BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

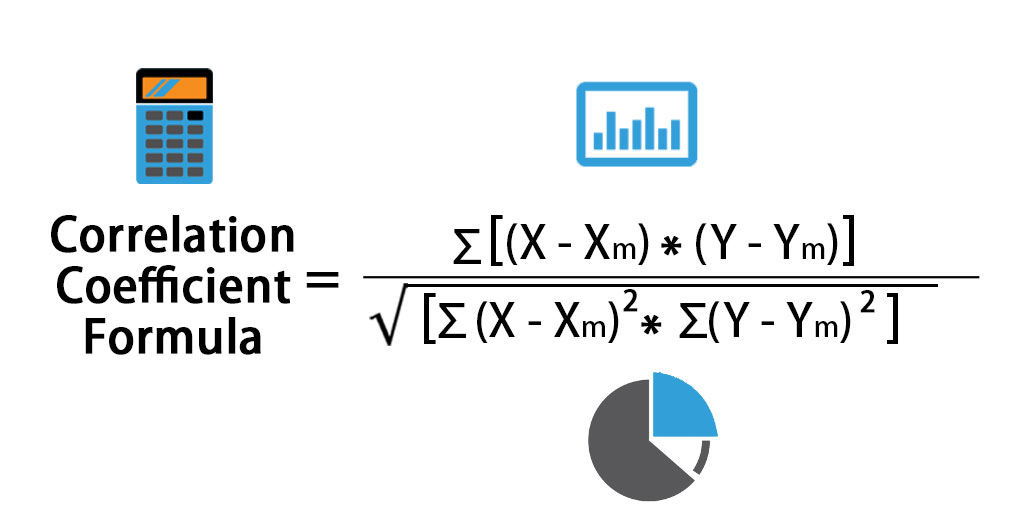

Correlation measures the relationship between two investments–the higher the correlation, the more likely they are to move in the same direction for a given set of economic or market events. Correlation, in the finance and investment industries, is a statistic that measures the degree to which two securities move in relation to each other. Correlations are used in advanced portfolio management, computed as the correlation coefficient which has a value that must fall between -1.0 and +1.0.

So if two securities are highly positively correlated, they will move in the same direction the vast majority of the time. Negatively correlated investments do the opposite–as one security rises, the other falls, and vice versa. No correlation means there is no relationship between the movement of two securities–the performance of one security has no bearing on the performance of the other.

Correlation is an important concept for portfolio diversification--combining assets with low or negative correlations can improve risk-adjusted performance over time by providing a diversity of payouts under the same financial conditions.

Life planning and behavioral finance as proposed for physicians and integrated by the Institute of Medical Business Advisors Inc., is unique in that it emanates from a holistic union of personal financial planning, human physiology and medical practice management, solely for the healthcare space. Unlike pure life planning, pure financial planning, or pure management theory, it is both a quantitative and qualitative “hard and soft” science, with an ambitious economic, psychological and managerial niche value proposition never before proposed and codified, while still representing an evolving philosophy. Its’ first-mover practitioners are called Certified Medical Planners™.

Financial Life Planning is an approach to financial planning that places the history, transitions, goals, and principles of the client at the center of the planning process. For the financial advisor or planner, the life of the client becomes the axis around which financial planning develops and evolves.

Financial Life Planning is about coming to the right answers by asking the right questions. This involves broadening the conversation beyond investment selection and asset management to exploring life issues as they relate to money.

Financial Life Planning is a process that helps advisors move their practice from financial transaction thinking, to life transition thinking. The first step is aimed to help clients “see” the connection between their financial lives and the challenges and opportunities inherent in each life transition.

But, for informed physicians, life planning’s quasi-professional and informal approach to the largely isolate disciplines of financial planning and medical practice management is inadequate. Today’s practice environment is incredibly complex, as compressed economic stress from HMOs managed care, financial insecurity from insurance companies, ACOs and VBC, Washington DC and Wall Street; liability fears from attorneys, criminal scrutiny from government agencies, and IT mischief from malicious electronic medical record [eMR] hackers. And economic bench marking from hospital employers; lost confidence from patients; and the Patient Protection and Affordable Care Act [PP-ACA] more than a decade ago. All promote “burnout” and converge to inspire a robust new financial planning approach for physicians and most all medical professionals.

The iMBA Inc., approach to financial planning, as championed by the Certified Medical Planner™ professional certification designation program, integrates the traditional concepts of financial life planning, with the increasing complex business concepts of medical practice management. The former topics are presented in this textbook, the later in our recent companion text: The Business of Medical Practice [Transformational Health 2.0 Skills for Doctors].

***

***

For example, views of medical practice, personal lifestyle, investing and retirement, both what they are and how they may look in the future, are rapidly changing as the retail mentality of medicine is replaced with a wholesale and governmental philosophy. Or, how views on maximizing current practice income might be more profitably sacrificed for the potential of greater wealth upon eventual practice sale and disposition.

Or, how the ultimate fear represented by Yale University economist Robert J. Shiller, in The New Financial Order: Risk in the 21st Century, warns that the risk for choosing the wrong profession or specialty, might render physicians obsolete by technological changes, managed care systems or fiscally unsound demographics. OR, if a medical degree is even needed for future physicians?

Say, what medical license?

Dr. Shirley Svorny, chair of the economics department at California State University, Northridge, holds a PhD in economics from UCLA. She is an expert on the regulation of health care professionals who participated in health policy summits organized by Cato and the Texas Public Policy Foundation. She argues that medical licensure not only fails to protect patients from incompetent physicians, but, by raising barriers to entry, makes health care more expensive and less accessible. Institutional oversight and a sophisticated network of private accrediting and certification organizations, all motivated by the need to protect reputations and avoid legal liability, offer whatever consumer protections exist today.

Yet, the opportunity to revise the future at any age through personal re-engineering, exists for all of us, and allows a joint exploration of the meaning and purpose in life. To allow this deeper and more realistic approach, the informed transformation advisor and the doctor client, must build relationships based on trust, greater self-knowledge and true medical business management and personal financial planning acumen.

[A] The iMBA Philosophy

As you read this ME-P website, we hope you will embrace the opportunity to receive the focused and best thinking of some very smart people. Hopefully, along the way you will self-saturate with concrete information that proves valuable in your own medical practice and personal money journey. Maybe, you will even learn something that is so valuable and so powerful, that future reflection will reveal it to be of critical importance to your life. The contributing authors certainly hope so.

At the Institute of Medical Business Advisors, and thru the Certified Medical Planner™ program, we suggest that such an epiphany can be realized only if you have extraordinary clarity regarding your personal, economic and [financial advisory or medical] practice goals, your money, and your relationship with it. Money is, after only, no more or less than what we make of it.

Ultimately, your relationship with it, and to others, is the most important component of how well it will serve you.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on April 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to colleague Dan Ariely PhD, Bereavement Sex is one of those coping mechanisms that sounds strange but makes sense when you think about it. In the face of loss, our brains crave connection and comfort.

Engaging in sex after a significant loss can be a way to feel alive and regain a sense of control. It’s a testament to our complex emotional wiring, where grief and intimacy intertwine.

*** Several years ago we noted that far too many mid-career, mature and physician clients using traditional stock brokers, management consultants and “financial advisors”, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc,. doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse related relationship was noted, and dubbed the “Doctor Effect.” In other words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning, professional portfolio and investing continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization was a confirmation of the industry culture which seemed to be: Bread for the advisor – Crumbs for the client!

And so, we at the the Institute of Medical Business Advisors Inc. (iMBA), and this Medical Executive-Post, formed a cadre’ of technology focused and highly educated doctors, financial advisors, attorneys, accountants, psychologists and educational visionaries who decided there must be a better way for their healthcare colleagues to receive financial planning advice, products and related management services within a culture of fiduciary responsibility.

We trust you agree with this ME Inc philosophy as illustrated in this free white paper available upon request.

PROFESSIONAL PORTFOLIO CONSTRUCTION [Investing Assets and their Management] Subscribe, Read, Like and Refer

Email whiote paper request here:MarcinkoAdvisors@outlook.com

Posted on January 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

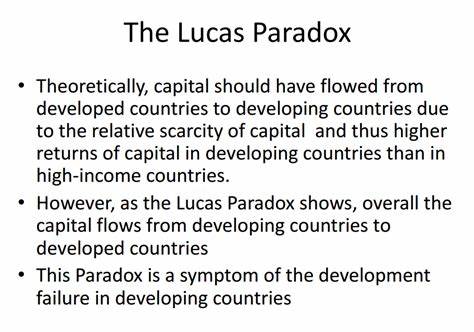

Capital is not flowing from developed countries to developing countries despite the fact that developing countries have lower levels of capital per worker, and therefore higher returns to capital.

