BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The theory emerged during a period when stock trading was dominated by institutions and wealthy individuals. Small investors, who could not afford 100‑share blocks, often purchased odd lots. Analysts observed that these traders tended to enter the market after prices had already risen significantly and to sell only after declines had already occurred. The odd‑lot theory formalized this observation into a broader claim: odd‑lot investors consistently act on emotion rather than analysis, making them a useful signal of crowd psychology.

Two assumptions sit at the heart of the theory:

Odd‑lot traders are generally uninformed. They are presumed to lack access to research, professional advice, or disciplined strategies.

Their behavior is reactive rather than predictive. They buy after feeling confident and sell after feeling fearful, which often means they are late to major turning points.

From these assumptions, analysts concluded that odd‑lot buying was a bearish sign and odd‑lot selling was bullish.

How the theory was used

Market services once tracked odd‑lot purchases and sales, publishing weekly statistics. Analysts interpreted these numbers in several ways:

Odd‑lot buying as a sell signal. If small investors were aggressively buying, it suggested optimism had peaked.

Odd‑lot selling as a buy signal. Heavy selling implied capitulation, a point at which fear had driven out the last hesitant holders.

Odd‑lot short selling as a bullish sign. Because odd‑lot traders were thought to be poor market timers, their attempts to short the market were interpreted as a sign that prices were likely to rise.

These interpretations were not mechanical rules but sentiment cues. The theory functioned similarly to modern contrarian indicators such as surveys of investor confidence or measures of retail trading activity.

Why the theory gained traction

The odd‑lot theory resonated for several reasons. First, it aligned with the broader belief that markets are driven by cycles of fear and greed. Small investors, lacking experience, were seen as especially vulnerable to these emotional swings. Second, the theory offered a simple, intuitive tool for identifying market extremes. In an era before sophisticated data analytics, any observable pattern in investor behavior was valuable. Finally, the theory fit the narrative that professional investors were more rational and disciplined, reinforcing the idea that the “smart money” moved opposite the crowd.

Limitations and criticisms

Despite its historical appeal, the odd‑lot theory has significant weaknesses.

Its assumptions about small investors are overly broad. Not all odd‑lot traders were uninformed; many simply lacked the capital to buy round lots.

Market structure has changed dramatically. Fractional shares, online brokerages, and algorithmic trading have blurred the distinction between small and large investors.

Retail investors today are more diverse. Some are inexperienced, but others are highly sophisticated, using advanced tools and strategies.

Empirical support is inconsistent. Studies over time have shown mixed results, with odd‑lot activity not reliably predicting market turning points.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Speed, Strategy and the Structure of Modern Stock Markets

High‑frequency trading (HFT) has become one of the most influential and controversial forces in modern financial markets. Built on the premise that speed itself can be a competitive advantage, HFT uses advanced algorithms, powerful computing infrastructure, and ultra‑fast data connections to execute trades in fractions of a second. While the practice has reshaped market structure and liquidity, it has also raised questions about fairness, stability, and the role of technology in finance. Understanding HFT requires examining not only how it works, but also why it emerged, what benefits it provides, and what risks it introduces.

At its core, high‑frequency trading is a subset of algorithmic trading distinguished by its extreme speed and high turnover. Firms engaged in HFT rely on sophisticated models that scan markets for tiny, fleeting price discrepancies. These opportunities might exist for only microseconds, far too short for human traders to exploit. To capture them, HFT firms invest heavily in technology: colocated servers placed physically close to exchange data centers, microwave transmission networks that shave milliseconds off communication times, and custom hardware designed to process market data at extraordinary speeds. In this environment, competitive advantage is measured not in minutes or even seconds, but in microseconds and nanoseconds.

The rise of HFT is closely tied to the evolution of market structure. As exchanges shifted from floor‑based trading to electronic platforms, barriers to rapid execution fell dramatically. Decimalization of stock prices increased the granularity of quotes, creating more opportunities for small price movements. Regulation that encouraged competition among trading venues also fragmented markets, allowing HFT firms to profit from price differences across exchanges. In many ways, HFT is a natural outcome of a system that rewards speed, efficiency, and the ability to process vast amounts of information instantly.

Proponents of high‑frequency trading argue that it provides several important benefits. One of the most frequently cited is improved liquidity. Because HFT firms often act as market makers—posting bids and offers and profiting from the spread—they can narrow the gap between buy and sell prices. This reduces transaction costs for all market participants. Additionally, the constant activity of HFT firms can make markets more efficient by quickly incorporating new information into prices. When an HFT algorithm detects a price discrepancy between two related assets, its rapid trades help bring those prices back into alignment. In theory, this contributes to more accurate valuations and smoother market functioning.

However, the benefits of HFT are accompanied by significant concerns. One of the most persistent criticisms is that HFT creates an uneven playing field. Firms with the resources to invest in cutting‑edge technology gain access to opportunities unavailable to slower participants. While markets have always rewarded those with better information or faster execution, the scale of advantage in HFT—measured in millionths of a second—raises questions about fairness and accessibility. Critics argue that markets should not be won simply by those who can afford the fastest cables or the most advanced servers.

***

***

Another concern is the potential for HFT to contribute to market instability. Because algorithms react to market conditions automatically and at high speed, they can amplify volatility during periods of stress. The most famous example is the 2010 “Flash Crash,” during which U.S. equity markets plunged and recovered within minutes. Although HFT was not the sole cause, its rapid withdrawal of liquidity played a role in the severity of the event. Similar, smaller disruptions have occurred since, highlighting the fragility that can arise when automated systems interact in unpredictable ways.

Moreover, some HFT strategies raise ethical and regulatory questions. Practices such as latency arbitrage—profiting from tiny delays in how information reaches different market participants—may technically comply with rules but still feel exploitative. Other strategies, like quote stuffing or spoofing, involve flooding markets with orders to confuse competitors or manipulate prices. While regulators have taken steps to curb abusive behavior, the complexity and opacity of HFT make oversight challenging.

Despite these concerns, high‑frequency trading is unlikely to disappear. It has become deeply embedded in the infrastructure of modern markets, and many of its functions—such as providing liquidity—are now essential. The challenge for regulators and market designers is to preserve the benefits of HFT while mitigating its risks. This may involve refining rules around market access, improving transparency, or designing trading systems that reduce the advantage of raw speed. Some exchanges have experimented with “speed bumps,” intentional delays that level the playing field by preventing any participant from acting too quickly. Others have explored batch auctions that execute trades at discrete intervals rather than continuously.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

