BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on July 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The price of gold dropped below $1,800 an ounce and appears hyper-focused on the soaring U.S. Dollar Index, which rose to 107.15. Over the last five days, the index is up by more than two points, and has risen five points over the last 30 days.

Children in the US are getting vaccinated at a lower rate than the rest of the nation, with only 300,000 kids under five receiving the vaccine since it became available two weeks ago. Health officials say this was expected since most parents want to get their kids vaccinated at a doctor’s office.

Finally, lumber markets were a harbinger of economic shifts during the pandemic and today’s slumping prices could be just as prescient. Lumber prices hit a record $1,607 per thousand board feet in May 2021, due to soaring demand for new homes, a boom in DIY home renovation activities, and production and supply chain issues stemming from the pandemic. Twelve months later, lumber prices collapsed to $648, a more than 50% decrease from $1,464 in March.

Posted on July 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Justice Department’s (JD) efforts returned almost $1.9 billion to the federal government or paid it out to private individuals. Of that money, about $1.2 billion went to the Medicare trust fund. About $98.7 million in federal Medicaid money was transferred to CMS. The JD opened 831 criminal healthcare fraud cases last year. Federal prosecutors filed criminal charges in 462 cases involving 741 defendants. A total of 312 defendants were convicted of healthcare fraud during the year. The JD opened 805 civil healthcare fraud investigations and had 1,432 civil healthcare fraud matters pending at the end of last year.

HHS Office of the Inspector General (OIG) investigations resulted in 504 criminal actions against individuals or entities accused of Medicare- and Medicaid-related crimes. The OIG filed 669 civil actions, which included false claims and unjust-enrichment lawsuits filed in federal district courts, and civil monetary penalties. The OIG excluded 1,689 individuals and entities from participating in federal healthcare programs, including Medicare and Medicaid.

Posted on July 2, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

The market is made up of thousands of stocks. And on any given day, investors are actively buying and selling them. This measure looks at the amount, or volume, of shares on the NYSE that are rising compared to the number of shares that are falling.

The formula: Breadth Line Value= (No.of Advance Stocks – No of Decline Stocks) + Breadth Line Value of the Previous day. When the number of advance stocks exceeds the number of the decline stocks then the breadth line will rise and vice versa.

Posted on July 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

Charter Communications (CHTR) is a significantly undervalued stock today. But are competition, 5G, and satellite internet significant threats to its business? How does its management compare to AT&T and Verizon? Read and/or listen to the analysis below.

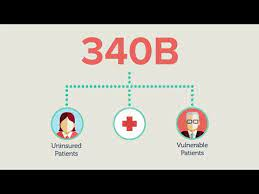

On June 15, 2022, the U.S. Supreme Court released its decision regarding the cuts made by the Department of Health and Human Services (HHS) to the 340B Drug Pricing Program, finding that HHS acted outside its statutory authority in changing reimbursement rates for one group of hospitals without first surveying them on their costs.

The 340B Drug Pricing Program allows hospitals and clinics that treat low-income, medically underserved patients to purchase certain “specified covered outpatient drugs” at discounted prices. (Read more…)

Posted on June 19, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Healthcare Partnerships – 5 Takeaways

• This year had the largest percentage of announced “mega merger” transactions in the last six years at 16.3% and, in more than one out of every 10 transactions, the smaller partner had a credit rating of A- or higher in 2021. • Since 2011, average smaller partner size by annual revenue has increased at a compound annual growth rate (CAGR) of approximately 8.0%. • Transactions involving a not-for-profit partner represented 87% of announced transactions. • Transactions involving rural or urban/rural sellers increased to 31% of announced transactions.

A recent survey from Syft of 100 hospital and supply chain leaders found:

• 65% said better supply chain management could improve margins by 1-3%, with 23% of respondents believing margins can improve by more than 3%. • 94% agreed that supply chain analytics can reduce supply chain costs. 76% said it can improve quality. • 24% said their organizations identify supply standardization opportunities very well. • 32% said it would cost their organizations more than $500,000 annually to meet new supply chain regulations like California Assembly Bill 2357.

Posted on June 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The federal tax deduction that businesses and self-employed taxpayers can use for their work-related miles on the road is suddenly getting more generous. The optional standard mileage rate for business-related driving is increasing to 62.5 cents a mile, starting in July, the Internal Revenue Service announced Thursday. That’s up from the 58.5-cents-a-mile rate first announced in December.

Rising inflation continues to frustrate consumers who are growing tired of shelling out more money. for example, Record gas prices helped push down the consumer sentiment index from 58.4 in May to 50.2 in June – the lowest recorded level since November 1952. The preliminary reading is comparable to the trough reached during the 1980 recession, according to Joanne Hsu, director of the university’s Surveys of Consumers. In May 1980, the sentiment reading hit 51.7, according to historical data. The final reading for June will be published on June 24th.

Markets: The S&P 500 is on the bear market watch list after a vicious sell-off yesterday capping off its worst week since January. Investors were disappointed by the inflation report that dropped Friday. Prices jumped 8.6% last month, which is a faster pace than in April and higher than expected. Rents, food, energy, and used cars all contributed to the price increases, putting even more pressure on the Fed to hike interest rates substantially throughout the summer and into the fall.