Classical economic theory predicts that capital should flow from rich countries to poor countries, due to the effect of diminishing returns of capital. Poor countries have lower levels of capital per worker – which explains, in part, why they are poor. In poor countries, the scarcity of capital relative to labor should mean that the returns related to the infusion of capital are higher than in developed countries.

In response, savers in rich countries should look at poor countries as profitable places in which to invest. In reality, things do not seem to work that way. Surprisingly little capital flows from rich countries to poor countries.

This puzzle, famously discussed in a paper by Robert Lucas in 1990, is often referred to as the “Lucas Paradox”.

Posted on January 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

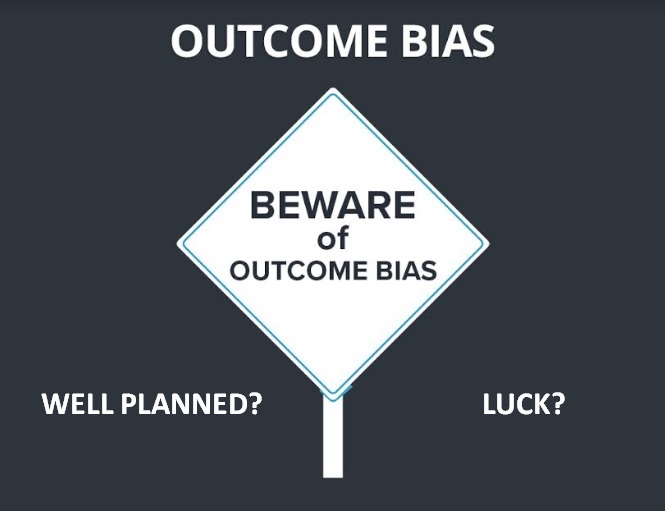

Outcome bias is judging a decision based on its result rather than the quality of the decision at the time it was made.

It’s like saying a bad poker play was smart because you won the hand. Or, a bad stock picker or financial advisor was good because the price went up!

According to psychologist and colleague Dan Ariely PhD, this bias ignores the process and focuses solely on the outcome. It’s why we celebrate lucky breaks and criticize thoughtful risks that didn’t pan out.

So, the next time you’re evaluating a decision, focus on the reasoning behind it, not just the end result.

Choice Overload is the difficulty in making a decision when faced with too many options. It’s like standing in front of an ice cream counter with 31 flavors and feeling paralyzed.

Among personal decision-makers, a prevention focus is activated and people are more satisfied with their choices after choosing among few options compared to many options, i.e. choice overload. However, individuals can also experience a reverse choice overload effect when acting as proxy decision-maker, too.

It is widely accepted that having more choices is inherently positive. When there are more available options from which to choose, an individual is more likely to be able to select the particular option that is the best fit and most likely to satisfy them. Choice is typically thought to be related to personal freedom and enhanced well-being.

Therefore, according to colleague Neal Baum MD, for most individuals the ultimate goal is to constantly maximize their choices in life to increase their overall satisfaction and well-being. The decision-making process, however, is a complex cognitive task that does not always lead to positive outcomes.

Thus, while having options is generally good, too many choices can lead to anxiety and decision fatigue. This is why curated selections and recommendations are so popular – they simplify the decision-making process’ according to another colleague Dan Ariely PhD.

So, when you’re overwhelmed by choices, narrow them down to a manageable number and make your decision easier.

Commodities: Commodities are raw materials or primary agricultural products that can be bought or sold on an exchange or market. Examples include grains such as corn, foods such as coffee, and metals such as copper.

Commodity Futures: Agreements to buy or sell a specific amount of a commodity or financial instrument at a particular price on a stipulated future date related to basic raw materials such as precious metals and natural resources.

Commodity Intensity: Commodity intensity refers to commodity usage per unit of economic growth. An emerging, more manufacturing-based economy will usually be more commodity intensive in terms of its growth than will a more developed, service-oriented economy.

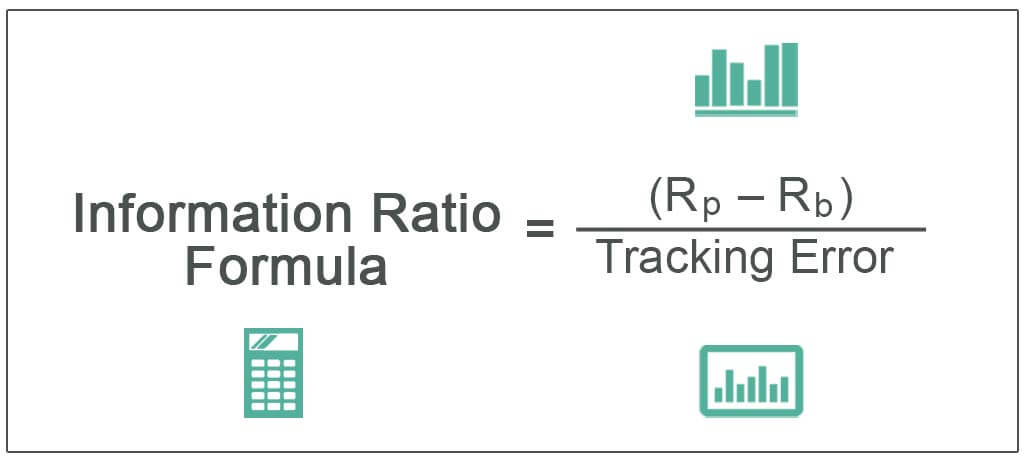

The Information Ratio (IR) is a risk-adjusted rate of return measure for comparing the performance of active investment managers over time. Its purpose is to help determine how much return an active portfolio manager has added per unit of active management risk.

Think of IR as a Sharpe Ratiofor active investment management; the IR is more focused than the Sharpe Ratio. Starting with the Sharpe Ratio’s formula, if we replace the excess return in the numerator with a portfolio’s active return (the average annualized return of an actively managed portfolio minus the average annualized return of the portfolio’s benchmark over a given period, adjusted for the portfolio’s market risk exposure), and you replace the Sharpe Ratio’s standard deviation of excess returns in the denominator with the standard deviation of a portfolio’s active returns over the period, you have the IR.

While the Sharpe Ratio expresses the amount of excess return per unit of overall risk, the IR computes only the active management-driven (alpha) returns per unit of alpha-driven risk. And while the Sharpe Ratio’s excess returns are calculated with regard to what is considered to be a relatively risk-free asset, such as a U.S. Treasury bill, the IR’s active returns are calculated with regard to each portfolio’s specific market benchmark.

The higher the IR, the better. The IR should be measured over a meaningful period of time, typically at least three to five years. The IR is not perfect–it can be influenced by external factors such as changes in market volatility. The standard deviation of active returns in the IR’s denominator is called tracking error. Tracking error will tend to increase in volatile markets for even the best active managers.

Two years ago, prior to the 2022 election, mental health experts alerted the medical world to their version of an assessment scale for yet another new condition – “doomscrolling.”

As defined by the National Library of Medicine in the article, “Constant exposure to negative news on social media and news feeds could take the form of ‘doomscrolling’ which is commonly defined as a habit of scrolling through social media and news feeds where users obsessively seek for depressing and negative information.”

And so, formally Doomscrolling or doomsurfing is the act of spending an excessive amount of time reading large quantities of news, particularly negative news, on the web and social media. Doomscrolling can also be defined as the excessive consumption of short-form videos or social media content for an excessive period of time without stopping. The concept was coined around 2020, particularly in the context of the COVID pandemic.

Surveys and studies suggest doomscrolling is predominant among youth. It can be considered a form of internet addiction disorder. In 2019, a study by the National Academy of Sciences found that it can be linked to a decline in mental and physical health. Numerous reasons for doomscrolling have been cited, including negativity bias and FOMO [fear of missing out], and attempts at gaining control over uncertainty.

QUERY: What about the roaring stock market, post the 2024 presidential election. Fundamental analysis or FOMO?

