BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

If you’ve ever listened to an early morning financial news broadcast, you’ve heard a reference to “futures” and how they affect the stock market before it opens. Physicians Investors follow the futures because it provides an indication of where stocks are headed at the opening bell. One of the most widely followed futures is the Dow Futures, whose underlying value is based on the Dow Jones Industrial Average, an index of 30 major U.S. companies.

***

***

DEFINITION: After the markets close at 4 pm New York time, implied open prices of the Dow Jones Industrial Average, S&P 500 Index, and NASDAQ, which fluctuate from minute to minute, can be calculated.

Considering the DJIA as an example, the basis of calculating implied open is the price of a “DJX index option futures contract “.

The first World Financial Planning Day was held on October 4, 2017. The Financial Planning Standards Board (FPSB) hosts the day. Every year, the FPSB partners with the International Organization of Securities Commissions (IOSCO).

***

Today, it is always held during the first Wednesday of October during IOSCO’s World Investor Week.

***

QUERY: But, what about the entire ecosystem of personal and professional financial planning, investing, risk, business and medical practice management for physicians and healthcare professionals? A vital, unique and complicated niche!

ANSWER: According to the Institute of Medical Business Advisors, Inc., WFP Day is every day for CERTIFIED MEDICAL PLANNER® professional certification holders.

So – If you are in this WFPD industry – Become a fiduciary focused board CERTIFIED MEDICAL PLANNER with extreme healthcare industry ecosystem specificity.

A decentralized autonomous organization (DAO), sometimes called a decentralized autonomous corporation (DAC), is an organization represented by rules encoded as a computer program that is transparent, controlled by the organization members and not influenced by a central government. A DAO’s financial transaction record and program rules are maintained on a blockchain. The precise legal status of this type of business organization is unclear.

A well-known example, intended for venture capital funding, was The DAO, which launched with $150 million in crowdfunding in June 2016, and was nearly immediately hacked and drained of US$50 million in cryptocurrency. The hack was reversed in the following weeks, and the money restored, via a hard fork of the Ethereum blockchain: the Ethereum miners and clients switched to the new fork.

A Ponzi scheme (/ˈpɒnzi/, Italian: [ˈpontsi]) is a form of fraud that lures investors and pays profits to earlier investors with funds from more recent investors. Recall Bernie Madoff.

The scheme leads victims to believe that profits are coming from legitimate business activity (e.g., product sales or successful investments), and they remain unaware that other investors are the source of funds. A Ponzi scheme can maintain the illusion of a sustainable business as long as new investors contribute new funds, and as long as most of the investors do not demand full repayment and still believe in the non-existent assets they are purported to own.

A pyramid scheme is a business model that recruits members via a promise of payments or services for enrolling others into the scheme, rather than supplying investments or sale of products. As recruiting multiplies, recruiting becomes quickly impossible, and most members are unable to profit; as such, pyramid schemes are unsustainable and often illegal.

A cap on how much the US government can borrow to finance its operations.

It was introduced during World War I so that Congress wouldn’t have to approve every bond issuance by the Treasury Department as it had done previously—freeing up more time for name-calling.

The debt ceiling has been suspended dozens of times over the years, including 3x during the Trump administration.

Without suspending the debt ceiling, the US wouldn’t be able to borrow money to pay its bills—and things would get ugly if that happened. The federal government would have to slash spending for programs like Medicaid, local governments would find it harder to borrow, and financial markets could go haywire.

In short, a failure to act would “produce widespread economic catastrophe,” Treasury Secretary Janet Yellen wrote in the Wall Street Journal.

Important note: The debt ceiling doesn’t account for new spending, like the $3.5 trillion proposal the Democrats have on the table. Instead, it’s about spending Congress has already authorized, such as paying out Social Security. Over the years, the debt ceiling has become a “political weapon,” according to the AP, as each party tries to blame the other for their spending habits and for heaping more debt on the US.

Do your children have income-generating assets in a custodial account?

If so, be sure you understand the so-called kiddie tax.

This law was passed to discourage wealthier individuals from transferring assets to their children to take advantage of their lower tax rates. The kiddie tax has seen many iterations but current rules tax a minor child’s unearned income—including capital gains distributions, dividends, and interest income—at the parents’ tax rate if it exceeds the annual limit ($2,200 in 2021).

The tax applies to dependent children under the age of 18 at the end of the tax year (or full-time students younger than 24) and works like this:

The first $1,100 of unearned income is covered by the kiddie tax’s standard deduction, so it isn’t taxed.

The next $1,100 is taxed at the child’s marginal tax rate.

