BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

“Malta has quietly leveraged the rising tide of the financial transparency imperative to attract hedge funds.“

There was a time when the quaint island sought to play on the traditional terrain, offering anonymity and a “laissez-faire regulatory regime,” not to mention very low taxes, as in no capital gains taxes and no taxes on dividends; all while English speaking and USD currency denominated.

***

***

While many leading domiciles for offshore hedge funds remain in the Caribbean – notably the Cayman Islands, the British Virgin Islands, Bermuda, and the Bahamas – the island of Malta is drawing attention, especially from European funds.

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BANK IDENTIFICATION NUMBER – DEFINED

By Staff Reporters

***

***

What Is a BIN Attack?

The BIN, or the Bank Identification Number, is the first six digits on a credit card. These are always tied to its issuing institution – usually a bank. In a BIN attack, fraudsters use these six numbers to algorithmically try to generate all the other legitimate numbers, in the hopes of generating a usable card number.

How Does a BIN Attack Work?

Fraudsters conduct BIN attacks by generating hundreds of thousands of possible credit card numbers and testing them out.

A fraudster looks up the BIN of the bank they will target. Ranging from four to six digits, this information is in the public domain and is thus easy to source.

Using dedicated software such as an auto-dialer, they generate thousands, often tens of thousands, combinations of possible existing card numbers by this issuer.

At this point, these credentials need to be tested. The fraudster identifies a suitable online shop or donation page.

They start card testing by attempting a small payment with each generated card number.

They keep track of the small percentage of card details that worked, which they are ready to use in earnest for their fraudulent pursuits.

***

***

Remember that the fraudster will start off with only six digits, yet there are many more card details required for a successful transaction. If those are entered erroneously, the transaction will decline. This includes the CVV number, the expiration date, as well as likely address verification service (AVS) failures. Card testing transactions are executed remotely in a fast fashion, so distance checks should also be a hint as well as velocity alerts.

Fraudsters may use bad merchant accounts directly for this purpose, or more frequently involve multiple online stores and services during a BIN attack, as their attempts keep getting blocked at most outlets.

Health actuaries analyze potential risks, profits and trends that will affect their employers, which are often in the health insurance, government health services and medical provider industries. They advise companies on issuing policies to consumers based on risks, calculated premiums and upcoming changes in health-care costs.

It’s common for an actuary to have a bachelor’s degree or higher in actuary studies, mathematics or statistics. Coursework on medical terminology and hierarchy of the medical field is also beneficial. In addition to academic education, certification is also necessary to reach “professional status,” which is required by most employers.

***

***

The professional organization, Society of Actuaries, certifies actuaries in the health and medical field. Their statistical work is commonly done with predictive tables, probability tables and life tables that are created on customized statistical analysis software such as Stata or XLSTAT.

The actuary field as a whole is growing faster than other fields, according to the Bureau of Labor Statistics [BLS]. In 2020, it expanded by 27 percent. The average annual salary for an actuary in 2010 was $87,650. More specifically, in the health insurance field, the salary was slightly higher at $91,000.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

DEFINITION

***

***

According to Wikipedia, a tontine (/ˈtɒntaɪn, -iːn, ˌtɒnˈtiːn/) is an investment linked to a living person which provides an income for as long as that person is alive. Such schemes originated as plans for governments to raise capital in the 17th century and became relatively widespread in the 18th and 19th centuries.

Tontines enable subscribers to share the risk of living a long life by combining features of a group annuity with a kind of mortality lottery. Each subscriber pays a sum into a trust and thereafter receives a periodical payout. As members die, their payout entitlements devolve to the other participants, and so the value of each continuing payout increases. On the death of the final member, the trust scheme is usually wound up.

Tontines are still common in France. They can be issued by European insurers under the Directive 2002/83/EC of the European Parliament. The Pan-European Pension Regulation passed by the European Commission in 2019 also contains provisions that specifically permit next-generation pension products that abide by the “tontine principle” to be offered in the 27 EU member states.

Questionable practices by U.S. life insurers in 1906 led to the Armstrong Investigation in the United States restricting some forms of tontines. Nevertheless, in March 2017, The New York Times reported that tontines were getting fresh consideration as a way for people to get steady retirement income.

According to Patricia Salber MD [personal communication], there are a number of reasons why direct patient access to laboratory medical results is a good idea:

Between 8 and 26% of abnormal test results, including those suspicious for cancer, are not followed up in a timely manner. Direct access could help reduce the number of times this occurs

Self-management, particularly of chronic illness has known benefits. Just like the QS people, many folks with chronic illness obtain and manage to self-acquired lab results every day via gluco-meters, home pulmonary function tests, blood pressure measurements, and so forth. Direct access to laboratory-acquired data, one could argue is a continuation of that personal responsibility

Patients want to be notified about their results in what they perceive as a timely fashion. In one study, patients who received direct notification of their bone density tests results were more likely to perceive they had timely notification compared to usual care even though there was no measurable effect on actual treatment received after three months

Being more responsible for test results could encourage consumers to try to learn more about the meaning of the test results, conceivably increasing their health literacy.

But, the arguments against direct access discussed include the following:

Patients prefer their physicians contact them directly when they have abnormal test results, although the major studies published in 2005 and 2009, preceded the extraordinary use of the internet to access health information that exists today.

There is concern over whether patients will know what to do when they receive the results – will they make erroneous interpretations or fail to contact their docs? This could be, but the intent of the proposed rule is shared access to the results. We suspect if the rule become law, docs will develop better notification mechanisms so that they reach the patient before the patient directly accesses the results or lab companies will design better lab test notifications with easy-to-understand interpretations or a whole new industry will appear that can provide instantly available individualized lab interpretation…or maybe all three of these would happen and that would be a very good thing.

Unknown impact of dual notification (doctors and patients) of lab test results on physician behavior…would docs simply shift responsibility for initiating follow-up care from themselves to their patients?

Would direct access of life-changing lab tests, such as HIV or malignancy, lead to unnecessary patient anxiety – or worse? (Conversely, is there less anxiety, desperation, or suicidal ideation if the bad news is delivered face to face?

Individuals likely may contact their physicians immediately after getting the lab results asking for a telephonic or face-to-face interpretation … it is not known how this would impact physician workload and/or potential for reimbursement [personal communication, Richard Hudson DO, Atlanta, GA].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

1035 Exchange

DEFINITION: A method of exchanging insurance-related assets without triggering a taxable event. Cash-value life insurance policies and annuity contracts are two products that may qualify for a 1035 exchange.

***

A 1035 exchange is a feature in the tax code that permits individuals to transfer funds from an existing life insurance endowment, or annuity policy to a new one without tax consequences.

These transactions are not subject to tax deductions or tax credits but rather tax deferrals, meaning that individuals would only pay taxes on any earnings once they receive money from the policy later.

