BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The Medicare Part A Trust Fund, formally known as the Hospital Insurance (HI) Trust Fund, occupies a central place in the United States’ health‑care landscape. It finances inpatient hospital services, skilled nursing facility care, hospice services, and some home health care for tens of millions of older adults and people with disabilities. Because it is funded primarily through payroll taxes, its financial health is often viewed as a barometer of the broader relationship between the American workforce, the federal budget, and the aging population. When projections indicate that the trust fund will remain solvent for an additional twelve years, the implications ripple far beyond accounting tables. This extended solvency horizon shapes political debates, influences health‑care planning, and affects the sense of security felt by current and future beneficiaries.

At its core, solvency means that the trust fund can fully pay its obligations without requiring legislative intervention. When analysts project twelve more years of solvency, they are essentially saying that the fund’s income—mainly payroll taxes, taxes on Social Security benefits, and interest—will be sufficient to cover expected expenditures for more than a decade. This is not a trivial achievement. Medicare Part A has long faced pressure from demographic shifts, particularly the retirement of the baby‑boomer generation and the corresponding slowdown in the growth of the working‑age population. As more people draw benefits and fewer workers contribute payroll taxes, the financial balance naturally tightens. Extending solvency by twelve years suggests that recent economic conditions, policy adjustments, or health‑care cost trends have temporarily eased that pressure.

One of the most important consequences of a longer solvency window is the breathing room it provides for policymakers. Medicare reform is notoriously difficult. It requires navigating ideological divides, balancing fiscal responsibility with social commitments, and confronting the political risks of altering a program that millions of Americans rely on. When insolvency looms just a few years away, the pressure to act can lead to rushed or contentious proposals. A twelve‑year buffer, however, allows for a more deliberate and thoughtful approach. Lawmakers can explore structural reforms, evaluate the long‑term effects of payment changes, and consider broader health‑care system improvements without the immediate threat of benefit disruptions.

***

***

For beneficiaries, the extension of solvency carries psychological and practical significance. Medicare is not merely a government program; it is a promise woven into the fabric of American retirement planning. Workers contribute payroll taxes throughout their careers with the expectation that Medicare will be there when they need it. News that the trust fund is projected to remain solvent for twelve more years reinforces that sense of reliability. It reassures current beneficiaries that their hospital coverage is secure and signals to younger workers that the system is not on the brink of collapse. While projections are not guarantees, they shape public confidence in ways that influence everything from personal financial planning to political engagement.

The extended solvency period also reflects underlying trends in health‑care spending and economic performance. When the economy grows, payroll tax revenue increases, strengthening the trust fund. Similarly, when health‑care cost growth slows—whether due to changes in provider behavior, technological improvements, or policy adjustments—Medicare’s expenditures rise more gradually. A twelve‑year solvency projection suggests that, at least for now, these forces are aligned in a favorable direction. It does not mean that long‑term challenges have disappeared, but it does indicate that the system is more resilient than some earlier forecasts suggested.

Still, the projection of twelve more years of solvency should not be interpreted as a signal to relax. The trust fund’s long‑term trajectory remains shaped by structural factors that will not resolve themselves. The aging population will continue to grow, and the ratio of workers to beneficiaries will continue to shrink. Health‑care costs, even when growing more slowly, still tend to outpace general inflation. Moreover, Medicare Part A relies heavily on payroll taxes, which are sensitive to economic cycles. A recession, a shift in employment patterns, or a slowdown in wage growth could quickly erode the projected solvency cushion. In this sense, the twelve‑year projection is both a reassurance and a warning: the system is stable for now, but not indefinitely.

***

***

The extended solvency window also invites a broader conversation about the future of Medicare financing. Some argue that the trust fund’s challenges highlight the need for new revenue sources, such as adjustments to payroll tax rates or expansions of the taxable wage base. Others advocate for reforms on the spending side, including changes to provider payments, incentives for value‑based care, or efforts to reduce unnecessary hospitalizations. Still others propose more sweeping transformations, such as integrating Medicare’s financing streams or rethinking the division between Part A and Part B. A twelve‑year horizon does not dictate which path policymakers should choose, but it does create space for a more comprehensive and less crisis‑driven debate.

Another dimension of the solvency discussion involves the broader health‑care system. Medicare is a major payer, and its policies influence hospitals, physicians, insurers, and state governments. When the trust fund is under severe financial strain, Medicare may adopt more aggressive cost‑control measures, which can ripple through the entire system. A longer solvency period reduces the immediate pressure for abrupt changes, allowing the health‑care sector to adapt more gradually. Hospitals, for example, can plan capital investments with greater confidence, and providers can engage in long‑term quality‑improvement initiatives without fearing sudden reimbursement cuts.

Ultimately, the projection of twelve more years of solvency for the Medicare Part A Trust Fund is a reminder of both the program’s durability and its vulnerability. It underscores the importance of economic growth, prudent policy choices, and ongoing efforts to improve the efficiency of health‑care delivery. It also highlights the need for vigilance. Solvency projections can shift from year to year, and a comfortable cushion today does not eliminate the need for long‑term planning. But for now, the extended horizon offers a measure of stability—an opportunity to strengthen Medicare for future generations while honoring the commitment made to those who depend on it today.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Pay‑for‑performance (P4P) has become one of the most widely discussed strategies for improving healthcare quality in modern health systems. At its core, P4P links financial incentives to specific measures of performance, such as patient outcomes, adherence to clinical guidelines, or efficiency metrics. The idea is straightforward: reward providers for delivering high‑quality care, and they will be more motivated to improve their practices. Yet the simplicity of the concept masks a complex set of challenges, trade‑offs, and ethical considerations that shape how P4P functions in real‑world healthcare environments.

One of the primary arguments in favor of P4P is that it attempts to shift healthcare away from volume‑based reimbursement. Traditional fee‑for‑service models reward providers for doing more—more tests, more procedures, more visits—regardless of whether those services improve patient health. P4P, in contrast, aims to reward value rather than volume. By tying payment to outcomes or evidence‑based processes, the model encourages clinicians to focus on preventive care, chronic disease management, and coordination across the continuum of care. In theory, this alignment of financial incentives with patient well‑being should lead to better outcomes and more efficient use of resources.

***

***

Another potential benefit of P4P is its ability to promote transparency and accountability. When performance metrics are clearly defined and publicly reported, providers have a clearer understanding of expectations and benchmarks. This can foster a culture of continuous improvement, where clinicians and organizations regularly evaluate their performance and identify opportunities for better care. For patients, transparency can empower more informed decision‑making and build trust in the healthcare system.

Despite these advantages, P4P is far from a perfect solution. One of the most persistent criticisms is that performance metrics often fail to capture the full complexity of patient care. Healthcare outcomes are influenced by a wide range of factors, many of which lie outside a provider’s control, such as socioeconomic conditions, patient adherence, and comorbidities. When incentives are tied to outcomes without adequate risk adjustment, providers may be unfairly penalized for caring for more complex or disadvantaged populations. This can inadvertently discourage clinicians from accepting high‑risk patients, undermining equity in access to care.

Another challenge is the potential for P4P to encourage “teaching to the test.” When financial rewards depend on specific metrics, providers may focus narrowly on those measures at the expense of other important aspects of care that are harder to quantify. This can lead to a checkbox mentality, where meeting the metric becomes more important than understanding the patient’s broader needs. In extreme cases, P4P can even incentivize gaming the system, such as upcoding diagnoses to make patient populations appear sicker and performance outcomes appear better.