Posted on December 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

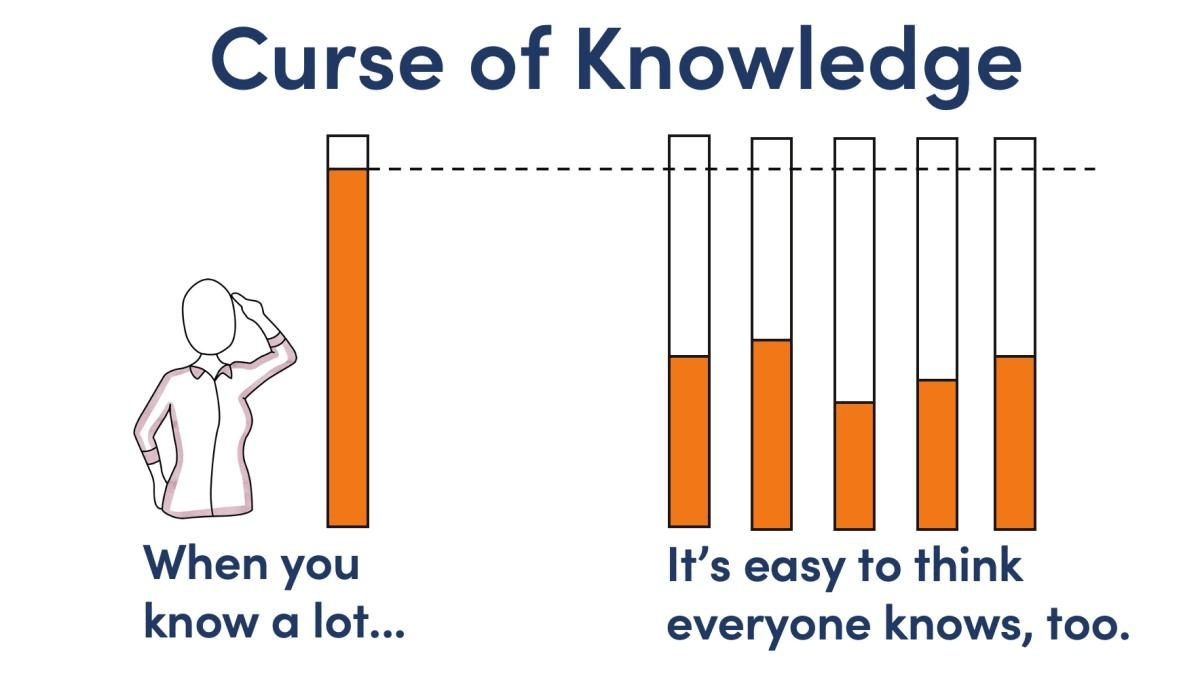

Similar to the availability heuristic (Tversky & Kahneman, 1974) and to some extent, the false consensus effect, once you really understand a new piece of information, that piece of information is now available to you and often becomes seemingly obvious. It might be easy to forget that there was ever a time you didn’t know this information and so, you assume that others, like yourself, also know this information: ie., the curse of knowledge.

However, it is often an unfair assumption that others share the same knowledge.

And so, the hindsight bias is similar to the curse of knowledge in that once we have information about an event, it then seems obvious that it was going to happen all along.

Market Capitalization: Market capitalization is the market value of all the equity of a company’s common and preferred shares. It is usually estimated by multiplying the stock price by the number of shares for each share class and summing the results.

Market Depth: The degree to which a market can execute large market orders without impacting the price of a security. For example, a “deep” market for a stock will have a sufficient number of both bid and ask orders to keep a big order from significantly moving the security’s price.

Market Maker: A market maker exists to “create a market” for specific company securities by being willing to buy and sell those securities at a specified displayed price and quantity to broker-dealer firms that are members of the exchange. These firms help keep financial markets liquid by making it easier for investors to buy and sell securities–they ensure that there is always someone to buy and sell to at the time of trade.

Market Neutral: Equity market neutral strategies seek to eliminate the risks of the equity market by holding up to 100% of net assets in long equity positions and up to 100% of net assets in short equity positions. These strategies attempt to exploit differences in stock prices by being long and short in stocks within the same sector, industry, market capitalization, etc. If successful, these strategies should generate returns independent of the equity market. Equity market neutral portfolios have two key sources of return:

the Treasury Bill return (the interest on proceeds from short sales held in cash as collateral)

the difference (the “spread”) between the return on the long positions and the return on the short positions. Stock picking, rather than broad market moves, should drive most of a market-neutral strategy’s total return (save for any return from the 100% cash position).

It’s important to point out that here is the risk of theoretical unlimited amount of loss with short selling, (i.e. the price of the short-sold stocks increases; the long position can only go down to $0).

Market Order: An order placed with a bank or brokerage firm to immediately buy or sell a security at the best available current price. May also be referred to as an “unrestricted order.”

Posted on December 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Shadow Self is like the dark twin you never knew you had. It’s the part of your personality that lurks in the background, hiding your less-than-perfect traits. Think of it as the villain in your personal movie, full of suppressed desires and impulses.

According to colleague Dan Ariely PhD, acknowledging your shadow self can be a bit like therapy – uncomfortable but ultimately enlightening.

So, embrace your inner Darth Vader, and you might just find a better balance between light and dark.

Municipal Securities (munis): Debt securities typically issued by or on behalf of U.S. state and local governments, their agencies or authorities to raise money for a variety of public purposes, including financing for state and local governments as well as financing for specific projects and public facilities. In addition to their specific set of issuers, the defining characteristic of munis is their tax status. The interest income earned on most munis is exempt from federal income taxes. Interest payments are also generally exempt from state taxes if the bond owner resides within the state that issued the security. The same rule applies to local taxes.

Another interesting characteristic of munis: Individuals, rather than institutions, make up the largest investor base. In part because of these characteristics, munis tend to have certain performance attributes, including higher after-tax returns than other fixed income securities of comparable maturity and credit quality and low volatility relative to other fixed-income sectors.

The two main types of munis are general obligation bonds (GOs) and revenue bonds. GOs are munis secured by the full faith and credit of the issuer and usually supported by the issuer’s taxing power. Revenue bonds are secured by the charges tied to the use of the facilities financed by the bonds.

Municipal Yield Curve: The yield curve that illustrates the yields of a certain type of municipal security at its various maturities.

Municipal Yield Ratio: A yield ratio most often used to determine the relative value of municipal securities compared with U.S. Treasury securities. The ratio consists of the yield of a municipal security of a certain maturity divided by the yield of a U.S. Treasury security of the same maturity.

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

LTC

By Anonymous Insurance Agent

***

***

Some retired people live on a fixed income and many of them live right on the edge of their financial capability. At some time in their life, they may have to make a choice regarding many purchases. In this case, we will illustrate “choice” using a couple’s purchase of Long-Term-Care Insurance [LTCI].

Of course, economics is the study of choice; wants, needs and scarcity, etc. In our case, if they decide to make the purchase they commit to a lifetime of premium payments. The financial tradeoff is this; if they make the commitment to purchase LTCI, they must give up something else.

Example: In order to maintain a monthly premium of $100 ($1,200per year), an elderly patient, retired layman or couple must essentially relegate about $30,000 of financial assets to generate the $100 necessary to make an average premium payment (assumes a 7% rate of return with 4% withdrawal rate) or [4% X $30,000 = $1,200 year]. Thus, if the monthly premium cost is $500 per month, the elder must give up the use of $150,000 of retirement asset just to generate enough cash flow to pay for the LTC insurance.

The married elder couple has to make the decision among lifestyle (dinners, vacations, gifts to children, prescription drugs, medical care or food and shelter) versus paying an insurance premium to provide for nursing home coverage for a need, which may be very real, but will not occur until sometime in the ambiguous future.

And so, when faced with such a tough economics, neither of which delivers peace of mind or a respectable solution; many will simply decide that, in either case, they may already end up impoverished.

Thus, many will often opt for the better lifestyle now … while they can enjoy it … together.

Real Bond Yield: For most bonds and other fixed-income securities, real yield is simply the yield you see listed online or in newspapers minus the premium added to help counteract the effects of inflation. Most “nominal” fixed-income yields include an “inflation premium” that is typically priced into the yields to help offset the effects of inflation.

Real yields, such as those for TIPS, don’t have the inflation premium. As a result, TIPS yields and other real yields are typically lower than most nominal yields

Negative Bond Yield: In a normal bond market environment, bond yields are positive, and bond issuers (including governments) make interest payments to investors who lend them money.

