BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on January 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

BY ERIC BRICKER MD

With 43 Million Americans Having Lost Their Job at Some Point During the Pandemic and About 1/2 Those Jobs Providing Health Insurance… the 1st Group–People Who Do Not Have Health Insurance–Needs to Be Aware of How These Programs Work.

In this Video You Will Learn the Patient Assistance Program Process for:

1) 2 of the Most Common Types of Insulin

2) The Highest-Revenue Medication in America: Humira

**Note: At the Time of the Video’s Recording, the Unemployment Rate in the US was 15%. As of November 2021, the Unemployment Rate is 4.2%.

Posted on January 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

31% of Americans Don’t Know How They’d Pay for Severe Illness

A recent survey by HealthcareInsider that polled 1,062 adults aged 18 and up asked, “If you were to experience a severe illness how would you pay for treatment?”

• Don’t know: 31% • Credit card: 26% • Non-retirement savings: 17% • Borrow money from family: 16% • Retirement savings: 11% • Health Savings Account: 9% • Borrow from a finance institution: 8% • Crowdfund online: 6%

Posted on January 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

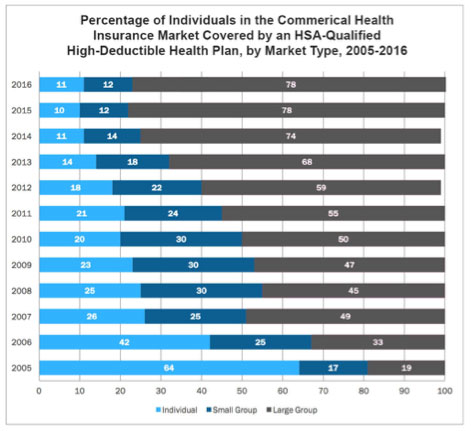

In the United States, a high-deductible health plan is a health insurance plan with lower premiums and higher deductibles than a traditional health plan. It is intended to incentivize consumer-driven healthcare. Being covered by an HDHP is also a requirement for having a health savings account. Some HDHP plans also offer additional “wellness” benefits, provided before a deductible is paid.

High-deductible health plans are a form of catastrophic coverage, intended to cover for catastrophic illnesses. Adoption rates of HDHPs have been growing since their inception in 2004, not only with increasing employer options, but also increasing government options. As of 2016, HDHPs represented 29% of the total covered workers in the United States; however, the impact of such benefit design is not widely understood.

***

% Covered Employees Enrolled in Account-Based CDHP’s

The physician, nurse, or other medical professional should easily recognize that there are a vast array of opportunities, obstacles, and pitfalls when it comes to managing one’s finances. Still, with some modicum of effort, the basic aspects of insurance, investments, taxes, accounting, portfolio management, retirement and estate planning, debt reduction, asset protection and practice management can be largely self-taught. Yet, it is realized that nuances and subtleties can make a well-intentioned financial plan fall short. The devil truly is in the details. Moreover, none of these areas can be addressed in isolation. It is common for a solution in one area to cause a new set of problems in another.

Accordingly, most health care practitioners would be well served to hire [independent, hourly compensated and prn] financial help. Unlike some medical problems, financial issues may not cause any “pain” or other obvious symptoms. Medical professionals tend to have far more complex financial situations than most lay people. Despite the complexities of the new world of health reform, far too many either do nothing; or give up all control totally, to an external advisor. This either/or mistake can be costly in many ways, and should be avoided.

In reality, and at various time in their careers, the medical professional needs a team comprised of at least a financial analyst, lawyer, management consultant, risk manager [actuary, mathematician or insurance counselor] and accountant. At various points in time, each member of the team, or significant others, will properly assume a role of more or less importance, but the doctor must usually remain the “quarterback” or leader; in the absence of a truly informed other, or Certified Medical Planner™.

This is necessary because only the doctor has the personal self-mandate with skin in the game, to take a big picture view. And, rightly or wrongly, investments dominate the information available regarding personal finance and the attention of most physicians. One is much more likely to need or want to discuss the financial markets with their financial advisor than private letter rulings by the IRS, or with their estate planning attorney or tax accountant. While hiring for expertise is a good idea, there is sinister way advisors goad doctors into using all their retail services; all of the time. That artifice is – the value of time.