Implementation complexity also poses a barrier. Designing fair, meaningful, and comprehensive performance measures requires significant administrative effort. Providers must invest time and resources into documentation, data reporting, and quality improvement initiatives. Smaller practices, which often lack the infrastructure of large health systems, may struggle to keep up with these demands. If the administrative burden outweighs the financial incentives, P4P can become more of a bureaucratic hurdle than a driver of improvement.

***

***

Ultimately, the effectiveness of pay‑for‑performance depends on thoughtful design and careful balancing of incentives. When metrics are clinically meaningful, risk‑adjusted, and aligned with broader goals of patient‑centered care, P4P can encourage positive change. When poorly designed, it risks distorting provider behavior and exacerbating inequities. As healthcare systems continue to evolve, P4P will likely remain part of the conversation, but it must be integrated with other reforms—such as care coordination models, population health strategies, and patient engagement efforts—to truly enhance quality and value.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Net Investment Income Tax (NIIT) occupies a distinctive place in the modern U.S. tax landscape. Introduced as part of the Affordable Care Act, it was designed to generate revenue from higher‑income households by taxing certain forms of unearned income. Although it affects a relatively small portion of taxpayers, its implications reach into investment strategy, tax planning, and broader debates about fairness and economic policy. Understanding how the NIIT works—and why it exists—offers insight into the evolving relationship between tax policy and wealth in the United States.

At its core, the NIIT is a 3.8 percent surtax applied to specific types of investment income for individuals whose modified adjusted gross income exceeds statutory thresholds. These thresholds—$200,000 for single filers and $250,000 for married couples filing jointly—are not indexed for inflation. As a result, over time, more taxpayers may find themselves subject to the tax even if their real purchasing power has not increased. This “bracket creep” is one of the subtle but important features of the NIIT, shaping its long‑term reach.

The tax applies only to “net investment income,” a term that includes interest, dividends, capital gains, rental income, royalties, and passive business income. It does not apply to wages, self‑employment earnings, or distributions from qualified retirement plans. The logic behind this distinction is straightforward: the NIIT targets income derived from wealth rather than labor. In practice, this means that two taxpayers with identical total income may face different NIIT liabilities depending on how much of their income comes from investments versus work.

The mechanics of the NIIT involve a comparison between two amounts: net investment income and the excess of modified adjusted gross income over the applicable threshold. The tax is applied to whichever of these two figures is smaller. This structure ensures that the NIIT functions as a surtax on high‑income households without taxing investment income for those below the threshold. It also means that taxpayers with large investment portfolios but modest overall income may avoid the tax entirely, while those with high wages and relatively small investment income may still owe it.

One of the most significant effects of the NIIT is its influence on investment behavior. Because the tax applies to capital gains, it can affect decisions about when to sell appreciated assets. Taxpayers may choose to time sales to avoid pushing their income above the threshold in a given year. Others may shift toward tax‑exempt investments, such as municipal bonds, or toward assets that generate unrealized rather than realized gains. The NIIT therefore becomes not just a revenue tool but a factor shaping the broader investment landscape.

The tax also interacts with other parts of the tax code in ways that can be complex. For example, rental real estate income is generally subject to the NIIT unless the taxpayer qualifies as a real estate professional and materially participates in the activity. Trusts and estates face their own NIIT rules, often reaching the surtax threshold at much lower income levels than individuals. These layers of complexity mean that the NIIT is often a central topic in tax planning for high‑income households, especially those with diverse investment portfolios.

Beyond its technical features, the NIIT reflects broader policy debates about equity and the distribution of tax burdens. Supporters argue that it helps ensure that high‑income individuals contribute a fair share to the cost of public programs, particularly those related to health care. Because investment income is disproportionately concentrated among wealthier households, the NIIT is seen as a way to align tax policy with ability to pay. Critics, however, contend that the tax discourages investment, adds unnecessary complexity, and imposes an additional layer of taxation on income that may already be subject to corporate taxes or other levies.

Despite these debates, the NIIT has become a stable part of the federal tax system. It raises billions of dollars annually and plays a role in funding health‑related initiatives. As discussions about tax reform continue, the NIIT often resurfaces as policymakers consider how best to balance revenue needs with economic incentives. Whether it remains unchanged, is expanded, or is modified in future legislation, the NIIT will continue to shape the financial decisions of high‑income taxpayers and contribute to the ongoing conversation about how the United States taxes wealth.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 8, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko; MBA MEd

***

***

What Medicare Does Not Cover: Understanding the Gaps in Coverage

Medicare, the federal health insurance program primarily for individuals aged 65 and older, provides essential coverage through its various parts—Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage). While it offers substantial support for many healthcare needs, Medicare does not cover everything. Understanding these gaps is crucial for beneficiaries to avoid unexpected expenses and plan for supplemental coverage.

One of the most significant omissions in Original Medicare (Parts A and B) is routine dental care. Services such as cleanings, fillings, tooth extractions, and dentures are generally not covered. Although Medicare began covering limited dental exams related to specific medical procedures in 2023 and 2024, comprehensive dental care remains excluded.

Vision care is another area where Medicare falls short. Routine eye exams, eyeglasses, and contact lenses are not covered unless related to specific medical conditions like cataract surgery. Similarly, hearing services, including exams and hearing aids, are not covered under Original Medicare, despite their importance to seniors’ quality of life.

Long-term care, such as custodial care in nursing homes or assisted living facilities, is also excluded. Medicare may cover short-term stays in skilled nursing facilities following hospitalization, but it does not pay for extended stays or help with daily activities like bathing and dressing.

Alternative therapies such as acupuncture, massage therapy, and chiropractic care are generally not covered unless deemed medically necessary. For example, Medicare may cover limited chiropractic services for spinal subluxation but not for general wellness or pain relief.

Cosmetic surgery is excluded unless it is required for reconstructive purposes following an accident or disease. Similarly, routine foot care and podiatry services are not covered unless related to specific medical conditions like diabetes.

To address these gaps, many beneficiaries turn to Medicare Advantage plans (Part C) or Medigap policies, which may offer additional benefits such as dental, vision, and hearing coverage. However, these plans vary widely, and not all supplemental policies cover every excluded service.

In conclusion, while Medicare provides a strong foundation for healthcare coverage, it leaves out several essential services that can significantly impact seniors’ health and finances. Awareness of these exclusions empowers beneficiaries to seek supplemental insurance, budget for out-of-pocket costs, and make informed decisions about their healthcare needs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 3, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

