BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The first World Financial Planning Day was held on October 4, 2017. The Financial Planning Standards Board (FPSB) hosts the day. Every year, the FPSB partners with the International Organization of Securities Commissions (IOSCO).

***

Today, it is always held during the first Wednesday of October during IOSCO’s World Investor Week.

***

QUERY: But, what about the entire ecosystem of personal and professional financial planning, investing, risk, business and medical practice management for physicians and healthcare professionals? A vital, unique and complicated niche!

ANSWER: According to the Institute of Medical Business Advisors, Inc., WFP Day is every day for CERTIFIED MEDICAL PLANNER® professional certification holders.

So – If you are in this WFPD industry – Become a fiduciary focused board CERTIFIED MEDICAL PLANNER with extreme healthcare industry ecosystem specificity.

Artificial intelligence is all around us. From self-driving cars to shopping suggestions and everything in between.

In this episode of The Entrepreneur MD, we sit down with Sergei and Daniel from Well-Ai who share with us how their platform uses Artificial Intelligence to augment physicians and improve patient outcomes.

Posted on October 5, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

FORPHYSICIAN INVESTORS

By David Belk MD

Health Insurance Company Financial Index

Below is a listing of the Nine largest for-profit health insurance Companies. The Annual financial statements are linked to the year for each Company and a four page summary report is linked to the name of the health insurance company at the top of the listing.

The relevant pages in each financial statement I used to prepare my summaries are listed next to each year’s statement. Aetna and Coventry’s summaries are combined because they merged in 2012. Health Net also Merged with Centene in 2016 leaving only seven major health insurance companies.

Posted on October 4, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

POST PANDEMIC HEALTH ECONOMICS

BY LAURA GLENN

***

As a leader in a community health system, Laura talks about how the COVID 19 pandemic has affected the economics of healthcare. Laura Glenn joined Munson Healthcare as the Vice President of the Physician Network in December, 2017.

In July, 2019 her role expanded and she was appointed the President of Ambulatory Services and Value Based Care. In this role, she remains responsible for integration of the employed and aligned physician practices across the system. In addition, she is responsible for advancing population health strategies including the Munson Clinical Integration Network and other value based payment models as well as providing leadership to the home health division, MHC’s clinical service lines and clinical business intelligence.

Posted on October 2, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

LESSONS FROM THE RETAIL SECTOR

***

Discover how ProMedica uses customer feedback and a digital-first approach to consumers to achieve stellar results across more than 400 facilities in 28 states.

Posted on October 2, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Bertalan Meskó, MD PhD

***

Two years ago, I was searching in the FDA’s database of artificial intelligence-based medical devices. The database had no such segment. What could I do? Started creating our own.

Together with fellow researchers at The Medical Futurist Institute, we created the first open-access, online database of FDA-approved A.I.-based technologies that got published in the prestigious journal npj Digital Medicine last year. Since then, we have repeatedly called upon the FDA to do its own database (and even offered ours), and finally, this past week the breakthrough happened: the FDA listed our database as a publicly available resource on the subject. I tell you why this step is important below.

Take care, Berci Bertalan Meskó, MD The Medical Futurist

Posted on October 1, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

***

BY MORNING BREW

The Legend of the $1 Trillion Platinum Coin

****

***

You may have heard that a deadline to suspend the debt ceiling is rapidly approaching, and if lawmakers don’t do anything it could lead to “economic catastrophe,” in the words of Treasury Secretary Janet Yellen.

But what if we told you there was a solution to the debt ceiling fiasco so crazy…it just might work?

The solution: Yellen could have the Treasury mint a $1 trillion platinum coin, deposit it at the Fed to “retire” loads of US federal debt, and then enable the government to carry on with business as usual without having to worry about defaulting on its existing debt.

“The Secretary may mint and issue platinum bullion coins and proof platinum coins in accordance with such specifications, designs, varieties, quantities, denominations, and inscriptions as the Secretary, in the Secretary’s discretion, may prescribe from time to time.”