Anything above $2,200 is taxed at the parents’ marginal tax rate.

So – If your child also has earned income, say from a summer job or legitimate work in your medical office or practice, the rules become more complicated.

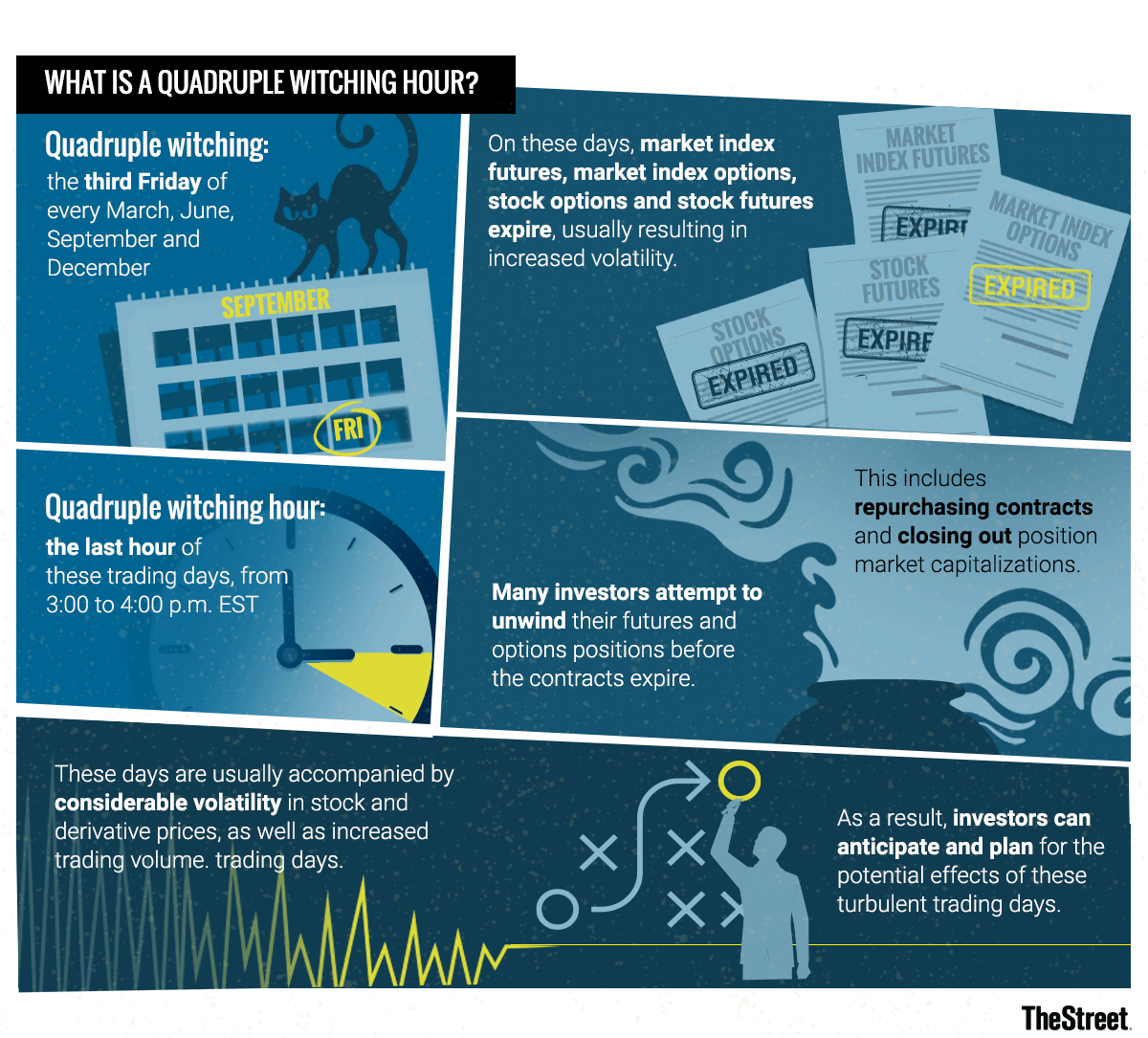

Markets: While yesterday was somewhat of a snoozefest on Wall Street, today should be more interesting. In a quarterly event known as “quadruple witching,” stock options, index options, stock futures, and index futures all expire on the same day, which can produce fireworks.

The phrase quadruple witching brings to mind stories that begin, “It was a dark and stormy night…” or folkloric visions of witches flying chaotically on broomsticks across the brightness of a moon.