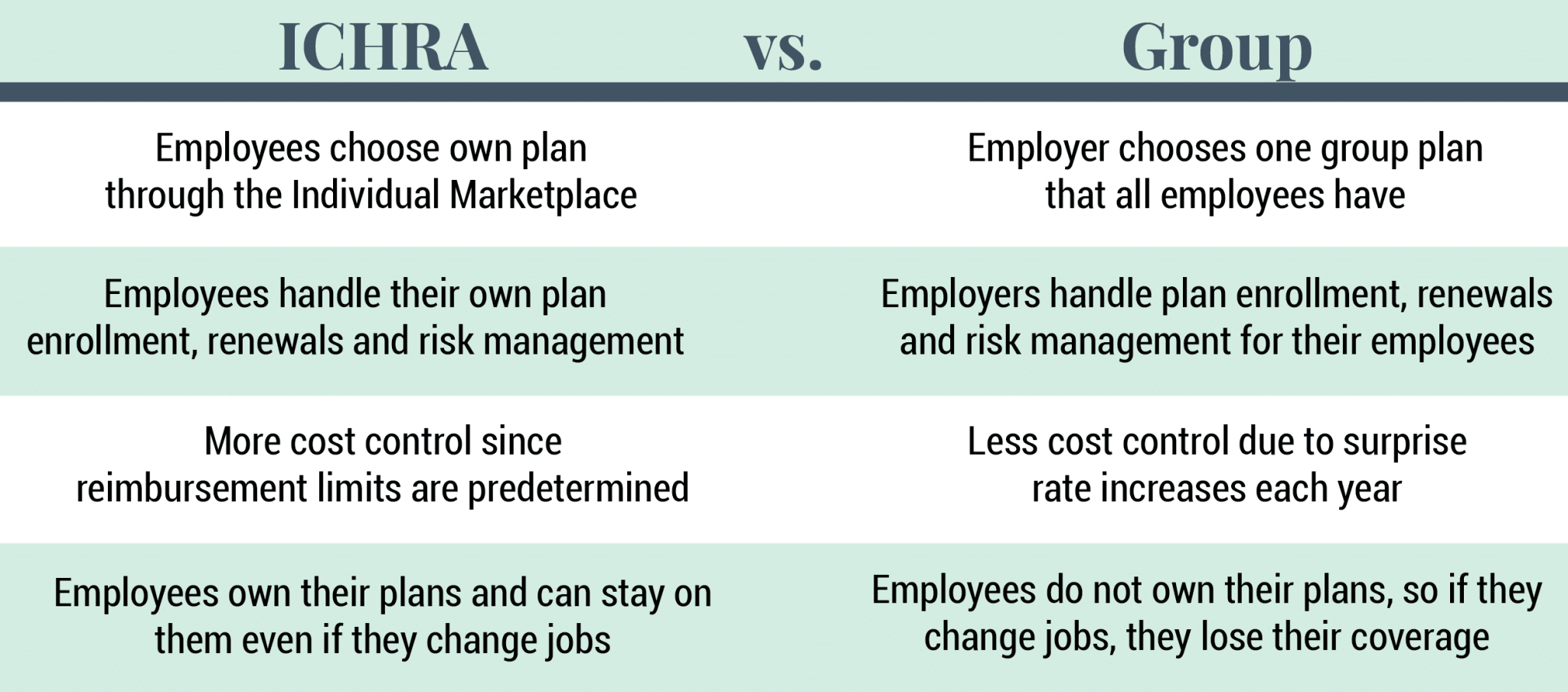

Alternative health coverage models like Short-Term Duration Plans, Health Care Sharing Ministries (HCSMs), and Individual Coverage Health Reimbursement Arrangements (ICHRAs) offer flexible, cost-conscious options for individuals and employers seeking alternatives to traditional insurance.

As the landscape of American healthcare continues to evolve, many consumers and employers are exploring non-traditional coverage models to address rising costs, limited access, and regulatory complexity. Among the most prominent alternatives are Short-Term Duration Plans, Health Care Sharing Ministries (HCSMs), and Individual Coverage Health Reimbursement Arrangements (ICHRAs)—each offering distinct advantages and trade-offs.

Short-Term Duration Plans are designed to provide temporary coverage for individuals experiencing gaps in insurance, such as between jobs or during waiting periods. These plans are typically less expensive than ACA-compliant insurance but come with significant limitations. They often exclude coverage for pre-existing conditions, maternity care, mental health services, and prescription drugs. While they offer affordability and quick enrollment, they lack the comprehensive protections mandated by the Affordable Care Act (ACA), making them a risky choice for those with ongoing health needs.

Health Care Sharing Ministries (HCSMs) represent a faith-based approach to healthcare financing. Members contribute monthly fees into a shared pool used to cover eligible medical expenses for others in the group. These arrangements are not insurance and are not regulated by state insurance departments, meaning they are not required to cover essential health benefits or guarantee payment. However, HCSMs appeal to individuals seeking community-based support and lower costs. They often include moral or religious requirements for membership and may exclude coverage for lifestyle-related conditions or services deemed inconsistent with their beliefs.

***

***

Individual Coverage Health Reimbursement Arrangements (ICHRAs) are employer-sponsored programs that allow businesses to reimburse employees for individual health insurance premiums and qualified medical expenses. Introduced in 2020, ICHRAs offer flexibility for employers to control costs while giving employees the freedom to choose plans that suit their needs. Unlike traditional group health insurance, ICHRAs shift the purchasing power to employees, promoting consumer choice and market competition. However, they require employees to navigate the individual insurance marketplace, which can be complex and variable depending on location and income.

Other emerging models include Direct Primary Care (DPC), where patients pay a monthly fee for unlimited access to a primary care provider, and Health Savings Accounts (HSAs) paired with high-deductible plans, which encourage consumer-driven healthcare spending. These models emphasize affordability, personalization, and preventive care, but may not offer sufficient protection against catastrophic health events.

In conclusion, alternative health coverage models provide valuable options for individuals and employers seeking flexibility and cost savings. However, they often come with trade-offs in coverage, regulation, and consumer protection. As ACA subsidies fluctuate and healthcare costs rise, these models are likely to gain traction—but consumers must carefully assess their health needs, financial risks, and eligibility before choosing a non-traditional path.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on December 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Employer-sponsored healthcare benefit programs have become a cornerstone of modern employment, shaping not only the financial well-being of workers but also the overall health of society. These programs represent a partnership between employers and employees, where organizations provide access to medical coverage as part of compensation packages. While wages remain the most visible form of remuneration, healthcare benefits often carry equal or greater significance, influencing job satisfaction, retention, and productivity.

At their core, employer-sponsored healthcare programs are designed to reduce the financial burden of medical expenses for employees. Healthcare costs can be unpredictable and overwhelming, and insurance coverage provides a safety net against sudden illness or injury. By offering group plans, employers can negotiate better rates with insurers, spreading risk across a larger pool of participants. This collective approach makes healthcare more affordable than if individuals were to purchase coverage independently. For employees, the assurance of medical support fosters peace of mind, allowing them to focus on their work without the constant worry of healthcare expenses.

From the employer’s perspective, healthcare benefits serve as a strategic tool for attracting and retaining talent. In competitive labor markets, robust benefit packages can distinguish one company from another. Workers often weigh healthcare coverage heavily when deciding between job offers, and organizations that provide comprehensive plans are more likely to secure skilled professionals. Moreover, offering healthcare benefits demonstrates a company’s commitment to employee welfare, reinforcing a culture of care and responsibility. This perception can strengthen loyalty and reduce turnover, ultimately saving organizations the costs associated with recruiting and training new staff.

***

***

Beyond recruitment and retention, healthcare benefits contribute directly to workplace productivity. Employees who have access to preventive care and regular medical services are less likely to suffer from untreated conditions that impair performance. Routine checkups, vaccinations, and screenings help identify health issues early, reducing absenteeism and minimizing disruptions to workflow. In addition, healthier employees tend to be more engaged, energetic, and capable of sustaining high levels of output. Employers thus benefit from a workforce that is not only present but also performing at its best.

Employer-sponsored healthcare programs also play a role in shaping organizational culture. When companies invest in employee health, they send a message that well-being is valued. This can foster trust and strengthen relationships between management and staff. In many cases, healthcare benefits are paired with wellness initiatives such as gym memberships, mental health resources, or nutritional counseling. These programs encourage healthier lifestyles, which in turn reduce long-term medical costs and enhance overall morale. The integration of healthcare and wellness initiatives reflects a holistic approach to employee support, extending beyond the workplace into personal lives.

Despite their advantages, employer-sponsored healthcare programs are not without challenges. Rising medical costs place pressure on employers to balance affordability with coverage quality. Smaller businesses may struggle to provide comprehensive plans, limiting their competitiveness in attracting talent. Additionally, employees may face limitations in provider networks or coverage options, leading to dissatisfaction. The complexity of healthcare systems can also create confusion, requiring employers to invest in education and communication to ensure employees understand their benefits. These challenges highlight the need for ongoing innovation and adaptation in benefit design.