Posted on May 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Jules Lipoff, MD: Senior fellow at the Leonard Davis Institute of Health Economics and an assistant professor of clinical dermatology at Perelman School of Medicine, both of the University of Pennsylvania. Erica Mark, medical student at the University of Virginia, contributed to this article.The opinions expressed in this article do not necessarily represent those of the University of Pennsylvania Health System or the Perelman School of Medicine.

***

If you follow the news or your social media feed, you know that crowdsourcing medical expenses is increasingly popular for financing health care costs. In fact, you might have contributed to one; 22 percent of American adults report donating to GoFundMe medical campaigns.

As of 2021, approximately $650 million, or about one-third of all funds raised by GoFundMe, went to medical campaigns. That staggering amount of money highlights how dysfunctional our health care system is, forcing people to resort to crowdsourcing to afford their medical care — but it’s not surprising. In the United States, 62 percent of bankruptcies are related to medical costs. This should be a wake-up call to address and reform the system further.

A recent study examined the growth in hospital prices paid by commercial health insurance companies compared to Medicare over a seven-year period and found that commercial health plan rates were, on average, 180% higher than Medicare rates as of 2019.

While the national ratio between commercial and Medicare hospital payment growth rates remained relatively stable during the seven-year study period, ratios varied widely on a regional basis. This Health Capital Topics article will discuss this recent study and its implications. (Read more…)

Posted on April 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

TRIVIA QUESTION: What date has never been known as Tax Day?

A. March 1st B. March 15th C. April 15th D. May 1st

ANSWER: D—May 1st.

After the 16th Amendment cleared the way for the modern version of the federal income tax, the first filing deadline fell on March 1, 1913. Congress shifted Tax Day to March 15 after passing the Revenue Act of 1918, which introduced a progressive income tax structure to increase revenue during World War I. Since 1954, Tax Day for most Americans has been April 15 (or the next business day if the 15th falls on a weekend or holiday).

The term “step-up” refers to the difference in value and tax liability that an asset has when it is acquired and when it is transferred to an inheritor.

EXAMPLE #2: The proverbial millionaire Doctor Joe, for example, could buy a home for $350,000 and sell it for $1 million, after which he’d pay taxes on the $650,000 gain. But if Dr. Joe passes the home onto his daughter Ella, and she has it appraised at $1 million, its value has taken a “step up” in value to $1 million. If Ella sells the home for $1 million or less, she wouldn’t owe anything in taxes.

ASSESSMENT: For billionaires like Jeff Bezos, Bill Gates and Elon Musk who earn far more through their investments than their salaries, this loophole is a perfect way to shield their wealth. Intergenerational wealth has contributed to surging inequality in America, which grew wider during the pandemic. Since 2019, the wealth of the top 400 richest people in the US increased by $1.4 trillion, per research from Gabriel Zucman and Emmanuel Saez, a pair of left-leaning economists at the University of California, Berkeley.

“Often, for these people, wealth accumulates tax-free their entire lives,” Frank Clemente, executive director at the left-leaning advocacy group Americans for Tax Fairness, opined. President Joe Biden proposed ending this loophole and making billionaires “pay their fair share,” so why does it look like his party won’t touch it?

Posted on April 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

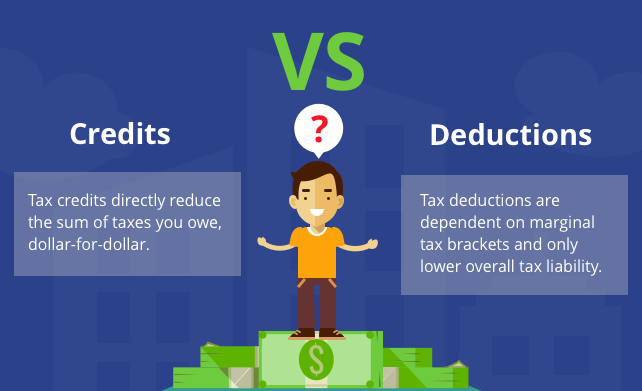

What is a tax deduction?

A deduction reduces the amount of income you pay taxes on, which means you could pay less in taxes. You subtract deductions from your income before calculating how much taxes you owe. How much a deduction saves you depends on your income tax bracket.

To calculate how much a deduction could reduce your taxes, you multiply the amount of the deduction by your marginal tax rate. For example, if a deduction is worth $5,000 and you are in the 10% tax bracket (the lowest), the deduction would reduce your taxes by $500.

A deduction’s value to you is tied to your tax rate. So if you’re paying a higher tax rate, you can reap more of a deduction’s benefit. The lower your tax rate, the less benefit a deduction will have for you. Imagine that you take a $5,000 deduction, but you’re in the 35% tax bracket — the second highest. Now you’re saving $1,750 in taxes.

On the other hand, a credit is a dollar-for-dollar reduction in the amount of tax you owe. For example, if you qualify for a $1,000 tax credit of some kind and owe $5,000 in taxes, that credit will reduce your tax burden to $4,000.

***

But – Do Not Claim Too Many Tax Deductions

Deductions are enticing to taxpayers because they can reduce the amount of your income before you calculate the tax you owe, which in turn might significantly lower how much you have to pay in taxes or increase your refund. But that doesn’t mean you should go wild writing things off on your tax returns, as experts say claiming too many deductions is the most common reason people end up getting audited by the IRS.