In an abnormal, or negative-yield environment, investors essentially pay the bond issuer to hold their money.

“Paradox of Medical Progress” is a language of medicine is loaded with misnomers, inaccuracies, and ambiguities, and is in need of reform.

Paradoxes on the other hand, deserve a different kind of attention. These seeming self-contradictions are set apart from other inconsistencies because of the truths they tell. The veracity of a paradox is at once appealing and vexing. Anyone who has tried to suppress a thought knows that trying not to think of white polar bears is a sure way to think of white polar bears!

The comic impact of a paradox was even famously explored in Joseph Heller’s Catch 22 and in Groucho Marx’s reluctance to be a member of any club that would accept him. However, the provocative nature of a paradox is its capacity to express familiar wisdom and this is particularly evident in medical science.

The more we learn, the more we learn how much we still have to learn; whereas, “what gets us into trouble is not what we don’t know, it’s what we know for sure that just ain’t so.”

On the significance of the knowledge paradox in biology, Lewis Thomas regarded ignorance as the only scientific truth of which he was confident, and discovering “the depth and scope of ignorance” as the greatest contribution of modern science.

Basis Points are used in financial literature to express values that are carried out to two decimal places (hundredths of a percentage point), particularly ratios, such as yields, fees, and returns. Basis points describe values that are typically on the right side of the decimal point–one basis point equals one one-hundredth of a percentage point (0.01%). So 25 basis points equals 0.25%, and 50 basis points equals 0.50%.

Only when basis points equal or exceed 100 does the value move to the left of the decimal point–100 basis points equals 1.00%, 500 basis points equals 5.00%, etc.

Bid/Ask Spread (also known as bid/offer spread) is the difference between the National Best Bid and the National Best Offer, which represents the implied cost to trade a security.

As compensation for the risk taken, the market maker (or dealer) earns the bid/offer spread in exchange for facilitating the trade. Wider spreads generally indicate higher costs associated with trading the underlying assets in the ETF, hedging costs, inventory management costs, and general market risk.

Prepayment risk is typically used in reference to mortgage-backed securities. It refers to the risk that mortgage refinancing activity might increase when market interest rates decline, which is generally not favorable for MBS investors.

For example, when homeowners refinance their mortgages, MBS investors are “prepaid,” shortening the life of their investments and forcing investors to reinvest the proceeds under lower interest rate conditions than what were most likely prevailing at the time of the original MBS investment.

Price adjustments for prepayment risk are one factor that helps explain why MBS, despite their generally high credit quality, have higher yields than comparable-maturity Treasury securities.

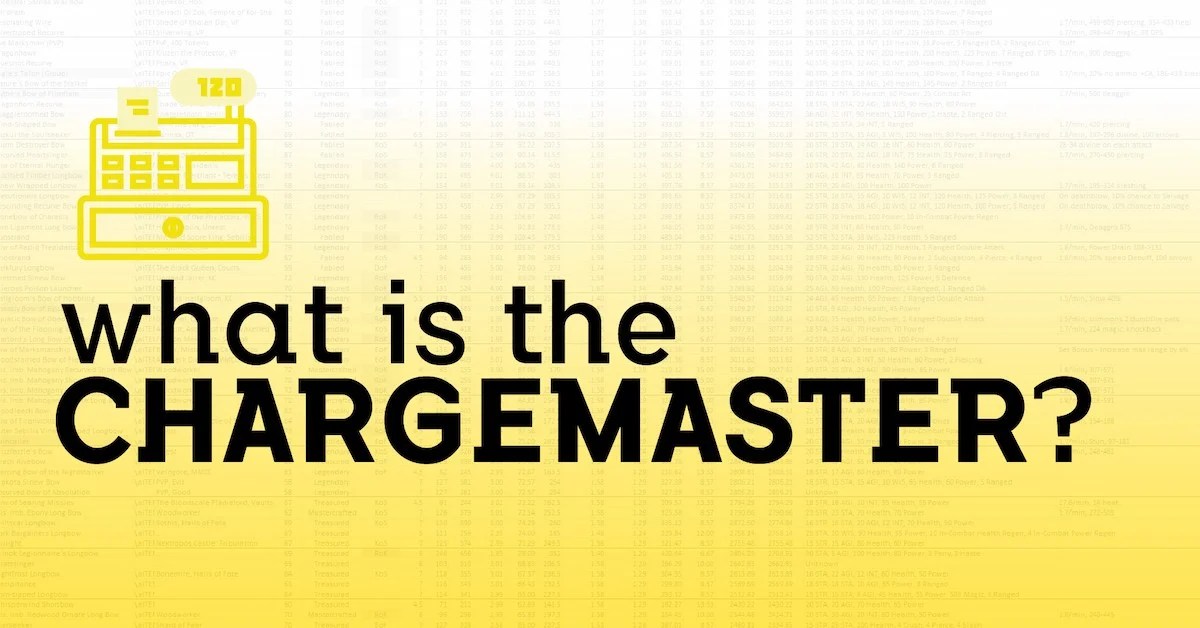

Classic Definition: A comprehensive review of a physician, clinic, facility, medical provider or hospital’s charges to ensure Medicare billing compliance through complete and accurate HCPCS/CPT and UB-92 revenue code assignments for all items including supplies and pharmaceuticals. The charge master captures the costs of each procedure, service, supply, prescription drug, and diagnostic test provided at the hospital, as well as any fees associated with services, such as equipment fees and room charges

Modern Circumstance: A charge master quizlet (charge description master [CDM]) document that contains a computer-generated list of procedures, services, and supplies with charges for each. Charge master rates are essentially the health care market equivalent of Manufacturer’s Suggested Retail Price (MSRP) in the car buying market. Poor charge master maintenance can lead to overpayments or underpayments. It can also lead to claim rejections from insurance companies, poor patient experience, or compliance violations.

Paradox Examples:

Superbills: An encounter form that is the financial record source document used by healthcare providers and other personnel to record treated diagnoses and services rendered to the patient during the current encounter. It is also called a superbill.

Payment rates: Almost no one actually pays the publicized charge master rates. The vast majority of health care consumers are represented by a payer of some kind, such as a commercial health insurance company, Medicaid, or Medicare. Commercial insurers negotiate the actual prices they pay during the process of contracting with providers. Medicare and Medicaid establish their own payment levels independent of hospitals’ charge master lists – Medicare through the federal government and Medicaid through state governments.

Cash pay: The sad irony of the charge master is that the uninsured are the most likely to be billed charge master rates because they are not represented by a third-party payer.

Problematic features: Other items also impede the ability of payers to have a comprehensive and accurate understanding of hospitals’ financial positions. For example, nonprofit hospitals are required to report charity care, bad debt expenses, community benefit initiatives, and uncompensated care. When these expenses are reported at the charge master level, expenses can be paradoxically overstated, potentially making a hospital’s financial position look worse than it actually is.

A trader can gain by throwing away some of his/her initial endowment.

SAMPLE: There is an economy with two commodities (x and y) and two traders (e.g. Alice and Bob).

In one situation, the initial endowments are (20,0) and (0,10), i.e, Alice has twenty units of commodity x and Bob has ten units of commodity y. Then, the market opens for trade. In equilibrium, Alice’s bundle is (4,2), i.e, she has four units of x and two units of y.

In the second situation, Alice decides to discard half of her initial endowment – she throws away 10 units of commodity x. Then, the market opens for trade. In equilibrium, Alice’s bundle is (5,5) – she has more of every commodity than in the first situation.

The “throw away paradox” was first described by Robert J. Aumann and B. Peleg as a note on a similar paradox by David Gale.