In the context of investing, quadruple witching also refers to possible chaos but chaos in the financial markets. Such chaos can erupt due to four different types of contracts on financial assets expiring on the same day. The quadruple witching hour is the last hour of the trading session on that day. The question is whether investors can make abnormally robust profits on quadruple witching days due to market fluctuations.

What Is Quadruple Witching?

Quadruple witching refers to four days during the calendar year when the contracts on four different kinds of financial assets expire. The days are the third Friday of March, June, September and December. The assets on which the contracts expire on that day are stock options, single stock futures, stock index futures and stock index options. Options contracts also expire monthly. Futures contracts expire quarterly.

Because all four types of contracts expire on the same day, the quadruple witching day usually sees a heavier volume of trading. This is why the reference to chaos is made about this witching day. Market volume is increased partly due to offsetting trades that are made automatically. Volume on quadruple witching days has increased roughly two-thirds of the time since 2005.

Recent Quadruple Witching Expiration Day

On June 18, 2021, a quadruple witching day, a near-record volume of single-stock equity options was set to expire at the end of the day in the amount of $818 billion. As a result, a near-record of single stock open interest of about $3 trillion stood on June 18, 2021. Open interest refers to how many contracts are open during any given point during the day. It is an important metric for traders to watch since a large amount of open interest can move the value of the underlying stock.

In response, lawmakers are considering a broad range of policy options, including one that would allow the federal government to negotiate prescription drug prices on behalf of Medicare beneficiaries and people enrolled in private plans, a proposal that has strong bipartisan public support.

This brief describes the current status of drug price negotiation proposals, looks back at the history of proposals to give the federal government the authority to negotiate drug prices in Medicare, describes the negotiation provisions in key legislation (H.R. 3), and discusses the potential spending effects for the federal government and individuals.

Posted on September 8, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

QUICK DEFINITION – INVESTING BASICS

MUTUAL COMPANY: A company that has no capital stock or stockholders. Rather, it is owned by its policy-owners and managed by a board of directors chosen by the policy-owners.

Any earnings, in addition to those necessary for the operation of the company and contingency reserves, are returned to the policy-owners in the form of policy dividends.

STOCK COMPANY: A joint-stock company is a business entity in which shares of the company’s stock can be bought and sold by shareholders.

Each shareholder owns company stock in proportion, evidenced by their shares (certificates of ownership). Shareholders are able to transfer their shares to others without any effects to the continued existence of the company.

Posted on September 6, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

DOCTORS MUST KNOW THE DIFFERENCE

Dr. David Marcinko MBA CMP®

J. Christopher Miller; JD

HISTORY

Do you remember when Andy DuFresne confronts the chief guard of his prison in The Shawshank Redemption and tells him to divert an inherited sum of money into his wife’s name? Even sixty-five years after the 1949 setting of that conversation, a common means of protecting assets from the reach of creditors is to transfer property into a spouse’s name. Assuming that the spouse is not also at substantial risk of being the target of lawsuits because of the spouse’s profession or lifestyle, it is an effective means of accomplishing that goal. Creditors with valid judgments against an individual may only attach and seize those assets owned by that individual. Anything worth doing is worth doing right, however, and there are several pointers to structuring asset ownership in a way that maximizes its protective value.

STATES

A small number of states, such as Hawaii, Pennsylvania, and Florida, have statutes that automatically protect property jointly owned by spouses from creditors of either spouse, but often not from creditors of both spouses together. Property that benefits from this characterization is held in as a “tenancy by the entirety,” and prevents only one spouse from transferring away property that the married couple obtained together. Again, variation in state law determines just how beneficial the formation of a “tenancy by the entirety” can be from an asset protection standpoint. This protection comes from a public interest in the preservation of marital assets, such that one spouse’s indiscretion may not harm the position of the other spouse.

The most significant limits to the advantage provided by the tenancies of the entirety are first, that the creditors with claims against both spouses may seize such jointly held property, and second, that upon the first death between the spouses, the property flows directly to the surviving spouse alone, who then no longer has the benefit of the creditor protection. Moreover, in April of 2002, the U.S. Supreme Court sharply curtailed the benefit provided by tenancies by the entirety by ruling that it does not shield an asset from the federal authorities, even if the tax liability was incurred only by one spouse.[1]

Some states in the South and West are community property states, which is similar to, but not the same as, tenancy by the entirety. Under the community property theory, all property acquired by either spouse during the residency in that state (or in some states, prior to or during the residency), will be considered jointly owned property even if titled to an individual spouse. Merely by moving to one of these community property states, a person can automatically shift assets, thus reducing the quantity of assets subject to the creditors of the wealthier spouse.