Don’t try writing off deductions that are no longer accepted by the IRS. The tax code has changed over the years, and there are some things the tax agency no longer recognizes. You should remember that some of the tax write-offs were terminated by the IRS, including deductions on alimony, moving expenses, and any expenses related to investing, hobbies, and tax preparation.

Posted on April 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

MANAGEMENT STRATEGIES, TOOLS TEMPLATES AND CASE STUDIES

***

Reviews:

Hospitals and Health Care Organizationsis a must-read for any physician and other health care provider to understand the multiple, and increasingly complex, interlocking components of the U.S. health care delivery system, whether they are employed by a hospital system, or manage their own private practices.

The operational principles, methods, and examples in this book provide a framework applicable on both the large organizational and smaller private practice levels and will result in better patient care. Physicians today know they need to better understand business principles and this book by Dr. David E. Marcinko and Professor Hope Rachel Hetico provides an excellent framework and foundation to learn important principles all doctors need to know. ―Richard Berning, MD, Pediatric Cardiology

… Dr. David Edward Marcinko and Professor Hope Rachel Hetico bring their vast health care experience along with additional national experts to provide a health care model-based framework to allow health care professionals to utilize the checklists and templates to evaluate their own systems, recognize where the weak links in the system are, and, by applying the well-illustrated principles, improve the efficiency of the system without sacrificing quality patient care. … The health care delivery system is not an assembly line, but with persistence and time following the guidelines offered in this book, quality patient care can be delivered efficiently and affordably while maintaining the financial viability of institutions and practices. ―James Winston Phillips, MD, MBA, JD, LLM

Posted on March 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

A basic understanding of hospital finance is crucial as leaders continue to create policy that shapes healthcare financing. This updated 30,000-foot view of hospital finance is intended to shed some light on the complex system.

Posted on March 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

New Reporting Warning Issued

By Staff Reporters

***

Virtual currency transactions are taxable by law just like transactions in any other property. Taxpayers transacting in virtual currency may have to report those transactions on their tax returns.

All taxpayers must answer a question about virtual currency on their return.

On March 18th, the IRS issued a new alert warning all taxpayers that they must answer a section about virtual currency on their 2021 tax refund this year, even if they did not deal with any digital transactions. According to the agency, there is a question on the top of all versions of Form 1040 that asks, “At any time during 2021, did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency?”

“All taxpayers filing Form 1040, Form 1040-SR or Form 1040-NR must check one box answering either ‘Yes’ or ‘No’ to the virtual currency question,” the IRS explained. “The question must be answered by all taxpayers, not just taxpayers who engaged in a transaction involving virtual currency in 2021.”

Posted on March 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

BY HEALTH CAPITAL CONSULTANTS, LLC.

DEFINITION: The False Claims Act, also called the “Lincoln Law”, is an American federal law that imposes liability on persons and companies who defraud governmental programs. It is the federal Government’s primary litigation tool in combating fraud against the Government. The law includes a provision that allows people who are not affiliated with the government, called “relators” under the law, to file actions on behalf of the government. Persons filing under the Act stand to receive a portion of any recovered damages.

On February 1, 2022, the U.S. Department of Justice (DOJ) announced their recovery of $5.6 billion in settlements and judgments from civil cases involving fraud and false claims for fiscal year (FY) 2021. Over $5 billion was recouped from the healthcare industry for federal losses alone, and included recoveries from drug and medical device manufacturers, managed care providers, hospitals, pharmacies, hospice organizations, laboratories, and physicians.

***

This figure is more than double the amount of healthcare-related recoveries secured in FY 2020, which totaled $1.8 billion. (Read more…)

Posted on March 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

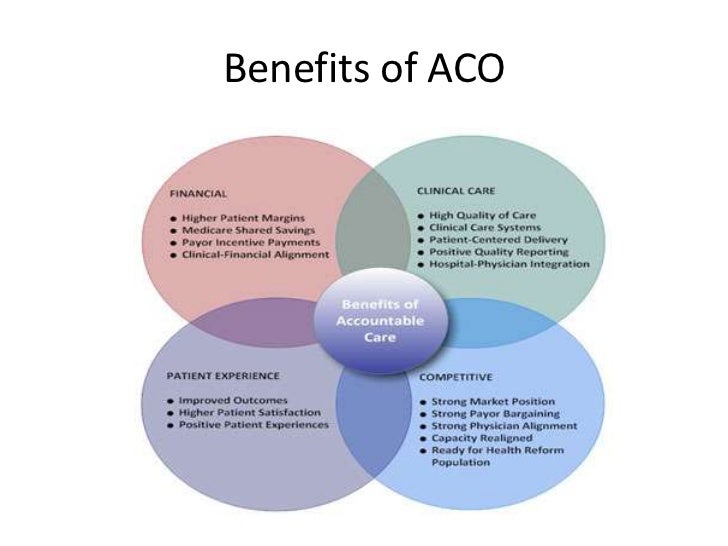

DEFINITION: An accountable care organization (ACO) is a group of doctors, hospitals, and other health care providers that work together on your care. Their goal is to give you — and other people on Medicare — better, more coordinated treatment. The largest effort in payment innovation in Medicare is a portfolio of accountable care organization (ACO) programs that include the Medicare Shared Savings Program (MSSP), the Next Generation model, and Comprehensive End Stage Renal Disease model. But drawbacks include limited choice as some patients will have trouble finding doctors outside of a specific group. The shortage of options could lead to higher patient costs. And, referral restrictions as ACOs provide doctors incentives to refer to specialists within the group.