Looking ahead, employer-sponsored healthcare programs are likely to evolve in response to changing workforce expectations and healthcare landscapes. Remote work, diverse employee demographics, and advances in medical technology will influence how benefits are structured. Employers may increasingly emphasize flexibility, offering customizable plans that cater to individual needs. Digital health tools, telemedicine, and wellness apps are already becoming integrated into benefit packages, expanding access and convenience. As organizations continue to adapt, the central principle remains the same: supporting employee health is both a moral responsibility and a strategic advantage.

In conclusion, employer-sponsored healthcare benefit programs are more than a financial perk; they are a vital component of modern employment relationships. By reducing medical costs, attracting talent, enhancing productivity, and fostering a culture of care, these programs create value for both employees and employers. While challenges persist, the continued evolution of healthcare benefits promises to strengthen their role in shaping healthier, more resilient workplaces. Ultimately, the success of these programs lies in their ability to balance economic realities with the human need for security and well-being.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd and Copilot A.I.

***

***

The Baylor method of nurse payments is a scheduling and compensation model that allows nurses to work weekend shifts while receiving full-time pay and benefits, offering flexibility and helping healthcare facilities address staffing shortages.

The Baylor method, also known as the Baylor Plan or Baylor Shift, originated at Baylor University Medical Center in Dallas, Texas, as a strategic response to nurse shortages and burnout. It was designed to retain experienced nurses by offering a more flexible work schedule that still met the demands of patient care. Under this model, nurses typically work two 12-hour shifts on the weekend—Saturday and Sunday—and receive compensation equivalent to a full 40-hour workweek.

This approach has become increasingly popular in hospitals, long-term care facilities, and other healthcare settings. The core idea is simple: by concentrating work hours into the weekend, nurses gain more time off during the week while employers maintain adequate staffing during traditionally hard-to-fill shifts. For many nurses, this arrangement provides a better work-life balance, allowing them to pursue education, spend time with family, or take on additional employment during the week.

***

***

Financially, the Baylor method is attractive to both nurses and employers. Nurses benefit from full-time pay and benefits—including health insurance, retirement contributions, and paid time off—while only working two days per week. Employers, on the other hand, can reduce turnover and improve weekend staffing without increasing overall labor costs. Some facilities even offer Baylor shifts with added incentives, such as shift differentials or bonuses, to further encourage weekend coverage.

However, the Baylor method is not without its challenges. Working two consecutive 12-hour shifts can be physically and emotionally demanding, especially in high-acuity units. Nurses may experience fatigue or burnout if they are not adequately supported. Additionally, because Baylor nurses are paid for 40 hours while only working 24, scheduling extra shifts during the week can complicate overtime calculations. Typically, overtime pay only kicks in after 40 actual hours worked, not hours paid, which can lead to confusion or dissatisfaction if not clearly communicated.

From an operational standpoint, the Baylor method helps facilities maintain consistent staffing levels during weekends, which are often underserved due to lower availability of part-time or weekday-only staff. It also allows for more predictable scheduling and can improve patient outcomes by ensuring continuity of care. Facilities that adopt the Baylor model often report higher nurse satisfaction and retention rates.

In conclusion, the Baylor method of nurse payments is a creative and effective solution to some of the most persistent challenges in healthcare staffing. By offering full-time compensation for weekend work, it provides nurses with flexibility and financial stability while helping facilities maintain high-quality care. As healthcare continues to evolve, models like the Baylor shift demonstrate the importance of innovative scheduling strategies that support both caregivers and patients.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Level-funded health care is an increasingly popular option for small to mid-sized businesses seeking a balance between cost control and comprehensive employee coverage. It blends features of fully insured and self-funded health plans, offering employers greater flexibility and potential savings while minimizing risk.

In a traditional fully insured plan, employers pay a fixed premium to an insurance carrier, which assumes all financial risk for employee claims. In contrast, self-funded plans allow employers to pay for claims out-of-pocket, which can lead to significant savings—but also exposes them to unpredictable costs. Level-funded plans sit between these two models, offering a structured and predictable approach to self-funding.

With level-funded health care, employers pay a fixed monthly amount that covers three components: estimated claims funding, stop-loss insurance, and administrative fees. The estimated claims portion is based on actuarial data and reflects the expected health care usage of the employee group. Stop-loss insurance protects the employer from catastrophic claims by capping their financial exposure. Administrative fees cover third-party services such as claims processing and customer support.

One of the key advantages of level-funded plans is the potential for cost savings. If actual claims fall below the estimated amount, employers may receive a refund or credit at the end of the year. This incentivizes wellness programs and preventive care, as healthier employees lead to lower claims. Additionally, level-funded plans often provide more transparency into claims data, allowing employers to better understand health trends and make informed decisions about benefits.

***

***

Another benefit is flexibility. Level-funded plans can be customized to suit the needs of a specific workforce, offering a range of coverage options and provider networks. This contrasts with the rigid structure of many fully insured plans. Employers also gain more control over plan design, which can help attract and retain talent in competitive job markets.

However, level-funded health care is not without challenges. It requires careful planning and a solid understanding of risk. Employers must be prepared for the possibility that claims may exceed projections, although stop-loss insurance helps mitigate this. Additionally, level-funded plans may not be suitable for very small groups or those with high-risk populations, as the cost of stop-loss coverage can be prohibitive.

Regulatory considerations also play a role. Level-funded plans are typically governed by federal ERISA laws rather than state insurance regulations, which can affect compliance and reporting requirements. Employers should work closely with benefits consultants or brokers to ensure they understand the legal landscape and choose a plan that aligns with their goals.

In conclusion, level-funded health care offers a compelling alternative for businesses seeking to manage costs while providing quality coverage. By combining predictability with the potential for savings and customization, it empowers employers to take a more active role in their health benefits strategy. As the health care landscape continues to evolve, level-funded plans are likely to remain a valuable option for organizations looking to strike the right balance between affordability and employee well-being.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

In the evolving landscape of digital health care, Amazon Pharmacy and GoodRx have emerged as two leading platforms offering consumers affordable and convenient access to prescription medications. While both aim to simplify the process of obtaining prescriptions, they differ significantly in their approach, pricing models, and user experience.

Amazon Pharmacy, launched in 2020, is a full-service online pharmacy that allows customers to order medications directly through Amazon. It offers fast, free delivery for Prime members and integrates with most insurance plans. One of its standout features is RxPass, a subscription service available to Prime members for $5 per month, which covers unlimited eligible generic medications. This model is particularly attractive to individuals who take multiple generics regularly, as it can significantly reduce out-of-pocket costs.

In contrast, GoodRx, founded in 2011, operates primarily as a price comparison and discount platform. It does not dispense medications itself but partners with local and mail-order pharmacies to help users find the lowest prices. GoodRx provides coupons that can be used at thousands of pharmacies nationwide, often resulting in substantial savings—especially for those without insurance. It also offers GoodRx Gold, a paid membership that unlocks deeper discounts and telehealth services.

***

***

When comparing the two, pricing transparency is a key differentiator. GoodRx excels in showing users a range of prices across different pharmacies, empowering them to choose the most cost-effective option. Amazon Pharmacy, while competitive, typically offers fixed prices and focuses more on convenience and integration with its broader ecosystem.

Convenience is another area where Amazon Pharmacy shines. With its streamlined ordering process, automatic refills, and integration with Amazon’s delivery network, it appeals to users who prioritize ease and speed. GoodRx, while convenient in its own right, requires users to present coupons at the pharmacy or use mail-order services, which may involve more steps.