Without this provision, policyholders would have to close their previous accounts and be subjected to both taxes and surrender charges before they could open a new account.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and IRS

***

***

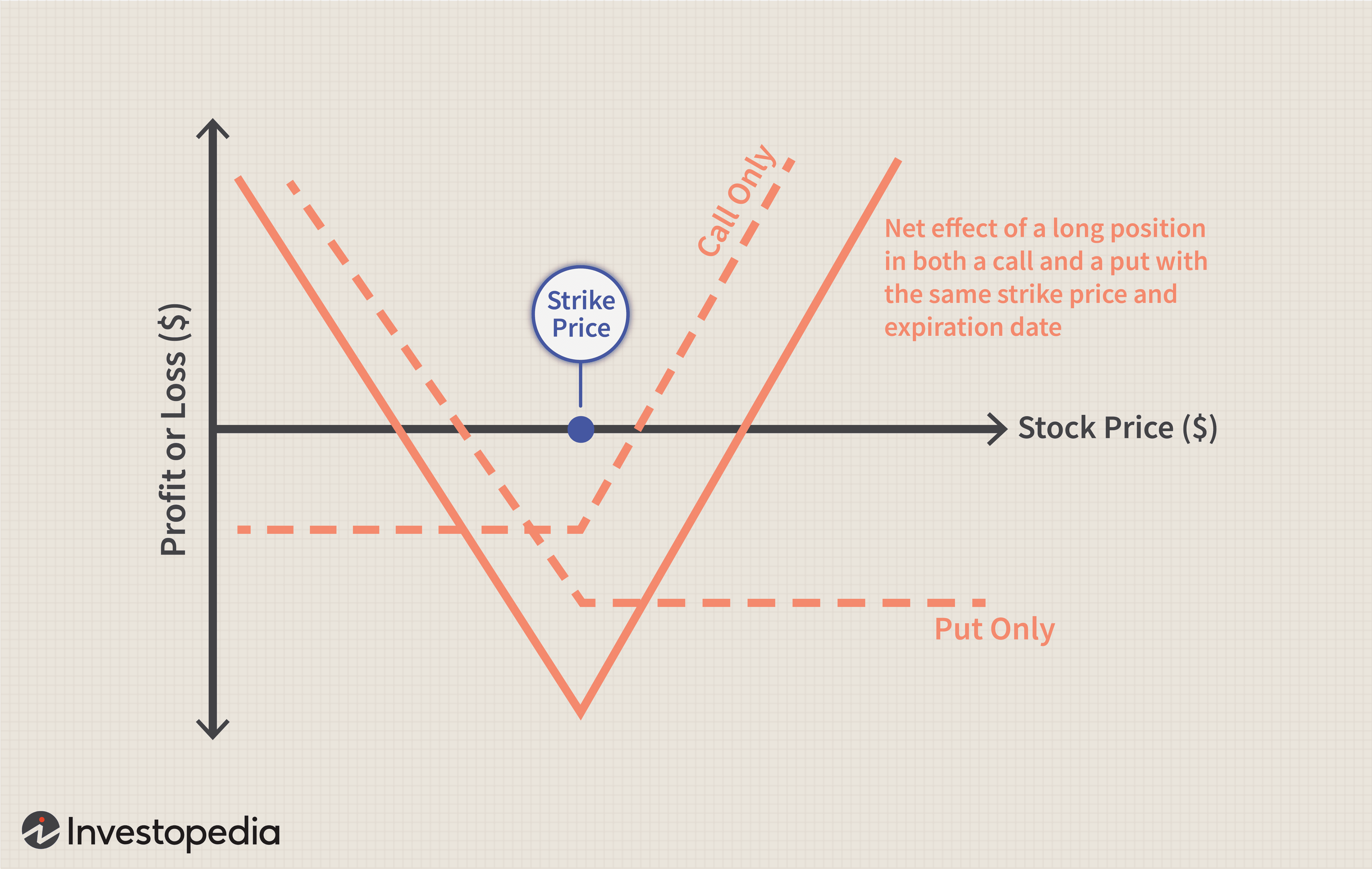

Straddles: A straddle is any set of offsetting positions on personal property. For example, a straddle may consist of a purchased option to buy and a purchased option to sell on the same number of shares of the security, with the same exercise price and period.

Personal property.

This is any actively traded property. It includes stock options and contracts to buy stock but generally does not include stock.

Straddle rules for stock.

Although stock is generally excluded from the definition of personal property when applying the straddle rules, it is included in the following two situations.

The stock is of a type that is actively traded, and at least one of the offsetting positions is a position on that stock or substantially similar or related property.

The stock is in a corporation formed or availed of to take positions in personal property that offset positions taken by any shareholder.

Note

For positions established before October 22, 2004, condition 1 above does not apply. Instead, personal property includes stock if condition 2 above applies or the stock was part of a straddle in which at least one of the offsetting positions was:

An option to buy or sell the stock or substantially identical stock or securities,

A securities futures contract on the stock or substantially identical stock or securities, or

A position on substantially similar or related property (other than stock).

Position

A position is an interest in personal property. A position can be a forward or futures contract or an option.

An interest in a loan denominated in a foreign currency is treated as a position in that currency. For the straddle rules, foreign currency for which there is an active inter bank market is considered to be actively traded personal property.

Offsetting position

This is a position that substantially reduces any risk of loss you may have from holding another position. However, if a position is part of a straddle that is not an identified straddle, do not treat it as offsetting to a position that is part of an identified straddle.

Presumed offsetting positions

Two or more positions will be presumed to be offsetting if:

The positions are established in the same personal property (or in a contract for this property), and the value of one or more positions varies inversely with the value of one or more of the other positions;

The positions are in the same personal property, even if this property is in a substantially changed form, and the positions’ values vary inversely as described in the first condition;

The positions are in debt instruments with a similar maturity, and the positions’ values vary inversely as described in the first condition;

The positions are sold or marketed as offsetting positions, whether or not the positions are called a straddle, spread, butterfly, or any similar name; or

The aggregate margin requirement for the positions is lower than the sum of the margin requirements for each position if held separately.

Related persons

To determine if two or more positions are offsetting, you will be treated as holding any position your spouse holds during the same period. If you take into account part or all of the gain or loss for a position held by a flow-through entity, such as a partnership or trust, you are also considered to hold that position.

RISK MANAGEMENT, LIABILITY INSURANCE AND ASSET PROTECTION ABBREVIATIONS

[Glossary of Important Acronyms]

Much has been written and much has been opined on the topic of medical risk management, insurance, asset protection and professional liability for physicians and healthcare providers in this textbook; and elsewhere.

But occasionally, we all still get lost in a wide array of abbreviations, acronyms, and initialisms that are constantly changing in this ecosystem.

And so, this glossary serves as a ready reference for those who want to know about these medical risk management definitions in a quick and ready fashion.

Acronyms and Abbreviations

AAASC American Association of Ambulatory Surgery Centers

AAHP American Association of Health Plans

ABN advance beneficiary notice

ABQAUR American Board of Quality Assurance and Utilization Review

ACE acute care episode

ACHCE American College of Health Care Executives

ACS American College of Surgeons

ADA Americans with Disabilities Act

ADC average daily census

ADL activities of daily living

ADT Admission/Discharge/Transfer

AHA American Hospital Association

AHIMA American Health Information Management Association

AHRQ Agency for Healthcare Research and Quality

AI average inventory

AIMR Association for Investment Management and Research

AIR assumed interest rate

ALE annualized loss expectancy

ALF assisted living facility

ALOS average length of stay

AMA American Medical Association

AMBAC AMBAC Indemnity Corporation

AMGA American Medical Group Association

ANSI American National Standards Institute

AP accounts payable

APA American Psychiatric Association

APC ambulatory payment classification

APG ambulatory payment group

APR annual percentage rate

AR accounts receivable

ASA American Society of Appraisers

ASC ambulatory surgery centers; also Accredited Standards Committee

ASHA American Surgical Hospital Association

ASO administrative services only

ASTC ancillary service technical component

ATM asynchronous transfer mode

AVG ambulatory visit group

BANTA best alternative to negotiated agreement

BBA Balanced Budget Act of 1997

BBRA Balanced Budget Refinement Act [1999]

BCP business continuity planning

BEA break-even analysis

BEP break-even point

BIPA Benefits Improvement and Protection Act [2000]

