BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 3, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Even though the Federal Reserve announced its interest rate decision yesterday, Jerome Powell wasn’t the government official investors were most anxious to hear from.

Instead, he was upstaged by Treasury Secretary Janet Yellen, who gave an update on the size of upcoming bond auctions. Although many were concerned about the US selling new debt into a market where interest rates are high and demand for bonds has flagged (pushing yields way up), the market liked what she had to say.

Yellenexplained that the government would focus on shorter-term notes rather than longer-term ones, which prompted a rally for 10 and 30 year bonds.

Merck reported $640 million in sales for its Covid-19 drug, Lagevrio, in Q3 earnings, blowing past analyst expectations of $140.8 million. Covid drug sales have dropped for most big pharma companies this year, with Pfizer lowering its total expected 2023 earnings by about $9 billion due mostly to declining Paxlovid sales. Merck attributed the boost to increasing demand for Lagevrio in Japan.

***

California’s largest health system agreed to a $200 million settlement on October 12th following an investigation that found the system has failed to provide timely behavioral health appointments for patients and has canceled more than 100,000 appointments.

Kaiser Permanente, which also runs a health plan, will “undertake a systemic overhaul” of its behavioral health services, Mary Watanabe, director of the Department of Managed Health Care (DMHC), the regulatory body that oversees managed care plans in California, said in a statement. The DMHC began investigating Kaiser in May 2022 after the Oakland-based health system saw a 20% increase in behavioral health patient complaints in 2021, the DMHC said in a statement.

President President Biden spoke Tuesday afternoon on what the White House has called a crackdown on “junk fees” in retirement planning. Such fees chip away at account balances over time, leading to lifetime savings that are up to 20% less than if advisors were held to the highest standards, according to a White House statement.

Under current regulations, advisors who provide advice to workers rolling their 401(k) or related plan into an individual retirement account are generally not considered a fiduciary—that is, a professional who must put clients’ interests ahead of their own. This means that an advisor could steer an investor into, say, an annuity that pays the advisor a big commission, even if it’s not the best option for the investor. In some cases, commission costs and other fees are baked into the product, as opposed to paid outright, and investors don’t realize that they are silently eating into returns over time.

***

The Federal Reserve left interest rates unchanged Wednesday as it continues to track inflation and the health of the economy. The central bank voted unanimously to leave its primary interest rate in the range of 5.25% to 5.50%. U.S. interest rates are the highest they’ve been in 23 years. That means interest rates on loans such as mortgages have gone up sharply, and so have payments on Treasury bonds and interest-bearing accounts.

Here is where the major benchmarks ended:

The S&P 500 Index was up 44.06 points (1.1%) at 4,237.86; the Dow Jones Industrial Average (DJI) was up 221.71 points (0.7%) at 33,274.58; the NASDAQ Composite was up 210.23 points (1.6%) at 13,061.47.

The 10-year Treasury note yield (TNX) was down about 11 basis points at 4.761%.

CBOE’s Volatility Index (VIX) was down 1.30 at 16.84.

In addition to technology, communication services and utilities were among the strongest sectors Wednesday. Energy shares were under pressure as crude oil futures extended this week’s slump and ended at a two-month low. The U.S. dollar index (DXY) tumbled from an earlier rally to a one-month high, potentially reflecting expectations that domestic interest rates may be near a peak.

Posted on October 24, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

And … Bill Gross Speaks

By Staff Reporters

***

***

The yield on the 10-year Treasury bond shot above 5% in early trading yesterday—hitting its highest since 2007 and rattling investors—before retreating a bit so everyone could chill out. While a high return on long-term government debt sounds like something only a Wall Street wonk would fret about, it can raise borrowing costs for everyone from homebuyers to small businesses.

Treasury yields have been rising steadily for almost two years as investors kept anticipating (correctly) that Jerome Powell would raise interest rates to combat persistent inflation.

Bond yields are used as the measure against which lots of other interest rates are set, so recent sky-high yields have contributed to the current eye-popping mortgage rates, which have made homeownership 52% more expensive than renting, and they’re part of the reason why the number of Americans struggling to make car payments is at its highest since at least 1994.

Yields crossed the symbolically significant 5% mark yesterday because investors rushed to sell off 10-year bonds, making them cheaper, per supply and demand—that boosted the bond yields, since yields move in the opposite direction from price.So, why did Wall Street press “sell” on Treasurys?

It’s usually a sign of confidence in the economy, but some analysts are concerned that this time, investors are shedding government debt because they perceive the US as being a spendthrift as the deficit grows. However, the traditional psychology may also be at play: The influential billionaire investor Bill Ackman is believed to have single-handedly stopped yesterday’s bond market sell-off by saying he’d ended his bet on 30-year Treasury bond prices falling because he thinks there is “too much risk in the world” and the economy isn’t as strong as it seems. The 10-year bonds dropped back to 4.85% yesterday afternoon.

In the last 20 months, the US Federal Reserve has jacked up interest rates to a 22-year high to tame soaring inflation. And inflation has come down to about half of its June 2022 peak. But the economy is still strong.

The Fed’s rate-hiking jamboree was expected to slow hiring, spending, and broader economic growth as unfortunate side effects of popping the inflation balloon. However, a series of recent reports shows that the US economy is still roaring in the ’20s:

Jobs: Employers smashed expectations by adding 336,000 jobs in September, and the unemployment rate remains at a low level of 3.8%.

Spending: Retail sales also blew past estimates in September, a sign that American consumers remain the undisputed shopping world champs. This probably helped: Americans’ household wealth surged 37% from 2019 to 2022, according to Fed data released on Wednesday. That’s more than double the second-highest increase on record.

Economy: After the strong retail sales numbers came out this week, Morgan Stanley raised its Q3 economic growth outlook to 4.9% from 4.5%. Context: One year ago this week, Bloomberg economists predicted a 100% chance of a recession…within a year.

Posted on August 18, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Mortgage rates have climbed to their highest levels in 21 years, according to data released by Freddie Mac on Thursday. The 30-year fixed-rate mortgage averaged 7.09% over the week ending on Thursday, marking a significant increase from 6.96% the week prior, the data showed.

The Federal Reserve has put forward an aggressive string of interest rate hikes as it tries to slash inflation by slowing the economy and choking off demand. That means borrowers face higher costs for everything from car loans to credit card debt to mortgages.

When the Fed imposed its first rate hike of the current series in March 2022, the average 30-year fixed mortgage stood at just 4.45%, Mortgage News Daily data shows.

***

Here is where the major benchmarks ended:

The S&P 500 Index was down 33.97 points (0.8%) at 4,370.36; the Dow Jones Industrial Average (DJIA) was down 290.91 points (0.8%) at 34,474.83; the NASDAQ Composite was down 157.70 points (1.2%) at 13,316.93.

The 10-year Treasury note yield (TNX) was up about 3 basis points at 4.286%.

CBOE’s Volatility Index (VIX) was up 1.22 at 18.00.

Consumer discretionary and retail were among the weakest sectors Thursday. Technology shares were also under pressure, even after Cisco Systems (CSCO) reported better-than-expected quarterly results.

Energy stocks held up somewhat better as crude oil futures rose about 1% after the Energy Department reported an unexpectedly large decline in U.S. supplies.

Posted on July 27, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Whether we’ll see another interest rate increase soon depends on what happens between now and the Fed’s next meeting in September. Jerome Powell will be watching to see if consumer prices come down more than they already have, thanks to previous rate hikes.

There are some promising signs that the worst is behind us:

Tomorrow, when the government releases the latest personal consumption expenditures price index—the Fed’s preferred measure for tracking inflation—it’s expected to show the lowest inflation increase since the end of 2021. And last month, the consumer price index showed inflation fell to 3%, which is above the Fed’s 2% target but an improvement from last June’s 9.1%.

Meanwhile, Coca-Cola—whose prices were 10% higher last quarter compared to Q2 2022—said it’s done marking up drinks for the year, and the CFO of Unilever said the packaged goods giant’s price inflation has peaked (though prices may still get higher).

But the FOMC wants more: Chairman Powell said that for inflation to be truly conquered, the job market, which currently boasts a low unemployment rate of 3.6%, will need to slow.

Posted on July 25, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By StaffReporters

***

***

Recession: Last October, economists surveyed by Bloomberg were predicting a 100% chance of a Recession. But currently, the Dow is riding a 10-day winning streak, and the S&P 500 is just over 5% away from its all-time high. This week, Wall Street will be glued to the Fed’s interest rate announcement and a heavy slate of earnings.

Final Fed rate hike? The Federal Reserve will likely announce another interest rate increase this week, but this could be the final hike in its 16-month quest to bring down inflation. If the Fed hikes 25 basis points as expected, interest rates would be at their highest level since 2001.