In a recent survey from AKASA healthcare finance leaders ranked the biggest challenges in recruiting and retention within the revenue cycle as healthcare organizations navigate significant staffing gaps across the board.

Posted on March 20, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Three [3] Key Findings

***

***

• Among patients aged 19-35, mental health conditions were the most common diagnosis associated with emergency ground ambulance in the period 2016-2020. • Throughout the period 2016-2020, advanced-life-support (ALS) accounted for a larger percentage of emergency ground ambulance claim lines than basic-life-support (BLS) services. For example, in 2020, 51.5% of emergency ground ambulance claim lines were associated with ALS compared to 48.5% associated with BLS. • Individuals 65 years and older were consistently the largest age group associated with emergency ground ambulance services, though their share of the distribution decreased from 37.7% in 2016 to 34% in 2020.

Posted on March 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Eric Bricker MD

An accumulator is a running total of money you’ve paid towards your out-of-pocket max for covered services. This includes any copayments, coinsurance, and other health care costs, but not your monthly premium payments.

Posted on March 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

The IRS considers taxpayers married if they are legally married under state law, live together in a state-recognized common-law marriage, or are separated but have no separation maintenance or final divorce decree as of the end of the tax year.

Of the 150.3 million tax returns filed in 2016, the latest year for which the IRS has published statistics, 3.07 million belonged to twosomes who filed separately.

These partners reported individual income and expenses on individual tax returns.

By filing separately, their similar incomes, miscellaneous deductions or medical expenses likely helped them save taxes.

***

Filing separately with similar incomes

A couple may pay the IRS less by filing separately when both physician spouses work and earn about the same amount.

When they compare the tax due amount under both joint and separate filing statuses, they may discover that combining their earnings puts them into a higher tax bracket.

Their savings depends on a variety of other factors, however, including their investment situation and whether they have children.

The “married filing separately” status cuts the deductions for IRA contributions and eliminates certain tax credits, among other tax breaks.

Using miscellaneous deductions by filing separately (for tax years prior to 2018)

Miscellaneous deductions can lower taxable income, but in order to enter them on Schedule A, they must add up to more than 2% of adjusted gross income (AGI).

Physician or other spouses with union dues, job-search costs, tax-preparation fees and un-reimbursed business expenses may find their miscellaneous deductions don’t qualify when their higher combined income raises their AGI.

A spouse who travel frequently for business could rack up a sizable tally in airline fees for baggage and itinerary changes that makes the miscellaneous deduction worth pursuing.

Beginning in 2018, these types of miscellaneous expenses are no longer deductible.

Filing separately to save with unforeseen expenses

Unless out-of-pocket medical expenses exceed 7.5% of AGI for 2021, they don’t qualify as a deduction.

Casualty losses must also total more than 10% of AGI and occur in a federally declared disaster area.

The spouse with the loss or substantial medical outlay calculates deductibility against his or her own lower AGI when the couple files separate returns. When one spouse can lower taxable income this way, married filing separately might trim a couple’s overall tax burden.

Filing separately to guard the future

When you don’t want to be liable for your partner’s tax bill, choosing the married-filing-separately status offers financial protection: the IRS won’t apply your refund to your spouse’s balance due. Separate returns make sense to prevent the IRS from seizing a spouse’s tax refund when the other has fallen behind on child support payments.

Couples in the process of divorcing may shun joint returns to avoid post-divorce complications with the IRS, while a spouse who questions her partner’s tax ethics may feel more comfortable living a separate tax life.

Couples living in community-property states should consider state law when deciding how to file.

Beginning in 2022, there will be few situations in which a patient can receive a bill for out-of-network care they believed would be covered by their insurance company. This new rule should especially benefit patients in emergency situations who don’t have the time or luxury to dig up the details on every provider they encounter.

The No Surprises Act also requires insurance companies to provide patients with at least 90 days of coverage if an in-network provider moves out of network. That way, patients aren’t forced to switch providers immediately if such a move happens while they’re in the middle of a treatment plan.

Now, the No Surprises Act does have its limitations. Patients can still get a bill for out-of-network care if they visit an urgent care clinic for non-emergency purposes. Also, if consumers are informed that the care they’re about to receive is out of network and they give written consent to move forward, then they may get billed for that care even once the new rule takes effect.

QPADEFINITION: The qualifying payment amount is generally the median of contracted rates for a specific service in the same geographic region within the same insurance market as of January 31, 2019. The rate will be adjusted per the Consumer Price Index for All Urban Consumers (CPI-U).

When trying to decide whether to buy a used car or a new one, it’s typically financially wiser to buy used. But if you want to buy new, you should plan to drive the car for 10 years or more.

Better yet – do not buy a new vehicle.

***

The 20/4/10 rule for buying a vehicle

If you have to borrow when buying a car, to avoid spending more than you can afford you should put down at least 20%, keep the loan limited to no more than four years (to avoid interest), and spend no more than 10% of your gross income on transportation costs (which includes the car payment, parking, gas, and insurance).

Posted on March 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

Dr. Eric Bricker Explains How Medicare Can Take Money Back from Hospitals if itWants. If the Hospital Thinks Medicare is Being Unfair, the Appeals Process Takes 3 Years!

