Psychological Biases Affecting Financial Planning and Investing

By Dr. David Edward Marcinko MBA MEd CMP®

http://www.MarcinkoAssociates.com

[Editor-in-Chief]

Sponsored: http://www.CertifiedMedicalPlanner.org

The following are some of the most common psychological biases. Some are learned while others are genetically determined (and often socially reinforced). While this essay focuses on the financial implications of these biases, they are prevalent in most areas in life.

[A] Incentives

It is broadly accepted that incenting someone to do something is effective, whether it be paying office staff a commissions to sell more healthcare products, or giving bonuses to office employees if they work efficiently to see more HMO patients. What is not well understood is that the incentives cause a sub-conscious distortion of decision-making ability in the incented person. This distortion causes the affected person – whether it is yourself or someone else – to truly believe in a certain decision, even if it is the wrong choice when viewed objectively. Service professionals, including financial advisors and lawyers, are affected by this bias, and it causes them to honestly offer recommendations that may be inappropriate, and that they would recognize as being inappropriate if they did not have this bias. The existence of this bias makes it important for each one of us to examine our incentive biases and take extra care when advising physician clients, or to make sure we are appropriately considering non-incented alternatives.

[B] Denial

Denial is a well known, but under-appreciated, psychological force. Physicians, clients and professionals (like everyone else) are prone to the mistake of ignoring a painful reality, like putting off an unpleasant call (thus prolonging a problematic situation and potentially making it worse) or not opening account statements because of the desire not to see quantitative proof of losses. Denial also manifests itself by causing human beings to ignore evidence that a mistake has been made. If you think of yourself as a smart person (and what professional doesn’t?), then evidence pointing to the conclusion that a mistake has been made will call into question that belief, causing cognitive dissonance. Our brains function to either avoid cognitive dissonance or to resolve it quickly, usually by discounting or rationalizing the disconfirming evidence. Not surprisingly, colleagues at Kansas State University and elsewhere, found that financial denial, including attempts to avoid thinking about or dealing with money, is associated with lower income, lower net worth, and higher levels of revolving credit.

[C] Consistency and Commitment Tendency

Human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks. In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”. Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake. It is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect. Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

[D] Pattern Recognition

On a biological level, the human brain has evolved to seek out patterns and to work on stimuli-response patterns, both native and learned. What this means is that we all react to something based on our prior experiences that had shared characteristics with the current stimuli. Many situations have so many possible inputs that our brains need to take mental short cuts using pattern recognition we would not gain the benefit from having faced a certain type of problem in the past. This often-helpful mechanism of decision-making fails us when past correlations or patterns do not accurately represent the current reality, and thus the mental shortcuts impair our ability to analyze a new situation. This biologic and social need to seek out patterns that can be used to program stimuli-response mechanisms is especially harmful to rational decision-making when the pattern is not a good predictor of the desired outcome (like short term moves in the stock market not being predictive of long term equity portfolio performance), or when past correlations do not apply anymore.

[E] Social Proof

It is a subtle but powerful reality that having others agree with a decision one makes, gives that person more conviction in the decision, and having others disagree decreases one’s confidence in that decision. This bias is even more exaggerated when the other parties providing the validating/questioning opinions are perceived to be experts in a relevant field, or are authority figures, like people on television. In many ways, the short term moves in the stock market are the ultimate expression of social proof – the price of a stock one owns going up is proof that a lot of other people agree with the decision to buy, and a dropping stock price means a stock should be sold. When these stressors become extreme, it is of paramount importance that all participants in the financial planning process have a clear understanding of what the long-term goals are, and what processes are in place to monitor the progress towards these goals. Without these mechanisms it is very hard to resist the enormous pressure to follow the crowd; think social media.

[F] Contrast

Sensation, emotion and cognition work by contrast. Perception is not only on an absolute scale, it also functions relative to prior stimuli. This is why room temperature water feels hot when experienced after being exposed to the cold. It is also why the cessation of negative emotions “feels” so good. Cognitive functioning also works on this principle. So one’s ability to analyze information and draw conclusions is very much related to the context with in which the analysis takes place, and to what information was originally available. This is why it is so important to manage one’s own expectations as well as those of clients. A client is much more likely to be satisfied with a 10% portfolio return if they were expecting 7% than if they were hoping for 15%.

[G] Scarcity

Things that are scarce have more impact and perceived value than things present in abundance. Biologically, this bias is demonstrated by the decreasing response to constant stimuli (contrast bias) and socially it is widely believed that scarcity equals value. People who feel an opportunity may “pass them by” and thus be unavailable are much more likely to make a hasty, poorly reasoned decision than they otherwise would. Investment fads and rising security prices elicit this bias (along with social proof and others) and need to be resisted. Understanding that analysis in the face of perceived scarcity is often inadequate and biased may help professionals make more rational choices, and keep clients from chasing fads.

[H] Envy / Jealousy

This bias also relates to the contrast and social proof biases. Prudent financial and business planning and related decision-making are based on real needs followed by desires. People’s happiness and satisfaction is often based more on one’s position relative to perceived peers rather than an ability to meet absolute needs. The strong desire to “keep up with the Jones” can lead people to risk what they have and need for what they want. These actions can have a disastrous impact on important long-term financial goals. Clear communication and vivid examples of risks is often needed to keep people focused on important financial goals rather than spurious ones, or simply money alone, for its own sake.