Earnings galore: Corporate America’s A-list will report Q2 earnings this week, including Meta, Alphabet, Microsoft, McDonald’s, Coca-Cola, and Exxon Mobil. In all, about one-third of companies in the S&P 500 will give financial updates over the next five days, so we should get a good look into the health of a bunch of different industries.

Posted on July 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to Morning Brew, the US banking system is about to speed up, potentially eliminating those frustrating waiting days it can take for money to hit your account. The Fed is launching its FedNow instant payment service later this month. The new system will enable banks to send each other cash instantly, 24/7, as an alternative to the existing system that runs only during regular business hours and often takes days to move money.

FedNow could put America’s banking system on track to catch up to countries like India and Nigeria, where high-speed payments are as common. The US does already have an instant payments system, but it’s private rather than government-backed, and it hasn’t been widely adopted. It’s mostly only used by big banks, and only 1.4% of US transactions happen in real time, according to payment systems company ACI Worldwide.

FedNow enabled services will soon likely appear at the 41 banks that have been certified to participate so far.

People moving money between banks or paying bills could complete their transactions in seconds without the need to plan payments days in advance.

Businesses will be able to access customer payments immediately and to send workers payments more frequently with instant direct deposit rather than the usual payroll cycle.

BUT … Faster payments could mean faster bank runs, too!

Some experts worry that allowing people to drain their bank accounts instantaneously could make SVB-style bank runs more likely. Smaller banks struggling with liquidity would have even less time to react to customer panic and get collateral for emergency government loans to cover fleeing cash.

But there are safeguards built in. FedNow has a transaction limit of $500,000, and banks can set their own ceilings to ensure that customers don’t pull their deposits.

Posted on June 22, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Wall Street’s major averages yesterday, on Wednesday, ended lower for a third straight session, weighed down by losses in growth stocks. And, sentiment was dampened by Federal Reserve Chair Jerome Powell’s largely hawkish reiteration that more rate hikes were likely.

Powell in his published opening remarks to his two-day testimony to Congress said that nearly all policymakers expect that interest rates would have to be raised further by the end of the year. The Fed chief then, in responses to questions from lawmakers, said that it may “make sense” for the central bank to raise rates at a “more moderate pace” going forward.

***

So, here is where the major benchmarks ended:

The S&P 500 Index was down 23.02 points (0.5%) at 4,365.69; the Dow Jones Industrial Average (DJIA) was down 102.35 (0.3%) at 33,951.52; the NASDAQ Composite was down 165.10 (1.2%) at 13,502.20.

The 10-year Treasury note yield (TNX) was little changed at 3.727%.

Cboe’s Volatility Index (VIX) was was down 0.68 at 13.19.

Technology shares were among the weakest performers Wednesday, with the Philadelphia Semiconductor Index (SOX) dropping nearly 2% to near a two-week low. Regional banks were also lower.

Energy stocks led sector gainers as crude oil futures jumped nearly 2% to a two-week high on hopes for stronger demand from China. Volatility based on the VIX sank to its lowest level since January 2020.

Posted on June 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: A consumer price index (CPI) is a price index, the price of a weighted average market basket of consumer goods and services purchased by households. Changes in measured CPI track changes in prices over time.

1. Energy is doing a lot of the work. Cheaper energy played a major role in pulling inflation down to 4% last month from 4.9% in April, per Axios. Gas prices plunged almost 20% from last year, when Russia’s invasion of Ukraine sent fuel costs to the moon, while broader energy prices fell nearly 12%.

2. “Revenge spending” is down. Once COVID pandemic lock downs lifted, Americans splurged on vacations, leisure, and recreation (new pickle ball paddles!) in what economists dubbed “revenge spending.” Now that everyone has taken their week long trip to Italy, there are signs that revenge spending is waning: Airfare prices dropped 13% annually in May and, according to the US Travel Association, hotel demand is below 2019 levels. Bad for your Instagram, but good for inflation.

3. Food prices are up. The cost of food ticked up 0.2% in May from April after staying flat in the previous two months, showing how inflation has persisted on grocery store shelves. But not all aisles are created equal—the price of eggs dropped nearly 14% from April (the biggest one-month drop since 1951), while fruit and veggie prices rose 1.3%.

4. More than anything else, rent is propping up inflation. Shelter costs are the largest category in the CPI report, and they’re still on the upward march, climbing 8.7% from a year earlier. The good news: Economists say this government data doesn’t reflect on-the-ground information, such as reports of softening rent by Zillow and Apartment List. Shelter costs in the CPI are expected to decline during the second half of the year.

Posted on June 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

FLAG DAY 2023

***

***

Measured year over year, inflation slowed to just 4 per cent in May — the lowest 12-month figure in over two years and well below April’s 4.9 per cent annual rise. The pullback was driven by tumbling gas prices and smaller increases in grocery prices and other items.

***

Here is where the major benchmarks ended, today:

The S&P 500® Index was up 30.08 points (0.7%) at 4,369.01; the Dow Jones industrial average was up 145.79 (0.4%) at 34,212.12; the NASDAQ Composite was up 111.40 (0.8%) at 13,573.32.

The 10-year Treasury note yield (TNX) was up about 6 basis points at 3.829%.

CBOE’s Volatility Index (VIX) was down 0.4 at 14.61.

Regional banks and oilfield services stocks led the gainers Tuesday. Crude oil futures rose 3% on expectations of stronger demand from China. Small-caps were also strong, with the Russell 2000 Index (RUT) rising more than 1% to its highest level since early March. The U.S. Dollar Index (DXY) fell to its lowest level in more than three weeks thanks to expectations interest rates could be near their peak.

Posted on June 13, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Markets: With investors keeping their fingers crossed that the Fed will pause its rate hikes when it meets tomorrow, the S&P 500 climbed to its highest in over a year yesterday, buoyed in part by Apple closing at a record high for the first time since January 2022.

Stock spotlight: The NASDAQ index has been on fire lately, but NASDAQ’s own stock fell after it announced plans to buy financial software-maker Adenza for $10.5 billion—its biggest purchase ever—as the company works to diversify its business beyond stock exchanges.

Posted on June 12, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The US economy remains “very, very hot,” though not as much as it was six to 12 months ago, said former Treasury Secretary Lawrence Summers. “The United States is, today, an underlying 4.5-5% inflation country,” Summers said, speaking via video link at the start of the two-day Caixin Asia New Vision Forum in Singapore. At the same time, soft landings “represent the triumph of hope over experience,” and commercial real estate is one area where there are likely to be “pockets of distress,” said Professor Summers of Harvard University.

At its meeting this week, the Federal Reserve is expected to do something it hasn’t done in the last 15 months: not raise interest rates. Chair Jerome Powell suggested it might be time to take a breather as a series of rate hikes filters through the economy.

***

Last week, the S&P 500 reached its fourth consecutive winning week and the NASDAQ seventh as investors find fewer things to be worried about. In a sign of that cautious optimism, Goldman Sachs slashed its probability of a recession in the next year from 35% to 25%.

Crypto: SEC Chair Gary Gensler dramatically escalated his war on crypto-currency last week, and prices took a big hit. Four of the 10 most valuable cryptocurrencies fell by at least 15%, per CoinMarketCap.

Posted on June 4, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The US kept adding jobs according to new data from the Bureau of Labor Statistics. The economy gained 339,000 pay-rolled employees in May, more than in each of the preceding three months and way more than the 190,000 Dow Jones predicted (to be fair, expert estimates low-balled 13 of the last 16 job reports, according to CNBC. This growth happened despite climbing interest rates, inflation, recent bank failures, and a nerve-racking debt ceiling standoff that threatened to destroy the economy And, Wall Street interpreted the data as a big green “buy” sign. For example:

Stocksleaped up last week as investors celebrated the deal to lift the debt ceiling being showed that the economy is still going strong. In fact, Lululemon stretched toward the heavens after beating earnings expectations thanks to a 24% year over year jump in sales.

But not all indications pointed to the hot streak continuing indefinitely.

The unemployment rate inched, wage growth slowed, and workers appear less self-assured in the labor market:

The self-employed lost 369,000 people from its ranks in May, a possible sign that folks might be ditching the self-employment for the security of a traditional employer.

And, recent data shows the quit rate has declined from an all-time high in late 2021, bringing an end to the pandemic job-hopping trend dubbed the Great Resignation.

Ultimately, the Fed will have to use the conflicting and mixed economic indicators to decide whether to further crank up interest rates at their next meeting. The Federal Reserve has been hinting that it might cease raising interest rates, and investors seem convinced the central bank will follow through and at least “skip” a hike this month even though the labor market is still radiating heat.