Posted on February 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

IRS: The IRS sent out a notice on February 23rd, warning taxpayers about a price hike coming in the next few months. The tax agency said that interest rates will increase for the calendar quarter starting April 1st, 2022. You can accrue interest on two types of payments: over-payment or underpayment. So starting in April, over-payments will have an interest rate of 4 percent, except for corporations which will earn a 3 percent rate and a 1.5 percent rate for the portion of a corporate over-payment that exceeds $10,000. In terms of underpayments, the interest rate will increase to 4 percent overall and 6 percent for large corporate underpayments.

“Under the Internal Revenue Code, the rate of interest is determined on a quarterly basis,” the IRS website explained. The tax agency did not change interest rates in this last quarter, which began Jan. 1, 2022. Before they get changed in April, the rates are currently 3 percent for general over-payments and 2 percent for corporation over-payments, with a 0.5 percent rate for the portion of a corporate over-payment exceeding $10,000. The underpayment interest is 3 percent right now, expect for large corporations which have a 5 percent rate.

***

***

CURRENCY INFLATION: Inflation may occur when the Federal Reserve, or another central bank, adds fiat currency into circulation at a rate that exceeds that of the economy’s growth rate. That creates a situation in which there are more dollars bidding on fewer goods and services. The result is that goods and services cost more. One reason that inflation has been a constant in the US since 1933 is that the FOMC has continually increased the money supply. In response to the 2008 financial crisis, the Fed dropped its lending rate close to zero as a way to inject more liquidity into the economy, which led to increased inflation but not hyperinflation. While those increases have usually moved in step with growth, that hasn’t always been the case.

And so, in response to the COVID-19 pandemic and subsequent lock-downs, the Federal Reserve released the equivalent of $3.8 trillion in new liquidity in 2020. That amount was equal to roughly 20% of the dollars previously in circulation. And it is one reason why many investors were watching the CPI closely in 2021.

EARNING REPORTS:

Monday: India GDP data; Earnings from Lordstown Motors, Groupon, HP, SmileDirectClub and Zoom Video

Tuesday: US and China manufacturing data; Earnings from AutoZone, Baidu, Domino’s Pizza, Hostess Brands, J.M. Smucker, Kohl’s, Target, AMC Entertainment and Salesforce

Wednesday: European inflation data; Earnings from Abercrombie & Fitch, Dine Brands, Dollar Tree, Snowflake and Victoria’s Secret

Thursday: ISM Non-Manufacturing Index; Earnings from Best Buy, Weibo, Costco and Gap

Friday: US jobs report

10-Year: Treasuries rallied to 1.902%.

Oil: The rise in oil prices is spilling over at the gas pump: The average gas price in the US has jumped 10 cents, to $3.64/gallon, in the past two weeks.

Partial SWIFT ban: Western governments put aside their hesitations and proposed banning some Russian lenders from SWIFT, the global messaging service that facilitates cross-border transactions. It’s a move that could cause turmoil across global financial markets.

Devaluation is the deliberate downward adjustment of the value of a country’s money related to another currency, group of currencies or currency standard. It is often confused with depreciation and is the opposite of revaluation which refers to the readjustment of a currency exchange rate.

The government of a country may decide to devalue its currency and like depreciation it is not the result of non-governmental activities.

One reason a country made devalue its currency is to combat a trade imbalance. Devaluation reduces the cost of a country’s export rendering them more competitive in the Global market which is which in turn increases the cost of imports.

If imports are more expensive domestic consumers are less likely to purchase them further strengthening domestic businesses because exports increase and imports decrease there is typically a better balance of payments because the trade deficit shrinks. In short a country that devalue its currency can produce is difficult because there is a greater demand for cheaper exports.

***

***

In accountancy, depreciation refers to two aspects of the same concept: first, the actual decrease of fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wear, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used (depreciation with the matching principle).

Depreciation is thus the decrease in the value of assets and the method used to reallocate, or “write down” the cost of a tangible asset (such as equipment) over its useful life span. Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report.

After an understandable slowdown in 2020, due to the onset of the COVID-19 pandemic, merger & acquisition (M&A) activity in the healthcare industry accelerated in 2021, and the industry is expected to continue the high number of deals and high deal volume in 2022.

***

***

This Health Capital Topics article will review the U.S. healthcare industry’s M&A activity in 2021, and discuss what these trends may mean for 2022. (Read more…)

Posted on February 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

By Staff Reporters

***

An annual study of over 1,500 U.S. consumers, shows:

• 55% of consumers find it stressful paying a healthcare bill. • 53% of consumers find it stressful understanding their plan’s coverage and benefits. • 53% of consumers find it stressful comprehending what they owe. • 59% of consumers find it stressful reconciling a bill issue with their payer.

Posted on February 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

MARKETS: The S&P 500 fell into a correction for the first time in two years, joining the NASDAQ Composite, as Russia sent troops into pro-Russian regions in Ukraine. The S&P 500 index ended down 1% at 4,304.76, below the correction level at 4,316.91, which would represent a 10% drop from its January 3rd record close. A correction is commonly defined by market technicians as a fall of at least 10% (but not greater than 20%) from a recent peak. The last time the S&P 500 entered a correction was February 27th 2020, when the market was being whipsawed by fears about the outbreak of the COVID pandemic.