The law is crystal clear, and has been deemed kosher by numerous academics. “The statute clearly does authorize the issuance of trillion-dollar coins,” Laurence Tribe, a Harvard Law professor, told Washington Monthly back in 2013.

In fact, nothing says we have to stop at $1 trillion. Yellen could go big with a $10 trillion coin, hypothetically. As Bloomberg’s Joe Weisenthal explains, none of this would lead to inflation because it’s merely an “accounting trick”—not an influx of money into the economy.

Have we tried this before? The $1 trillion platinum coin idea seems to pop up every time the US faces a debt ceiling crunch. It was first introduced by a Georgia lawyer in 2010 and gained traction during the debt-ceiling crisis of 2011.

Things really turned up in 2013, when the government was…you guessed it, facing another debt ceiling deadline. The hashtag #MintTheCoin became popular on Twitter, and economists like Paul Krugman advocated for unleashing the coin. “If we have a crisis over the debt ceiling, it will be only because the Treasury Department would rather see economic devastation than look silly for a couple of minutes,” he wrote.

But each time the $1 trillion coin is mentioned as a way of resolving debt ceiling problems, the people in charge dismiss it as a distraction from Congress doing its job. “Neither the Treasury nor the Federal Reserve believes that the law can or should be used to produce platinum coins for the purpose of avoiding an increase in the debt limit,” The Treasury wrote during…well, yes, another debt ceiling emergency in 2015.

As for our current predicament, the Biden administration rejected the minting of the $1 trillion coin yet again last week.

Bottom line: Perhaps some enterprising future Treasury Secretary will manifest the platinum coin into existence, but for now it remains as mythical as Camelot.

Posted on September 30, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Senate passes last-minute deal to avert government shutdown

The Senate on Thursday afternoon just passed a deal party leaders reached late Wednesday to avert a government shutdown that would have affected hundreds of thousands of federal workers and slammed an economy still struggling to recover from the pandemic, all with just hours left to stave off a crisis.

How much will it cost you to start a dental practice – with Business Plan?

There are many costs to consider to set up a successful dental practice. Note that the following values are not the exact amount but an average of setting up a dental practice:

Purchase price – this includes valuation fees of between $1,000-4,500, solicitor fees of between $4,000 – 17,000, accountancy and bank fees of around $3,000, and bank solicitors, which can be up to $3,500. Many of these can be reduced or obliterated.

Materials – $40,000

Lab fees – $36,000

Staff costs – $82,000

Other costs (associates fees) – [$245,000 – $295,000]

Other Factors

“Big” Tech – Many startup doctors want to include CBCT or CAD/CAM or 3D printing in their startup, any of which can add $25,000-$175,000. In other situations, waiting is the best option.

Cabinetry Preferences – Costs for cabinetry can range from $5,000 to $175,000.

Practice Management Software (PMS) – Pricing will range from a few thousand dollars to $25,000; OR none at all.

Mechanical Delivery – Typically referred to as chairs, lights, and units, this category of dental equipment costs will range between $5,000 and $100,000 based on your startup plans.

Vision – Ignore the so-called “experts” who will try to create a cookie-cutter model for your equipment costs. That is the thinking of corporate dentistry. You want a customized private practice vision that allows you to create a model matching your standards. Prioritize your vision, so your values and philosophy will lead your dental equipment budget and purchasing decisions. Your equipment budget will be—and should be—customized.

It has been well documented that the COVID-19 pandemic resulted in unprecedented increases in telemedicine utilization across the U.S. However, rural providers and patients, as evidenced by their lower rates of telemedicine usage during this time, have not been able to take advantage of the opportunities provided by telemedicine to the same extent as urban providers.