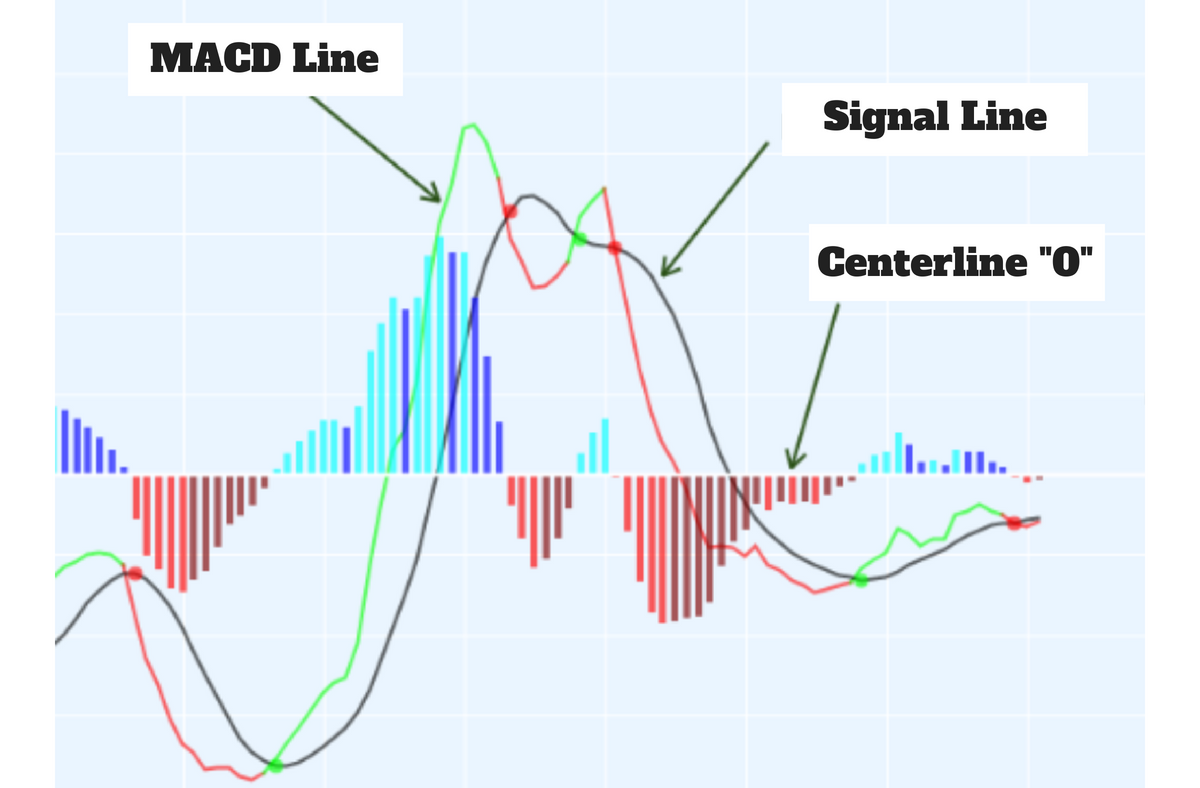

Example of historical stock price data (top half) with the typical presentation of a MACD(12,26,9) indicator (bottom half). The blue line is the MACD series proper, the difference between the 12-day and 26-day EMAs of the price. The red line is the average or signal series, a 9-day EMA of the MACD series. The bar graph shows the divergence series, the difference of those two lines.

***

MACD, short for moving average convergence/divergence, is a trading indicator used in technical analysis of securities prices, created by Gerald Appel in the late 1970s. It is designed to reveal changes in the strength, direction, momentum, and duration of a trend in a stock’s price.

The MACD indicator (or “oscillator”) is a collection of three time series calculated from historical price data, most often the closing price. These three series are: the MACD series proper, the “signal” or “average” series, and the “divergence” series which is the difference between the two. The MACD series is the difference between a “fast” (short period) exponential moving average (EMA), and a “slow” (longer period) EMA of the price series. The average series is an EMA of the MACD series itself.

The MACD indicator thus depends on three time parameters, namely the time constants of the three EMAs. The notation “MACD(a,b,c)” usually denotes the indicator where the MACD series is the difference of EMAs with characteristic times a and b, and the average series is an EMA of the MACD series with characteristic time c. These parameters are usually measured in days. The most commonly used values are 12, 26, and 9 days, that is, MACD (12,26,9). As true with most of the technical indicators, MACD also finds its period settings from the old days when technical analysis used to be mainly based on the daily charts. The reason was the lack of the modern trading platforms which show the changing prices every moment. As the working week used to be 6-days, the period settings of (12, 26, 9) represent 2 weeks, 1 month and one and a half week. Now when the trading weeks have only 5 days, possibilities of changing the period settings cannot be overruled. However, it is always better to stick to the period settings which are used by the majority of traders as the buying and selling decisions based on the standard settings further push the prices in that direction.

Although the MACD and average series are discrete values in nature, but they are customarily displayed as continuous lines in a plot whose horizontal axis is time, whereas the divergence is shown as a bar chart (often called a histogram).

***

MACD indicator showing vertical lines (histogram)

A fast EMA responds more quickly than a slow EMA to recent changes in a stock’s price. By comparing EMAs of different periods, the MACD series can indicate changes in the trend of a stock. It is claimed that the divergence series can reveal subtle shifts in the stock’s trend.

Since the MACD is based on moving averages, it is a lagging indicator. As a future metric of price trends, the MACD is less useful for stocks that are not trending (trading in a range) or are trading with unpredictable price action. Hence the trends will already be completed or almost done by the time MACD shows the trend.

The Firm Foundation Theory of investing is one of the most influential approaches to stock valuation. It rests on the belief that every financial asset possesses an intrinsic value that can be objectively determined through careful analysis of its fundamentals. This theory contrasts sharply with more speculative approaches, such as the “Castle-in-the-Air” theory, which emphasizes crowd psychology and market sentiment.

At its core, the Firm Foundation Theory was popularized by economist John Burr Williams in his 1938 book The Theory of Investment Value. Williams argued that the intrinsic value of a stock is equal to the present value of all future dividends the company is expected to pay. In other words, the worth of a stock is not determined by short-term price movements or investor enthusiasm, but by the long-term cash flows it generates. This principle has become a cornerstone of fundamental analysis, influencing investors such as Warren Buffett, who is often cited as a practitioner of this approach.

The theory assumes that while market prices may fluctuate due to speculation, fear, or irrational exuberance, they will eventually regress toward intrinsic value. This creates opportunities for disciplined investors: when a stock trades below its intrinsic value, it represents a buying opportunity; when it trades above, it may be time to sell. Thus, the Firm Foundation Theory provides a rational framework for identifying mispriced securities and making long-term investment decisions.

***

***

One of the strengths of this theory is its emphasis on objective analysis. By focusing on dividends, earnings, and growth potential, it encourages investors to ground their decisions in measurable financial data rather than emotional impulses. This approach aligns with the broader philosophy of value investing, which seeks to purchase securities at a discount to their true worth. It also offers a counterbalance to speculative bubbles, reminding investors that prices untethered from fundamentals are unsustainable in the long run.

However, the Firm Foundation Theory is not without challenges. Forecasting future dividends and earnings is inherently uncertain. Companies may change their payout policies, face unexpected competition, or encounter macroeconomic shocks that alter their growth trajectory. Additionally, the theory assumes that markets will eventually correct mispricings, but in reality, irrational exuberance or pessimism can persist for extended periods. Critics argue that this makes the theory more idealistic than practical in certain contexts.