PROPERTY

Community property and land owned as tenants-by-the-entirety is different from a third type of ownership called Joint Tenancy with Rights of Survivorship, sometimes abbreviated as “JTWROS”. Joint tenancy with rights of survivorship may ease some burdens associated with probating a decedent’s estate, but this form of ownership is not ideal when viewed through the asset protection prism.

An alternative is to hold assets in the name of one spouse or the other, or as “tenants-in-common.” Tenancy-in-common is best described as a situation in which each spouse owns a one-half undivided share in the property, but does not have the automatic right to full ownership at the death of the other spouse.

Three advantages flow from this form of ownership:

Neither spouse owns the property exclusively.

A creditor seizing the interest of one spouse would not have a valuable asset because it could not evict the remaining spouse, so creditors will attack these assets only as a last resort to satisfy their claims. However, a lien recorded against either fractional interest would have to be satisfied upon its sale, so that the net proceeds would be reduced by the amount of the lien. For this reason, tenancy-in-common is only a temporary means of protecting an asset from an adverse judgment, and not quite the same as fully separate ownership. This flaw is one reason why many estate planners recommend the funding of property into the name of a spouse or family member less vulnerable to adverse judgments.

If either spouse were to die, only half of the property would be subject to estate tax.

Ownership of property as tenants-in-common helps in the estate planning arena by facilitating the process of equalizing the assets held by each spouse. Changes made during 2010 and 2013 to the estate tax laws have pushed the federal estate tax exemption above $5 million, so fewer individuals (less than ½ of 1% of the general public by some estimates) will realize an actual tax savings from such planning. Even more appealing is that surviving spouses can now claim the unused exemption left behind by a deceased spouse. Estate tax concerns are now playing a much smaller role in recommending how spouses own their property.

A dying spouse has the ability to control how his or her interest is distributed.

In many simple Wills, all property of a spouse is given by bequest to the surviving spouse. Such a bequest could include partial ownership interests in real estate. If the surviving spouse is concerned about asset protection, this additional property would not be beneficial because it would easily be sacrificed to the survivor’s creditors. One way of avoiding this result is to build an estate plan in which each spouse bequests the partial interest owned by that spouse to a trust. At the first death between two spouses, the trust will hold the partial ownership interest for the benefit of the surviving spouse. The trust holding the partial residence interest preserves the deterrent faced by creditors of the surviving spouse because seizure of the surviving spouse’s interest would not terminate the spouse’s right to use the land provided for in the trust.

A different set of rules applies to property held jointly by medical professionals who are not married to each other. If property is owned jointly among siblings or business associates instead of a business entity, the owners should make sure that the deed names them as tenants-in-common. Otherwise, each successive death among the owners will shift the ownership to the survivors, and leave the family of the deceased owner with no lasting value from the owner’s investment into the property and its improvements.

LONG TERM

Assets should be held in a way that protects them from creditors for the long term. The form of asset holdings should thus be a significant part of the discussions held with professional advisors, so that the protection lasts beyond your death or that of your spouse. Structure the protected assets so that they do not flow back to you if your spouse should pass away. In this manner, integrated asset protection, estate planning, and financial planning unite to protect the family’s interests by extending the benefits of creditor protection for the long term.

ASSESSMENT: Your comments are appreciated.

****

[1] See United States v. Craft, 535 U.S. 274 (Apr. 17, 2002).

Posted on September 5, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL CLAIMS ADJUDICATION

By Eric Bricker MD

Claims Adjudication Occurs between a Healthcare Provider Submitting a Claim to a Health Insurance Company and the Insurance Company Making a Payment Back to the Provider.

Posted on August 29, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

EMR OVERVIEW

BY ERIC BRICKER MD

Electronic Medical Records (EMRs) are Used by 80-90% of Hospitals and Physician Practices. One Study Found that EMRs Have Lowered Patient Mortality by 0.09%.

