BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on April 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

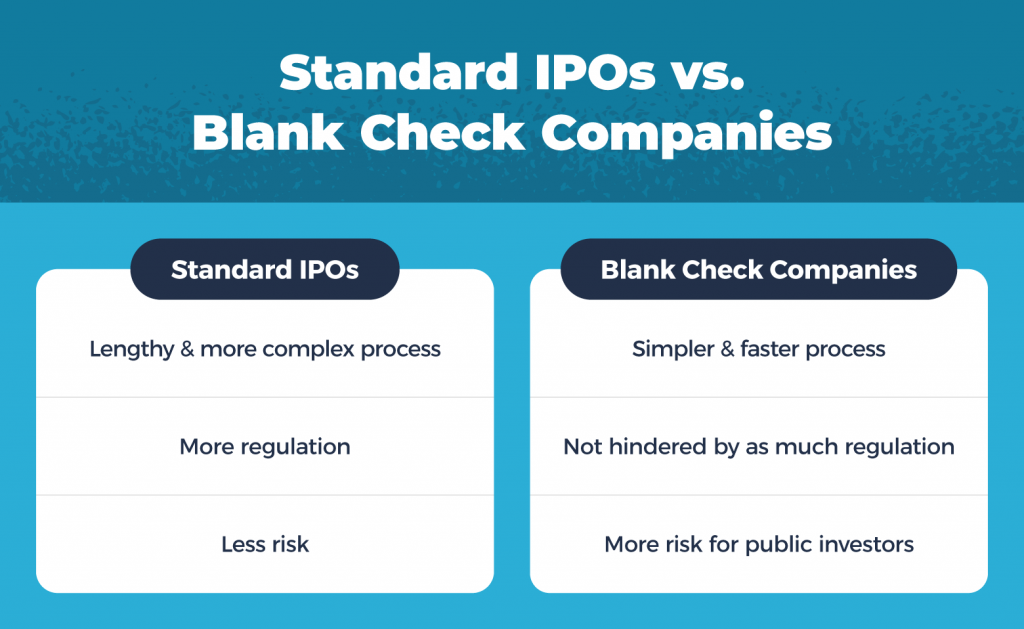

DEFINITION: A blank check company is a development stage company that has no specific business plan or purpose or has indicated its business plan is to engage in a merger or acquisition with an unidentified company or companies, other entity, or person.

Posted on April 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By American Journal of Public Health

***

***

DEFINITION: Public health is “the science and art of preventing disease, prolonging life and promoting health through the organized efforts and informed choices of society, organizations, public and private, communities and individuals”.

Pink sheets are an over-the-counter (OTC) market that connects broker-dealers electronically. There is no trading floor and the quotations are also all done electronically. Since there is no central trading floor or stock exchange like the New York Stock Exchange (NYSE), the pink sheet-listed companies do not have the same criteria to fulfill as the companies listed on national stock exchanges. Many stocks listed on the pink sheets are low-priced penny stocks that trade for under $5 a share.

Pink sheets got their name because the original pink sheets listing the stocks were actually printed and distributed on pink pieces of paper. Trading over-the-counter (OTC) refers to the process of how securities listed on the pink sheets are traded through a broker-dealer network.

An inverse exchange-traded fund is an exchange-traded fund, traded on a public stock market, which is designed to perform as the inverse of whatever index or benchmark it is designed to track. These funds work by using short selling, trading derivatives such as futures contracts, and other leveraged investment techniques.

Posted on March 12, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

6. In the long run, stocks revert to their fair value

***

***

EDITOR’S NOTE: Although it has been some time since speaking live with busy colleague Vitaliy Katsenelson CFA, I review his internet material frequently and appreciate this ME-P series contribution. I encourage all ME-P readers to do the same and consider his value investing insights carefully.

By Vitaliy Katsenelson, CFA

***

6. In the long run, stocks revert to their fair value

Reversion to fair value is not a pie-in-the-sky concept. If a stock is significantly undervalued for a long time, then this undervaluation gets cured, eventually. That can happen through share buybacks – the company can basically buy all of its shares and take itself private.

Or it can happen by the company’s paying out its earnings in dividends, thus creating yields that the market will not be able to ignore. Or the company’s competitors will realize that it is cheaper for them to buy the company than to replicate its assets on their own. Either way, undervaluation gets cured.

This faith that undervaluation will not last forever is paramount to value investing. But this is not your regular faith, which requires belief without proof. This is evidence-supported faith with hundreds of years of data to back it. Just look at the US stock market: it has gone through cycles when it was incredibly cheap and others when it was incredibly expensive. At some points in its journey from one extreme to the other, it touched its fair value, even if it was transitory.

Historically, value investing (owning undervalued companies) has done significantly better than other strategies. Paradoxically, the reason it has done well in the long run is because it did not work consistently in the short run. If something works consistently (keyword), everybody piles into it and it stops working.

These aforementioned cycles of temporary brilliance and dumbness are not just common to us mere mortals. Even Warren Buffett’s Berkshire Hathaway goes through them. As just one example, in 1999, when the stock market went up 21%, Berkshire Hathaway stock declined 19%. In 1999, the financial press was writing obituaries for Buffett’s investment prowess.

Suddenly, in 1999, Buffett’s IQ was lagging the market by 40%. At the time, investors were infatuated with internet stocks that were not making money but that were supposed to have a bright future. Investors were selling unsexy “old economy” stocks that Buffett owned in order to buy the “new economy” ones.

If at the end of 1999, you were to sell Berkshire Hathaway and buy the S&P 500 instead, you would have done the easy thing, but it would have been a large (though very common) mistake. Over the next three years Berkshire Hathaway gained over 30% while the S&P declined over 40%. During the year 1999, Buffett’s IQ did not change much; in fact, the (book) value of businesses Berkshire Hathaway owned went up by 0.5% that year. But in 1999, the market’s attention was somewhere else and it chose to price Berkshire Hathaway 19% lower.

As a value investor, if you do a reasonable job estimating what the business is worth, then at some point the stock market will price it accordingly. You need to have faith. I am acutely aware how wishful this statement sounds. But this faith, the belief in mean reversion, has to be deeply ingrained in our psyche. It will allow us to remain rational when people around us are not.

Posted on March 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

EDITOR’S NOTE: Although it has been some time since speaking live with busy colleague Vitaliy Katsenelson CFA, I review his internet material frequently and appreciate this ME-P series contribution. I encourage all ME-P readers to do the same and consider his value investing insights carefully.

By Vitaliy Katsenelson, CFA

***

5. Risk is a permanent loss of capital (not volatility)

Conventional wisdom views volatility as risk. Not value investors. We befriend volatility, embrace it, and try to take advantage of it. For someone who has not researched a company, it is not readily apparent whether a decline in shares is temporary or permanent. After all, if you don’t know what the company is worth, the quoted price becomes the quotient of intrinsic value. If you do know what the company is worth, then the change in intrinsic value is all that is going to matter. The price quoted on the exchange will be your friend, allowing you to take advantage of the difference between intrinsic value and quoted stock price. If the quoted stock price is significantly cheaper than your estimated intrinsic value, you buy it (or buy more of it if you already own it). If the opposite is true, you sell it.

What is a company worth?