Insurance compatibility also varies. Amazon Pharmacy accepts most major insurance plans, making it a viable option for insured individuals. GoodRx, on the other hand, is often used by those without insurance or with high deductibles, as its discounts can sometimes beat insurance copays.

However, both platforms have limitations. Amazon Pharmacy’s RxPass is restricted to generic medications and excludes certain states due to regulatory issues. GoodRx’s discounts may not apply to all medications, and prices can fluctuate depending on location and pharmacy.

In terms of user experience, Amazon offers a seamless, tech-driven interface with customer support and medication management tools. GoodRx provides educational resources, price alerts, and a mobile app that helps users track savings and prescriptions.

Ultimately, the choice between Amazon Pharmacy and GoodRx depends on individual needs. For those seeking a one-stop solution with predictable costs and fast delivery, Amazon Pharmacy may be ideal. For users who want to shop around for the best deal or lack insurance, GoodRx offers unmatched flexibility and savings.

As digital health continues to grow, both platforms are reshaping how Americans access medications—making prescriptions more affordable, transparent, and accessible than ever before.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Classic: Acute care is a branch of secondary health care where a patient receives active but short-term treatment for a severe injury or episode of illness, an urgent medical condition, or during recovery from surgery. In medical terms, care for acute health conditions is the opposite from chronic care, or longer term care.

Modern: Acute care is active, short-term treatment for a severe injury or episode related to illness, an urgent medical condition or recovery from surgery.

Posted on October 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A. I.

***

***

Value-Based Medical Care: A Paradigm Shift in Healthcare

In recent years, the healthcare industry has undergone a transformative shift from volume-driven services to outcome-focused care. This evolution is embodied in the concept of value-based medical care, a model that emphasizes delivering high-quality healthcare while controlling costs and improving patient outcomes. Unlike traditional fee-for-service systems, which reward providers for the quantity of services rendered, value-based care aligns incentives with the value of care provided—measured by patient health outcomes relative to the cost of achieving them.

Core Principles of Value-Based Care

At its heart, value-based medical care is built on several foundational principles:

Patient-Centeredness: Care is tailored to individual needs, preferences, and values, promoting shared decision-making and holistic treatment.

Quality Over Quantity: Providers are rewarded for improving health outcomes, reducing hospital readmissions, and preventing disease rather than performing more procedures.

Integrated Care Delivery: Coordination among healthcare professionals ensures seamless transitions between services, reducing fragmentation and duplication.

Data-Driven Accountability: Performance metrics and health analytics guide clinical decisions and track progress toward better outcomes.

Cost Efficiency: By focusing on prevention and effective management of chronic conditions, value-based care aims to reduce unnecessary spending.

Benefits for Patients and Providers

For patients, value-based care offers a more personalized and proactive approach to health. It encourages preventive screenings, chronic disease management, and wellness programs that lead to longer, healthier lives. Providers benefit from shared savings programs, performance bonuses, and stronger relationships with their patients. Moreover, healthcare systems can allocate resources more effectively, reducing waste and improving overall population health.

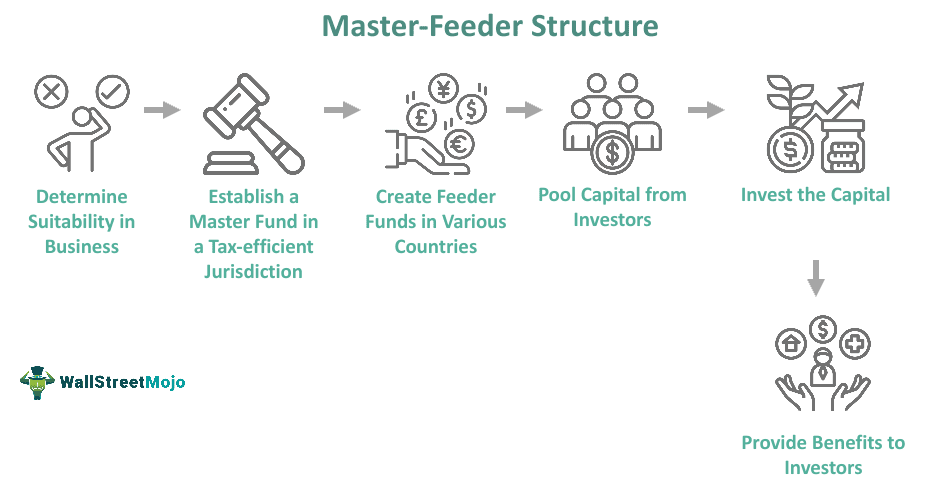

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

The hedge fund manager I am considering also runs an offshore fund under a “master feeder” arrangement.

A PHYSICIAN’S QUESTION:What does this mean? In which fund should I invest?

The master feeder arrangement is a two-tiered investment structure whereby investors invest in the feeder fund. The feeder fund in turn invests in the master fund. The master fund is therefore the one that is actually investing in securities. There may be multiple feeder funds under one master fund. Feeder funds under the same master can differ drastically in terms of fees charged, minimums required, types of investors, and many other features – but the investment style will be the same because only the master actually invests in the market.

A master feeder structure is a very popular arrangement because it allows a portfolio manager to pool both onshore and offshore assets into one investment vehicle (the master fund) that allocates gains and losses in an asset-based, proportional manner back to the onshore and offshore investors. All investors, both offshore and onshore, get the same return. In this manner, the portfolio manager, despite offering more than one fund with different characteristics to different populations, is not faced with the dilemma of which fund to favor with the best investment ideas.

A manager may offer an offshore fund because there is demand for that manager’s skill either abroad, where investors may wish to preserve anonymity, or more commonly where investors simply do not wish to become entangled with the United States tax code. American citizens should generally avoid the offshore fund, since American citizens are taxed on their allocated share of offshore corporation profits whether or not a distribution occurs. Therefore, there is no benefit for most American taxpayers investing in an offshore fund.

Tax-exempt institutions, such as medical foundations, in the United States may have reason to consider an offshore hedge fund, however. Domestic tax-exempt organizations are generally not subject to unrelated business taxable income (UBTI) – the portion of hedge fund income that comes about as a result of the use of leverage – when investing with an offshore corporation. If the same tax-exempt organization were to invest in a domestic fund, and if UBTI was generated, then the organization would have to pay taxes on that UBTI. Most domestic hedge funds generate UBTI.

Classic: A pre-payment plan refers to health insurance plans that provide medical or hospital benefits in service rather than dollars, such as the plans offered by various Health Maintenance Organizations. A method providing in advance for the cost of predetermined benefits for a population group, through regular periodic payments in the form of premiums, dues, or contributions including those contributions that are made to a health and welfare fund by employers on behalf of their employees!

Modern: A Prepaid Group Practice Plan specifies health services are rendered by participating physicians to an enrolled group of persons, with a fixed periodic payment made in advance by (or on behalf of) each person or family. If a health insurance carrier is involved, a contract to pay in advance for the full range of health services to which the insured is entitled under the terms of the health insurance contract.

Examples:

Pre-Paid Hospital Service Plan: The common name for a health maintenance organization (HMO), a plan that provides comprehensive health care to its members, who pay a flat annual fee for services.

Pre-Paid Premium: An insurance or other premium payment paid prior to the due date. In insurance, payment by the insured of future premiums, through paying the present (discounted) value of the future premiums or having interest paid on the deposit.

Pre-Paid Prescription Plan: A drug reimbursement plan that is paid in advance.