BLS Bureau of Labor Statistics

BPD border protection device

BS balance sheet

BSA Bank Secrecy Act

BVS business valuation standard

CA certificate authority

CAC Carrier Advisory Committee

CAS cost accounting standards

CASB Cost Accounting Standards Board

CC common criteria [for IT Security Evaluation —ISO/IEC 15408]; complication or comorbidity [for MS-DRGs]

CCA certified cost accountant

CCC cash conversion cycle

CCEVS common criteria evaluation and validation scheme

CCHIT Certification Commission for Healthcare Information Technology

CCU critical care unit

CDC Centers for Disease Control and Prevention

CDH consumer-directed healthcare

CDHP consumer-directed healthcare plan

CDPM Clinical Data Project Manager

CDSS clinical decision support system

CEO Chief Executive Officer

CF conversion factor

CFA Chartered Financial Analyst

CFO Chief Financial Officer

CFR Code of Federal Regulations

CHAMP Children’s Health and Medicare Protection Act of 2007

CHAMPUS Civilian Health and Medical Program of the Uniformed Services

CHE Certified Healthcare Executive

CHIPS Center for Healthcare Industry Performance Studies

CIA Corporate Integrity Agreement

CIO Chief Information Officer

CIP Customer Identification Program

CIS computer information systems

CLIA Clinical Laboratory Improvement Act

CLT capitation liability theory

CME continuing medical education

CMI case mix index

CMIO Chief Medical Information Officer

CMIS contribution margin income statement

CMN Certificate of Medical Necessity

CMP Certified Medical Planner ™

CMS Centers for Medicare and Medicaid Services [formerly HCFA]

COD cash on delivery

COGME Council of Graduate Medical Education

COH cash on hand

COLA cost of living allowance

CON Certificate of Need

COO Chief Operating Officer

COSO Committee of Sponsoring Organizations

COTS commercial off-the-shelf

CPHQ Certified Physician in Healthcare Quality

CPIM Certificate in Production and Inventory Management

CPI-U Consumer Price Index—urban

CPM critical (clinical) path method

CPOE computerized physician order entry [system]

CPR computer-based patient record

CPT current procedural terminology

CQI continuous quality improvement

CRL Certification Revocation List

CRM customer relationship management

CRVS California Relative Value Studies

CSO Chief Security Officer

CT scan computed tomography scan [also called CAT scan]

CUSIP Committee on Uniform Security Identification Procedures

Candid CIO: Will Weider, CIO of Ministry Health Care and Affinity Health System, offers his perspectives on administration issues in this blog.

Christina’s Considerations: Christina Thielst is a hospital and healthcare administrator and entrepreneur with a deep desire for continually improving the health of the community being served. This is her blog.

Healing Hospitals — Formerly Ask a Hospital President: F. Nicholas “Nick” Jacobs has more than 20 years experience in hospital management, with an acknowledged reputation for innovation and consumer-centered leadership.

Hospital Impact: Part of the Fierce network of health sites, this site is becoming popular among healthcare administrators for its news updates, tips and opinions on health care matters.

Leading the Way to Medical Excellence: the president of McLeod Health non-profit institutions provides weekly insights into his facilities and health care in general.

Let’s Talk Health Care: Bruce Bullen, Interim Chief Executive Officer at Harvard Pilgrim in Massachusetts, provides and open and ongoing conversation about health care administration.

Life as a Healthcare CIO: Dr. John Halamka records his experiences with infrastructure, applications, policies, management, and governance as he supports 3,000 doctors, 18,000 faculty and about three million patients.

Managed Care Matters: Joe Paduda shares his knowledge on managed care for group health, health policy, health research, and medical news for insurers, employers, and healthcare providers.

More than Medicine: Tom Quinn, president and CEO of Community General Hospital in Syracuse, New York, began his career as a hospital kitchen worker. His perspective on administration reflects his knowledge on how hospitals work from every angle.

Running a Hospital: A CEO of a large Boston hospital shares thoughts on hospitals, medicine and health care issues.

St. Joseph Medical Center: Chief Executive Officer at St. Joseph Medical Center in Missouri, Mr. Kashman, provides personal insight into administrative matters and general topics.

Todd’s Perspective: Todd Linden, president and CEO of Grinnell Regional Medical Center, offers insights into medical administration and guest bloggers provide insight into various departments.

Wachter’s World: This blog focuses on hospitals, hospitalists, quality, safety, policy and much more from Robert M. Wachter, MD, Professor and Associate Chairman of the Department of Medicine at the University of California, San Francisco.

Legal Matters

Drug and Device Law: This blog contains an attorney’s personal views (and those of several other Dechert attorneys) on topics that arise in the defense of pharmaceutical and medical device product liability litigation.

Drug Injury Watch: Learn more about drug injury lawsuits from an attorney who represents patients and their families.

FDA Law Blog: Hyman, Phelps & McNamara, P.C. is the largest dedicated food and drug law firm in the country. Their knowledge about laws and regulations governing drugs, medical devices, foods, dietary supplements, and cosmetics is helpful to anyone interested in these topics.

Health Care Law Blog: Bob Coffield’s expertise lies in helping businesses and health care providers weave through a variety of state and federal health care regulations and assisting them in business transactions.

Health Plan Law: This site contains information about group health plans, claims administration and related ERISA fiduciary issues. This site also contains tutorials.

HealthBlawg: this is David Harlow’s popular health care law blog, offering expert insights and easy-to-understand analysis.

Healthcare Law Blog: Holland & Hart’s healthcare practice provides insight into this arena, including HIPAA, Stark law, the Anti-kickback Statute and more.

HIPAA Blog: Join in on this discussion of medical privacy issues often buried in “political arcana.”

HIPAA, HiTech & HIT: This updated blog brings insight into legal issues, developments and other pertinent information that relates to the creation, use and exchange of electronic health records.

HIT Blawg: This blog is focused on national health information technology legal trends and current news on this topic.

Home Care Law Blog: Learn more about legal and policy issues in the home health care, private duty and hospice industries from Gilliland & Markette LLP.

Med Law Blog: This law blog focuses on topics that range from compliance to contracts and from employee benefits to HIPAA and HIT.

Physician Law: This blog provides and easy way to stay on top of current news, updates and useful tips relating to legal issues that affect physicians and non-institutional providers.

eHealth and Health IT

Chilmark Research: This blog provides perspectives on key IT trends in the healthcare sector.

davidrothman.net: David is the Information Services Specialist at the Community General Hospital Medical Library, but he also provides great ideas for 2.0 tools and tips for healthcare industry professionals on this blog.

e-CareManagement blog: Vince Kuraitis, owner of Better Health Technologies, LLC, has a passion for disease management and care coordination that dates back to 1995.

e-HealthExpert: A non-profit organization provides a free and open forum to support the development of expertise in the field of eHealth, Healthcare Information Systems, and Health IT (Clinical IT).

eHealth: John Sharp is an IT Manager for a major medical center in Northeast Ohio, with a focus on ehealth, personal health records, Web 2.0 technologies, Windows Sharepoint Services and project management.

Found In Cache: If you would prefer a professional’s take on social media matters, Web sites and all things technological, then follow Ed Bennett, a technology expert for a Maryland medical care system.

Future Health IT: A health IT and EPR advocate from the UK provides a format to discuss the future of health care and IT.

Informaticopia: This UK blogger provides eclectic news and views on health informatics and elearning.

MedGadget: Stay ahead of the gadget curve with this site, which offers information about the newest health care gadgets on the market as well as emerging medical technologies.

Neil Versel’s Healthcare IT Blog: A healthcare journalist’s provides his views on the major segment of the industry he covers — and, he provides a ton of links to other sites as well.

Schwartz Healthcare IT Blog: A variety of authors from Schwartz Communications provide insights into ways to use IT effectively within healthcare facilities.

