BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

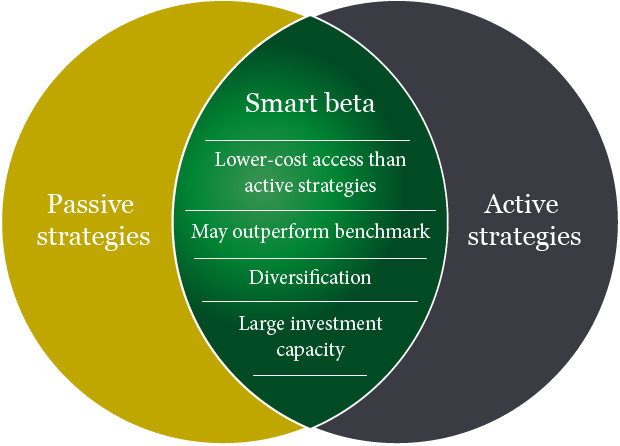

Offering a blend of active and passive styles of management, a smart beta portfolio is low cost due to the systematic nature of its core philosophy – achieving efficiency by way of tracking an underlying index (e.g., MSCI World Ex US). Combining with optimization techniques traditionally used by active managers, the strategy aims at risk/return potentials that are more attractive than a plain vanilla active or passive product.

Originally theorized by Harry Markowitz in his work on Modern Portfolio Theory (MPT), smart beta is a response to a question that forms the basis of MPT – how to best construct the optimally diversified portfolio. Smart beta answers this by allowing a portfolio to expand on the efficient frontier (post-cost) of active and passive. As a typical investor owns both the active and index fund, most would benefit from adding smart beta exposure to their portfolio in addition to their existing allocations.

Assessment: The smart beta approach is an arguably perfect intersection between traditional value investing and the efficient market hypothesis. But, is it worth the cost?

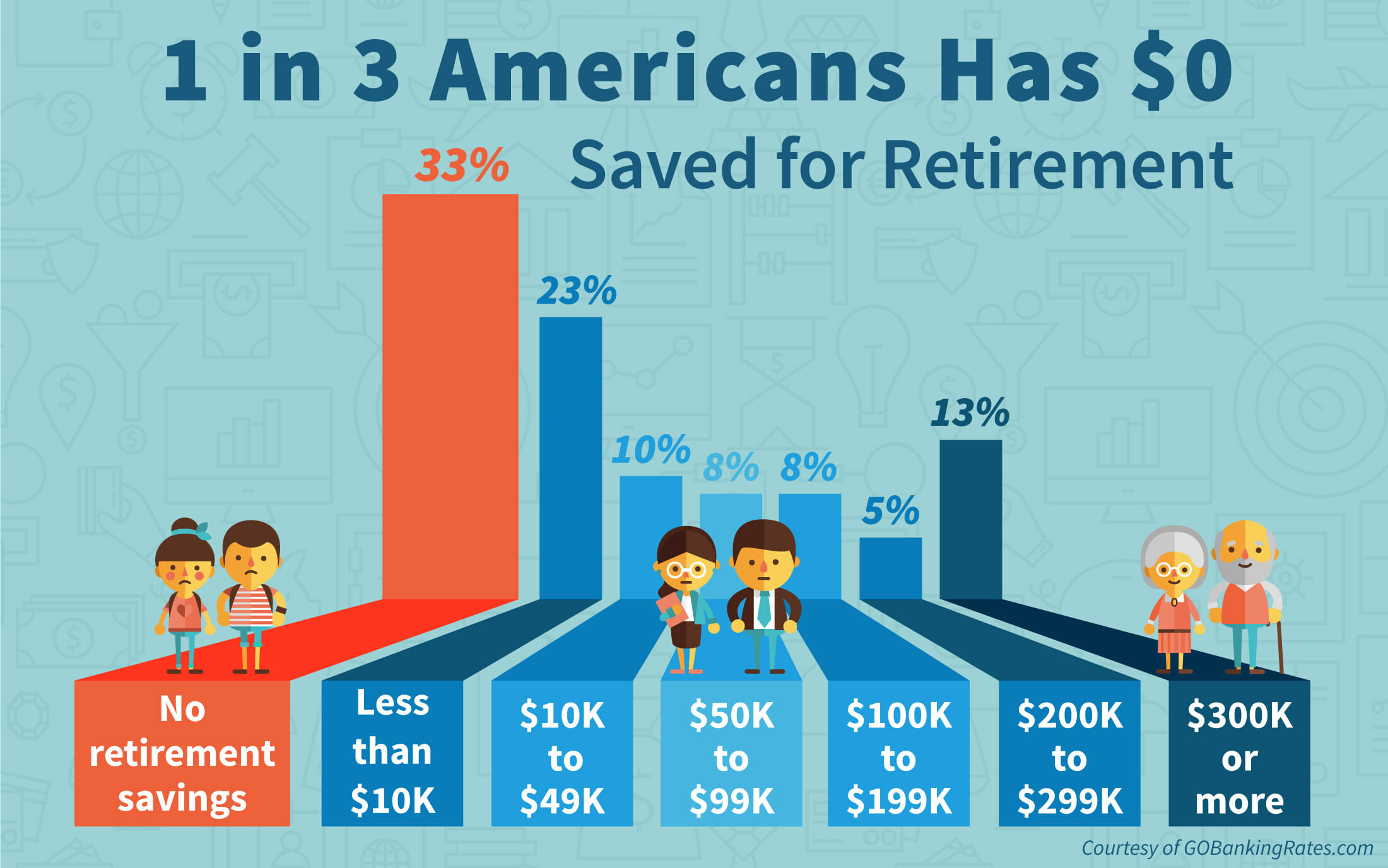

According to the National Institute on Retirement Security, almost 40 million households have no retirement savings at all. The Employee Benefit Research Institute (EBRI) estimates in its 2019 Retirement Security Projection Model that America’s current retirement savings deficit is $3.8 trillion.

What does that mean? Well, the EBRI report aggregates the savings deficit of all U.S. households headed by someone between the ages of 35 and 64, inclusive. In total, those households have $3.8 trillion fewer dollars in savings than they should have for retirement.

For more recent data, Fidelity Investments reported that in the third quarter of 2022 the average account balance for an IRA was $101,900. Employees with a 401(k) averaged $97,200, while those with a 403(b) had $87,400.

Fidelity also estimated that “an average retired couple age 65 in 2022 may need approximately $315,000 saved (after tax) to cover health care expenses in retirement.” Keeping in mind that more Americans are also living longer than ever before, they will face more challenges to cover medical expenses in retirement.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David E. Marcinko MBAMEd CMP

SWARM INTELLIGENCE IN MEDICINE

***

Warm Learning or Swarm Intelligence, is how swarms of bees or birds move in response to their environment.

When applied to data there is “more peer-to-peer communications, more peer-to-peer collaboration, more peer-to-peer learning and that’s the reason why swarm learning will become more and more important as … as the center of gravity shifts” from centralized to decentralized data.

Medicine Example:

Consider this example, “A hospital trains their machine learning models on chest X-rays and sees a lot of tuberculosis cases, but very little of lung collapsed cases. So therefore, this neural network model, when trained, will be very sensitive to what’s detecting tuberculosis and less sensitive towards detecting lung collapse.”

“However, we get the converse of it in another hospital. So what you really want is to have these two hospitals combine their data so that the resulting neural network model can predict both situations better. But since you can’t share that data, swarm learning comes in to help reduce that bias of both the hospitals.”

And this means, “each hospital is able to predict outcomes, with accuracy and with reduced bias, as though you have collected all the patient data globally in one place and learned from it.”

Moreover, it’s not just hospital and patient data that must be kept secure. What swarm learning does is to try to avoid or reduce the sharing of data, or totally prevent the sharing of data, to [a model] where you only share the insights, or you share the learnings.