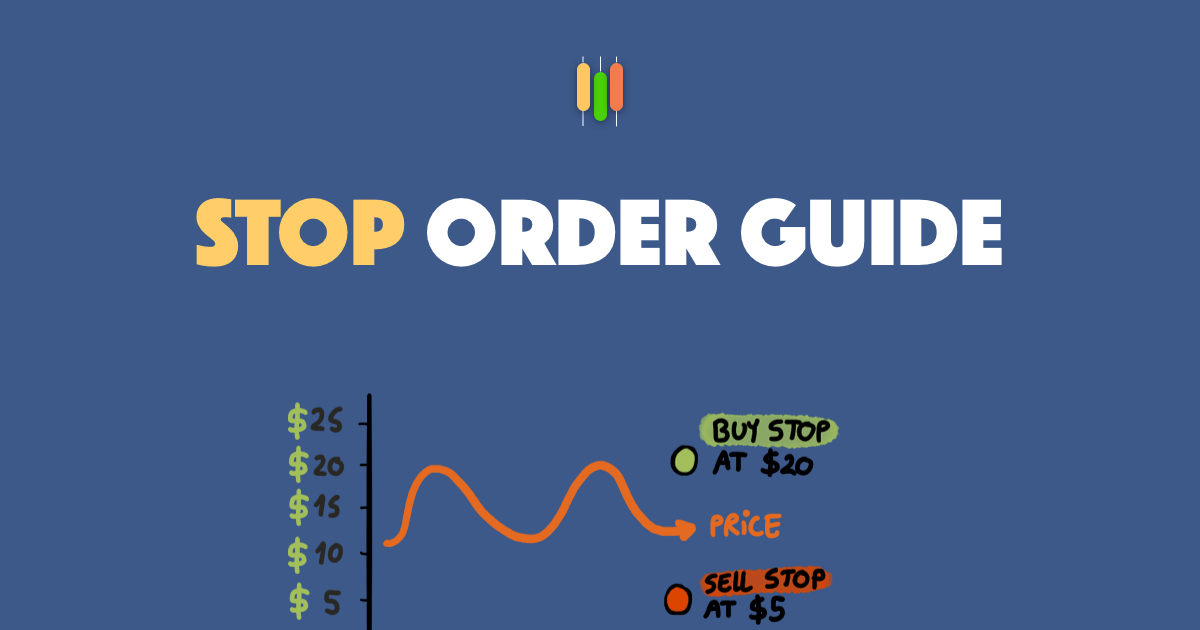

A Stop order, also known as a “stop-loss order,” a stop order is an order placed with a bank or brokerage firm to either buy or sell a security after it reaches a specified price. Once the price is reached, the stop order becomes a market order, meaning there is no guarantee that an order will be completely filled at the specified stop price.

A Stop-limit order is order placed with a bank or brokerage firm to buy or sell a fixed amount of an investment after it reaches a specified or better price, combining the features of a stop order and a limit order.

A stop-limit order requires investors to set two price points: the first initiates the stop (the order to buy or sell) and the second sets the limit, or price beyond which the investor would not like to buy or sell. The investor also sets a time frame for which the order is valid before being cancelled. If the investor’s price cannot be met during the specified time frame, the order will be cancelled.

Posted on November 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

You may have heard the complaint that the internet, blogs, vlogs and social media will be the downfall of information dissemination; but, Socrates reportedly said the same thing about the written word.

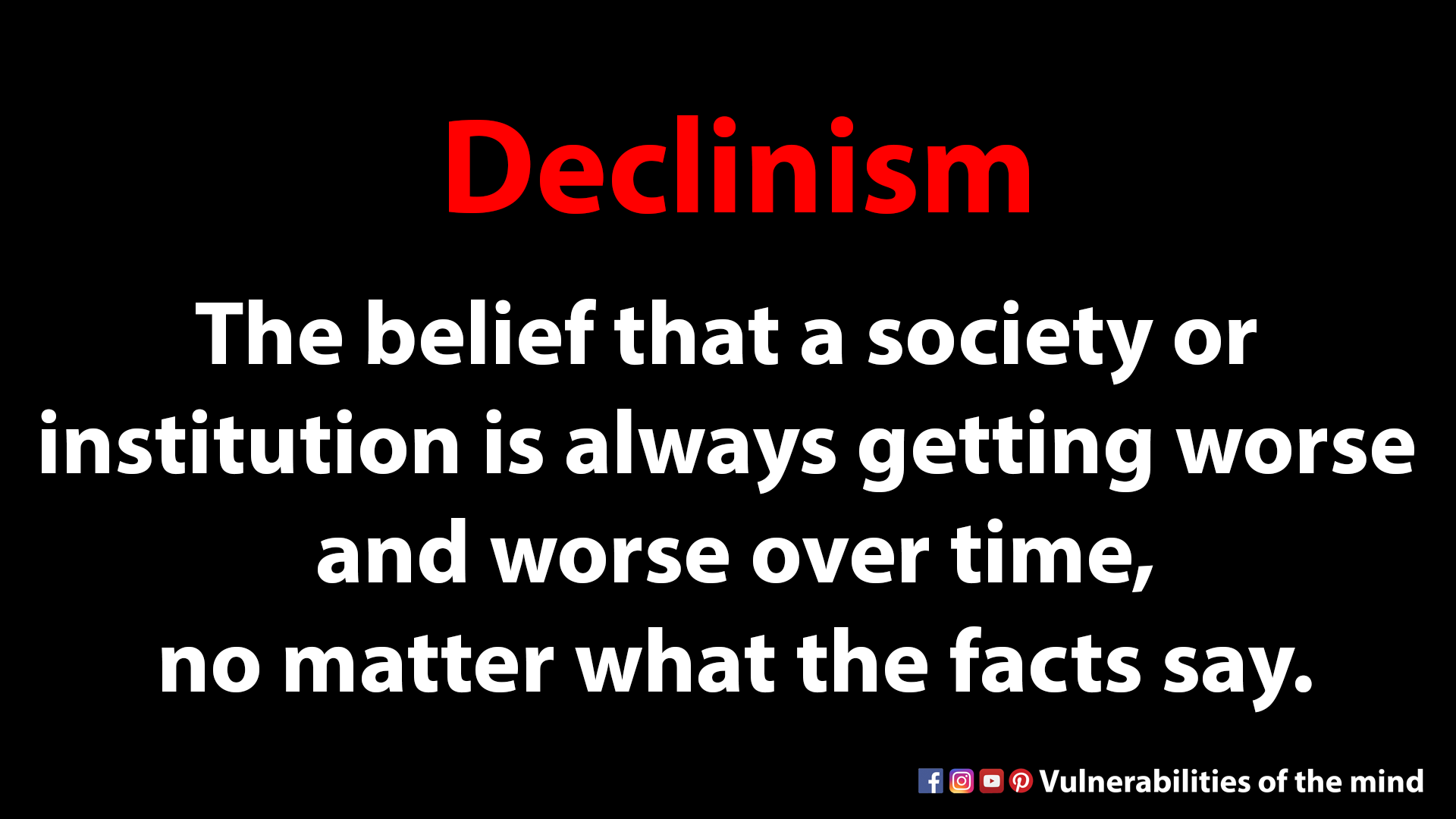

Declinism refers to a bias in favor of the past over and above “how things are going.” Similarly, you might know a member of an older generation who prefaces grievances with, “Well, back in my day” before following up with how things are supposedly getting worse.

The decline bias may result from something before — we just don’t like change. People like their worlds to make sense, they like things wrapped up in nice, neat little packages.

Our world is easier to engage in when things make sense to us. When things change, so must the way in which we think about them; and because we are cognitively lazy (Kahenman, 2011; Simon, 1957), we try our best to avoid changing our thought processes.

Posted on November 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

The number of people living with Alzheimer’s disease is growing. The ripple effect is straining families, communities, and the healthcare system, yet talking about the disease on a personal level can be difficult.

November is Alzheimer’s Awareness Month because it can happen in any family, and because it’s worth talking about the challenges of living with or caring for someone with this disease.

You may notice splashes of teal and purple sprouting up this November, as both colors are associated with Alzheimer’s awareness. Teal is the color of the Alzheimer’s Foundation of America, chosen for its calming effect. Purple is the signature color of the Alzheimer’s Foundation, which stands for strength in the fight against Alzheimer’s disease.