On August 18, 2021, the Health Resources and Services Administration (HRSA) of the Department of Health and Human Services (HHS) announced the latest attempt to ameliorate this issue – the distribution of nearly $20 million to 36 recipients for the purpose of strengthening telehealth services in rural and underserved communities and expanding innovation and quality. (Read more…)

Posted on September 28, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

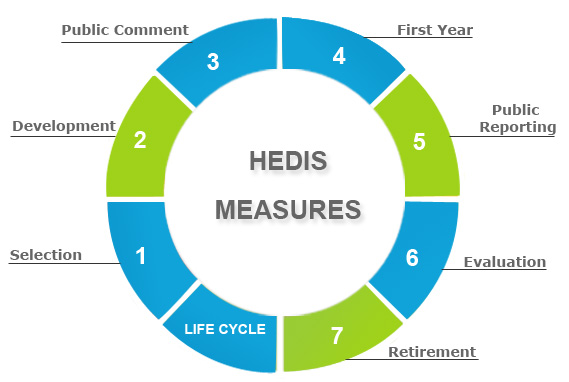

90 NCQI MEASUREMENTS

BY ERIC BRICKER MD

The Healthcare Effectiveness Data and Information Set (HEDIS) is a tool used by more than 90 percent of U.S. health plans to measure performance on important dimensions of care and service. More than 190 million people are enrolled in health plans that report quality results using HEDIS.

The National Committee for Quality Assurance is an independent 501 nonprofit organization in the United States that works to improve health care quality through the administration of evidence-based standards, measures, programs, and accreditation.

Posted on September 26, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

***

REPORTEDLY FUNDING ANTI-AGEING VENTURES TO CHEAT DEATH

“Not Today – Death”

***

By Alma Fabiani

***

Jeff Bezos is allegedly investing in Altos Labs, a biological reprogramming tech company currently looking into a variety of methods that could help reverse the ageing process,

Bezos is said to have a fairly long-standing interest in longevity research. But although Altos Labs has so far managed to recruit some impressive names in the biological reprogramming sector, as well as some pretty big investors, its research still needs a lot of work before it can ever be applied to humans.

Posted on September 26, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BY ENTREPRENUER MD AND ROBERT PEARL MD

In this episode the Entrepreneur MD is joined by Dr Robert Pearl, MD, to talk about his latest book Uncaring and the need to stand up against the current healthcare model.

Posted on September 24, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

HEALTHCARE ECONOMIST

By Eric Bricker MD

Uwe Reinhardt PhD was a Princeton Healthcare Economist Who Passed Away in 2017. He Was Possibly the Most Well Known Healthcare Economist in America and Even the World.

A decentralized autonomous organization (DAO), sometimes called a decentralized autonomous corporation (DAC), is an organization represented by rules encoded as a computer program that is transparent, controlled by the organization members and not influenced by a central government. A DAO’s financial transaction record and program rules are maintained on a blockchain. The precise legal status of this type of business organization is unclear.

A well-known example, intended for venture capital funding, was The DAO, which launched with $150 million in crowdfunding in June 2016, and was nearly immediately hacked and drained of US$50 million in cryptocurrency. The hack was reversed in the following weeks, and the money restored, via a hard fork of the Ethereum blockchain: the Ethereum miners and clients switched to the new fork.

A Ponzi scheme (/ˈpɒnzi/, Italian: [ˈpontsi]) is a form of fraud that lures investors and pays profits to earlier investors with funds from more recent investors. Recall Bernie Madoff.

The scheme leads victims to believe that profits are coming from legitimate business activity (e.g., product sales or successful investments), and they remain unaware that other investors are the source of funds. A Ponzi scheme can maintain the illusion of a sustainable business as long as new investors contribute new funds, and as long as most of the investors do not demand full repayment and still believe in the non-existent assets they are purported to own.

A pyramid scheme is a business model that recruits members via a promise of payments or services for enrolling others into the scheme, rather than supplying investments or sale of products. As recruiting multiplies, recruiting becomes quickly impossible, and most members are unable to profit; as such, pyramid schemes are unsustainable and often illegal.

A cap on how much the US government can borrow to finance its operations.