And, this bearish market isn’t sparing 2021 winners like Home Depot, which fell the most in nearly two years after supply-chain bottlenecks squeezed its margins. HD was the Dow’s biggest gainer last year.

IRS: According to a news release issued by the IRS, taxpayers now have the option to verify their identities during live, virtual interviews with agents. The agency stresses that no bio-metric data will be required for those interviews.

However, taxpayers once again have the option to verify their identity using ID.me’s facial recognition services. Addressing privacy concerns, the IRS says new requirements are in place to ensure that images provided will be deleted upon verification. That would apply to any new IRS accounts created and those where selfies have already been collected.

Posted on February 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Virtual Currency – Real Taxation

By Staff Reporters

What you need to report to the IRS

The IRS treats virtual currencies as property, which means they’re taxed similarly to stocks. If all you did was purchase cryptocurrency with U.S. dollars, and those assets have been sitting untouched in an exchange or your cryptocurrency wallet, you shouldn’t need to worry about reporting to the IRS.

***

Reporting is required when certain events come into play, most commonly:

Trading one cryptocurrency for another.

Selling cryptocurrency for fiat dollars (government-issued currency).

Using cryptocurrency to buy goods or services (e.g., paying for a cup of coffee with cryptocurrency).

A critical distinction to make is that triggering a taxable event doesn’t necessarily mean you’ll owe taxes, said Andrew Gordon, an Illinois-based certified public accountant and tax attorney. Just because you have to report a transaction doesn’t mean you’ll end up owing the IRS for it.

Posted on February 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

IRS Tax Implications

By Staff Reporters

***

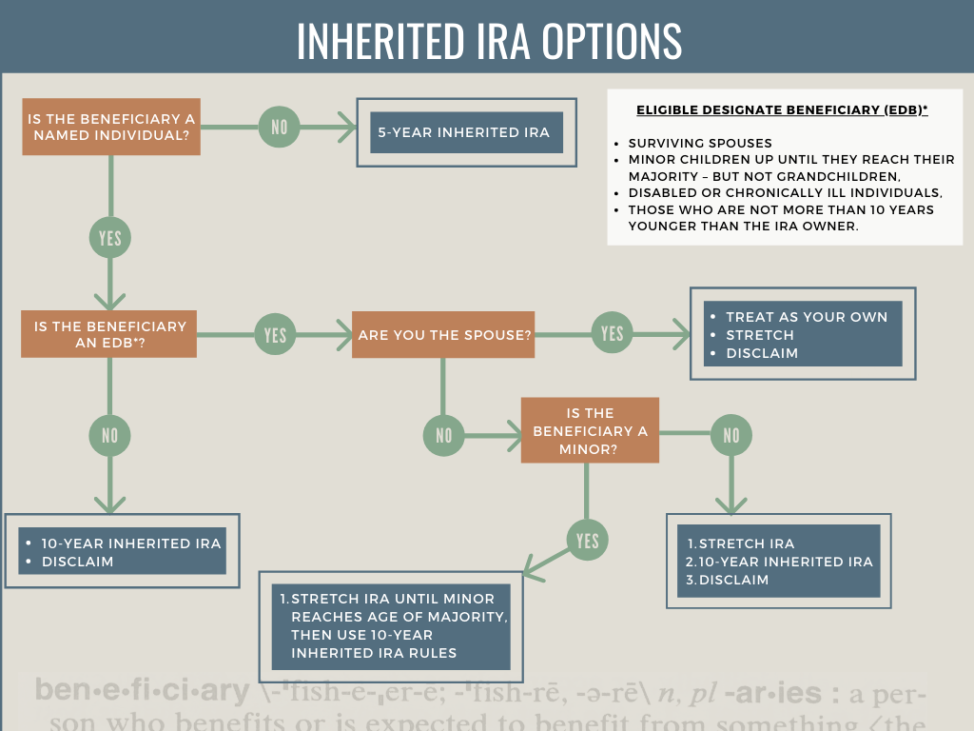

If you inherited a tax-deferred retirement plan, such as a traditional IRA, you’ll have to pay taxes on the money. But you can make the tax hit less onerous.

Spouses can roll the money into their own IRAs and postpone distributions—and taxes—until they’re 70½. All other beneficiaries who want to continue to benefit from tax-deferred growth must roll the money into a separate account known as an inherited IRA. Make sure the IRA is rolled directly into your inherited IRA. If you take a check, you won’t be allowed to deposit the money. Rather, the IRS will treat it as a distribution and you’ll owe taxes on the entire amount.

Once you’ve rolled the money into an inherited IRA, you must take required minimum distributions every year—and pay taxes on the money—based on your age and life expectancy. Deadlines are critical: You must take your first RMD by December 31st. of the year following the death of your parent (or whoever left you the account). Otherwise, you’ll be required to deplete the entire account within five years after the year following your parent’s death.

The December 31st. deadline is also important if you are one of several beneficiaries of an inherited IRA. If you fail to split the IRA among the beneficiaries by that date, your RMDs will be based on the life expectancy of the oldest beneficiary, which may force you to take larger distributions than if the RMDs were based on your age and life expectancy.

You can take out more than the RMD, but setting up an inherited IRA gives you more control over your tax liabilities. You can, for example, take the minimum amount required while you’re working, then increase withdrawals when you’re retired and in a lower tax bracket.