[An Internet WIKI CROWD-SOURCED Curation Project]*

To keep up with the ever-changing healthcare industrial complex, we must learn new definitions and re-learn old terminology in order to correctly apply it to practice. By aggregating the most up-to-date abbreviations, acronyms, definitions and terms, the Health DictionarySeries offers a wealth of information to help understand the ever-changing terms-of-art in healthcare today.

Each 10,000 item handbook is essential for doctors, nurses, benefits managers and insurance agents, CPAs, and administrators; as well as graduate and under graduate students and professors. Our goal to for each dictionary to be designated as a Doody’s Core Title.

Dictionary of Health Insurance and Managed Care

With more than 8,000 definitions, 4,000 abbreviations and acronyms, and a 3,000 item oeuvre of resources, readings, and nomenclature derivatives, this dictionary covers the Medicare, managed care and Medicaid, private insurance, Veteran’s Administration and PP-ACA language of the entire health and long-term care insurance sector.

Dictionary of Health Economics and Finance

Health economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, mathematics, the actuarial sciences, stochastics and statistics, salary reimbursements, physician payments, compensation and forecasting are all commingled arenas.

Dictionary of Health Information Technology Security

There is a myth that all healthcare stakeholders understand the meaning of information technology jargon. In truth, the vernacular of contemporary systems is unique, and often misused or misunderstood. Moreover, emerging Heath Information Technology (HIT) thru the HITECG initiatives; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert in a position of maximum uncertainty and minimum productivity.

*NOTE: A wiki website allows users to add or update content using their browser thru a hosted server created by the collaborative effort of site visitors. The Hawaiian term “wiki wiki” means “super fast.”

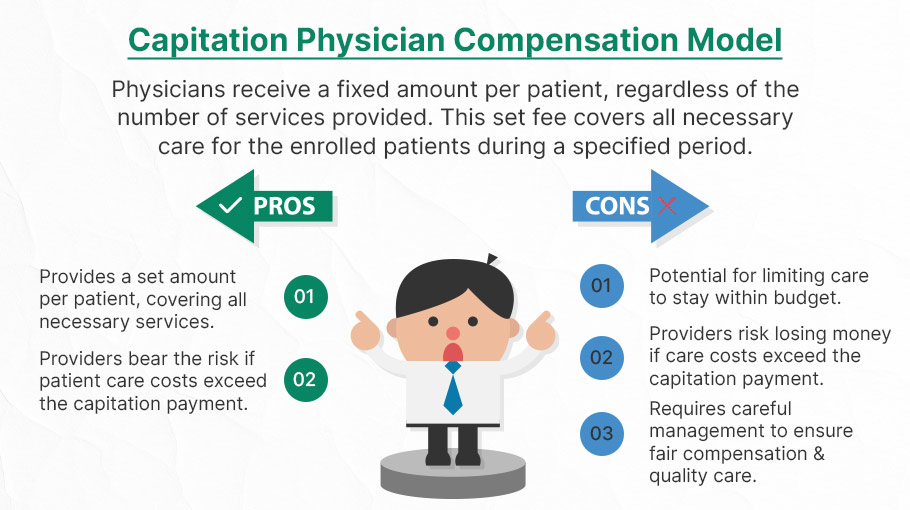

Capitation is a type of healthcare payment system in which a physician or hospital is paid a fixed amount of money per patient for a prescribed period by an insurer or physician association. The cost is based on the expected healthcare utilization costs for a group of patients for that year.

With capitation, the physician—otherwise known as the primary care physician— is paid a set amount for each enrolled patient whether a patient seeks care or not. The PCP is usually contracted with an HMO whose role it is to recruit patients.

According to Richard Eskow, CEO of Health Knowledge Systems of Los Angeles, capitated medical reimbursement has been used in one form or another, in every attempt at healthcare reform since the Norman Conquest. Some even say an earlier variant existed in ancient China [personal communication].

Initially, when Henry I assumed the throne of the newly combined kingdoms of England and Normandy, he initiated a sweeping set of healthcare reforms. Historical documents, though muddled, indicate that soon thereafter at least one “physician,” John of Essex, received a flat payment honorarium of one penny per day for his efforts. Historian Edward J. Kealey opined that sum was roughly equal to that paid to a foot-soldier or a blind person. Clearer historical evidence suggests that American doctors in the mid-19th century were receiving capitation-like payments. No less an authoritative figure than Mark Twain, in fact, is on record as saying that during his boyhood in Hannibal, MO his parents paid the local doctor $25/year for taking care of the entire family regardless of their state of health.

Later, Sidney Garfield MD [1905-1984] is noted as one of the great under-appreciated geniuses of 20th century American medicine stood in the shadow cast by his more celebrated partner, Henry J. Kaiser. Garfield was not the first physician to embrace the notion of prepayment capitation, nor was he the first to understand that physicians working together in multi-specialty groups could, through collaboration and continuity of care, outperform their solo practice colleagues in almost every measure of quality and efficiency. The Mayo brothers, of course, had prior claim to that distinction. What Garfield did, was marry prepayment to group practice, providing aligned financial incentives across every physician and specialty in his medical group, as well as a culture of group accountability for the care of every member of the affiliated health plan. He called it “the new economics of medicine,” and at its heart was a fundamentally new paradigm of care that emphasized – prevention before treatment – and health before sickness. Under his model: the fewer the sick – the greater the remuneration. And: the less serious the illness, the better off the patient and the doctors.

Such ideas were heresy to the reigning fee-for-service, solo practice, ideologues of the mainstream medical establishment of the 1940s and ‘50s, of course. Throughout the period, Garfield and his group physicians were routinely castigated by leaders of the AMA and county medical associations as socialistic and unethical. The local medical associations in Garfield’s expanding service areas – the San Francisco Bay Area, Los Angeles, and Portland, Oregon – blocked group practice physicians from association membership, effectively shutting them out of local hospitals, denying them patient referrals or specialty society accreditation. Twice in the 1940s, formal medical association charges were brought against Garfield personally, at one time temporarily succeeding in suspending his license to practice medicine.

Of course, capitation payments made a comeback in the first cost-cutting managed care era of the 1980-90s because fee-for-service medicine created perverse incentives for physicians by paying more for treating illnesses and injuries than it does for preventing them — or even for diagnosing them early and reducing the need for intensive treatment later. Nevertheless, the modern managed care industry’s experience with capitation wasn’t initially a good one. The 1980-90s saw a number of HMOs attempt to put independent physicians, especially primary care doctors, into a capitation reimbursement model. The result was often negative for patients, who found that their doctors were far less willing to see them — and saw them for briefer visits — when they were receiving no additional income for their effort. Attempts were also made to aggregate various types of health providers — including hospitals and physicians in multiple specialties — into “capitation groups” that were collectively responsible for delivering care to a defined patient group. These included healthcare facilities and medical providers of all types: physicians, osteopaths, podiatrists, dentists, optometrists, pharmacies, physical therapists, hospitals and skilled nursing homes, etc.

However, the healthcare industry isn’t collective by nature, and these efforts tended to be too complicated to succeed. One lesson that these experiments taught is that provider behavior is difficult to change unless the relationship between that behavior and its consequences is fairly direct and easy to understand.

Today, the concept of prepayment and medical capitation is to uncouple compensation from the actual number of patients seen, or treatments and interventions performed. This is akin to a fixed price restaurant menu, as opposed to an àla carte eatery.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITIONS

By Staff Reporters

***

***

Rate Review & the 80/20 Rule

The health care law provides 2 ways to hold insurance companies accountable and help keep your costs down: Rate Review and the 80/20 rule.