[I] Fear

Financial fear is probably the most common emotion among physicians and all clients. The fear of being wrong – as well as the fear of being correct! It can be debilitating, as in the corollary expression on fear: the paralysis of analysis.

According to Paul Karasik, there are four common investor and physician fears, which can be addressed by financial advisors in the following manner:

- Fear of making the wrong decision: ameliorated by being a teacher and educator.

- Fear of change: ameliorated by providing an agenda, outline and/or plan.

- Fear of giving up control: ameliorated by asking for permission and agreement.

- Fear of losing self-esteem: ameliorated by serving the client first and communicating that sentiment in a positive manner.

Psychological Traps

Now, as human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

- Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

- Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

- Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

- Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

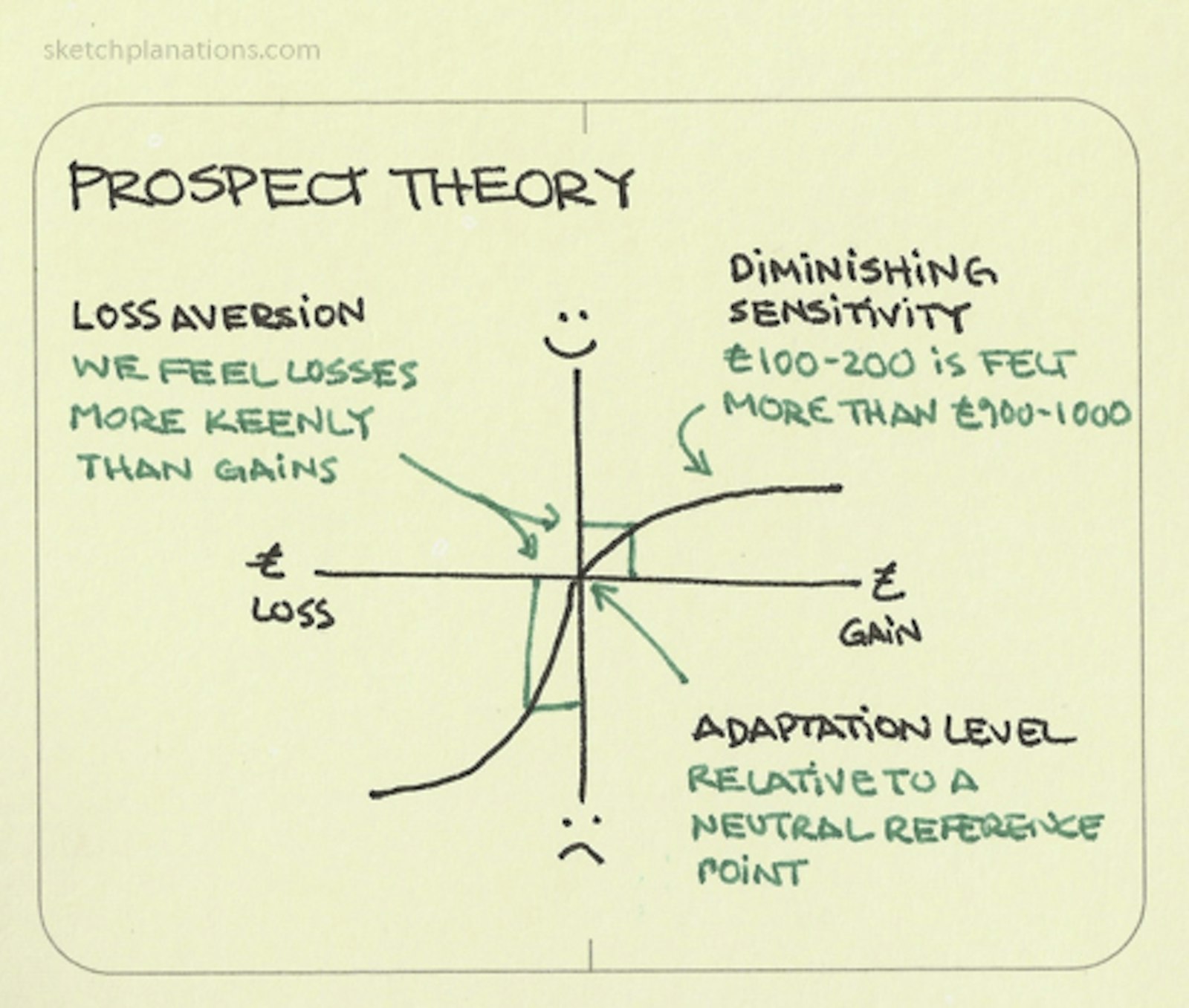

- Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

- Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under-perform the market by a significant margin over time.

- Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

- Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Textbook Order: https://www.routledge.com/Risk-Management-Liability-Insurance-and-Asset-Protection-Strategies-for/Marcinko-Hetico/p/book/9781498725989

Your thoughts are appreciated.

THANK YOU

***

Share this:

Filed under: Career Development, CMP Program, Financial Planning, iMBA, Inc., Investing, Risk Management, Touring with Marcinko | Tagged: certified medical planner, Certified Medical Planner™, CMP, CMP Program, Dr. David Marcinko, Financial Planning, investing bias, psychology | 7 Comments »