True integrated physician focused and financial planning is at its core a service business, not a product or sales endeavor. And, increasingly money is more likely to be at the top of the list for providers as the healthcare environment is contracting.

So, eschewing the quarterback model of advice, and choosing to self-educate thru this book and elsewhere, may be one of the best efforts a smart physician can make.

Posted on January 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

INFLATION – Did we say [Health Care] Inflation?

****

***

Why? Inflation, which is the rate of price increases over time, affects all of us on a personal level. We pay electric bills, go grocery shopping, decorate our houses, buy cars—and this year all of those things got more expensive. Especially health care.

Thanks to a nefarious mix of soaring demand for goods and snarled supply chains, US consumer prices jumped the most in 39 years in November, and the 6.8% inflation rate marked the sixth straight month inflation grew by 5% or more. Producer prices, which can eventually trickle down to individuals, also increased at their fastest pace on record last month.

Of course, some inflation is good for the economy when wages keep up with rising prices (the Fed aims for a 2% inflation rate over time). But, so far in the pandemic, that hasn’t happened. While many Americans have gotten a raise in 2021, wage gains haven’t been sufficient to offset inflation, resulting in the erosion of purchasing power—especially for folks on a more or less fixed income.

Where do we go from here?

After months of claiming inflation was “transitory,” the Fed has dropped that term and adopted a more hawkish monetary policy to tamp down surging prices. The central bank is winding down its bond-buying stimulus program faster than originally planned, and also plans to hike interest rates three times in 2022.

In its inflation-fighting efforts, the Fed isn’t alone on the front lines. The Bank of England became the first major central bank to raise interest rates during the pandemic in order to combat the biggest annual jump in consumer prices in 10 years. Russia has raised rates seven times this year. Mexico, Chile, Costa Rica, Pakistan, and Hungary are among other countries which are tightening monetary policy to combat higher prices.

Looking ahead…as if economic policymakers needed another inflation curveball, Omicron has taken the mound. Central banks generally don’t expect the new variant to significantly dent economic growth, but they do think it may prolong inflation by exacerbating the supply–demand imbalance that fueled higher prices in the first place.

Posted on December 29, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Wendell Potter is a Famous Ex-Executive from Cigna Who Left His High Paying PR Job in 2007 to Reveal the True Story Behind Health Insurance Carrier Public Relations.

Utilizing data from FAIR Health, the Urban Institute conducted an October 2021 study which reviewed commercial insurance claims across the U.S. (for approximately 60 insurers and third-party administrators covering over 150 million Americans under age 65) from March 2019 through February 2020.

This study assessed the gap between commercial insurance payments and Medicare payments for professional physician services to determine whether the payment gap between Medicare and commercial insurance differs by specialty. (Read more…)

When President Joe Biden was elected in 2020, there was much anticipation and speculation regarding what his election would mean for the U.S. healthcare industry in the coming years.

As an ardent supporter of the Patient Protection and Affordable Care Act (ACA) who campaigned on offering a public insurance option similar to Medicare, many in the healthcare industry assumed that the Biden Administration would be a strong proponent of continuing the shift to value-based care, which shift was largely spurred by his predecessor and former boss, Barack Obama, with the passage of the ACA. (Read more…)

Posted on December 8, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

TOPICS PREVIOUSLY MENTIONED ON THE ME-P

By Staff Reporters

***

Markets: Omicron who? Fed tapering what? Stocks continued to roar back from their post-Thanksgiving hangover, with tech shares leading the way. The NASDAQ had its best day since March.

Covid: Pfizer’s Covid-19 vaccine is less effective, but still provides some protection, against the Omicron variant, an early study from South Africa showed.

US Government: Congress had a busy evening. Lawmakers reached a deal to raise the country’s debt ceiling, and the House passed a $768 billion defense policy bill that increases pay for service members.

Posted on December 6, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

StockMarketInvesting Perspectives

By Staff Reporters

***

Markets: With stocks selling off sharply last week, at least we still have Crypto, right? Right? Bitcoin tanked more than 20% at one point this weekend, dragging many other digital tokens with it. El Salvador, for one, bought the dip.

