BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The Evolving Landscape of Broker-Dealer Recruitment

Broker-dealer recruitment has become a dynamic and competitive arena within the financial services industry. As firms vie for top talent, the strategies and incentives used to attract and retain financial advisors have evolved significantly. In an environment shaped by regulatory changes, technological innovation, and shifting advisor expectations, broker-dealers must continuously refine their recruitment approaches to remain competitive and relevant.

At the heart of broker-dealer recruitment is the pursuit of experienced financial advisors who bring with them established client relationships and significant assets under management. These advisors are highly sought after because they can generate immediate revenue and enhance a firm’s market presence. According to recent industry reports, firms like LPL Financial, Commonwealth, and Cetera have ramped up their recruitment efforts by investing in platform enhancements, rebranding initiatives, and technology upgrades to appeal to both seasoned professionals and the next generation of advisors.

One of the most significant trends in broker-dealer recruitment is the emphasis on value-added services. Advisors today are not merely looking for the highest payout or signing bonus; they are increasingly drawn to firms that offer robust support systems, including compliance assistance, marketing resources, and advanced technology platforms. Broker-dealers that can demonstrate a commitment to advisor growth and client service excellence are more likely to attract top-tier talent.

The competitive nature of the industry has also led to the rise of aggressive recruitment tactics, including lucrative transition packages and equity offers. While these financial incentives can be effective, they are increasingly being supplemented by strategic differentiators such as flexible affiliation models, access to alternative investment platforms, and opportunities for practice acquisition or succession planning.

Moreover, the recruitment landscape is being reshaped by broader economic and regulatory forces. The implementation of Regulation Best Interest (Reg BI) and the ongoing impact of high interest rates have prompted advisors to reassess their affiliations and seek firms that provide clarity, stability, and strategic guidance. Broker-dealers that proactively address these concerns and offer transparent, advisor-centric solutions are better positioned to succeed in the recruitment race.

In conclusion, broker-dealer recruitment is no longer just about offering the biggest check. It is about creating a compelling value proposition that resonates with advisors’ professional goals and personal values. Firms that invest in technology, culture, and advisor support—while remaining agile in response to industry trends—will be best equipped to attract and retain the talent necessary for long-term success.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Investing may seem complicated, but today there are many ways for the newly minted physician [MD, DO, DPM, DMD or DDS] to begin, even with minimal knowledge and only a small amount to invest. Starting as soon as possible will help you get closer to the retirement you deserve.

***

Why is investing important?

Investing often feels like a luxury reserved for the already wealthy physician. Many of us find it difficult to think about investing for the future when there are so many things we need that money for right now; medical school loans, auto, home and children; etc. But, at some point, we’re going to want to stop working and enjoy retirement. And simply put, retirement is expensive.

Most calculations advise that you aim for enough savings to give you 70% to 80% of your pre-retirement income for 20 years or more. Depending on your goals for retirement, that means you could need between $500,000 and $1 million in savings by the time you retire. That may not sound attainable, but with the power of compounding growth, it’s not as hard to achieve as you think. The key is starting as soon as possible and making smart choices.

The short answer is “now,” no matter what your age. Due to the way the gains in investments can compound, the earlier you start the better. Money invested in your 20s could very easily grow over 20 times before you retire, without you having to do much.That is powerful. Even if you’re in your 50s or older, you can still make significant progress toward meeting your goals in retirement.

How much should you invest per month?

Most financial experts say you should invest 10% to 15% of your annual income for retirement. That’s the goal, but you don’t have to get there immediately. Whatever you can start investing today is going to help you down the road.

So, if 10% to 15% is too much right now, start small and build toward that goal over time. You can actually start investing with $5 if you want. And you should. Some investment products require a minimum investment, but there are plenty that don’t, and a lot of online brokerage accounts can be started for free.

The best investments for you are going to depend on your age, goals, and strategy. The important thing is to get started. You’ll learn as you go. If you have questions, a dedicated DIYer or investment advisor can help give you the guidance and options you need.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Understanding Stock Market Options: A Strategic Investment Tool

Stock market options are financial instruments that offer investors a versatile way to participate in the equity markets. Unlike traditional stock trading, options provide the right—but not the obligation—to buy or sell an underlying asset at a predetermined price within a specified time frame. This flexibility makes options a powerful tool for hedging, speculation, and income generation.

There are two primary types of options: calls and puts. A call option gives the holder the right to buy a stock at a specific price, known as the strike price, before the option expires. Investors typically purchase call options when they anticipate a rise in the stock’s price. Conversely, a put option grants the right to sell a stock at the strike price, and is used when an investor expects the stock to decline. Each option contract typically represents 100 shares of the underlying stock.

Options are traded on regulated exchanges such as the Chicago Board Options Exchange (CBOE), and their prices are influenced by several factors. These include the underlying stock’s price, the strike price, time until expiration, volatility, and prevailing interest rates. The premium, or cost of the option, reflects these variables and represents the maximum loss for the buyer.

***

***

One of the most compelling uses of options is hedging. Investors can use options to protect their portfolios against adverse price movements. For example, owning put options on a stock can offset potential losses if the stock’s value drops. This strategy is akin to purchasing insurance and is especially valuable during periods of market uncertainty.

Options also enable speculative strategies with limited capital. Traders can leverage options to bet on price movements without owning the underlying asset. While this can lead to significant gains, it also carries substantial risk, particularly if the market moves against the position. Therefore, understanding the mechanics and risks of options is crucial before engaging in such trades.

Another popular strategy involves writing options, or selling them to collect premiums. Covered call writing, for instance, involves holding a stock and selling call options against it. This generates income but caps potential upside if the stock surges beyond the strike price. Similarly, cash-secured puts allow investors to earn premiums while potentially acquiring stocks at a discount.

Despite their advantages, options are not suitable for all investors. Their complexity and potential for rapid loss require a solid grasp of financial concepts and disciplined risk management. Regulatory bodies and brokerages often require investors to pass suitability assessments before granting access to options trading.

In conclusion, stock market options are dynamic instruments that offer a range of strategic possibilities. Whether used for hedging, speculation, or income, they provide flexibility that traditional stock trading cannot match. However, their effective use demands education, experience, and a clear understanding of market behavior. For informed investors, options can be a valuable addition to a diversified financial toolkit.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Why It Is Difficult to Be a Part-Time Financial Planner Today

In theory, part-time financial planning offers flexibility and work-life balance, making it an attractive option for professionals seeking reduced hours. However, in practice, the role of a financial planner has evolved into a demanding, full-time commitment. The complexity of financial markets, client expectations, regulatory requirements, and technological advancements make part-time financial planning increasingly difficult to sustain.

One of the primary challenges is client relationship management. Financial planning is deeply personal and trust-based. Clients expect consistent communication, timely updates, and proactive advice. A part-time planner may struggle to maintain the same level of responsiveness as full-time counterparts, especially during volatile market conditions or life-changing events like retirement, divorce, or inheritance. Delayed responses or limited availability can erode client confidence and damage long-term relationships.

***

***

Another obstacle is the rapid pace of financial change. Tax laws, investment products, insurance regulations, and retirement planning strategies are constantly evolving. Staying current requires ongoing education, certifications, and industry engagement. For part-time planners, keeping up with these changes while managing clients and administrative tasks can be overwhelming. Falling behind risks offering outdated or suboptimal advice, which could lead to compliance issues or client dissatisfaction.