The Health IT Channel: For a different perspective on IT and EHR as well as other health care issues, watch a few videos at this site.

The Healthcare IT Guy: The CEO of Netspective, a Java/.NET consultancy that specializes in healthcare IT with an emphasis on e-health, EMRs, data integration, and legacy modernization, supplies tips and information for physicians and healthcare administration.

ACKNOWLEDGEMENTS: To Mackenzie H. Marcinko PhD of iMBA Inc., Perry D’Alessio CPA CMP™ [Hon] New York, NY; and Daniel B. Moisand CFP®, Principal for Moisand Fitzgerald Tamayo, Melbourne, FL.

You can also listen to a professional narration of this article on iTunes & online.

ENCORE: March 22, 2004

A basic property of religion is that the believer takes a leap of faith: to believe without expecting proof. Often you find this property of religion in other, unexpected places – for example, in the stock market. It takes a while for a company to develop a “religious” following: only a few high-quality, well-respected companies with long track records ever become worshipped by millions of investors. My partner, Michael Conn, calls these “religion stocks.” The stock has to make a lot of shareholders happy for a long period of time to form this psychological link.

The stories (which are often true) of relatives or friends buying few hundred shares of the company and becoming millionaires have to fester a while for a stock to become a religion. Little by little, the past success of the company turns into an absolute – and eternal – truth. Investors’ belief becomes set: the past success paints a clear picture of the future.

Gradually, investors turn from cautious shareholders into loud cheerleaders. Management is praised as visionary. The stock becomes a one-decision stock: buy. This euphoria is not created overnight. It takes a long time to build it, and a lot of healthy pessimists have to become converted into believers before a stock becomes a “religion.”

Once a stock is lifted up to “religion” status, beware: Logic is out the window. Analysts start using T-bills to discount the company’s cash flows in order to justify extraordinary valuations. Why, they ask, would you use any other discount rate if there is no risk? When a T-bill doesn’t do the trick, suddenly new and “more appropriate” valuation metrics are discovered.

Other investors don’t even try to justify the valuation – the stock did well for me in the past, why would it stop working in the future? Faith has taken over the stock. Fundamentals became a casualty of “stock religion.” These stocks are widely held. The common perception is that they are not risky.

The general public loves these companies because they can relate to the companies’ brands. A dying husband would tell his wife, “Never sell _______ (fill in the blank with the company name).” Whenever a problem surfaces at a “religion stock,” it is brushed away with the comment that “it’s not like the company is going to go out of business.” True, a “religion stock” company is a solid leader in almost every market segment where it competes and the company’s products carry a strong brand name. However, one should always remember to distinguish between good companies and good stocks.

Coca-Cola is a classic example of a “religion stock.” There are very few companies that have delivered such consistent performance for so long and have such a strong international brand name as Coca-Cola. It is hard not to admire the company.

But admiration of Coca-Cola achieved an unbelievable level in the late nineties. In the ten years leading up to 1999, Coca-Cola grew earnings at 14.5% a year, very impressive for a 103-year-old company. It had very little debt, great cash flow and a top-tier management. This admiration came at a steep price: Coca-Cola commanded a P/E of 47.5. That P/E was 2.7 times the market P/E. Even after T-bills could no longer justify Coke’s valuation, analysts started to price “hidden” assets – Coke’s worldwide brand. No money manager ever got fired for owning Coca-Cola.

The company may not have had a lot of business risk. But in 1999, the high valuation was pricing in expectations that were impossible for any mature company to meet. “The future ain’t what it used to be” – Yogi Berra never lets us down. Success over a prolonged period of time brings a problem to any company – the law of large numbers.

Enormous domestic and international market share, combined with maturity of the soft drink market, has made it very difficult for Coca-Cola to grow earnings and sales at rates comparable to the pre-1999 years. In the past five years, earnings and sales have grown 2.5% and 1.5% respectively. After Roberto C. Goizueta’s death, Coke struggled to find a good replacement – which it acutely needed.

Old age and arthritis eventually catch up with “religion stocks.” No company can grow at a fast pace forever. Growth in earnings and sales eventually decelerates. That leads to a gradual deflation of the “religion” premium. For Coke, the descent from its “religious” status resulted in a drop of nearly 20% in the share price – versus an increase of 65% in the broad market over the same time. And at current prices, the stock still is not cheap by any means. It trades at 25 times December 2004 earnings, despite expectations for sales growth in the mid single digits and EPS growth in the low double digits.

It takes a while for the religion premium to be totally deflated because faith is a very strong emotion. A lot of frustration with sub-par performance has to come to the surface.

Disappointment chips away at faith one day at a time. “Religion” stocks are not safe stocks. The leap of faith and perception of safety come at a large cost: the hidden risk of reduction in the “religion premium.” The risk is hidden because it never showed itself in the past. “Religion” stocks by definition have had an incredibly consistent track record. Risk was rarely observed.

However, this hidden risk is unique because it is not a question of if it will show up but a question of when. It is very hard to predict how far the premium will inflate before it deflates – but it will deflate eventually. When it does, the damage to the portfolio can be huge.

Religion stocks generally have a disproportionate weight in portfolios because they are never sold – exposing the trying-to-be-cautious investor to even greater risks. Coca-Cola is not alone in this exclusive club. General Electric, Gillette, Berkshire Hathaway are all proud members of the “religion stock” club as well. Past members would include: Polaroid – bankrupt; Eastman Kodak – in a major restructuring; AT&T – struggling to keep its head above water. That stock is down from over $80 in 1999 to $18 today.

Emotions have no place in investing. Faith, love, hate, and disgust should be left for other aspects of our life. More often than not, emotions guide us to do the opposite of what we need to do to be successful. Investors need to be agnostic towards “religion stocks.” The comfort and false sense of certainty that those stocks bring to the portfolio come at a huge cost: prolonged under performance.

My thoughts today (20+ years later)

This is one of the first investment articles I ever wrote. I had just started writing for TheStreet.com. It’s interesting to read this article more than 20 years later. I am surprised my writing was not as bad as I had feared (though in many cases it was worse than I feared when I read my other early articles).

So much has happened since then – I am a different person today than I was back then. I have two more kids; I have written three more books and a thousand articles. The last two decades were my formative years as an investor and adult.

The goal of the article was not to make predictions but to warn readers that the long-term success of certain companies creates a cult-like following and deforms thinking. In fact, my original article – the one I submitted to TheStreet.com – did not mention any companies other than Coke. The editors wanted me to include more names so that the article would show up on more pages of Yahoo! Finance.

With the exception of Berkshire Hathaway, all of these companies have produced mediocre or horrible returns. In the best case, their fundamental returns in their old age were only a fraction of what they were when these companies were younger and the world was their oyster.

To my surprise, Coke’s stock is still trading at a high valuation. Its business has performed like the old-timer it is, with revenue and earnings growing by only 3–4% a year. The days of double-digit revenue and earnings growth were left in the 80s and 90s, though the high valuation remained.

Posted on March 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Electronic Data Gathering, Analysis, and Retrieval

By Staff Reporters

***

***

EDGAR (Electronic Data Gathering, Analysis, and Retrieval) is an internal database system operated by the U.S. Securities and Exchange Commission (SEC) that performs automated collection, validation, indexing, and accepted forwarding of submissions by companies and others who are required by law to file forms with the SEC. The database contains a wealth of information about the commission and the securities industry which is freely available to the public via the Internet.

In September 2017, SEC Chairman Jay Clayton revealed the database had been hacked and that companies’ data may have been used by criminals for insider trading.

Posted on March 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What is Honeypot?