Rate Review

Rate Review helps protect you from unreasonable rate increases. Insurance companies must now publicly explain any rate increase of 15% or more before raising your premium. This does not apply to grandfathered plans.

The 80/20 Rule generally requires insurance companies to spend at least 80% of the money they take in from premiums on health care costs and quality improvement activities. The other 20% can go to administrative, overhead, and marketing costs.

The 80/20 rule is sometimes known as Medical Loss Ratio, or MLR. If an insurance company uses 80 cents out of every premium dollar to pay for your medical claims and activities that improve the quality of care, the company has a Medical Loss Ratio of 80%.

Insurance companies selling to large groups (usually more than 50 employees) must spend at least 85% of premiums on care and quality improvement.

If your insurance company doesn’t meet these requirements, you’ll get a rebate on part of the premium that you paid.

Will I get a rebate check from my insurance company?

If your insurance company doesn’t meet its 80/20 targets for the year, you’ll get back some of the premium that you paid.

You may see the rebate in a number of ways:

A rebate check in the mail

A lump-sum deposit into the same account that was used to pay the premium, if you paid by credit card or debit card

A direct reduction in your future premium

Your employer may also use one of the above rebate methods, or apply the rebate in a way that benefits employees

If you or your employer will get a rebate, your insurance company must notify you by August 1.

If you have an individual insurance policy, you’ll get the rebate directly from your insurance company.

For small group and large group plans, the rebate is usually paid to the employer. It may use one of the above rebate methods, or apply the rebate in a way that benefits employees.

FYI: The 80/20 rebate rules don’t apply when an insurance company has fewer than 1000 enrollees in a particular state or market.

For Rate Review: These requirements don’t apply to grandfathered plans. Check your plan’s materials or ask your employer or your benefits administrator to find out if your health plan is grandfathered.

For the 80/20 Rule: These rights apply to all individual, small group, and large group health plans, whether your plan is grandfathered or not.

Classic: The portion of medical expenses a patient is responsible for paying.

Modern: Refers to the maximum you will pay during your policy period, which is typically a year, before your plan starts to pay 100% of your allowed amount. The costs of your deductible, co-pay, and co-insurance are included here, but not your premium.

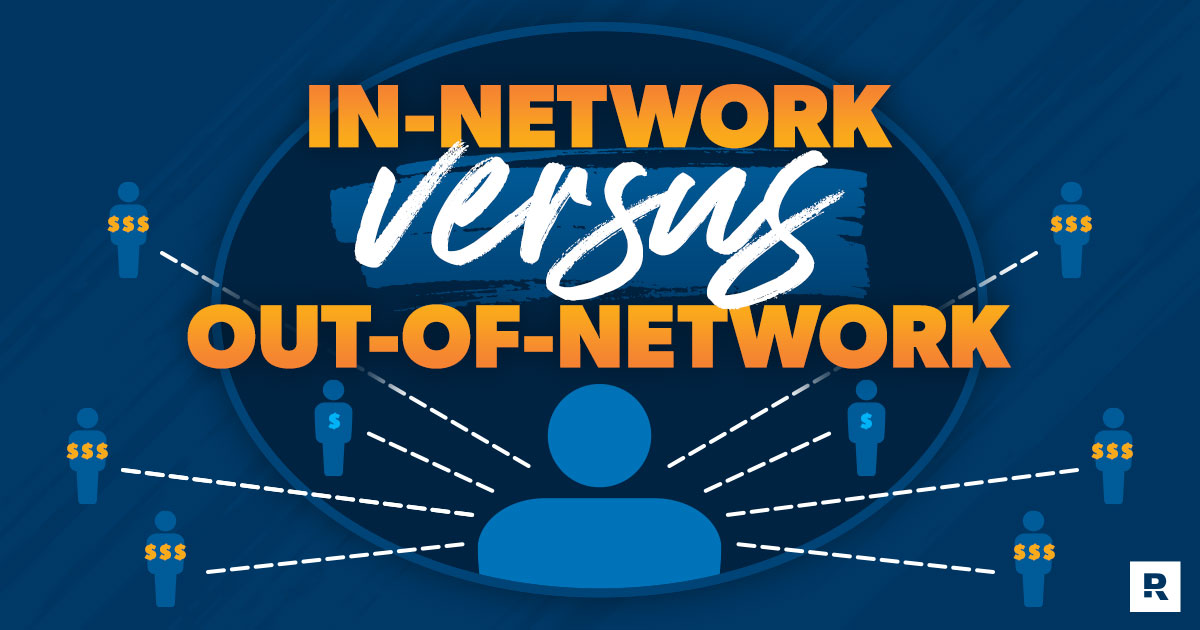

Classic: “Out-of-network” health care providers do not have an agreement with your insurance company to provide care. While insurance companies may have some out-of-network benefits, medical care from an out-of-network provider will usually cost more out-of-pocket than an in-network provider.

Modern: The amount that a health care insurance plan will contribute toward out-of-network services will vary by your insurance company and is often based on a “reasonable and customary” amount that the service should cost

Example: If you go to an out-of-network dentist and are billed $300 for the service, your insurance company may contribute $200 toward paying this cost because $200 is the amount it has decided is “reasonable and customary” for this service. When out-of-network, any remaining cost above this amount ($100 in this case) may have to be fully covered by the person receiving care. When out-of-network, the usual coinsurance rates that apply in-network may not apply out-of-network. Additionally, out-of-network service costs may not count toward an annual deductible.

If an insurer uses 80 cents out of every premium dollar to pay its customers’ medical claims and activities that improve the quality of care, the company has a medical loss ratio of 80%. A medical loss ratio of 80% indicates that the insurer is using the remaining 20 cents of each premium dollar to pay overhead expenses, such as marketing, profits, salaries, administrative costs, and agent commissions.

The Affordable Care Act sets minimum medical loss ratios for different markets, as do some state laws.

Posted on August 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL PROVIDER PAYMENTS LOWERED

***

***

Statistic: $2.8+ billion dollars

That’s how much Blue Cross and Blue Shield plans agreed to pay to settle litigation over claims they conspired to lower payments to providers. (Healthcare Dive)

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A silent, non-directed, ghost, blind, faux, or “mirror” PPO, HMO, or other provider model is not really a formalized managed care organization [MCO] at all. Rather, it was simply an intermediary attempt, and Ponzi-like scheme, to negotiate practitioner fees downward, by promising a higher volume of patients in exchange for the discount.

Of course, the intermediary [discount-broker] then resells the packaged contract product to any willing insurance company, HMO, PPO or other payer, thereby pocketing the difference as a nice profit. Sometime, these virtual organizations are just indemnity companies in disguise.

NOTE: The term indemnity insurance refers to an insurance policy that compensates an insured party for certain unexpected damages or losses up to a certain limit—usually the amount of the loss itself. Insurance companies provide coverage in exchange for premiums paid by the insured parties.

These policies are commonly designed to protect professionals and business owners when they are found to be at fault for a specific event such as misjudgment or malpractice. They generally take the form of a letter o indemnity.

***

As part of a silent PPO scheme, insurers try to pass off the discount as legitimate on Explanation of Benefit [EOB] forms. Physicians should not fall for this ploy, since pricing pressure will be forced even lower in the next round of “real” PPO negotiations!

Medical providers should also be on guard for silent HMOs, MCOs and any other silent insurance variation, since these virtual organizations do not exist, except as exploitable arbitrage situations for the middleman.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Doctors and dentists earn money by treating patients. CPAs and Attorneys have clients, and retail stores buy items low and sell them at higher prices. This is called a business model.

