists), is perhaps one of the most important environments to understand, as it comprises a provider’s expectation of future return on investment.

Let’s say a physician decided to sell his practice and move to another state. The value of the sale was based, in part, on the yearly gross of the practice. The physician accepted installment payment terms from the buyer and moved to the new state. The buyer began to practice medicine at his new office. Although he was busy, his gross never approached the gross of the prior physician.

Eventually the buyer defaulted on the loan. The selling physician sued for the deficit. The defaulting physician and his forensic consultants then performed an in-depth evaluation of the seller’s practice. The buyer and his team noticed some discrepancies in the billing patterns and practices of the seller. Considering these discrepancies to constitute Medicare and insurance billing fraud, the seller counter-sued the buyer on the grounds of misrepresentation, alleging the gross receipts of the practice purchase price, was grossly inflated.

ASSESSMENT: Therefore, the buyer determined that the seller had fraudulently misrepresented the potential of the practice. He also notified state and federal authorities and filed complaints of insurance fraud against the seller.

The seller thought that he would move to the good life in the new state, but his old practice kept him in constant legal trouble.

Posted on November 10, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

For Doctors and Advisors

BOOK REVIEWS WITH FOREWORD

Reviews

Written by doctors and healthcare professionals, this textbook should be mandatory reading for all medical school students―highly recommended for both young and veteran physicians―and an eliminating factor for any financial advisor who has not read it. The book uses jargon like ‘innovative,’ ‘transformational,’ and ‘disruptive’―all rightly so! It is the type of definitive financial lifestyle planning book we often seek, but seldom find. ―LeRoy Howard MA CMPTM,Candidate and Financial Advisor, Fayetteville, North Carolina I taught diagnostic radiology for over a decade. The physician-focused niche information, balanced perspectives, and insider industry transparency in this book may help save your financial life. ―Dr. William P. Scherer MS, Barry University, Ft. Lauderdale, Florida This book was crafted in response to the frustration felt by doctors who dealt with top financial, brokerage, and accounting firms. These non-fiduciary behemoths often prescribed costly wholesale solutions that were applicable to all, but customized for few, despite ever-changing needs. It is a must-read to learn why brokerage sales pitches or Internet resources will never replace the knowledge and deep advice of a physician-focused financial advisor, medical consultant, or collegial Certified Medical Planner™ financial professional. ―Parin Khotari MBA,Whitman School of Management, Syracuse University, New York In today’s healthcare environment, in order for providers to survive, they need to understand their current and future market trends, finances, operations, and impact of federal and state regulations. As a healthcare consulting professional for over 30 years supporting both the private and public sector, I recommend that providers understand and utilize the wealth of knowledge that is being conveyed in these chapters. Without this guidance providers will have a hard time navigating the supporting system which may impact their future revenue stream. I strongly endorse the contents of this book.

―Carol S. Miller BSN MBA PMP,President, Miller Consulting Group, ACT IAC Executive Committee Vice-Chair at-Large, HIMSS NCA Board Member This is an excellent book on financial planning for physicians and health professionals. It is all inclusive yet very easy to read with much valuable information. And, I have been expanding my business knowledge with all of Dr. Marcinko’s prior books. I highly recommend this one, too. It is a fine educational tool for all doctors.

―Dr. David B. Lumsden MD MS MA,Orthopedic Surgeon, Baltimore, Maryland There is no other comprehensive book like it to help doctors, nurses, and other medical providers accumulate and preserve the wealth that their years of education and hard work have earned them. ―Dr. Jason Dyken MD MBA, Dyken Wealth Strategies, Gulf Shores, Alabama I plan to give a copy of this book written ‘by doctors and for doctors’ to all my prospects, physician, and nurse clients. It may be the definitive text on this important topic. ―Alexander Naruska CPA, Orlando, Florida