Regulatory compliance adds another layer of complexity. Financial planners must adhere to strict standards set by organizations like FINRA, the SEC, and state regulators. These include documentation, disclosures, fiduciary responsibilities, and continuing education. Compliance is non-negotiable and time-consuming, regardless of hours worked. Part-time planners face the same scrutiny and liability as full-time professionals, but with fewer hours to manage the workload.

Technology, while a powerful tool, also presents challenges. Clients increasingly expect digital access to their portfolios, real-time updates, and virtual meetings. Managing these platforms requires technical proficiency and regular maintenance. Part-time planners may find it difficult to keep systems updated, troubleshoot issues, or provide tech support, especially if they lack dedicated staff.

Business development is another hurdle. Building and maintaining a client base requires networking, marketing, and referrals. Part-time planners often have limited time to attend events, follow up with leads, or cultivate relationships. This can hinder growth and make it difficult to compete with full-time advisors who are more visible and accessible.

Finally, there’s the issue of income and scalability. Many financial planners earn through commissions, assets under management (AUM), or fee-based models. Part-time work often means fewer clients and lower revenue, which can make it hard to justify the costs of licensing, insurance, software, and office space. Without scale, profitability becomes a challenge.

In conclusion, while the idea of part-time financial planning may seem appealing, the realities of the profession make it difficult to execute effectively. The demands of client care, compliance, education, and business development require consistent attention and availability. Unless the industry adapts to support flexible models, part-time financial planners will continue to face significant barriers to success.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and A.I.

***

***

Stocks: Stock Market Indexes recovered yesterday from their losses, though the Dow remained in the red.

Commodities: Gold is rising above $4,200 to another new all-time high. Meanwhile, oil dropped to nearly a five-month low as trade tensions raised the specter of slowing economic growth.

Crypto: Bitcoin, ethereum, and altcoins of all shapes and sizes remain repressed after a massive selloff last weekend erased billions in crypto positions.

The S&P 500, short for the Standard & Poor’s 500 Index, is one of the most widely followed stock market indices in the world. It tracks the performance of 500 of the largest publicly traded companies in the United States, offering a broad snapshot of the overall health and direction of the U.S. economy. Created in 1957 by the financial services company Standard & Poor’s, the index has become a benchmark for investors, analysts, and economists alike.

Composition and Criteria The S&P 500 includes companies from a wide range of industries, such as technology, healthcare, finance, energy, and consumer goods. To be included in the index, a company must meet specific criteria: it must be based in the U.S., have a market capitalization of at least $14.5 billion (as of 2025), be highly liquid, and have a public float of at least 50% of its shares. Additionally, the company must have positive earnings in the most recent quarter and over the sum of its most recent four quarters.

Some of the most recognizable names in the S&P 500 include Apple, Microsoft, Amazon, Johnson & Johnson, JPMorgan Chase, and ExxonMobil. These companies are selected by a committee that reviews eligibility and ensures the index remains representative of the broader market.

How It Works The S&P 500 is a market-capitalization-weighted index, meaning that companies with larger market values have a greater influence on the index’s performance. For example, a significant movement in Apple’s stock price will affect the index more than a similar movement in a smaller company’s stock. This weighting system helps reflect the real impact of large corporations on the economy.

The index is updated in real time during trading hours and is used by investors to gauge market trends. It also serves as the basis for many investment products, such as mutual funds and exchange-traded funds (ETFs), which aim to replicate its performance.

Why It Matters The S&P 500 is considered a leading indicator of U.S. equity markets and the economy as a whole. When the index rises, it often signals investor confidence and economic growth. Conversely, a decline may indicate uncertainty or economic slowdown. Because it includes companies from diverse sectors, the S&P 500 provides a more balanced view than narrower indices like the Dow Jones Industrial Average, which only tracks 30 companies.

Investment and Strategy Many investors use the S&P 500 as a benchmark to measure the performance of their portfolios. Passive investment strategies, such as index funds, aim to match the returns of the S&P 500 rather than beat it. This approach has gained popularity due to its low fees and consistent long-term performance.

In summary, the S&P 500 is more than just a number—it’s a powerful tool that reflects the pulse of the American economy. By tracking the performance of 500 major companies, it offers insights into market trends, investor sentiment, and economic health. Whether you’re a seasoned investor or just starting out, understanding the S&P 500 is essential to navigating the world of finance.

The Looming Cryptocurrency Crisis: Risks on the Horizon

Cryptocurrency has revolutionized the financial landscape, offering decentralized alternatives to traditional banking and investment systems. However, as digital assets become more integrated into global markets, concerns about a potential future cryptocurrency crisis are mounting. From regulatory uncertainty to systemic vulnerabilities, the risks associated with crypto are increasingly being scrutinized by economists, governments, and investors.

One of the most pressing concerns is regulatory instability. Cryptocurrencies operate in a fragmented legal environment, with different countries adopting varying stances—from full embrace to outright bans. The lack of unified global regulation creates loopholes that can be exploited for money laundering, tax evasion, and fraud. If major economies suddenly impose strict regulations or sanctions, it could trigger a rapid devaluation of crypto assets and erode investor confidence.

Another risk stems from market volatility and speculative behavior. Unlike traditional assets backed by tangible value or government guarantees, cryptocurrencies are often driven by hype, social media trends, and speculative trading. This creates a fragile ecosystem where prices can swing wildly. A sudden crash—similar to the 2022 Terra/Luna collapse—could wipe out billions in investor wealth and destabilize related financial institutions.

***

***

Technological vulnerabilities also pose a threat. While blockchain is considered secure, the platforms built on it are not immune to hacks, bugs, or exploitation. High-profile breaches of exchanges and wallets have already resulted in massive losses. As crypto adoption grows, so does the incentive for cybercriminals to target these systems. A coordinated attack on a major exchange or blockchain network could have cascading effects across the entire crypto economy. Geopolitical tensions may also catalyze a crisis. For instance, recent reports suggest that aggressive trade policies—such as the U.S. imposing 100% tariffs on Chinese imports—can indirectly impact crypto markets by shaking investor sentiment and triggering sell-offs.

The interconnection with traditional finance is another area of concern. As banks and hedge funds increasingly invest in crypto, the line between decentralized finance and conventional markets blurs. This integration means that a crypto collapse could spill over into broader financial systems, potentially triggering a global crisis. The 2023 banking collapses, which were partially linked to crypto exposure, serve as a warning of how intertwined these systems have become.

Geopolitical tensions may also catalyze a crisis. For instance, recent reports suggest that aggressive trade policies—such as the U.S. imposing 100% tariffs on Chinese imports—can indirectly impact crypto markets by shaking investor sentiment and triggering sell-offs. In such scenarios, cryptocurrencies may not serve as the safe haven they were once believed to be.

Lastly, overreliance on stablecoins and algorithmic assets introduces systemic risk. Many investors use stablecoins to hedge volatility, but these assets are only as stable as their underlying reserves and governance. If a major stablecoin fails, it could lead to a liquidity crunch and panic across exchanges and DeFi platforms.