Determining the intrinsic value requires a combination of art and science, in that order – it is not quoted on the exchanges. We go about this the same way a businessman would figure how much he’d want to pay for a gas station or a McDonald’s franchise. Analysis of each company will be different, but at the core we estimate the cash flows the business will produce for shareholders in the long run (at least ten years) and what the business will be worth then (based on our estimate of its earnings power at the time). The combination of the two provides us an approximation of what the business is worth now. To further embed “the right” type of risk analysis into our investment operating system, we build financial models. Models help us to understand businesses better and provide insights as to which metrics matter and which don’t. They allow us to stress test the business: We don’t just look at the upside but spend a lot of times looking at the downside – we try to “kill” the business. We look at known risks and try to imagine unknown ones; we try to quantify their impact on cash flows. This “killing” helps to us understand how much of a discount (margin of safety) we should demand to what the business is worth. By applying this discount to fair value, we arrive at a buy price. For every stock we buy we probably look at a few dozen (at least).

For instance, if we are looking at a company that is selling products or services to consumers, we’ll be focusing on customer-acquisition costs. We try to drill down to the essential operating metrics of each company. If it’s a convenience store retailer, we’ll look into gallons of gas sold and profit per gallon. If it’s an oil driller, we’ll look at utilization rates, rigs in service, average revenue per rig per day. If it’s a pharmaceuticals company, we’ll have revenue lines for each major drug it sells and model the company for the eventuality that patents will run out. (Revenues usually decline 80-90% when a patent expires).

These models help us to understand the economics of the business. We usually build two type of models. We start with what we call the “tablecloth” model. This is a very detailed, in-depth model that zeros in on different aspects of the business. But the risk we run with a tablecloth model is that we get lost in the trees and forget about the forest.

This brings us to our “napkin” model. It’s a much simpler and smaller model that focuses only on the essentials of the business. It is easier to build the tablecloth model than the “napkin.” If we can build a napkin model, that means we understand the drivers of the business – we understand what matters. Models are important because they help us remain rational. It is only the matter of time before a stock we own will “blow up” (or, in layman’s terms, decline).

In this type of analysis, what happens this month, this quarter, or even this year is only important in the context of the long run – unless the company’s good or bad earnings report in any quarter changes our assumptions on the company’s long-term cash flows. If you methodically focus on what the company is worth and if your Total IQ is maximized, then price fluctuations are just noise. Volatility becomes your friend because you can rationally take advantage of it. It’s an under-appreciated gift from Mr. Market.

Side Note:As an advisor, I feel it is one of my great responsibilities to be an honest and clear communicator. There is an asymmetry of information between us and our clients. We have invested weeks and months of research into the analysis of each stock; therefore, we have a good idea what each company is worth. Our clients have not done this research, and they should not have to – that is what they hired us to do.This is why we pour our heart and soul into our quarterly letters – we want to close this informational gap and so we try as hard as we can to explain what we think the companies in our portfolio are worth. Our letters are often 15-20 pages long.

Posted on March 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

EDITOR’S NOTE: Although it has been some time since speaking live with busy colleague Vitaliy Katsenelson CFA, I review his internet material frequently and appreciate this ME-P series contribution. I encourage all ME-P readers to do the same and consider his value investing insights carefully.

By Vitaliy Katsenelson, CFA

***

4. Margin of safety – leave room in your buy price for being wrong

Margin of safety is a function of two dimensions: a company’s quality and its growth.

I am generalizing here, but exogenous events have a greater impact on a lower-quality business than a higher-quality one. Thus a high-quality company needs a lower margin of safety than a lower-quality one.

A company that is growing earnings and paying dividends has time on its side and thus may not need as much margin of safety as a lower-growing one.

We quantify both a company’s quality and growth, and thus margin of safety is deeply embedded in our investment operating system.

The larger discount to the stock’s fair value (the $1) the less clairvoyance you need to have about the future of the business. For instance, in 2013, when Apple stock was trading at $400 (pre-split) we didn’t have to have a very clear crystal ball about Apple’s future; Apple just had to be able to barely fog the mirror.

In later years, at $900, we need to have a lot more precision in our analysis of Apple’s future.

QPADEFINITION: The qualifying payment amount is generally the median of contracted rates for a specific service in the same geographic region within the same insurance market as of January 31, 2019. The rate will be adjusted per the Consumer Price Index for All Urban Consumers (CPI-U).

When trying to decide whether to buy a used car or a new one, it’s typically financially wiser to buy used. But if you want to buy new, you should plan to drive the car for 10 years or more.

Better yet – do not buy a new vehicle.

***

The 20/4/10 rule for buying a vehicle

If you have to borrow when buying a car, to avoid spending more than you can afford you should put down at least 20%, keep the loan limited to no more than four years (to avoid interest), and spend no more than 10% of your gross income on transportation costs (which includes the car payment, parking, gas, and insurance).

Devaluation is the deliberate downward adjustment of the value of a country’s money related to another currency, group of currencies or currency standard. It is often confused with depreciation and is the opposite of revaluation which refers to the readjustment of a currency exchange rate.

The government of a country may decide to devalue its currency and like depreciation it is not the result of non-governmental activities.

One reason a country made devalue its currency is to combat a trade imbalance. Devaluation reduces the cost of a country’s export rendering them more competitive in the Global market which is which in turn increases the cost of imports.

If imports are more expensive domestic consumers are less likely to purchase them further strengthening domestic businesses because exports increase and imports decrease there is typically a better balance of payments because the trade deficit shrinks. In short a country that devalue its currency can produce is difficult because there is a greater demand for cheaper exports.

***

***

In accountancy, depreciation refers to two aspects of the same concept: first, the actual decrease of fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wear, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used (depreciation with the matching principle).

Depreciation is thus the decrease in the value of assets and the method used to reallocate, or “write down” the cost of a tangible asset (such as equipment) over its useful life span. Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report.

BE AWARE ALL ADVISORS … NEXT GEN FINANCIAL ADVICE IS HERE?

Are you a financial planner, insurance agent or investment advisor seeking to assist your physician clients with medical practice enhancement solutions, along with healthcare targeted financial planning services, but don’t know where to turn for help?

OR, maybe you’ve already had a bad experience with a young physician or astute healthcare professional client that was actually more informed than you in these areas?

OR, a doctor/nurse client who demanded a true fiduciary advisor [not fee-based advice, with no dual licenses and no arbitration clauses] documented in writing].

After an understandable slowdown in 2020, due to the onset of the COVID-19 pandemic, merger & acquisition (M&A) activity in the healthcare industry accelerated in 2021, and the industry is expected to continue the high number of deals and high deal volume in 2022.

***

***

This Health Capital Topics article will review the U.S. healthcare industry’s M&A activity in 2021, and discuss what these trends may mean for 2022. (Read more…)

Posted on February 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

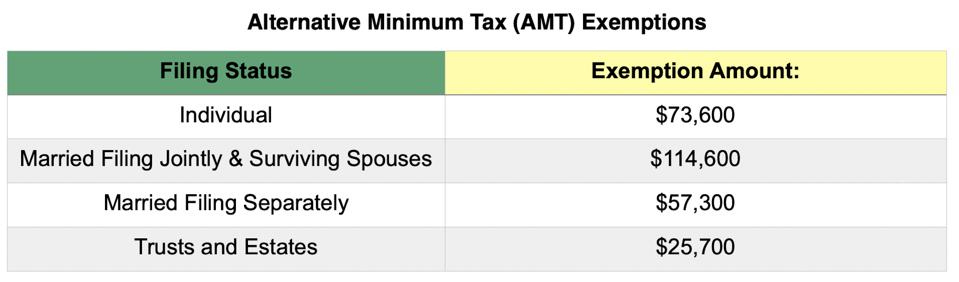

Alternative Minimum Tax

DEFINITION: The alternative minimum tax (AMT) is a tax imposed by the United States federal government in addition to the regular income tax for certain individuals, estates, and trusts. As of tax year 2018, the AMT raises about $5.2 billion, or 0.4% of all federal income tax revenue, affecting 0.1% of taxpayers, mostly in the upper income ranges.