Covid: At first glance, Omicron does not appear to cause more severe illness, Dr. Fauci said yesterday. Early results out of South Africa, where Omicron is spreading, show it’s not driving up hospitalizations. Fauci called the data “a bit encouraging.”

Posted on November 30, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

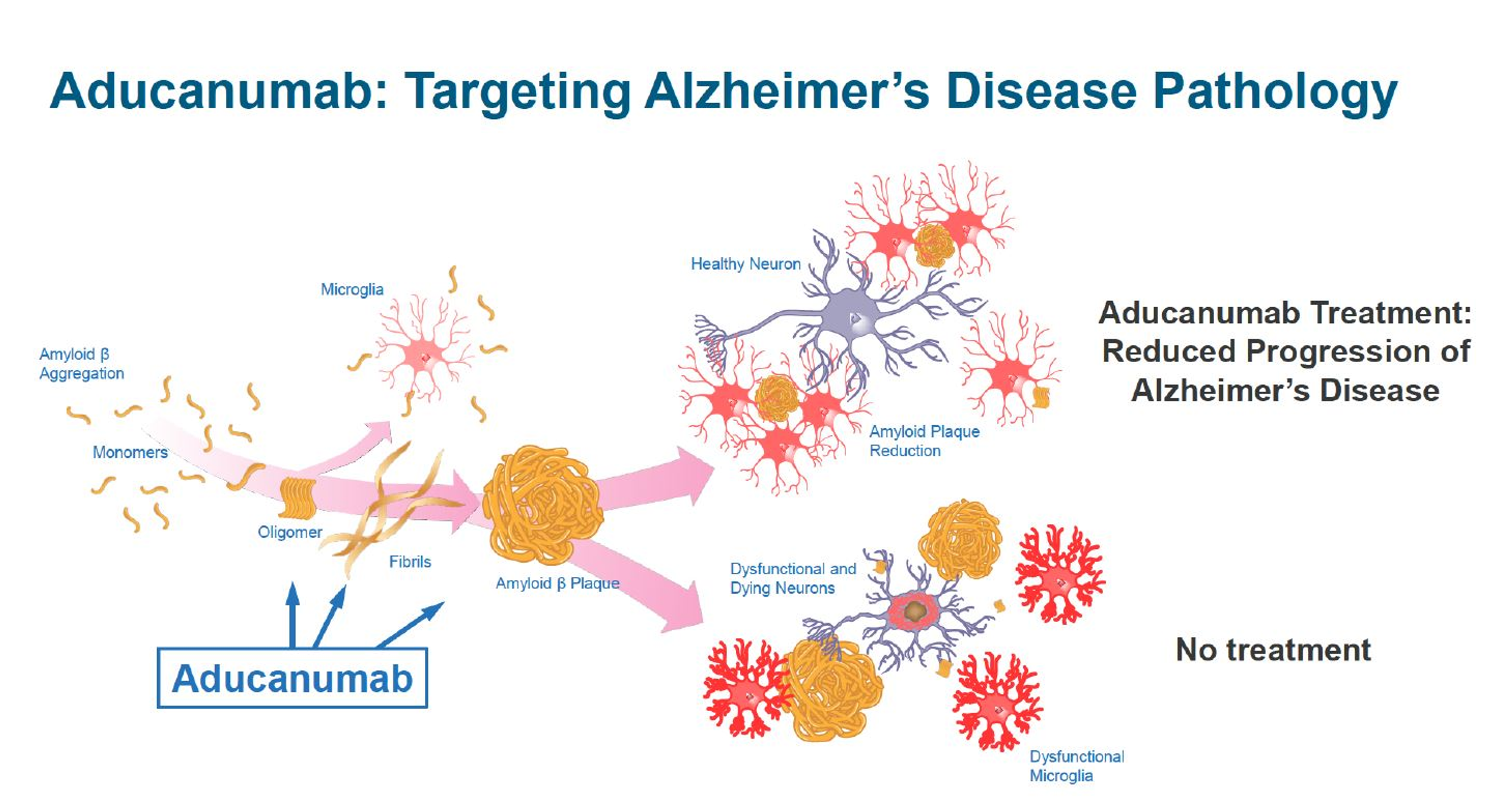

BIG PHARMA AND ECONOMICS

By Health Care Renewal

***

Aducanumab, sold under the brand name Aduhelm, is a medication designed to treat Alzheimer’s disease. It is an amyloid beta-directed monoclonal antibody that targets aggregated forms of amyloid beta found in the brains of people with Alzheimer’s disease to reduce its buildup.