Despite these limitations, the Firm Foundation Theory remains a vital tool in the investor’s toolkit. It underpins many valuation models used today, including discounted cash flow (DCF) analysis, which extends Williams’s dividend-based approach to include broader measures of cash generation. By insisting that stocks have a calculable intrinsic value, the theory provides a disciplined lens through which investors can evaluate opportunities and avoid being swayed by market noise.

In conclusion, the Firm Foundation Theory offers a rational, fundamentals-driven perspective on investing. While it requires careful forecasting and is vulnerable to uncertainty, its emphasis on intrinsic value continues to guide prudent investors. By reminding us that stocks are ultimately worth the cash they return to shareholders, the theory stands as a bulwark against speculation and a foundation for long-term wealth building.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

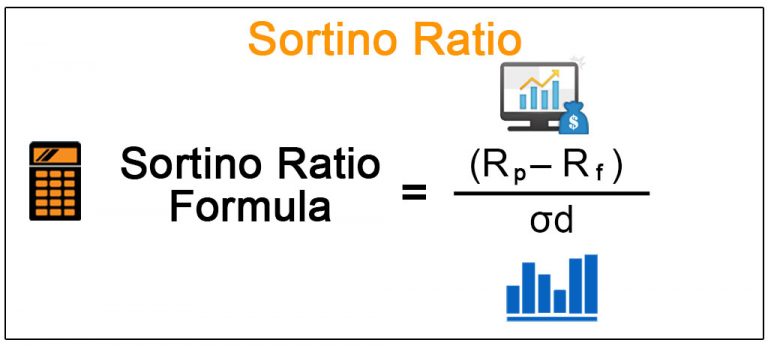

In the field of investment analysis, one of the most important challenges is balancing risk and reward. Investors want to maximize returns, but they also want to minimize the chances of losing money. Traditional measures such as the Sharpe Ratio have long been used to evaluate risk‑adjusted performance, but they treat all volatility the same. This means that both upward and downward swings in returns are penalized equally, even though investors generally welcome upside volatility. To address this limitation, the Sortino Ratio was developed as a more refined tool that focuses specifically on downside risk.

Definition and Formula

The Sortino Ratio measures the excess return of an investment relative to the risk‑free rate, divided by the standard deviation of negative returns. In formula form:

σd\sigma_d = standard deviation of downside returns

This formula highlights the unique feature of the Sortino Ratio: it only considers harmful volatility, ignoring fluctuations that exceed expectations.

Why It Matters

The key advantage of the Sortino Ratio is its ability to separate “good” volatility from “bad” volatility. Upside volatility, which represents returns above the target or minimum acceptable rate, is not penalized. Downside volatility, which represents returns below expectations, is penalized heavily. This distinction makes the Sortino Ratio especially useful for investors who prioritize capital preservation. For example, retirees or individuals saving for short‑term goals may prefer investments with higher Sortino Ratios because they indicate stronger protection against losses.

Practical Applications

The Sortino Ratio has several practical uses:

Portfolio Evaluation: Investors can compare funds or strategies using the Sortino Ratio. A higher ratio suggests better risk‑adjusted performance.

Risk Management: By focusing on downside deviation, managers can identify investments that minimize losses during downturns.

Goal‑Oriented Investing: For individuals with specific financial targets, the Sortino Ratio helps ensure that chosen investments align with their tolerance for risk.

For instance, a mutual fund with a Sortino Ratio of 2 is generally considered strong, meaning it generates twice the return per unit of downside risk.

Comparison with the Sharpe Ratio

While both the Sharpe and Sortino Ratios measure risk‑adjusted returns, they differ in how they treat volatility. The Sharpe Ratio penalizes all fluctuations, whether positive or negative. The Sortino Ratio, however, only penalizes harmful volatility. This makes the Sortino Ratio more investor‑friendly, especially for those who care more about avoiding losses than capturing every possible gain. In practice, the Sharpe Ratio is better for broad comparisons across asset classes, while the Sortino Ratio is better for evaluating downside protection in portfolios.

Limitations

Despite its strengths, the Sortino Ratio is not without limitations:

Data Sensitivity: It requires accurate downside deviation data, which can be difficult to calculate.

Threshold Choice: Results vary depending on the minimum acceptable return chosen.

Context Dependence: It should be used alongside other metrics, such as the Sharpe or Treynor Ratios, for a complete picture of risk and return.

Conclusion

The Sortino Ratio is a powerful tool for investors who want to measure performance while minimizing exposure to harmful volatility. By focusing exclusively on downside risk, it provides a more realistic assessment of whether returns justify the risks taken. While not perfect, it complements other risk‑adjusted metrics and is especially valuable for investors with low tolerance for losses. In today’s uncertain markets, understanding and applying the Sortino Ratio can help investors make smarter, more resilient decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BASIC DEFINITIONS

By Dr. David Edward Marcinko MBA MEd

***

***

A financial warrant is similar to an option, but it is typically issued directly by a company rather than traded on an exchange. Warrants allow holders to purchase shares of the issuing company at a fixed price, known as the exercise price, within a specified time frame. Unlike options, which are standardized and traded on secondary markets, warrants are often attached to bonds or preferred stock as a “sweetener” to make those securities more attractive to investors.

🔑 Key Features of Warrants

Right, not obligation: Investors can choose whether to exercise the warrant depending on market conditions.

Longer maturity: Warrants often have longer lifespans than options, sometimes lasting several years.

Issued by companies: They are a direct financing tool, unlike exchange-traded options.

Dilution effect: When exercised, new shares are created, which can dilute existing shareholders’ equity.

📊 Types of Warrants

Equity warrants: Allow purchase of common stock at a set price.

Bond warrants: Sometimes attached to debt instruments, giving bondholders the right to buy equity.

Detachable vs. non-detachable: Detachable warrants can be traded separately from the bond or preferred share they were issued with, while non-detachable ones remain tied.

Exotic warrants: Some markets offer specialized versions, such as knock-out warrants or mini-futures, which add complexity and leverage.

💼 Uses in Corporate Finance

Companies issue warrants for several reasons:

Capital raising: Warrants encourage investors to buy bonds or preferred shares, providing immediate funding.

Employee incentives: Similar to stock options, warrants can reward employees with potential future equity.

Strategic deals: Warrants may be used in mergers or acquisitions to align interests between parties.

⚖️ Benefits and Risks

Benefits:

Provide leverage, allowing investors to control more shares with less capital.

Offer long-term exposure to a company’s growth potential.

Can enhance returns if the underlying stock price rises above the exercise price.

Risks:

Warrants may expire worthless if the stock price never exceeds the exercise price.

Dilution reduces the value of existing shares when warrants are exercised.

Higher volatility compared to traditional equity investments.

📌 Conclusion

Financial warrants occupy a unique space between corporate finance and speculative investing. They serve as capital-raising tools for companies and leveraged opportunities for investors, but they also carry risks of dilution and expiration without value. Understanding their mechanics, types, and strategic uses is essential for anyone navigating modern financial markets.