It was introduced during World War I so that Congress wouldn’t have to approve every bond issuance by the Treasury Department as it had done previously—freeing up more time for name-calling.

The debt ceiling has been suspended dozens of times over the years, including 3x during the Trump administration.

Without suspending the debt ceiling, the US wouldn’t be able to borrow money to pay its bills—and things would get ugly if that happened. The federal government would have to slash spending for programs like Medicaid, local governments would find it harder to borrow, and financial markets could go haywire.

In short, a failure to act would “produce widespread economic catastrophe,” Treasury Secretary Janet Yellen wrote in the Wall Street Journal.

Important note: The debt ceiling doesn’t account for new spending, like the $3.5 trillion proposal the Democrats have on the table. Instead, it’s about spending Congress has already authorized, such as paying out Social Security. Over the years, the debt ceiling has become a “political weapon,” according to the AP, as each party tries to blame the other for their spending habits and for heaping more debt on the US.

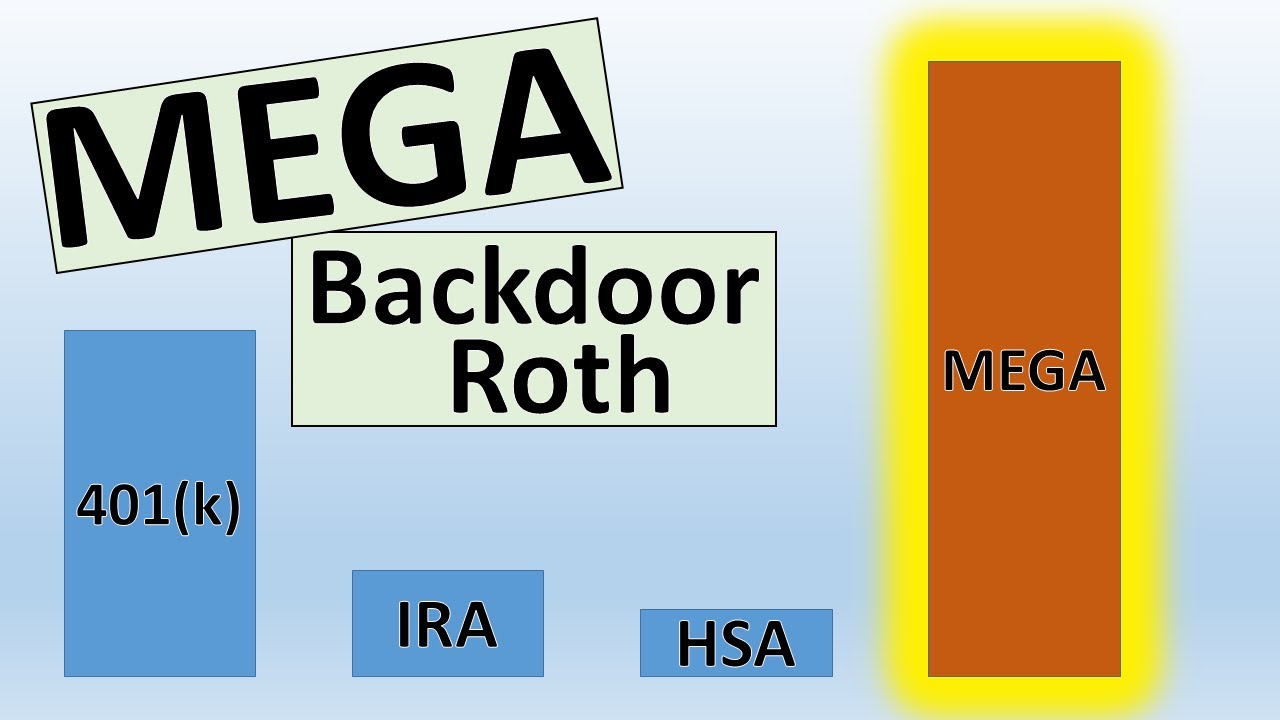

If you’re a physician looking to get ahead on planning for retirement, you’re likely familiar with individual retirement accounts, or IRAs. An IRA is a tax-advantaged vehicle that helps you grow your retirement savings. Roth IRAs are particularly attractive, because you don’t pay taxes on withdrawals in retirement.