The science of the modern medical practice valuation can be traced to the Estate of Edgar A. Berg v. Commissioner (T. C. Memo 1991-279). In this case, the Court criticized CPAs as not being qualified to perform business valuations, failing to provide analysis of an appropriate discount rates, and making only general references to justify their “Opinion of Value.”

In rejecting accountants, the Court accepted IRS economists because of background, education and training, as well as discount rate calculations and reproducible evidence applied to the assets being examined. This marked the beginning of the Tax Court leaning toward the side with the most comprehensive appraisal. Previously, it had a tendency to “split the difference.” Now, some feel the Berg case launched the valuation profession; especially for contemporaneous health economists.

But, it was not until after 1995 that the IRS issued guidelines for the valuation of physician practices. As a result, the Uniform Standards of Professional Appraisal Practice [USPAP] requires that a blended constellation of three recognized valuation approaches (income, market, and cost approaches) be considered when estimating fair market value.

Operative Valuation Definitions

When pursuing any discussion of medical practice worth, two key elements must be understood: (1) the valuation process, and (2) fair market value. According to the Dictionary of Health Economics and Finance

Practice valuation is the “the formal process of determining the worth of a healthcare or other medical business entity, at a specific point in time, and the act or process of determining fair market value.”

Fair market value [FMV] is “a legal term generally meaning the price at which a willing buyer will buy, and a willing seller will sell an asset in an open free market with full disclosure.” IRS Revenue Ruling 59-60 clearly states that FMV “is essentially a future prophesy and must be based on facts available at the required date of appraisal”

Unfortunately, the value of a medical practice cannot be directly observed by activity in thinly traded private markets. Perhaps this is why we continually observe the following valuation blunders? They are committed by both sellers and buyers who are pursuing opposite objectives; sale price maximization versus price minimization?

Top 10 Blunders:

Not Understanding What a Medical Practice Valuation Is and Is Not

Valuations are not source document fraud audits.

Valuations are material representations providing a range of transferable worth.

Valuations are reproducible estimates based on economic assumptions.

Valuations are not “back-of-the envelope multiples” using specious benchmarks.

Valuations are defensible and “signed-off” attesting to USPAP/IRS formats.

Financial accounting value [book-value] is not fair market value.

Professional valuators represent only one party at arm’s length; not both sides.

Engagement solicitor and/or valuation payer is the client.

Unbiased valuators do not provide financing or equity-participation schemes. Although not standardized, the Institute of Medical Business Advisors, Inc uses the following three levels that approximate engagement types for the industry.

2. A Limited Valuation lacks additional suggested USPAP procedures. It is considered an “agreed-upon-procedure”, used in circumstances where the client is the only user [i.e., updating a buy-sell agreement, or practice buy-in for a valued associate] and not for external purposes. No onsite visit is needed. A formal Opinion of Value is not rendered.

3. Not Observing Industry Standards, Rules and Regulations

Specifically, in USPAP transactions involving physician practices, the IRS implied:

Ad-Hoc Valuation is low level engagement that provides a gross and non-specific approximation of value based on limited meters by involved parties. Neither a written report, nor an Opinion of Value is rendered. It is often used periodically as an internal organic growth / decline gauge.

A Comprehensive Valuation is an extensive service designed to provide an unambiguous Opinion of Value range. It is supported by all procedures that valuators deem relevant with mandatory onsite review. This “gold-standard” is suitable for contentious situations like divorce, partnership dissolution, estate planning and gifting, etc. The written Opinion of Value is applicable for litigation support activities like depositions and trial. It is also useful for external reporting to bankers, investors, the public and IRS, etc.

4. Not Understanding Engagement Types and Levels

Discounted cash flow (DCF) analysis is the most relevant income approach and must be done on an “after-tax” basis.

Practice collections must be projected based on reasonable assumptions for the practice and market; etc.

Physician compensation must be based on market rates consistent with age, experience and productivity.

Majority premiums and minority discounts are to be considered.Goodwill represents the difference between practice purchase price and the value of the net assets. Personal goodwill results from the charisma, skills and reputation of a specific doctor. Its attributes accrue solely to the individual, are not transferable and can’t be sold. It has little or no economic value as it “goes to the grave” with the doctor. Transferable medical practice goodwill has value, may be transferred, and is defined as the unidentified residual attributes that contribute to the propensity of patients and managed care contracts (and their revenue streams) to return in the future (Schilbach v. Commissioner, T.C. Memo 1991-556). And so, one must also appreciate the: (i) impact of a changing environment; (ii) practice transfer in a local market which can augment or blunt goodwill value; and the (iii) determination of whether patients or HMOs return because of true goodwill, or are mandated by contractual obligations; among many other multi-variable determinants.

Even the Goodwill Registry however, a classic source used to determine the average percentage of revenue contributed to practice goodwill, may be dated for some specialties leading to abnormally high values.

5. Not Understanding the Value of Practice Goodwill: Unlimited life span.

6. Not Understanding the Value of Personal Goodwill: Limited life span.

Now, to further confuse the issue, how each kind of goodwill is allocated in situations like divorce depends on state law. For example, some courts include both kinds of goodwill to be apportioned – some exclude both – and others pursue a case-by-case approach.

7. Not Understanding “Excess Earnings Capitalization”

Another way to determine goodwill value is through “excess earnings capitalization.” This economic method looks at the difference between salary, and what you’d have to pay a comparable doctor replacement.

As an example, when you subtract the numbers, and divide the result by 20%, an important percentage referred to as the Capitalization Rate emerges. The final number gives a dollar value for practice goodwill. Courts seem to prefer this method in divorces because it tends to reflect a practice’s current value.

8. Not Understanding the Present Compensation versus Future Value Paradox

Regardless of practice business model, physician compensation is inversely related to practice value. In other words, the more a doctor takes home in above-average salary, the less the practice is generally worth, and vice versa; ceteris paribus

9. Substituting Benchmarks and Formulas for Practice Specificity

In the stable economic past, industry benchmarks might have been used as quick and inexpensive substitutes for professionally prepared valuations. Muck like preparing one’s own income tax return today – while legal – it is a fraught with peril if challenged. The Courts seem to frown on this simplistic and dated methodology.

Moreover, generic benchmark formulas assume a financial statement reporting standard that just does not exist in public accounting.

Therefore, most every competitive issue that impacts value should be addressed with each practice engagement. This includes, but is not limited to contemporary dislocations by third parties, Medicare and commercial payers; retail clinics and changes in supply/demand and specialty trends; rise of ambulatory surgery centers and specialty hospitals; outsourced care and medical tourism, alterations in resource based-relative value units, APCs, DRGs and newer MS-DRGs; the Medicare Modernization Act, HIPAA, OSHA, EEOC, Sarbanes-Oxley and US Patriot Acts, PP-CA, and ACOs; among other regulations.

Current employee trends to high-deductible health care plans [HD-HCPs] and private concierge medicine must also be considered, as well as demographic and employer shifts to defined contribution plans – from defined benefits plans – to name just a few more complicating issues.

10. Not Aggregating or “Normalizing” Financial Information

Employees may be interviewed and financial information must be gathered before a medical practice can be properly valued. The following data, for the most recent three year period, serves as a starting point:

Sample medical record chart review is increasingly being demanded.