In conclusion, while cryptocurrency offers transformative potential, it also carries significant risks that could culminate in a future crisis. To mitigate these dangers, stakeholders must push for clearer regulations, stronger technological safeguards, and more transparent financial practices. Without proactive measures, the next financial meltdown may not come from Wall Street—but from the blockchain.

NOTE: A crypto mogul has been found dead inside his luxury car in Ukraine after the digital currency market nosedived. Konstantin Galich, 32, also known as Kostya Kudo, has died after one of the worst turmoils shook the cryptocurrency market. The entrepreneur, who became a well-known figure in the crypto industry, was reportedly found with a gunshot wound to his head in his black Lamborghini parked up in Kyiv’s Obolonskyi neighbourhood. His death was later confirmed on his Telegram channel in a post saying ‘Konstantin Kudo tragically passed away. The causes are being investigated. We will keep you posted on any further news.’

The October 2025 Stock Market Crash: A Perfect Storm of Geopolitics and Investor Panic

The weekend of October 10–12, 2025, marked one of the most dramatic downturns in global financial markets in recent memory. What began as a series of unsettling headlines quickly snowballed into a full-blown market crash, sending shockwaves through economies and portfolios worldwide. This event was not the result of a single catalyst but rather a convergence of geopolitical tensions, speculative excess, and investor psychology.

At the heart of the crisis was a sudden escalation in U.S.–China trade relations. President Donald Trump abruptly canceled a scheduled diplomatic meeting with Chinese President Xi Jinping and announced a sweeping 100% tariff on all Chinese imports. This move reignited fears of a prolonged trade war, reminiscent of the economic standoff that rattled markets in the late 2010s. Investors, already jittery from months of uncertainty, interpreted the announcement as a signal of deteriorating global cooperation and retaliatory economic measures to come.

The impact was immediate and severe. Major U.S. indices plummeted: the S&P 500 dropped 2.7%, the Nasdaq fell 3.6%, and the Dow Jones Industrial Average lost 1.9%. These declines marked the worst single-day performance since April and triggered automatic trading halts in several sectors. The selloff was not confined to the United States; European and Asian markets mirrored the panic, with steep losses across the board.

Compounding the crisis was a massive liquidation in the cryptocurrency market. As traditional assets tumbled, investors rushed to offload digital holdings, leading to the largest crypto wipeout in history. Trillions of dollars in value evaporated within hours, further destabilizing investor confidence and draining liquidity from the broader financial system.

Another underlying factor was growing concern over the valuation of artificial intelligence (AI) stocks. The International Monetary Fund (IMF) had recently issued a warning that the AI sector was exhibiting signs of a speculative bubble, drawing parallels to the dot-com era. With many AI companies trading at astronomical price-to-earnings ratios, the crash exposed the fragility of investor sentiment and the dangers of overexuberance in emerging technologies.

Perhaps most telling was the psychological shift among investors. The weekend saw widespread capitulation, with many choosing to exit the market entirely rather than weather further volatility. This behavior—marked by fear-driven decision-making and herd mentality—is often a hallmark of deeper financial crises. It underscores the importance of trust and stability in maintaining market equilibrium.

In conclusion, the October 2025 stock market crash was a multifaceted event driven by geopolitical shocks, speculative risk, and emotional contagion. It serves as a stark reminder of how interconnected and fragile global markets have become. As policymakers and investors assess the damage, the focus must shift toward restoring confidence, recalibrating risk, and ensuring that future growth is built on sustainable foundations rather than speculative fervor.

COMMENTS APPRECIATED

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Buying or selling stocks requires access to one of the major exchanges, such as the New York Stock Exchange (NYSE) or the National Association of Securities Dealers Automated Quotations (NASDAQ). To trade on these exchanges, you must be a member of the exchange or belong to a member firm. Member firms and many individuals who work for them are licensed as brokers or broker-dealers by the Financial Industry Regulatory Authority (FINRA).

And so, a stockbroker executes orders in the market on behalf of clients. A stockbroker may also be known as a registered representative or investment advisor. Most stockbrokers work for a brokerage firm and handle transactions for several individual and institutional customers. Stockbrokers are often paid on commission, although compensation methods vary by employer.

Remember: SBs work for their firm and not the client. Stock brokers are not fiduciaries.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on October 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

The VIX, or CBOE Volatility Index, is often called the “fear gauge” of the stock market. It measures the market’s expectations for volatility over the next 30 days, based on options prices for the S&P 500.

The Dow Jones Industrial Average (DJIA), often referred to simply as “the Dow,” is one of the oldest and most well-known stock market indices in the world. It was created in 1896 by Charles Dow, the co-founder of The Wall Street Journal, and is designed to represent the performance of the broader U.S. stock market, specifically focusing on 30 large, publicly traded companies. These companies are considered leaders in their respective industries and serve as a barometer for the overall health of the U.S. economy.

The Composition of the DJIA

The DJIA includes 30 companies, which are selected by the editors of The Wall Street Journal based on various factors such as market influence, reputation, and the stability of the company. These companies represent a wide array of sectors, including technology, finance, healthcare, consumer goods, and energy. Notably, the companies chosen for the DJIA are not necessarily the largest companies in the U.S. by market capitalization, but rather those that are most indicative of the broader economy. Some of the prominent companies listed in the DJIA include names like Apple, Microsoft, Coca-Cola, and Johnson & Johnson.

However, the list of 30 companies is not static. Over time, companies may be added or removed to reflect changes in the economic landscape. For example, if a company experiences significant decline or no longer represents a leading sector, it might be replaced with another company that better reflects modern economic trends. This periodic reshuffling ensures that the DJIA continues to be a relevant measure of economic activity.

How the DJIA is Calculated

The DJIA is a price-weighted index, which means that the value of the index is determined by the share price of the component companies, rather than their market capitalization. To calculate the DJIA, the sum of the stock prices of all 30 companies is divided by a special divisor. This divisor adjusts for stock splits, dividends, and other corporate actions to maintain the integrity of the index over time. The price-weighted method means that higher-priced stocks have a greater impact on the movement of the index, regardless of the overall size or economic weight of the company.

For instance, if a company with a higher stock price like Apple experiences a significant change in value, it will influence the DJIA more than a company with a lower stock price, even if the latter has a larger market capitalization. This makes the DJIA somewhat different from other indices, like the S&P 500, which is weighted by market cap and gives more weight to larger companies in terms of their economic impact.

Significance of the DJIA

The DJIA is widely regarded as a barometer of the U.S. stock market’s performance. Investors and analysts closely monitor the movements of the Dow to gauge the overall health of the economy. When the DJIA rises, it generally suggests that investors are optimistic about the economic outlook and that large companies are performing well. Conversely, when the DJIA falls, it often signals economic uncertainty or a downturn in market conditions.

Despite being a narrow index, with only 30 companies, the DJIA holds substantial sway in financial markets. It is widely covered in the media and is often cited in discussions about the state of the economy. In fact, the performance of the DJIA is considered a key indicator of investor sentiment and economic confidence.

However, the DJIA has its limitations. Since it only includes 30 companies, it does not necessarily represent the broader market or capture the performance of smaller companies. Other indices, like the S&P 500, which includes 500 companies, offer a more comprehensive view of the market’s performance.