Posted on November 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

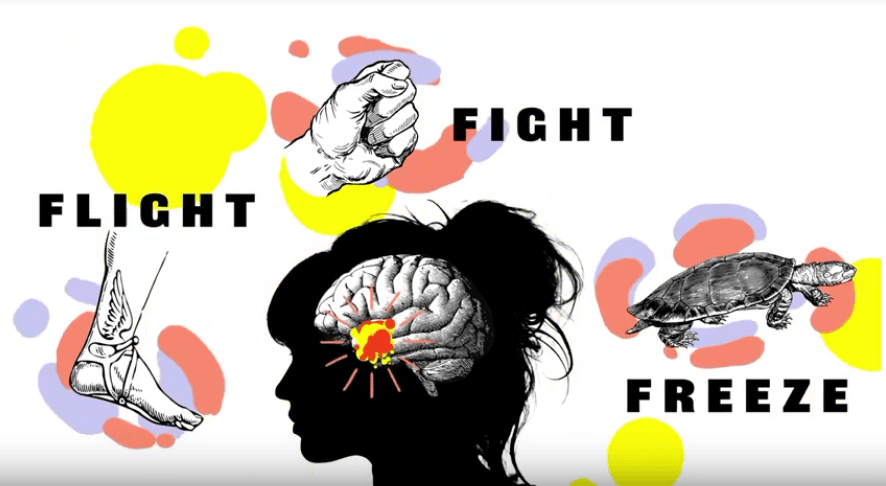

The Fight or Flight Response is our built-in alarm system, ready to spring into action at the first sign of danger. Whether it’s a charging lion or an impending deadline, our bodies react the same way – heart racing, adrenaline pumping, ready to fight or flee. This ancient survival mechanism is great for escaping predators but less helpful when dealing with modern stressors.

So, the next time you feel your heart racing over a tough email or stock market loss, remember: it’s just your caveman brain doing its thing.

Social Proof is a subtle but powerful reality that having others agree with a decision one makes, gives that person more conviction in the decision, and having others disagree decreases one’s confidence in that decision.

This bias is even more exaggerated when the other parties providing the validating/questioning opinions are perceived to be experts in a relevant field, or are authority figures, like doctors, attorneys, financial advisors, teachers and/or people on television. In many ways, the short term moves in the stock market are the ultimate expression of social proof – the price of a stock one owns going up is proof that a lot of other people agree with the decision to buy, and a dropping stock price means a stock should be sold.

According to colleague Dan Ariely PhD, when these stressors become extreme, it is of paramount importance that all participants in the financial planning and investing process have a clear understanding of what the long-term goals are, and what processes are in place to monitor the progress towards these goals.

Without these mechanisms it is very hard to resist the enormous pressure to follow the crowd; think social media and related influences.

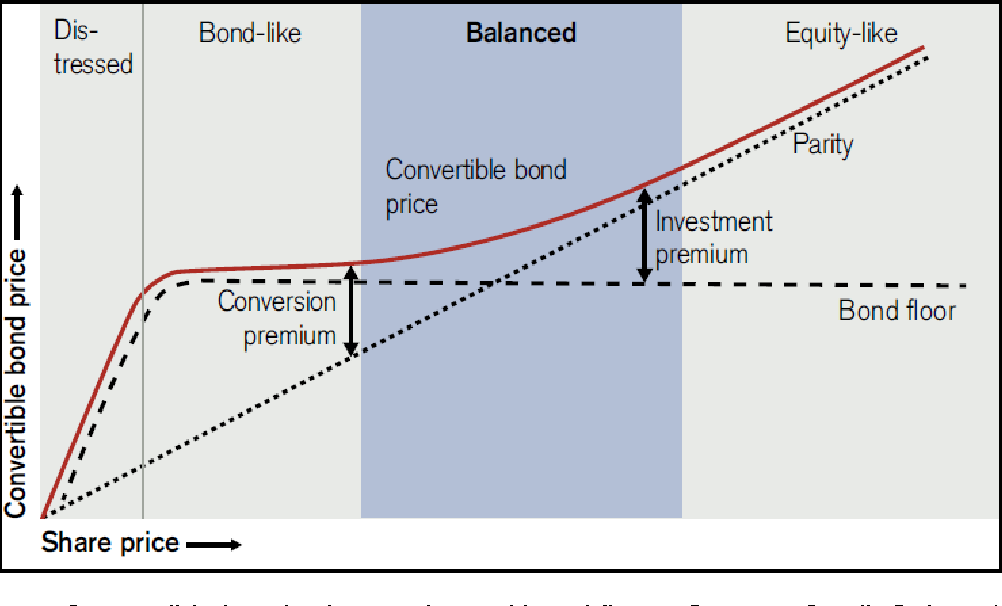

Convertible securities are those that can be converted at the investor’s choice into other investments, normally into shares of the issuer’s underlying common stock. Convertibles are typically issued as bonds or preferred stock.

Convertible bonds, which provide an ongoing stream of income, can be converted into a preset number of shares of the company’s common stock and have a maturity date. Unlike common stock, which pays a variable dividend depending on a corporation’s earnings, convertible preferred stock pays a fixed quarterly dividend. It can be converted into common stock at any time, but often are perpetual.

Corporate securities (corporate bonds and notes) are debt instruments issued by corporations, as distinct from those issued by governments, government agencies, or municipalities.

Corporate securities typically have the following features: 1) they are taxable, 2) they tend to have more credit (default) risk than government or municipal securities, so they tend to have higher yields than comparable-maturity securities in those sectors; and 3) they are traded on major exchanges, with prices published in newspapers.

Equity market neutral strategies seek to eliminate the risks of the equity market by holding up to 100% of net assets in long equity positions and up to 100% of net assets in short equity positions. These strategies attempt to exploit differences in stock prices by being long and short in stocks within the same sector, industry, market capitalization, etc. If successful, these strategies should generate returns independent of the equity market.

Equity market neutral portfolios have two key sources of return: 1) the Treasury Bill return (the interest on proceeds from short sales held in cash as collateral), and 2) the difference (the “spread”) between the return on the long positions and the return on the short positions. Stock picking, rather than broad market moves, should drive most of a market-neutral strategy’s total return (save for any return from the 100% cash position).

Extended Equity Strategies attempt to provide better returns than possible with long-only investments

An example of an extended equity strategy is a 130/30 portfolio, which gets its designation from taking a 130% long position and a 30% short position. In practice, this would mean $100mm invested in stocks that are viewed as attractive.

Next, the manager would borrow and sell short $30mm of unattractive stocks. Then the manager uses the proceeds from the short sale to buy an additional $30mm of attractive stocks. This results in a portfolio that has 130% long and 30% short exposure to stocks, or “extended” exposure to equities relative to a long-only, 100% stock portfolio.

Note: It’s important to point out that here is the risk of theoretical unlimited amount of loss with short selling, (i.e. the price of the short-sold stocks increases; the long position can only go down to $0).

Classic Definition: A doctor announces to her hospitalized patient that there will be a painful medical test sometime during the following week. The patient begins to speculate about when it might occur, until another patient announces that there is no reason to worry because a medical surprise test is impossible.

The test cannot be given on Friday, because by the end of the day on Thursday we would know that the test must be given the next day. Nor can the test be given on Thursday, because, given that we know that the test cannot be given on Friday, by the end of the day on Wednesday we would know that the test must be given the next day. And likewise for Wednesday, Tuesday, and Monday!

Modern Circumstance: The patient spends a restful weekend not worrying about the test, yet is very surprised when it is given on Wednesday. How could this happen?

Paradox Example: There are various versions of this paradox; one of them, called the Hangman, concerns a condemned prisoner who is clever but ultimately overconfident. The implications of the paradox are as yet unclear, and there is virtually no agreement about how it should be solved.

Yield: For bonds and other fixed-income securities, yield is a rate of return on those securities. There are several types of yields and yield calculations. “Yield to maturity” is a common calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity.

Yield curve: A line graph showing the yields of fixed income securities from a single sector (such as Treasuries or municipals), but from a range of different maturities (typically three months to 30 years), at a single point in time (often at month-, quarter- or year-end). Maturities are plotted on the x-axis of the graph, and yields are plotted on the y-axis. The resulting line is a key bond market benchmark and a leading economic indicator.

Yield to maturity [real yield to maturity]: Yield to maturity is a common performance calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity. Real yield to maturity is simply yield to maturity minus any “inflation premium” that had been added/priced in. (See Real yield.)

Yield ratio: A ratio of one yield divided by another. Most often used as a relative value measurement.

Yield spread: A “spread,” in fixed income parlance, is simply a difference. Yield spreads measure yield differences, typically between debt securities with high credit ratings (which typically have lower yields) and those with lower ratings (which typically have higher yields). Yield spreads can also be measured between debt securities with different maturities (shorter-maturity securities typically have lower yields and longer-maturity securities typically have higher yields).

Yield trap: An investment that can lure investors with an attractive yield that may not be fundamentally sustainable, or that may lead to undesired price volatility. Yield traps can lurk in both the equity and fixed income markets. They have a tendency to prey on those who can least afford them, including retirement investors looking for increased relative income and stability, who may have been too focused on their income goals and not enough on stability.