Did you inherit a Roth IRA? And so, as long as the original owner funded the Roth at least five years before he or she died, you don’t have to pay taxes on the money. You can’t, however, let it grow tax-free forever. If you don’t need the money, you can transfer it to an inherited Roth IRA and take RMDs under the same rules governing a traditional inherited IRA. But with a Roth, your RMDs won’t be taxed.

Posted on February 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

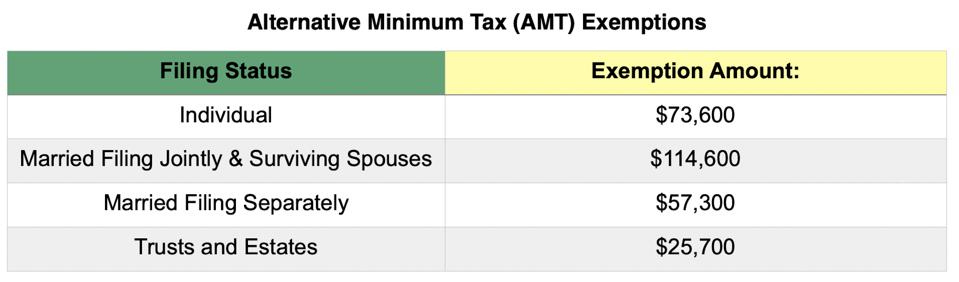

Alternative Minimum Tax

DEFINITION: The alternative minimum tax (AMT) is a tax imposed by the United States federal government in addition to the regular income tax for certain individuals, estates, and trusts. As of tax year 2018, the AMT raises about $5.2 billion, or 0.4% of all federal income tax revenue, affecting 0.1% of taxpayers, mostly in the upper income ranges.

DEFINITION: The Medicare Payment Advisory Commission is an independent, non-partisan legislative branch agency headquartered in Washington, D.C. MedPAC was established by the Balanced Budget Act of 1997.

*** In a January 2022 meeting of MedPAC, commissioners reviewed various recommendations related to the Medicare fee schedule for various health sectors, and unanimously agreed to update Medicare payments to hospitals and keep physician payment rates the same for 2023. This Health Capital Topics article will review the recommendations made by MedPAC for each of the health sectors and their respective payment systems. (Read more…)

Posted on February 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

SYNOPSIS: The home office deductionallows qualified taxpayers to deduct certain home expenses when they file taxes. And, now that some doctors and many of us are working remotely, you may be wondering whether working from home will yield any tax breaks. If your small medical or healthcare consulting or other business qualifies you for a home office tax deduction, should you be concerned about triggering an audit? How does a business qualify in the first place; etc?

Well, to claim the home office deduction on their 2021 tax return, taxpayers generally must exclusively and regularly use part of their home or a separate structure on their property as their primary place of business.

***

If I work from home, do I qualify for a home office tax deduction?

If you’re an employee working remotely rather than an employer or business owner, you unfortunately don’t qualify for the home office tax deduction (however, please note that it is still available to some as a state tax deduction). Prior to the Tax Cuts and Job Acts (TCJA) tax reform passed in 2017, employees could deduct unreimbursed employee business expenses, which included the home office deduction. However, for tax years 2018 through 2025, the itemized deduction for employee business expenses has been eliminated.

If I’m self-employed, should I take the home office tax deduction?

You may have heard that taking the home office deduction sends a red flag to the IRS and ups your chances of being audited. Although there may have been some merit to this advice in the past, changes in the tax rules in the late 1990s made it easier for people who work out of their homes to qualify for these write-offs. So if you qualify, by all means, take it.

Do I qualify for the home office tax deduction?

Generally speaking, to qualify for the home office deduction, you must meet one of these criteria:

Exclusive and regular use: You must use a portion of your house, apartment, condominium, mobile home, boat or similar structure for your business on a regular basis. This also includes structures on your property, such as an unattached studio, barn, greenhouse or garage. It doesn’t include any part of a taxpayer’s property used exclusively as a hotel, motel, inn, or similar business.

Principal place of business: Your home office must be either the principal location of your business or a place where you regularly meet with customers or clients. Some exceptions to this rule include day care and storage facilities.

What is “exclusive use”?

The biggest roadblock to qualifying for these deductions is that you must use a portion of your home exclusively and regularly for your business.

The law is clear and the IRS is serious about the exclusive-use requirement. Say you set aside a room in your home for a full-time business and you work in it ten hours a day, seven days a week. If you let your children use the office to do their homework, you violate the exclusive-use requirement and forfeit the chance for home office deductions.

The exclusive-use rule doesn’t mean:

You’re forbidden to make a personal phone call from the office.

You have to rush outside whenever a family member needs a moment of your time.

Although individual IRS auditors may be more or less strict on this point, some advisers say you meet the spirit of the exclusive-use test as long as personal activities invade the home office no more than they would be permitted to in an office building. The office can also be a section of a room if the division is clear — thanks to a partition, for example — and you can show that personal activities are excluded from the business section.

What is “regular use”?

There’s no specific definition of what constitutes regular use. Clearly, if you use an otherwise empty room only occasionally and its use is incidental to your business, you’d fail this test. If you work in the home office a few hours or so each day, however, you might pass. This test is applied to the facts and circumstances of each case the IRS challenges.

What does “principal place of business” mean?

In addition to passing the exclusive- and regular-use tests, your home office must be either the principal location of that business or a place for regular customer or client meetings.