Conclusion

The Dow Jones Industrial Average is a key metric for understanding the state of the U.S. economy and the stock market. Although it has evolved over the years, it continues to provide valuable insights into the performance of large, influential companies. While it is not a perfect reflection of the market as a whole, the DJIA remains one of the most important and widely recognized indices in global finance. Through its historical significance and its role in shaping market sentiment, the Dow has cemented its place as a cornerstone of financial analysis.

Artificial Intelligence and Investing: A Transformative Partnership

Artificial Intelligence (AI) is revolutionizing the world of investing, reshaping how decisions are made, risks are assessed, and portfolios are managed. As financial markets grow increasingly complex and data-driven, AI offers powerful tools to navigate this landscape with greater precision, speed, and insight.

At its core, AI refers to systems that can perform tasks typically requiring human intelligence—such as learning, reasoning, and problem-solving. In investing, this translates into algorithms that can analyze vast amounts of financial data, detect patterns, and make predictions with remarkable accuracy. Machine learning, a subset of AI, enables these systems to improve over time by learning from new data, making them especially valuable in dynamic markets.

One of the most significant applications of AI in investing is algorithmic trading. These systems can execute trades at lightning speed, responding to market fluctuations in milliseconds. By analyzing historical data and real-time market conditions, AI-driven trading platforms can identify optimal entry and exit points, often outperforming human traders. High-frequency trading firms have long relied on such technologies to gain competitive advantages.

AI also enhances portfolio management through robo-advisors—digital platforms that use algorithms to provide personalized investment advice. These tools assess an investor’s goals, risk tolerance, and time horizon, then construct and manage a diversified portfolio accordingly. Robo-advisors democratize access to financial planning, offering low-cost, automated solutions to individuals who might not afford traditional advisory services.

Risk assessment is another area where AI shines. By processing alternative data sources—such as social media sentiment, news articles, and satellite imagery—AI can uncover hidden risks and opportunities. For instance, a sudden spike in negative sentiment around a company on Twitter might signal reputational issues, prompting investors to reevaluate their positions. AI models can also forecast macroeconomic trends, helping investors anticipate shifts in interest rates, inflation, or geopolitical events.

Moreover, AI is transforming fundamental analysis. Natural language processing (NLP) allows machines to read and interpret earnings reports, SEC filings, and analyst commentary. This enables investors to extract insights from unstructured data that would be time-consuming to analyze manually. AI can even detect subtle linguistic cues that may indicate a company’s future performance or management’s confidence.

Despite its advantages, AI in investing is not without challenges. Models can be opaque, making it difficult to understand how decisions are made—a phenomenon known as the “black box” problem. There’s also the risk of overfitting, where algorithms perform well on historical data but fail in real-world scenarios. Ethical concerns, such as bias in data and the potential for market manipulation, must also be addressed.

In conclusion, AI is reshaping the investing landscape, offering tools that enhance efficiency, accuracy, and accessibility. While it’s not a panacea, its integration into financial markets marks a profound shift in how capital is allocated and wealth is managed. As technology continues to evolve, investors who embrace AI will be better positioned to thrive in an increasingly data-driven world.

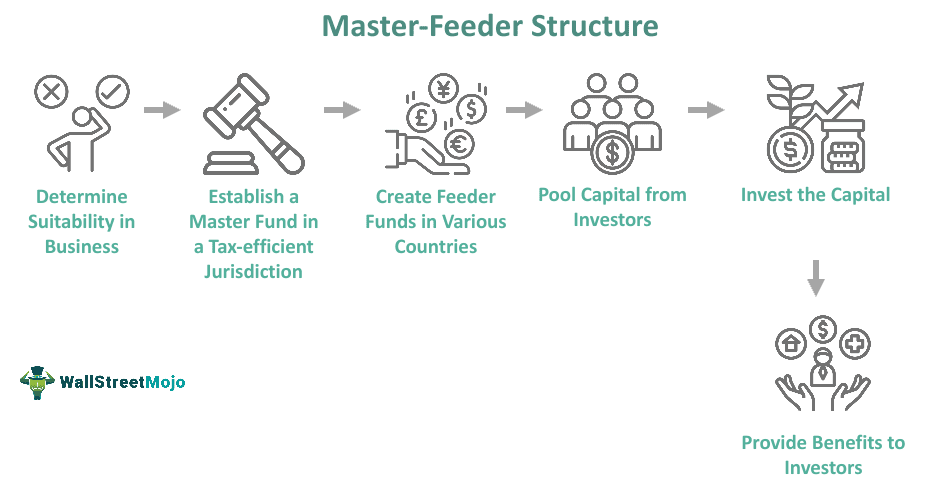

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

The hedge fund manager I am considering also runs an offshore fund under a “master feeder” arrangement.

A PHYSICIAN’S QUESTION:What does this mean? In which fund should I invest?

The master feeder arrangement is a two-tiered investment structure whereby investors invest in the feeder fund. The feeder fund in turn invests in the master fund. The master fund is therefore the one that is actually investing in securities. There may be multiple feeder funds under one master fund. Feeder funds under the same master can differ drastically in terms of fees charged, minimums required, types of investors, and many other features – but the investment style will be the same because only the master actually invests in the market.

A master feeder structure is a very popular arrangement because it allows a portfolio manager to pool both onshore and offshore assets into one investment vehicle (the master fund) that allocates gains and losses in an asset-based, proportional manner back to the onshore and offshore investors. All investors, both offshore and onshore, get the same return. In this manner, the portfolio manager, despite offering more than one fund with different characteristics to different populations, is not faced with the dilemma of which fund to favor with the best investment ideas.

A manager may offer an offshore fund because there is demand for that manager’s skill either abroad, where investors may wish to preserve anonymity, or more commonly where investors simply do not wish to become entangled with the United States tax code. American citizens should generally avoid the offshore fund, since American citizens are taxed on their allocated share of offshore corporation profits whether or not a distribution occurs. Therefore, there is no benefit for most American taxpayers investing in an offshore fund.

Tax-exempt institutions, such as medical foundations, in the United States may have reason to consider an offshore hedge fund, however. Domestic tax-exempt organizations are generally not subject to unrelated business taxable income (UBTI) – the portion of hedge fund income that comes about as a result of the use of leverage – when investing with an offshore corporation. If the same tax-exempt organization were to invest in a domestic fund, and if UBTI was generated, then the organization would have to pay taxes on that UBTI. Most domestic hedge funds generate UBTI.

After a lifetime of hard work practicing medicine and saving, you’re at the retirement finish line. Instead of a paycheck, you’re relying on your nest egg and investment income to cover the bills. Picking the right investments is even more important, as you won’t have much chance to recover as a retired MD, DO, DPM or DDS.

“You made it to the top of the mountain through a systematic approach and are trying to make your way down safely,” says retirement planner John Gillet John Gillet in Hollywood, Fla. “Why throw all caution to the wind and try something different now?”