Health professionals are small business owners who need to apply their self-discipline tactics in establishing and operating successful practices. Talented trainees are leaving the medical profession because they fail to balance the cost of attendance against a realistic business and financial plan. Principles like budgeting, saving, and living below one’s means, in order to make future investments for future growth, asset protection, and retirement possible are often lacking. This textbook guides the medical professional in his/her financial planning life journey from start to finish. It ranks a place in all medical school libraries and on each of our bookshelves. ―Dr. Thomas M. DeLauro DPM, Professor and Chairman – Division of Medical Sciences, New York College of Podiatric Medicine

Physicians are notoriously excellent at diagnosing and treating medical conditions. However, they are also notoriously deficient in managing the business aspects of their medical practices. Most will earn $20-30 million in their medical lifetime, but few know how to create wealth for themselves and their families. This book will help fill the void in physicians’ financial education. I have two recommendations: 1) every physician, young and old, should read this book; and 2) read it a second time! ―Dr. Neil Baum MD, Clinical Associate Professor of Urology, Tulane Medical School, New Orleans, Louisiana

I worked with a Certified Medical Planner™ on several occasions in the past, and will do so again in the future. This book codified the vast body of knowledge that helped in all facets of my financial life and professional medical practice. ―Dr. James E. Williams DABPS, Foot and Ankle Surgeon, Conyers, Georgia

Almost everything you own and use for personal or investment purposes is a capital asset. Examples include a home, personal-use items like household furnishings, and stocks or bonds held as investments. When you sell a capital asset, the difference between the adjusted basis in the asset and the amount you realized from the sale is a capital gain or a capital loss.

Generally, an asset’s basis is its cost to the owner, but if you received the asset as a gift or inheritance, refer to Topic No. 703 for information about your basis.

For information on calculating adjusted basis, refer to Publication 551, Basis of Assets. You have a capital gain if you sell the asset for more than your adjusted basis. You have a capital loss if you sell the asset for less than your adjusted basis. Losses from the sale of personal-use property, such as your home or car, aren’t tax deductible.

Posted on October 22, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

By Morning Brew, NF and Staff Reporters

One of the world’s most prolificoffshore tax havens is locatedmore than 1,000 miles from any shore.

The US state of South Dakota now rivals notorious tax shelters like Panama, the Cayman Islands, and Switzerland as a destination for the top 0.01% to shield their wealth from the grubby hands of tax authorities, the newly released Pandora Papers show.

Quick recap: The Pandora Papers, published one week ago, represent one of the biggest leaks of financial docs in history. They show how celebrities, world leaders, and business magnates take advantage of opaque financial laws to hold onto as much of their wealth as they can…and, in some cases, get away with crimes.

And while none of that is particularly surprising, what is surprising is the changing geography of tax havens. The ultrarich are taking their money out of traditional tax shelters like the island of Jersey (one of the Channel Islands) and stashing it in rural US states like Nevada, Wyoming, and, most of all…South Dakota.

Of the more than 200 US trusts appearing in the Pandora Papers, 81 were located in South Dakota.

South Dakota’s trust industry held $367 billion in anonymous, untraceable assets in 2020, a nearly 4x increase from $75.5 billion in 2011. And these trusts aren’t catering to cattle ranchers who made it big—they’re linked to individuals in 40 different countries outside the US.

The bigger issue? 28 US-based trusts are linked to individuals or companies accused of misconduct overseas, such as money laundering, bribery, and human rights abuses, per the Washington Post.

***

And now the question you’ve all been waiting for…

Why South Dakota?

It’s not why most people arrive in South Dakota—by accident. For decades, the state has intentionally loosened regulations on its financial services sector to grow its economy and create finance jobs, particularly in the city of Sioux Falls.

This deregulation push, spurred by trust industry insiders, turned a South Dakotan trust into “the most potent force-field money can buy,” wrote the Guardian’s Oliver Bullough.

By setting up a trust in South Dakota…

Your assets are protected from claims by creditors, angry clients, or even your ex-spouse (a level of security not afforded by other tax havens).

You are not subject to income tax, inheritance tax, or capital gains tax in the state…because South Dakota has none of those.