Posted on November 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

November 13th, 2024

***

***

World Kindness Day is an international holiday first introduced in 1998 by the World Kindness Movement.

The holiday is devoted to promoting kindness throughout the world, understanding the positive potential of large and small acts of kindness, and unifying together as human beings.

Posted on November 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The operator of the longest-running money laundering machine in dark web history, Bitcoin Fog, has been sentenced to 12 years and six months in US prison. Roman Sterlingov, 36, a Russian-Swedish national, was also ordered to repay more than half a billion dollars accrued from the cryptocurrency mixing service that he ran for a decade between 2011 and 2021.

r Elliott Investment Management is at it again, this time with a $5 billion stake in industrial conglomerate Honeywell. Shares gained 3.87% on the news.

Shopify announced its ninth consecutive quarter of beating analyst revenue expectations, pushing shares up 21.04%.

Bad news is good news: 40% of the workforce at 23andMe is getting laid off to cut costs. Shareholders cheered, and shares climbed 2.17%.

Where’s the beef? Tyson Foods popped 6.55% after announcing strong earnings thanks to higher beef and chicken prices last quarter.

Sentinel One climbed 2.01% after Deutsche Bank analysts upgraded the cybersecurity stock from “hold” to “buy,” noting it should profit from CrowdStrike’s outage earlier this year.

Holding company IAC is considering a spinoff of home improvement services platform Angi (formerly Angie’s List). Nobody liked that: Shares of IAC fell 12.56%, and Angi plummeted 26.34%.

Payments processor Shift4 Payments sank 5.69% after crushing revenue expectations but missing on earnings.

Mosaic dropped 7.74% thanks to Hurricane Milton, which disrupted the fertilizer company’s business across the board.

The S&P 500® index (SPX) fell 17.36 points (–0.29%) to 5,983.99; the Dow Jones Industrial Average® ($DJI) lost 382.15 points (–0.86%) to 43,910.98; and the NASDAQ Composite®($COMP) decreased 17.36 points (–0.09%) to 19,281.40.

The 10-year Treasury note yield added 12 basis points to 4.43%.

The CBOE Volatility Index® (VIX) fell to 14.81, unusual on a day when stocks lost ground.

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Doctors, Facing Another Pay Cut, Call for Permanent Medicare Payment Reform

The Centers for Medicare and Medicaid Services (CMS) is moving forward with a 2.9% cut to physician payments in 2025 despite protest from major industry groups. CMS has finalized the calendar year 2025 Medicare Physician Fee Schedule rule that sets payment rates for next year and also outlines new policies focused on primary care, preserved telehealth flexibilities, and a strengthened Medicare Shared Savings Program (MSSP).

But, provider groups were quick to condemn CMS’ decision to go ahead with the pay cut, which was proposed in the draft rule released in July. In a statement, Bruce Scott, MD, president of the American Medical Association (AMA), pointed out that that while physicians are receiving a 2.8% payment cut next year, medical practice costs for physicians will increase by 3.5% in 2025. After adjusted for inflation, Medicare reimbursement to physicians has decreased 29% since 2001, the AMA says.

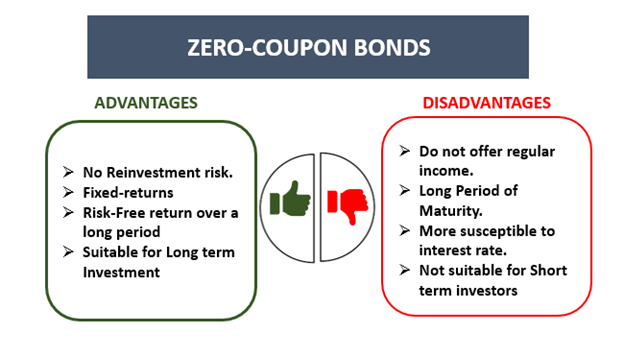

Zero-coupon securities (aka zeros) are debt securities [bonds] that, unlike most of their debt security counterparts, make no periodic interest payments to investors. Instead, they are sold at a deep discount (with an imputed interest rate priced into the discount), then redeemed for their full face value at maturity.

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

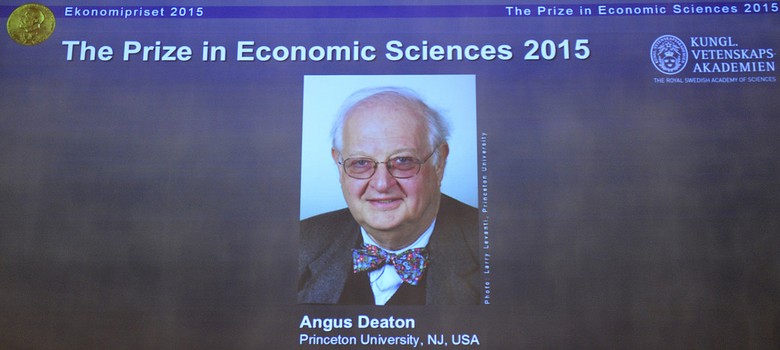

Angus Deaton’s 1980s studies, including one called “Why is consumption so smooth?” gave birth to a concept called the Deaton Paradox — in short, sharp shocks to income didn’t seem to cause similarly large shocks to consumption.

IOW: Consumption varies surprisingly smoothly despite sharp variations in income.

According to David Henderson, this was an important development in understanding the actions of consumers, causing economists to rethink the “permanent income hypothesis” developed by Milton Friedman, which suggested that people spend based on their lifetime income.

And, Mike Bird wrote a good article on Deaton the highlighted the Nobel Prize in Economics Committee.

A paradox is a logic and self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

***

And so, as we plan for our financial future thru a New Year Resolution for 2025, it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

According to Adam Grossman, here are seven [7] of the paradoxes that can bedevil financial decision-making, clients and financial advisors, alike:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds. More:https://tinyurl.com/285vftx4

There’s the paradox that the stock market may appear over valued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as the recent 2024 election results attest.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Classic Definition: Despite rising costs, health care often is of poor quality. Evidence from a classic medical improvement outcomes study assessed care of patients with several chronic diseases. This study found that patients’ functional health status outcomes are similar to care rendered by specialists and generalists but that generalists use far fewer resources. Similar outcome at lower cost represents higher value.

Modern Circumstance: Current solutions to improving care quality may do more harm than good if they focus more on diseases than on people. Efforts to improve the parts (evidence-based care of specific diseases) may not necessarily improve the whole (the health of people and populations).

Expanding access to specialty care, for example, has been proposed as both a source of and a solution for deficiencies in quality of care. Primary care is touted as an essential building block of a high-value health care system even as it is undermined by systems attempting to improve the quality, effectiveness, and value of their health care..

Paradox Example: The above contradictions plague improvement efforts in health care systems around the world, particularly the United States The paradox is that compared with specialty care or with systems dominated by specialty medical care, primary care is associated with the following: (1) poorer quality care for individual diseases, yet (2) similar functional health status at lower cost for people with chronic disease, and (3) better quality, better health, greater health equity and lower costs for whole peoples and populations.

And so, this contradiction plagues improvement efforts in health care systems around the world, particularly the United States.

These are considered to be large developing economies that are part of a global, twenty-first century shift in economic power and influence away from the more established, traditional developed economies of the twentieth century.

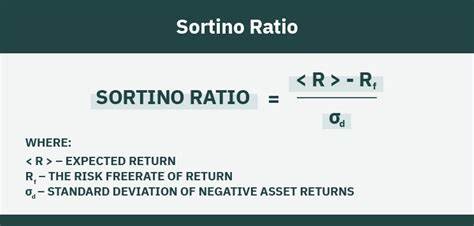

The Sortino Ratio is similar to the Sharpe Ratio, it is a measure of risk-adjusted performance which looks at returns through the lens of the risk taken to achieve that performance, but instead of volatility of return, it uses downside variance as its measure of risk.

Posted on November 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Memory is Fallible. Think you have a great memory? Think again.

According to psychologist and colleague Dan Ariely PhD, memory is more like a game of telephone than a recording device. Each time you recall an event, your brain makes tiny edits, adding some flair or skipping the boring parts. It’s why you can’t remember where you left your keys but can vividly recall an embarrassing moment from high school.

So, the next time someone says, “I remember it like it was yesterday,” know that yesterday might be a heavily edited rerun.