A Honeypot is a network-attached system used as a trap for cyber-attackers to detect and study the tricks and types of attacks used by hackers. It acts as a potential target on the internet and informs the defenders about any unauthorized attempt at the information system.

Honeypots are mostly used by large companies and organizations involved in cybersecurity. It helps cybersecurity researchers to learn about the different types of attacks used by attackers. It is suspected that even cyber criminals use these honeypots to decoy researchers and spread wrong information. The cost of a honeypot is generally high because it requires specialized skills and resources to implement a system such that it appears to provide an organization’s resources while still preventing attacks at the back end and access to any production system.

Advantages of Honeypot

Acts as a rich source of information and helps collect real-time data.

Identifies malicious activity even if encryption is used.

Wastes hackers’ time and resources.

Improves security.

Disadvantages of Honeypot

Being distinguishable from production systems, it can be easily identified by experienced attackers.

Having a narrow field of view, it can only identify direct attacks.

A honeypot once attacked can be used to attack other systems.

Fingerprinting(an attacker can identify the true identity of a honeypot ).

What is Honeynet?

A honeynet is made up of two or more honeypots connected via a network. Having a linked network of honeypots can be beneficial. It allows organizations to trace how an attacker interacts with a single resource or network point while also monitoring how a hacker moves between network points and interacts with numerous points at the same time.

The goal is to induce hackers to believe that they have successfully breached the network. Having more false network destinations makes the arrangement appear more realistic.

Posted on February 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

VIRAL AUDIO DEBATES

By Staff Reporters

***

***

Auditory Illusions are like magic tricks for your ears. They make you hear things that aren’t there or misinterpret sounds. Think of the famous “Yanny or Laurel” debate – two people hear completely different words from the same audio clip.

NOTE: Yanny or Laurel is an auditory illusion that became popular in May 2018, in which a short audio recording of speech can be heard as one of two words. 53 percent of over 500,000 respondents to a Twitter poll reported hearing a man saying the word “Laurel”, while 47 percent of people reported hearing a voice saying the name “Yanny”. Analysis of the sound frequencies has confirmed that both sets of sounds are present in the mixed recording, but some users focus on the higher-frequency sounds in “Yanny” and cannot seem to hear the lower sounds of the word “Laurel”. When the audio clip is slowed to lower frequencies, the word “Yanny” is heard by more listeners, while faster playback loudens “Laurel.”

According to colleague Dan Ariely PhD, our brains love patterns, sometimes too much, leading us to hear phantom sounds or misinterpret music lyrics. It’s a reminder that our senses are easily fooled, so don’t believe everything you hear.

While health care is not “do-it-yourself,” an informed patient can be an asset. A poorly informed patient, on the other hand, clearly complicates treatment. Assume the responsibility of being the primary information source and educator for your patient. To help deal with a self-diagnosing patient, consider the following as suggested by: David B. Troxel, MD, Medical Consultant to The Doctors Company:

Encourage patients to always check with you about the accuracy of information obtained from external sources. Use the intake time to find out what Internet information the patient has found.

Directly discuss what the patient has read, even if the patient’s external source is a good one in your professional opinion. The exchange enhances your relationship with the patient and can increase treatment compliance. Welcome questions, and help put the patient’s information in the appropriate context.

Provide your patient with a list of Web sites that provide accurate information, such as the Centers for Disease Control and Prevention (www.cdc.gov). Make sure the patient understands the limitations of the Internet.

Document in the patient’s chart your diagnosis, your treatment management plan, and medication prescribed, as well as the reasons behind your decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

“Show Me the Money”

By Staff Reporters

***

***

In some situations, an inheritance might complicate an estate and add to the estate tax burden. If there are sufficient assets and income to accomplish financial goals, more assets are not needed. A disclaimer may be useful. This is an unqualified refusal to accept a gift or inheritance, that is, when you “just say no”. You have decided not to accept a sizable gift made under a will, trust or other document.

When you disclaim the property, certain requirements must be met:

The disclaimer must be irrevocable;

The refusal must be in writing;

The refusal must be received within nine months;

You must not have accepted any interest in the property; and

As a result of the refusal, the property will pass to someone else.

The property passes under the terms of the decedents will, as if you had predeceased the decedent. If the filer of the disclaimer has control, the property will be included in the disclaimant’s estate and can only be passed to another as a gift for as an inheritance. The intent of the disclaimer is to renounce and never take control of the property.

Posted on February 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

ORIGINAL: May 2021 | Matt Cohlmia

As the future of healthcare becomes digitized, the threat of disruption to health systems has never been greater. Despite their best intentions, the flood of new competitors and ever-proliferating modalities of care each compete for patient attention, creating the potential for a fragmented, confusing, and impersonal patient experience. At the same time, health systems possess the breadth of care, the access to data, and the patient trust to become their community’s preferred partner in care.

But to achieve success, they must leverage these resources to create easy to navigate and personalized experiences for their patients, and for the first time ever, those are within reach.

Scambaiters pose as potential victims to waste the time and resources of scammers, gather information useful to authorities, and publicly expose scammers. They may document scammers’ tools and methods, warn potential victims, provide discussion forums, disrupt scammers’ devices and systems using remote access trojans and computer viruses, or take down fraudulent webpages, while some scam baiters simply call scammers to annoy them and waste their time dealing with a scam baiter, therefore allowing scammers less time to scam potential victims.

Some scambaiters are motivated by a sense of civic duty, some simply engage for their own amusement, or a combination of both.

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

LEGIT or NOT?

By Staff Reporters

***

***

A new pathway will result in a degree called the “Doctor of Medical Science” (DMS); this training is designed for someone—not a physician—to practice clinical medicine with all of the privileges afforded to a medical doctor in the discipline of primary care.

Lincoln Memorial University (LMU) recently announced the start of this new program. In a recent press release they stated, “Lincoln Memorial University is pleased to announce a new type of medical training with its launch of the brand new Doctor of Medical Science (DMS) degree. The only one of its kind, this program bridges the gaps between physician and physician assistant (PA) training for the development of a new type of doctoral trained provider to aid Appalacia and other health care shortage areas.”

The DMS will be for Physician Assistants who have at least three years experience in clinical practice. The curriculum will be a two year program and will consist of 50 credits. The first year will have online didactics delivered by clinical and PhD specialists on staff at LMU-DeBusk College of Osteopathic Medicine and other teaching hospitals. The second year will be more online didactics specific to a clinical specialty.

LMU has already received approval for this program from the Southern Association of Colleges and Schools Commission on Colleges.