You never actually have to go to South Dakota.

In sum, if you’re a shady billionaire or a corrupt president of a Latin American country with something to hide, South Dakota looks like a mighty attractive place to shield your fortune from governments.

Or, rather, the US more broadly is an attractive place to hide your wealth. After years of bashing “offshore” havens for sheltering tax avoiders, the US has moved up to second in the world rankings for financial secrecy.

Generally speaking, all income is taxable unless it’s specifically excluded, as is the case with certain gifts and inheritances. In most instances, the income you earn will be reported to both you and the government on an information return, such as a Form 1099 or W-2. If the income you report doesn’t match the IRS’s records, you could face problems down the road—so be sure you include the income from all of the following forms that are applicable to your situation:

1099-B: The form on which financial institutions report capital gains.

1099-DIV: The form on which financial institutions report dividends.

1099-MISC: The form used to report various types of income, such as royalties, rents, payments to independent contractors, and numerous other types of income.

1099-R:The form on which financial institutions report withdrawals from tax-advantaged retirement accounts.

Form 1099-INT: The form on which financial institutions report interest income.

Form SSA-1099:The form on which the Social Security Administration reports Social Security benefits (a portion of which may be taxable, depending on your level of income).

Form W-2:The form on which employers report total annual compensation, payroll taxes, contributions to retirement accounts, and other information.

If you receive an inaccurate statement of income, immediately contact the responsible party to request a corrected form and have them resend the documents to both you and the IRS as soon as possible to avoid delaying your tax return. Also, be aware that you must report income for which there is no form, such as renting out your vacation home.

When you sell an investment, you’ll need to know both the cost basis (what you paid for the investment) and the sale price to determine your net gain or loss. The cost basis of your investment may need to be adjusted to account for commissions, fees, stock splits, or other events, which could help reduce your taxable gain or increase your net loss.

Financial institutions are required to adjust your investments’ cost basis and provide that information on a Form 1099. However, brokerages aren’t required to report the cost basis for investments purchased prior to a certain date, which means you’ll be responsible for supplying that information (see the table below). Be sure to keep records of all investment purchases and sales—even those for which your brokerage is responsible.

Your reporting responsibility

Depending on security type and date of purchase, you—rather than your brokerage—could be responsible for reporting the cost basis of your investment to the IRS.

An August 2021 study published in the Journal of the American Medical Association (JAMA) analyzed medical and surgical episodes of care in U.S. hospitals to determine whether outcomes differed in hospitals that participated in Medicare’s Bundled Payments for Care Improvement (BPCI) Initiative depending on whether the patient being treated was attributed to a Medicare Shared Savings Program (MSSP) accountable care organization (ACO).

This Health Capital Topics article will discuss the study’s findings and potential policy implications.(Read more…)

In Response to a Question Regarding the Ending of Haven Healthcare–the Joint Venture Among Berkshire Hathaway, JP Morgan Chase and Amazon to Improve Healthcare for their Employee Health Plan Members–Warren Buffett Made the Following Statement:

“Healthcare is the Tapeworm of the US Economy and the TAPEWORM WON.”

Additionally, Warren Buffett Goes on to Say that ‘Prestigious‘ People in the Community Run Hospital Boards and These People Are ‘Fairly Happy‘ with the Healthcare System the Way It Currently Is.

It is Likely that Warren Buffett Formed Some of This Opinion in Speaking About Healthcare with the Vice Chairman of Berkshire Hathaway, Charlie Munger, and Berkshire Board Member and Famous CEO, Tom Murphy.

Charlie Munger Has Served on the Board of a Los Angeles Hospital for 31 Years and Tom Murphy Currently Serves on the NYU Langone Hospital System Board of Directors.

The Support of the Status Quo by ‘Prestigious,’ ‘Fairly Happy’ Hospital Board Members Cannot Be Understated… It Blocks Change and Warren Buffett Appears to Think Similarly.