Posted on February 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

According to Tejvan Pettinger, a public good has two characteristics:

Non-rivalry: This means that when a good is consumed, it doesn’t reduce the amount available for others. – E.g. benefiting from a street light doesn’t reduce the light available for others but eating an apple would.

Non-excludability: This occurs when it is not possible to provide a good without it being possible for others to enjoy. For example, if you erect a dam to stop flooding – you protect everyone in the area (whether they contributed to flooding defenses or not.

A public good is often (though not always) under-provided in a free market because its characteristics of non-rivalry and non-excludability mean there is an incentive not to pay. In a free market, firms may not provide the good as they have difficulty charging people for their use.

Posted on February 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Insights For Doctors and All Investors

***

By Vitaliy Katsenelson CFA

***

NOTE: This piece is a little more technical, and contains a bit more stock-market jargon, than most essays you get from me. While how we build portfolios is important to us and our clients, we realize that the puts and takes might bore many readers.

Posted on February 12, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it is – How it Works

By Staff Reporters

****

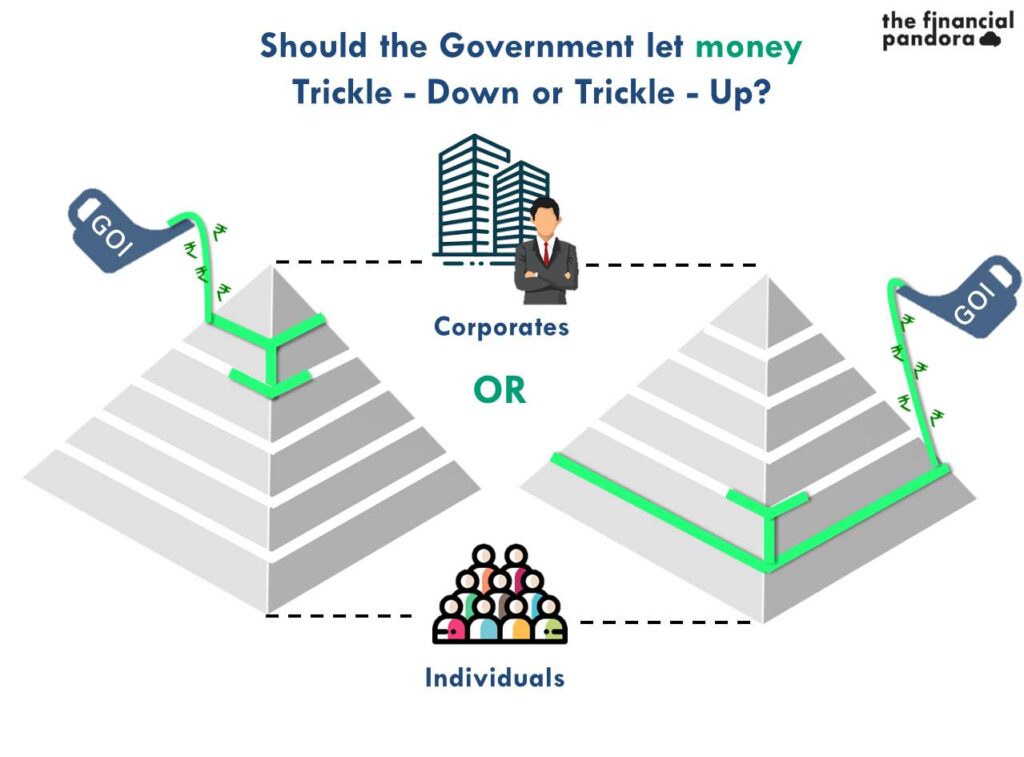

DEFINITION: Trickle-down economics is a colloquial term for supply-side economic policies. In recent history, the term has been used by critics of supply-side economic policies, such as “Reaganomics”. Whereas general supply-side theory favors lowering taxes overall, trickle-down theory more specifically advocates for a lower tax burden on the upper end of the economic spectrum. Empirical evidence shows that the proposition is regressive and has never managed to achieve all of its stated goals as described by the Reagan administration.

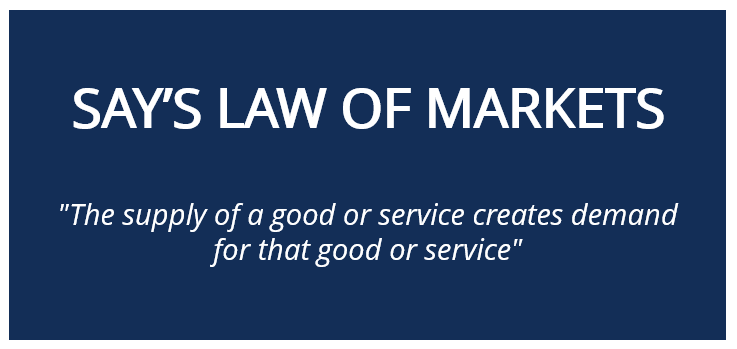

SAY’S LAW: In classical economics, Say’s law, or the law of markets, is the claim that the production of a product creates demand for another product by providing something of value which can be exchanged for that other product. Thus, production is the source of demand

Posted on February 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it Is – How it Works

By Staff Reporters

***

DEFINITION: In classical economics, Say’s law, or the law of markets, is the claim that the production of a product creates demand for another product by providing something of value which can be exchanged for that other product. Thus, production is the source of demand.

Posted on February 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

SYNOPSIS: The home office deductionallows qualified taxpayers to deduct certain home expenses when they file taxes. And, now that some doctors and many of us are working remotely, you may be wondering whether working from home will yield any tax breaks. If your small medical or healthcare consulting or other business qualifies you for a home office tax deduction, should you be concerned about triggering an audit? How does a business qualify in the first place; etc?

Well, to claim the home office deduction on their 2021 tax return, taxpayers generally must exclusively and regularly use part of their home or a separate structure on their property as their primary place of business.

***

If I work from home, do I qualify for a home office tax deduction?

If you’re an employee working remotely rather than an employer or business owner, you unfortunately don’t qualify for the home office tax deduction (however, please note that it is still available to some as a state tax deduction). Prior to the Tax Cuts and Job Acts (TCJA) tax reform passed in 2017, employees could deduct unreimbursed employee business expenses, which included the home office deduction. However, for tax years 2018 through 2025, the itemized deduction for employee business expenses has been eliminated.

If I’m self-employed, should I take the home office tax deduction?

You may have heard that taking the home office deduction sends a red flag to the IRS and ups your chances of being audited. Although there may have been some merit to this advice in the past, changes in the tax rules in the late 1990s made it easier for people who work out of their homes to qualify for these write-offs. So if you qualify, by all means, take it.

Do I qualify for the home office tax deduction?

Generally speaking, to qualify for the home office deduction, you must meet one of these criteria:

Exclusive and regular use: You must use a portion of your house, apartment, condominium, mobile home, boat or similar structure for your business on a regular basis. This also includes structures on your property, such as an unattached studio, barn, greenhouse or garage. It doesn’t include any part of a taxpayer’s property used exclusively as a hotel, motel, inn, or similar business.