There’s one problem: you can’t contribute to a Roth IRA directly if you make above a certain income. A backdoor IRA, though, can solve your problem by allowing you to convert a traditional IRA into a Roth.

Here’s how it works:

First, place your contribution in a traditional IRA—which has no income limits.

Then, move the money into a Roth IRA using a Roth conversion.

But make sure you understand the tax consequences before using this strategy.

The mega backdoor Roth allows you to put up to $38,500 in a Roth IRA or Roth 401(k) in 2021, on top of the regular contribution limits for those accounts. If you have a Roth 401(k) at work (and the plan allows for the mega option as described below), generally you can choose whether the final destination of your mega contributions is the Roth 401(k) or a Roth IRA. If your employer offers only a traditional 401(k), then your mega contributions would end up in a Roth IRA.

Here’s a quick summary of what you need to have in place for the ideal mega backdoor Roth strategy:

A 401(k) plan that allows “after-tax contributions.” After-tax contributions are a separate bucket of money from your traditional and Roth 401(k) contributions. About 43% of 401(k) plans allow after-tax contributions, according to a 2017 survey of large and midsize employers by consulting firm Willis Towers Watson.

Your employer offers either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan. If you’re not sure, ask your human resources department or plan administrator.

You’ve got money left over to save, even after maxing out your regular 401(k) and Roth IRA contributions.

Posted on September 19, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

AT YOUR SERVICE

Dr. David Edward Marcinko is Speaking Up

Dr. David Edward Marcinko MBA CMP® enjoys personal coaching and public speaking and gives as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These have included lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

His talks and podcasts tend to be engaging, iconoclastic, and humorous. His most popular presentations include a diverse variety of topics and typically include those in all iMBA, Inc’s textbooks, handbooks, white-papers and most topics covered on this blog.

Posted on September 19, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Learn WHY Hospital Prices Are Kept SECRET

***

BY ERIC BRICKER MD

The New York Times Posted an Article Explaining Hospital Prices for Patients on Private Insurance Plans Such as Blue Cross, United Healthcare, Cigna and Aetna.

Do your children have income-generating assets in a custodial account?

If so, be sure you understand the so-called kiddie tax.

This law was passed to discourage wealthier individuals from transferring assets to their children to take advantage of their lower tax rates. The kiddie tax has seen many iterations but current rules tax a minor child’s unearned income—including capital gains distributions, dividends, and interest income—at the parents’ tax rate if it exceeds the annual limit ($2,200 in 2021).

The tax applies to dependent children under the age of 18 at the end of the tax year (or full-time students younger than 24) and works like this:

The first $1,100 of unearned income is covered by the kiddie tax’s standard deduction, so it isn’t taxed.

The next $1,100 is taxed at the child’s marginal tax rate.

Anything above $2,200 is taxed at the parents’ marginal tax rate.

So – If your child also has earned income, say from a summer job or legitimate work in your medical office or practice, the rules become more complicated.