It is especially important to eliminate one-time, non-recurring practice expenses. These are adjusted for excessive or below normal expenses on the profit and loss statement. Such “normalization” can produce a big surprise for benchmark proponents and formula-driven advocates when a selling doctor runs personal expenditures through the practice that a buyer [or Court] wouldn’t consider legitimate. Of course, such shenanigans are less noted using professional USPAP/IRS guidelines. Conversely, you may have to defend legitimate business expenses that an appraiser may seek to normalize. For example, doctors may pay for a vehicle through their practice, but if used to travel between multiple offices and hospitals, the expense may be legitimate. Of course, normalization is a sophisticated and time-intensive process. But, it is where the expert earns his/her professional fee, and defends the resulting valuation range when challenged.The most important credential to look for is fiduciary experience, specificity and independence. Some doctors mistakenly turn to those who may have never appraised a practice before. And, just because an appraiser has initials behind his name, doesn’t mean he understands the peculiarities of medical specialties, especially podiatry. We believe that only an independent health economist, who will be your advocate under Securities Exchange Commission [SEC] fiduciary [not lower “suitability”] guidelines, should be selected. Of course, it is almost impossible to answer concerns regarding fees without specific information. The cost of a valuation can range from $0 (benchmarks-rule of thumb) to $50,000 for an onsite team of experts for behemoth practices and ambulatory surgery centers. Keep in mind that in most cases you want to ensure the value determination will stand up to IRS scrutiny, so the $0 rule-of-thumb is not an optionExternal appraisals, or poorly aggregated financial information, onsite reviews and litigation support services incur additional costs; yet most doctors find the money well spent. Expect to pay a retainer and sign a formal professional engagement letter.

Assessment

Don’t be surprised if a sales-broker does not consider the above issues as the modern health era emerges. Most agent-appraisers are predominantly concerned with earning commissions by working both transaction parties, and may not represent your best interests. And, they are usually not obliged to disclose conflicts-of-interest and don’t provide legal testimony.

As a result, a good medical practice is no longer necessarily a good business; and retiring doctors can no longer automatically expect to extract premium sales prices. Moreover, uninformed young physicians should not be goaded to over-pay. Regardless of your dismay – or delight – in the changing healthcare milieu, always be foreword thinking and remember the admonition, Trust-but Verify, for any business transaction.

But, it is a fait accompli that medical practice worth is presently deteriorating. As the population ages and third-party reimbursements plummet, doctors are commoditized and traditional retail medicine is replaced by more efficient wholesale business models like workplace health clinics. The recent sub-prime mortgage de-fault fiasco, potential tax-reform law expiration and the political specter of a nationalized healthcare system, only adds fuel to the macro-economic fires of uncertainly.

Finally, once practice price is mutually agreed upon, sales contract terms and agreements present a plethora of financing challenges for both involved parties to consider [bank loan payment rates and length, personal promissory guarantees, down-payment offsets, earn-out arrangements, Uniform Commercial Codes-1 asset guarantees, etc] in their due-diligence efforts.

However, most reputable firms use a blended fee-schedule of fixed and hourly rates (plus expenses). So, doctors should expect to spend approximately $5,000-15,000 for an average sized – limited appraisal – that is completely suitable for most internal activities.

Moreover, look-out if the valuation not done at an-arm’s-length and independent manner; or worse still, if it is performed for both parties simultaneously.

Selecting the Wrong Valuator and Not Understanding Professional Fees

Realize too, that the appraiser may also add expenses that have not been incurred; like an office manager’s salary if your spouse is in that role for free. This produces a lower appraised value and is common in small medical practices. Honoraria are another example that does not figure into value calculations.

For example, we recall one doctor who painted his personal residence and wrote it-off as a valid business expense. Deleting other major expenses such as country club memberships, make a practice look more profitable—good news if you’re selling it, bad news if you’re getting a divorce.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Marcinko & Associates is financial guide. We help answer your questions in an empowering way. We educate and guide medical colleagues to understand their financial picture and to make better financial decisions. We strive to simplify everything, clear up confusion, and address specific needs and goals.

Simply put, we’re a financial services company on a mission to empower financial freedom for all healthcare professionals; only. We work with doctors, nurses, medical providers, individuals and all sizes of organizations to offer investment, wealth management and retirement solutions so everyone can have a clear and simple understanding of where their finances and career is today and where it is headed tomorrow.

Whatever your financial situation, we do not shame, criticize, or sell. We enrich, educate and empower. We work only with medical colleagues at every stage of their financial journey [students, interns, residents, practitioners, mid-career and mature physicians], through big life personal changes to annual employment reviews, in order to help them understand, invest, and protect their money and lifestyle.

Assess, develop, and align financial retirement and estate planning goals

Risk Management: Malpractice, home, life, medical, auto and personal indemnity

Life Insurance Need Reviews: whole, universal and term

Business, operations, HR, employment negotiations and medical practice management

Annuity Need Reviews: Indexed and Fixed [Pros and Cons].

***

***

At Marcinko & Associates we discuss specific needs and answer specific questions. We educate and make personalized recommendations that you are free to use, incorporate or disregard. Referrals to trusted specialists and strategic alliance partners then occur if – and as – needed [pro re nata].

Posted on October 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

AVERAGE REVENUE PER CASE

By Staff Reporters

***

Podiatry is 3rd in Average Revenue Per Case in ASCs

***

***

Orthopedic surgery topped the pack for ASC revenue per case, according to VMG Health’s “Multi-Specialty ASC Benchmarking Study” for 2022.

The specialty was only the fourth most-represented among ASC cases, however. Nationally, gastroenterology was the most-represented specialty among ASCs, with 32 percent of all cases, followed by ophthalmology, with 26 percent, and pain management and orthopedics, with 22 and 21 percent, respectively.

The following are some of the most common psychological biases. Some are learned while others are genetically determined (and often socially reinforced). While this essay focuses on the financial implications of these biases, they are prevalent in most areas in life.

[A] Incentives

It is broadly accepted that incenting someone to do something is effective, whether it be paying office staff a commissions to sell more healthcare products, or giving bonuses to office employees if they work efficiently to see more HMO patients. What is not well understood is that the incentives cause a sub-conscious distortion of decision-making ability in the incented person. This distortion causes the affected person – whether it is yourself or someone else – to truly believe in a certain decision, even if it is the wrong choice when viewed objectively. Service professionals, including financial advisors and lawyers, are affected by this bias, and it causes them to honestly offer recommendations that may be inappropriate, and that they would recognize as being inappropriate if they did not have this bias. The existence of this bias makes it important for each one of us to examine our incentive biases and take extra care when advising physician clients, or to make sure we are appropriately considering non-incented alternatives.

[B] Denial

Denial is a well known, but under-appreciated, psychological force. Physicians, clients and professionals (like everyone else) are prone to the mistake of ignoring a painful reality, like putting off an unpleasant call (thus prolonging a problematic situation and potentially making it worse) or not opening account statements because of the desire not to see quantitative proof of losses. Denial also manifests itself by causing human beings to ignore evidence that a mistake has been made. If you think of yourself as a smart person (and what professional doesn’t?), then evidence pointing to the conclusion that a mistake has been made will call into question that belief, causing cognitive dissonance. Our brains function to either avoid cognitive dissonance or to resolve it quickly, usually by discounting or rationalizing the disconfirming evidence. Not surprisingly, colleagues at Kansas State University and elsewhere, found that financial denial, including attempts to avoid thinking about or dealing with money, is associated with lower income, lower net worth, and higher levels of revolving credit.

[C] Consistency and Commitment Tendency

Human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks. In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”. Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake. It is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect. Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

[D] Pattern Recognition

On a biological level, the human brain has evolved to seek out patterns and to work on stimuli-response patterns, both native and learned. What this means is that we all react to something based on our prior experiences that had shared characteristics with the current stimuli. Many situations have so many possible inputs that our brains need to take mental short cuts using pattern recognition we would not gain the benefit from having faced a certain type of problem in the past. This often-helpful mechanism of decision-making fails us when past correlations or patterns do not accurately represent the current reality, and thus the mental shortcuts impair our ability to analyze a new situation. This biologic and social need to seek out patterns that can be used to program stimuli-response mechanisms is especially harmful to rational decision-making when the pattern is not a good predictor of the desired outcome (like short term moves in the stock market not being predictive of long term equity portfolio performance), or when past correlations do not apply anymore.