Principal place of business: Your home office must be either the principal location of your business or a place where you regularly meet with customers or clients. Some exceptions to this rule include day care and storage facilities.

What is “exclusive use”?

The biggest roadblock to qualifying for these deductions is that you must use a portion of your home exclusively and regularly for your business.

The law is clear and the IRS is serious about the exclusive-use requirement. Say you set aside a room in your home for a full-time business and you work in it ten hours a day, seven days a week. If you let your children use the office to do their homework, you violate the exclusive-use requirement and forfeit the chance for home office deductions.

The exclusive-use rule doesn’t mean:

You’re forbidden to make a personal phone call from the office.

You have to rush outside whenever a family member needs a moment of your time.

Although individual IRS auditors may be more or less strict on this point, some advisers say you meet the spirit of the exclusive-use test as long as personal activities invade the home office no more than they would be permitted to in an office building. The office can also be a section of a room if the division is clear — thanks to a partition, for example — and you can show that personal activities are excluded from the business section.

What is “regular use”?

There’s no specific definition of what constitutes regular use. Clearly, if you use an otherwise empty room only occasionally and its use is incidental to your business, you’d fail this test. If you work in the home office a few hours or so each day, however, you might pass. This test is applied to the facts and circumstances of each case the IRS challenges.

What does “principal place of business” mean?

In addition to passing the exclusive- and regular-use tests, your home office must be either the principal location of that business or a place for regular customer or client meetings.

If your home office is in a separate, unattached structure — a detached garage converted into an office, for example — you don’t have to meet the principal-place-of-business or the deal-with-clients test. As long as you pass the exclusive- and regular-use tests, you can qualify for home business write-offs.

What if your business has just one home office, but you do most of your work elsewhere?

Remember that the requirement is that your home office is your principal place of business, not your principal workplace. As long as you use the home office to conduct your administrative or management chores and you don’t make substantial use of any other fixed location to conduct those tasks, you can pass this test.

If you’re an employee of another company but also have your own part-time business based in your home, you can pass this test even if you spend much more time at the office where you work as an employee.

This rule makes it much easier to claim home office deductions for individuals who conduct most of their income-earning activities somewhere else (such as outside salespeople or tradespeople).

***

***

What qualifies as a business?

As with the regular-use test, whether your endeavors qualify as a business depends on the facts and circumstances. The more substantial the activities, in terms of time and effort invested and income generated, the more likely you are to pass the test.

Making money from your efforts is a prerequisite, but for purposes of this tax break, profit alone isn’t necessarily enough. If you use your den solely to take care of your personal investment portfolio, for example, you can’t claim home office deductions because your activities as an investor don’t qualify as a business.

Taxpayers who use a home office exclusively to manage rental properties may qualify for home office tax status but as property managers rather than investors.

What if I operate a child care or storage facility?

The exclusive-use test doesn’t apply if you use part of your house to:

Provide day care services for children, older adults or individuals with disabilities. If you care for children in your home between 7 a.m. and 6 p.m. each day, for example, you can use that part of the house for personal activities the rest of the time and still claim business deductions. To qualify for the tax break, your home care business must meet any applicable state and local licensing requirements.

Store product samples or inventory you sell in your business. Assume your home-based business is the retail sale of home-cleaning products and that you regularly use half of your basement to store inventory. Occasionally using that part of the basement to store personal items wouldn’t cancel your home office deduction. To qualify for this exception, your home must be the principal location of your business.

How do I calculate the home office tax deduction?

Your home office business deductions are based on either the percentage of your home used for the business or a simplified square footage calculation.

The most exact way to calculate the business percentage of your house is to measure the square footage devoted to your home office as a percentage of the total area of your home. If the office measures 150 square feet, for example, and the total area of the house is 1,200 square feet, your business percentage would be 12.5%.

An easier calculation is acceptable if the rooms in your home are all about the same size. In that case, you can figure out the business percentage by dividing the number of rooms used in your business by the total number of rooms in the house.

Special rules apply if you qualify for home office deductions under the day care exception to the exclusive-use test.

Your business-use percentage must be reduced because the space is available for personal use part of the time.

To do that, you compare the number of hours the child care business is operated, including preparation and cleanup time, to the total number of hours in the year (8,760).

Assume you use 40% of your house for a nursing daycare business that operates 12 hours a day, five days a week for 50 weeks of the year.

12 hours x 5 days x 50 weeks = 3,000 hours per year.

3,000 hours ÷ 8,760 total hours in the year = 0.34 (34%) of available hours.

34% of available hours x 40% of the house used for business = 13.6% business write-off percentage.

Simplified square footage method

Beginning with 2013 tax returns, the IRS began offering a simplified option for claiming the deduction. This new method uses a prescribed rate multiplied by the allowable square footage used in the home.

For 2021, the prescribed rate is $5 per square foot with a maximum of 300 square feet.

If the office measures 150 square feet, for example, then the deduction would be $750 (150 x $5).

The space must still be dedicated to business activities.

With either method, the qualification for the home office deduction is determined each year. Your eligibility may change from one year to the next. Finally, please note that only certain expenses such as rent, mortgage interest and property taxes qualify for the deduction, and the deduction is limited to $10,000.

The International Franchise Association (IFA) estimates that that about $1 trillion in sales, or 40% of all retail sales, were made through franchised establishment last year. On the positive side, franchises offer a branded practice concept with management training and access to proprietary methods, marketing and advertising campaigns and a host of support.

Moreover, there are franchises available for virtually every healthcare product or service, including: diet, weight loss and fitness; vein care and laser surgery; vitamins, nutriceuticals and pharmaceuticals; plastic and cosmetic surgery; dermatology, tanning and skin care; home healthcare and extended, etc. Some well know established healthcare and medical franchises are: Doctors Express, Being There Senior Care, Home Care Assistance, Personal Training Institute, Inches-A-Weigh, Remedy Intelligent Staffing, Visiting Angels, Unlimited MedSearch, prnYourHealth and Any Lab Test Now, etc.

On the downside, franchises incur high start-up costs, rules and obligations, payment of franchise percentages and many contractual obligations. Questions to consider when contemplating this business entity include:

Franchise stability, track record, licensing and costs.

Training, support and proximity of other franchises.

Independence, ownership laws, contracts and dispute resolutions,

Screening methods, market size and potential market share.

Replacement cost and transferability?

For more information on Uniform Franchise Offerings Circulars (UFOCs) contact www.FranChoice.com or:

Posted on February 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

An interval fund is a type of closed-end fund with shares that do not trade on the secondary market. Instead, the fund periodically offers to buy back a percentage of outstanding shares at net asset value (NAV). The rules for interval funds, along with the types of assets held, make this investment largely illiquid compared with other funds.

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Decentralized Autonomous Organizations in Health Care?

By Staff Reporters

****

DEFINITION: A decentralized autonomous organization (DAO), sometimes called a decentralized autonomous corporation (DAC), is an organization represented by rules encoded as a computer program that is transparent, controlled by the organization members and not influenced by a central government. A DAO’s financial transaction record and program rules are maintained on a blockchain.

Posted on February 2, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IT IS – HOW IT WORKS – WHY?

UPDATE: Hits $90 dollars/barrel

By Staff Reporters

***

What it is: Exactly what it sounds like. The North American crude oil benchmark, known as West Texas Intermediate (WTI), is one of three main oil benchmarks used around the globe. While WTI is sourced primarily from Texas, it’s considered one of the highest-quality oils and is often refined into gasoline.