***

***

Definitions

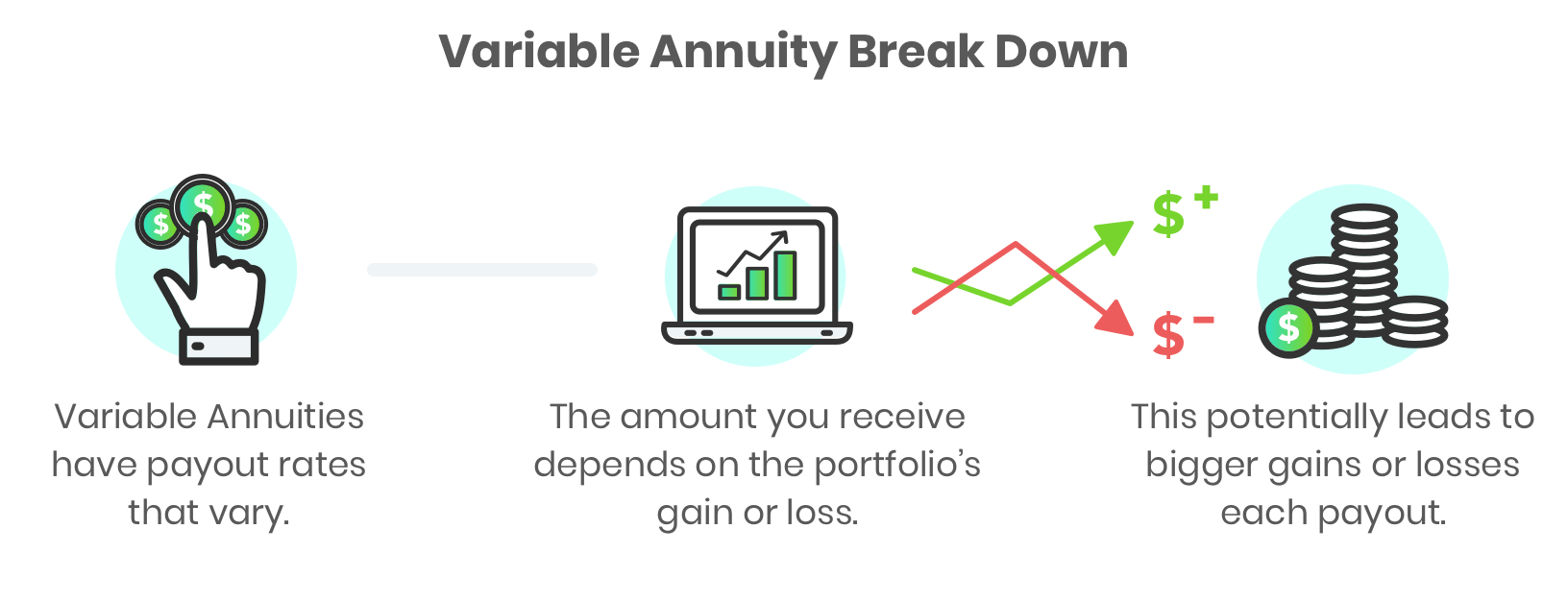

An annuity is an insurance contract designed to grow your money and then repay it as income. There are different versions. An immediate annuity turns your lump sum into future guaranteed income payments, like your own personal pension. They are simple to understand with no or small fees.

Fixed annuities pay a guaranteed interest rate over a set period to grow your money, like 5% a year for five years. These options could make sense as part of a retirement plan.

A variable annuity, on the other hand, invests your savings in mutual funds. While you can buy riders that guarantee a minimum income, you’ll be paying very much for it. “All in, the annual fees can be 3% or more of your balance,” says Jeff Bailey, an advisor from Nashville. “That’s a huge withdrawal rate from your portfolio versus investing on your own.”

The variable annuity will lock up your money for years. If you cancel early, you owe a surrender charge that could start at 7% or more of your annuity balance before gradually going down as time goes by. “Clients believe they can walk away with their contract value, but that’s often not true,” says Bailey.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Asset allocation is one of the key factors contributing to long-term investment success.

When designing a portfolio that represents their risk tolerance, investors should be aware that a portfolio that is 50% stocks is likely to obtain approximately half of the gain when the market advances but suffer only half the loss when the market declines.

This general principle frequently holds true over extended investing cycles, but can waiver during shorter holding periods.

Case Model

For example, a fairly typical physician client of mine who has a 50% stock, 50% bond portfolio has obtained a return of 4.62% over the last 12 months, while the S&P 500 has obtained a return of 14.31% over the same time period (as of 10/30/14).

An investor expecting to obtain half the return of the index would anticipate a return of 7.15%, and by this measuring stick, has underperformed the market by over 2.50% during the last year.

What caused this differential?

Answer

The issue resides in how we define “the market.” In this example, we use the S&P 500 index as a measure for how the market as a whole is performing. As you may know, the S&P 500 (and the Dow Jones Industrial Average, for that matter) consists solely of large company U.S. stocks.

Of course, a diversified portfolio owns a mixture of large, mid, and small cap U.S. stocks, as well as international and emerging market equities. Consequently, comparing the performance of a basket of only large cap stocks to the performance of a diversified portfolio made up of a variety of different asset classes isn’t an apples-to-apples comparison.

***

***

Frequently, the diversified portfolio will outperform the non-diversified large cap index because several of the components of the diversified portfolio will obtain higher returns than those achieved by large cap holdings.

However, the past 12 months has been a case where a diversified portfolio underperformed the large cap index because large cap stocks were the best performing asset class over the time period. In fact, over the last twelve months, there has been a direct correlation between company size and stock performance (as of 10/30/14):

Large Cap Stocks (S&P 500): 14.92%

Mid Cap Stocks (Russell Mid Cap): 11.08%

Small Cap Stocks (Russell 2000): 4.45%

International Stocks (Dow Jones Developed Markets): -1.05%

Since large cap stocks were the best performing element of a diversified portfolio over the last 12 months, in retrospect, an investor would have obtained a superior return by owning only large cap stocks during the period as opposed to owning a diversified mix of different equities. Does this mean owning only large cap stocks rather than a diversified portfolio is the best investment approach going forward? Of course not.

Year after year, we don’t know which asset category will provide the best return and a diversified portfolio ensures we have exposure to each year’s big winner. Additionally, although large caps were this year’s winner, they could easily be next year’s big loser, and a diversified portfolio ensures we don’t have all our investment eggs in one basket.

Don’t be overly concerned if your diversified portfolio is underperforming a non-diversified benchmark over a short period of time. As always, long-term results should be more heavily weighted than short-term swings, and having a diversified portfolio is likely to maximize the probability of coming out ahead over an extended period.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

ME-P readers might believe the hedge fund industry is a small, exclusive club of elites, rich investors. But a new count by Preqin shows that it’s actually a large—and growing—sector of investing.

In fact, there may be more hedge funds globally (30,000+) than Burger King locations (18,700), and more more hedge fund managers than Taco Bell managers, per the FTE

The major indexes ticked lower last week, though, as artificial intelligence names like Oracle got hit after some analysts expressed concerns over the eye-watering costs of the AI build-out.

Posted on September 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

A meme is an idea, behavior, or style that spreads by means of imitation from person to person within a culture and often carries symbolic meaning representing a particular phenomenon or theme. A meme acts as a unit for carrying cultural ideas, symbols, or practices, that can be transmitted from one mind to another through writing, speech, gestures, rituals, or other imitable phenomena with a mimicked theme. Supporters of the concept regard memes as cultural analogues to genes in that they self-replicate, mutate, and respond to selective pressure. In popular language, a meme may refer to an internet meme, typically an image, that is remixed, copied, and circulated in a shared cultural experience online.