[E] Social Proof

It is a subtle but powerful reality that having others agree with a decision one makes, gives that person more conviction in the decision, and having others disagree decreases one’s confidence in that decision. This bias is even more exaggerated when the other parties providing the validating/questioning opinions are perceived to be experts in a relevant field, or are authority figures, like people on television. In many ways, the short term moves in the stock market are the ultimate expression of social proof – the price of a stock one owns going up is proof that a lot of other people agree with the decision to buy, and a dropping stock price means a stock should be sold. When these stressors become extreme, it is of paramount importance that all participants in the financial planning process have a clear understanding of what the long-term goals are, and what processes are in place to monitor the progress towards these goals. Without these mechanisms it is very hard to resist the enormous pressure to follow the crowd; think social media.

[F] Contrast

Sensation, emotion and cognition work by contrast. Perception is not only on an absolute scale, it also functions relative to prior stimuli. This is why room temperature water feels hot when experienced after being exposed to the cold. It is also why the cessation of negative emotions “feels” so good. Cognitive functioning also works on this principle. So one’s ability to analyze information and draw conclusions is very much related to the context with in which the analysis takes place, and to what information was originally available. This is why it is so important to manage one’s own expectations as well as those of clients. A client is much more likely to be satisfied with a 10% portfolio return if they were expecting 7% than if they were hoping for 15%.

[G] Scarcity

Things that are scarce have more impact and perceived value than things present in abundance. Biologically, this bias is demonstrated by the decreasing response to constant stimuli (contrast bias) and socially it is widely believed that scarcity equals value. People who feel an opportunity may “pass them by” and thus be unavailable are much more likely to make a hasty, poorly reasoned decision than they otherwise would. Investment fads and rising security prices elicit this bias (along with social proof and others) and need to be resisted. Understanding that analysis in the face of perceived scarcity is often inadequate and biased may help professionals make more rational choices, and keep clients from chasing fads.

[H] Envy / Jealousy

This bias also relates to the contrast and social proof biases. Prudent financial and business planning and related decision-making are based on real needs followed by desires. People’s happiness and satisfaction is often based more on one’s position relative to perceived peers rather than an ability to meet absolute needs. The strong desire to “keep up with the Jones” can lead people to risk what they have and need for what they want. These actions can have a disastrous impact on important long-term financial goals. Clear communication and vivid examples of risks is often needed to keep people focused on important financial goals rather than spurious ones, or simply money alone, for its own sake.

[I] Fear

Financial fear is probably the most common emotion among physicians and all clients. The fear of being wrong – as well as the fear of being correct! It can be debilitating, as in the corollary expression on fear: the paralysis of analysis.

According to Paul Karasik, there are four common investor and physician fears, which can be addressed by financial advisors in the following manner:

Fear of making the wrong decision: ameliorated by being a teacher and educator.

Fear of change: ameliorated by providing an agenda, outline and/or plan.

Fear of giving up control: ameliorated by asking for permission and agreement.

Fear of losing self-esteem: ameliorated by serving the client first and communicating that sentiment in a positive manner.

Now, as human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under-perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

A class action lawsuit has been filed in Minnesota against UnitedHealth Group (NYSE:UNH) over allegations that the health insurer and its subsidiary, NaviHealth, used a faulty algorithm to deny rehabilitation care for Medicare Advantage beneficiaries. California-based Clarkson Law Firm filed the lawsuit in the U.S. District Court of Minnesota on Tuesday following an investigative report published by the health-focused news site Stat.

It alleges that UnitedHealth and its subsidiary, NaviHealth, used the computer algorithm named nH Predict to “systematically deny claims” of patients recovering from debilitating illnesses in nursing homes. According to the lawsuit, despite its 90% error rate, the company used the algorithm to deny claims, knowing that only 0.2% would appeal its decision. According to Stat, Humana (HUM), the nation’s second-largest player in the Medicare Advantage market behind UnitedHealth (UNH), also uses nH Predict. UnitedHealth (UNH) denied it used the NaviHealth predict tool to arrive at coverage decisions.

***

***

Ironically, UnitedHealth’s (NYSE:UNH) Optum Rx unit announced plans to move eight insulin products to “preferred” status on formularies to further expand the number of patients benefiting from $35 or less monthly out-of-pocket costs for the lifesaving therapy.

Optum Rx, UNH’s pharmacy benefit manager (PBM), said that effective January 1, 2024, all short- and rapid-acting insulins will move to Tier 1 in commercial formularies, a list of drugs the company maintains to indicate coverage for insured patients.

According to the Dupont Decomposition Equation – which involves the conglomeration of net operating income, revenues, expenses and average operating assets – ROI and economic profit is increased in three prioritized ways:

Cost and expense reductions.

Revenue increases [Rev]

Reduced average operating assets [AOO]

Note: ROI = NOI / Rev X Rev / AOO

Cost and expense reductions

Although many hospitals have reduced expenses, postponed projects and put clinical or information technology projects on hold because of the current healthcare conundrum, this may be unwise and quality may suffer. And, mental health care programs are almost always the first cost center to be reduced in tough times.

Upgrades today, especially with concurrent marketing and advertising promotions, may well be considered a strategic competitive advantage, and at bargain basement prices for those with cash or credit. This cost reduction is easy because it gives the biggest buck-bang in the ROI equation, and is the first line of ROI augmentation by savvy administrators and CEOs. It is also intuitive and wholly “wrung-out” in the marketplace, to date.

Revenue increases

On the other hand, revenues can usually be only incrementally increased by improving services like emergency care, urgent care, wellness, out-patient and/or surgical departments. This is the more difficult part of the equation and yields a positive, but lesser return in the ROI equation.

The following medical practice procedures will markedly increase upfront office collections:

Train staff to handle exceptions. What is your policy if the patient payment is significant? Will you allow 25% payments—one today and three over the next three months? Communicate your policy to all staff. What will you do if a patient shows up without an insurance card? There will be other exceptions. Train employees to call the appropriate practice-management contact when an exception does not fit in the categories you provide and make sure those managers are responsive.

Understand that not everyone will shine in collections. The value of this new front-desk function should be reflected in job descriptions and wages. Track staff performance and hold employees accountable for collection goals. The most successful practices collect in the 90% range.

Provide professional signage that states your basic policy. “Payments are due at time of service.” Avoid typewritten, lengthy explanations taped to walls or desks that look like clutter.

Reduced average operating assets

Finally, any delay in updating facilities – while easy and may reduce operating assets – there is little ROI advantage and profit potential. Of course, facility asset upgrades mean borrowing funds through tax-exempt bonds – the main source of debt for most hospitals – and is currently difficult or impossible in this climate. Loans from banks, private investors, angels, venture capitalists or other financial institutions are similarly difficult to obtain. Thus, this part of the equation may often be neglected; as is the case now.

“A reliable way to make people believe in falsehoods is frequent repetition, because familiarity is not easily distinguished from truth.” – Daniel Kahneman

As I was watching with interest more [fake] news such as stories surrounding evidence by citations of Russian involvement in US elections and fake prices leading to some violent market gyrations as in Bitcoin and the Corona Virus Pandemic, and societal musings around the thematic of hoaxes … we decided to offer this theme.

Enter the WOOZLE

And so, the Woozle effect, also known as evidence by citation, or a woozle, occurs when frequent citation of previous publications that lack evidence misleads individuals, groups and the public into thinking or believing there is evidence, and non-facts become urban myths and factoids.

Posted on October 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The FTC said it would allow Chevron’s $53 billion purchase of Hess, but it barred Hess CEO John B. Hess from sitting on Chevron’s board over his communications with OPEC.

Soon, students may not need an extra year of college to attain CPA licensure. The AICPA and NASBA have proposed a “competency-based experience pathway” to licensure—with no post-bachelor’s coursework required.

Energy was the top-performing sector in the S&P 500 today thanks to rising fears of fighting between Iran and Israel. APA Corp. rose 4.91%, Halliburton climbed 3.10%, and Occidental Petroleum gained 3.33%.