Posted on May 13, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Here is where the major benchmarks ended this week:

The S&P 500 Index was down 6.54 points (0.2%) at 4124.08; the Dow Jones industrial average was down 8.89 at 33,300.62; the NASDAQ Composite was down 43.76 (0.4%) at 12,284.74.

The 10-year Treasury yield was up about 7 basis points at 3.464%.

CBOE’s Volatility Index was up 0.10 at 17.03.

Consumer Discretionary Socks led the declines Friday among S&P 500 sectors, with financials and energy shares also weaker. Worries over the potential for more trouble in the banking sector helped send the KBW Regional Bank Index to its lowest close since late 2020. Utilities and Consumer Staples were among the stronger performers.

Jerome Powell May Get a New No. 2. President Biden said yesterday that he would nominate economist Philip Jefferson, who is already on the Fed’s board, to become second-in-command at the central bank, replacing Lael Brainard. He also plans to nominate the current US rep to the World Bank, Adriana Kugler, to an empty board seat. She would be the Fed’s first Latina governor. If confirmed by the Senate, the pair will jump into their new roles as the Fed continues to try to curb inflation without tipping the economy into a recession.

Posted on May 11, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks were a mixed bag yesterday after the consumer price index showed prices rose 4.9% last month, marking the 10th month in a row of cooling inflation and the first time inflation has dipped below 5% in two years. That’s still higher than the Fed’s 2% target, but it leaves space for Jerome Powell to chill out a bit. Tech stocks got a boost from that news, especially Google’s parent, Alphabet, which also benefited from rolling out its new AI.

Economists polled by the Wall Street Journal had forecast the CPI increasing 0.4% and advancing 5.0% over the past year. The core inflation rate rose 0.4% in April for the second straight month, in line with economists forecasts. For the year, the core inflation rate, excluding food and energy prices, increased 5.5% down from a 5.6% rise in March.

“The below 5% headline CPI number is a sigh of relief to a market on edge,” said Alexandra Wilson-Elizondo, co-head of portfolio management for multi asset solutions at Goldman Sachs Asset Management.

Traders hoped that the lower-than-expected inflation data may leave room for the U.S. central bank to refrain from raising interest rates further at its June meeting.

“The data today will be interpreted as not hot enough to force the Fed’s hand in June … We do not think this one data point will determine the outcome of the June FOMC meeting because we still have a string of economic data to process between now and then,” wrote Wilson-Elizondo.

“The details of the print suggest that we are still a meaningful distance from the Fed’s 2% target, giving little reason for the Fed to cut this year.”

Investors priced in the Federal Reserve beginning to trim borrowing costs in coming months, a hope that is seen underpinning stocks of late and helping the S&P 500 index move towards the top of the 3,800 to 4,200 range its has held all year.

Posted on May 11, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Because the inflation data came in roughly as expected, Wall Street sees the door still open for the Federal Reserve to leave interest rates alone at its next meeting in June. That would be the first time it hasn’t raised rates at a meeting in more than a year, and a pause would offer some breathing room for the economy and financial markets.

Today is the last day of the US Covid-19 public health emergency, which has been in place since Jan. 31st, 2020. With it comes the end of certain Covid-era rules, though some telehealth protections have been extended through the end of 2024. Here’s to all the medical professionals who got us through, and a remembrance for the millions who lost their lives to Covid.

***

Brightline, a California-based mental health startup, laid off 20% of its staff this week following a data breach. North Carolina is the latest state to consider changes to the prior authorization process that advocates say delays care. A board member at Geisinger claims that consolidation prompted the healthcare provider to sell to Kaiser Permanente. Texas Gov. Greg Abbottsaid the state should address mental health issues in the wake of a shopping mall mass shooting, but did not call for gun control reform.

Finally, here is where the major benchmarks ended yesterday:

The S&P 500 Index was up 18.47 points (0.5%) at 4137.64; the Dow Jones industrial average was down 30.48 (0.1%) at 33,531.33; the NASDAQ Composite was up 126.89 (1.0%) at 12,306.44.

The 10-year Treasury yield was down about 8 basis points at 3.441%.

CBOE’s Volatility Index was down 0.80 at 16.91.

Oilfield services providers and other energy companies were among the laggards Wednesday, pressured by a more-than 1% drop in WTI crude oil futures.

Financial sector stocks struggling to escape the effects of the bank volatility earlier this spring helped push the KWB Regional Bank Index back near a 2½-year low reached last week.

Posted on May 4, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

MAY THE FOURTH BE WITH YOU

***

***

Many pharma companies reported earnings in the last week, and the common thread is crashing Covid-related sales.

For example, AstraZeneca’s Covid medication sales dropped $1.5b in Q1, Merck’s Covid antiviral sales fell 88% from the same quarter in 2022, and Roche’s diagnostics division sales fell 28% from Q1 2022, thanks to low Covid-test demand. Clearly, pharma companies have to figure out how to pivot their strategies in a post-Covid world.

The CDCwill not continue to track Covid-19 community spread as the country enters the endemic stage of the pandemic.

***

The Food and Drug Administration approved Wednesday the first-ever vaccine to combat severe respiratory syncytial virus, or RSV. Arexvy, the new vaccine developed by GlaxoSmithKline, was approved for adults 60 and older and was 82% effective at preventing lower respiratory tract illness caused by RSV, according to trial data. It was also 94% effective in those who had at least one underlying medical condition.

***

The Federal Reserve voted unanimously to raise interest rates by a quarter point yesterday, the tenth rate hike since the central bank started its battle against inflation last March. The move comes amid ongoing fragility in the banking sector triggered partly by higher interest rates, and following the collapse of three regional banks. Markets had anticipated the rate hike, and remained fairly muted after the Fed’s announcement.

***

Finally, here’s where the major indexes ended up:

The S&P 500® Index was down 28.83 points at 4090.75; the Dow Jones industrial average was down 270.29 (0.8%) at 33,414.24; the NASDAQ Composite was down 55.18 (0.5%) at 12,025.33.

The 10-year Treasury yield was down about 7 basis points at 3.367%.

CBOE’s Volatility Index was up 0.52 at 18.30.

Energy companies were among the market’s weakest performers as crude oil continued a recent decline, with WTI crude futures falling more than 4% under $70 a barrel—a nearly six-week low.

Semiconductor and financial shares were also weak. The U.S. dollar index dropped sharply in the wake of the Fed announcement before rebounding.

Posted on May 3, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: The relative calm after JPMorgan scooped up First Republic Bank lasted all of…one day. Two other West Coast lenders, PacificWest and Western Alliance, both tumbled in a sign investors still smell blood among regional banks.

Economy: Happy Fed Decision Day to all who celebrate. With inflation sizzling at still-uncomfortably high levels, Chair Jerome Powell is expected to announce the central bank’s 10th straight interest rate hike this afternoon. But many economists expect this rate increase could be the grand finale.

Layoffs jump to the highest level since late 2020. The number of job openings in the US dropped to a nearly two-year low in March, and layoffs increased to their highest point since December 2020, the Labor Department revealed yesterday. In this “bad news is good news” economic environment, the Fed will be pleased that the boiling-hot labor market is cooling off. It means less pressure on inflation and more justification to pause hiking rates.

Posted on May 1, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Detailing Oversight Lapses

By Staff Reporters

***

***

The Fed says it’s time for new bank rules

Just in time for a new looming bank failure, the Federal Reserve issued a 102-page report dissecting the corpse of Silicon Valley Bank. Meanwhile, FRB [First Republic Bank] FRB was just sold to JPMorgan Chase.

And in an accompanying letter, Michael Barr, the Fed’s vice chair for supervision, called for stricter rules to be applied to more financial institutions and for more tools to be given to regulators to bring firms with poor capital planning and risk management into line.

Posted on April 29, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Compensation pay for US workers picked up in the first three months of the year, showing that a major source of inflationary pressure persists and cementing the path for an interest rate hike at the Federal Reserve’s meeting next week. The Employment Cost Index, released Friday by the Bureau of Labor Statistics, showed that workers were paid 1.2% more in wages and benefits in the first quarter from the prior three-month period. That’s up from analysts’ expectations of 1.1%.

Markets: Stocks rose yesterday, finishing strong to give the Dow its best month since January. But First Republic Bank tanked again as rumors flew about its fate, again.

Economy: For all the Fed watchers, new data released makes it look like another rate hike could be in store next week. The data shows wages are still trending upward, and one of the Fed’s favorite inflation measures rose slightly last month.

Here’s where markets ended.

The S&P 500 Index was up 34.13 (0.8%) at 4169.48, a nearly three-month high; the Dow Jones industrial average was up 272.00 (0.8%) at 34,098.16; the NASDAQ Composite was up 84.35 (0.7%) at (12,226.58.

The 10-year Treasury yield was down about 9 basis points at 3.437%.

CBOE’s Volatility Index was down 1.27 at 15.76.

Energy companies were among the strongest sectors today with help from a rally in crude oil futures. Transportation and financial stocks were also strong. Utilities and consumer discretionary sectors were among the weakest sectors.

Posted on April 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A rally on Wall Street yesterday is lifting stocks to their highest level in almost two months following the latest sign that inflation continues to cool. Yesterday’s report showed that prices paid to producers last month were 2.7% higher than a year earlier, the lowest inflation level there in more than two years. The hope on Wall Street is that easier inflation on the wholesale level will not only support profits for companies but also flow through to cooler inflation for consumers. A day earlier, a separate report said inflation for consumers slowed to 5%.

Inflation and how high the Federal Reserve will hike interest rates to tame it have been at the center of Wall Street’s struggles for more than a year. The Fed has hiked rates at such a feverish pace over the last year that it’s already slowed parts of the economy and caused strains to appear in the banking system.

And so, stocks climbed on the cooler-than-expected PPI, and perhaps some optimism around the Q1 earnings season, with several big banks reporting Friday. However, expectations around Fed policy didn’t budge much.

Bond yields were little changed and markets still see a 70% probability of the Fed enacting a quarter-point rate increase in May, according to the CME FedWatch tool.

The following is a round-up of yesterday’s market activity:

The S&P 500 Index was up 54.27 points (1.3%) at 4146.22; the Dow Jones industrial average was up 383.19 (1.1%) at 34,029.69; the NASDAQ Composite was up 236.93 (2.0%) at 12,166.27.

The 10-year Treasury yield was up about 3 basis points at 3.447%.

Posted on April 12, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A closely-watched government measure of inflation is expected to show that price increases cooled further last month. March’s Consumer Price Index (CPI), slated for release today,is expected to come in at5.2%, a slowdown from February’s 6% annual gain, according to estimates from Bloomberg. The number would mark the slowest annual increase in consumer prices since May 2021 but would still be significantly above the Federal Reserve’s 2% target. The Fed has been raising interest rates to try to bring down inflation, but the central bank risks sending the economy into a recession by hiking rates too high too fast.

The following is a round-up of today’s market activity:

The S&P 500® Index was down 0.17 point at 4108.94; the Dow Jones industrial average was up 98.27 (0.3%) at 33,684.79; the NASDAQ Composite was down 52.48 (0.4%) at 12,031.88.

The 10-year Treasury yield was up about 1 basis point at 3.428%.

CBOE’s Volatility Index was up 0.12 at 19.09.

Energy companies led the gainers, with the PHLX Oil Service Index jumping nearly 2% behind strength in crude oil futures, which rallied to their highest levels since late January. The transportation and financial sectors were also strong.

The U.S. dollar weakened slightly, while gold futures climbed nearly 1% to end a three-day tumble.

Over the past decade, the Federal Reserve has manipulated asset prices by interfering with free markets by deciding what both short-term and long-term interest rates should be. This resulted in an increase in risk-taking behavior among investors.

Risk became a four-letter word uttered only by curmudgeons; the only thing investors feared was being left out. The more risk you took, the more money you made – until you lost it all.

In a previous ME-P column I explained why any currency-issuing country, like the US, will never default on its obligations or run out of money with which to purchase goods and services priced in its own currency. Sovereign nations that are currency issuers have no solvency constraints, unlike currency users such as individuals, corporations, and government entities that don’t issue currency.

To follow up, let’s look at what has become known as Modern Monetary Realism (MMR). Economist Cullen O. Roche describes it in a 2011 article on his Pragmatic Capitalism website titled “Understanding the Monetary System.”

This theory came into existence in 1971 when President Nixon eliminated the gold standard and allowed the government to print money at will. This was a paradigm shift in our monetary policy that’s gone largely unnoticed for decades by many educators, economists, and politicians.

Guiding MMR Principles

The principles of MMR are:

The Federal Reserve works in partnership with the US Treasury to issue currency. All other units of government, private entities, and individuals are users of the currency.

The government creates money by minting coins, printing cash, and issuing reserves. The private banking sector creates money by creating loans and bank deposits.

The Federal Government cannot “go broke.” It is inaccurate to compare it to households, companies, and local governments, which all are users of money and can go bankrupt.

The major constraint on currency issuers (sovereign governments like the US) is inflation. It behooves governments to manage the money supply prudently in order to avoid impoverishing their citizens through devaluing the currency.

Floating exchange rates between countries are a necessity to help maintain equilibrium and flexibility in the global economy. Nations that unduly inflate their currency suffer the consequences of devalued currency, shrinking purchasing power, and contracting lifestyles.

The debt of a sovereign currency issuer is default-free. The issuer can always meet debt obligations in the currency which it issues.

Cullen O. Roche Speaks

Roche suggests that a functional government supports the country’s financial system in four ways:

The US government was created by the people, for the people. “It exists to further the prosperity of the private sector—not to benefit at its expense.” Roche argues that when government becomes corrupt by obtaining too much power or issuing too much currency that results in high inflation, it then becomes susceptible to a revolt and dissolution.

Government’s role is to be actively involved in regulating and helping to build an infrastructure within which the private sector can generate economic growth. Roche views regulation as not only beneficial, but necessary to temper the inevitable irrationality that can disrupt markets. Still, he emphasizes that it is the private sector, not the public sector, which drives innovation, productivity, and economic growth.

Money, while a creation of law, must be accepted by the private sector while prudently regulated by the federal government, keeping in mind that the purpose of the regulation is to maximize private sector prosperity.

“Because the Federal government is not a business or a household it should not manage its balance sheet for its own benefit,” notes Roche, “but in a way that most benefits the private sector and encourages private sector prosperity, productivity, innovation and growth.”

Assessment

Like me, you may need to re-read this a couple of times to begin to grasp the concepts. Once you throw off the outdated pre-1971 model of the monetary system, understanding the basics of MMR isn’t difficult. Knowing the basics of how our monetary system works will help physicians, and all of us, frame the important issues in the turmoil unfolding in Europe and in our own upcoming elections.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 11, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Financial regulators have closed Silicon Valley Bank and taken control of its deposits, the Federal Deposit Insurance Corp. announced yesterday, in what is the largest U.S. bank failure since the global financial crisis more than a decade ago.

The FDIC said in the announcement that insured depositors will have access to their deposits no later than Monday morning.

SVB’s branch offices will also reopen at that time, under the control of the regulator.

The FDIC’s standard insurance covers up to $250,000 per depositor, per bank, for each account ownership category.

And, the crypto company SB announced yesterday that it’s winding down operations and liquidating Silvergate Bank, which has about $11 billion in assets. Silvergate has been struggle throughout crypto’s downturn—especially after the collapse of FTX, one of its biggest customers. Last quarter, Silvergate fired 40% of its workforce, reported a $1 billion loss, and took out billions in loans…but apparently it wasn’t enough.

U.S. equities ended the day and week sharply lower, as the markets continued to look for hints regarding future monetary policy decisions. The moves came amid a flurry of news and economic data, as the February labor report showed stronger-than-expected job gains, and a lower-than-anticipated increase in wages, but a rise in the unemployment rate. The report was in stark contrast to January’s blowout figures, and seemed to soothe some of the anxiety over the Fed’s future actions.

In earnings news, Ulta Beauty handily beat estimates and provided upbeat guidance, and Oracle offered mixed quarterly results and increased its dividend, but Gap fell well short of expectations amid a tumble in online sales, and it saw a shakeup in management.

Treasury yields tumbled in the wake of the labor report and worries surrounding the banking sector, and the U.S. dollar was sharply lower, while crude oil and gold prices traded to the upside.

Asian stocks finished lower, and markets in Europe saw widespread losses, led by shares of banking companies, amid uncertainty regarding the overall effects of rate hikes.

Posted on March 8, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Dow Jones Industrial Average decreased 575 points (1.7%) to 32,856, the S&P 500 Index was 62 points (1.5%) lower at 3,986, and the NASDAQ Composite lost 145 points (1.3%) to 11,530. In moderate volume, 3.8 billion shares of NYSE-listed stocks were traded, and 5.3 billion shares changed hands on the NASDAQ. WTI crude oil fell $2.88 to $77.58 per barrel. Elsewhere, the gold spot price tumbled $34.80 to $1,819.80 per ounce, and the Dollar Index jumped 1.2% to 105.59.

***

And, a key recession indicator flashed its loudest warning ever after Federal Reserve Chairman Jerome Powell said benchmark rates will likely go higher than once anticipated. The inversion between the 2-year and 10-year Treasury yields hit a record 103.5 basis points on Tuesday, according to Refinitiv data. It later narrowed to 102.4 basis points. In normal economic times, shorter-term yields are below longer-term yields. But for months, the 2- and 10-year yields have been inverted amid growing recession fears, as the Fed continues to tighten policy to rein in inflation. The 2-year yield currently sits at 4.992% while the 10-year yield is 3.968%. Meanwhile, there’s a 61.6% probability the Fed will raise its benchmark rate by 50 basis points on March 22, up from 31.4% a day earlier.

***

Finally, the economic calendar introduced a read on wholesale inventories, which was un-revised from the preliminary report at a m/m decline in January. Meanwhile, consumer credit for January expanded at a slower-than-expected pace. Q4 earnings season continues to wrap up, as Dick’s Sporting Goods bested earnings estimates, raised its quarterly dividend, and issued full-year guidance that came in above forecasts. In other equity news, Meta Platforms is planning another round of layoffs that could affect thousands of workers, according to a Bloomberg News report.

Treasury yields were mixed, and the U.S. dollar rallied, while crude oil and gold prices were sharply lower.

Asian stocks ended mixed following the Reserve Bank of Australia’s 25 bp rate hike, and European stocks were lower, as international investors digested Powell’s comments.

Posted on February 25, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to Bloomberg, former Treasury Secretary Lawrence Summers said worrying signals of a potential sharp drop-off in activity combined with strength in other indicators point toward an uncertain economic outlook.

Here is Why:

Inventories “look to be building up relative to sales.”Companies are “reporting concerns about their order books.”The business sector appears to have a high payroll head-count relative to “the level of output they’re producing.”“Consumer savings are being depleted, with a low savings rate.” And, “there is stuff when you look down the road a bit that has to be substantially concerning about the Wile E. Coyote kind of moment,” reiterating his reference to the cartoon character that falls off a cliff.

Federal Reserve policymakers will need to “stay nimble and flexible” given the uncertainty, Summers said. The central bank should “resist the pressure to be giving strong signals about what it’s going to do next.”

Finally, the former Treasury chief also reiterated the lack of past examples in which the US managed to avoid a recession when the unemployment rate dropped below 4% and inflation went above 4%. “That’s a powerful historical truth and I think it’s one that’s relevant to our current situation.”

The latest unemployment-rate reading was 3.4%, while the consumer price index climbed 6.4% in January on a year-on-year basis.

***

Stocks Fell Following Hot Inflation Report and U.S. equities ended the day and week lower as the markets reacted to a Fed-favored gauge of inflation that came in hotter-than-expected. PCE and Core PCE Price Indexes rose more than anticipated, while personal income increased less than expected, and spending jumped. The moves came as equities have shown some volatility amid festering uncertainty regarding the ultimate economic impact of aggressive global central bank tightening as a result of persistent inflation. In other economic news, new home sales rose, and consumer sentiment was surprisingly revised the upside.

Treasury yields were higher, and the U.S. dollar gained ground, while crude oil prices increased, and gold traded to the downside. Q4 earnings season rounded a corner this week with some second-tier results hitting the tape, as Autodesk disappointed with its guidance and Intuit bested expectations, while Warner Bros. Discovery fell well short of forecasts.

In other equity news, shares of Boeing declined after the company paused delivery of its 787 Dreamliner planes. Asian stocks finished mixed, and markets in Europe fell, with economic data in the respective regions keeping the anxiety over future global monetary policy elevated.

Posted on February 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks ended the week subdued when a red-hot jobs report once again got investors biting their nails over what the Fed will do next—though the S&P and NASDAQ both eked out positive weeks. The tech stock rally started losing steam after several big companies reported disappointing quarterly results, with Amazon being the one investors cooled on most.

More specifically, racing game publisher Motorsport Games (NASDAQ:MSGM) is seeing more volatility, tumbling 24.2% Friday after announcing a $4M at-the-market offering. The company entered a definitive agreement to issue and sell 232,188 shares of its class A common stock at $17.39 per share. The stock has slid $5.46 to trade at $17.50. The closing of this new offering is set for on or around February 7th with H.C. Wainwright & Co. acting as exclusive placement agent. Gross proceeds will be about $4.03M, which Motorsport Games will put toward development of multiple games, working capital and general purposes.

Still, it was the most eventful week for the stock in many months. On Monday it launched a debt-for-equity exchange to shore up its balance sheet, sending the stock lower by 8.7%. After regaining full compliance with Nasdaq listing rules, the stock jumped 714% Tuesday, moving from $2.63 a share to $21.40. After moving up another 73% Wednesday, the company then moved to convert all remaining debt in a new debt-for-equity exchange, and the stock fell 38% Thursday. Before Friday’s decline, the stock moved up an aggregate 482% in five days.

Posted on February 4, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Treasury yields jumped after a much stronger-than-expected U.S. January jobs report clouded investor expectations for the Federal Reserve to end its interest rate hiking cycle in coming months. Treasury Yields and debt prices move opposite each other:

The yield on the 2-year Treasury note rose 14.9 basis points to 4.233%.

The 10-year Treasury note yield jumped 9.9 basis points to 3.498%.

The 30-year Treasury bond yield was up 6.9 basis points at 3.626%.

***

U.S. equities declined in a choppy trading session following a stronger-than-expected January labor report, and some uninspiring earnings results from mega-cap stocks. Non farm payroll additions beat estimates by a large amount, and the unemployment rate declined, solidifying the notion of a tight job market.

Meanwhile, a read on domestic services sector activity moved back into expansion territory. Mega-cap stocks were in focus today, as Dow member Apple missed estimates and posted its first quarterly decline in revenues since 2019, and Alphabet also posted discouraging quarterly results, while Qualcomm bested EPS estimates by a penny, but fell short on the revenue side.

Notably, the retail giant Amazon is finally starting to feel the economic pinch. The e-commerce company, which most people thought was unstoppable, has reportedly had its first unprofitable year since 2014. The company released this week that it has lost over $2 billion in 2022, despite holiday-season sales increasing by 9%.

Asian and European stocks finished mixed, as the markets continued to process the week’s monetary policy decisions, as well as some services sector data across the globe.

***

Elon Musk was found not liable for investors’ losses in a securities fraud trial over his 2018 tweet that he had “funding secured” to take Tesla private at $420 per share, continuing the tech mogul’s streak of favorable verdicts over his erratic behavior. Plaintiff Glen Littleton and fellow members of the class action sued Musk and Tesla, including its board of directors, over the tweet and Musk’s subsequent statements, alleging the notion that financing was in place had been false. They said shareholders suffered steep financial harms because of panicked sales in the 10 days following the tweet, as Tesla and Musk engaged in damage control.