Posted on November 29, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Markets: Stocks dropped sharply in the post-Thanksgiving trading session on Friday due to concerns over the new Covid variant, Omicron. The Dow fell 2.5% for its worst day of the year, and the S&P also tumbled 2.3%. Oil prices and travel stocks also got rocked given fresh worries over travel demand, while “stay-at-home” names like Peloton and Zoom got a boost.

Economy: It’s still way too early to know the impact of Omicron on economic growth. As we laid out last week, the Fed is under pressure to accelerate the winding down of its stimulus measures in order to battle inflation, but the new variant could change the calculus. Investors dialed back their expectations of a sooner-than-expected rate increase on Friday.

Let’s say a physician decided to sell his practice and move to another state. The value of the sale was based, in part, on the yearly gross of the practice. The physician accepted installment payment terms from the buyer and moved to the new state. The buyer began to practice medicine at his new office. Although he was busy, his gross never approached the gross of the prior physician.

Eventually the buyer defaulted on the loan. The selling physician sued for the deficit. The defaulting physician and his forensic consultants then performed an in-depth evaluation of the seller’s practice. The buyer and his team noticed some discrepancies in the billing patterns and practices of the seller. Considering these discrepancies to constitute Medicare and insurance billing fraud, the seller counter-sued the buyer on the grounds of misrepresentation, alleging the gross receipts of the practice purchase price, was grossly inflated.

ASSESSMENT: Therefore, the buyer determined that the seller had fraudulently misrepresented the potential of the practice. He also notified state and federal authorities and filed complaints of insurance fraud against the seller.

The seller thought that he would move to the good life in the new state, but his old practice kept him in constant legal trouble.

Posted on November 10, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

For Doctors and Advisors

BOOK REVIEWS WITH FOREWORD

Reviews

Written by doctors and healthcare professionals, this textbook should be mandatory reading for all medical school students―highly recommended for both young and veteran physicians―and an eliminating factor for any financial advisor who has not read it. The book uses jargon like ‘innovative,’ ‘transformational,’ and ‘disruptive’―all rightly so! It is the type of definitive financial lifestyle planning book we often seek, but seldom find. ―LeRoy Howard MA CMPTM,Candidate and Financial Advisor, Fayetteville, North Carolina I taught diagnostic radiology for over a decade. The physician-focused niche information, balanced perspectives, and insider industry transparency in this book may help save your financial life. ―Dr. William P. Scherer MS, Barry University, Ft. Lauderdale, Florida This book was crafted in response to the frustration felt by doctors who dealt with top financial, brokerage, and accounting firms. These non-fiduciary behemoths often prescribed costly wholesale solutions that were applicable to all, but customized for few, despite ever-changing needs. It is a must-read to learn why brokerage sales pitches or Internet resources will never replace the knowledge and deep advice of a physician-focused financial advisor, medical consultant, or collegial Certified Medical Planner™ financial professional. ―Parin Khotari MBA,Whitman School of Management, Syracuse University, New York In today’s healthcare environment, in order for providers to survive, they need to understand their current and future market trends, finances, operations, and impact of federal and state regulations. As a healthcare consulting professional for over 30 years supporting both the private and public sector, I recommend that providers understand and utilize the wealth of knowledge that is being conveyed in these chapters. Without this guidance providers will have a hard time navigating the supporting system which may impact their future revenue stream. I strongly endorse the contents of this book.

―Carol S. Miller BSN MBA PMP,President, Miller Consulting Group, ACT IAC Executive Committee Vice-Chair at-Large, HIMSS NCA Board Member This is an excellent book on financial planning for physicians and health professionals. It is all inclusive yet very easy to read with much valuable information. And, I have been expanding my business knowledge with all of Dr. Marcinko’s prior books. I highly recommend this one, too. It is a fine educational tool for all doctors.