Defensestocks rose for much the same reason, with Lockheed Martin up 3.66%, NorthropGrumman trading 3.04% higher, and L3Harris Technologies up 3.03%

Hess Corp. and Chevron rose after the FTC declared that, as long as John Hess isn’t allowed to sit on the board, the two companies might be allowed to merge. Shares of Hess gained 2.34%, while Chevron climbed 1.68%.

New Fortress Energy popped 6.49% on the news that it has priced a public offering of 46 million shares at $8.46 per share. That will go a long way to helping the struggling energy stock rake in some much-needed cash.

ArcosDorados, the world’s biggest McDonald’s franchisee, jumped 14.56% after it renewed its agreement with McDonald’s, locking down a flat royalty rate for the next decade.

What’s down

Signet Jewelers fell 7.91% on the news that CEO Virginia Drosos, who has led the company to strong success over the past seven years, will retire.

HP sank 3.09% after Citi analysts downgraded the company based on lower PC and printer demand in the years ahead.

Disney received a rare analyst downgrade today from Raymond James analysts, who think that theme park attendance will continue to slow in the next 12 to 18 months. Shares dropped 2.14%.

Amentum Holdings plummeted 20.16% only a day after the engineering services company debuted on the S&P 500.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX)fell 53.73 points (–0.93%) to 5,708.75; the Dow Jones Industrial Average® ($DJI) declined 173.18 points (–0.41%) to 42,156.97; the NASDAQ Composite® ($COMP) lost 278.81 points (–1.53%) to 17,910.36.

The 10-year Treasury note yield (TNX) fell six basis points to 3.74%.

The CBOE Volatility Index® (VIX) jumped to 19.28, the highest in nearly a month.

The American economy is seemingly fairing so well that UBS has signaled a potential return to the glory days. The European finance giant believes Uncle Sam is inching closer to a ‘Roaring 20s’ scenario, placing the likelihood of an incoming booming economic cycle at 50%. The phrase goes back to the same decade a century ago, when massive economic growth prompted a construction boom and rising prosperity for families.

Today, colleges and universities are beginning to identify students who are adept at learning online and reward top achievers and professors. Employers, graduate and business schools are beginning to troll MOOCs [massive open online courses] seeking viable job, and academic, candidates.

Definition

A massive open online course ( MOOC / m uː k / ) is an online course aimed at unlimited participation and open access via the web. In addition to traditional course materials such as filmed lectures, readings, and problem sets , many MOOCs provide interactive courses with user forums to support community interactions among students, professors, and teaching assistants (TAs) as well as immediate feedback to quick quizzes and assignments.

In fact, when I last checked, the nation’s graduate, B-school and MBA students were enrolled in more than 118 online MBA/MPH/MSH healthcare administration programs. MOOCs offer greater access for a larger number of students, at significantly lower costs than on-site programs.

By the same token, technology like Blackboard®, Cengage, eXplorance, BANNER and Kalture must be used to full potential. Smart phones, PCs and tablets, videos, interactive games, A.I. simulators and apps with Skype®-like virtual classrooms and cloud storage are obvious embellishments to online initiatives.

***

***

Definition

A Moodle is a free and open-source learning management system written in PHP and distributed under the GNU General Public License. Developed on pedagogical principles, Moodle is used for blended learning, distance education, flipped classroom and other e-learning projects in schools, universities, workplaces and other sectors.

Note: PHP is a popular general-purpose scripting language that is especially suited to web development. Fast, flexible and pragmatic, PHP powers everything from your blog to the most popular websites in the world.

Disposablecredit cards are the newest innovation to help reduce fraud and assumed identity scams on e-commerce based websites. As with traditional credit cards, these cards are numbered, but used only once. Then, electronically they are erased so that there is nothing left in the merchant’s database for hackers to steal.

But, in 2014, Congress began looking at new ways to keep personal credit card information safe after several high-profile security breaches at some of America’s top retailers.

WHY? Current credit cards use easy to hack magnetic strip technology from the 1960s. Many consumers want more secure “pin & chip” cards which have been in use in Europe for years. Even though micro-chip technology costs billions to implement, merchants are moving in that direction as they issue new cards to consumers. Most modern polls show nearly half of all people surveyed are extremely concerned about the safety of their personal credit card information.

Burner Cards: Similar to a burner phone or “throwaway” social media account, burner credit cards are temporary, virtual credit cards that are not your “main” credit card. The bank or burner card app will give you a temporary number that links back to your main credit card which you can use for online purchases.

An ANonymousCreditCard provides an extreme degree of privacy and prevents the tracking of your expenses by a spouse, people with bad intentions or government monitoring agencies. It is important to realize that there are plenty of legitimate reasons for wanting to buy something discreetly through an AnonymousCreditCard.

Credit Card Mistakes to Avoid

No number has as far-reaching an impact on your money as your credit scores.

Here are some obstacles, physicians and all of us, should dodge on the road to financial security:

If you are denied a credit card, you have the right to obtain a credit report free from the agency which denied you. Your request must be made in writing and within thirty-sixty days. Consumer credit is governed by the Fair Credit Reporting Act (FCRA). The regulations are issued by and enforced by the Federal Trade Commission. Certain states offer consumers additional rights. Credit reporting agencies are referred to as a “consumer reporting agency”.

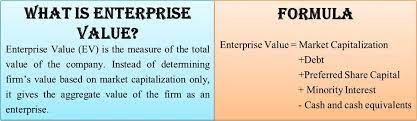

The enterprise value [EV] tends to be thought of as a theoretical takeover price if a company were to be bought. It is calculated as market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents.

Enterprise value = common equity at market value (this line item is also known as “market cap”) + debt at market value (here debt refers to interest-bearing liabilities, both long-term and short-term) + minority interest at market value, if any + preferred equity at market value + unfunded pension liabilities and other debt-deemed provisions – value of associate companies – cash and cash equivalents.