EXAMPLE Investing Meme:

“Sell in May and Go Away” is an investment strategy for stocks based on a theory (sometimes known as the Halloween indicator) that the period from November to April inclusive has significantly stronger stock market growth on average than the other months. In such strategies, stock holdings are sold or minimized at about the start of May and the proceeds held in cash; stocks are bought again in the autumn. So, “Sell in May” can be characterized as the memetic belief that it is better to avoid holding stock during the summer period.

The Wall Street adage — ‘Sell Rosh Hashana; buy Yom Kippur’ — focuses on the market’s performance between these two Jewish holidays. This seasonal stock-market trading pattern is upon us — and worth observing.

Rosh Hashanah is the Jewish New Year while Yom Kippur is the Day of Atonement. So, according to Mark Hulbert, it might seem arbitrary to make stock-investment decisions by blending religious observance with financial strategy, but there’s one old trading folklore commonly or meme mentioned during this time of year: “Sell Rosh Hashanah, buy Yom Kippur.”

This Wall Street adage suggests that U.S. stocks tend to fall over the 10 days the Jewish High Holidays are observed, so investors would be better off selling beforehand and buying afterward. But some market analysts believe investors should be wary of this seasonal trading pattern this year.

Historically, the “sell Rosh Hashanah, buy Yom Kippur” strategy is closely tied to the stock market’s tendency to under perform in September, with investors often looking to “minimize exposure” during this period, according to Yehuda Leibler, chief strategy and technology officer at ARX Advisory.

The Series 65 exam — the NASAA Investment Advisers Law Examination — is a North American Securities Administrators Association (NASAA) exam administered by FINRA.

The exam consists of 130 scored questions and 10 unscored questions. Candidates have 180 minutes to complete the exam. In order for a candidate to pass the Series 65 exam, they must correctly answer at least 92 of the 130 scored questions.

Economy: Headline PCE rose from 2.6% on an annual basis in July to 2.7% in August, while core PCE stayed flat at 2.9%—all in line with analyst expectations.

Stocks: Solid inflation numbers helped equities arrest their recent selloff and offset the latest batch of tariffs. However, all three major indexes still ended the week lower than where they started.

Commodities: Oil climbed as Ukrainian drones continue to strike Russian energy infrastructure. Meanwhile, gold hit another all-time high, and rose above $3,800 for the first time ever at one point today.

According to Wayne Firebaugh CPA, CFP®, CMP™ alpha measures non-systematic return on investment [ROI], or the return that cannot be attributed to the market.

It shows the difference between a fund’s actual return and its expected performance given the level of systematic (or market) risk (as measured by beta).

Example

For example, a fund with a beta of 1.2 in a market that returns 10% would be expected to earn 12%. If, in fact, the fund earns a return of 14%, it then has an alpha of 2 which would suggest that the manager has added value. Conversely, a return below that expected given the fund’s beta would suggest that the manager diminished value.

In a truly efficient market, no manager should be able to consistently generate positive alpha. In such a market, the endowment manager would likely employ a passive strategy that seeks to replicate index returns. Although there is substantial evidence of efficient domestic markets, there is also evidence to suggest that certain managers do repeat their positive alpha performance.

In fact, a 2002 study by Roger Ibbotson and Amita Patel found that “the phenomenon of persistence does exist in domestic equity funds.” The same study suggested that 65% of mutual funds with the highest style-adjusted alpha repeated with positive alpha performances in the following year.

More Research

Additional research suggests that active management can add value and achieve positive alpha in concentrated portfolios.

A pre 2008 crash study of actively managed mutual funds found that “on average, higher industry concentration improves the performance of the funds. The most concentrated funds generate, after adjusting for risk … the highest performance. They yield an average abnormal return [alpha] of 2.56% per year before deducting expenses and 1.12% per year after deducting expenses.”

FutureMetrics

FutureMetrics, a pension plan consulting firm, calculated that in 2006 the median pension fund achieved record alpha of 3.7% compared to a 60/40 benchmark portfolio, the best since the firm began calculating return data in 1988. Over longer periods of time, an endowment manager’s ability to achieve positive alpha for their entire portfolio is more hotly debated. Dimensional Fund Advisors, a mutual fund firm specializing in a unique form of passive management, compiled FutureMetrics data on 192 pension funds for the period of 1988 through 2005.

Their research showed that over this period of time approximately 75% of the pension funds underperformed the 60/40 benchmark. The end result is that many endowments will use a combination of active and passive management approaches with respect to some portion of the domestic equity segment of their allocation.

Assessment

One approach is known as the “core and satellite” method in which a “core” investment into a passive index is used to capture the broader market’s performance while concentrated satellite positions are taken in an attempt to “capture” alpha. Since other asset classes such as private equity, foreign equity, and real assets are often viewed to be less efficient, the endowment manager will typically use active management to obtain positive alpha from these segments.

Notes:

Ibbotson, R.G. and Patel, A.K. Do Winners Repeat with Style? Summary of Findings – Ibbotson & Associates, Chicago (February 2002).

Kacperczyk, M.T., Sialm, C., and Lu Zheng. On Industry Concentration of Actively Managed Equity Mutual Funds. University of Michigan Business School. (November 2002).

2007 Annual US Corporate Pension Plan Best and Worst Investment Performance Report. FutureMetrics, April 20, 2007.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@outlook.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on September 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Bonds: The 10-year Treasury yield popped on solid economic data yesterday, including weekly jobless claims falling to their lowest since mid-July and Q2 GDP rising unexpectedly.

Stocks: But good news for the labor market and economy is bad news for anyone hoping the Federal Reserve cuts interest rates next month, and the major indexes sank for a third day in a row yesterday. All eyes now turn to today’s key PCE reading.

Crypto: Digital assets continued to tumble yesterday with ether falling below $4,000 for the first time in months. There may be more pain ahead: $22 billion in crypto options expire today.

An app, which is short for “application,” is a type of software that can be installed and run on a computer, tablet, smartphone or other electronic devices. An app most frequently refers to a mobile application or a piece of software that is installed and used on a computer. Most apps have a specific and narrow function.

An easy and fairly cheap way for novices to get into investing is to use a robo-advisor. Basically, the funds you contribute will be invested by an algorithm based upon your goals, which are usually determined by taking a survey. This helps keep fees low; the algorithm doesn’t rely on a human expert to make trades, and you don’t have to spend significant amounts of time researching your investments. While this is a good way to start, it may not be the best option in the long run.

Online Brokerage or Investment Apps

More options are becoming available all the time, and they have opened trading to a much larger percentage of the population. That is a great thing, but it’s important to remember that “easier to invest” doesn’t necessarily mean it’s easy to invest well.

Be wary of apps that “gamify” trading and encourage risky choices. Keep in mind that trusted names offer more security, so do your research when you are selecting a platform.

A Financial Self Discovery Questionnairefor Medical Professionals

For understanding your relationship with money, it is important to be aware of yourself in the contexts of culture, family, value systems and experience. These questions will help you. This is a process of self-discovery. To fully benefit from this exploration, please address them in writing. You will simply not get the full value from it if you just breeze through and give mental answers. While it is recommended that you first answer these questions by yourself, many people relate that they have enjoyed the experience of sharing them with others who are important to them.

As you answer these questions, be conscious of your feelings, actually describing them in writing as part of your process.