In essence, warrants are a bridge between debt and equity, offering flexibility to issuers and optionality to investors. Their role in corporate finance highlights the innovative ways companies structure securities to balance risk, reward, and capital needs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

Money supply measures—M0, M1, M2, and M3—are essential tools used by economists and policymakers to assess liquidity, guide monetary policy, and understand economic health. Each measure reflects a different level of liquidity and plays a unique role in financial analysis.

The money supply refers to the total amount of monetary assets available in an economy at a specific time. It includes various forms of money, ranging from physical currency to more liquid financial instruments. To better understand and manage economic activity, central banks and economists categorize money into different measures based on liquidity: M0, M1, M2, and M3.

M0, also known as the monetary base or base money, includes all physical currency in circulation—coins and paper money—plus reserves held by commercial banks at the central bank. It represents the most liquid form of money and is directly controlled by the central bank through tools like open market operations and reserve requirements.

M1 builds on M0 by adding demand deposits (checking accounts) and other liquid deposits that can be quickly converted into cash. It includes:

Physical currency held by the public

Traveler’s checks

Demand deposits at commercial banks

M1 is a key indicator of immediate spending power in the economy. A rapid increase in M1 can signal rising consumer activity, while a decline may indicate tightening liquidity.

M2 expands further by including near-money assets—those that are not as liquid as M1 but can be converted into cash relatively easily. M2 includes:

All components of M1

Savings deposits

Money market securities

Certificates of deposit (under $100,000)

M2 is widely used by economists and the Federal Reserve to gauge intermediate-term economic trends. It reflects both spending and saving behavior, making it a critical tool for forecasting inflation and guiding interest rate decisions.

M3, though no longer published by the Federal Reserve since 2006, includes M2 plus large time deposits, institutional money market funds, and other larger liquid assets. M3 provides a broader view of the money supply, especially useful for analyzing long-term investment trends and credit expansion. Some countries, like the UK and India, still track M3 for macroeconomic planning.

These measures are not just academic—they have real-world implications. For instance, during the COVID-19 pandemic, the U.S. saw a historic surge in M2 due to stimulus payments and quantitative easing. This expansion raised concerns about future inflation, which materialized in subsequent years. Monitoring money supply helps central banks adjust monetary policy to maintain price stability and support economic growth.

In conclusion, money supply measures offer a layered view of liquidity in the economy, from the most liquid (M0) to broader aggregates (M3).

Understanding these categories helps policymakers, investors, and businesses anticipate economic shifts, manage inflation, and make informed financial decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Risk arbitrage, often referred to as merger arbitrage, is a specialized investment strategy that seeks to exploit pricing inefficiencies arising during corporate mergers, acquisitions, or other restructuring events. Unlike traditional arbitrage, which involves risk-free profit opportunities from price discrepancies across markets, risk arbitrage carries inherent uncertainty because it depends on the successful completion of corporate transactions. Despite its name, it is not risk-free; rather, it is a calculated approach to profiting from the probability of deal closure.

At its core, risk arbitrage involves buying the stock of a company being acquired and, in some cases, shorting the stock of the acquiring company. For example, if Company A announces it will acquire Company B at $50 per share, but Company B’s stock trades at $47, arbitrageurs may purchase shares of Company B, betting that the deal will close and the stock will rise to the agreed acquisition price. The $3 difference represents the potential arbitrage profit. However, this spread exists precisely because of uncertainty: regulatory approval, financing challenges, shareholder resistance, or unforeseen market conditions could derail the transaction, leaving arbitrageurs exposed to losses.

The practice of risk arbitrage has a long history in Wall Street. It gained prominence in the mid-20th century, particularly during the wave of conglomerate mergers in the 1960s and leveraged buyouts in the 1980s. Hedge funds and specialized arbitrage desks at investment banks became key players, using sophisticated models to assess the likelihood of deal completion. Today, risk arbitrage remains a central strategy for event-driven funds, which focus on corporate actions as catalysts for investment opportunities.

One of the defining features of risk arbitrage is its reliance on probability analysis. Investors must evaluate not only the financial terms of the deal but also the legal, regulatory, and political environment. For instance, antitrust regulators may block a merger if it reduces competition, or foreign investment committees may intervene in cross-border acquisitions. Arbitrageurs often assign probabilities to deal completion and calculate expected returns accordingly. A deal with high regulatory risk may offer a wider spread, but the probability of failure tempers the attractiveness of the trade.

Risk arbitrage also plays an important role in market efficiency. By narrowing the spread between target company stock prices and acquisition offers, arbitrageurs help align market prices with expected outcomes. Their activity provides liquidity to shareholders of target firms and signals market confidence—or skepticism—about deal success. In this sense, arbitrageurs act as informal referees of corporate transactions, reflecting collective judgment about feasibility.

Nevertheless, risk arbitrage is not without controversy. Critics argue that it can encourage speculative behavior and amplify volatility around merger announcements. Moreover, when deals collapse, arbitrageurs can suffer significant losses, as seen in high-profile failed mergers. The strategy requires not only financial acumen but also resilience in managing downside risk.

In conclusion, risk arbitrage is a sophisticated investment strategy that blends financial analysis with legal and regulatory insight. While it offers opportunities for profit, it demands careful risk management and a deep understanding of corporate dynamics. Far from being risk-free, it is a calculated gamble on the successful execution of complex transactions. For investors willing to navigate uncertainty, risk arbitrage remains a compelling, though challenging, avenue in modern financial markets.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

A Special Purpose Acquisition Company (SPAC) is a corporate entity created solely to raise capital through an initial public offering (IPO) with the intention of merging with or acquiring an existing private company. Unlike traditional firms, SPACs have no commercial operations at the time of their IPO. They exist as shell companies, holding investor funds in trust until a suitable target is identified. This unique structure has earned them the nickname “blank check companies.”

How SPACs Work

The lifecycle of a SPAC typically unfolds in three stages:

Formation and IPO: Sponsors—often experienced investors or industry executives—form the SPAC and take it public, raising funds from investors.

Target Search: The SPAC has a limited time frame, usually 18–24 months, to identify and negotiate with a private company to merge with.

De-SPAC Transaction: Once a merger is completed, the private company effectively becomes public, bypassing the traditional IPO process.

This process allows private firms to access public markets more quickly and with fewer regulatory hurdles compared to conventional IPOs.

Advantages of SPACs

SPACs gained traction because they offered several benefits:

Speed and Certainty: Traditional IPOs can be lengthy and uncertain, while SPACs provide a faster route to public markets.

Flexibility in Valuation: Unlike IPOs, SPACs can negotiate valuations directly with target companies.

Access to Expertise: Sponsors often bring industry knowledge and networks that can help the acquired company grow.

Investor Opportunity: Investors can participate early, with the option to redeem shares if they dislike the proposed merger.

Risks and Criticisms

Despite their appeal, SPACs are not without controversy:

Sponsor Incentives: Sponsors typically receive a significant stake (often 20%) at a low cost, which can misalign their interests with ordinary investors.

Uncertain Targets: Investors commit funds without knowing which company will be acquired, creating risk.

Performance Concerns: Studies show that many SPACs underperform after completing mergers, with share prices often declining.

Regulatory Scrutiny: Authorities have warned investors to carefully evaluate SPACs, especially regarding projections of future performance, which are less restricted than in IPOs.