Posted on February 1, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

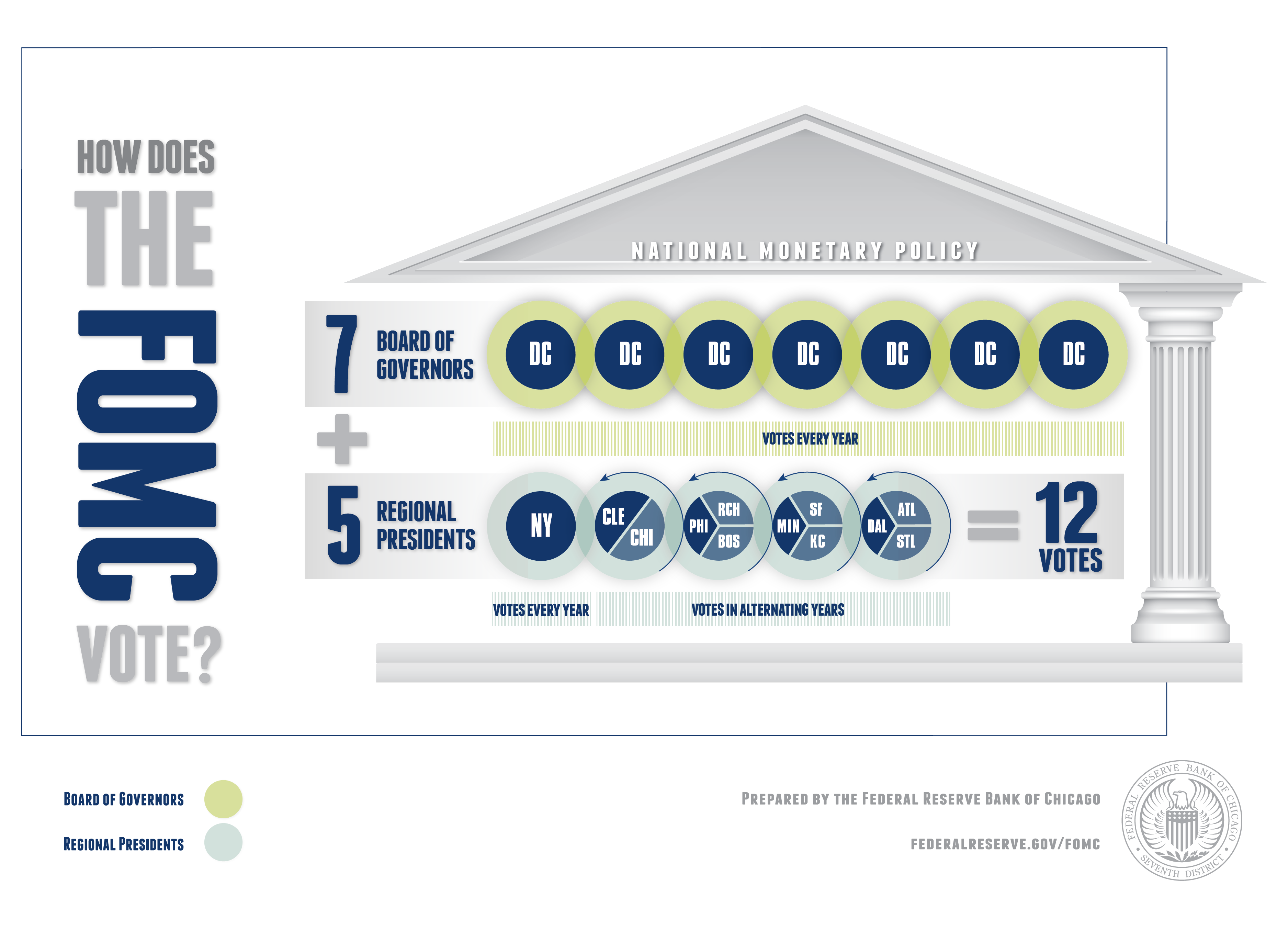

DEFINITION:

According to Wikipedia, the Federal Open Market Committee (FOMC), a committee within the Federal Reserve System (the Fed), is charged under United States law with overseeing the nation’s open market operations (e.g., the Fed’s buying and selling of United States Treasury securities). This Federal Reserve committee makes key decisions about interest rates and the growth of the United States money supply. Under the terms of the original Federal Reserve Act, each of the Federal Reserve banks was authorized to buy and sell in the open market bonds and short term obligations of the United States Government, bank acceptances, cable transfers, and bills of exchange. Hence, the reserve banks were at times bidding against each other in the open market. In 1922, an informal committee was established to execute purchases and sales. The Banking Act of 1933 formed an official FOMC.

The FOMC is the principal organ of United States national monetary policy. The Committee sets monetary policy by specifying the short-term objective for the Fed’s open market operations, which is usually a target level for the federal funds rate (the rate that commercial banks charge between themselves for overnight loans).

The FOMC also directs operations undertaken by the Federal Reserve System in foreign exchange markets, although any intervention in foreign exchange markets is coordinated with the U.S. Treasury, which has responsibility for formulating U.S. policies regarding the exchange value of the dollar.

The Federal Reserve is set to announce today whether it will impose another interest rate hike, the central bank’s latest move in a months long fight that has eased inflation but risks plunging the U.S. into a recession.

The Fed [FOMC] has put forward a string of borrowing cost increases as it tries to slash price hikes by slowing the economy and choking off demand. The approach, however, risks tipping the U.S. economy into a downturn and putting millions out of work.

And so, at a meeting in December 2022, the Fed raised its short-term borrowing rate a half-percentage point, pulling back from three consecutive 0.75% increases and signaling confidence that sky-high inflation could be brought down to normal levels.

Economists expect the Fed to continue softening its approach with a 0.25% rate hike today? The decision comes weeks after a government report showed that inflation slowed in December, marking six consecutive months of easing price increases.

Posted on February 1, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Foreign-exchange volatility hammered North America’s corporate profits by a record in the third quarter, though signs of relief are on the horizon. Currency oscillations cost North American companies $43.2 billion in the July to September period — an all-time high since data tracking started a decade ago — according to Kyriba Corp. That’s a 26% spike from the previous quarter, also a record, according to the corporate-treasury management software company. And, public companies pointed to the euro, Canadian dollar and ruble as the currencies weighing the most on profits in the period, followed by the Chinese yuan and the Japanese yen, according to Kyriba’s report. The euro and the loonie had also earned top mentions in the firm’s second-quarter report.

U.S. equities ended a choppy trading session higher, as investors sifted through a host of earnings and economic data, and awaited tomorrow’s monetary policy decision from the Federal Reserve. Several Dow members were in focus, as McDonald’s beat earnings estimates, and Caterpillar missed expectations due to unfavorable foreign currency impacts.

In other equity news, UPS posted higher-than-expected earnings, declared a new quarterly dividend, and revamped its share repurchase program, while Pfizer beat forecasts but issued lower-than-anticipated guidance, and General Motors trounced expectations and offered an upbeat full-year outlook.

The economic calendar heated up, with the Q4 Employment Cost Index coming in lower than expected, and home prices declining by a smaller amount than anticipated in November. More reports came out after the opening bell, as January’s consumer confidence unexpectedly declined, and the Chicago PMI fell further into contraction territory.

Treasury yields were lower, and the U.S. dollar dipped, while crude oil prices increased, as did gold. Asian stocks were mostly lower amid a swarm of economic reports.

European markets finished mixed following the economic data, and as investors awaited monetary policy decisions from the European Central Bank and Bank of England later this week.

Posted on January 20, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The number of people seeking unemployment benefits in the U.S. reached a four-month low last week, a sign that employers are holding on to their workers despite the Federal Reserve’s efforts to slow the economy and tamp down inflation. U.S. jobless aid applications for the week ending January14th fell by 15,000 to 190,000, from 205,000 the week before, according to the Labor Department. The four-week moving average of claims, which can even out the week-to-week volatility, declined by 6,500 to 206,000. Jobless claims generally serve as a proxy for layoffs, which have been relatively low since the pandemic wiped out millions of jobs in the spring of 2020. And, the labor market is closely watched by the Federal Reserve, which raised interest rates seven times last year in a bid to slow job growth and bring down stubbornly high inflation.

According to Bloomberg, Netflix Inc. co-founder Reed Hastings is stepping aside as Chief Executive Officer of the company he’s led for more than two decades, leaving the position to his two longtime associates, Ted Sarandos and Greg Peters.

***

U.S. stocks were lower, adding to yesterday’s sharp draw downs as investors remain concerned regarding the Fed’s monetary policy decisions and its ultimate impact on the economy. Economic data was mixed, as housing starts came in above estimates, building permits missed forecasts, and jobless claims unexpectedly dropped, while Philadelphia’s manufacturing output improved more than expected but remained contractionary. Q4 earnings season continued to heat up, as Dow member Procter & Gamble matched estimates, while Discover Financial Services topped forecasts but offered cautious guidance about charge offs, and Allstate Corporation issued a Q4 profit warning.

Treasury yields gained modest ground, and the U.S. dollar declined, while crude oil and gold prices rose.

Asian stocks finished mixed and markets in Europe saw widespread losses, trimming some of its strong start to 2023.

***

Finally, bankrupt Crypto exchange FTX is looking into the possibility of reviving its business, Chief Executive Officer John Ray just told the Wall Street Journal. Ray, who took over the reins in November, has set up a task force to explore restarting FTX.com, the company’s main international exchange. The CEO also told the Journal that he would look into whether reviving FTX’s international exchange would recover more value for the company’s customers than his team could get from simply liquidating assets or selling the platform. FTX’s native token FTT surged nearly 30% after the report.

Posted on December 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Mark Cuban Cost Plus Drug Company is teaming up with EmsanaRx, a pharmacy benefit manager (PBM) focused on employer plans, to make lower-cost prescription drugs more accessible to patients through their employers. The program, EmsanaRx Plus, is described as “a standalone pipeline” for employers to supply drugs to employees through Cost Plus Drugs, an online pharmacy that offers more than 1,000 of the most in-demand generic medications at significantly marked-down prices.

And, according to Bloomberg, US lawmakers are aiming to make regional Federal Reserve banks comply with public record requests after a string of scandals in the central bank system. Massachusetts Democrat Elizabeth Warren and Pennsylvania Republican Patrick Toomey plan to propose legislation to subject the regional branches to congressional information requests under the Freedom of Information Act.