Posted on February 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

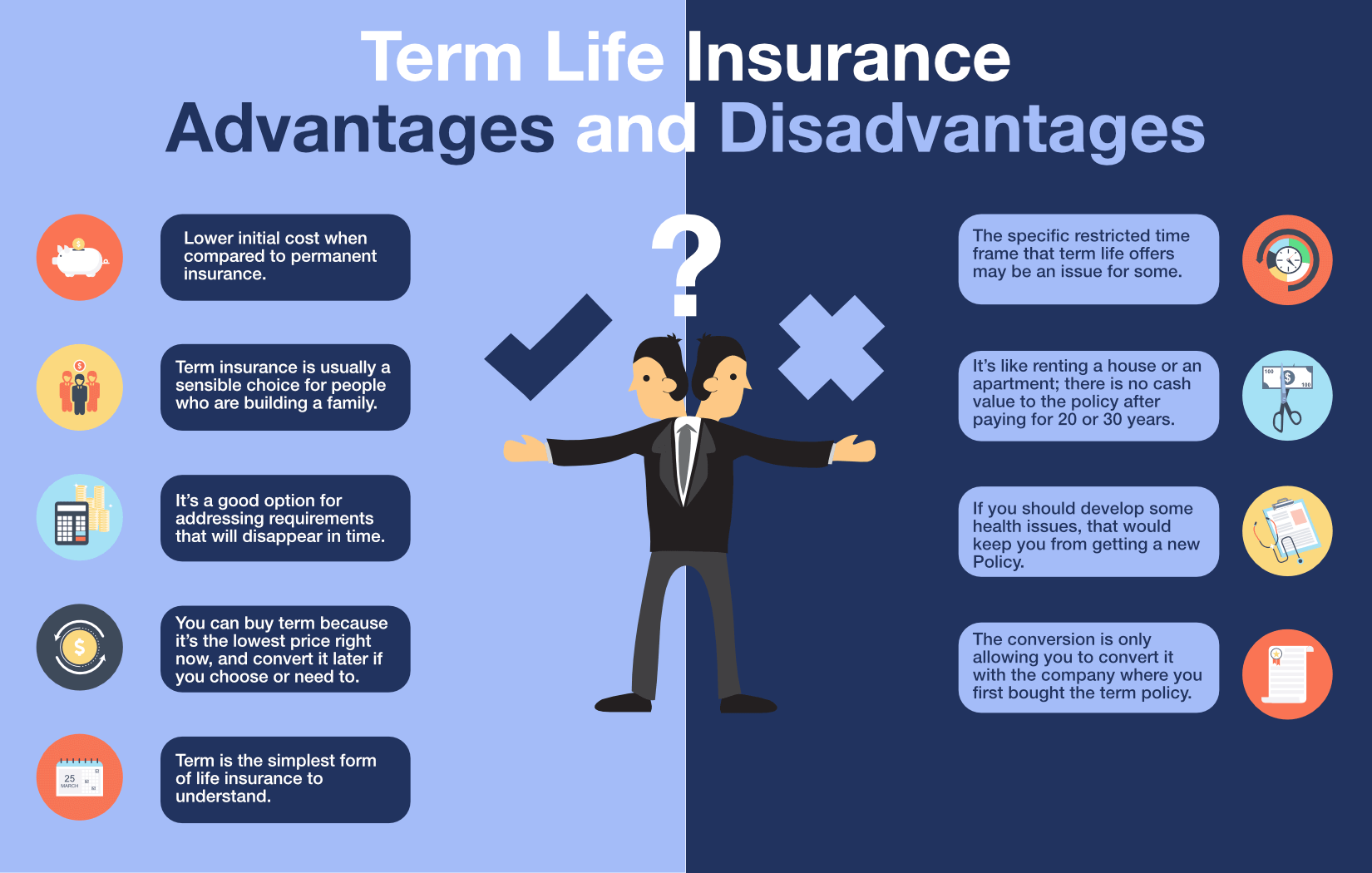

Life Insurance: A contract under which an insurance company promises, in exchange for premiums, to pay a set benefit when the policyholder dies.

Several factors will affect the cost and availability of life insurance, including age, health and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance.

Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Posted on February 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Term Insurance: Life insurance that provides coverage for a specific period. If the policyholder dies during that time, his or her beneficiaries receive the benefit from the policy. If the policyholder outlives the term of the policy, it is no longer in effect. Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased.

Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications.

And, you should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

A certified financial planner (CFP®) helps individuals plan their financial futures. CFPs are not focused only on investments; they help their clients achieve specific long-term financial goals, such as saving for retirement, buying a house, or starting a college fund for their children.

To become a CFP®, a person must complete a course of study and then pass a two-part examination. The exam covers wealth management, tax palnning, insurance, retirement planning, estate planning, and other basic personal finance topics. These topics are all important for someone seeking to help clients achieve financial goals.

Chartered Financial Analyst (CFA)

A CFA, on the other hand, conducts investing in larger settings, normally for large investment firms on both the buy side and the sell side, mutual funds or hedge funds. CFAs can also provide internal financial analysis for corporations that are not in the investment industry. While a CFP® focuses on wealth management and planning for individual clients, a CFA focuses on wealth management for a corporation.

To become a CFA, a person must complete a rigorous course of study and pass three examinations over the course of two or more years. In addition, the candidate must adhere to a strict code of ethics and have four years of work experience in an investment decision-making setting.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

While IAs and FAs may seem the same, they are not the same. The Financial Industry Regulatory Authority (FINRA) and the Securities Exchange Commission (SEC) have clearly defined investment advisors as distinct from financial advisors.

The term financial advisor is a generic one that can encompass many different financial professionals, although it most commonly refers to stock brokers (individuals or companies that buy and sell securities).

Investment advisor, on the other hand, is a legal term and thus has a more clear-cut definition – or at least as clear as legalese is apt to be.

KEY DIFFERENCES:

Financial advisors help with all aspects of your finances, including saving, budgeting, insurance, retirement planning, and taxes.

Investment advisors focus specifically on choosing and managing investment portfolios.

Financial advisors offer broader financial guidance, while investment advisors concentrate solely on investments.

Investment advisors are held to the fiduciary standard, while financial advisors who work as brokers may operate under different rules.

Posted on January 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to colleague Dan Ariely PhD,Pre-Procurement Ownership is when you start to feel ownership over something before you actually have it. It’s like mentally moving into a house or car before you’ve signed the papers and moved in or driven away

This psychological quirk makes us more likely to commit to purchases because we’ve already imagined them as ours. Marketers exploit this by encouraging us to “try before you buy.”

So, next time you’re trying on a new men’s suit or woman’s skirt, be aware: your brain might already be claiming ownership.

Academic Team of Internationally Known Contributors

D. E. Marcinko & Associates is one of the most academically published authorities on the topic of financial planning and private wealth management for physicians, nurses and medical professionals. We have published 33 major peer reviewed textbooks redacted in the Library of Medicine, Institute of Health and the Library of Congress, in four languages, with over 5,025 online white papers, web-posts and related publications. These cover a range of financial planning topics from medical malpractice, risk management and insurance, to investment policy statement analysis and endowment funding management, and to taxation, retirement, estate and legacy planning.

Financial planning, business and strategic management, FMV for practice and clinics and related “hard” topics are included.

***

We also include “soft” subjects from investor psychology, ethics and lost fortunes to luxury spending, from understanding the middle-class millionaire to the political philosophies of physicians and the affluent. Our corpus of work is regularly consulted by doctors, medical, business, graduate and nursing schools, to elite advisors, private and investment bankers, wealth managers, venture capitalists, academics and the press.

Did you know that at MARCINKO & Associates, all medical colleagues throughout the United States may contact us when they are considering the sale, purchase, strategic operating improvement, merger, acquisition and/or other financial business or related personal financial planning transaction?

Our difference is “hard” knowledge and insider financial guidance that helps medical colleagues, nurses, private practitioners, clinics, ambulatory surgery, radiology and outpatient wound care centers realize their ultimate economic goals. This typically includes managerial and cost accounting, financial ratio analysis, fair market valuation business appraisals, business plan creation and personal financial planning.

Our “expert witness” business litigation support service and divorce mediation, arbitration, asset division, settlement and second opinion offerings are always available, as well.

And, our “soft” skill professional career guidance and mentoring center includes executive coaching, consulting and mentoring advisory programs for stressed, conflicted or burned-out physicians and medical practitioners.

Most importantly, our professional fees are reasonable and always transparent.

MARCINKO & Associates also serves universities, medical, business, graduate and nursing schools; physicians, dentists, podiatrists, optometrists and legal societies. This includes accountants, financial service providers, wealth and hedge fund managers, emerging entities, hospitals, CEOs and their BODs, the press, media and related organizations.