Historical Context and Trends

SPACs first appeared in the 1990s but remained niche until the early 2020s, when they experienced a boom. In 2020 and 2021, hundreds of SPAC IPOs raised billions of dollars, fueled by market liquidity and investor enthusiasm. High-profile deals, such as DraftKings and Virgin Galactic, brought attention to the model. However, by the mid-2020s, enthusiasm cooled due to poor post-merger performance and tighter regulations.

Conclusion

SPACs represent a fascinating innovation in financial markets, offering an alternative to traditional IPOs. Their advantages in speed, flexibility, and access to capital made them attractive during periods of market optimism. Yet, their risks—misaligned incentives, uncertain outcomes, and regulatory challenges—have tempered investor enthusiasm. While SPACs are unlikely to disappear entirely, their future will depend on whether they can evolve into a more transparent and sustainable mechanism for taking companies public.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

+ Plus / – Minus Two Weeks

Stock market crashes have long been associated with the fall season, particularly October, which has earned a reputation as a month of financial turmoil. While crashes can occur at any time, the clustering of several historic downturns in autumn has led many investors to believe that markets are more vulnerable during this period.

Historical Patterns of Fall Crashes

Some of the most devastating collapses in financial history have taken place in the fall. The Wall Street Crash of 1929 began in late October and marked the start of the Great Depression. In October 1987, markets experienced “Black Monday,” when the Dow Jones Industrial Average plunged more than 20% in a single day. More recently, the global financial crisis of 2008 saw some of its steepest declines in September and October. These events have cemented autumn’s reputation as a season of heightened risk.

Why the Fall Is Riskier

Several factors contribute to the perception that fall is a dangerous time for markets:

Investor psychology: The memory of past crashes in October can heighten anxiety, making traders more prone to panic selling.

Fiscal cycles: Many institutional investors close their books at the end of September, leading to portfolio adjustments and sell-offs in October.

Economic data releases: Key reports on employment, corporate earnings, and government budgets often arrive in the fall, influencing sentiment.

Global events: Political and economic developments frequently coincide with autumn months, adding uncertainty.

Statistical Evidence and Skepticism

Despite the historical examples, statistical studies suggest that crashes are not inherently more likely in October than in other months. Market downturns are rare events, and their clustering in autumn may be more coincidence than causation. Crashes have also occurred outside the fall, such as the bursting of the dot-com bubble in spring 2000 and the COVID-19 crash in March 2020. This suggests that the so-called “October Effect” may be more psychological than empirical.

Lessons for Investors

Whether or not fall crashes are statistically more likely, the historical record offers important lessons:

Diversify investments to reduce vulnerability to sudden downturns.

Avoid panic selling, since many crashes are followed by rapid recoveries.

Prepare for volatility, as autumn often brings heightened uncertainty.

Conclusion

Stock market crashes are not guaranteed to happen in the fall, but history has made October synonymous with financial turmoil. The clustering of major downturns during this season has created a psychological bias that influences investor behavior. Whether coincidence or pattern, the lesson is clear: autumn is a time when vigilance, discipline, and preparation are especially important for market participants.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

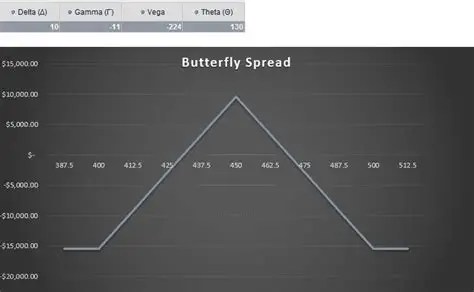

Investing in Butterfly Spreads

Options trading provides investors with a wide range of strategies to suit different market conditions. One of the more refined approaches is the butterfly spread, a strategy designed to profit from stability in the price of an underlying asset. It combines multiple option contracts at different strike prices to create a position with limited risk and limited reward. The name comes from the shape of its profit-and-loss diagram, which resembles the wings of a butterfly.

Structure of the Strategy

A typical butterfly spread involves four options contracts with three strike prices. In a long call butterfly spread, the investor buys one call at a lower strike, sells two calls at a middle strike, and buys one call at a higher strike. This creates a payoff that peaks if the underlying asset closes at the middle strike price. Losses are capped at the initial premium paid, while profits are capped at the difference between the strikes minus the premium.

Variations of Butterfly Spreads

Butterfly spreads can be built with calls, puts, or a mix of both:

Long Call Butterfly: Profits if the asset stays near the middle strike.

Long Put Butterfly: Similar structure but using puts.

Iron Butterfly: Combines calls and puts, selling an at-the-money straddle and buying protective wings.

Reverse Iron Butterfly: Designed to benefit from sharp price movements and volatility.

Each variation adapts to different market expectations, but all share the principle of balancing risk and reward.

Benefits of Butterfly Spreads

Defined Risk: The maximum loss is known upfront.

Cost Efficiency: Requires less capital than outright buying options.

Neutral Outlook: Works best when the investor expects little price movement.

Flexibility: Can be tailored to different market conditions with calls, puts, or combinations.

Drawbacks and Risks

Limited Profit Potential: Gains are capped, which may not appeal to aggressive traders.

Dependence on Timing: The strategy works only if the asset closes near the middle strike at expiration.

Complexity: Requires careful planning of strike prices and expiration dates.

Example in Practice

Suppose a stock trades at $100, and the investor expects it to remain near that level. They could set up a butterfly spread with strikes at $95, $100, and $105. If the stock closes at $100, the strategy delivers maximum profit. If the stock moves significantly away from $100, the investor’s loss is limited to the premium paid. This makes the butterfly spread particularly useful in calm, low-volatility markets.

Conclusion

The butterfly spread is a disciplined options strategy that thrives in stable markets. It offers a balance between risk control and profit potential, making it attractive to traders who prefer structured outcomes. While the rewards are capped, the defined risk and cost efficiency make butterfly spreads a valuable tool for investors who anticipate minimal price movement and want to manage their exposure carefully.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

American Depository Receipts Defined

In the modern era of globalization, financial instruments that connect investors across borders have become indispensable. Among these, American Depository Receipts (ADRs) stand out as a powerful mechanism that allows U.S. investors to participate in foreign equity markets without the complexities of international trading. ADRs not only simplify access to global companies but also enhance the ability of foreign corporations to raise capital in the United States. This essay explores the origins, structure, regulatory frameworks, benefits, risks, and real-world examples of ADRs, highlighting their role in the integration of global finance.

Historical Development

The concept of ADRs emerged in 1927 when J.P. Morgan introduced the first ADR for the British retailer Selfridges. At the time, American investors faced significant hurdles in purchasing foreign shares, including currency conversion, unfamiliar trading practices, and regulatory differences. ADRs solved these problems by creating a U.S.-based certificate that represented ownership in foreign shares, denominated in dollars, and traded on American exchanges.

Over the decades, ADRs expanded rapidly, especially during the post-World War II era when globalization accelerated. By the late 20th century, ADRs had become a mainstream tool for accessing international equities, with companies from Europe, Asia, and Latin America increasingly using them to tap into U.S. capital markets.