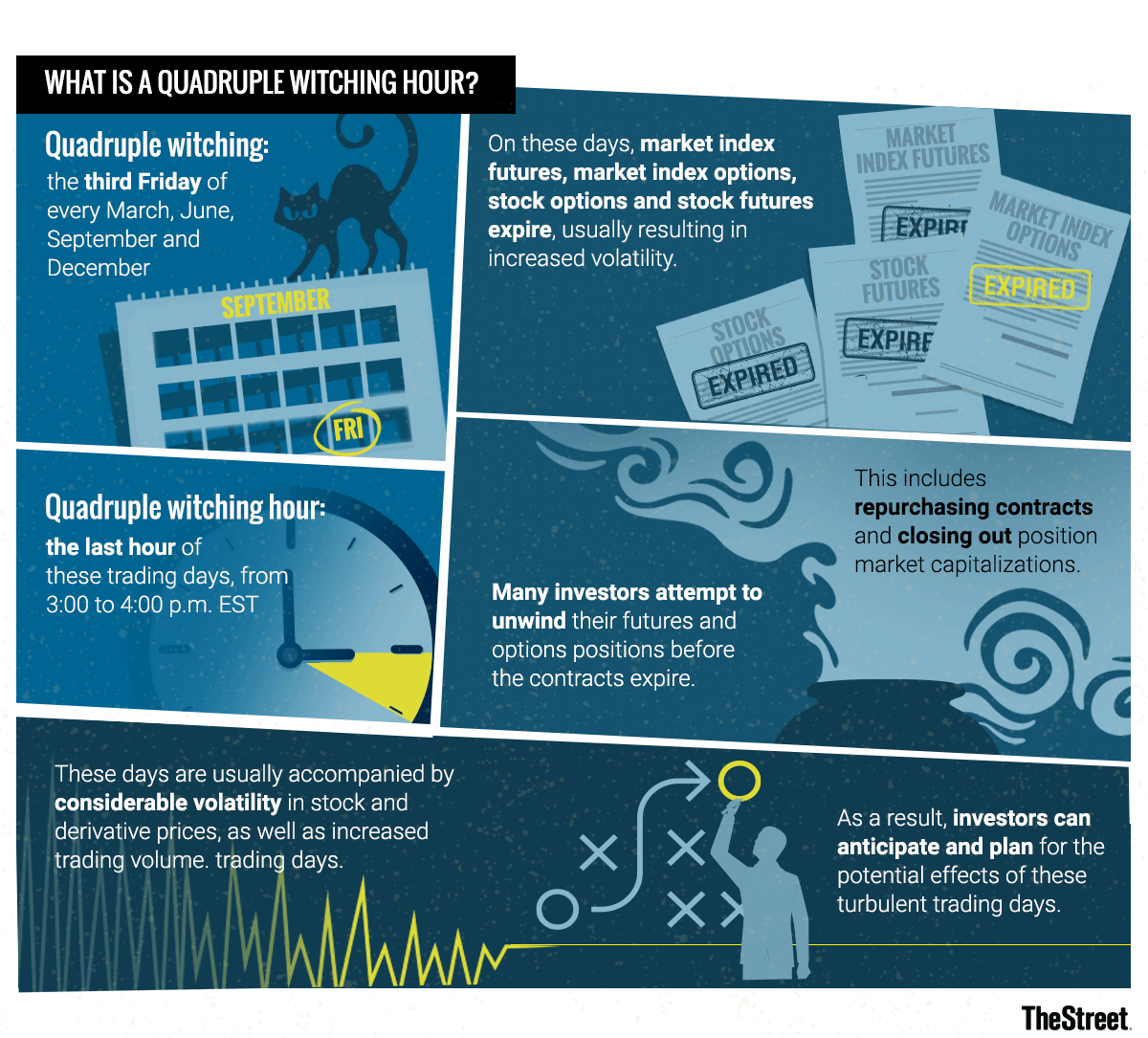

Markets: While yesterday was somewhat of a snoozefest on Wall Street, today should be more interesting. In a quarterly event known as “quadruple witching,” stock options, index options, stock futures, and index futures all expire on the same day, which can produce fireworks.

The phrase quadruple witching brings to mind stories that begin, “It was a dark and stormy night…” or folkloric visions of witches flying chaotically on broomsticks across the brightness of a moon.

In the context of investing, quadruple witching also refers to possible chaos but chaos in the financial markets. Such chaos can erupt due to four different types of contracts on financial assets expiring on the same day. The quadruple witching hour is the last hour of the trading session on that day. The question is whether investors can make abnormally robust profits on quadruple witching days due to market fluctuations.

What Is Quadruple Witching?

Quadruple witching refers to four days during the calendar year when the contracts on four different kinds of financial assets expire. The days are the third Friday of March, June, September and December. The assets on which the contracts expire on that day are stock options, single stock futures, stock index futures and stock index options. Options contracts also expire monthly. Futures contracts expire quarterly.

Because all four types of contracts expire on the same day, the quadruple witching day usually sees a heavier volume of trading. This is why the reference to chaos is made about this witching day. Market volume is increased partly due to offsetting trades that are made automatically. Volume on quadruple witching days has increased roughly two-thirds of the time since 2005.

Recent Quadruple Witching Expiration Day

On June 18, 2021, a quadruple witching day, a near-record volume of single-stock equity options was set to expire at the end of the day in the amount of $818 billion. As a result, a near-record of single stock open interest of about $3 trillion stood on June 18, 2021. Open interest refers to how many contracts are open during any given point during the day. It is an important metric for traders to watch since a large amount of open interest can move the value of the underlying stock.

Taking a distribution from a tax qualified retirement plan, such as a 401(k), prior to age 59 1/2 is generally subject to a 10 percent early withdrawal tax penalty.

However, the IRS rule of 55 may allow you to receive a distribution after attaining age 55 (and before age 59 1/2 ) without triggering the early penalty if your plan provides for such distributions.

The distribution would still be subject to an income tax withholding rate of 20 percent, however. (If it turns out that 20 percent is more than you owe based on your total taxable income, you will get a refund after filing your yearly tax return.)

Posted on September 16, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ByBertalan Meskó, MDPhD

Elizabeth Holmes has no idea how much damage she has done with Theranos. As I often wrote, for digital technologies to gain ground and become part of our everyday lives, we need not only technological solutions but a cultural paradigm shift. Holmes rolled a massive rock in front of it.

Similarly, Facebook’s data privacy practices do not increase people’s confidence in the company’s products. All the scandals that have surrounded the social network could backfire when Facebook wants to step into healthcare – and this is exactly what we wrote about in our latest article, Is There A Place For Facebook In Healthcare? In it, we looked at what Facebook currently does in medicine and evaluated whether those are viable ways to follow in the future.

Take care, Berci Bertalan Meskó, MDPhD The Medical Futurist

Posted on September 15, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

CULTURE IN HEALTHCARE

Culture is a factor to consider with healthcare. Depending on the culture they may seek alternative treatment such as homeopathic and treatment they have been raised with in their country Some cultures will get medications from their country because they believe in their medical system more then what is offered.

BY IHME

***

Dr. Joseph L. Dieleman, Associate Professor in the Department of Health Metric Sciences at the University of Washington, is the lead author of the study “US Health Care Spending by Race and Ethnicity, 2002-2016,” published August 17, 2021 in the Journal of the American Medical Association

Posted on September 15, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

CONFLICTS OF INTEREST?

The New York Times Had an Excellent Article on the FDA on September 2, 2021.

The Article Described How the FDA Began Receiving Funding from the Pharmaceutical Industry Itself to Pay for FDA Employee Salaries in 1992–a Potential Conflict-of-Interest. Subsequently, a Study Found that 1/3 of Drugs Approved by the FDA Were Found to Have Safety Problems from 2000 -2010. Another Potential Conflict-of-Interest is Number of FDA Regulators Who Leave Their Positions to Take High-Paying Jobs at Pharmaceutical Companies.

Posted on September 14, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BY NIHCM

INFO-GRAPHIC

Gum disease remains one of the most prevalent chronic diseases in the United States with 46% of adults over 30 showing symptoms. Although significant improvements have been made to improve oral health in America, many people still experience barriers to preventive or essential dental care.

Black Americans, Latinos, and Native Americans, as well as low-income populations, children and pregnant women are at greater risk of oral health diseases. The disparities experienced by these populations have only been exacerbated by the pandemic.

***

***

In this infographic highlights the challenges to achieving optimal oral health and identifies opportunities for advancing health equity moving forward.