How it works: WTI is the physical commodity behind oil futures contracts traded on the New York Mercantile Exchange. Oil futures = financial instruments that allow investors to buy “abstract oil.” When the futures contract expires, that investment is converted into IRL oil, cashed out, or rolled into a future futures contract.

Why it matters: Oil prices are affected by economic conditions, supply and demand, and geopolitical forces. The coronavirus pandemic caused a historic collapse in prices this spring, and while prices have stabilized, the outlook is shaky.

Posted on February 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

Tax planning can be quite a tedious process, but there are benefits for all seniors to make it less taxing. And senor medical professionals should take particular note:

Free Advice: IRS-certified volunteers will help older taxpayers with tax return preparation and electronic filing between January 1st and April 15th each year.

No Withdrawal Penalties: Anyone aged 59 years or over can withdraw money from an IRA, without incurring the common 10% tax.

Catch-Up Contributions: Healthcare Workers aged 50 or older can defer income tax on an extra $6,500 or a total of $26,000 if contributed to a 401(k) plan, resulting in a tax savings of $6,240 for an older worker in the 24% tax bracket.

Additional IRA Contribution: Workers age 50 and older can contribute an additional $1,000 to an IRA, or a total of $7,000 in 2020.

Posted on January 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

FOR PHYSICIANS AND ALL OF US!

Br. Dr. David E. Marcinko MBA

By Staff Reporters

***

It’s been announced that January 24th 2022 is the official start of the tax filing season. This means it’s that time of year again to buy some pricey tax software and prepare your return on your own, hire a tax prep pro, CPA, or take advantage of the Free File Program from the IRS.

A Capital Gain [CG] occurs when you sell something for more than you spent to acquire it. This happens with investments, but it also applies to personal property, such as a car. Every physician and taxpayer should understand these basic facts about capital gains taxes.

Capital gains aren’t just for doctors or rich people

Anyone who sells a capital asset should know that capital gains tax may apply. And as the Internal Revenue Service points out, just about everything you own qualifies as a capital asset. That’s the case whether you bought it as an investment, such as stocks or property, or for personal use, such as a car or a big-screen TV.

If you sell something for more than your “basis” in the item, then the difference is a capital gain, and you’ll need to report that gain on your taxes. Your basis is usually what you paid for the item. It includes not only the price of the item, but any other costs you had to pay to acquire it, including:

Sales taxes, excise taxes and other taxes and fees

Shipping and handling costs

Installation and setup charges

In addition, money spent on improvements that increase the value of the asset—such as a new addition to a building—can be added to your basis. Depreciation of an asset can reduce your basis.

In most cases, your home is exempt

The single biggest asset many people have is their home, and depending on the real estate market, a homeowner might realize a huge capital gain on a sale. The good news is that the tax code allows you to exclude some or all of such a gain from capital gains tax, as long as you meet three conditions:

You owned the home for a total of at least two years in the five-year period before the sale.

You used the home as your primary residence for a total of at least two years in that same five-year period.

You haven’t excluded the gain from another home sale in the two-year period before the sale.

If you meet these conditions, you can exclude up to $250,000 of your gain if you’re single, $500,000 if you’re married filing jointly.

Length of ownership matters

If you sell an asset after owning it for more than a year, any gain you have is a “long-term” capital gain. If you sell an asset you’ve owned for a year or less, though, it’s a “short-term” capital gain. How much your gain is taxed depends on how long you owned the asset before selling.

The tax bite from short-term gains is significantly larger than that from long-term gains – typically 10-20% higher.

This difference in tax treatment is one of the advantages a “buy-and-hold” investment strategy has over a strategy that involves frequent buying and selling, as in day trading.

People in the lowest tax brackets usually don’t have to pay any tax on long-term capital gains. The difference between short and long term, then, can literally be the difference between taxes and no taxes.

Capital losses can offset capital gains

As anyone with much investment experience can tell you, things don’t always go up in value. They go down, too. If you sell something for less than its basis, you have a capital loss. Capital losses from investments—but not from the sale of personal property—can be used to offset capital gains.

If you have $50,000 in long-term gains from the sale of one stock, but $20,000 in long-term losses from the sale of another, then you may only be taxed on $30,000 worth of long-term capital gains.

$50,000 – $20,000 = $30,000 long-term capital gains

If capital losses exceed capital gains, you may be able to use the loss to offset up to $3,000 of other income. If you have more than $3,000 in excess capital losses, the amount over $3,000 can be carried forward to future years to offset capital gains or income in those years.

Business income isn’t a capital gain

If you operate a business that buys and sells items, your gains from such sales will be considered—and taxed as—business income rather than capital gains.

For example, many people buy items at antique stores and garage sales and then resell them in online auctions. Do this in a businesslike manner and with the intention of making a profit, and the IRS will view it as a business.

The money you pay out for items is a business expense.

The money you receive is business revenue.

The difference between them is business income, subject to employment taxes.

Whether you have stock, bonds, ETFs, cryptocurrency, rental property income or other investments, this info is vital to increase your tax knowledge and understanding all while doing your taxes.

Here are eight things to keep in mind as you prepare to file your 2021 taxes.

1. Income tax brackets have shifted a bit

There are still seven tax rates, but the income ranges (tax brackets) for each rate have shifted slightly to account for inflation. For 2021, the following rates and income ranges apply:

Tax rate

Taxable income brackets:Single filers

Taxable income brackets:Married couples filing jointly (and qualifying widows or widowers)

10%

$0 to $9,950

$0 to $19,900

12%

$9,951 to $40,525

$19,901 to $81,050

22%

$40,526 to $86,375

$81,051 to $172,750

24%

$86,376 to $164,925

$172,751 to $329,850

32%

$164,926 to $209,425

$329,851 to $418,850

35%

$209,426 to $523,600

$418,851 to $628,300

37%

$523,601 or more

$628,301 or more

Source: Internal Revenue Service

2. The standard deduction has increased slightly

After an inflation adjustment, the 2021 standard deduction has increased slightly to $12,550 for single filers and married couples filing separately and $18,800 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction has risen to $25,100.

3. Itemized deductions remain the same

For most filers, taking the higher standard deduction is more practical and saves the hassle of keeping track of receipts. But if you have enough tax-deductible expenses, you might benefit from itemizing.

The following rules for itemized deductions haven’t changed much for 2021, but they’re still worth pointing out.

State and local taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is capped at $10,000.

Mortgage interest deduction: The mortgage interest deduction is limited to $750,000 of indebtedness. But people who had $1,000,000 of home mortgage debt before December 16, 2017, will still be able to deduct the interest on that loan.

Medical expenses: Only medical expenses that exceed 7.5% of adjusted gross income (AGI) can be deducted in 2021.

Charitable donations: The cash donation limit of 100% of AGI remains in place for 2021, if donations were made to operating charities.1

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

4. IRA and 401(k) contribution limits remain the same

The traditional IRA and Roth contribution limits in 2021 remain the same as in 2020. Individuals can contribute up to $6,000 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution. If you’re able to max out your IRA, consider doing so—you may qualify to deduct some or all of your contribution.

The 2021 contribution limit for 401(k) accounts also stays at $19,500. If you’re age 50 or older, you qualify to make an additional $6,500 catch-up contribution as well.

5. You can save a bit more in your health savings account (HSA)

For 2021, the max you can contribute into an HSA is $3,600 for an individual (up $50 from 2020) and $7,200 for a family (up $100). People age 55 and older can contribute an extra $1,000 catch-up contribution.