Structure and Mechanics

An ADR is issued by a U.S. depositary bank, which holds the underlying shares of a foreign company in custody. Each ADR corresponds to a specific number of shares—sometimes one, sometimes multiple, or even a fraction. Investors buy and sell ADRs in U.S. dollars, and dividends are paid in dollars as well, eliminating the need for currency conversion.

Key structural features include:

Depositary Banks: Institutions such as J.P. Morgan, Citibank, and Bank of New York Mellon act as custodians and issuers of ADRs.

ADR Ratios: The number of foreign shares represented by one ADR can vary, allowing flexibility in pricing.

Trading Platforms: ADRs can be listed on major exchanges like the NYSE or NASDAQ, or traded over-the-counter.

Regulatory Framework

ADRs are subject to U.S. securities regulations, which vary depending on the level of ADR issued:

Level I ADRs: Traded over-the-counter, requiring minimal disclosure. They are primarily used for visibility rather than fundraising.

Level II ADRs: Listed on U.S. exchanges, requiring compliance with SEC reporting standards, including reconciliation of financial statements to U.S. GAAP or IFRS.

Level III ADRs: Allow foreign companies to raise capital directly in U.S. markets through public offerings. These require the highest level of regulatory compliance, including registration with the SEC and adherence to corporate governance standards.

This tiered system ensures that investors receive appropriate levels of transparency while giving foreign companies flexibility in their approach to U.S. markets.

Benefits for Investors

ADRs offer numerous advantages to American investors:

Convenience: Investors can buy shares in foreign companies without dealing with foreign exchanges or currencies.

Diversification: ADRs provide access to global firms across industries, enhancing portfolio diversification.

Transparency: ADRs listed on U.S. exchanges must comply with SEC regulations, ensuring reliable financial reporting.

Liquidity: ADRs trade on familiar platforms, making them easily accessible to retail and institutional investors alike.

Benefits for Companies

Foreign corporations also benefit significantly from ADRs:

Access to Capital: ADRs open the door to the world’s largest pool of investors.

Global Visibility: Listing in the U.S. enhances reputation and credibility.

Improved Liquidity: Shares become more widely traded, increasing market efficiency.

Investor Base Diversification: Companies can attract both domestic and international investors, reducing reliance on local markets.

Risks and Challenges

Despite their advantages, ADRs carry certain risks:

Currency Risk: ADR values are tied to foreign shares denominated in local currencies, making them vulnerable to exchange rate fluctuations.

Political and Economic Risk: Instability in the issuing company’s home country can affect performance.

Taxation: Dividends may be subject to foreign withholding taxes before conversion to U.S. dollars.

Regulatory Differences: Even with SEC oversight, differences in accounting standards and corporate governance can pose challenges.

Case Studies

1. Alibaba Group (China) Alibaba’s ADRs, listed on the NYSE in 2014, marked one of the largest IPOs in history, raising $25 billion. This demonstrated the power of ADRs to connect Chinese companies with American investors, despite regulatory complexities between the two countries.

2. Toyota Motor Corporation (Japan) Toyota’s ADRs have long provided U.S. investors with access to one of the world’s largest automakers. By listing ADRs, Toyota expanded its investor base and strengthened its global presence.

3. Royal Dutch Shell (Netherlands/UK) Shell’s ADRs illustrate how multinational corporations use ADRs to maintain visibility in U.S. markets while managing complex cross-border structures.

The Role of ADRs in Global Finance

ADRs embody the globalization of capital markets. They facilitate cross-border investment, enhance market efficiency, and foster economic integration. For investors, ADRs represent a gateway to international diversification. For companies, they provide access to the deepest capital markets in the world.

Conclusion

American Depositary Receipts are more than just financial instruments; they are symbols of global interconnectedness. By bridging the gap between U.S. investors and foreign companies, ADRs have reshaped the landscape of international finance. They balance convenience with exposure to global risks, offering both opportunities and challenges. As globalization continues to evolve, ADRs will remain a vital tool for investors and corporations alike, reinforcing their role as a cornerstone of modern capital markets.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The 3-5-7 Rule is a trading strategy that helps investors manage risk and maximize gains by setting clear limits on losses and targets for profits. It’s a simple yet powerful framework for disciplined decision-making.

In the volatile world of trading, success often hinges not just on identifying opportunities but on managing risk with precision. The 3-5-7 Rule is a widely respected risk management strategy designed to help traders protect their capital while pursuing consistent returns. This rule provides a structured approach to trading by setting specific thresholds for risk exposure and profit expectations.

At its core, the 3-5-7 Rule breaks down into three key components:

3% Risk Per Trade: Traders should never risk more than 3% of their total account value on a single trade. This limit ensures that even if a trade goes against them, the loss is manageable and doesn’t jeopardize their overall portfolio.

5% Total Exposure Across All Positions: The rule advises that total exposure across all open positions should not exceed 5% of the account value. This prevents over-leveraging and reduces the impact of correlated losses during market downturns.

7% Profit Target: For every trade, the goal is to achieve a profit that is at least 7% greater than the potential loss. This risk-to-reward ratio helps ensure that even with a lower win rate, traders can remain profitable over time.

The beauty of the 3-5-7 Rule lies in its simplicity and adaptability. It can be applied across various asset classes—stocks, forex, crypto—and suits both beginners and seasoned traders. By enforcing discipline, it helps traders avoid emotional decisions, such as chasing losses or holding onto losing positions too long. Moreover, this rule encourages thoughtful position sizing. Traders must calculate their entry and exit points carefully, factoring in stop-loss levels and account size. This analytical approach fosters better trade planning and reduces impulsive behavior.

Another advantage is its scalability. As a trader’s account grows, the percentages remain constant, but the dollar amounts adjust accordingly. This keeps the strategy relevant and effective regardless of portfolio size. In practice, the 3-5-7 Rule acts as a safety net. It doesn’t guarantee profits, but it significantly reduces the likelihood of catastrophic losses. It also promotes consistency, which is crucial for long-term success in trading.

In conclusion, the 3-5-7 Rule is more than just a guideline—it’s a mindset. It teaches traders to respect risk, plan strategically, and aim for favorable outcomes.

By adhering to this rule, traders can navigate the unpredictable markets with greater confidence and control.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

High-frequency trading (HFT) is a form of algorithmic trading that uses powerful computers and complex programs to execute thousands of trades in fractions of a second. It has transformed modern financial markets by increasing speed, liquidity, and efficiency—but also raised concerns about fairness and stability.

High-frequency trading emerged in the early 2000s as technological advances allowed financial firms to process market data and execute trades faster than ever before. HFT firms use sophisticated algorithms to analyze multiple markets and identify short-term opportunities. These trades are often held for mere seconds or milliseconds, and profits are made by exploiting tiny price discrepancies across assets or exchanges.

One of the defining features of HFT is its reliance on speed. Firms invest heavily in infrastructure—such as co-location services near exchange servers and fiber-optic cables—to gain microsecond advantages over competitors. This race for speed has led to a technological arms race, where milliseconds can mean millions in profit.