―Dr. David B. Lumsden MD MS MA,Orthopedic Surgeon, Baltimore, Maryland There is no other comprehensive book like it to help doctors, nurses, and other medical providers accumulate and preserve the wealth that their years of education and hard work have earned them. ―Dr. Jason Dyken MD MBA, Dyken Wealth Strategies, Gulf Shores, Alabama I plan to give a copy of this book written ‘by doctors and for doctors’ to all my prospects, physician, and nurse clients. It may be the definitive text on this important topic. ―Alexander Naruska CPA, Orlando, Florida

Health professionals are small business owners who need to apply their self-discipline tactics in establishing and operating successful practices. Talented trainees are leaving the medical profession because they fail to balance the cost of attendance against a realistic business and financial plan. Principles like budgeting, saving, and living below one’s means, in order to make future investments for future growth, asset protection, and retirement possible are often lacking. This textbook guides the medical professional in his/her financial planning life journey from start to finish. It ranks a place in all medical school libraries and on each of our bookshelves. ―Dr. Thomas M. DeLauro DPM, Professor and Chairman – Division of Medical Sciences, New York College of Podiatric Medicine

Physicians are notoriously excellent at diagnosing and treating medical conditions. However, they are also notoriously deficient in managing the business aspects of their medical practices. Most will earn $20-30 million in their medical lifetime, but few know how to create wealth for themselves and their families. This book will help fill the void in physicians’ financial education. I have two recommendations: 1) every physician, young and old, should read this book; and 2) read it a second time! ―Dr. Neil Baum MD, Clinical Associate Professor of Urology, Tulane Medical School, New Orleans, Louisiana

I worked with a Certified Medical Planner™ on several occasions in the past, and will do so again in the future. This book codified the vast body of knowledge that helped in all facets of my financial life and professional medical practice. ―Dr. James E. Williams DABPS, Foot and Ankle Surgeon, Conyers, Georgia

Health Insurance Companies Paid for Hospital Outpatient Services at an Even Higher Average Rate of 293% of Medicare.

A Detailed Look at the RAND Analysis Reveals that the ‘Basket’ of Services at Each Hospital Had Very Little Data.

For Example, the RAND Study’s Data for the Baylor Scott & White Hospital System in Dallas – Fort Worth Represented Only 0.4% of the Hospital’s Total Revenue.

For the Texas Health Hospital System Also in Dallas – Fort Worth, the RAND Study’s Data Only Represented 0.96% of the Hospital’s Total Revenue.

That Sample Size Is Likely Too Small to Make Accurate Comparisons from One Hospital System to Another Regarding their Commercial Insurance Prices Relative to Medicare.

ASSESSMENT: Your thoughts and comments are appreciated.

Posted on October 29, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Impact of Moving Older Adults from Employer Coverage to Medicare

Peterson-KFF’s recent brief “How Lowering the Medicare Eligibility Age Might Affect Employer-Sponsored Insurance Costs” explores potential percent reduction in employer health plan spending if all enrollees in age group leave large employer-sponsored coverage.

The brief found:

• Ages 60-64 would cause a 15% reduction • Ages 55-64 would cause a 30% reduction • Ages 50-64 would cause a 43% reduction

A June 2021 PricewaterhouseCoopers (PwC) report found that healthcare costs have been on a steady decline for the past decade, but trailing effects from the COVID-19 pandemic could cause increases above anticipated rates over the next several years.

In 2007, the annual cost growth for healthcare spending was 11.9% and declined steadily until 2017, where it floated between 5.5% and 6.0% until 2020. However, projected healthcare cost growth for 2022 is expected to reach 6.5% due to factors such as deferred or forgone care, increased mental health issues, preparation for future pandemics, and investment in digital tools. (Read more...)

Health care in the US is technologically advanced but expensive, costing about $3.6 trillion in 2018, which was 16.9% of gross domestic product (GDP) (1). This percentage is significantly higher than in any other nation.

According to the Organization for Economic Cooperation and Development (OECD), in 2018 the next highest spending countries were Switzerland (12.2% of GDP) and France, Germany, Sweden, and Japan (each about 11%), while the average of the 35 OECD countries (OECD35) was 8.8% (2).

ASSESSMENT: Of course, the absolute amount and the rate of increase of health care spending in the US are widely regarded as unsustainable. Consequences of increased US spending on health care include the following:

:max_bytes(150000):strip_icc()/inflation_FINAL-5c8975c946e0fb0001a0bf75.png)