Posted on October 5, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

FORPHYSICIAN INVESTORS

By David Belk MD

Health Insurance Company Financial Index

Below is a listing of the Nine largest for-profit health insurance Companies. The Annual financial statements are linked to the year for each Company and a four page summary report is linked to the name of the health insurance company at the top of the listing.

The relevant pages in each financial statement I used to prepare my summaries are listed next to each year’s statement. Aetna and Coventry’s summaries are combined because they merged in 2012. Health Net also Merged with Centene in 2016 leaving only seven major health insurance companies.

Posted on October 1, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

***

BY MORNING BREW

The Legend of the $1 Trillion Platinum Coin

****

***

You may have heard that a deadline to suspend the debt ceiling is rapidly approaching, and if lawmakers don’t do anything it could lead to “economic catastrophe,” in the words of Treasury Secretary Janet Yellen.

But what if we told you there was a solution to the debt ceiling fiasco so crazy…it just might work?

The solution: Yellen could have the Treasury mint a $1 trillion platinum coin, deposit it at the Fed to “retire” loads of US federal debt, and then enable the government to carry on with business as usual without having to worry about defaulting on its existing debt.

“The Secretary may mint and issue platinum bullion coins and proof platinum coins in accordance with such specifications, designs, varieties, quantities, denominations, and inscriptions as the Secretary, in the Secretary’s discretion, may prescribe from time to time.”

The law is crystal clear, and has been deemed kosher by numerous academics. “The statute clearly does authorize the issuance of trillion-dollar coins,” Laurence Tribe, a Harvard Law professor, told Washington Monthly back in 2013.

In fact, nothing says we have to stop at $1 trillion. Yellen could go big with a $10 trillion coin, hypothetically. As Bloomberg’s Joe Weisenthal explains, none of this would lead to inflation because it’s merely an “accounting trick”—not an influx of money into the economy.

Have we tried this before? The $1 trillion platinum coin idea seems to pop up every time the US faces a debt ceiling crunch. It was first introduced by a Georgia lawyer in 2010 and gained traction during the debt-ceiling crisis of 2011.

Things really turned up in 2013, when the government was…you guessed it, facing another debt ceiling deadline. The hashtag #MintTheCoin became popular on Twitter, and economists like Paul Krugman advocated for unleashing the coin. “If we have a crisis over the debt ceiling, it will be only because the Treasury Department would rather see economic devastation than look silly for a couple of minutes,” he wrote.

But each time the $1 trillion coin is mentioned as a way of resolving debt ceiling problems, the people in charge dismiss it as a distraction from Congress doing its job. “Neither the Treasury nor the Federal Reserve believes that the law can or should be used to produce platinum coins for the purpose of avoiding an increase in the debt limit,” The Treasury wrote during…well, yes, another debt ceiling emergency in 2015.

As for our current predicament, the Biden administration rejected the minting of the $1 trillion coin yet again last week.

Bottom line: Perhaps some enterprising future Treasury Secretary will manifest the platinum coin into existence, but for now it remains as mythical as Camelot.

A decentralized autonomous organization (DAO), sometimes called a decentralized autonomous corporation (DAC), is an organization represented by rules encoded as a computer program that is transparent, controlled by the organization members and not influenced by a central government. A DAO’s financial transaction record and program rules are maintained on a blockchain. The precise legal status of this type of business organization is unclear.

A well-known example, intended for venture capital funding, was The DAO, which launched with $150 million in crowdfunding in June 2016, and was nearly immediately hacked and drained of US$50 million in cryptocurrency. The hack was reversed in the following weeks, and the money restored, via a hard fork of the Ethereum blockchain: the Ethereum miners and clients switched to the new fork.

:max_bytes(150000):strip_icc()/inflation_FINAL-5c8975c946e0fb0001a0bf75.png)

![DR. DAVID EDWARD MARCINKO FACFAS MBA CFP MBBS [Hon] [Executive Summary] - PDF Free Download](https://educationdocbox.com/docs-images/75/71938560/images/8-1.jpg)