HFT contributes significantly to market liquidity, meaning it helps ensure that buyers and sellers can transact quickly at stable prices. By constantly placing and updating orders, HFT firms narrow bid-ask spreads and reduce transaction costs for other market participants. This has made markets more efficient and accessible, especially for retail investors.

However, HFT is not without controversy. Critics argue that it creates an uneven playing field, where firms with access to advanced technology and capital can dominate markets. Concerns about market manipulation—such as quote stuffing (flooding the market with orders to slow competitors) or spoofing (placing fake orders to move prices)—have led to increased regulatory scrutiny.

The 2010 Flash Crash is often cited as a cautionary example of HFT’s potential risks. During this event, the Dow Jones Industrial Average plunged nearly 1,000 points in minutes before rebounding. Investigations revealed that automated trading systems, including HFT algorithms, contributed to the sudden loss of liquidity and extreme volatility.

Regulators have responded by implementing safeguards such as circuit breakers, which pause trading during extreme price movements, and requiring firms to register and disclose their trading strategies. The Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) continue to monitor HFT’s impact on market integrity.

Despite its challenges, HFT remains a dominant force in global finance. It accounts for a significant portion of trading volume in equities, futures, and foreign exchange markets. Many institutional investors rely on HFT strategies to manage large portfolios and hedge risks.

In conclusion, high-frequency trading represents both the promise and peril of technological innovation in finance. While it enhances market efficiency and liquidity, it also introduces new risks and ethical dilemmas.

As markets evolve, balancing innovation with fairness and stability will be essential to ensuring that HFT serves the broader interests of investors and the economy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Short Interest Theory suggests that high levels of short interest in a stock may actually signal a potential price increase, contrary to traditional bearish interpretations.

Short Interest Theory is a contrarian investment concept that challenges conventional wisdom in financial markets. Traditionally, a high short interest—meaning a large percentage of a company’s shares are being sold short—is seen as a bearish signal, indicating that many investors expect the stock’s price to decline. However, Short Interest Theory flips this assumption, proposing that a high short interest can actually be a bullish indicator, suggesting a potential upward price movement due to a phenomenon known as a “short squeeze.”

To understand this theory, it’s important to grasp the mechanics of short selling. When investors short a stock, they borrow shares and sell them on the open market, hoping to repurchase them later at a lower price and pocket the difference. However, if the stock price rises instead of falling, short sellers face mounting losses. To limit these losses, they may be forced to buy back the stock at higher prices, which increases demand and drives the price up even further. This chain reaction is what’s known as a short squeeze.

Short Interest Theory posits that when short interest reaches unusually high levels, the stock becomes a prime candidate for a short squeeze. Investors who follow this theory look for stocks with high short interest ratios—often measured as the number of shares sold short divided by the stock’s average daily trading volume. A high ratio suggests that it would take many days for all short sellers to cover their positions, increasing the likelihood of a rapid price surge if positive news or buying pressure emerges.

This theory gained widespread attention during the GameStop (GME) saga in early 2021. Retail investors noticed that GME had an extremely high short interest—more than 100% of its float—and began buying shares en masse. This triggered a historic short squeeze, sending the stock price soaring and forcing institutional short sellers to cover their positions at massive losses. The event served as a real-world validation of Short Interest Theory and highlighted the power of collective investor behavior in modern markets.

Despite its appeal, Short Interest Theory is not without risks. Betting on a short squeeze can be speculative and volatile. Not all heavily shorted stocks experience upward momentum; some may continue to decline if the negative sentiment is justified by poor fundamentals or weak earnings. Moreover, timing a short squeeze is notoriously difficult, and investors can suffer significant losses if the anticipated rebound fails to materialize.

In conclusion, Short Interest Theory offers a compelling contrarian perspective on market sentiment. By interpreting high short interest as a potential bullish signal, it encourages investors to look beyond surface-level indicators and consider the dynamics of market psychology and trading behavior. While it can lead to lucrative opportunities, especially in the context of short squeezes, it also demands careful analysis and risk management. As with any investment strategy, understanding the underlying fundamentals and market context is essential for making informed decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