At DEMarcinko & Associates an “expert witness” possesses specialized knowledge in a particular field and is qualified to provide deposition or testimony in court and under oath. This testimony can be based on their personal experience, education, training or research. The role of an expert witness is to provide objective and unbiased opinions, analysis, and insights to help a lawyer, judge and/or jury understand technical or complex issues related to the case.

An expert witness can be called by either the prosecution or the defense in a legal case. The expert witness may be required to provide a written report or affidavit detailing their opinions, analyses and conclusions, and they may be asked to testify in court to provide oral testimony and answer questions from the judge and lawyers.

Posted on January 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Institute for Supply Management (ISM) Manufacturing Index. Now, published on a monthly basis, the ISM surveys more than 300 manufacturing firms on employment, production, new orders, supplier deliveries, and inventories.

A composite diffusion index of national manufacturing conditions is constructed, where readings above (below) 50 percent indicate an expanding (contracting) manufacturing sector.

Posted on January 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US stocks largely rose on Monday as chip names popped and investors awaited the release of key monthly jobs data later this week.

The S&P 500 (^GSPC) was up about 0.5%, while the Dow Jones Industrial Average (^DJI) fell about 0.1% after being higher for most of the session. The tech-heavy NASDAQ Composite (^IXIC) led the gains, adding about 1.2%, after a tech-led rally on Friday.

LAS VEGAS (AP) — A vehicle caught fire and exploded Wednesday outside the lobby of President-elect Donald Trump’s hotel in Las Vegas, authorities said.

Las Vegas police said they are investigating the fire and explosion, but neither they nor the Clark County Fire Department immediately provided more details. A county spokeswoman said in a statement that the fire was in the hotel’s valet area and was reported at 8:40 a.m.

Posted on December 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Habituation is your brain’s way of tuning out repetitive stimuli. It’s like background noise – after a while, you stop noticing it. This mental autopilot helps us focus on new and important information, but it can also make us overlook the familiar. It’s why you might not notice a smell in your house that’s obvious to a visitor.

To combat habituation, according to colleague Dan Ariely PhD, try changing up your routine and environment. Fresh experiences keep your brain engaged and alert.

Posted on December 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

DEFINED

***

***

Witness Stress is caused by witnessing a traumatic event and can lead to memory issues and confusion, affecting how accurately we remember details. This stress makes eyewitness testimonies more prone to error.

According to colleague Dan Ariily PhD, it highlights the role of stress in memory distortion and why additional support is often necessary for witnesses.

Posted on December 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHACMP™

INTRODUCING OUR NEXT GENERATION e-BOOK LIBRARYFROM iMBA, Inc.

An e-book is an electronic or digital book that can be read on a computer or a handheld device.

Our new e-books consists of text, images, and are fixed to a specific spot on the page.

And, our e-books are a data files similar in content and structure to a word-processing document that comes in a PDF format. To use our e-books, you need to purchase and download it to a device that has a .pdf file reader app, such as ADOBE® or similar on a smartphone, tablet or computer. A PDF, also known as a portable document format, is the format most people are familiar with and used in our e-books. PDFs are known for their ease of use and ability to hold custom layouts. They are the most commonly used e-Book formats, especially by professionals and adult-learners.

You can then access the e-book and read it, or highlight pages and even take side notes.

e-Books Save Money

With no manufacturing, printing, binding or shipping costs, e-Books are cheaper than traditional hard or paper back books.The price of each specialized and highly niche focused e-Book [50-100 pages] is only $25, whereas similar paperback printed books of this type generally cost $145, or more!

Posted on December 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

An Oft Neglected Chore

[By Dr. David Edward Marcinko MBA MEd]

Hello ME-P Readers!

Doctors and Colleagues – You have probably noticed the weather is getting colder, and you’ve made some changes, right? Thanksgiving is past and X-mass day is nigh! Have you started wearing jackets, packed up the flip-flops, and replaced the A/C with heat?

If you have, that is great, but what have you done to prepare your car for the cold winter months?

Betchya didn’t know that, much like your patients, your car needs to be equally prepared for the colder seasons! It’s a fact—your car reacts to the colder weather in many of the same ways us humans do. Sure, we have blood and skin, where cars have oil and metal, but stay with me here.

There are a few simple things you can do to make sure your trusted car is ready to battle the elements. So; let’s take a quick look at my classic 2000 Jaguar XJ-V8-XL touring sedan; and those pesky winter car tasks.

The List

First of all, your car’s electrical system can take a beating in the cold. The battery has a Cold Cranking Amps (CCA) rating, which should help you determine if it’s powerful enough for those snowy days. The higher the number, the better you’re protected from being stranded. An inspection of your electrical system is always a good idea, though.

Second, you should also consider inspecting the windshield wipers on your vehicle. It’s an easy thing to forget about until you really need them, and then of course they’re worn out. Winter weather, with frost, ice, snow, and dry air can really deteriorate the rubber in wipers.

Third, though it may seem backwards, your vehicle’s cooling system should be in good working condition as well. If the coolant mixture and levels aren’t correct, you could have some very, very expensive repairs waiting for you. Overheating is less of an issue, but your engine actually freezing when not running is a very real, and expensive, danger. And, did you know that your engine’s cooling system also controls your heat inside! A cooling system malfunction could also mean some very cold commutes for you.

Next, headlights are often ignored, too, until you get caught out one night with burnt-out bulbs. With the days getting shorter, and the nights getting much longer and darker, it’s not a bad idea to replace your headlights. Why not upgrade them while you’re at it? The price difference is minimal, and the difference in visibility will make night driving a true joy.

Finally, let’s talk about tires. Some tires are much more suited to winter weather than others! Some tires, especially on performance cars, are rated for summer use only, while others might be “three season” tires. Of course, many cars come standard with all-season tires as well. For those that encounter frequent winter conditions, though, a set of full-winter tires is the best option.

Assessment

Now, just like the patients in your waiting room …. NEXT!

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@outlook.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on December 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Pro hac vice is Law Latin that means “for this time [only]” (literally, “for this turn”). When a lawyer is admitted to a case pro hac vice, a court has granted them a limited license to practice in a jurisdiction where they otherwise would not be licensed to do so.

For example, a lawyer licensed only to practice in California may nonetheless practice in a New York case once a court has granted them admission pro hac vice, so long as the lawyer practices only within the limited scope of their pro hac vice admission. In almost all U.S. jurisdictions, lawyers who practice pro hac vice must do so in conjunction with a local lawyer acting as local counsel. Local counsel typically acts as an anchor to the bar of a foreign jurisdiction, exposing local counsel to liability for the acts or omissions of the lawyer admitted pro hac vice. Local counsel therefore usually assumes, at a minimum, a role of monitoring the lawyer admitted pro hac vice.

Posted on December 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ALMOST ALL ABOUT CREDIT

By Staff Reporters

***

***

Credit Rating and Scoring

The category in which a credit agency classifies you is based upon payment history. Recently, credit reporting agencies have shifted away from ratings to a system known as credit scoring. Your score is determined by proprietary formulas that are based on your credit history, the higher the better. The practical benefits of this scoring system are numerous.

First, medical professionals do not need to be experts at deciphering credit reports since the same scoring system is used by many different companies.

Correcting Credit Report Errors

A credit bureau is not the place to get an item to be fixed on your credit report. Rather, you must take it up directly with the credit issuer. In any case, a late payment noted on a credit report by a durable medical equipment vendor, for example, has to be addressed directly with that merchant. The DME merchant then has 30 days to acknowledge your complaint and respond to you. In the meantime, you do not have to pay for the disputed items. Most credit errors cannot be reported or kept on your credit report for more than seven years.