Finally, insiders and other media have identified numerous US lawmakers not complying with the federal STOCK Act. Their excuses range from oversights, to clerical errors, to inattentive accountants. Congress is now considering banning lawmakers from trading individual stocks.

Posted on December 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

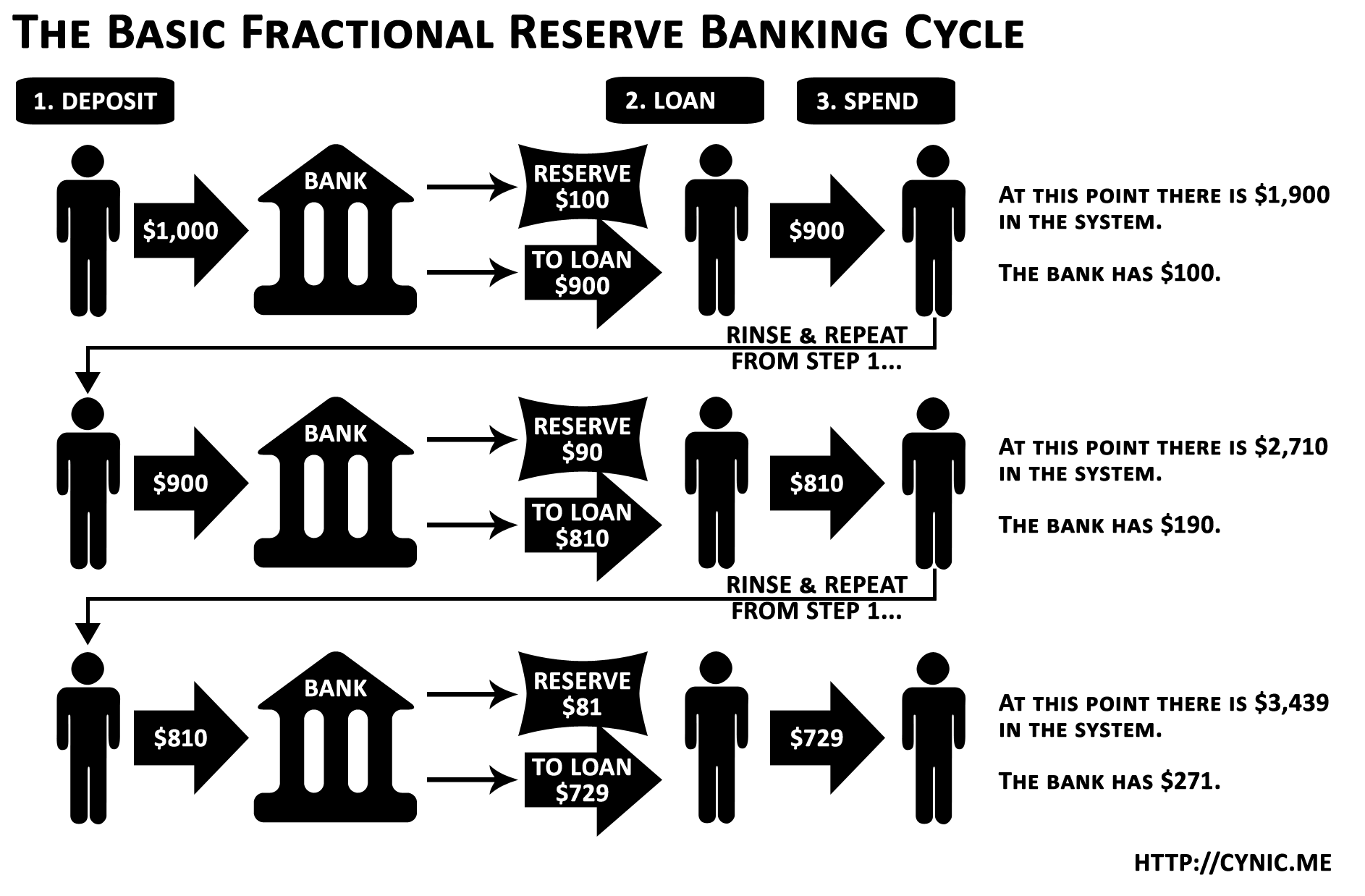

Fractional reserve banking is a system in which only a fraction of bank deposits are backed by actual cash on hand and available for withdrawal. This is done to theoretically expand the economy by freeing capital for lending. Today, most economies’ financial systems use fractional reserve banking.

Posted on November 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities extended yesterday’s sharp drop that followed the Federal Reserve’s fourth-straight 75-basis point rate hike and some hawkish comments. As a result of the Fed’s monetary policy decision, Treasury yields and the U.S. dollar climbed noticeably higher. The Fed’s rate hike was trailed by today’s announcement from the Bank of England to hike its benchmark interest rate by 75 bps, though it tried to suppress expectations of future aggressiveness of that magnitude. The U.S. dollar’s rally came as the British pound fell, along with the euro, as the markets digested the monetary policy actions and comments.

Crude oil prices fell, and gold traded lower. In economic news, jobless claims dipped, the trade balance widened more than expected, Q3 productivity rebounded less than fore-casted and labor costs moderated more than projected. Additionally, factory orders figures were mixed, along with October reads on services sector output. Earnings season continues to roll on, with Qualcomm cutting its guidance, though eBay topped estimates and issued a positive outlook. Moreover, Booking Holdings topped expectations and Marriott decreased despite exceeding profit projections.

Asian stocks declined, though markets in Japan were closed for a holiday, and European stocks were mostly lower as the markets digested the decisions from the Fed and Bank of England.

Posted on October 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

The Fed is poised to raise interest rates just one more time in November before stopping, according to Ed Yardeni. That’s because there is a growing risk that financial markets are on the verge of instability due to a soaring US dollar.

“The soaring dollar has been associated in the past with creating financial crisis on a global basis,” Yardeni just told told Bloomberg.

Posted on September 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Federal Reserve hiked its key interest rate by 0.75% for the third time in a row as it races to get ahead of the galloping inflation that is sapping the earnings of American consumers. In its latest economic forecast, the Federal Open Market Committee said it now projects that the U.S. unemployment rate will climb from 3.7% to 4.4% — meaning hundreds of thousands more Americans will be without jobs.

The stock market did not respond well after the interest rate news was announced, with the Dow Jones Industrial Average dropping 522 points, or 1.7%, at the close. The S&P and NASDAQ saw similar percentage drops.

Posted on June 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

So far this year, Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), Amazon (NASDAQ: AMZN), and Tesla (NASDAQ: TSLA) have announced plans for splitting their stocks.

And, the FOMC’s $9 trillion portfolio is about to be reduced in a process intended to supplement rate hikes and buttress the central bank’s fight against inflation. “Quantitative tightening” is the opposite of “quantitative easing”. It’s basically a way to reduce the money supply floating around in the economy and helps to augment rate hikes in a predictable manner — though, by how much remains unclear.

Finally, the market for public listings [IPOs] has essentially stalled. No companies, including SPACs, went public in the US last week for the first time in two years, according to Renaissance Capital.

Posted on April 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

After last week’s sharp decline, the S&P is down 5.7% so far in April and is on track for its worst monthly drop since March 2020, when the spreading COVID-19 pandemic blasted stocks.

And, battered U.S. stocks are facing a potentially painful stretch in the weeks ahead as hawkish Federal Reserve policy, rising bond yields, geopolitical uncertainty and the corporate earnings season fuel investor unease. For example:

REPORTINGCOMPANIES:

Monday: Germany business climate; Earnings from PepsiCo and Whirlpool

Tuesday: US consumer confidence; Earnings from 3M, General Electric, JetBlue, UPS, Warner Bros. Discovery, Alphabet, General Motors, Mondelez, Microsoft and Visa

Wednesday: Earnings from Boeing, Harley-Davidson, Kraft Heinz, Spotify, Ford Motor, Mattel, Meta and PayPal

Thursday: Bank of Japan policy decision; US first quarter GDP; Earnings from Caterpillar, Altria, Domino’s Pizza, Mastercard, Twitter, Amazon, Apple, Intel, Roku and Robinhood

Friday: Europe first quarter GDP and inflation data; US personal income and spending data; PCE Price Index; Earnings from ExxonMobil and Chevron

One measure of investor anxiety, the CBOE Volatility Index, known as Wall Street’s fear gauge, on Friday notched its largest one-day gain in about five months to close at a five-week high of 28.21.

Posted on April 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Wall Street’s main stock benchmarks closed higher Thursday after two days of declines.

St. Louis Fed President James Bullard said the central bank is “behind the curve” on fighting inflation.