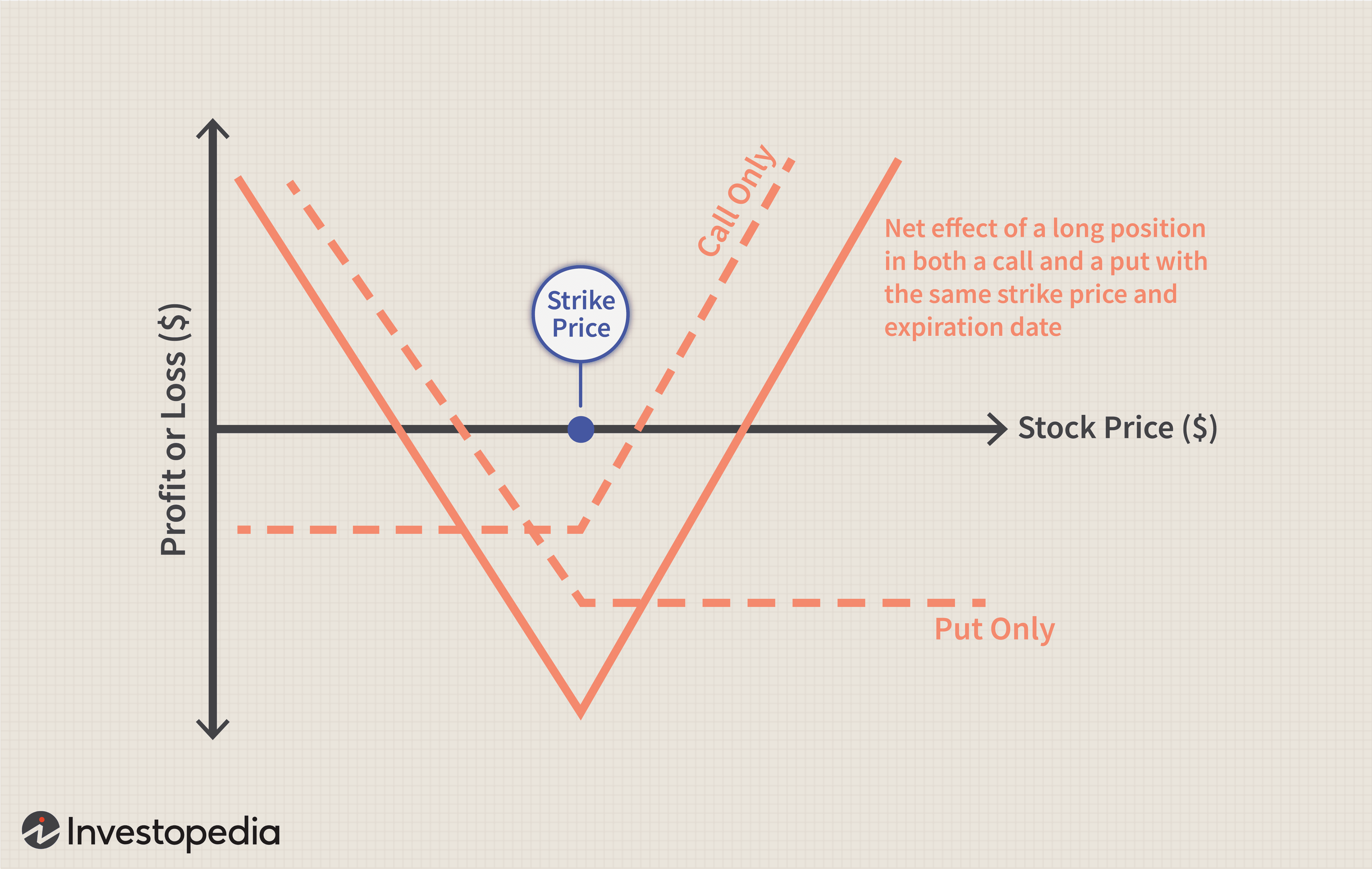

Understanding Stock Market Options: A Strategic Investment Tool

Stock market options are financial instruments that offer investors a versatile way to participate in the equity markets. Unlike traditional stock trading, options provide the right—but not the obligation—to buy or sell an underlying asset at a predetermined price within a specified time frame. This flexibility makes options a powerful tool for hedging, speculation, and income generation.

There are two primary types of options: calls and puts. A call option gives the holder the right to buy a stock at a specific price, known as the strike price, before the option expires. Investors typically purchase call options when they anticipate a rise in the stock’s price. Conversely, a put option grants the right to sell a stock at the strike price, and is used when an investor expects the stock to decline. Each option contract typically represents 100 shares of the underlying stock.

Options are traded on regulated exchanges such as the Chicago Board Options Exchange (CBOE), and their prices are influenced by several factors. These include the underlying stock’s price, the strike price, time until expiration, volatility, and prevailing interest rates. The premium, or cost of the option, reflects these variables and represents the maximum loss for the buyer.

***

***

One of the most compelling uses of options is hedging. Investors can use options to protect their portfolios against adverse price movements. For example, owning put options on a stock can offset potential losses if the stock’s value drops. This strategy is akin to purchasing insurance and is especially valuable during periods of market uncertainty.

Options also enable speculative strategies with limited capital. Traders can leverage options to bet on price movements without owning the underlying asset. While this can lead to significant gains, it also carries substantial risk, particularly if the market moves against the position. Therefore, understanding the mechanics and risks of options is crucial before engaging in such trades.

Another popular strategy involves writing options, or selling them to collect premiums. Covered call writing, for instance, involves holding a stock and selling call options against it. This generates income but caps potential upside if the stock surges beyond the strike price. Similarly, cash-secured puts allow investors to earn premiums while potentially acquiring stocks at a discount.

Despite their advantages, options are not suitable for all investors. Their complexity and potential for rapid loss require a solid grasp of financial concepts and disciplined risk management. Regulatory bodies and brokerages often require investors to pass suitability assessments before granting access to options trading.

In conclusion, stock market options are dynamic instruments that offer a range of strategic possibilities. Whether used for hedging, speculation, or income, they provide flexibility that traditional stock trading cannot match. However, their effective use demands education, experience, and a clear understanding of market behavior. For informed investors, options can be a valuable addition to a diversified financial toolkit.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The S&P 500, short for the Standard & Poor’s 500 Index, is one of the most widely followed stock market indices in the world. It tracks the performance of 500 of the largest publicly traded companies in the United States, offering a broad snapshot of the overall health and direction of the U.S. economy. Created in 1957 by the financial services company Standard & Poor’s, the index has become a benchmark for investors, analysts, and economists alike.

Composition and Criteria The S&P 500 includes companies from a wide range of industries, such as technology, healthcare, finance, energy, and consumer goods. To be included in the index, a company must meet specific criteria: it must be based in the U.S., have a market capitalization of at least $14.5 billion (as of 2025), be highly liquid, and have a public float of at least 50% of its shares. Additionally, the company must have positive earnings in the most recent quarter and over the sum of its most recent four quarters.

Some of the most recognizable names in the S&P 500 include Apple, Microsoft, Amazon, Johnson & Johnson, JPMorgan Chase, and ExxonMobil. These companies are selected by a committee that reviews eligibility and ensures the index remains representative of the broader market.

How It Works The S&P 500 is a market-capitalization-weighted index, meaning that companies with larger market values have a greater influence on the index’s performance. For example, a significant movement in Apple’s stock price will affect the index more than a similar movement in a smaller company’s stock. This weighting system helps reflect the real impact of large corporations on the economy.

The index is updated in real time during trading hours and is used by investors to gauge market trends. It also serves as the basis for many investment products, such as mutual funds and exchange-traded funds (ETFs), which aim to replicate its performance.

Why It Matters The S&P 500 is considered a leading indicator of U.S. equity markets and the economy as a whole. When the index rises, it often signals investor confidence and economic growth. Conversely, a decline may indicate uncertainty or economic slowdown. Because it includes companies from diverse sectors, the S&P 500 provides a more balanced view than narrower indices like the Dow Jones Industrial Average, which only tracks 30 companies.

Investment and Strategy Many investors use the S&P 500 as a benchmark to measure the performance of their portfolios. Passive investment strategies, such as index funds, aim to match the returns of the S&P 500 rather than beat it. This approach has gained popularity due to its low fees and consistent long-term performance.

In summary, the S&P 500 is more than just a number—it’s a powerful tool that reflects the pulse of the American economy. By tracking the performance of 500 major companies, it offers insights into market trends, investor sentiment, and economic health. Whether you’re a seasoned investor or just starting out, understanding the S&P 500 is essential to navigating the world of finance.

Posted on October 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

The VIX, or CBOE Volatility Index, is often called the “fear gauge” of the stock market. It measures the market’s expectations for volatility over the next 30 days, based on options prices for the S&P 500.

“THE INVESTOR’S CHIEF problem—even his worst enemy—is likely to be himself.” So wrote Benjamin Graham, the father of modern investment analysis.

With these words, written in 1949, Graham acknowledged the reality that investors are human. Though he had written an 800 page book on techniques to analyze stocks and bonds, Graham understood that investing is as much about human psychology as it is about numerical analysis.

In the decades since Graham’s passing, an entire field has emerged at the intersection of psychology and finance. Known as behavioral finance, its pioneers include Daniel Kahneman, Amos Tversky and Richard Thaler. Together, they and their peers have identified countless human foibles that interfere with our ability to make good financial decisions. These include hindsight bias, recency bias and overconfidence, among others. On my bookshelf, I have at least as many volumes on behavioral finance as I do on pure financial analysis, so I certainly put stock in these ideas.

At the same time, I think we’re being too hard on ourselves when we lay all of these biases at our feet. We shouldn’t conclude that we’re deficient because we’re so susceptible to biases. Rather, the problem is that finance isn’t a scientific field like math or physics. At best, it’s like chaos theory. Yes, there is some underlying logic, but it’s usually so hard to observe and understand that it might as well be random. The world of personal finance is bedeviled by paradoxes, so no individual—no matter how rational—can always make optimal decisions.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just last year.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.”

In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.