BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on June 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Casey McIntyre, a 38-year-old book publisher and mother of one, helped wipe out more than $30 million in unpaid medical bills for other people…without being alive to see it. McIntyre’s husband posted a message on her behalf after she died of ovarian cancer last year, asking people to participate in a “debt jubilee” that pays off the medical bills of others. The response has been overwhelming:

As of recently, the nonprofit RIP Medical Debt has received more than $300,000 in donations through McIntyre’s campaign. The organization relieves $10,000 of medical debt for every $100

Posted on June 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

The retail pharmacy giants have made a string of multi-billion dollar deals!

By Staff Reporters

***

***

CVS and Walgreens have been spending money like there is no tomorrow! In fact, the two retail pharmacy giants have made a string of multi-billion dollar acquisitions of primary care providers in the past couple years, including the $5.2 billion VillageMD acquisition in 2021 (Walgreens) and the $10.6 billion plan to buy Oak Street Health (CVS).

VillageMD also bought primary care clinic operator Summit Health-CityMD in January 2023, which Walgreens invested $3.5 billion in, and CVS spent roughly $8 billion to acquire Signify Health, a value-based payment platform, in September 2022.

That’s a huge range in percentages, but even if we split it right down the middle, that means at least 50% of medical bills are wrong—50% of the medical bills that are coming into your house and mine—and most healthcare consumers don’t even realize it.

“Collectively the healthcare industry spends over $350 Billion to submit and process claims while still working with cumbersome workflows, inefficient processes, and a changing landscape marked by increasing out-of-pocket cost for patients as well as increasing operating costs.”

The Norm Continues Downhill

For many years hospitals and healthcare organizations have struggled to maintain and improve their operating margins. They continue to face a widening gap between their operating costs and the revenues required to cover not only current costs, but also to finance strategic growth initiatives and investments.

Faced with increased operational costs and associated declines in rates of reimbursement, many healthcare hospital executives and leaders are concerned that they will not achieve margin targets. To stabilize the internal financial issue, some hospital have focused on lowering expenses in order to save costs – an area they control and an area that will show an immediate impact; however, that is not the best solution.

Beware Cost Reductions

Hospital executives are concerned with the effect that these reductions may have on patient quality and service. Finding ways to maximize workflow to lower operating costs is vital. Every dollar not collected negatively impacts short- and long term capital projects, lowers patient satisfaction scores and possibly affects quality of patient care.

Status Today

Hospitals, healthcare organizations and all medical providers are under great pressure to collect revenue in order to remain solvent. And so, here are some of the issues impacting the modern hospital revenue cycle as Obama-Care, or the PP-ACA of 2010, as launched last decade?

Issues Impacting the Revenue Cycle

Several of the major leading issues facing the revenue cycle are:

Impact of Consumer-driven Health – This process has emerged as a new approach to the traditional managed care system, shifting payment flows and introducing new “non-traditional” parties into the claims processing workflow. As market adoption enters the mainstream, consumer-driven health stands to alter the healthcare landscape more dramatically than anything we have seen since the advent of managed care. This process places more financial responsibility on the consumer to encourage value-drive healthcare spending decisions.

Competing high-priority projects –Hospitals are feeling pressured to maximize collections primarily because they know changes are coming down the pike due to healthcare reform and they know they will need to juggle these major initiatives along with the day-to-day revenue cycle operations.

Lack of skilled resources in several areas – Hospital have struggled to find the right personnel with sufficient knowledge of project management, clinical documentation improvement, coding and other revenue cycle functions, resulting in inefficient operations.

Narrowing margins – Declines in reimbursement are forcing hospitals to look at their organization to determine if they can increase efficiencies and automate to save money. Hospitals are faced with the potential of increased cost to upgrade and adapt clinical software while not meeting budget projections. There are a number of factors contributing to the financial pressure including inefficient administrative processes such as redundant data collection, manual processes, and repetitive rework of claims submissions. Also included are organizations using outdated processes and legacy technologies.

Significant market changes – Regardless of what happens with the Patient Protection and Affordable Care Act, hospitals will have to deal with fluctuating amounts of insured and uninsured patients and variable payments.

Limited access to capital – With the trend towards more complex and expensive systems, industry may not have the internal resources and funding to build and manage these systems that keep pace with the trends.

Need to optimize revenue – There are five core areas hospitals have to examine carefully and they are:

ICD-10 – This is an entirely new coding and health information technology issue but is also a revenue issues

System integration – Hospitals need to look at integrating software and hardware systems that can combine patient account billing, collections and electronic health records.

Clinical documentation – Meaningful use will require detailed documentation in order for payment to be made and this is another revenue issue.

Billing and claims management – Reducing denials and reject claims, training staff, improving point-of-service collections and decreasing delays in patient billing can improve the revenue cycle productivity,

Contract analysis– Hospitals need to focus more on negotiating rates with insurers in order to increase revenue.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A relatively new method of registration under the Act of ’33 is known as shelf registration.

Under this rule, an issuer may register any amount of securities that, at the time the registration statement becomes effective, is reasonably expected to be offered and sold within two years of the initial effective date of the registration.

Once registered, the securities may be sold continuously or periodically within 2 years without any waiting period for a registration to clear issuers generally like shelf registration because of the flexibility it gives them to take advantage of changing market conditions.

In addition, the legal, accounting, and printing costs involved in issuance are reduced, since a single registration statement suffices for multiple offerings within the 2 year period. In effect, what the issuer does is register securities that will meet its financing needs for the next 2 years.

It issues what it needs at the current time, and puts the balance on the “shelf” to be taken off the shelf as needed.

Conclusion:

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, urls and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Contact: MarcinkoAdvisors@msn.com

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, I.T, business and policy management ecosystem.

DEFINITION: A Health Savings Account (HSA) is a tax-advantaged account created for or by individuals covered under high-deductible health plans (HDHPs) to save for qualified medical expenses. Contributions are made into the account by the individual or their employer and are limited to a maximum amount each year. The contributions are invested over time and can be used to pay for qualified medical expenses, such as medical, dental, and vision care and prescription drugs.

A Health Savings Account [HSA] can be a good or bad investment to pass on, depending on who the estate planning heir is in relation to you. If you leave it to a spouse, they’ll be able to continue using the money for medical expenses with no taxes or penalties, said Pam Horack, CFP at Pathfinder Planning LLC of Lake Wylie, South Carolina.