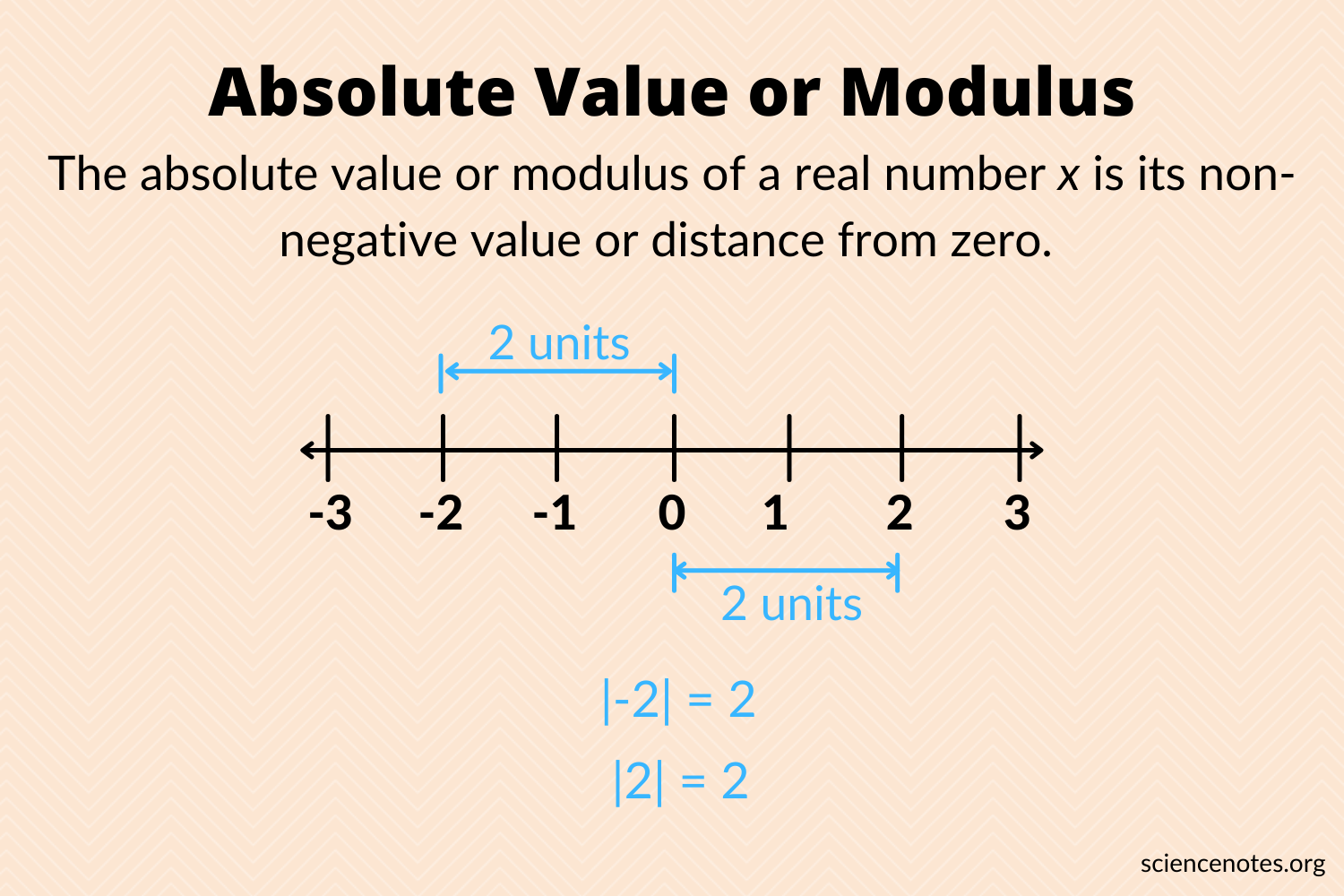

In mathematics, the absolute value or modulus of a real number x, denoted |x|, is the non-negative value of x without regard to its sign. Namely, |x| = x if x is positive, and |x| = −x if x is negative (in which case −x is positive), and |0| = 0. For example, the absolute value of 3 is 3, and the absolute value of −3 is also 3. The absolute value of a number may be thought of as its distance from zero.

***

In finance, absolute value, also known as an intrinsic value, refers to a business valuation method that uses discounted cash flow (DCF) analysis to determine a company’s financial worth. The absolute value method differs from the relative value models that examine what a company is worth compared to its competitors. Absolute value models try to determine a company’s intrinsic worth based on its projected cash flows.

Absolute value refers to a business valuation method that uses discounted cash flow analysis to determine a company’s financial worth.

Investors can determine if a stock is currently under or overvalued by comparing what a company’s share price should be given its absolute value to the stock’s current price.

There are some challenges with using the absolute value analysis including forecasting cash flows, predicting accurate growth rates, and evaluating appropriate discount rates.

Absolute value, unlike relative value, does not call for the comparison of companies in the same industry or sector.

ACOs are groups of doctors, hospitals, and other health care providers, who come together voluntarily to give coordinated high-quality care to their Medicare patients. The goal of coordinated care is to ensure that patients get the right care at the right time, while avoiding unnecessary duplication of services and preventing medical errors.

When an ACO succeeds both in delivering high-quality care and spending health care dollars more wisely, the ACO will share in the savings it achieves for the Medicare program.

Now, suppose that in a new Accountable Care Organization [ACO] contract, a certain medical practice was awarded a new global payment or capitation styled contract that increased revenues by $100,000 for the next fiscal year. The practice had a gross margin of 35% that was not expected to change because of the new business. However, $10,000 was added to medical overhead expenses for another assistant and all Account’s Receivable (AR) are paid at the end of the year, upon completion of the contract.

Cost of Medical Services Provided (COMSP):

The Costs of Medical Services Provided (COMSP) for the ACO business contract represents the amount of money needed to service the patients provided by the contract. Since gross margin is 35% of revenues, the COMSP is 65% or $65,000. Adding the extra overhead results in $75,000 of new spending money (cash flow) needed to treat the patients. Therefore, divide the $75,000 total by the number of days the contract extends (one year) and realize the new contract requires about $ 205.50 per day of free cash flows.

Assumptions

Financial cash flow forecasting from operating activities allows a reasonable projection of future cash needs and enables the doctor to err on the side of fiscal prudence. It is an inexact science, by definition, and entails the following assumptions:

All income tax, salaries and Accounts Payable (AP) are paid at once.

Durable medical equipment inventory and pre-paid advertising remain constant.

Gains/losses on sale of equipment and depreciation expenses remain stable.

Gross margins remain constant.

The office is efficient so major new marginal costs will not be incurred.

Physician Reactions:

Since many physicians are still not entirely comfortable with global reimbursement, fixed payments, capitation or ACO reimbursement contracts; practices may be loath to turn away short-term business in the ACA era. Physician-executives must then determine other methods to generate the additional cash, which include the following general suggestions:

1. Extend Account’s Payable

Discuss your cash flow difficulties with vendors and emphasize their short-term nature. A doctor and her practice still has considerable cache’ value, especially in local communities, and many vendors are willing to work them to retain their business

2. Reduce Accounts Receivable

According to most cost surveys, about 30% of multi-specialty group’s accounts receivable (ARs) are unpaid at 120 days. In addition, multi-specialty groups are able to collect on only about 69% of charges. The rest was written off as bad debt expenses or as a result of discounted payments from Medicare and other managed care companies. In a study by Wisconsin based Zimmerman and Associates, the percentages of ARs unpaid at more than 90 days is now at an all time high of more than 40%. Therefore, multi-specialty groups should aim to keep the percentage of ARs unpaid for more than 120 days, down to less than 20% of the total practice. The safest place to be for a single specialty physician is probably in the 30-35% range as anything over that is just not affordable.

The slowest paid specialties (ARs greater than 120 days) are: multi-specialty group practices; family practices; cardiology groups; anesthesiology groups; and gastroenterologists, respectively. So work hard to get your money, faster. Factoring, or selling the ARs to a third party for an immediate discounted amount is not usually recommended.

3. Borrow with Short-Term Bridge Loans

Obtain a line of credit from your local bank, credit union or other private sources, if possible in an economically constrained environment. Beware the time value of money, personal loan guarantees, and onerous usury rates. Also, beware that lenders can reduce or eliminate credit lines to a medical practice, often at the most inopportune time.

4. Cut Expenses

While this is often possible, it has to be done without demoralizing the practice’s staff.

5. Reduce Supply Inventories

If prudently possible; remember things like minimal shipping fees, loss of revenue if you run short, etc.

6. Taxes

Do not stop paying withholding taxes in favor of cash flow because it is illegal.

Hyper-Growth Model:

Now, let us again suppose that the practice has attracted nine more similar medical contracts. If we multiple the above example tenfold, the serious nature of potential cash flow problem becomes apparent. In other words, the practice has increased revenues to one million dollars, with the same 35% margin, 65% COMSP and $100,000 increase in operating overhead expenses. Using identical mathematical calculations, we determine that $750,000 / 365days equals $2,055.00 per day of needed new free cash flows! Hence, indiscriminate growth without careful contract evaluation and cash flow analysis is a prescription for potential financial disaster.

Once the value of all personal assets and liabilities is known, net worth can be determined with the following formula: Net worth = assets minus liabilities. Obviously, higher is better.

In The Millionaire Next Door, Thomas H. Stanley, PhD, and William H. Danko give the following benchmark for net worth accumulation. Although conservative for physicians of a past generation, it may be more applicable in the future because of current managed care environment. Here is the guide: Multiple your age by your annual pre-tax income from all sources; except inheritances, and then divide by ten.

Example:

As an HMO pediatrician, Dr. Curtis earned $ 90,000 last year. So, if she is 35, her net worth should be at least $ 315,000.

How do you get to that point? In a word, consume less and save more. Stanley and Danko found that the typical millionaire set aside 15 percent of earned income annually and has enough invested to survive 10 years, at current income levels if he stopped working.

Question: If Dr. Curtis lost her job tomorrow, how long could she pay herself the same salary? Could you?