Stocks appeared to take in stride Bullard’s view that the Fed needs to raise rates by 3 percentage points this year.

The NASDAQ Composite recovered a portion of the 2% slump it suffered on Wednesday, and the S&P 500 and the Dow Jones Industrial Average joined the tech-concentrated index in rising for the first time in three sessions.

Stocks overcame earlier losses and appeared to absorb remarks by St. Louis Fed President James Bullard who reportedly said on Thursday the Fed is “behind the curve” in curbing inflation. He said the central bank will need to raise interest rates another 3 percentage points by the end of 2022, according to Reuters. The Fed in March raised its fed funds rate by 25 basis points from near zero.

Judge Ketanji Brown Jackson will become the first Black woman to ever serve on the US Supreme Court, after being confirmed by the Senate in a 53–47 vote. She’ll replace Justice Stephen Breyer, who is retiring this summer.

Posted on April 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks ended lower but off their worst levels, with the tech-heavy NASDAQ Composite bearing the brunt of selling pressure for a second session Wednesday after minutes of the Federal Reserve’s March policy meeting outlined plans for shrinking the central bank’s nearly $9 trillion balance sheet.

The Dow Jones Industrial Average ended with a loss of around 145 points, or 0.4%, near 34,497, according to preliminary figures, while the S&P 500 sank around 44 points, or 1%. to finish near 4,481. The NASDAQ Composite shed around 315 points, or 2.2%, closing near 13,889.

And, the 10-year treasury yield, which indicates the level of investor confidence in the markets, jumped to 2.62% which was the highest level since March, 2019. The move higher is partly due to continued momentum from Tuesday’s 28.19% rise, which was propelled by U.S. Federal Reserve Governor Lael Brainard’s hawkish comments. However, the 5-year yield remained inverted and higher then the 30-year yield. The spike higher in bond yields

Posted on March 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A mountain of economic data and earnings news emerged over the past month for two popular FAANG stocks that announced they’d be enacting stock splits.

First up was Alphabet (NASDAQ: GOOGL) (NASDAQ: GOOG), the parent company of internet search engine Google and streaming platform YouTube. Alphabet announced a 20-for-1 forward stock split that, as of the closing bell on March 9th, would bring its share price down to around $133 (for the Class A shares, GOOGL). Shareholders still need to vote to approve the split, which is expected to take effect in mid-July.

And, last week e-commerce giant Amazon (NASDAQ: AMZN) followed suit with a 20-for-1 forward stock split announcement of its own. Assuming it receives shareholder approval, Amazon’s lofty share price will come down to around $139, based on its March 9th close. This will be Amazon’s first stock split since September 1999.

Finally, the Federal Reserve is expected to raise its target fed funds rate by a quarter percentage point from zero at the end of its two-day meeting Wednesday. Investors are also looking to the central bank for its new forecasts for rates, inflation and the economy, given the uncertainty from the escalated geopolitical tensions.

Posted on March 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Economy: Federal Reserve Chair Jerome Powell told Congress that “it’s too soon to say” how the war in Ukraine will affect the central bank’s plans, but for now it’s not enough to derail the FOMC from hiking interest rates later this month.

Markets: Stocks rose across the board with strong corporate fundamentals outshining geopolitical worries…at least for a day. Intel had a strong showing after its CEO got a shout-out in the State of the Union address (to be fair, we have no idea if those two things are related).

Posted on February 20, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

Federal Reserve Chair Jerome Powell and his colleagues can expect to see their upcoming key inflation metric accelerate this week to a fresh four-decade high last seen when Paul Volcker led the U.S. central bank.

The personal consumption expenditures price index, which the Federal Reserve uses for its inflation target, likely jumped 6% in January from a year earlier, according to the median of a Bloomberg survey of economists. The core measure, which excludes food and fuel, is forecast to climb 5.2%.

And, less than a month before the FOMC’s next policy meeting, a sharper-than-projected advance in the price gauge could turn up the heat for a half-point increase in the benchmark interest rate. January’s consumer-price index rose more than forecast, with broad advances in the costs of goods and services.

Posted on February 19, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

MARKETS: Stocks closed down for a second straight week in the US— and sunk deeper into the red for 2022 so far — as investors assess the risks from escalating tensions in Ukraine and a shift in monetary policy by the Federal Reserve.

And, after another day of turbulence, the Dow and the S&P 500 both fell 0.7% (with the Dow ending Friday at 34,079) and the tech-heavy NASDAQ composite declined 1.2%. The NASDAQ has fallen farthest of the three major U.S. stock indexes to date, down 13.4% for the year, while the S&P 500 is off 8.8% and the Dow is down 6.2%.

Specifically, Intel’s shares declined $2.47, or 5.2%, while those of Boeing were off $4.38 (2.1%), combining for a roughly 45-point drag on the Dow. Salesforce.com Inc. Caterpillar and Honeywell International Inc. also contributed significantly to the decline.

STOCKS:

Shopify, which represented the Covid e-commerce boom, is down 62% from its peak.

Roblox, which represented the Covid gaming boom, is down 63%.

Netflix, which represented the Covid streaming boom, is down 43%.

Noteworthy: A $1 move in any of the Dow’s 30 components equates to a 6.59-point swing.

UKRAINE: Investors watched the latest developments in Ukraine, where Russia has been amassing troops on the border. The tensions are yet another concern for investors as they also try to determine how the economy will react to rising inflation and looming interest rate hikes.

Posted on February 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

GLOBALMARKETS: Stabilized on Friday after the threat of a potential Russian invasion of Ukraine propelled the Dow to its worst day of 2022. Australia’s S&P/ASX 200 and Japan’s benchmark Nikkei closed down 1% and 0.4%, respectively, while South Korea’s Kospi was little changed. Chinese markets were mixed. As the benchmark Shanghai Composite Index gained 0.7%, Hong Kong’s Hang Seng Index dropped 1.9%. In Europe, stocks were little changed at the open. London’s FTSE 100 and France’s CAC 40 each rose 0.2%, while Germany’s DAX ticked up 0.1%.

DOMESTIC MARKETS: The Dow plummeted 622 points, or 1.8% — hitting its lowest level so far this year in the process. The S&P 500 fell 2.1% and the NASDAQ was down 2.9%. All three indices are now in the red for the week. Finally, US futures pointed up slightly with Dow futures, S&P 500 futures and NASDAQ futures rising 0.6%, 0.7% and 0.8%, respectively.

FOMC: Jim Bullard, the president of the St. Louis Federal Reserve and member of the Federal Open Market Committee, said that the Federal Reserve wants to pursue the best policy as members debate how quickly they should raise interest rates. He called for a full percentage point interest rate hike by July, 2022. And, billionaire investor Carl Icahn predicts the Fed’s money-printing party will end badly because the government can’t control inflation

Posted on January 29, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Stock Market: US stocks jumped yesterday with the NASDAQ 100 surging more than 3% as a wave of corporate earnings results helped investors overcome fears of a hawkish Federal Reserve.

Federal Reserve: Friday’s action helped the broader stock market indices end the week mostly flat after a series of volatile trading sessions sparked by the Federal Reserve’s Wednesday meeting. The Dow Jones Industrial Average recorded a swing of 1,100 points on Monday alone.

Economy: Americans are the most pessimistic about the economy they’ve been in a decade — with spirits even lower than in the early pandemic lock-downs in spring 2020. The University of Michigan’s Consumer Sentiment Index sank to 67.2 from 70.6 in January, according to data published Friday. Economists surveyed by Bloomberg expected sentiment to slide to 68.7. The final January figure is the lowest since November 2011 and sits 11.8 points below levels seen one year ago.

Cyber-Crime: Lazarus, a known cyber-crime group with ties to the North Korean government, has managed to abuse the MSFT Windows Update Client to distribute malware, cybersecurity researchers from Malwarebytes have found. In a blog post detailing their findings, the researchers said they were investigating a phishing campaign impersonating Lockheed Martin, an American aerospace, arms, defense, information security, and technology corporation.

Posted on January 27, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: Stocks were in the green yesterday until Fed Chair Jerome Powell explained that the Federal Reserve Open Market Committee was planning to start hiking interest rates in March to combat soaring inflation. Then, they tanked and Treasury yields rose sharply higher. Microsoft still had a solid day after its superb earnings report offered bullish signs for the entire software industry. But, stock markets in Asia tumbled to their lowest in nearly 15 months after America’s central bank chief confirmed widely expected plans to tackle higher inflation with an increase in interest rates this year, beginning in March. And finally, Cryptos got crushed, again!

FOMC: “With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds rate,” said Chairman Powell.