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (which usually has lower premiums as well). Learn more about the benefits of an HSA.

6. The Child Tax Credit has been expanded

For 2021, the American Rescue Plan Act (ARPA) has temporarily modified the Child Tax Credit requirements and amounts for household incomes below $75,000 for single filers and $150,000 for married filing jointly.

First, the ARPA has raised the age limit for dependents from 16 to 17. In addition, the child tax credit has increased from $2,000 to $3,000 for children age 6 through 17 and up to $3,600 for children under 6. If your income exceeded the above limits but was below $200,000 for single filers or $400,000 for joint filers, you’ll receive the standard child tax credit of $2,000 per child.

The IRS began sending monthly advance Child Tax Credit payments to eligible families in July and sent its last advance in December. If your dependent didn’t qualify for the child tax credit, you may still qualify for up to $500 of tax credits under the “credit for other dependents” (see IRS Publication 972 for more details). Tax credits, which reduce the tax you owe dollar for dollar, are generally better than deductions, which reduce your taxable income.

7. The alternative minimum tax (AMT) exemption has gone up

Until the AMT exemption enacted by the Tax Cuts and Jobs Act expires in 2025, the AMT will continue to affect mostly households with incomes over $500,000. Still, the AMT has investment implications for some high earners.

For 2021, the AMT exemptions are $73,600 for single filers and $114,600 for married taxpayers filing jointly. The phase-out thresholds are $1,047,200 for married taxpayers filing a joint return and $523,600 for all other taxpayers.

8. The estate tax exemption is even higher

The estate and gift tax exemption, which is indexed to inflation, has risen to $11.7 million for 2021. But the now-higher exemption is set to expire at the end of 2025, meaning it could be essentially cut in half at that time if Congress doesn’t act.

The annual gift exclusion, which allows you to give money to your loved ones each year without incurring any tax liability or using up any of your lifetime estate and gift tax exemption, stays at $15,000 per recipient.

Don’t get caught off guard

As you prepare to file your taxes for 2021, here are a few additional items to consider.

If you’re not retired, the 10% early withdrawal penalty that was waived for retirement account distributions in 2020 has been reinstated for 2021.

If you’re age 72 or older, make sure you’ve taken your required minimum distribution (RMD) from your retirement accounts or else you face a 50% penalty on any undistributed funds (unless it’s your first RMD, in which case, you can wait until April 1, 2022).

If you haven’t contributed to your retirement accounts already, now is the time. Review your earnings for the year and take advantage of any deductions that can lower your tax bill. Also, keep an eye on Washington for any last-minute tax changes that could affect your return before you file. Tax season will be here before you know it, and it’s never too early to start preparing.

1Operating charities, or qualifying public charities, are defined by Internal Revenue Code section 170(b)(1)(A). You can use the Tax Exempt Organization Search tool on IRS.gov to check an organization’s eligibility.

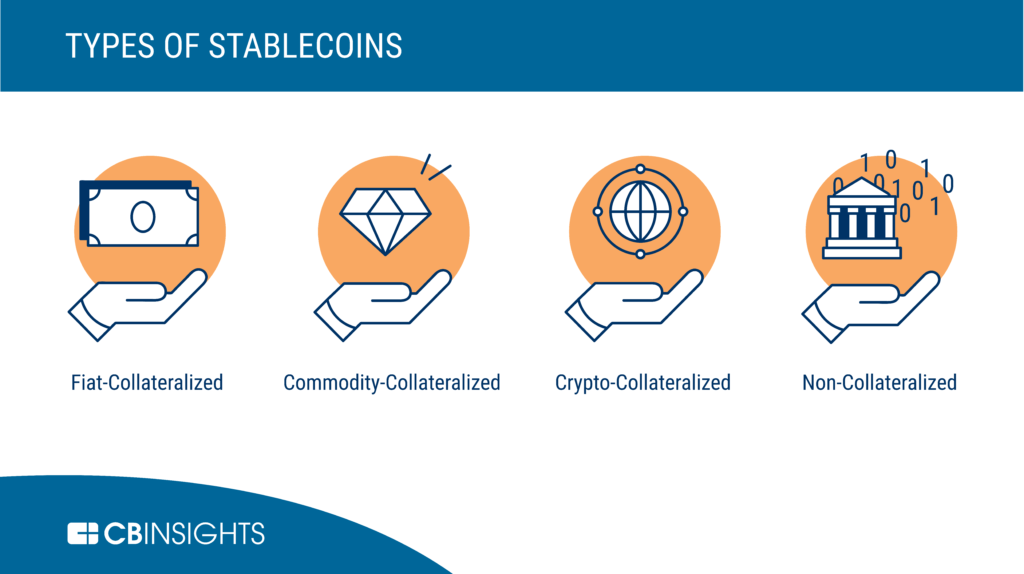

DEFINITION: Stablecoins are blockchain-based digital currencies that have been created with the aim to have a stable value. Stablecoins achieve price-stability through various different methods such as a peg against a fiat currency or a commodity, through collateralization against other cryptocurrencies or through algorithmic coin supply management.

Every stable coin includes a specific set of mechanisms that mostly behave in the same way. In general, stable coins keep collateral of the asset and manage the supply. In this way, they incentivize the market, which allows trade of the coin for no more or less than $1.

A stable coin can be considered the best depending on several factors: It should be stable. PAX is one the most stable stablecoin. It should be liquid and available on most exchanges. It should be backed by FIAT. PAX is 100% collateralized in US bank accounts. It should be regulated. It should be redeemable.

Posted on December 17, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IT IS – HOW IT WORKS – WHY?

By Staff Reporters

***

10-Year Note

What it is: The 10-year Treasury note is a debt instrument the U.S. government issues to fund itself. The Federal Reserve closely watches the “yield” (i.e. the return on investment) as a benchmark for other interest rates.

How it works: The U.S. Treasury issues bonds that are auctioned to investment banks by the Federal Reserve; banks can then sell those bonds to investors. The 10-year matures over—you guessed it—10 years, with interest paid out every six months until the full value is paid out at the end.

Why it matters: The 10-year is considered another safe-haven asset for investors. But as demand goes up, the yield goes down. Investors can even end up paying more than the face value of the Treasury note (but some are willing to accept the tradeoff for the low-risk investment).

Posted on December 13, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ALL TIME HIGHS?

***

Markets: The S&P begins the week after closing at an all-time high last Friday. The index has closed at a record more times this year (67) than in any other year since 1995. It needs 10 more to tie the mark.

More S&P fun facts: Microsoft, Alphabet, Apple, Nvidia, and Tesla alone account for over a third of the S&P’s gains this year.

Posted on November 19, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Hospitals Must Treat All Patients

BY ERIC BRICKER MD

***

The Emergency Medical Treatment and Active Labor Act is an act of the United States Congress, passed in 1986 as part of the Consolidated Omnibus Budget Reconciliation Act

Once you do retire, and put your physician or medical career behind you, it’s important to realize that, at some point, the IRS expects you to draw down your 401(k) balance. Starting at age 72, you need to take required minimum distributions (RMDs).

Your annual RMD amount depends on the balance of your 401(k) and a formula that determines your life expectancy.

***

***

QUERY: But – What happens if you don’t take your RMD for the year?

ANSWER: Well, you could end up paying a penalty. In fact, it’s a pretty hefty penalty of up to 50% of the amount you were supposed to withdraw. Paying that penalty can be pretty costly for someone living in retirement. As long as you’re vigilant and stay on top of the situation, though, you can avoid the penalty as well as these other costly 401(k) mistakes.

Almost everything you own and use for personal or investment purposes is a capital asset. Examples include a home, personal-use items like household furnishings, and stocks or bonds held as investments. When you sell a capital asset, the difference between the adjusted basis in the asset and the amount you realized from the sale is a capital gain or a capital loss.

Generally, an asset’s basis is its cost to the owner, but if you received the asset as a gift or inheritance, refer to Topic No. 703 for information about your basis.

For information on calculating adjusted basis, refer to Publication 551, Basis of Assets. You have a capital gain if you sell the asset for more than your adjusted basis. You have a capital loss if you sell the asset for less than your adjusted basis. Losses from the sale of personal-use property, such as your home or car, aren’t tax deductible.

DEFINITION: The meaning of meme stocks is sort of self-explanatory: hyped stocks that perform well. But from a fundamental perspective, they shouldn’t do well at all.

For example, Reddit forums and social media hype drive meme stocks. Speculators on Twitter and Reddit united together to trade their favorite companies in hopes of driving them “to the moon.”

It may not be fair to call them speculators. These hype beasts want to buy and hold stocks of companies that might not have a great long-term outlook.

Brokerages like Robinhood helped level the playing field with apps and ‘easier’ access. That’s giving retail traders more opportunity. Robinhood traders can buy with just a few clicks on their smartphones and use partial positions to buy chunks of stocks.

Posted on October 11, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BYSTEVE WINOKER

Hi David,

I hope this note finds you well. Here at GE, September was an important month for us. We concluded our annual strategy reviews with each business, complementing the quarterly operating reviews with a longer-term focus. I had the opportunity to participate in many of the review processes and came away impressed with our progress, leadership team, and the growth opportunities that lie ahead as we innovate for the future of flight, precision health, and energy transition.

In my last investor update, I shared the exciting news that GE announced an agreement to acquire BK Medical, and in the spirit of growth and innovation, I’d like to share a few more recent business highlights that illustrate how our teams are delivering for our customers:

At Aviation, Bamboo Airways signed a Memorandum of Understanding agreement to purchase GEnx engines for its Boeing 787-9 aircraft. This order of 10 firm and 20 options, valued at a list price of approximately $2 billion, will help the airline expand its transcontinental flight network. Dang Tat Thang, CEO of Bamboo Airways, said, “The selection of the GEnx engines for our Boeing 787-9 aircraft will help increase the operational efficiency and service quality of Bamboo Airways on Vietnam-U.S. nonstop flights as well as many potential international routes.”

Renewable Energyannounced today that it received an order to supply Haliade-X turbines for Massachusetts’s Vineyard Wind 1, the first utility-scale offshore wind installation in the U.S. Additionally, our Haliade-X offshore wind prototype turbine recently became the first in the industry to operate at 14 MW, increasing our customers’ ability to produce more power from a single turbine.

Gas Powerannounced the delivery, installation, and commissioning of four TM2500 aeroderivative gas turbines in only 42 days to supplement renewable power generation for the State of California’s Department of Water Resources during peak demand season. GE’s TM2500s start and ramp up quickly in just minutes and will help enhance the reliability and sustainability of California’s grid.

We’re excited about what the future holds, as our teams are highly focused on executing for our customers, leveraging lean to drive meaningful progress and innovating for a more sustainable world.

We look forward to sharing more on our 3Q’21 earnings call on Tuesday, October 26. As always, I welcome your feedback.

If you’ve ever listened to an early morning financial news broadcast, you’ve heard a reference to “futures” and how they affect the stock market before it opens. Physicians Investors follow the futures because it provides an indication of where stocks are headed at the opening bell. One of the most widely followed futures is the Dow Futures, whose underlying value is based on the Dow Jones Industrial Average, an index of 30 major U.S. companies.

***

***

DEFINITION: After the markets close at 4 pm New York time, implied open prices of the Dow Jones Industrial Average, S&P 500 Index, and NASDAQ, which fluctuate from minute to minute, can be calculated.

Considering the DJIA as an example, the basis of calculating implied open is the price of a “DJX index option futures contract “.

The first World Financial Planning Day was held on October 4, 2017. The Financial Planning Standards Board (FPSB) hosts the day. Every year, the FPSB partners with the International Organization of Securities Commissions (IOSCO).

***

Today, it is always held during the first Wednesday of October during IOSCO’s World Investor Week.

***

QUERY: But, what about the entire ecosystem of personal and professional financial planning, investing, risk, business and medical practice management for physicians and healthcare professionals? A vital, unique and complicated niche!

ANSWER: According to the Institute of Medical Business Advisors, Inc., WFP Day is every day for CERTIFIED MEDICAL PLANNER® professional certification holders.

So – If you are in this WFPD industry – Become a fiduciary focused board CERTIFIED MEDICAL PLANNER with extreme healthcare industry ecosystem specificity.

Posted on October 4, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

POST PANDEMIC HEALTH ECONOMICS

BY LAURA GLENN

***

As a leader in a community health system, Laura talks about how the COVID 19 pandemic has affected the economics of healthcare. Laura Glenn joined Munson Healthcare as the Vice President of the Physician Network in December, 2017.

In July, 2019 her role expanded and she was appointed the President of Ambulatory Services and Value Based Care. In this role, she remains responsible for integration of the employed and aligned physician practices across the system. In addition, she is responsible for advancing population health strategies including the Munson Clinical Integration Network and other value based payment models as well as providing leadership to the home health division, MHC’s clinical service lines and clinical business intelligence.

How much will it cost you to start a dental practice – with Business Plan?

There are many costs to consider to set up a successful dental practice. Note that the following values are not the exact amount but an average of setting up a dental practice:

Purchase price – this includes valuation fees of between $1,000-4,500, solicitor fees of between $4,000 – 17,000, accountancy and bank fees of around $3,000, and bank solicitors, which can be up to $3,500. Many of these can be reduced or obliterated.

Materials – $40,000

Lab fees – $36,000

Staff costs – $82,000

Other costs (associates fees) – [$245,000 – $295,000]

Other Factors

“Big” Tech – Many startup doctors want to include CBCT or CAD/CAM or 3D printing in their startup, any of which can add $25,000-$175,000. In other situations, waiting is the best option.

Cabinetry Preferences – Costs for cabinetry can range from $5,000 to $175,000.

Practice Management Software (PMS) – Pricing will range from a few thousand dollars to $25,000; OR none at all.

Mechanical Delivery – Typically referred to as chairs, lights, and units, this category of dental equipment costs will range between $5,000 and $100,000 based on your startup plans.

Vision – Ignore the so-called “experts” who will try to create a cookie-cutter model for your equipment costs. That is the thinking of corporate dentistry. You want a customized private practice vision that allows you to create a model matching your standards. Prioritize your vision, so your values and philosophy will lead your dental equipment budget and purchasing decisions. Your equipment budget will be—and should be—customized.

A decentralized autonomous organization (DAO), sometimes called a decentralized autonomous corporation (DAC), is an organization represented by rules encoded as a computer program that is transparent, controlled by the organization members and not influenced by a central government. A DAO’s financial transaction record and program rules are maintained on a blockchain. The precise legal status of this type of business organization is unclear.

A well-known example, intended for venture capital funding, was The DAO, which launched with $150 million in crowdfunding in June 2016, and was nearly immediately hacked and drained of US$50 million in cryptocurrency. The hack was reversed in the following weeks, and the money restored, via a hard fork of the Ethereum blockchain: the Ethereum miners and clients switched to the new fork.

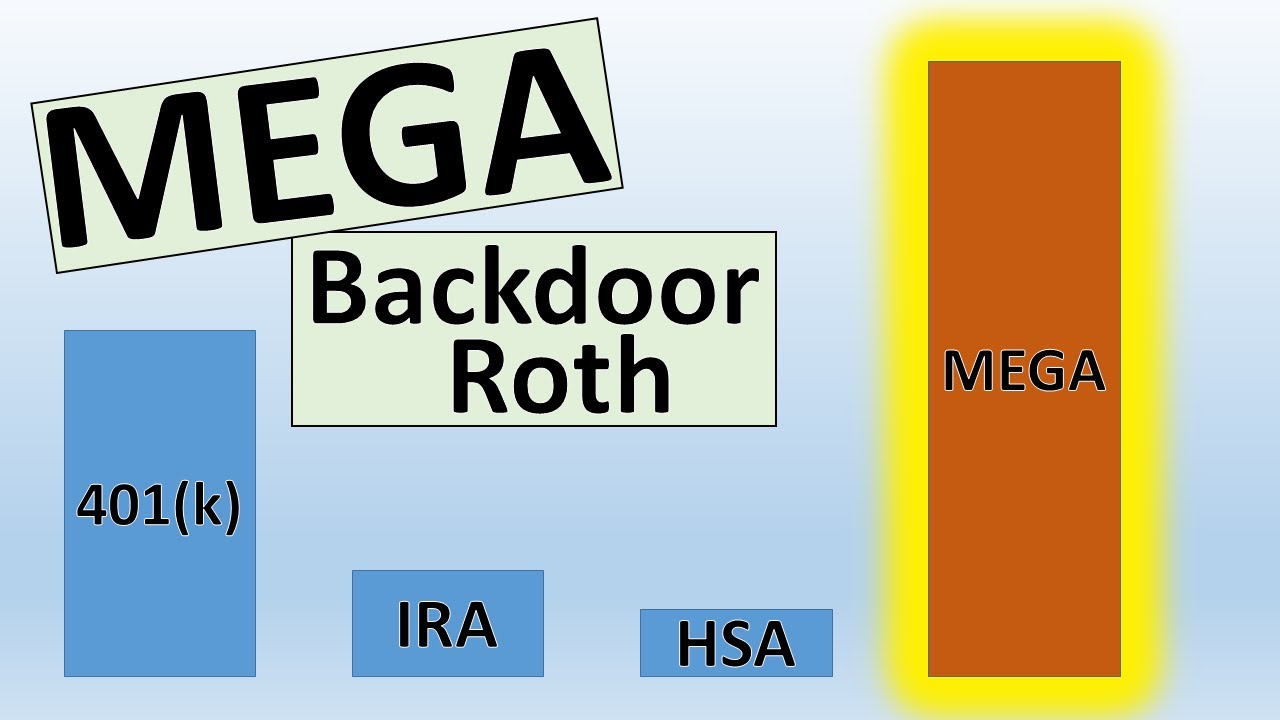

If you’re a physician looking to get ahead on planning for retirement, you’re likely familiar with individual retirement accounts, or IRAs. An IRA is a tax-advantaged vehicle that helps you grow your retirement savings. Roth IRAs are particularly attractive, because you don’t pay taxes on withdrawals in retirement.

There’s one problem: you can’t contribute to a Roth IRA directly if you make above a certain income. A backdoor IRA, though, can solve your problem by allowing you to convert a traditional IRA into a Roth.

Here’s how it works:

First, place your contribution in a traditional IRA—which has no income limits.

Then, move the money into a Roth IRA using a Roth conversion.

But make sure you understand the tax consequences before using this strategy.

The mega backdoor Roth allows you to put up to $38,500 in a Roth IRA or Roth 401(k) in 2021, on top of the regular contribution limits for those accounts. If you have a Roth 401(k) at work (and the plan allows for the mega option as described below), generally you can choose whether the final destination of your mega contributions is the Roth 401(k) or a Roth IRA. If your employer offers only a traditional 401(k), then your mega contributions would end up in a Roth IRA.

Here’s a quick summary of what you need to have in place for the ideal mega backdoor Roth strategy:

A 401(k) plan that allows “after-tax contributions.” After-tax contributions are a separate bucket of money from your traditional and Roth 401(k) contributions. About 43% of 401(k) plans allow after-tax contributions, according to a 2017 survey of large and midsize employers by consulting firm Willis Towers Watson.

Your employer offers either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan. If you’re not sure, ask your human resources department or plan administrator.

You’ve got money left over to save, even after maxing out your regular 401(k) and Roth IRA contributions.

An IRA in which distributions continue after the primary beneficiary’s death.

For an IRA to be inherited, the primary beneficiary must have already been receiving the required minimum distribution; the distributions either continue or are re-calculated based upon the secondary beneficiary’s life expectancy.

If the secondary beneficiary is the widow(er) of the primary beneficiary, she/he may roll over the inherited IRA into her/his own IRA without penalty.

Posted on September 9, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ALERT FOR PHYSICIANS AND ALL INVESTORS

***

1. You can trade actively in a Roth IRA

Some physician investors may be concerned that they can’t actively trade in a Roth IRA. But there’s no rule from the IRS that says you can’t do so. So you won’t get in legal trouble if you do.

But there may be some extra fees if you trade certain kinds of investments. For example, while brokers won’t charge you if you trade in and out of stocks and most ETFs on a short-term basis, many mutual fund companies will charge you an early redemption fee if you sell the fund. This fee is usually assessed only if you’ve owned the fund for fewer than 30 days.

2. Any gains are tax-free – forever

The ability to avoid taxes on your investments is an incredible benefit. You’ll be able to escape – perfectly legally – taxes on dividends and capital gains. Not surprisingly, this superpower makes the Roth IRA very popular, but to enjoy its benefits, you must abide by a few rules.

The Roth IRA limits you to a $6,000 maximum annual contribution (for 2021), and you won’t be able to withdraw earnings from the account until retirement age (59 1/2) or later and after owning the account for at least five years. However, you can withdraw your contributions to the account without being taxed at any time, but you won’t be able to replace those contributions later.

Many traders use margin in their accounts. With a margin loan, the broker extends you capital to invest beyond what you actually own. It’s a useful tool, especially if you’re trading frequently. Unfortunately, margin loans are not available in IRA accounts.

For frequent traders the ability to trade on margin is not just about magnifying your returns. It’s also about having the ability to sell a position and immediately buy another. In a cash account (like a Roth IRA), you have to wait for a transaction to settle, and that takes a couple days. In the meantime you’re unable to trade with that money even though it’s credited to your account.

PLUS A FOURTH RULE

4. You don’t get to deduct losses

If you’re trading in a taxable brokerage account, you’ll get a tax write-off if you make a losing investment. Some investors even make sure they’re getting the largest write-off they can using a process called tax-loss harvesting. They scoop up that benefit and then even repurchase the stock or fund later (after 30 days) if they think it’s poised to rise in the future.

But if you’re trading in a Roth IRA, you won’t get the ability to write off losses. Changes to the tax code in 2017 eliminated the ability to claim any benefit from losses in an IRA account.

![DR. DAVID EDWARD MARCINKO FACFAS MBA CFP MBBS [Hon] [Executive Summary] - PDF Free Download](https://educationdocbox.com/docs-images/75/71938560/images/8-1.jpg)