Posted on September 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Why Hospitals, Clinics and Medical Offices are Not Hotels, or Manufacturing Plants or Production Assembly Lines, etc!

By Dr. David E. Marcinko FACFAS, MBA, MEd, CMP™

[Editor-in-Chief]

The rising cost of health insurance remains a major concern for business; despite the Affordable Care Act [ACA] of March 2010. Local and national news publications have trumpeted that healthcare costs are not just rising but are growing in proportion to the cost of other goods and services.

Many of these publications have expressed the widely held view that because of the “inflation gap,” the cost of medical expenses needs curbing. Proponents of this viewpoint attribute the growth in the gross domestic product (GDP) devoted to personal medical services (from 5% in 1965 to approximately 14% in 2005 and 17% in 2012) to increases in both total national medical expenditures as well as prices for specific services, and then conclude that there is a need to rein in the growing costs of healthcare services for the average American, even if it be through a legislative mandate.

Healthcare Is the Economy

According to colleague Robert James Cimasi MHA, AVA, CMP™ of Health Capital Consultants LLC in St. Louis, MO, healthcare cannot be separated from the economy at large. Although economists have cited the aging population as the reason for the increase in healthcare’s share of the GDP, other voices assert that financial greed among HMOs, pharmaceutical companies, hospitals, and medical providers like doctors and nurses is responsible. In reality, the rise in healthcare expenditures is, at least in large part, the result of a much deeper economic force.

As economist William J. Baumol of New York University explained in a November 1993 New Republic article: “the relative increase in healthcare costs compared with the rest of the economy is inevitable and an ineradicable part of a developed economy. The attempt [to control relative costs] may be as foolhardy as it is impossible”.

Baumol’s observation is based on documented and significant differences in productivity growth between the healthcare sector of the economy and the economy as a whole.

Low Productivity Growth

Healthcare services have experienced significantly lower productivity growth rates than other industry sectors for three reasons, according to Cimasi:

1) Healthcare services are inherently resistant to automation. Innovation in the form of technological advancement has not made the same impact on healthcare productivity as it has in other industry sectors of the economy. The manufacturing process can be carried out on an assembly line where thousands of identical (or very similar) items can be produced under the supervision of a few humans utilizing robots and statistical sampling techniques (e.g., defects per 1,000 units). The robot increases assembly line productivity by accelerating the process and reducing labor input. In medicine, most technology is still applied in a patient-by-patient manner — a labor-intensive process. Patients are cared for one at a time. Hospitals and physician offices cannot (and, most would agree, should not) try to operate as factories because patients are each unique and disease is widely variable.

2) Healthcare is local. Unlike other labor-intensive industries (e.g., shoe making), healthcare services are essentially local in nature. They cannot regularly be delivered from Mexico, India or Malaysia. They must be provided locally by local labor. Healthcare organizations must compete within a local community with low or no unemployment among skilled workers for high quality and higher cost labor.

3) Healthcare quality is — or is believed to be — correlated with the amount of labor expended. For example, a 30-minute office visit with a physician is perceived to be of higher quality than a 10-minute office visit. In mass production, the number of work-hours per unit is not as important a predictor of product quality as the skills and talents of a small engineering team, which may quickly produce a single design element for thousands of products (e.g., a common car chassis).

Assessment

Healthcare suffers a number of serious consequences when its productivity grows at a slower rate than other industries, the most serious being higher relative costs for healthcare services. The situation is an inevitable and ineradicable part of a developed economy.

For example, as technological advancements increase productivity in the computer, and eHR, manufacturing industry, wages for computer industry labor likewise increase. However, the total cost per computer produced actually declines. But in healthcare (where technological advancements do not currently have the same impact on productivity), wage increases that would be consistent with other sectors of the economy yield a problem: the cost per unit of healthcare produced increases.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Marcinko & Associates is financial guide. We help answer your questions in an empowering way. We educate and guide medical colleagues to understand their financial picture and to make better financial decisions. We strive to simplify everything, clear up confusion, and address specific needs and goals.

Simply put, we’re a financial services company on a mission to empower financial freedom for all healthcare professionals; only. We work with doctors, nurses, medical providers, individuals and all sizes of organizations to offer investment, wealth management and retirement solutions so everyone can have a clear and simple understanding of where their finances and career is today and where it is headed tomorrow.

Whatever your financial situation, we do not shame, criticize, or sell. We enrich, educate and empower. We work only with medical colleagues at every stage of their financial journey [students, interns, residents, practitioners, mid-career and mature physicians], through big life personal changes to annual employment reviews, in order to help them understand, invest, and protect their money and lifestyle.

Assess, develop, and align financial retirement and estate planning goals

Risk Management: Malpractice, home, life, medical, auto and personal indemnity

Life Insurance Need Reviews: whole, universal and term

Business, operations, HR, employment negotiations and medical practice management

Annuity Need Reviews: Indexed and Fixed [Pros and Cons].

***

***

At Marcinko & Associates we discuss specific needs and answer specific questions. We educate and make personalized recommendations that you are free to use, incorporate or disregard. Referrals to trusted specialists and strategic alliance partners then occur if – and as – needed [pro re nata].

Experts estimate that it can cost more than $1 million to recruit and train a replacement for a doctor who leaves the profession because of burnout. But, as no broad calculation of burnout costs exists, Dr. Tait Shanafelt [Mayo Clinic researcher and Stanford Medicine’s first Chief Physician Wellness Officer] said Stanford, Harvard Business School, Mayo Clinic and the American Medical Association (AMA) are further cost estimating the issue. Nevertheless, Shanafelt and other researchers have shown that burnout erodes job performance, increases medical errors, and leads doctors to leave a profession they once loved.

Fortunately, we can help. From formal coaching to second career opinions, mentoring and advising, we can help with our remediation executive career programs. Regardless of what is happening in your life, it is wonderful to have a non-partial, confidential and informed career coach and sounding board on your side.

CITE: JAMA Internal Medicine [Effect of a Professional Coaching Intervention on the Well-Being and Distress of Physicians].

Did you know that at MARCINKO & Associates, all medical colleagues throughout the United States may contact us when they are considering the sale, purchase, strategic operating improvement, merger, acquisition and/or other financial business or related personal financial planning transaction?

Our difference is “hard” knowledge and insider financial guidance that helps medical colleagues, nurses, private practitioners, clinics, ambulatory surgery, radiology and outpatient wound care centers realize their ultimate economic goals. This typically includes managerial and cost accounting, financial ratio analysis, fair market valuation business appraisals, business plan creation and personal financial planning.

Our “expert witness” business litigation support service and divorce mediation, arbitration, asset division, settlement and second opinion offerings are always available, as well.

And, our “soft” skill professional career guidance and mentoring center includes executive coaching, consulting and mentoring advisory programs for stressed, conflicted or burned-out physicians and medical practitioners.

Most importantly, our professional fees are reasonable and always transparent.

MARCINKO & Associates also serves universities, medical, business, graduate and nursing schools; physicians, dentists, podiatrists, optometrists and legal societies. This includes accountants, financial service providers, wealth and hedge fund managers, emerging entities, hospitals, CEOs and their BODs, the press, media and related organizations.

According to the website, Engage with Grace, we make choices throughout our lives — where we want to live, what types of activities will fill our days, and with whom we spend our time, etc. These choices are often a balance between our desires and our means, but at the end of the day, they are decisions made with intent.

Somehow when we get close to death, however, we stop making decisions. We get frozen in our tracks and can’t talk about our preferences for end of life care.

Death Studies

Studies loom out there — 73% of Americans would prefer to die at home, but anywhere between 20-50% of Americans die in hospital settings. More than 80% of Californians say their loved ones “know exactly” or have a “good idea” of what their wishes would be if they were in a persistent coma, but only 50% say they’ve talked to them about their preferences.

But, end of life experience is about a lot more than statistics. It’s about all of us.