More formally, a business model identifies the products or services the business plans to sell, the target market, and any anticipated expenses, in order to outline how to generate a profit. Business models are important for both new and established businesses. They help companies attract investment, recruit talent, and motivate management and staff.

Businesses should regularly update their business model, or they’ll fail to anticipate trends and challenges ahead. Business models also help investors to evaluate companies that interest them and employees to understand the future of a company they may aspire to join.

***

The Business Model of Pharmacy Benefits Managers

In the United States, health insurance providers often hire a third party to handle price negotiations, insurance claims, and distribution of prescription drugs. Providers that use such pharmacy benefit managers include commercial health plans, self-insured employer plans, Medicare Part D [drug] plans, the Federal Employees Health Benefits Program, and state government employee plans. PBMs are designed to aggregate the collective buying power of en-rollees through their client health plans, enabling plan sponsors and individuals to obtain lower prices for their prescription drugs. PBMs negotiate price discounts from retail pharmacies, rebates from pharmaceutical manufacturers, and mail-service pharmacies which home-deliver prescriptions without consulting face-to-face with a pharmacist.

Pharmacy benefit management companies can make revenue in several ways.

First, they collect administrative and service fees from the original insurance plan.

Then, they can also collect rebates from the manufacturer.

Traditional PBMs do not disclose the negotiated net price of the prescription drugs, allowing them to resell drugs at a public list price (also known as a sticker price), which is higher than the net price they negotiate with the manufacturer. This practice is known as “spread pricing”. The industry argues that savings are trade secrets. Pharmacies and insurance companies are often prohibited by PBMs from discussing costs and reimbursements. This leads to lack of transparency.

***

***

Therefore, states are often unaware of how much money they lose due to spread pricing, and the extent to which drug rebates are passed on to en-rollees of Medicare plans. In response, states like Ohio, West Virginia, and Louisiana have taken action to regulate PBMs within their Medicaid programs.

For instance, they have created new contracts that require all discounts and rebates to be reported to the states. In return, Medicaid pays PBMs a flat administrative fee.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Insurers selling plans on ACA exchanges are expected to hike premiums next year as subsidies on them are set to expire, with the average person expected to be paying 75% more, according to an analysis from the nonpartisan research group KFF.

One Big Beautiful Bill Act (OBBBA; OBBB; BBB), or the Big Beautiful Bill, is a budget reconciliation bill in the 119th US Congress.

Hospitals are not happy with the health care provisions of the bill, which would reduce the support they receive from states to care for Medicaid enrollees and leave them with more uncompensated care costs for treating uninsured patients.

“The real-life consequences of these nearly $1 trillion in Medicaid cuts – the largest ever proposed by Congress – will result in irreparable harm to our health care system, reducing access to care for all Americans and severely undermining the ability of hospitals and health systems to care for our most vulnerable patients,” said Rick Pollack, CEO of the American Hospital Association.

The association said it is “deeply disappointed” with the bill, even though it contains a $50 billion fund to help rural hospitals contend with the Medicaid cuts, which hospitals say is not nearly enough to make up for the shortfall.

Posted on June 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A June 11th report from global professional services firm Alvarez & Marsal (A&M) predicts that more beneficiaries might soon ditch insurance coverage for options like short-term, limited duration plans or healthcare sharing ministries (HCSMs), which aren’t regulated like health insurance and aren’t required to comply with ACA protections like covering maternity care or pre-existing conditions.

Nvidia extended its winning streak to five days, rising another 1.73% as the AI trade continues to recover.

EchoStar climbed 13.16% after the parent company of Dish TV disclosed that President Trump did in fact prod the FCC to make a deal.

Cyngn soared another 20.07% following a big day of gains after the company that makes self-driving tech for industrial vehicles announced a partnership with Nvidia.

Strong earnings from Nike (more on that later) propelled sporting goods stocks higher today. ONHoldings rose 1.74%, while Dick’s Sporting Goods climbed 3.59%.

Domestic power producers popped on reports that Trump is planning to issue an executive order increasing energy production to meet AI demand. Vistra gained 2.44%, GE Vernova climbed 2.54%, and Vertiv added 2.71%.

What’s down

Coinbase Global ended its winning streak, tumbling 5.77% after GENIUS Act hype propelled the crypto stock skyward all week long. Traders took profits in Circle as well, pushing the stablecoin stock down 15.54%.

Chinese EV maker LiAuto fell 1.93% on its weaker-than-expected deliveries forecast for the second quarter.

Fellow Chinese EV maker Xiaomi stunned markets with reports that it received 240,000 orders for its new SUV within 18 hours of its debut, but shares still sank 4%.

Pony.ai lost 6.31% on a report that Uber is considering helping its founder Travis Kalanick fund his acquisition of the US subsidiary of the Chinese autonomous vehicle company.

Gold miners tumbled while the price of the precious metal fell as investors took a risk-on stance. Newmont lost 4.11%, BarrickMining fell 3.44%, and KinrossGold shed 6.18%.

Today’s trade deal reopens the door for Chinese rare earth imports, bad news for US producers like MPMaterials (down 8.59%) and USA Rare Earth (down 12.14%).

Consumer Fraud in the Health Insurance Marketplace

Don’t be a Victim of Consumer Fraud in the Health Care Marketplace

Beware of…

People asking for money to enroll you in Marketplace or “Obamacare” insurance. Legitimate enrollment agents will NOT ask for money.

High-pressure visits, mail solicitations, e-mails, and phone calls from people pretending to work for the government. No one should threaten you with legal action if you do not sign up for a plan. Always ask for identification if someone comes to your door.

People you did not contact who request personal information. They may be trying to steal your identity. No one from the government will call or email you to sell you an insurance plan or ask for personal identifying information. Be careful when giving out personal information, such as credit card, banking, or Social Security numbers.

Sham websites. Always look for official government seals, logos or website addresses.

Note: If you are a Medicare beneficiary, you do NOT need to buy insurance in the new Health Insurance Marketplace.

Posted on May 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Health Insurance Co-Payments Upfront or Lose Your Appointment

Definition: A co-payment is a fixed amount you pay each time you get a particular type of healthcare service, and co-pays will generally be quite a bit smaller than deductibles. However, deductibles and co–pays are both fixed amounts, as opposed to coinsurance, which is a percentage of the claim.

On some health plans, certain services are covered with a co-pay before you’ve met the deductible, while other health insurance plans have co-pays only after you’ve met your deductible. And, the pre-deductible versus post-deductible co-pay rules often vary based on the type of medical service you’re receiving.

Starting in June 2025, Cleveland Clinic patients who can’t pay their co-pay on the spot will have non-emergency appointments rescheduled or cancelled. This new policy could make it harder for low-income people who prefer to be billed to see a clinic doctor, and create delays that could lead to medical emergencies down the road.

For example, a delay in care can mean six to eight more weeks of a tumor growing or a blood clot developing or an infection brewing.

Posted on May 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Oak Street Health, headquartered in Chicago and a wholly-owned subsidiary of CVS Health since 2023, has agreed to pay $60 million to resolve allegations that it violated the False Claims Act by paying kickbacks to third-party insurance agents in exchange for recruiting seniors to Oak Street Health’s primary care clinics.

The Anti-Kickback Statute prohibits anyone from offering or paying, directly or indirectly, any remuneration — which includes money or any other thing of value — to induce referrals of patients or to provide recommendations of items or services covered by Medicare, Medicaid and other federally funded programs. Under the Medicare Advantage (MA) Program, also known as Part C, Medicare beneficiaries have the option to obtain their health care through privately-operated insurance plans known as MA plans. Some MA Plans contract with health care providers, including Oak Street Health, to provide their plan members with primary care services.