A company that invests in real estate and whose shares trade on a public exchange.

Real Estate Investment Trust (REIT)

A real estate operating company (REOC) is similar to a real estate investment trust (REIT), except that an REOC will reinvest its earnings into the business, rather than distributing them to unit holders like REITs do.

Also, REOCs are more flexible than REITs in terms of what types of real estate investments they can make.

Derivatives are securities whose performance and/or structure is derived from the performance and/or structure of other assets, interest rates, or indexes. If used moderately and in appropriate situations, derivatives can help stabilize portfolios and/or enhance returns. However, if used in excess and/or in inappropriate circumstances, they can be harmful, potentially causing portfolio instability and/or losses. Derivatives are similar to medicine in their behavior–usually safe when used as directed, potentially toxic when abused.

There are many different types of derivative securities and many different ways to use them. Some derivative securities, such as mortgage-related and other asset-backed securities, are in many respects like any other investment, although they may be more volatile or less liquid than more traditional debt securities.

Futures and options are commonly used for traditional hedging purposes to attempt to protect portfolios from exposure to changing interest rates, securities prices or currency exchange rates, and for cash management purposes as a low-cost method of gaining exposure to a particular securities market without investing directly in those securities.

Certain other derivative securities may be described as structured investments. A structured investment is a security whose value or performance is linked to an underlying index or other security or asset class. Structured investments include collateralized mortgage obligations (CMOs). Structured investments also include securities backed by other types of collateral.

According to Wikipedia, a fundamental tenet of the paradox is that the customer, i.e. the potential purchaser of the information describing a technology (or other information having some value, such as facts), wants to know the technology and what it does in sufficient detail as to understand its capabilities or have information about the facts or products to decide whether or not to buy it. Once the customer has this detailed knowledge, however, the seller has in effect transferred the technology to the customer without any compensation. This has been argued to show the need for patent protection [HIPPA].

If the buyer trusts the seller or is protected via contract, then they only need to know the results that the technology will provide, along with any caveats for its usage in a given context. A problem is that sellers lie, they may be mistaken, one or both sides overlook side consequences for usage in a given context, or some unknown-unknown affects the actual outcome.

Posted on November 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Artificial Scarcity refers to the intentional limitation of the availability of a product or resource to create a sense of rarity, which often drives up its perceived value and price.

Think: surge pricing

And, circumstances with insufficient competition can lead to suppliers exercising enough market power to constrict supply. The clearest example is a monopoly, where a single producer has complete control over supply and can extract a additional price.

By creating a temporary shortage, sellers or producers can increase demand and capitalize on consumers’ fear of missing out, thereby influencing market dynamics to their advantage. This strategy is frequently used in marketing, particularly for limited-edition items or high-demand products.

Posted on November 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

FREE SAMPLES

The Art of Giving – And Receiving – Value!

By Staff Reporters

***

***

Imagine you’re at a party, and someone hands you a drink. Your first instinct? Find something to give back. This is [sales] reciprocity in action – our built-in psychological urge to repay kindness.

According to colleague Dan Ariely PhD, it’s like a cosmic balance sheet in our brains, ensuring we don’t owe anyone a favor. This is why companies give out free samples. They’re not just being nice; they know you’ll feel a pang of guilt if you walk away without buying something.

THINK: Free financial planning dinner seminar and prospecting event. That’s you – the Sales Prospect!

So, next time someone does you a favor, remember: it’s not just seller kindness, it’s science!

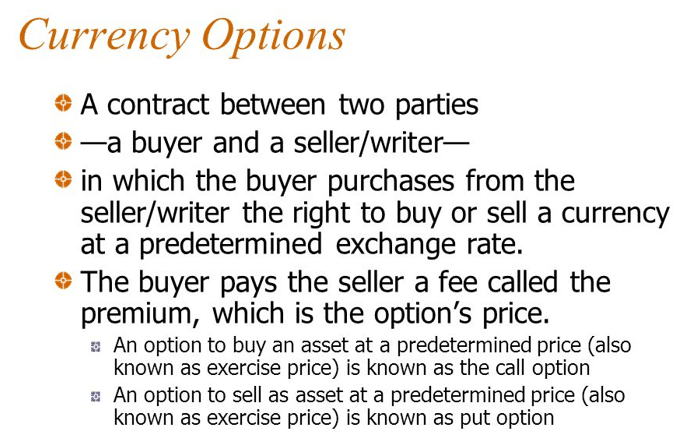

Currency Hedging is a risk-management strategy, as part of a foreign investment strategy, currency hedging is designed to reduce the impact from changes in the relative values of currencies involved in the foreign investment strategy.

In any foreign investment strategy, a significant part of the potential risk and return comes from exposure to relative currency value fluctuations. If exposure to those currency fluctuations is minimized, investors can experience more of a “pure play” exposure to the foreign investments. There is a variety of possible currency hedging strategies, ranging from swaps, options, and spot contracts to simply buying foreign currencies.

Currency Overlay is a financial trading strategy used to separate the management of currency risk from other portfolio strategies. A currency overlay manager can seek to hedge the risk from adverse movements in exchange rates, and/or attempt to profit from tactical currency views.

Stocks surged and stayed higher all yesterday day on news of Donald Trump’s presidential victory. The Dow rocketed over 1,350 points as soon as markets opened, and all three indexes ended the day at record highs.

Treasuryyields have paralleled Trump’s chances of taking the White House for the last few weeks, and his election sent them soaring to over 4.46% at one point today.

Oil and gold both fell as the dollar rose after Trump’s win. The greenback popped on the promise of Trump’s protectionist tariff policies and the lower likelihood of the Fed cutting interest rates as fast as previously expected.

Bitcoin surged as traders celebrated the beginning of the new, friendlier regulatory environment that Trump promised during his campaign.

Posted on November 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The cocktail party effect is the ability of the human hearing and auditory system to focus one’s listening attention on a particular speaker in a noisy environment, such as a crowded party. This allows people to focus on a specific conversation while filtering out other nearby conversations and background noise.

Consider that you’re at a crowded party, noise everywhere, but you hear your name mentioned across the room. How? Welcome to the Cocktail Party Effect.

Your brain is like a highly trained butler, filtering out the background chatter to catch something personally relevant. It’s not just your name, either; it could be juicy gossip or a mention of free pizza or an exciting new stock tip you’ve been considering; or even an IPO.

So, according to psychologist colleague Dan Ariely PhD, this selective attention keeps us sane in a noisy world, helping us focus on the things that matter – like whether that person just said “free drinks” or “freeloading, or “free-stock trading.”

Posted on November 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

One more group of stocks that soared on a Trump election: Big Tech companies with antitrust problems. Another Trump presidency should go a long way toward clearing up the regulatory hurdles many companies have faced recently, which is why Alphabet popped 3.99% and Amazon rose 3.8%.

CVS Health surged 11.33% after meeting revenue forecasts but missing earnings expectations. However, the miss was due to a one-time charge, so shareholders quickly forgave the healthcare retailer.

Planet Fitness gained 6.09% on a surprise bid for bankrupt fitness chain Blink Holdings in an attempt to bolster its own gym business.

Stocks Down

Super Micro Computer had a chance to show the world it wasn’t committing the fraud it has recently been accused of. Instead, the company announced it is still unable to determine when it will file the quarterly report due August 29. Shares crashed 18.05%.

Home builder stocks sank on fears that a Trump presidency will slow the rate of Fed rate cuts, keeping mortgage rates higher for longer. DR Horton fell 3.8%, Lennar dropped 4.84%, PulteGroup lost 3.09%, and TollBrothers tumbled 1.46%.

Cannabis stocks were betting big on a ballot measure in Florida to allow the sale of recreational marijuana. The initiative’s failure sent shares of Curaleaf plummeting 29.17%, TrulieveCannabis plunged 38.8%, and AyrWellness sank 55.87%.

The S&P 500®index (SPX) rose 146.28 points (2.53%) to 5,929.04; the Dow Jones Industrial Average® ($DJI) added 1,508.05 points (3.57%) to 43,729.93; and the NASDAQ Composite®($COMP) gained 544.29 points (2.95%) to 18,983.47—a new closing high.

The 10-year Treasury note yield (TNX) surged 14 basis points to 4.43%, its highest level since July.

The CBOE Volatility Index® (VIX) fell sharply to 16.3 as election-related uncertainty diminished.