Childhood

What is your first memory of money?

What is your happiest moment with Money? Your most unhappy?

Name the miscellaneous money messages you received as a child.

How were you confronted with the knowledge of differing economic circumstances among people, that there were people “richer” than you and people “poorer” than you?

Cultural heritage

What is your cultural heritage and how has it interfaced with money?

To the best of your knowledge, how has it been impacted by the money forces? Be specific.

To the best of your knowledge, does this circumstance have any motive related to Money?

Speculate about the manners in which your forebears’ money decisions continue to affect you today?

Family

How is/was the subject of money addressed by your church or the religious traditions of your forebears?

What happened to your parents or grandparents during the Depression?

How did your family communicate about money?

How? Be as specific as you can be, but remember that we are more concerned about impacts upon you than historical veracity.

When did your family migrate to America (or its current location)?

What else do you know about your family’s economic circumstances historically?

Your parents

How did your mother and father address money?

How did they differ in their money attitudes?

How did they address money in their relationship?

Did they argue or maintain strict silence?

How do you feel about that today?

Please do your best to answer the same questions regarding your life or business partner(s) and their parents.

Childhood: Revisited

How did you relate to money as a child? Did you feel “poor” or “rich”? Relatively? Or, absolutely? Why?

Were you anxious about money? Did you receive an allowance? If so, describe amounts and responsibilities.

Did you have household responsibilities?

Did you get paid regardless of performance?

Did you work for money?

If not, please describe your thoughts and feelings about that.

***

***

Same questions, as a teenager, young adult, older adult.

Credit

When did you first acquire something on credit?

When did you first acquire a credit card?

What did it represent to you when you first held it in your hands?

Describe your feelings about credit.

Do you have trouble living within your means?

Do you have debt?

Adulthood

Have your attitudes shifted during your adult life? Describe.

Why did you choose your personal path? a) Would you do it again? b) Describe your feelings about credit.

Adult attitudes

Are you money motivated? If so, please explain why? If not, why not? How do you feel about your present financial situation? Are you financially fearful or resentful? How do you feel about that?

Will you inherit money? How does that make you feel?

If you are well off today, how do you feel about the money situations of others? If you feel poor, same question.

How do you feel about begging? Welfare? If you are well off today, why are you working?

Do you worry about your financial future?

Are you generous or stingy? Do you treat? Do you tip?

Do you give more than you receive or the reverse? Would others agree?

Could you ask a close relative for a business loan? For rent/grocery money?

Could you subsidize a non-related friend? How would you feel if that friend bought something you deemed frivolous?

Do you judge others by how you perceive they deal with their Money? Do you feel guilty about your prosperity? Are your siblings prosperous?

What part does money play in your spiritual life?

Do you “live” your Money values?

Conclusion

There may be other questions that would be useful to you. Others may occur to you as you progress in your life’s journey. The point is to know your personal money issues and their ramifications for your life, work, and personal mission.

This will be a “work-in-process” with answers both complex and incomplete. Don’t worry.

Just incorporate fine-tuning into your life’s process.

The Series 6 exam — the Investment Company and Variable Contracts Products Representative Qualification Examination (IR) — assesses the competency of an entry-level representative to perform their job as an investment company and variable contracts products representative.

The exam measures the degree to which each candidate possesses the knowledge needed to perform the critical functions of an investment company and variable contract products representative, including sales of mutual funds and variable annuities.

Candidates must pass the Securities Industry Essentials (SIE) exam and the Series 6 exam to obtain the Investment Company and Variable Contracts Products registration.

The study of behavioral economics has revealed much about how different biases can affect our finances—often for the worse.

Take loss aversion: Because we feel a financial setback more acutely than a commensurate gain, we often cling to failed investments to avoid realizing the loss. Another potential hazard is present bias, or the tendency to prefer instant gratification over long-term reward, even if the latter gain is greater.

When it comes to money, sometimes it’s difficult to make rational decisions. Here, are three behavioral financial biases that could be impeding financial goals.

ANCHORING BIAS

Anchoring Bias happens when we place too much emphasis on the first piece of information we receive regarding a given subject. Anchoring is the mental trick your brain plays when it latches onto the first piece of information it gets, no matter how irrelevant. You might know this as a ‘first impression’ when someone relies on their own first idea of a person or situation.

Example: When shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this financial advice, even though the guideline provided may cause us to spend more than we can afford.

Example: Imagine you’re buying a car, and the salesperson starts with a high price. That number sticks in your mind and influences all your subsequent negotiations. Anchoring can skew our decisions and perceptions, making us think the first offer is more important than it is. Or, subsequent offers lower than they really are.

Example: Imagine an investor named Jane who purchased 100 shares of XYZ Corporation at $100 per share several years ago. Over time, the stock price declined to $60 per share. Jane is anchored to her initial price of $100 and is reluctant to sell at a loss because she keeps hoping the stock will return to her original purchase price. She continues to hold onto the stock, even as it declines, due to her anchoring bias. Eventually, the stock price drops to $40 per share, resulting in significant losses for Jane.

In this example, Jane’s nchoring bias to the original purchase price of $100 prevents her from rationalizing to sell the stock and cut her losses, even though market conditions have changed. So, the next time you’re haggling for your self, a potential customer or client, or making another big financial decision, be aware of that initial anchor dragging you down.

HERD MENTALITY BIAS

Herd Mentality Bias makes it very hard for humans to not take action when everyone around us does.

Example: We may hear stories of people making significant monetary profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Example: During the dotcom bubble of the late 1990’s many investors exhibited a herd mentality. As technology stocks soared to astronomical valuations, investors rushed to buy these stocks driven by the fear of missing out on the gains others were enjoying. Even though some of these stocks had questionable fundamentals, the herd mentality led investors to follow the crowd.

In this example, the herd mentality contributed to the overvaluation of technology stocks. Eventually, it led to the dot-com bubble’s burst, causing significant losses for those who had unthinkingly followed the crowd without conducting proper research or analysis.

OVERCONFIDENT INVESTING BIAS

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

ASSESSMENT

Finally, questions remain after consuming this cognitive bias review.

Question: Can behavioral cognitive biases be eliminated by financial advisors in prospecting and client sales endeavors?

A: Indeed they can significantly reduce their impact by appreciating and understanding the above and following a disciplined and rational decision-making sales process.

Question: What is the role of financial advisors in helping clients and prospects address behavioral biases?

A: Financial advisors can provide an objective perspective and help investors recognize and address their biases. They can assist in creating well-structured investment and financial plans, setting realistic goals, and offering guidance to ensure investment decisions align with long-term objectives.

Question:How important is self-discipline in overcoming behavioral biases?

A; Self-discipline is crucial in overcoming behavioral biases. It helps investors and advisors adhere to their investment plans, avoid impulsive decisions, and stay focused on long-term goals reducing the influence of emotional and cognitive biases.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological biases to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

REFERENCES:

Marcinko, DE; Dictionary of Health Insurance and Managed Care. Springer Publishing Company, New York, 2007.

Marcinko, DE: Comprehensive Financial Planning Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2016.

Marcinko, DE: Risk Management, Liability and Insurance Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2017.

Nofsinger, JR: The Psychology of Investing. Rutledge Publishing, 2022

Winters, Scott: The 10X Financial Advisor: Your Blueprint for Massive and Sustainable Growth. Absolute Author Publishing House, 2020.