“However, if you leave an HSA to your child, estate or other organization, it may be considered income in the year it is received,” she said. “They are not allowed to use the tax advantages for their own healthcare and the income could inadvertently throw your heirs into a higher tax bracket.”

*** One important equity concept that medical professionals should be aware of is the idea of stock splits.

In a stock split, a corporation issues a set number of shares in exchange for each share held by share holders. Typically, a stock split increases the number of shares owned by a shareholder.

For example, XYZ Corp. may declare a 2-for-1 split, which means that share holders will receive two shares for each share that they own. However, corporations can also declare a reverse stock split, such as a 1-for-2 split where shareholders would receive 1 share for every two shares that they own.

While stock splits can either increase or decrease the number of shares that a share holder owns, the most important thing to understand about stock splits is that they have no impact on the aggregate value of the shareholder’s position in the company.

Using the XYZ Corp. example above, if the stock is trading at $10 per share, an investor owning 100 shares has a 24 total position of $1,000. After the 2-for-1 split occurs the investor will now own 200 shares, but the value of the stock will adjust downward from $10 per share to $5 per share.

Thus, the investor still owns $1,000 of XYZ stock. While stock splits are often interpreted as signals from management that conditions in the company are strong, there is no intrinsic reason that a stock split will result in subsequent stock appreciation.

Many physicians and other investors — even those that meet net worth guidelines — are surprised to learn that there exists a $500 – 999 billion, or more, alternative investment industry that is not generally marketed to the public. Such alternative investments have also been known as hedge funds or private investment funds.

Unlike mutual funds, these alternative investments can be structured in a wide variety of ways. Because of the very same regulations discussed above, these funds cannot be advertised, but they are far from illegal or illicit.

In fact, physicians were among the most significant early investors in one of the last century’s most successful hedge funds. Mr. Warren Buffett, Chairman of Berkshire Hathaway, Inc. and a legendary investor got his start in 1957 running the Buffett Partnership, an alternative investment fund not open to the general public. Mr. Buffett’s first public appearance as a money manager was before a group of physicians in Omaha, Nebraska. Eleven decided to put some money with him. A few of these original investors followed him into Berkshire Hathaway, now among the most highly valued companies in the world.

The alternative investment, or hedge, funds of today are similar to the original Buffett Partnership in many ways. So, we will discuss several unique terms which potential investors should be aware.

Hedge funds may feature a hurdle rate as part of the calculation of the fund manager’s performance incentive compensation. Also known as a “benchmark,” the hurdle rate is the amount, expressed in percentage points, an investor’s capital account must appreciate before the account becomes subject to a performance incentive fee. Potential medical investors should view the hurdle rate as a form of protection in context with other features of the fee arrangement.

The hurdle rate, which benchmarks a single year’s performance, may be considered mutually exclusive of any other year, or the hurdle rate may compound each year. The former case is more common. In the latter case, a portfolio manager failing to attain a hurdle rate in the first year will find the effective hurdle rate considerably higher during the second year.

Once a fund manager attains the hurdle rate for an investor, the medical investor’s capital account may be charged a performance incentive fee only on the performance above and beyond the hurdle rate. Alternatively, the account may be charged a performance fee for the entire level of performance, including the performance required to attain the hurdle rate. Other variations on the use of the hurdle rate exist, and are limited only by the contract signed between the fund manager and the investor. The hurdle rate is not generally a negotiating point, however.

Example:

A fund charges a performance fee with a 6 percent hurdle rate, calculated in mutually exclusive manner. Dr. Lanouettea, a radiologist investor places $100,000 with the fund. The first year’s performance is 5 percent. The investor therefore owes no performance fee during the first year because the portfolio manager did not attain the hurdle rate. During year two, the portfolio manager guides the fund to a 7 percent return. Because the hurdle rate is mutually exclusive of any other year, the portfolio manager has attained the 6 percent hurdle rate and is entitled to a performance fee.

Highwater Mark

Some funds feature a highwater mark provision, also known as a ”loss-carryforward” provision. As with the hurdle rate, potential investors should consider the highwater mark a form of protection. A high water mark is an amount equal to the greatest value of an investor’s capital account, adjusted for contributions and withdrawals. The high water mark ensures that the hedge fund manager charges a performance incentive fee only on the amount of appreciation over and above the highwater mark set at the time the performance fee was last charged. The current trend is for newer funds to feature this highwater mark, while older, larger funds may not feature it.

Example:

A fund charges a 20 percent performance fee with a highwater mark but no hurdle rate. Dr. Butalak, a dentist investor contributes $100,000 to the fund. During the first year, the hedge fund manager grows that capital account to $110,000 and charges a 20 percent performance fee, or $2,000. The ending capital account balance and highwater mark is therefore $108,000. During year two, the account falls back to $100,000, but the highwater mark remains $108,000. During year three, in order for the manager to charge a performance fee, the manager must grow the capital account to a level above $108,000.

Clawback Provision

Rarely, a fund may provide investors with a clawback provision. This term, borrowed from the venture capital fund world, such provisions result in a refund to the investor of all or part of a previously charged performance fee if a certain level of performance is not attained in subsequent years. Such refunds in the face of poor or inadequate performance may not be legal in some states or under certain authorities.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on June 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: 4.6%. That’s how much the average income tax refund increased YoY, from $2,878 in April 2023 to $3,011 as of April 5th. (Axios)

Quote: “Wall Street has never been known for high character and high values. Is there a willingness to support Trump if it looks like he’s on the right track? Yes. I’m not proud of that, and I’m not part of that either.”—Dan Lufkin, co-founder of investment bank Donaldson, Lufkin & Jenrette (Bloomberg)

Read: Bank of America’s CEO sees an overall cautiousness on display in the current spending choices of consumers and businesses. (CNBC)

The May jobs report will drop on Friday: Little change is expected from April, when the unemployment rate ticked up to 3.9% and fewer jobs were added than expected (175,000). This jobs report will be one of the final pieces of economic data to drop before the Fed meets on June 11th and 12th. The central bank is unlikely to announce an interest rate cut.

Software is no longer eating the world. For the first time, chip stocks now account for the heaviest weighting in the S&P 500, taking the top spot away from software companies last week. Salesforce and other enterprise software giants are getting crushed as companies prioritize generative AI investments (chips and servers) over SaaS products.