If your home office is in a separate, unattached structure — a detached garage converted into an office, for example — you don’t have to meet the principal-place-of-business or the deal-with-clients test. As long as you pass the exclusive- and regular-use tests, you can qualify for home business write-offs.

What if your business has just one home office, but you do most of your work elsewhere?

Remember that the requirement is that your home office is your principal place of business, not your principal workplace. As long as you use the home office to conduct your administrative or management chores and you don’t make substantial use of any other fixed location to conduct those tasks, you can pass this test.

If you’re an employee of another company but also have your own part-time business based in your home, you can pass this test even if you spend much more time at the office where you work as an employee.

This rule makes it much easier to claim home office deductions for individuals who conduct most of their income-earning activities somewhere else (such as outside salespeople or tradespeople).

***

***

What qualifies as a business?

As with the regular-use test, whether your endeavors qualify as a business depends on the facts and circumstances. The more substantial the activities, in terms of time and effort invested and income generated, the more likely you are to pass the test.

Making money from your efforts is a prerequisite, but for purposes of this tax break, profit alone isn’t necessarily enough. If you use your den solely to take care of your personal investment portfolio, for example, you can’t claim home office deductions because your activities as an investor don’t qualify as a business.

Taxpayers who use a home office exclusively to manage rental properties may qualify for home office tax status but as property managers rather than investors.

What if I operate a child care or storage facility?

The exclusive-use test doesn’t apply if you use part of your house to:

Provide day care services for children, older adults or individuals with disabilities. If you care for children in your home between 7 a.m. and 6 p.m. each day, for example, you can use that part of the house for personal activities the rest of the time and still claim business deductions. To qualify for the tax break, your home care business must meet any applicable state and local licensing requirements.

Store product samples or inventory you sell in your business. Assume your home-based business is the retail sale of home-cleaning products and that you regularly use half of your basement to store inventory. Occasionally using that part of the basement to store personal items wouldn’t cancel your home office deduction. To qualify for this exception, your home must be the principal location of your business.

How do I calculate the home office tax deduction?

Your home office business deductions are based on either the percentage of your home used for the business or a simplified square footage calculation.

The most exact way to calculate the business percentage of your house is to measure the square footage devoted to your home office as a percentage of the total area of your home. If the office measures 150 square feet, for example, and the total area of the house is 1,200 square feet, your business percentage would be 12.5%.

An easier calculation is acceptable if the rooms in your home are all about the same size. In that case, you can figure out the business percentage by dividing the number of rooms used in your business by the total number of rooms in the house.

Special rules apply if you qualify for home office deductions under the day care exception to the exclusive-use test.

Your business-use percentage must be reduced because the space is available for personal use part of the time.

To do that, you compare the number of hours the child care business is operated, including preparation and cleanup time, to the total number of hours in the year (8,760).

Assume you use 40% of your house for a nursing daycare business that operates 12 hours a day, five days a week for 50 weeks of the year.

12 hours x 5 days x 50 weeks = 3,000 hours per year.

3,000 hours ÷ 8,760 total hours in the year = 0.34 (34%) of available hours.

34% of available hours x 40% of the house used for business = 13.6% business write-off percentage.

Simplified square footage method

Beginning with 2013 tax returns, the IRS began offering a simplified option for claiming the deduction. This new method uses a prescribed rate multiplied by the allowable square footage used in the home.

For 2021, the prescribed rate is $5 per square foot with a maximum of 300 square feet.

If the office measures 150 square feet, for example, then the deduction would be $750 (150 x $5).

The space must still be dedicated to business activities.

With either method, the qualification for the home office deduction is determined each year. Your eligibility may change from one year to the next. Finally, please note that only certain expenses such as rent, mortgage interest and property taxes qualify for the deduction, and the deduction is limited to $10,000.

Posted on February 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

DEFINITION: An accountable care organization is a healthcare organization that ties provider reimbursements to quality metrics and reductions in the cost of care. ACOs in the United States are formed from a group of coordinated health-care practitioners. They use alternative payment models, normally, capitation.

The International Franchise Association (IFA) estimates that that about $1 trillion in sales, or 40% of all retail sales, were made through franchised establishment last year. On the positive side, franchises offer a branded practice concept with management training and access to proprietary methods, marketing and advertising campaigns and a host of support.

Moreover, there are franchises available for virtually every healthcare product or service, including: diet, weight loss and fitness; vein care and laser surgery; vitamins, nutriceuticals and pharmaceuticals; plastic and cosmetic surgery; dermatology, tanning and skin care; home healthcare and extended, etc. Some well know established healthcare and medical franchises are: Doctors Express, Being There Senior Care, Home Care Assistance, Personal Training Institute, Inches-A-Weigh, Remedy Intelligent Staffing, Visiting Angels, Unlimited MedSearch, prnYourHealth and Any Lab Test Now, etc.

On the downside, franchises incur high start-up costs, rules and obligations, payment of franchise percentages and many contractual obligations. Questions to consider when contemplating this business entity include:

Franchise stability, track record, licensing and costs.

Training, support and proximity of other franchises.

Independence, ownership laws, contracts and dispute resolutions,

Screening methods, market size and potential market share.

Replacement cost and transferability?

For more information on Uniform Franchise Offerings Circulars (UFOCs) contact www.FranChoice.com or: