BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on January 7, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

FINANCIAL DEFINITIONS

By Dr. David Edward Marcinko MBA MEd

***

***

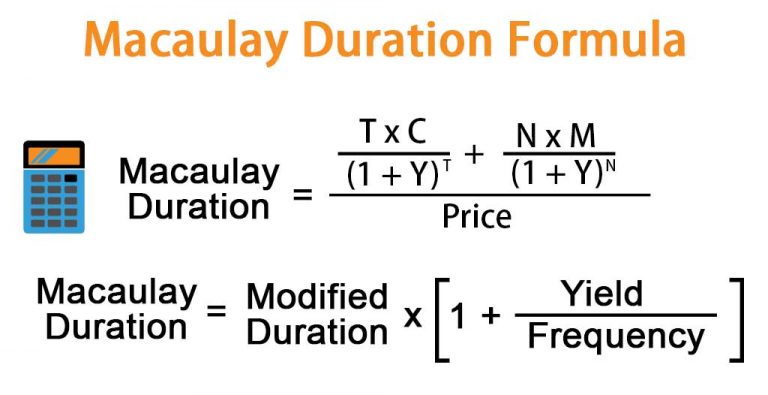

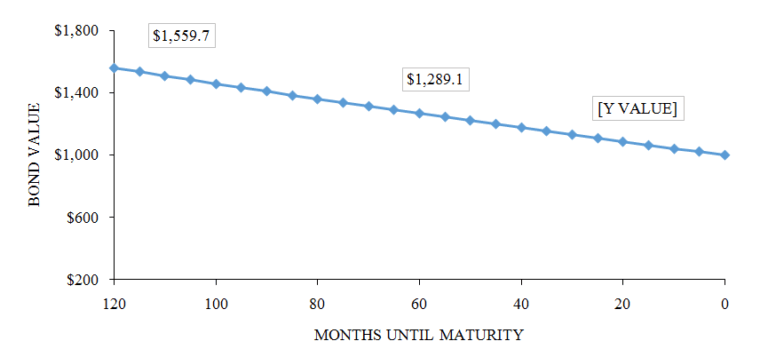

Macaulay duration is a foundational concept in fixed-income investing that measures the weighted average time until a bondholder receives the bond’s cash flows. It is essential for understanding interest rate risk and managing bond portfolios.

Named after economist Frederick Macaulay, Macaulay duration represents the average time in years that an investor must hold a bond to recover its present value through coupon and principal payments. Unlike simple maturity, which only reflects the final payment date, Macaulay duration accounts for the timing and magnitude of all cash flows, weighted by their present value. This makes it a more precise tool for evaluating a bond’s sensitivity to interest rate changes.

To calculate Macaulay duration, each cash flow is discounted to its present value using the bond’s yield to maturity. These present values are then weighted by the time at which each payment occurs. The formula is:

Where CFtCF_t is the cash flow at time tt, yy is the yield to maturity, and PP is the bond’s price. The result is expressed in years.

Why does this matter? Macaulay duration is crucial for investors who want to match the timing of their liabilities with their assets—a strategy known as immunization. By aligning the duration of a bond portfolio with the time horizon of future liabilities, investors can minimize the impact of interest rate fluctuations. For example, pension funds often use duration matching to ensure they can meet future payouts regardless of rate changes.

Duration also helps investors compare bonds with different maturities and coupon structures. Generally, bonds with longer maturities and lower coupons have higher durations, meaning they are more sensitive to interest rate changes. Conversely, short-term or high-coupon bonds have lower durations and are less affected by rate shifts.

While Macaulay duration is a powerful tool, it has limitations. It assumes a flat yield curve and constant interest rates, which rarely hold true in dynamic markets. For more precise risk management, investors often use modified duration, which adjusts Macaulay duration to estimate the percentage change in a bond’s price for a 1% change in interest rates.

In practice, Macaulay duration is most useful for long-term planning and strategic asset allocation. It provides a clear measure of time-weighted cash flow exposure and helps investors build portfolios that are resilient to interest rate volatility.

Whether used for individual bond selection or broader portfolio construction, understanding Macaulay duration equips investors with a deeper grasp of fixed-income dynamics.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

The Firm Foundation Theory of investing is one of the most influential approaches to stock valuation. It rests on the belief that every financial asset possesses an intrinsic value that can be objectively determined through careful analysis of its fundamentals. This theory contrasts sharply with more speculative approaches, such as the “Castle-in-the-Air” theory, which emphasizes crowd psychology and market sentiment.

At its core, the Firm Foundation Theory was popularized by economist John Burr Williams in his 1938 book The Theory of Investment Value. Williams argued that the intrinsic value of a stock is equal to the present value of all future dividends the company is expected to pay. In other words, the worth of a stock is not determined by short-term price movements or investor enthusiasm, but by the long-term cash flows it generates. This principle has become a cornerstone of fundamental analysis, influencing investors such as Warren Buffett, who is often cited as a practitioner of this approach.

The theory assumes that while market prices may fluctuate due to speculation, fear, or irrational exuberance, they will eventually regress toward intrinsic value. This creates opportunities for disciplined investors: when a stock trades below its intrinsic value, it represents a buying opportunity; when it trades above, it may be time to sell. Thus, the Firm Foundation Theory provides a rational framework for identifying mispriced securities and making long-term investment decisions.

***

***

One of the strengths of this theory is its emphasis on objective analysis. By focusing on dividends, earnings, and growth potential, it encourages investors to ground their decisions in measurable financial data rather than emotional impulses. This approach aligns with the broader philosophy of value investing, which seeks to purchase securities at a discount to their true worth. It also offers a counterbalance to speculative bubbles, reminding investors that prices untethered from fundamentals are unsustainable in the long run.

However, the Firm Foundation Theory is not without challenges. Forecasting future dividends and earnings is inherently uncertain. Companies may change their payout policies, face unexpected competition, or encounter macroeconomic shocks that alter their growth trajectory. Additionally, the theory assumes that markets will eventually correct mispricings, but in reality, irrational exuberance or pessimism can persist for extended periods. Critics argue that this makes the theory more idealistic than practical in certain contexts.

Despite these limitations, the Firm Foundation Theory remains a vital tool in the investor’s toolkit. It underpins many valuation models used today, including discounted cash flow (DCF) analysis, which extends Williams’s dividend-based approach to include broader measures of cash generation. By insisting that stocks have a calculable intrinsic value, the theory provides a disciplined lens through which investors can evaluate opportunities and avoid being swayed by market noise.

In conclusion, the Firm Foundation Theory offers a rational, fundamentals-driven perspective on investing. While it requires careful forecasting and is vulnerable to uncertainty, its emphasis on intrinsic value continues to guide prudent investors. By reminding us that stocks are ultimately worth the cash they return to shareholders, the theory stands as a bulwark against speculation and a foundation for long-term wealth building.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

Money supply measures—M0, M1, M2, and M3—are essential tools used by economists and policymakers to assess liquidity, guide monetary policy, and understand economic health. Each measure reflects a different level of liquidity and plays a unique role in financial analysis.

The money supply refers to the total amount of monetary assets available in an economy at a specific time. It includes various forms of money, ranging from physical currency to more liquid financial instruments. To better understand and manage economic activity, central banks and economists categorize money into different measures based on liquidity: M0, M1, M2, and M3.

M0, also known as the monetary base or base money, includes all physical currency in circulation—coins and paper money—plus reserves held by commercial banks at the central bank. It represents the most liquid form of money and is directly controlled by the central bank through tools like open market operations and reserve requirements.

M1 builds on M0 by adding demand deposits (checking accounts) and other liquid deposits that can be quickly converted into cash. It includes:

Physical currency held by the public

Traveler’s checks

Demand deposits at commercial banks

M1 is a key indicator of immediate spending power in the economy. A rapid increase in M1 can signal rising consumer activity, while a decline may indicate tightening liquidity.

M2 expands further by including near-money assets—those that are not as liquid as M1 but can be converted into cash relatively easily. M2 includes:

All components of M1

Savings deposits

Money market securities

Certificates of deposit (under $100,000)

M2 is widely used by economists and the Federal Reserve to gauge intermediate-term economic trends. It reflects both spending and saving behavior, making it a critical tool for forecasting inflation and guiding interest rate decisions.

M3, though no longer published by the Federal Reserve since 2006, includes M2 plus large time deposits, institutional money market funds, and other larger liquid assets. M3 provides a broader view of the money supply, especially useful for analyzing long-term investment trends and credit expansion. Some countries, like the UK and India, still track M3 for macroeconomic planning.

These measures are not just academic—they have real-world implications. For instance, during the COVID-19 pandemic, the U.S. saw a historic surge in M2 due to stimulus payments and quantitative easing. This expansion raised concerns about future inflation, which materialized in subsequent years. Monitoring money supply helps central banks adjust monetary policy to maintain price stability and support economic growth.

In conclusion, money supply measures offer a layered view of liquidity in the economy, from the most liquid (M0) to broader aggregates (M3).

Understanding these categories helps policymakers, investors, and businesses anticipate economic shifts, manage inflation, and make informed financial decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Bonds: The 10-year Treasury yield popped on solid economic data yesterday, including weekly jobless claims falling to their lowest since mid-July and Q2 GDP rising unexpectedly.

Stocks: But good news for the labor market and economy is bad news for anyone hoping the Federal Reserve cuts interest rates next month, and the major indexes sank for a third day in a row yesterday. All eyes now turn to today’s key PCE reading.

Crypto: Digital assets continued to tumble yesterday with ether falling below $4,000 for the first time in months. There may be more pain ahead: $22 billion in crypto options expire today.

Posted on September 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: The NASDAQ rose to its fifth record high of the week, while the S&P 500 and the Dow sank late in the day as investors turned their attention to the FOMC meeting next week.

Bonds: While equities climbed all week long, the bond market has been sending signals that weak economic data really isn’t great news.

Commodities: Oil rallied after President Trump expressed his growing frustration with Vladimir Putin and threatened further energy and financial sanctions. Meanwhile, the US may ask its G7 counterparts to apply 100% tariffs against China and India for purchasing Russian crude.

Here are some of the most common risks associated with fixed income securities.

Interest Rate Risk

The market value of the securities will be inversely affected by movements in interest rates. When rates rise, market prices of existing debt securities fall as these securities become less attractive to investors when compared to higher coupon new issues. As prices decline, bonds become cheaper so the overall return, when taking into account the discount, can compete with newly issued bonds at higher yields. When interest rates fall, market prices on existing fixed income securities tend to rise because these bonds become more attractive when compared to the newly issued bonds priced at lower rates.

Price Risk

Investors who need access to their principal prior to maturity have to rely on the secondary market to sell their securities. The price received may be more or less than the original purchase price and may depend, in general, on the level of interest rates, time to term, credit quality of the issuer and liquidity.

Among other reasons, prices may also be affected by current market conditions, or by the size of the trade (prices may be different for 10 bonds versus 1,000 bonds), etc. It is important to note that selling a security prior to maturity may affect actual yield received, which may be different than the yield at which the bond was originally purchased. This is because the initially quoted yield assumed holding the bond to term. As mentioned above, there is an inverse relationship between interest rates and bond prices. Therefore, when interest rates decline, bond prices increase, and when interest rates increase, bond prices decline.

Generally, longer maturity bonds will be more sensitive to interest rate changes. Dollar for dollar, a long-term bond should go up or down in value more than a short-term bond for the same change in yield. Price risk can be determined through a statistic called duration, which is featured at the end of the fixed income section.

Liquidity risk is the risk that an investor will be unable to sell securities due to a lack of demand from potential buyers, sell them at a substantial loss and/or incur substantial transaction costs in the sale process. Broker/dealers, although not obligated to do so, may provide secondary markets.

Reinvestment Risk

Downward trends in interest rates also create reinvestment risk, or the risk that the income and/or principal repayments will have to be invested at lower rates. Reinvestment risk is an important consideration for investors in callable securities. Some bonds may be issued with a call feature that allows the issuer to call, or repay, bonds prior to maturity. This generally happens if the market rates fall low enough for the issuer to save money by repaying existing higher coupon bonds and issuing new ones at lower rates. Investors will stop receiving the coupon payments if the bonds are called. Generally, callable fixed income securities will not appreciate in value as much as comparable non-callable securities.

Similar to call risk, prepayment risk is the risk that the issuer may repay bonds prior to maturity. This type of risk is generally associated with mortgage-backed securities. Homeowners tend to prepay their mortgages at times that are advantageous to their needs, which may be in conflict with the holders of the mortgage-backed securities. If the bonds are repaid early, investors face the risk of reinvesting at lower rates.

Purchasing Power Risk

Fixed income investors often focus on the real rate of return, or the actual return minus the rate of inflation. Rising inflation has a negative impact on real rates of return because inflation reduces the purchasing power of the investment income and principal.

Posted on September 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and A.I.

***

***

Markets: Stocks started off Friday on a high note after a weak jobs report raised hopes that the Fed will cut interest rates this month. But the rally faded as the afternoon wore on, while 10-year bond yields tumbled to their lowest level since April.

Trade: President Trump said “fairly substantial” tariffs for semi-conductors are coming “very shortly,” but hinted that companies like Apple will be spared. He also clapped back at EU regulators for fines against Google.

Offbeat commodities: Raw sugar prices hit a two-month low as Brazilian producers churn out more of the sweet stuff, cocoa prices are expected to pop after Cargill paused production in Ivory Coast, and corn hit its highest price since July thanks to strong export demand.

Posted on September 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: Markets slowed along yesterday with the S&P 500 and NASDAQ buoyed after a pivotal antitrust ruling for Alphabet pushed big tech stocks higher across the board.

Bonds: The 30-year Treasury pushed 5% yesterday as traders fret about the Fed’s independence and the odds of interest rate cuts.

Commodities: Oil sank on reports that OPEC+ is contemplating increasing its crude output next month, while gold reached yet another new record high as uncertainty swirling around the future of tariffs continued to rise. JPMorgan analysts now think the precious metal could climb as high as $4,250 by the end of next year.

Posted on September 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Bonds: Treasury yields rose yesterday as investors dug into a Federal appeals court ruling last Friday stating that most of President Trump’s tariffs are illegal. The 30-year yield closed in on the key 5% level. Stocks: Equities tumbled across the board as technology stocks sold off and pulled the rest of the market down with them. Commodities: Gold hit a new record high as traders hedged against tariff uncertainty and braced themselves for an extremely important US jobs report on Friday that could make or break the case for the Fed to start cutting rates.

Posted on August 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Bonds: Long-term Treasury yields rose and short-term yields fell after President Trump fired Fed Governor Lisa Cook opening the gap between 5-year and 30-year yields to its widest point in three years.

Stocks: Equities barely budged on the latest FOMC drama with investors’ attention fully focused on Nvidia earnings tomorrow afternoon.

Trade Craft: President Trump vowed retaliation against countries that apply a digital services tax against US tech companies. He may also slap a 200% tariff on China if that country restricts trade on rare earth magnets.

Posted on August 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Types of investments

Once a physician [MD, DO, DPM or DDS] has a brokerage account, the young doctior will need to decide what to invest in. There are lots of options, and each comes with different benefits and drawbacks. Here are some of the most common options for new physician investors.

Stocks are the first thing most people think about when they are considering investing, but they are not the only option. The prices of stocks change daily, sometimes by large amounts, as the market adjusts to news and various cycles. For that reason, it’s important to do your research. If you’re just beginning with a retirement account, you could also consider the longer-term products listed below.

Index funds and mutual funds.

Index funds attempt to replicate the performance of an un-managed market index. The performance of mutual funds [open and closed] varies. You can often get involved for a lower initial investment, and they can provide good diversification,which makes your portfolio better equipped to handle market fluctuations [active and passive].

For that reason, many financial experts say they should form the core of your retirement portfolio. While they have many similar characteristics, there are important differences. Read more about some of the differences in index funds and mutual funds.

These technically aren’t investment products; they are a contract between you and an insurance company. However, they work to accomplish a similar goal. There are immediate annuities that convert some of your existing savings into lifetime payments, but if we’re talking about saving for retirement, a deferred income annuity is the closest comparison. You make premium payments into the deferred annuity on a regular or irregular basis depending on the contract terms, and when you reach retirement age, you annuitize those savings and receive payments for the rest of your life. They can make a valuable addition to a retirement savings strategy.

Other investments.

There are many other types of investments and financial vehicles: bonds [local, state or US], money market funds, certificates of deposit through a brokerage account or investment apps. Even the cash value of life insurance can play a part. They are all designed to address different needs and have benefits and drawbacks and may be important to your overall strategy.

Crypto.com is a cryptocurrency company based in Singapore that offers various financial services, including an app, exchange, and noncustodial DeFi wallet, NFT marketplace, and direct payment service in cryptocurrency. As of 2024, the company reportedly had more than 100 million customers and more than 4,000 employees.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Stocks: The stock markets rose today after Jerome Powell opened the door to interest rate cuts. The Dow soared to a new all-time high, while small-cap stocks in the Russell 2000 had a banner day.

Bonds: Yields fell while the chances of a rate cut after the Fed’s next meeting in September rose to 83%.

Commodities: Gold rose on rate cut hopes while oil fell as peace talks between Ukraine and Russia stalled. But the biggest winner is coffee: prices have risen for six straight days to cap off its biggest weekly gain since 2021.

Posted on August 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: The Dow climbed thanks to UnitedHealth and Warren Buffett while the rest of the market sank as the stock rally slowed. But, despite Friday’s decline, both the S&P 500 and NASDAQ wrapped up winning weeks.

Bonds: Both 10-year and 2-year Treasury yields continued to climb after Thursday’s PPI reading and Friday’s consumer confidence and retail sales data.

Commodities: All eyes were on Anchorage, Alaska as President Trump concluded talks with President Putin—discussions that will be crucial for crude’s future.

Posted on August 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.and Staff Reporters

***

***

President Trump is set to sign an executive order allowing alternative assets such as cryptocurrency, private equity investments, and real estate in 401(k) accounts. Those accounts are a veritable gold mine—Americans have stashed approximately $12.5 trillion away for retirement, and alternative asset managers have been chomping at the bit to get a piece of that pie.

According to Brew Markets, the changes have been a long time coming. All the way back in his first term, Trump ordered the Labor Department to review how to incorporate private equity investments into retirement accounts, an effort that was later reversed under President Biden. This latest move expands beyond private equity, coinciding with Trump’s push to bring crypto mainstream.

Proponents argue that alternative assets in 401(k) accounts will enhance investment diversification and could provide retirees with greater profits. Detractors note that these assets are less liquid, less transparent, and generally more risky than investing retirement funds into publicly traded stocks and bonds.

Trade: President Trump signed an executive order late yesterday unleashing a wave of new tariffs on 69 US trading partners that will go into effect on August 7th. Here’s a handy list of tariffs and their economic effects for anyone else having trouble keeping track of all these new numbers.

Markets: Stocks opened lower and kept falling thanks to a double whammy of new tariff rates and a shocking slowdown in the labor market, while bond yields tumbled.

Commodities: Goldjumped as the likelihood of a rate cut rose due to the latest jobs report, while oil sank on reports that OPEC+ may announce a crude production boost as soon as this weekend.

Stocks: Investors were pleased to hear about the trade deal with Japan yesterday and reports of an agreement with the EU coming soon kept the stock rally alive through market close. The S&P 500 notched its 12th new closing record this year, and the NASDAQ ended the day above 21,000 for the first time.

Bonds: Treasury yields rose a bit after an auction of 20-year notes was met with strong demand, indicating investor appetite for longer-term US debt.

Commodities: Oil inched higher while gold edged lower as investors hedge their bets in anticipation of more trade deals before the August 1st deadline.

The Fed Drama: A White House official said President Trump will likely fire Jerome Powell soon. Stockssank at the thought of the Fed head being shown the door, offsetting the pleasant surprise of a flat wholesale inflation reading.

Markets: Stocks managed to recoup their losses after Trump said it’s “highly unlikely” that he will fire Powell, but bonds remained shaken.

Crypto: Bitcoin bounced higher after the crypto bills currently under consideration in the House of Representatives cleared a key hurdle.

Stocks: Jobless claims came in lower than expected, the 30-year US bond auction met with strong demand, and Delta Airlines unofficially kicking off earnings season with a solid report. The S&P 500 and the NASDAQhit record highs.

Crypto: Bitcoin reached a record high for the second day in a row, hitting $113,863.31 today. The crypto’s price has stayed above $100k for 60 consecutive days.

Commodities: Coffee futures in New York climbed as much as 3.5% in response to President Trump’s threat to slap 50% tariffs on Brazil, which is the top producer of higher-end arabica coffee.

Stocks: The major indexes plowed higher with the minutes of the last FOMC meeting showing that officials were not at all united about when to begin cutting rates. Investors also treated more tariff letters sent by President Trump to seven more countries including Iraq and the Philippines as not vital.

Bonds: US Treasuries snapped a five-day losing streak after a $39 billion sale of 1-year notes was met with solid demand.

Posted on July 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets wrapped the trading day with another win thanks to a shockingly strong jobs report this morning. Both the S&P 500 and the NASDAQ hit new record highs.

Stocks: The S&P 500 and the NASDAQ started the second half of the year on the wrong foot, while the Dow climbed despite investors’ trepidation about conflict in Congress. But the Senate passed its version of the big, beautiful bill this afternoon, potentially getting us one step closer to ending all the drama.

Bonds: 10-year Treasury yields fell to their lowest level in two months this morning ahead of Jerome Powell’s appearance at a central banking conference today. There, Powell demurred on the possibility of a July rate cut, reiterating his wait-and-see approach.

Safe havens: The US dollar gained ground after a terrible first half of the year, while gold rose as investors braced themselves for the big jobs report on Friday.

Posted on June 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks: Markets sagged as fighting between Israel and Iran continued, with investors worried about escalation after President Trump called for the “unconditional surrender” of Iran’s Supreme Leader Ali Khamenei. The Wall Street Journal reported that he is considering a potential US strike against Iran.

Commodities: Oil prices popped this morning after Trump warned that Tehran should be evacuated.

Bonds: Yields sank after US retail sales came in much lower than anticipated, raising fears of an economic slowdown.

Posted on June 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: Israel and Iran exchanged missile strikes for a fourth day, but investors are betting that the conflict will remain at least somewhat contained. Reports that Iran wants to de-escalate the conflict and even restart nuclear talks seemed to underline that idea, and markets rose strongly throughout the afternoon.

Commodities: Gold fell as hopes of a ceasefire between Israel and Iran made investors more bullish, while Iranian oil infrastructure was spared from the attacks, pushing crude prices lower.

Bonds: A $13 billion 20-year bond auction this afternoon yielded strong demand, rounding out a series of solid auctions over the last few days that seemingly point to renewed investor confidence in US fixed income.

here are many ways for a doctor, osteopath, podiatrist or dentist to financially invest. Traditionally, this meant picking individual stocks and bonds. Today, there are many other ways to purchase securities en mass. For example:

MUTUAL FUND: A regulated investment company that manages a portfolio of securities for its shareholders.

Open End Mutual Funds: An investment company that invests money in accordance with specific objectives on behalf of investors. Fund assets expand or contract based on investment performance, new investments and redemptions. Trade at Net Asset Value or the price the fund shares scheduled with the US Securities and Exchange Commission (SEC) trade. NAV can change on a daily basis. Therefore, per-share NAV can, as well.

Closed End Mutual Funds: Older than open end mutual funds and more complex. A CEMF is an investment company that registers shares SEC regulations and is traded in securities markets at prices determined by investments. Shares of closed-end funds can be purchased and sold anytime during stock market hours. CEMF managers don’t need to maintain a cash reserve to redeem or / repurchase shares from investors. This can reduce performance drag that may otherwise be attributable to holding cash. CEMFs may be able to offer higher returns due to the heavier use of leverage [debt]. They are subject to volatility, less liquid than open-end funds, available only through brokers and may sells at a heavily discount or premium to [NAV] determined by subtracting its liabilities from its assets. The fund’s per-share NAV is then obtained by dividing NAV by the number of shares outstanding. .

Sector Mutual Funds: Sector funds are a type of mutual fund or Exchange-Traded Fund (ETF) that invests in a specific sector or industry such as technology, healthcare, energy, finance, consumer goods, or real estate. Sector funds focus on a particular industry, allowing investors to gain targeted exposure to specific market areas. The goal is to outperform the overall market by investing in companies within a specific sector that is expected to perform well. However, they are also more susceptible to market fluctuations and specific sector risks, making them a more specialized and potentially higher-risk investment option.

EXCHANGE TRADED FUNDS: ETFs are a type of fund that owns various kinds of securities, often of one type. For example, a stock ETF holds stocks, while a bond ETF holds bonds. One share of the ETF gives buyers ownership of all the stocks or bonds in the fund. If an ETF held 100 stocks, then those who owned the fund would own a stake – albeit a very tiny one – in each of those 100 stocks.

ETFs are typically passively managed, meaning that the fund usually holds a fixed number of securities based on a specific preset index of investments. These are tax efficient. In contrast, many mutual funds are actively managed, with professional investors trying to select the investments that will rise and fall.

The Standard & Poor’s 500 Index is perhaps the world’s best-known index, and it forms the basis of many ETFs. Other popular indexes include the Dow Jones Industrial Average and the National Association of Securities Dealers Automated Quotations [NASDAQ] Composite Index.

ETFs based on these funds are called Index Funds and just buy and hold whatever is in the index and make no active trading decisions. ETFs trade on a stock exchange during the day, unlike mutual funds that trade only after the market closes. With an ETF you can place a trade whenever the market is open and know exactly the price you’re paying for the fund.

INDEX FUNDS: Index funds mirror the performance of benchmarks like the DJIA. These passive investments are an unimaginative way to invest. Passive index funds tracking market benchmarks accounted for just 21% of the U.S. equity fund market in 2012. By 2024, passive index funds had grown to about half of all U.S. fund assets. This rise of passive funds has come as they often outperform their actively managed peers. According to the widely followed S&P Indices Versus Active (SPIVA) scorecards, about 9 out of 10 actively managed funds didn’t match the returns of the S&P 500 benchmark in the past 15 years.

ASSESSMENT

Investing in individual stocks is psychologically and academically different than investing in the above funds, according to psychiatrist and colleague Ken Shubin-Stein MD, MPH, MS, CFA who is a professor of finance at the Columbia University Graduate School of Business When you buy shares of a company, you are putting all your eggs in one basket. If the company does well, your investment will go up in value. If the company does poorly, your investment will go down. Fund diversification helps reduce this risk.

CONCLUSION

Investing in the above fund types will help mitigate single company security risk.

References:

1. Fenton, Charles, F: Non-Disclosure Agreements and Physician Restrictive Covenants. In, Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

Readings:

1. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

4. Shubin-Stein, Kenneth: Unifying the Psychological and Financial Planning Divide [Holistic Life Planning, Behavioral Economics, Trading Addiction and the Art of Money]. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on June 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

A Basic Overview for Emerging Physician and Medical Professional Investors

By Somnath Basu; PhD, MBA

There are three basic considerations in any investment decision.

1] The first is the understanding of the investment objective or why the investment is being made. While this may seem somewhat irrelevant at first – why would you be investing if you do not know what you are doing – combining investment objectives can pose problems down-stream.

For example, if you are saving for your retirement so that you can afford the retirement lifestyle you desire (the investment objective), your saving plan should not include any savings you are making for your children’s education (a separate investment objective). Compounding the two savings streams in one plan can very easily lead to one or both of the plans failing.

2] The second consideration is the time horizon of the investment. As a rough guide, investments that need to mature in the next 5-7 years can be considered as short term, 8-15 years as medium term and the rest as long term.

3] Finally, and probably the most important consideration of all is the importance you attach (priority) to achieving your investment objective; in other words, how safe and secure should your investments be. For example, if you are 70 years old and considering how you should invest your retirement funds so that your expenses are covered say for the next 25 years, you do not want a large margin of error in how your investments turn out; you can ill afford to be broke when you are older and hence you want your investments to be as secure as possible.

On the other hand, if the investment is for a second home or a boat, for example, you may wish to engage in some risk taking which may help in lowering your upfront investment needs. It is very important for any investor to clearly understand how much loss they can bear from any investment decision.

Decision Matrix

It is useful to express the investment framework described above as a simple decision matrix. Using the matrix (shown below) as a decision support system should clarify and simplify most investment decisions.

Understanding where in the matrix your decision falls is a very good first step of your decision. Both these elements (safety and time) will ultimately decide the kinds of financial instruments that will reside in your portfolio. We will examine the structure of each of the 9 possible combinations shown in the matrix. Before doing so, let us start by examining the various investment alternatives (e.g. stocks, bonds, etc.) since they have an implicit connection with the two dimensions portrayed in our matrix.

Stocks

Stocks are the most well known and popular form of financial investments. Stocks may be further segregated between large cap and small cap stocks, where the term “cap” is surrogate for the size of the underlying corporation or firm.

Stocks may represent investments in both domestic and international companies. Within the international category, stocks may represent corporations registered in developed (safer) or emerging (riskier) markets. In terms of our matrix dimensions, stocks are best suited when the decision is of medium or long term. In terms of safety, large cap (both domestic and international) stocks are the safest, while small cap and emerging market stocks are the most risky. The riskier the stock, the greater are the profit possibilities as are the chances of large losses.

Bonds

The second common type of investment are bonds Generally, bonds are much safer than stocks with the exception of a class of bonds known as high yield (or junk) bonds. Bonds are issued by companies, governments (domestic and international) and other agencies such as local governments (municipal bonds or “munis” which are especially desirable for those in high income tax rate categories) and quasi-government agencies such as Federal Home Loan Bank, Student Loan Administration, Agricultural Cooperative Banks, etc (collectively known as “Agency” bonds such as Ginnie/Fannie/Sallie Mae, Freddie Mac, etc.).

Government bonds are the safest, followed by agency and municipal bonds and then by bonds issues by corporations.

Corporate bonds may be safe (which are assigned credit safety ratings such as AAA, AA, BBB, etc.) or risky (junk bonds with ratings such as BB, CCC, CC etc.).

Bonds can be used for all time horizons, their maturities ranging from 3 months to 30 years. Very short term bond and bond like instruments (with maturities of one year or less) are known as money market securities which are generally safer than most other investments.

Alternate Investments

Other types of investments include real estate (long term, risky), commodities (such as energy, basic building materials, precious metals, etc.) which are also risky and which may be used for both short term and long term purposes and provide a good hedge (counter balance) in an inflationary environment, derivatives (options and futures) which are very risky and typically short term in nature. Derivatives are generally suggested for very sophisticated investors and are best left alone otherwise.

Risk Reduction

A very important feature about investments is that when various types of investments are bundled together in a portfolio, they help to reduce the risk of the investment decision without affecting the profits in a comparable way. This basic aspect of mixing various kinds of investments (stocks, bonds, etc) to reduce risk is known as diversification and it is a “must” for any investment portfolio. It is a “must” because this technique of risk reduction is generally costless (unless you are paying a financial advisor to do this for you) and it is very worthwhile. All other methods of risk reduction have cost implications.

Scenario Matrix

Armed with this nomenclature regarding various investment types we can now go about examining what the 9 combination (Scenario) portfolios may look like for investment purposes.

Starting with Scenario 1, if you wish to make a short term decision that is very important to you and needs to be very safe, investments should be made in very short term bonds (government or treasury bills)and other similar money market (short term, safe) securities. International short term bonds of developed countries may also be included. Such investment products are generally available through mutual funds or Exchange Traded Funds (or ETFs). ETFs are just like mutual funds except that they are usually cheaper, much easier to buy and sell and may provide tax deferral benefits.

If your investment falls in the Scenario 2 category, include agency/municipal bonds as well as some domestic and international (developed country) large cap stocks while for Scenario 3, smaller portions of small cap and emerging market stocks may be added proportionately while reducing some of the safer investments.

If your investment was a Scenario 4 type of investment, corporate large cap stocks (both domestic and international) could be added to agency or corporate (domestic and international) bonds. Before investing in stocks (in any Scenario) for this Scenario 4, a good question to ask is the following: how profitable were stock investments in the last 3-5 years? If the answer is “very profitable” then reduce the proportion of stocks as compared to bonds in the portfolio. If the last few years were not good, then it would be good to increase their comparable shares. The main reason for this “fine tuning” is that the fortunes of stocks (and many other types of investments) follow a cyclical pattern and the cycle is related to the general cycle of economic (GDP) growth and contraction.

It can be seen now how Scenarios 5 and 6 (as also 8 and 9) will follow a similar pattern as before, increasing proportionally in stocks (of all sizes, domestic/international), real estate, commodities, etc. Portfolios falling in these groups may also include some small cap and emerging market stocks as well as high yield or junk bonds. The proportion of these riskier investments would of course be higher for Scenario 6 over Scenario 5 (and Scenario 9 over 8).

For Scenario 7, the investment portfolio would typically resemble one that would be like an opposite of the portfolio in Scenario 1 and would include a greater proportion of large cap (domestic/international) stocks and a much smaller proportion of bonds. As we move towards Scenarios 8 and 9, the portfolios would be dominated by small cap and emerging market stocks as well as junk bonds.

Assessment

In the discussion above, I have tried to generalize the investment decision in a simplifying way. While the discussion may have centered more on stocks and bonds, it is important to note that all portfolios must “diversify” the investment risks by expanding upon the various types of investment products contained in the portfolios. The very fact that a portfolio contains various types of investments will ensure that the portfolio will perform better than those which are not as well diversified. This will be so in spite of any one of the investment types underperforming at any point in time and the diversification benefit will be received consistently over long periods of time. A popular analogy to this diversification benefit is the common phrase of not putting all eggs in one basket.

Editor’s Note: Somnath Basu PhD is program director of the California Institute of Finance in the School of Business at California Lutheran University where he’s also a professor of finance. He can be reached at (805) 493 3980 or basu@callutheran.edu

Conclusion

The above approach to investment decision-making can be considered as a basic template that can be used universally. For those seeking greater sophistication and who have a foundation built on the above model, expert advice is strongly recommended.

And so, your thoughts and comments on this ME-P are appreciated. Financial advisors please chime in on the debate? Is Basu correct; why or why not? Review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@outlook.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed

And, credible sponsors and like-minded advertisers are always welcomed.

Bonds: The 10-year yield fell after CPI came in lower than analysts expected. The Treasury Department’s auction of 10-year bonds also went well, with strong participation from traders a key sign of demand for fixed income. Zero Coupon: https://medicalexecutivepost.com/2024/11/12/bonds-zero-coupon/

FIVE INVESTING MISTAKES OF DOCTORS; PLUS 1 VITAL TIP

As a former US Securities and Exchange Commission [SEC] Registered Investment Advisor [RIA] and business school professor of economics and finance, I’ve seen many mistakes that doctors must be aware of, and most importantly, avoid. So, here are the top 5 investing mistakes along with suggested guideline solutions.

Mistake 1: Failing to Diversify Investment but Beware Di-Worsification

A single investment may become a large portion of your portfolio as a result of solid returns lulling you into a false sense of security. The Magnificent Seven stocks are a current example:

Apple, up +5,064%% since 1/18/2008

Amazon, up +30,328% since 9/6/2002

Alphabet, up +1,200% since 7/20/2012

Tesla, up +21,713% since 11/16/2012

Meta, up +684% since 2/20/2015

Microsoft, up +22% since 12/21/2023

Nvidia, up +80,797% since 4/15/2005

Guideline: The Magnificent Seven [7] has grown from 9% of the S&P 500 at the end of 2013 to 31% at the end of 2024! That means even if you don’t own them, you’re still very exposed if you have an Index Fund [IF] or Exchange Traded Fund [ETF] that tracks the market. Accordingly, diversification is the only free lunch in investing which can reduce portfolio risk. But, remember the Wall Street insider aphorism that states: “Di-Versification Means Always Having to Say Your Sorry.”

The term “Di-Worsification” was coined by legendary investor Peter Lynch in his book, One Up On Wall Street to refer to over-diversifying an investment portfolio in such a way that it reduces your overall risk-return characteristics. In other words, the potential return rises with an increase in risk and invested money can render higher profits only if willing to accept a higher possibility of losses [1].

A podiatrist can easily fall into the trap of chasing securities or mutual funds showing the highest return. It is almost an article of faith that they should only purchase mutual funds sporting the best recent performance. But in fact, it may actually pay to shun mutual funds with strong recent performance. Unfortunately, many struggle to appreciate the benefits of their investment strategy because in jaunty markets, people tend to run after strong performance and purchase last year’s winners.

Similarly, in a market downturn, investors tend to move to lower-risk investment options, which can lead to missed opportunities during subsequent market recoveries. The extent of underperformance by individual investors has often been the most awful during bear markets. Academic studies have consistently shown that the returns achieved by the typical stock or bond fund investors have lagged substantially.

Guideline: Understand chasing performance does not work.Continually monitor your investments and don’t feel the need to invest in the hottest fund or asset category. In fact, it is much better to increase investments in poor performing categories (i.e. buy low). Also keep in remind rebalancing of assets each year is key. If stocks perform poorly and bonds do exceptionally well, then rebalance at the end of the year. In following this strategy, this will force a doctor into buying low and selling high each year.

Often doctors make their investment decisions under the belief that stocks will consistently give them solid double-digit returns. But the stock markets go through extended long-term cycles.

In examining stock market history, there have been 6 secular bull markets (market goes up for an extended period) and 5 secular bear markets (market goes down) since 1900. There have been five distinct secular bull markets in the past 100+ years. Each bull market lasted for an extended period and rewarded investors.

For example, if an investor had started investing in stocks either at the top of the markets in 1966 or 2000, future stock market returns would have been exceptionally below average for the proceeding decade. On the other hand, those investors fortunate enough to start building wealth in 1982 would have enjoyed a near two-decade period of well above average stock market returns. They key element to remember is that future historical returns in stocks are not guaranteed. If stock market returns are poor, one must consider that he or she will have to accept lower projected returns and ultimately save more money to make up for the shortfall. For example,

The May 6th, 2010, flash crash, also known as the crash of 2:45, was a United States trillion-dollar stock market plunge which started at 2:32 pm EST and lasted for approximately 36 minutes.

And, investors who have embraced the “buy the dip” strategy in 2025 have been handsomely rewarded, with the S&P 500 delivering its strongest post-pull back returns in over three decades.

According to research from Bespoke Investment Group, the S&P 500 has gained an average of 0.36% in the trading session following a down day so far in 2025. The only year with a comparable performance was 2020, which saw a 0.32% average post-dip gain [2].

The most recent example came on May 27, 2025 when the S&P 500 surged more than 2% after falling 0.7% in the final session before the holiday weekend. The rally was sparked by President Trump’s decision to scale back huge previously threatened tariffs on EU —a recurring catalyst behind many of 2025’s rebound.

Guideline: Beware of projecting forward historical returns. Doctors should realize that the stock markets are inherently volatile and that, while it is easy to rely on past historical averages, there are long periods of time where returns and risk deviate meaningfully from historical averages.

Some doctors believe they are “smarter than the market” and can time when to jump in and buy stocks or sell everything and go to cash. Wouldn’t it be nice to have the clairvoyance to be out of stocks on the market’s worst days and in on the best days?

Using the S&P 500 Index, our agile imaginary doctor-investor managed to steer clear of the worst market day each year from January 1st, 1992 to March 31st, 2012. The outcome: s/he compiled a 12.42% annualized return (including reinvestment of dividends and capital gains) during the 20+ years, sufficient to compound a $10,000 investment into $107,100.

But what about another unfortunate doctor-investor that had the mistiming to be out of the market on the best day of each year. This ill-fated investor’s portfolio returned only 4.31% annualized from January 1992 – March 2012, increasing the $10,000 portfolio value to just $23,500 during the 20 years. The design of timing markets may sound easy, but for most all investors it is a losing strategy.

More contemporaneously on December 18th 2024, the DJIA plummeted 2.5%, while the S&P 500 declined 3% and the NASDAQ tumbled 3.5%

Guideline: If it looks too good to be true, it probably is. While jumping into the market at its low and selling right at the high is appealing in theory, we should recognize the difficulties and potential opportunity and trading costs associated with trying to time the stock market in practice. In general, colleagues are be best served by matching their investment with their time horizon and looking past the peaks / valleys along the way.

Mistake 5: Failing to Recognize the Impact of Fees and Expenses

A free dinner seminar or a polished stock-broker sales pitch may hide the total underlying costs of an investment. So, fees absolutely matter.

The first costing step is determining what the fees actually are. In a mutual fund, these costs are found in the company’s obligatory “Fund Facts”. This manuscript clearly outlines all the fees paid–including up front fees (commissions and loads), deferred sales charges and any switching fees. Fund management expense ratios are also part of the overall cost. Trading costs within the fund can also impact performance.

Here is a list of the traditional mutual fund fees:

Front End Load: The commission charged to purchase a fund through a stock broker or financial advisor. The commission reduces the amount you have available to invest. Thus, if you start with $100,000 to invest, and the advisor charges up to an 8 percent front end load, you end up actually investing $92,000.

Deferred Sales Charge (DSC) or Back End Load: Imposed if you sell your position in the mutual fund within a pre-specified period of time (normally one – five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: Costs of the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing fees.

Annual Administration Fee: Many mutual fund companies also charge a fee just for administering the account – usually under $100-150 per year.

Guideline: Know and understand all fees.

For example: A 1 percent disparity in fees may not seem like much but it makes a considerable impact over a long time period.

Consider a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the investor pays a 2 percent operating fee. In comparison, if s/he opted for a fund that charged a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000!

This is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more savings over a long period of time.

One Vital Tip: Investing Time is on Your Side

Despite thousands of TV shows, podcasts, textbooks, opinions and university studies on investing, it really only has three simple components. Amount invested, rate of return and time. By far, the most important item is time! For example:

Nvidia: if you invested $1,000 in 2009, you’d have $338,103 today.

Apple: if you invested $1,000 in 2008, you’d have $48,005 today.

Netflix: if you invested $1,000 in 2004, you’d have $495,679 today.

Unfortunately, this list of investing mistakes is still being made by many doctors. Fortunately, by recognizing and acting to mitigate them, your results may be more financially fruitful and mentally quieting.

REFERENCES:

1. Lynch, Peter: One Up on Wall Street [How to Use What You Already Know to Make Money in the Market]: Simon and Shuster (2nd edition) New York, 2000.

1. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York, 2006.

3. Marcinko, DE; Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] CRC Press, New York, 2015.

BIO: As a former university Professor and Endowed Department Chair in Austrian Economics, Finance and Entrepreneurship, the author was a NYSE Registered Investment Advisor and Certified Financial Planner for a decade. Later, he was a private equity and wealth manager

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on June 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: Equities inched higher on a handful of optimistic headlines. First, the US and China trade teams met in London today with hopes the two superpowers could resolve disputes over export curbs. Also, a new survey from the New York Fed found that consumer expectations for inflation eased across all time horizons in May. STOCKS: https://medicalexecutivepost.com/2025/04/18/stocks-basic-definitions/

Stocks: The S&P 500 touched 6,000 points for the first time since February and wrapped up its fifth positive week in the past seven following a better-than-expected jobs report. The vibes got even better in the afternoon following a President Trump announcement that the US and China trade teams will meet in London on Monday. STOCKS: https://medicalexecutivepost.com/2025/04/18/stocks-basic-definitions/

Bonds: Treasury yields ticked up in response to the solid May jobs report, a sign that investors were reducing bets on the scale of rate cuts this year. That’s not what Trump wants to hear: He urged Fed Chair Jerome Powell to slash interest rates by a jumbo-sized full point to pour “rocket fuel” on the economy. REVENUE BONDS: https://medicalexecutivepost.com/2024/12/20/bonds-revenue/

Oil: Oil prices have gone sideways for three straight weeks now, trading within a $4 range around $65/barrel since the middle of May. We’ll let you know when something interesting happens. CRUDE OIL:https://medicalexecutivepost.com/2024/08/14/wti-crude-oil/

According to wikipedia, the S&P 500 Dividend Aristocrats is a stock market index composed of the companies in the S&P 500 index that have increased their dividends in each of the past 25 consecutive years. It was launched in May 2005.

There are other indexes of dividend aristocrats that vary with respect to market cap and minimum duration of consecutive yearly dividend increases. Components are added when they reach the 25-year threshold and are removed when they fail to increase their dividend during a calendar year or are removed from the S&P 500. However, a study found that the stock performance of companies improves after they are removed from the index The index has been recommended as an alternative to bonds for investors looking to generate income.

To invest in the index, there are several exchange traded funds (ETFs), which seek to replicate the performance of the index.

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Bonds breathed a sigh of relief after 30-year Treasury yields fell back below 5% as Japanese central bankers took precautionary measures to shore up their finances.

Gold tumbled as investors continue to throw money at risk assets, while bitcoin maintained its recent gains.

CoreWeave can’t stop, won’t stop: The AI hyperscaler was downgraded by Barclays analysts, who think its near-term upside is limited, but shares still rose 20.66%.

VF Corp., the parent company of The North Face, JanSport, etc, rose 12.92% after disclosing that members of its C-suite splurged on the stock.

SoundhoundAI is a retail trader favorite, and now Piper Sandler analysts like it,too: The AI voice platform jumped 16.05% on an upgrade.

Southwest gained 5.53% on reports that the airline is rolling out $35 baggage fees beginning tomorrow.

Movie theater stocks popped on a record-breaking Memorial Day weekend at the box office: AMC soared 23.77%, Cinemark climbed 3.82%, and MarcusCorp. gained 10.12%.

What’s down

PDD Holdings plunged 13.64% after the Chinese e-commerce retailer reported a hefty 47% decline in profits last quarter.

Trump Media & Technology Group tumbled 10.38% after the company announced it’s raising $2.5 billion to buy bitcoin.

ChampionHomes sank 16.39% after the homebuilder missed Wall Street expectations last quarter by a mile.

RocketPharmaceuticals dropped 62.84% after the biotech reported that a patient participating in a gene therapy trial died over the weekend.

Posted on May 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks wavered throughout the day as the 10-year Treasury yield rose back above 4.5%, making a convincing argument for investors to buy risk-free bonds with big yields rather than equities.

Yields on both 20-year and 30-year Treasuries traded above 5% after the Republican tax and spending bill passed the House, raising fears of a bigger US deficit and lower creditworthiness in the years ahead.

Bitcoin continued to climb last night, hitting a new record high of $111,886.41 in the wee hours of the morning before losing some ground throughout the trading session today.

Nike gained 2.30% on the news that it will begin selling its shoes on Amazon for the first time since 2019.

Fannie Mae popped 46.73% and FreddieMac jumped 42.50% on President Trump’s comments that he’s seriously considering bringing the mortgage giants public.

Advance Auto Parts exploded 57.14% higher after better-than-feared earnings made it clear that its turnaround plan is working.

Urban Outfitters soared 22.84% after reporting EPS of $1.16 last quarter, far better than the $0.84 per share analysts had forecast.

Snowflake gained 13.47% thanks to a strong first quarter and management’s expectation that revenue will rise about 25% this quarter.

What’s down

Walmart lost 0.48% on the news that it will cut 1,500 jobs in a corporate restructuring.

Analog Devices fell 4.63% even though the semiconductor maker beat Wall Street estimates on both sales and profits last quarter.

Health insurance stocks took a hit on reports that the US government will conduct “aggressive” Medicare Advantage audits. Humana sank 7.58%, UnitedHealthGroup fell 2.08%, and CVSHealth dropped 3.06%.

Posted on May 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

When S&P downgraded the US’ credit rating in August 2011, it sparked the worst one-day decline in US stocks since the Great Financial Crisis. Today was the first day of trading after Moody’s downgraded the US’ credit rating, and while stocks sank at the open, they recovered a lot of lost ground after investors decided to buy the dip.

The downgrade pushed yields on 30-year Treasury bonds above 5% at the open, while 10-year yields rose to 4.55% at one point. But yields on both notes fell throughout the afternoon as buyers crept back into the bond market.

Gold was the big winner today as investors sought safety, while the CBOE Volatility Index, or VIX, popped higher.

Investors largely shrugged at Nvidia’smany announcements today, including the ability for customers to use non-Nvidia chips in Nvidia products. Shares rose just 0.13%.

UnitedHealth Group posted a 8.18% gain as investors turned their attention to the suddenly cheap health insurance giant.

Novavax exploded 15.01% higher thanks to the FDA’s approval of its new Covid-19 vaccine.

TXNM Energy popped 6.98% to an all-time high on the announcement that Blackstone will acquire the power provider for $11.5 billion.

What’s down

Tesla tumbled 2.25% after Chinese tech giant Xiaomi announced it will debut its Yu7 sports utility vehicle, a clear Tesla challenger in a key market, on Thursday.

Walmart lost 0.12% after Treasury Secretary Scott Bessent met with company leadership to discuss how the retailer could “eat the tariffs.”

Bath & Body Works sank 0.56% after the retailer named former Nike exec Daniel Heaf as its new CEO effective immediately.

Reddit fell 4.63% due to a downgrade from Wells Fargo analysts who think the social media platform will lose search traffic to Google AI.

Diageo is down 0.69% after the maker of Johnnie Walker whiskey said it will take an annual tariff hit of $150 million.

Alibaba dropped 0.40% on a New York Times report that the Trump Administration is concerned with Apple’s plan to use Alibaba AI on its iPhones.

JPMorgan fell 1% as shareholders at the bank’s investment division grapple with CEO Jamie Dimon’s departure.

Solar stocks sank after the Republican tax and spending bill moved forward with a commitment to end clean energy tax credits earlier than planned. First Solar fell 7.59%, SunRun lost 7.84%, and AES lost 4.10%.

The Dow Jones exploded 1,000 points in pre-market trading, and the rally never waned toay. Both the Dow and the S&P 500 are nearly back to even for the year, while the NASDAQ clawed its way out of bear market territory.

Bonds tumbled while yields soared as the market pushed the timing for the Fed to cut interest rates back from July to September.

Gold sank as traders passed right on by the go-to investment for safety and sprinted straight toward equities.

Crude oil popped on the hopes of stronger economic growth for both the US and China now that the two countries are finally engaging in trade discussions.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

US Markets

After one of the most volatile weeks in Wall Street history, the S&P 500 closed 5.7% higher for its best week since 2023. But investors are taking little comfort with the rebound in stocks.

A declining dollar fell to a three-year low against the euro on Friday and spiking bond yields have some observers warning of a monumental, structural shift away from the US as a safe haven due to the recent tariff turmoil.

An alternative investment is a financial asset that does not fall into one of the conventional investment categories. Conventional categories include stocks, bonds, and cash. Alternative investments can include private equity or venture capital, hedge funds, managed futures, art and antiques, commodities, and derivatives contracts. Real estate is also often classified as an alternative investment.

QUESTION: But what about a medical, podiatric or dental practice?

***

***

AnAlternate Asset Class Surrogate?

A medical practice is much like an alternative investment [AI], or alternate asset class in, two respects.

First, it provides the work environment that generates personal income which has been considered generous, to date.

Second, it has inherent appreciation and sales value that can be part of an exit (retirement) or succession planning transfer strategy.

Conclusion

So, unlike the emerging thought that offers Social Security payments as a surrogate for an asset classes; or a federally insured AAA bond – a medical practice might also be considered by some folks as an asset class within a well diversified modern investment portfolio.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on April 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500 (GSPC) dropped almost 3.5%, while the tech-heavy NASDAQ Composite (IXIC) tumbled 4.3%. The Dow Jones Industrial Average (^DJI) fell about 1,000 points, or 2.5%. The 10-year Treasury yield (^TNX), in high focus amid bond market whiplash, ended the day flat around 4.39%.

The major averages sank to session lows after the White House confirmed updated tariff figures released on Thursday brings the total increased levies on Chinese goods to 145%, not 125% as previously stated.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

Posted on April 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Treasury notes are typically considered one of the world’s safest safe-haven assets—the US has always repaid bondholders on their investment, plus yield (interest). That’s why you can usually count on the bond market to rally when the stock market craters. And, vice-versa. But not this time:

The benchmark 10-year bond yield, which moves inversely to bond prices, had its steepest spike this week since the 2008 financial crisis. The 10-year yield is more closely watched than the 30-year yield (which also spiked) in part because it influences home and auto loan rates.

A Treasury auction of 3-year bonds on Tuesday was met with the softest demand since December 2023. That helped drive the bond sell-off on fears of a pullback among international investors, who hold $8.5 trillion in US Treasuries (Japan and China lead the pack).

Posted on April 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS – MARKET VOLATILITY

By Staff Reporters

***

***

US stocks nosedived on Thursday, with the Dow tumbling more than 1,200 points as President Trump’s surprisingly steep “Liberation Day” tariffs sent shock waves through markets worldwide. The tech-heavy NASDAQ Composite (IXIC) led the sell-off, plummeting over 4%. The S&P 500 (GSPC) dove 3.7%, while the Dow Jones Industrial Average (^DJI) tumbled roughly 3%. [ongoing story].

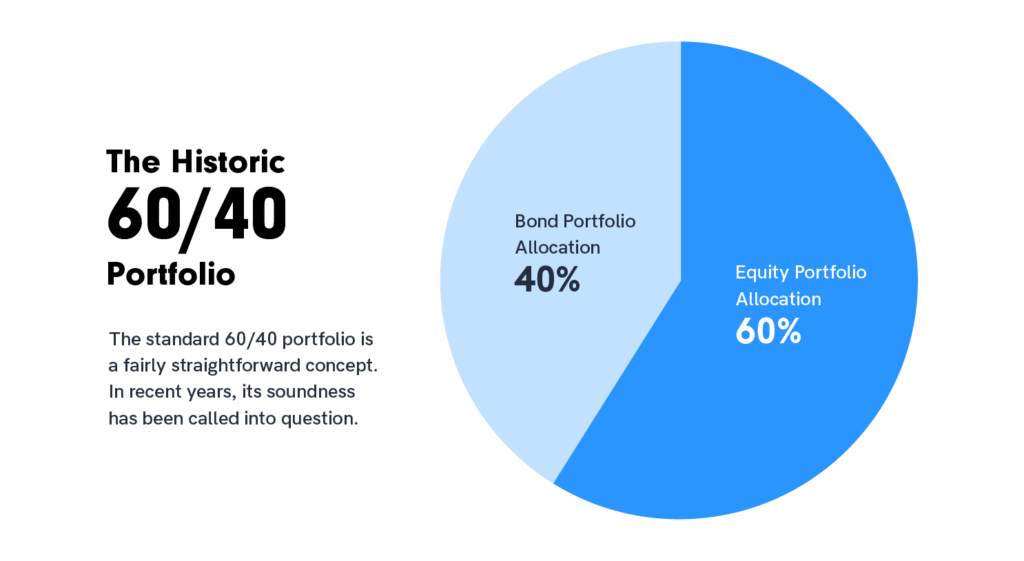

So, does the traditional 60 stock / 40 bond strategy still work or do we need another portfolio model?

***

The 60/40 strategy evolved out of American economist Harry Markowitz’s groundbreaking 1950s work on modern portfolio theory, which holds that investors should diversify their holdings with a mix of high-risk, high-return assets and low-risk, low-return assets based on their individual circumstances.

While a portfolio with a mix of 40% bonds and 60% equities may bring lower returns than all-stock holdings, the diversification generally brings lower variance in the returns—meaning more reliability—as long as there isn’t a strong correlation between stock and bond returns (ideally the correlation is negative, with bond returns rising while stock returns fall).

For 60/40 to work, bonds must be less volatile than stocks and economic growth and inflation have to move up and down in tandem. Typically, the same economic growth that powers rallies in equities also pushes up inflation—and bond returns down. Conversely, in a recession stocks drop and inflation is low, pushing up bond prices.

***

But, the traditional 60/40 portfolio may “no longer fully represent true diversification,” BlackRock CEO Larry Fink writes in a new letter to investors.

Instead, the “future standard portfolio” may move toward 50/30/20 with stocks, bonds and private assets like real estate, infrastructure and private credit, Fink writes.

Here’s what experts say individual investors may want to consider before dabbling in private investments.

It may be time to rethink the traditional 60/40 investment portfolio, according to BlackRock CEO Larry Fink. In a new letter to investors, Fink writes the traditional allocation comprised of 60% stocks and 40% bonds that dates back to the 1950s “may no longer fully represent true diversification.“