Genesis and Epiphany

In the summer of 2008, Matt Holt (Founder of Health2.0) and Alexandra Drane (President of Eliza) met with some friends for dinner. Over their second cocktail, they got deep into conversation about these very topics. Many of us live with such intent — why do we put the end of our lives in someone else’s control? Why isn’t this topic a conversation that people are having? How could we help start it? And it hit them — What if we could work together to start a viral movement — a movement focused on improving the end of life experience? What if we took responsibility for starting a national (even global) discussion that, until now, most of us haven’t had?

Engage With Grace

The One Slide Project was designed with one simple goal: to help get the conversation about end of life experience started. The idea is simple: Create a tool to help get people talking. One Slide, with just five questions on it. Five questions designed to help get us talking with each other, with our loved ones, about our preferences. And we’re asking people to share this One Slide — wherever and whenever they can… at a presentation, at dinner, at their book club. Just One Slide with five questions to help get all of us talking about death. Just One Slide that we as a community could collectively rally around sharing — in meetings, at a conference, or over a drink.

This is the link to the slide, and this is what we are asking you to do …

Share it any time you can — at the end of presentations, at dinner, or at your book club. Think of the slide as currency and donate just two minutes whenever you can. Commit to being able to answer these five questions about end of life experience for yourself and for your loved ones. Then commit to helping others do the same. Get this conversation started.

Assessment

Let’s start a viral movement driven by the change we as individuals can affect …and the incredibly positive impact we could have collectively. Donate just two minutes to adding just this One Slide to the end of your presentations. Get others involved. Help ensure that all of us — and the people we care for — can end our lives in the same purposeful way we live them.

Just One Slide, just one goal. Think of the enormous difference we can make together.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top

-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Financial advisors don’t ascribe to the Hippocratic Oath. People don’t go to work on “Wall Street” for the same reasons other people become firemen and teachers. There are no essays where they attempt to come up with a new way to say, “I just want to help people.”

Financial Advisor’s are Not Doctors

Some financial advisors and insurance agents like to compare themselves to CPAs, attorneys and physicians who spend years in training and pass difficult tests to get advanced degrees and certifications. We call these steps: barriers-to-entry. Most agents, financial product representatives and advisors, if they took a test at all, take one that requires little training and even less experience. There are few BTEs in the financial services industry.

For example, most insurance agent licensing tests are thirty minutes in length. The Series #7 exam for stock brokers is about 2 hours; and the formerly exalted CFP® test is about only about six [and now recently abbreviated]. All are multiple-choice [guess] and computerized. An aptitude for psychometric savvy is often as important as real knowledge; and the most rigorous of these examinations can best be compared to a college freshman biology or chemistry test in difficulty.

Yet, financial product salesman, advisors and stock-brokers still use lines such as; “You wouldn’t let just anyone operate on you, would you?” or “I’m like your family physician for your finances. I might send you to a specialist for a few things, but I’m the one coordinating it all.” These lines are designed to make us feel good about trusting them with our hard-earned dollars and, more importantly, to think of personal finance and investing as something that “only a professional can do.”

Unfortunately, believing those lines can cost you hundreds of thousands of dollars and years of retirement.

***

***

Suitability Rule

A National Association of Securities Dealers [NASD] / Financial Industry Regulatory Authority [FINRA] guideline that require stock-brokers, financial product salesman and brokerages to have reasonable grounds for believing a recommendation fits the investment needs of a client. This is a low standard of care for commissioned transactions without relationships; and for those “financial advisors” not interested in engaging clients with advice on a continuous and ongoing basis. It is governed by rules in as much as a Series #7 licensee is a Registered Representative [RR] of a broker-dealer. S/he represents best-interests of the firm; not the client.

And, a year or so ago there we two pieces of legislation for independent broker-dealers-Rule 2111 on suitability guidelines and Rule 408(b)2 on ERISA. These required a change in processes and procedures, as well as mindset change.

Note: ERISA = The Employee Retirement Income Security Act of 1974 (ERISA) codified in part a federal law that established minimum standards for pension plans in private industry and provides for extensive rules on the federal income tax effects of transactions associated with employee benefit plans. ERISA was enacted to protect the interests of employee benefit plan participants and their beneficiaries by:

Requiring the disclosure of financial and other information concerning the plan to beneficiaries;

Establishing standards of conduct for plan fiduciaries ;

Providing for appropriate remedies and access to the federal courts.

ERISA is sometimes used to refer to the full body of laws regulating employee benefit plans, which are found mainly in the Internal Revenue Code and ERISA itself. Responsibility for the interpretation and enforcement of ERISA is divided among the Department Labor, Treasury, IRS and the Pension Benefit Guarantee Corporation.

Yet, there is still room for commissioned based FAs. For example, some smaller physician clients might have limited funds [say under $100,000-$250,000], but still need some counsel, insight or advice.

Or, they may need some investing start up service from time to time; rather than ongoing advice on an annual basis. Thus, for new doctors, a commission based financial advisor may make some sense.

Prudent Man Rule

This is a federal and state regulation requiring trustees, financial advisors and portfolio managers to make decisions in the manner of a prudent man – that is – with intelligence and discretion. The prudent man rule requires care in the selection of investments but does not limit investment alternatives. This standard of care is a bit higher than mere suitability for one who wants to broaden and deepen client relationships.

***

***

Prudent Investor Rule

The Uniform Prudent Investor Act (UPIA), adopted in 1992 by the American Law Institute’s Third Restatement of the Law of Trusts, reflects a modern portfolio theory [MPT] and total investment return approach to the exercise of fiduciary investment discretion. This approach allows fiduciary advisors to utilize modern portfolio theory to guide investment decisions and requires risk versus return analysis. Therefore, a fiduciary’s performance is measured on the performance of the entire portfolio, rather than individual investments

Fiduciary Rule

The legal duty of a fiduciary is to act in the best interests of the client or beneficiary. A fiduciary is governed by regulations and is expected to judge wisely and objectively. This is true for Investment Advisors [IAs] and RIAs; but not necessarily stock-brokers, commission salesmen, agents or even most financial advisors. Doctors, lawyers, and the clergy are prototypical fiduciaries.

***

***

More formally, a financial advisor who is a fiduciary is legally bound and authorized to put the client’s interests above his or her own at all times. The Investment Advisors Act of 1940 and the laws of most states contain anti-fraud provisions that require financial advisors to act as fiduciaries in working with their clients. However, following the 2008 financial crisis, there has been substantial debate regarding the fiduciary standard and to which advisors it should apply. In July of 2010, The Dodd-Frank Wall Street Reform and Consumer Protection Act mandated increased consumer protection measures (including enhanced disclosures) and authorized the SEC to extend the fiduciary duty to include brokers rather than only advisors, as prescribed in the 1940 Act. However, as of 2014, the SEC has yet to extend a meaningful fiduciary duty to all brokers and advisors, regardless of their designation.

Ultimately, physician focused and holistic “financial lifestyle planning” is about helping some very smart people change their behavior for the better. But, one can’t help doctors choose which opportunities to take advantage of along the way unless there is a sound base of technical knowledge to apply the best skills, tools, and techniques to achieve goals in the first place.

Most of the harms inflicted on consumers by “financial advisors” or “financial planners” occur not due to malice or greed but ignorance; as a result, better consumer protections require not only a fiduciary standard for advice, but a higher standard for competency.

The CFP® practitioner fiduciary should be the minimum standard for financial planning for retail consumers, but there is room for post CFP® studies, certifications and designations; especially those that support real medical niches and deep healthcare specialization like the Certified Medical Planner™ course of study [Michael E. Kitces; MSFS, MTax, CLU, CFP®, personal communication].

Being a financial planner entails Life-Long-Learning [LLL]. One should not be allowed to hold themselves out as an advisor, consultant, or planner unless they are held to a fiduciary standard, period. Corollary – there’s nothing wrong with a suitability standard, but those in sales should be required to hold themselves out as a salesperson, not an advisor.