For legitimate late payments you should contact the credit grantor and negotiate to take one of the following steps. Be tenacious, and either remove the late payment or write a letter explaining that the problem has been resolved and you now are a good credit risk again. This letter is a powerful tool and should be saved with other permanent financial records. The industry term for it is a letter of correction.

Credit Repair Services

Credit repair services are oversold and their claims tend to be exaggerated. They do not have an inside track to the consumer reporting agencies. Good credit repair services are experienced in communicating with creditors and can help with legitimate repairs. They cannot restore your credit rating or your good name.

However, realize that with some time and effort you can accomplish the same results yourself.

Achieving your financial, wealth and medical practice management goals is important, but handling everything on your own can be overwhelming. That’s where we come in. At D. E. Marcinko & Associates, our team of dual degree experienced physician advisors and medical consultants is here to guide you every step of the way. We believe in providing unbiased, high-quality financial and business advice.

For example, we offer a one-time written financial plan with oral evaluation for a flat fee with no ongoing sales or assets under management fees or commissions. Together, we can create a personalized financial plan tailored to your unique goals, empowering you to make confident, informed decisions as you navigate your financial future.

Other Services Include:

Estate Planning We have a network of qualified legal professionals that we can refer you to for state specific estate planning needs.

Tax Strategy We can work alongside your CPA for tax planning purposes. If needed, we can refer you to a qualified tax professional.

Investment Analysis If you have investments, we review your accounts to make sure they are aligned with your long-term goals.

401-k Allocations We evaluate your 401(k) allocations and provide recommendations that align with your goals.

Education Savings We help you explore the various ways to plan and save for education expenses.

Insurance & Risk Management We assess your insurance coverage to ensure it adequately protects you against potential risks; as well as evaluate and provide expert litigation witnesses, as needed.

Medical Practice Management We evaluate your current or potential medical practice to determine value and/or private equity offers or physician practice management formats [PPMC] for new, mid-career or retiring physicians, nurses and dentists.

D. E. Marcinko & Associates is unique and fully committed to all phases of a medical professionals personal and business life cycle. We are at your service 24/7: Email MarcinkoAdvisors@outlook.com

Think of synthetic equity as a communal garden. You don’t own the plot, and you don’t necessarily have a say in what’s planted, but you’re guaranteed a share of the crops that are harvested.

Synthetic equity is a form of deferred compensation that mirrors some of the benefits of real stock ownership without granting actual shares. It’s a contractual agreement between you and your employer that entitles you to a payout upon certain events—such as an IPO, acquisition, or surpassing earnings milestones.

Companies use synthetic equity plans to motivate their personnel through growth-related incentives. In other words, it grants employees a sense of ownership without issuing shares or altering the business’s ownership structure. As the company succeeds and appreciates in value, so does your potential payout. Although you don’t own actual shares of company stock, you are compensated as if you did.

According to Carla McCabe, synthetic equity programs also have a significant tax advantage to both business owners and the key employees.

For example, when a key employee receives shares under the firm’s synthetic equity program, the IRS does not recognize that receipt as taxable income to the employee until he or she actually receives the money. This usually occurs when the firm is sold or when the employee retires and is cashed out (assuming the employee’s synthetic shares are vested). This is very attractive considering that regular shares are taxed as ordinary income and the employee basically has to pay the associated tax even though he or she didn’t receive any cash.

Of course, all this begs the question: Why would a company offer synthetic equity instead of actual equity?

Two years ago, prior to the 2022 election, mental health experts alerted the medical world to their version of an assessment scale for yet another new condition – “doomscrolling.”

As defined by the National Library of Medicine in the article, “Constant exposure to negative news on social media and news feeds could take the form of ‘doomscrolling’ which is commonly defined as a habit of scrolling through social media and news feeds where users obsessively seek for depressing and negative information.”

And so, formally Doomscrolling or doomsurfing is the act of spending an excessive amount of time reading large quantities of news, particularly negative news, on the web and social media. Doomscrolling can also be defined as the excessive consumption of short-form videos or social media content for an excessive period of time without stopping. The concept was coined around 2020, particularly in the context of the COVID pandemic.

Surveys and studies suggest doomscrolling is predominant among youth. It can be considered a form of internet addiction disorder. In 2019, a study by the National Academy of Sciences found that it can be linked to a decline in mental and physical health. Numerous reasons for doomscrolling have been cited, including negativity bias and FOMO [fear of missing out], and attempts at gaining control over uncertainty.

QUERY: What about the roaring stock market, post the 2024 presidential election. Fundamental analysis or FOMO?

Posted on November 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

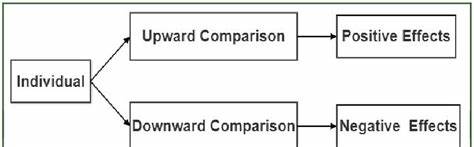

According to some studies, as much as 10 percent of our thoughts involve comparisons of some kind. Social comparison theory is the idea that individuals determine their own social and personal worth based on how they stack up against others. The theory was developed in 1954 by psychologist Leon Festinger. Later research has shown that people who regularly compare themselves to others may find motivation to improve, but may also experience feelings of deep dissatisfaction, guilt or remorse, and engage in destructive behaviors like lying or disordered eating.

***

Downward Comparison is the act of comparing oneself to others who are worse off to feel better about one’s situation. It’s like looking at someone else’s messy desk to feel better about your clutter.

On the other hand, Upward Comparison is the act of comparing oneself to others who are better off to feel bad about one’s situation. It’s like looking at someone else’s neat desk and feel worse about your own clutter.

Finally, according to Dan Ariely PhD, these coping mechanisms boosts self-esteem or depress us with a sense of relief or dread. While helpful in moderation, relying too much on upward or downward comparisons can help hinder personal growth and/or depress growth or empathy; etc.

So, them sparingly and remember: upward comparisons can inspire you to improve and strive for better; while downward comparisons have the opposite effects.

Posted on November 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The proposed Credit Card Competition Act (CCCA) could devastate credit card rewards at the national level if passed. Now, states are getting involved too Read on.

Ross Stores rose 2.19% after beating earnings estimates but missing sales forecasts last quarter, with shoppers spending less thanks to inflation.

MicroStrategy tumbled big time yesterday after a short seller report highlighted the risk inherent in betting it all on bitcoin, but the stock recovered 6.19% today.

Super Micro Computer continues to recover from the brink of defeat, rising another 11.62% as investors beg the tech company’s forgiveness for ever doubting it.

Data analytics company Elastic sprang 14.77% higher today on a strong earnings report highlighted by rising demand from customers building AI applications.

STOCKS DOWN

Tax-filing company Intuit sank 5.68% after reporting strong earnings last quarter but forecasting weaker results this quarter.

Reddit dropped 7.18% after a one-two punch from shareholders: Tencent Holdings sold a chunk of its stake in the social media company, while Advance Magazine Publishers is selling its stake but, through some financial trickery, is keeping control of the shares.

Palo Alto Networks may have beaten earnings expectations yesterday afternoon, but the cybersecurity stock fell 3.61% after shareholders weren’t impressed by its full-year guidance.

The S&P 500® index (SPX) rose 20.63 points (0.35%) to 5,969.34 to end the week up 1.68%; the $DJI gained 426.16 points (0.97%) to 44,296.51 to end the week up 1.96%; and the NASDAQ Composite®($COMP) added 31.23 points (0.16%) to 19,003.65 to end the week up 1.73%.

The 10-year Treasury note yield fell two basis points to 4.41% and is down two basis points for the week, while the 2-year note yield rose seven basis points this week as rate cut odds fell.

The CBOE Volatility Index® (VIX)fell sharply to 15.31 and finished slightly lower for the week.

Posted on November 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***