Investment bankers are not really bankers at all. The fact that the word banker appears in the name is partially responsible for the false impressions that exist in the medical community regarding the functions they perform.

For example, they are not permitted to accept deposit, provide checking accounts, or perform other activities normally construed to be commercial banking activities. An investment bank is simply a firm that specializes in helping other corporations obtain money they need under the most advantageous terms possible. When it comes to the actual process of having securities issued, the corporation approaches an investment banking firm, either directly, or through a competitive selection process and asks it to act as adviser and distributor.

Investment bankers, or under writers, as they are sometimes called, are middlemen in the capital markets for corporate securities. The corporation requiring the funds discusses the amount, type of security to be issued, price and other features of the security, as well as the cost to issuing the securities. All of these factors are negotiated in a process known as negotiated underwriting. If mutually acceptable terms are reached, the investment banking firm will be the middle man through which the securities are sold to the general public. Since such firms have many customers, they are able to sell new securities, without the costly search that individual corporations may require to sell its own security.

Thus, although the firm in need of additional capital must pay for the service, it is usually able to raise the additional capital at less expense through the use of an investment banker, than by selling the securities itself. The agreement between the investment banker and the corporation may be one of two types. The investment bank may agree to purchase, or underwrite, the entire issue of securities and to re-offer them to the general public. This is known as a firm commitment.

When an investment banker agrees to underwrite such a sale; it agrees to supply the corporation with a specified amount of money. The firm buys the securities with the intention to resell them. If it fails to sell the securities, the investment banker must still pay the agreed upon sum.

Thus, the risk of selling rests with the underwriter and not with the company issuing the securities.

The alternative agreement is a best efforts agreement in which the investment banker makes his best effort to sell the securities acting on behalf of the issuer, but does not guarantee a specified amount of money will be raised. When a corporation raises new capital through a public offering of stock, one might inquire where the stock comes from. The only source the corporation has is authorized, but previously un-issued stock. Anytime authorized, but previously un-issued stock (new stock) is issued to the public, it is known as a primary offering.

If it’s the very first time the corporation is making the offering, it’s also known as the Initial Public Offering (IPO). Anytime there is a primary offering of stock, the issuing corporation is raising additional equity capital.

A secondary offering, or distribution, on the other hand, is defined as an offering of a large block of outstanding stock. Most frequently, a secondary offering is the sale of a large block of stock owned by one or more stockholders. It is stock that has previously been issued and is now being re-sold by investors. Another case would be when a corporation re-sells its treasury stock.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Series 7 exam — the General Securities Representative Qualification Examination (GS) — assesses the competency of an entry-level registered representative to perform their job as a general securities representative.

The exam measures the degree to which each candidate possesses the knowledge needed to perform the critical functions of a general securities representative, including sales of corporate securities, municipal securities, investment company securities, variable annuities, direct participation programs, options and government securities.

Stocks: The Russell 2000 went 967 days without hitting a new record high until Thursday. But, it looks like it will have to keep waiting for the next one—the small-cap-focused index fell, even as the DJIA, NASDAQ and S&P 500 rose to new closing highs on Friday.* Bonds: 2-year yields and 10-year yields both hit two-week intra-day highs even after the FOMC cut interest rates, indicating that traders still aren’t sure how the economy will perform in the months ahead. Commodities: Arabica futures fell on reports that lawmakers will introduce a bipartisan bill to exempt coffee from tariffs.

Posted on September 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

***

Federal Reserve Chairman Jerome Powell just announced that the central bank [FOMC] would cut interest rates amid President Donald Trump’s attempts to reshape the Fed’s independence.

The chairman announced that the Federal Reserve would cut the interest rate by .25 points, the first time that it cut interest rates since December.

A paradox is a statement or situation that seems contradictory but actually makes sense when you think about it more deeply. It challenges logic and often reveals a hidden truth.

FLEXIBLY DOGMATIC PARADOX

The Flexibly Dogmatic Paradox suggests that no matter how sensible your financial planning, investing or wealth management process is there will be uncomfortably long periods when it looks broken. And process is the best way of ensuring you keep standing for something because if you don’t stand for something, you’ll fall for anything. This is why, when assessing an investment fund, focus 50% on the manager’s character and 50% on their process. Everything else is detail. There are few guarantees in investing, but the fact that markets will batter you emotionally is one of them.

Example: During volatile times, the temptation to abandon the process is strong. But that’s why it’s there. Process is what forces one fund manager to keep buying unbroken companies when everyone else thinks they’re bust, and another to keep faith with a top-quality company when the mob says it’s too expensive The best fund managers dogmatically stick to their process when it’s out of favor. Then, when it returns to favor, the elastic pings back: they recapture lost ground surprisingly fast. However, every rule has an exception. And spotting the exceptions to their process is something the true greats have a knack for buying and selling.

***

***

Example: In 2007, US value manager Bill Miller had the makings of an investment legend, but the financial crisis wrecked all that. His process told him to double down into falling share prices, which had worked well for years. But it doesn’t work if the companies go bust, which many of his financial stocks did in 2008.

The fact is that no matter how good it is, a process operated without human judgment is just an algorithm. The best fund managers and financial prospectors and sales men/women know this.

They stick dogmatically to their process but somehow remain flexible enough to spot the occasions when it’s about to drive them into a brick wall.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

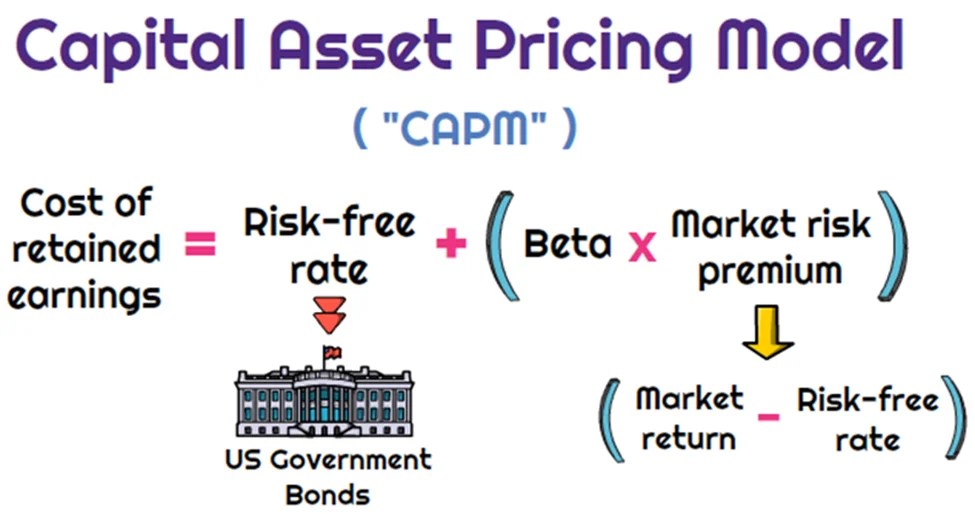

Dr. Harry Markowitz is credited with developing the framework for constructing investment portfolios based on the risk-return tradeoff. William Sharpe, John Lintner, and Jan Mossin are credited with developing the Capital Asset Pricing Model (CAPM).