There’s an aspect to retirement that many physicians do not plan for … the transition from work and practice to retirement. Your work has been an important part of your life. That’s why the emotional adjustments of retirement may be some of the most difficult ones.

For example, what would you like to do in retirement? Your retirement vision will be unique to you. You are retiring to something not from something that you envisioned. When you have more time, you would like to do more traveling, play golf or visit more often, family and friends. Would you relocate closer to your kids? Learn a new art or take a new class? Fund your grandchildren’s education? Do you have philanthropic goals? Perhaps you would like to help your church, school or favorite charity? If your net worth is above certain limits, it would be wise to take a serious look at these goals. With proper planning, there might be some tax benefits too. Then you have to figure how much each goal is going to cost you.

If have a list of retirement goals, you need to prioritize which goal is most important. You can rate them on a scale of 1 to 10; 10 being the most important. Then, you can differentiate between wants and needs. Needs are things that are absolutely necessary for you to retire; while wants are things that still allow retirement but would just be nice to have.

Recent studies indicate there are three phases in retirement, each with a different spending pattern [Richard Greenberg CFP®, Gardena CA, personal communication]. The three phases are:

The Early Retirement Years. There is a pent-up demand to take advantage of all the free time retirement affords. You can travel to exotic places, buy an RV and explore forty-nine states, go on month-long sailing vacations. It’s possible during these years that after-tax expenses increase during these initial years, especially if the mortgage hasn’t been paid off yet. Usually the early years last about ten years until most retirees are in their 70’s.

Middle Years. People decide to slow down on the exploration. This is when people start simplifying their life. They may sell their house and downsize to a condo or townhouse. They may relocate to an area they discovered during their travels, or to an area close to family and friends, to an area with a warm climate or to an area with low or no state taxes. People also do their most important estate planning during these years. They are concerned about leaving a legacy, taking care of their children and grandchildren and fulfilling charitable intent. This a time when people spend more time in the local area. They may start taking extension or college classes. They spend more time volunteering at various non-profits and helping out older and less healthy retirees. People often spend less during these years. This period starts when a retiree is in his or her mid to late 70’s and can last up to 20 years, usually to mid to late-80’s.

Late Years. This is when you may need assistance in our daily activities. You may receive care at home, in a nursing home or an assisted care facility. Most of the care options are very expensive. It’s possible that these years might be more expensive than your pre-retirement expenses. This is especially true if both spouses need some sort of assisted care. This period usually starts when the retiree is their 80’s; however they can sometimes start in the mid to late 70’s.

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement.

Planning Issues – Mid Career

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement

Planning Issues – Late Career

Three to five years before you retire, start making the transition from work to retirement.

Try out different hobbies;

Find activities that will give you a purpose in retirement;

Establish friendships outside of the office or hospital;

Discuss retirement plans with your spouse.

If you plan to relocate to a new place, it is important to rent a place in that area and stay for few months and see if you like it. Making a drastic change like relocating and then finding you don’t like the new town or state might be very costly mistake. The key is to gradually make the transition.

An IRA in which distributions continue after the primary beneficiary’s death.

For an IRA to be inherited, the primary beneficiary must have already been receiving the required minimum distribution; the distributions either continue or are re-calculated based upon the secondary beneficiary’s life expectancy.

If the secondary beneficiary is the widow(er) of the primary beneficiary, she/he may roll over the inherited IRA into her/his own IRA without penalty.

![DR. DAVID EDWARD MARCINKO FACFAS MBA CFP MBBS [Hon] [Executive Summary] - PDF Free Download](https://educationdocbox.com/docs-images/75/71938560/images/8-1.jpg)

/u-s-debt-ceiling-why-it-matters-past-crises-9ee4f4a3337c4203997fb191a9858b8c.gif)

:strip_icc():format(webp)/what-is-the-rule-of-55-2894280-v1-fa6b42c5a8f647e8aa5776a550c121a5-1fc39bd85b914af9b2682601f2cefdf6.png)