Approximately 250 hospitals across the U.S. are completely or partially physician owned. These physician-owned hospitals (POHs) can offer a variety of services, from general care to specialty services, such as cardiovascular or orthopedic care, known as “focused factories.”

Over the past several decades, healthcare providers and policymakers have claimed that POHs have a negative impact on the healthcare industry, suggesting that: (1) POHs “cherry-pick” the most profitable patients; (2) the quality of care provided at POHs is substandard; and, (3) conflicts of interest exist due to the financial incentive for physician owners to refer patients to their POHs. (Read more…)

Posted on June 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

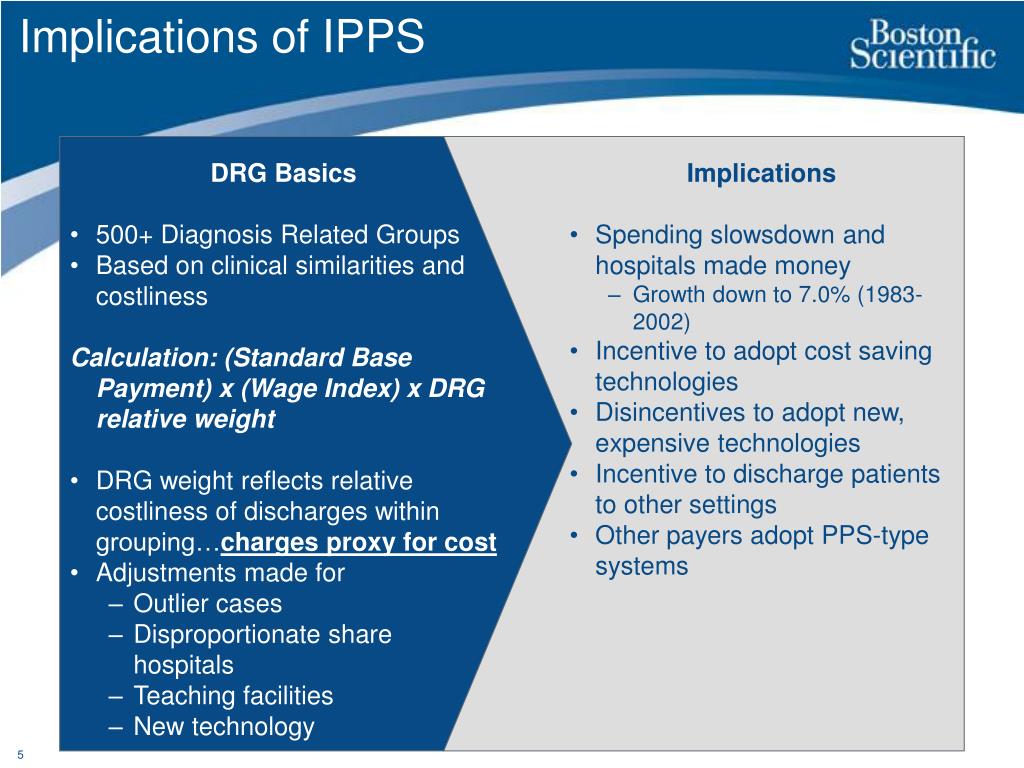

On April 10th, 2024, the Centers for Medicare & Medicaid Services (CMS) released its proposed rules for the payment and policy updates for the Medicare inpatient prospective payment system (IPPS) and long-term care hospital prospective payment system (LTCH PPS) for fiscal year (FY) 2025.

Posted on June 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

The Institute of Medical Business Advisors is a leading national scope provider of healthcare economics, finance, investing, managerial accounting, policy, management and business administration education and medical practice management textbooks, reports, hand-books, dictionaries, journals, white-papers, fair-market valuations [FMV] and legal advisory opinions using multi-platform and traditional seminars and channels of knowledge distribution. iMBA helps the nation’s financial, healthcare and education professionals make decisive improvements in their direction and performance by empowering them through unbiased information, consultants and proprietary tools, books, templates and B-school styled case models.A virtuous “win-win” situation for all concerned.

The firm serves universities, medical, business, graduate and nursing schools; physicians, dentists, attorneys and legal societies – accountants, financial service providers, stock brokers, RIAs, wealth and hedge fund managers – emerging entities, hospitals, clinics, outpatient centers, CXOs and their BODs – the press, media and related academic entities.

Posted on May 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS THE “MEDICARE COST CONTROL EFFICIENCY” PARADOX?

The 800 Pound Gorilla in the Medical Treatment Room

By Staff Reporters

Blogger Ezra Klein opined more than a decade ago that one of the dirty little secrets of the health-care system is that Medicare has done a much better job controlling costs than private health insurers. It is a paradox!

DEFINITION: A paradox is a seemingly absurd or self-contradictory statement or proposition that when investigated may prove to be well founded or true.

***

***

QUERY:But, what about Medicare, cost control efficiency, today?

Posted on May 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On May 9th, 2024, the University of Pittsburgh Medical Center (UPMC), a large nonprofit healthcare system that owns a number of hospitals, medical practices, and other subsidiaries, announced that they would pay $38 million to settle a longstanding Stark Law case which had triggered a violation of the False Claims Act (FCA). The lawsuit claimed that several of UPMC’s surgeons ordered complex and unnecessary procedures to increase their earnings.

Posted on May 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Shopping Suggestions

By Rick Kahler MS CFP®

Shopping for a financial adviser you can trust has never been easy. The Department of Labor [DOL] rule requiring brokers to act in a fiduciary capacity when dealing with retirement plan assets has not made it any easier. The government’s intent was to help consumers clearly distinguish when financial professionals can be relied upon to give unbiased financial advice or when they are acting in their own interests to sell a financial product. Unfortunately, the rule has only exacerbated the confusion.

When shopping for financial advisers, you need to investigate their education, niche, process, compensation structure, and experience to see whether they are a good fit for your needs. Equally important, it’s up to you to do a background check and determine whose interest the adviser is looking out for. No one else will do it for you.

Two-Steps

Here are two important steps you can take to greatly increase your chances of getting someone who will truly be looking out for you.

First, ask any adviser you deal with to sign a statement affirming they will act in the capacity of a fiduciary to you, meaning you will be a client, not a customer. A copy of this form can be found at www.advisorperspectives.com. Advisers unwilling to sign the Form Adv are not likely to be fiduciaries who will put your interests first.

Second, check the adviser’s background. If advisers receive any type of fee, they are held to a fiduciary standard automatically by the SEC. Still, it’s wise to check their background for any misconduct, which you can do at www.adviserinfo.sec.gov. If advisers sell securities, mutual funds, private REITs, or limited partnerships and receive any type of commission, they will be regulated by FINRA. You can go to BrokerCheck.finra.org to view their records for misconduct.

It’s important to check an adviser’s background because being found guilty of misconduct doesn’t mean they can’t actively be selling financial products.

For example, in a March 7 article at kitces.com, financial planner and writer Michael Kitces points out that over 73% of FINRA-registered brokers who FINRA lists as having a misconduct “are still employed a year later, despite the fact that such brokers are a whopping 5x more likely to engage in misconduct again in the future.”

Kitces explains that while just 7.3% of all FINRA brokers have some type of misconduct on their records, only about half of them actually lose their jobs and about half of those find employment with another firm. Additionally, it seems some firms have more of a culture of employing brokers with misconduct.

***

***

The top five brokerage firms with the highest (15% or more) concentration of brokers with misconduct are Oppenhiemer & Co, First Allied Securities, Wells Fargo Advisers Financial Network, UBS Financial Services, and Cetera Advisers. This is according to a working paper, “The Market for Financial Adviser Misconduct,” by Mark Egan, Gregor Matvos, and Amit Seru, business school professors at the University of Chicago and University of Minnesota. Geographic location also makes a big difference with the states of California, Florida, and New York having counties with much higher concentrations of brokers guilty of misconduct (15 – 30%) than states like Pennsylvania, Kansas, Iowa, Kentucky, and Vermont with the counties having the lowest concentration (2 – 3%).

Kitces reminds us that the “single greatest predictor of whether a broker will engage in misconduct is whether he/she has engaged in any prior misconduct.”

Assessment

For this reason, it’s crucial to make FINRA’s Broker Check part of your research before hiring a financial adviser. Before trusting any adviser to put your interests first, look out for your own interests by investigating the adviser’s history.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

T+1 DayImplications

By Staff Reporters

***

***

Starting today on May 28th, 2024, the settlement period for most securities traded on U.S. exchanges or over the counter will shorten from two business days (T+2) to one business day (T+1). For most investors, this event may have little or no impact. However, there are a few key things to know.

New shortened settlement period reduces risk.

The T+1 settlement period may benefit investors like you by reducing credit and liquidity risks present between the trade date and the settlement date. This is an industry-wide change for most security transactions and types, such as stocks, bonds, municipal securities, exchange-traded products, secondary market CDs, unit investment trusts, and certain mutual funds and limited partnerships that trade on U.S. exchange or over the counter. There will be no change to the settlement period for treasuries, options, or futures as they already use the T+1 settlement period.

Cost basis Implications

After T+1 goes into effect, any changes to your cost basis method will have to be made within one business day of the trade, not two.

Margin interest implications

If you place a trade in a margin account and then need to sell money market funds (“MMFs”) to cover your purchase, the funds will need to be available prior to or on the same day as the trade settlement to avoid being charged margin interest. For trades placed for bonds, equities and other securities, the MMFs will need to be sold by 4 p.m. ET the same day the purchase trade is placed.To avoid accruing margin interest:•MMFs will need to be sold by 4 p.m. ET to cover trading in the after-hours market that same day.•MMFs will need to be sold by 4 p.m. ET to cover purchases of Fixed Income securities that can be traded until 5 p.m. ET the same day.

Your next steps.

The new settlement period will automatically apply to any new trades executed on or after May 28, 2024. You may need to pay closer attention to how the shorter settlement time could affect your investment, trading, or tax decisions.

Posted on May 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A Non-Traditional Accounting System

[By Dr. David Marcinko MBA MEd CMP]

Sooner or later you will want to ascertain and then demonstrate the cost effectiveness of your medical care. By using the process of Activity Based Cost (ABC) management, you will be able to do so. But, if you’re using a traditional accounting system, you won’t know a thing about your activity costs. Here’s how.

Traditional Cost Accounting Methods

In a traditional medical practice cost accounting system, costs are assigned to different procedures and services based on volume. In others words, office costs are spread over the entire office’s product line and you may not know the true profitability of any single medical activity. So, if the office is doing more “procedures” than general medicine, for example, more indirect office overhead costs will be allocated to the procedural portion of the practice.

ABC management, on the other hand, determines the actual costs of the resources that each service consumes. Because general medicine requires more human resources than “technical procedures,” ABC management will assign more costs to the general medical portion of the practice.

Accordingly, most physicians, office managers, and their accountants are surprised that a prior notion of office profitability is different than previously thought. ABC management is just more accurate in measuring medical service profitability than traditional accounting methods.

Medical Activity Cost Drivers

Examples of medical activities that are office cost drivers include such items as monitoring vital signs, taking radiographic images, removing dressings or casts, performing laboratory tests or veni-punctures, surgical set-ups or operative procedures; etc.

However, in the office setting, the most economically important activities are listed as specific CPT codes for each medical specialty. The most important end result of ABC management is the shift of general overhead costs to low volume services from high volume services. These effects are not symmetrical as there is a bigger dollar effect on the per-unit costs of the low volume service.

ABC Managerial Accounting Improvements

ABC management improves office managerial cost accounting systems in three ways:

It increases the number of cost pools used to accumulate general overhead office costs. Rather than accumulate overhead costs in a single office-wide pool, costs are accumulated by activity, service or procedure.

It changes the base used to assign general overhead costs to services or patients. Rather than assigning costs on the basis of a measure of volume (employee or doctor hours), costs are assigned on the basis of medical services or activities that generated those costs.

It changes the nature of many overhead costs in that those formerly considered indirect, are now traced to specific activities or services. The office service mix may then be adjusted accordingly, for additional profit.

Methodology

In order to perform an ABC analysis for your medical office, calculate the cost of delivering a single unit of medical or surgical activity using only the work component of the resource based relative value scale (RBRVS).

Do this by adding up your office’s average variable expenses for the prior 1-3 years. Now, count the number of work resource based relative value units (RBRVUs) delivered for each CPT code for the same time period, using the latest edition of the Federal Register to obtain the latest list of RVUs by CPT code. Then divide total variable expenses by the total number of work RVUs in order to arrive at the marginal cost of a single unit of service for the time period being evaluated.

For example, if your office had variable expenses of $480,000, and produced 80,000 work RVUs last year, it cost $6, on top of the office’s fixed expenses, to deliver one unit of work product. So, if an HMO plan offers to reimburse you at a rate of $11 per member, per month, and you can expect to reasonably deliver on average of one RVU pm/pm, you’ll earn enough on the contract to cover your marginal costs and some of your fixed and direct expenses.

Remember, this method assumes that you have the excess operating capacity and time slots, available and unused, to see the additional patients of the new plan without adding extra overhead expenses to service the contract.

If not, or if you plan for capitation to become a major portion of your practice, you might want the capitated contract(s) to cover all your office expenses, so be sure to include both the fixed and other direct costs to your variable cost calculations. ABC determines the actual costs of resources rendered for each activity and represents a real measure of practice profitability. Office service mix can then be changed to either maximize revenues or better suit your practice personality.

A Caveat

Suppose however, that a medical service is competitively priced but still shows that the CPT code is unprofitable. For example, the costs of special requests can adversely affect office profits. Yet, special patient requests are one of the biggest reasons that a CPT code or procedure isn’t profitable.

In this case, look closely at activity costs and determine which ones are being performed inefficiently. Improving the efficiency of those kinds of medical services, or referring them out or abandoning them all together, will increase office profitability.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

VARIANCE AND BOTTLE-NECK ACCOUNTING

DR. DAVID E. MARCINKO MBA MEd CMP

Any healthcare organization usually has several processes involved in the utilization of its patient services. Unfortunately, bottlenecks may arise which constrain the amount of services any given healthcare entity can deliver.

Accounting Definition

An accounting “bottleneck” is a process that has a low output and limits total healthcare entity revenues. If a medical business entity wants to increase sales or revenues, it has to solve its bottleneck [ie., access management] problems.

Traditional Variance Analysis Dilemma

With traditional variance analysis [VA], managers and administrators analyze the difference between budgeted patient revenues and actual revenues. Typically, differences between budgeted revenues and actual revenues are analyzed as seen in the example below.

Initially postulated by Horngren and Foster for manufacturing processes, VA can now be modified for medical business entity use.

Example:

Patient Service Units

Contract/UCR Fee

Budgeted sales revenues

10,000,000

*

1,23

=

$ 12,300,000

Actual sales revenues

9,000,000

*

1,21

=

$ 10,890,000

-/- —————-

Total variance

$ 1,410,000

Traditional Assessment

Actual patient revenues were lower than budgeted; and the unfavorable patient sales volume variance was (9,000,000 – 10,000,000) * $ 1,23 = – $ 1,230,000.

The actual patient revenue price was lower than budgeted as the unfavorable price variance was: ($ 1,21 – $ 1,23) * 9,000,000 = – 180,000.

Traditional variance analysis however does not point out which of the processes were bottlenecks, which caused the negative volume variance.Thus, a normal variance analysis can’t be used to solve bottlenecks in a clinic, hospital or medical practice.

Enter B-N Accounting

In bottleneck accounting however, managers and healthcare administrators determine the bottlenecks in a medical organization.And, a bottleneck accounting report shows which process were bottlenecks occur and how much money is lost in each bottleneck.

Example:

Bottleneck Patient Sales Revenues

$ 800,000

Bottleneck Dep. II

$ 350,000

Other Bottlenecks

$ 80,000

+ —————-

Total Volume Variance

$ 1,230,000

Conclusion:

The managerial accounting modification for “bottlenecks” not only points out the bottlenecks to solve, it also shows which bottleneck is to be handled first.

And so, what are your thoughts on this accounting machination? Please comment.

References:Horngren, C. T. and G. Foster, ‘Cost Accounting, A Managerial Emphasis’, Prentice-Hall, Inc. 1987.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the MedicalExecutive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

While financial planning rules of thumbs are useful to people as general guidelines, they may be too oversimplified in many situations, leading to underestimating or overestimating an individual’s needs. This may be especially true for physicians and many medical professionals. Rules of thumb do not account for specific circumstances or factors occurring at a particular time, or that could change over time, which should be considered for making sound financial decisions.

For example, in a tight job market, an emergency fund amounting to six months of household expenses does not consider the possibility of extended unemployment. I’ve always suggested 2-3 years for doctors. Venture capitalist lay-offs of physicians during the pandemic confirm this often criticized benchmark opinion of mine.

As another example, buying life insurance based on a multiple of income does not account for the specific needs of the surviving family, which include a mortgage, the need for college funding and an extended survivor income for a non-working spouse. Again a huge home mortgage, or several children or dependents, may be the financial bane of physician colleaguesand life insurance.

A home purchase should cost less than an amount equal to two and a half years of your annual income. I think physicians in practice for 3-5 years might go up to 3.5X annual income; ceteras paribus.

Save at least 10-15% of your take-home income for retirement. Seek to save 20% or more.

Have at least five times your gross salary in life insurance death benefit. Consider 10X this amount in term insurance if young, and/or with several children or other special circumstances.

Pay off your highest-interest credit cards first. Agreed.

The stock market has a long-term average return of 10%. Agreed, but appreciated risk adjusted rates of return..

You should have an emergency fund equal to six months’ worth of household expenses. Doctors should seek 2-3 years.

Your age represents the percentage of bonds you should have in your portfolio. Risk tolerance and assets may be more vital.

Your age subtracted from 100 represents the percentage of stocks you should have in your portfolio. Risk tolerance and assets may still be more vital.

A balanced portfolio is 60% stocks, 40% bonds. With historic low interest rates, cash may be a more flexible alternative than bonds; also avoid most bond mutual funds as they usually never mature.

There are also rules of thumb for determining how much net worth you will need to retire comfortably at a normal retirement age. Here is the calculation that Investopedia uses to determine your net worth:

If you are employed and earning income: ((your age) x (annual household income)) / 10.

If you are not earning income or you are a student: ((your age – 27) x (annual household income)) / 10.

The U.S. healthcare payment and delivery system is increasingly moving to a value- and quality-based system. Accountable care organizations (ACOs) are at the forefront of delivering high-quality and cost-effective care to millions of Medicare beneficiaries and privately insured patients, incentivized by substantial shared savings for those who increase quality while containing costs.

This third installment of a five-part series on the valuation of ACOs will discuss the reimbursement environment in which ACOs participate.(Read more…)

Posted on May 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Women’s health startups are still closing multi million-dollar funding deals despite a challengingventure capital (VC) landscape in which VC dollars are on track to fall by 73% this year compared to last.

For example, in the last year, virtual maternity care program Pomelo Careraised $33 million in seed and Series A rounds led by Andreessen Horowitz; Caraway Health, a digital mental, physical, and reproductive health services platform, raised almost $17 million in a Series A round led by Maveron and GV (formerly Google Ventures); and Intrinsic, which acquires brands that make women’s health products, announced a $15 million equity fund raise (which is when a company raises money by selling its shares).

Posted on May 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd CMP

Understanding the Prisoner’s Dilemma

[From Wikipedia, the free encyclopedia]

As all economists and psychologists know, the prisoner’s dilemma is a standard example of a game analyzed in game theory that shows why two completely “rational” individuals might not cooperate, even if it appears that it is in their best interests to do so. It was originally framed by Merrill Flood and Melvin Dresher working at RAND in 1950. Albert W. Tucker formalized the game with prison sentence rewards and named it, “prisoner’s dilemma” (Poundstone, 1992), presenting it as follows:

Two members of a criminal gang are arrested and imprisoned. Each prisoner is in solitary confinement with no means of communicating with the other. The prosecutors lack sufficient evidence to convict the pair on the principal charge. They hope to get both sentenced to a year in prison on a lesser charge.

Simultaneously, the prosecutors offer each prisoner a bargain. Each prisoner is given the opportunity either to: betray the other by testifying that the other committed the crime, or to cooperate with the other by remaining silent.

The offer is:

If A and B each betray the other, each of them serves 2 years in prison

If A betrays B but B remains silent, A will be set free and B will serve 3 years in prison (and vice versa)

If A and B both remain silent, both of them will only serve 1 year in prison (on the lesser charge)

It is implied that the prisoners will have no opportunity to reward or punish their partner other than the prison sentences they get, and that their decision will not affect their reputation in the future. Because betraying a partner offers a greater reward than cooperating with him, all purely rational self-interested prisoners would betray the other, and so the only possible outcome for two purely rational prisoners is for them to betray each other.

***

***

The interesting part of this result is that pursuing individual reward logically leads both of the prisoners to betray, when they would get a better reward if they both kept silent.

In reality, humans display a systemic bias towards cooperative behavior in this and similar games, much more so than predicted by simple models of “rational” self-interested action. A model based on a different kind of rationality, where people forecast how the game would be played if they formed coalitions and then they maximize their forecasts, has been shown to make better predictions of the rate of cooperation in this and similar games given only the payoffs of the game.

An extended “iterated” version of the game also exists, where the classic game is played repeatedly between the same prisoners, and consequently, both prisoners continuously have an opportunity to penalize the other for previous decisions. If the number of times the game will be played is known to the players, then (by backward induction) two classically rational players will betray each other repeatedly, for the same reasons as the single shot variant. In an infinite or unknown length game there is no fixed optimum strategy, and Prisoner’s Dilemma tournaments have been held to compete and test algorithms.

In Health Economics

Advertising is sometimes cited as a real-example of the prisoner’s dilemma.

When cigarette advertising was legal in the United States, competing cigarette manufacturers had to decide how much money to spend on advertising. The effectiveness of Firm A’s advertising was partially determined by the advertising conducted by Firm B. Likewise, the profit derived from advertising for Firm B is affected by the advertising conducted by Firm A. If both Firm A and Firm B chose to advertise during a given period, then the advertising cancels out, receipts remain constant, and expenses increase due to the cost of advertising. Both firms would benefit from a reduction in advertising.

***

***

However, should Firm B choose not to advertise, Firm A could benefit greatly by advertising. Nevertheless, the optimal amount of advertising by one firm depends on how much advertising the other undertakes. As the best strategy is dependent on what the other firm chooses there is no dominant strategy, which makes it slightly different from a prisoner’s dilemma. The outcome is similar, though, in that both firms would be better off were they to advertise less than in the equilibrium. Sometimes cooperative behaviors do emerge in business situations.

For instance, cigarette manufacturers endorsed the making of laws banning cigarette advertising, understanding that this would reduce costs and increase profits across the industry. This analysis is likely to be pertinent in many other business situations involving advertising

Without enforceable agreements, members of a cartel are also involved in a (multi-player) prisoners’ dilemma. ‘Cooperating’ typically means keeping prices at a pre-agreed minimum level. ‘Defecting’ means selling under this minimum level, instantly taking business (and profits) from other cartel members. Anti-trust authorities want potential cartel members to mutually defect, ensuring the lowest possible prices for consumers.

The prisoner’s dilemma game can be used as a model for many real world situations involving cooperative behavior. In casual usage, the label “prisoner’s dilemma” may be applied to situations not strictly matching the formal criteria of the classic or iterative games: for instance, those in which two entities could gain important benefits from cooperating or suffer from the failure to do so, but find it merely difficult or expensive, not necessarily impossible, to coordinate their activities to achieve cooperation.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

COMMENTS APPRECIATED

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

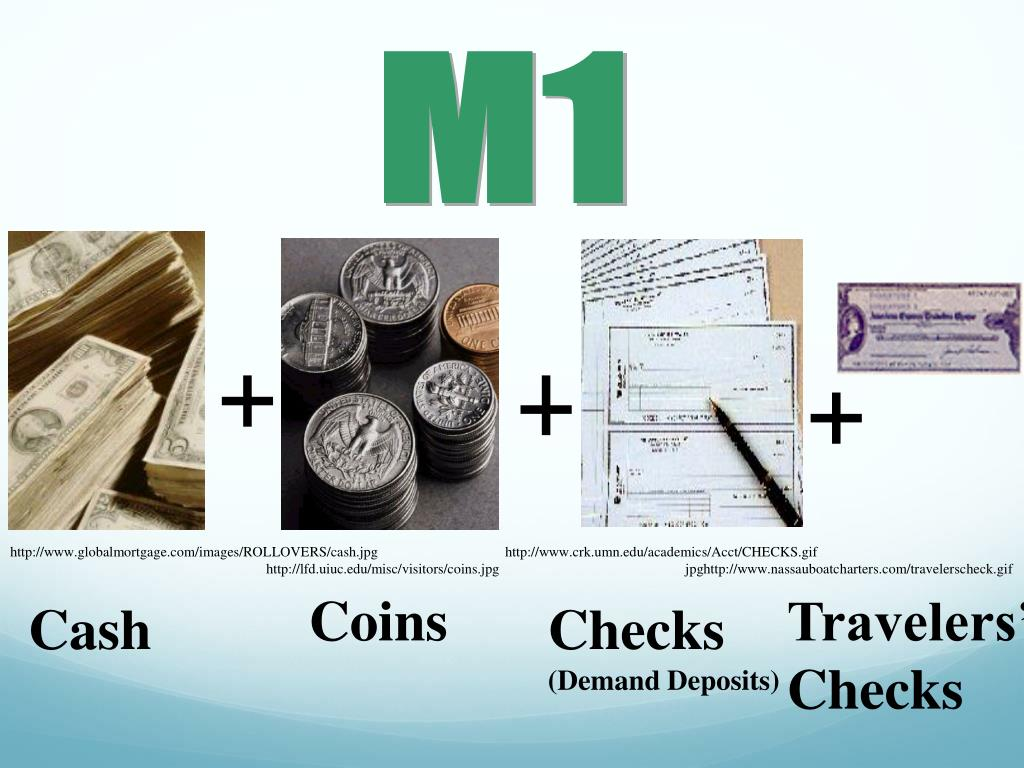

DEFINITION: In macro-economics, the money supply (or money stock) refers to the total volume of currency held by the public at a particular point in time. There are several ways to define “money”, but standard measures usually include currency in circulation (i.e. physical cash) and demand deposits (depositors’ easily accessed assets on the books of financial institutions . The Central Bank [FOMC] of a country may use a definition of what constitutes legal tender for its purposes.

Though there are a few variations of money supply, most economists tend to focus on M1 and M2. The former takes into account cash and coins in circulation, as well as demand deposits in checking accounts and traveler’s checks. In other words, money that’s either in your hand or can be accessed very easily.

Meanwhile, M2 accounts for everything in M1 and adds savings accounts, money market funds, and certificates of deposit (CDs) below $100,000. It’s money you have access to, but it takes a little extra effort to put this capital to work. It’s M2 money supply that’s raising eyebrows on Wall Street and making history.

***

What’s of interest is what’s happened to M2 money supply over the trailing year. Following a peak of $21.7 trillion in July 2022, M2 has fallen to a fresh reading of $20.81 trillion, as of May 2023. Although the May reading was higher than April and broke a nine-month downtrend, we’ve still witnessed a 4.1% aggregate drop in M2 from its all-time high.

Considering that M2 enjoyed a historic expansion during the pandemic, it’s certainly possible that a 4.1% decline can be shrugged off as nothing more than money supply reverting back to the mean. But history suggests otherwise.

Though history rarely repeats itself on Wall Street, it often rhymes. We haven’t seen a meaningful year-over-year decline in M2 money supply since the Great Depression in 1933.

***

And so, based on what we’re seeing from M2 money supply, commercial bank lending, and domestic banks tightening their lending standards for C&I loans, the ingredients for a U.S. recession are most definitely there. Stock losses have, historically, been most pronounced in the months that follow the official declaration of a recession by the eight-economist panel of the National Bureau of Economic Research.

However, Wall Street’s performance is largely dependent on your investment time frame. If you’re patient, these and other potentially worrisome money metrics represent nothing more than temporary white noise.

Although some doctors might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a practice. And so, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times; like today with the stock market busts, venture capitalists invading health care, corona virus the pandemic, aging baby boomer physicians and the great resignation; etc.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little money can sure reduces the unhappiness.”

Unfortunately, today there is still more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks, ACA, and increased competition to floundering equity markets, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes. And then Covid-19, corona, and covid.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.1

How To Prepare A Personal Cash Flow Budget

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medial office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the podiatrist can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.2

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of the specter of rising inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.3

In fact, I have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. The new limit is $250,000. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).4

How To Budget In The Midst Of A [Corona] Crisis

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives of the corona pandemic. A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”5

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.6

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.7

The Author:

Dr. Marcinko is a former university endowed chairman and professor, former certified financial planner and has been a medical management advisor for more than two decades. He is the CEO of www.MedicalBusinessAdvisors.com, a health economics and business finance consulting firm.

References:

1. Marcinko DE (Ed). The Business of Medical Practice (Advanced Profit Maximizing Techniques for Savvy Doctors). Springer Publishers, New York, NY, 2000 and 2004 2. Marcinko DE (Ed). Financial Planning for Physicians and Advisors, Jones and Bartlett Publishers, Sudbury, MA, 2005 3. Marcinko DE (Ed). Risk Management and Insurance Panning for Physicians and Advisors, Jones and Bartlett Publishers, Sudbury, MA, 2006. 4. Marcinko DE, Hetico HR. The Dictionary of Health Insurance and Managed Care. Springer Publishing, New York, 2007. 5. Marcinko DE, Hetico HR. The Dictionary of Health Economics and Finance. Springer Publishing, New York, 2008. 6. Marcinko DE, Hetico HR. Healthcare Organizations (Financial Management Strategies). Standard Technical Publishers, Blaine, WA, 2009. Additional Reference 7. Schmuckler E. Bridging Financial Planning and Human and Human Psychology. In, Marcinko DE (Ed): Financial Planning for Physicians and Healthcare Professionals. Aspen Publications, New York, NY, 2001, 2002 and 2003.

Posted on May 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

It’s the first anniversary of the Medicaid unwinding for many states, a process that kicked off when federal rules that had kept people on Medicaid and the Children’s Health Insurance Program (CHIP) through the pandemic expired. And while states could redetermine eligibility again, things have “unwound” more than some experts predicted. Children were kicked off the rolls at higher rates than adults, according to a new study the Urban Institute released May 2. Twelve states—Montana, Iowa, South Dakota, Alabama, Idaho, Georgia, Texas, Arkansas, Oklahoma, Florida, Mississippi, Colorado—exceeded 100% of their total projections for disenrolling children.

The S&P 500® index (SPX) was little changed at 5,187.67; the Dow Jones Industrial Average gained 172.13 points (0.4%) to 39,056.39; the NASDAQ Composite® ($COMP) declined 29.80 points (0.2%) to 16,302.76.

The 10-year Treasury note yield (TNX) rose more than 3 basis points to 4.496%.

The CBOE Volatility Index® (VIX) fell 0.23 to 13.00.

Retail and real estate shares were among the weakest areas Wednesday, while banks and utilities were firm. Utility shares extended a nearly month-long rally, which may in part reflect greater expectations for Fed rate cuts. Lower interest rates can make utility shares with high dividend yields relative to Treasuries more appealing. The Dow Jones Utility Average ($DJU) rose 0.5% to end at its highest level since late July and is up 12% from a mid-April low.

And, Shopify’s value plunged by nearly $20 billion after the online payments company released a gloomy forecast for this quarter. It’s the latest pandemic darling to stumble: According to the Financial Times, the firms that skyrocketed during lockdowns have lost a collective $1.5 trillion in value since the end of 2020.

Steward Health Care System, the largest U.S. physician-owned hospital operator, is expected to file for chapter 11 bankruptcy as soon as Sunday, according to a WSJ report, which cited people familiar with the matter. Steward Health Care is the largest tenant of Medical Properties Trust (NYSE: MPW). Steward Health Care hired restructuring advisers to improve its liquidity and restore its balance sheet in January 2024.

DEFINITION: Mental accounting attempts to describe the process whereby people code, categorize and evaluate economic outcomes. The concept was first named by Richard Thaler. Mental accounting deals with the budgeting and categorization of expenditures. People budget money into mental accounts for expenses or expense categories

Mental Accounting is the act of bucketizing investments and then reviewing the performance of the individual buckets separately (e.g. investing at low savings rate while paying high credit card interest rates).

***

Examples of mental accounting are: (1) matching costs to benefits (wanting to pay for vacation before taking it and getting paid for work after it was done, even though from perspective of time value of money the opposite should be preferred0, (2) aversion to debt (don’t like long-term debt for short-term benefit), (3) sunk-cost effect (illogically considering non-recoverable costs when making forward-going decisions).

In investing, treating buckets separately and ignoring interaction (correlations) induces people not to sell losers (even though they get tax benefits), prevent them from investing in the stock market because it is too risky in isolation (however much less so when looked at as part of the complete portfolio including other asset classes and labor income and occupied real estate), thus they “do not maximize the return for a given level of risk taken).

Financial benchmarking can assist healthcare managers and professional financial advisors in understanding the operational and financial status of their organization or practice.

The general process of financial benchmarking analysis may include three elements: (1) Historical subject benchmarking; (2) Benchmarking to industry norms; and, (3) Financial ratio analysis.

History

Historical subject benchmarking compares a healthcare organization’s most recent performance with its reported performance in the past in order to: examine performance over time; identify changes in performance within the organization (e.g., extraordinary and non-recurring events); and, to predict future performance.

As a form of internal benchmarking, historical subject benchmarking avoids issues such as: differences in data collection and use of measurement tools; and, benchmarking metrics that often cause problems in comparing two different organizations.

However, it is necessary to common size data in order to account for company differences over time that may skew results.

Benchmarking

Benchmarking to industry norms, analogous to Fong and colleagues’ concept of industry benchmarking, involves comparing internal company-specific data to survey data from other organizations within the same industry. This method of benchmarking provides the basis for comparing the subject entity to similar entities, with the purpose of identifying its relative strengths, weaknesses, and related measures of risk.

***

***

Financial Ratio Analysis

The process of benchmarking against industry averages or norms will typically involve the following steps:

Identification and selection of appropriate surveys to use as a benchmark, i.e., to compare with data from the organization of interest. This involves answering the question, “In which survey would this organization most likely be included?”;

If appropriate, re-categorization and adjustment of the organization’s revenue and expense accounts to optimize data compatibility with the selected survey’s structure and definitions (e.g., common sizing); and,

Calculation and articulation of observed differences of organization from the industry averages and norms, expressed either in terms of variance in ratio, dollar unit amounts, or percentages of variation.

Trends

Financial ratio analysis typically involves the calculation of ratios that are financial and operational measures representative of the financial status of an enterprise. These ratios are evaluated in terms of their relative comparison to generally established industry norms, which may be expressed as positive or negative trends for that industry sector. The ratios selected may function as several different measures of operating performance or financial condition of the subject entity.

The Selected Ratios

Common types of financial indicators that are measured by ratio analysis include:

Liquidity. Liquidity ratios measure the ability of an organization to meet cash obligations as they become due, i.e., to support operational goals. Ratios above the industry mean generally indicate that the organization is in an advantageous position to better support immediate goals. The current ratio, which quantifies the relationship between assets and liabilities, is an indicator of an organization’s ability to meet short-term obligations. Managers use this measure to determine how quickly assets are converted into cash.

Activity. Activity ratios, also called efficiency ratios, indicate how efficiently the organization utilizes its resources or assets, including cash, accounts receivable, salaries, inventory, property, plant, and equipment. Lower ratios may indicate an inefficient use of those assets.

Leverage.Leverage ratios, measured as the ratio of long-term debt to net fixed assets, are used to illustrate the proportion of funds, or capital, provided by shareholders (owners) and creditors to aid analysts in assessing the appropriateness of an organization’s current level of debt. When this ratio falls equal to or below the industry norm, the organization is typically not considered to be at significant risk.

Profitability. Indicates the overall net effect of managerial efficiency of the enterprise. To determine the profitability of the enterprise for benchmarking purposes, the analyst should first review and make adjustments to the owner(s) compensation, if appropriate. Adjustments for the market value of the “replacement cost” of the professional services provided by the owner are particularly important in the valuation of professional medical practices for the purpose of arriving at an ”economic level” of profit.

Data Homogeneity

The selection of financial ratios for analysis and comparison to the organization’s performance requires careful attention to the homogeneity of data. Benchmarking of intra-organizational data (i.e., internal benchmarking) typically proves to be less variable across several different measurement periods.

However, the use of data from external facilities for comparison may introduce variation in measurement methodology and procedure. In the latter case, use of a standard chart of accounts for the organization or recasting the organization’s data to a standard format can effectively facilitate an appropriate comparison of the organization’s operating performance and financial status data to survey results.

Operational benchmarking is used to target non-central work or business processes for improvement. It is conceptually similar to both process and performance benchmarking, but is generally classified by the application of the results, as opposed to what is being compared. Operational benchmarking studies tend to be smaller in scope than other types of benchmarking, but, like many other types of benchmarking, are limited by the degree to which the definitions and performance measures used by comparing entities differ. Common sizing is a technique used to reduce the variations in measures caused by differences (e.g., definition issues) between the organizations or processes being compared.

Common Sizing