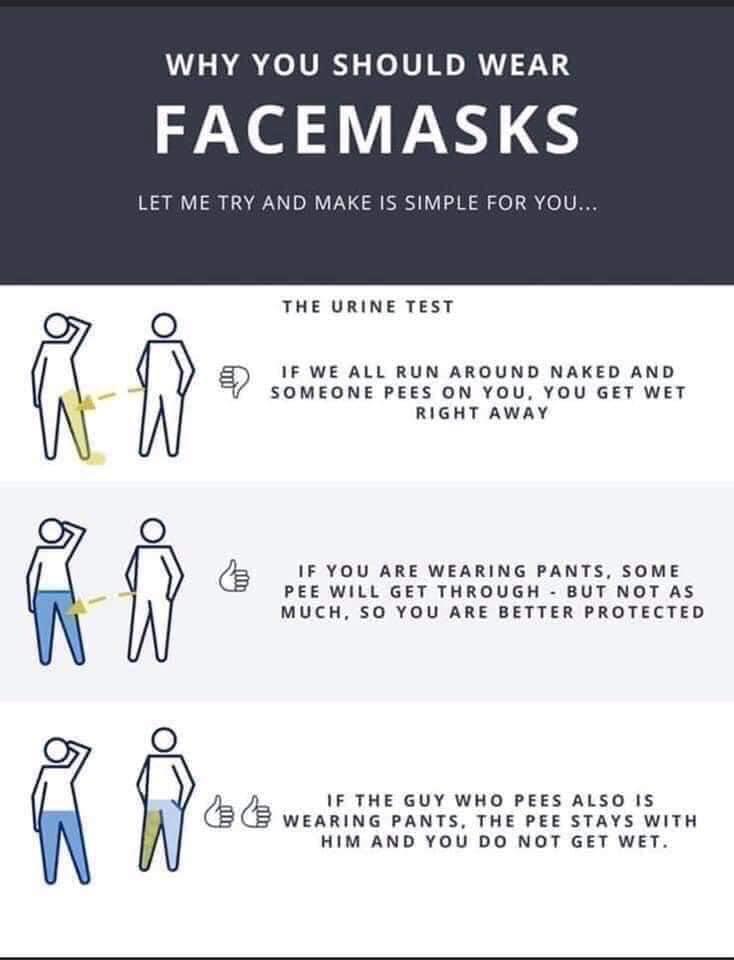

A Balaclava, also known as a balaclava helmet or Bally or ski mask, is a form of cloth headgear designed to expose only part of the face, usually the eyes and mouth.

Now, depending on style and how it is worn, only the eyes, mouth and nose, or just the front of the face are unprotected. Versions with a full face opening may be rolled into a hat to cover the crown of the head or folded down as a collar around the neck.

Here is my version for the Corona Virus pandemic! Glasses and a mouth cover complete the look and proposed utility.

***

***

So, I’ve written 30 major medical, business, economics and finance textbooks including three dictionaries of 30,000 peer-reveiwed terms. But, this was a new word previously unknow to me. How about you?

***

RUNNER-UPS

***

***

ASSESSMENT: Your thoughts and comments are appreciated.

***

BUSINESS TEXTS FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXOs

Posted on August 11, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Review

This is a handy, word-packed reference book with health information technology terminology of the past, present, and future. The paperback book is small and compact in size but amazingly full of words, abbreviations, and even names of leaders in the health information technology industry. While any book like this will require updating on a periodic basis, many of the terms will remain relevant for a good period of time. I found the dictionary very useful and recommend it as a good addition to the reference shelf in the office or library.

—Doody’s Book Review

From the Back Cover

Over10,000 Detailed Entries!

“”There is a myth that all stakeholders in the healthcare space understand the meaning of basic information technology jargon. In truth, the vernacular of contemporary medical information systems is unique, and often misused or misunderstood? Moreover, an emerging national Heath Information Technology (HIT) architecture; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert medical, nursing, public policy administrator or paraprofessional in a position of maximum uncertainty and minimum productivity ?The Dictionary of Health Information Technology and Security will therefore help define, clarify and explain…You will refer to it daily.””

–– Richard J. Mata, MD, MS, MS-CIS, Certified Medical Planner? (Hon), Chief Medical Information Officer [CMIO], Ricktelmed Information Systems, Assistant Professor Texas State University, San Marcos

Posted on August 4, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

***

TEXTBOOKREVIEW

Drawing on the expertise of decision-making professionals, leaders, and managers in health care organizations, Hospitals & Health Care Organizations: Management Strategies, Operational Techniques, Tools, Templates, and Case Studies addresses decreasing revenues, increasing costs, and growing consumer expectations in today’s increasingly competitive health care market.

Offering practical experience and applied operating vision, the authors integrate Lean managerial applications, and regulatory perspectives with real-world case studies, models, reports, charts, tables, diagrams, and sample contracts. The result is an integration of post PP-ACA market competition insight with Lean management and operational strategies vital to all health care administrators, comptrollers, and physician executives. The text is divided into three sections:

Managerial Fundamentals

Policy and Procedures

Strategies and Execution

Using an engaging style, the book is filled with authoritative guidance, practical health care–centered discussions, templates, checklists, and clinical examples to provide you with the tools to build a clinically efficient system. Its wide-ranging coverage includes hard-to-find topics such as hospital inventory management, capital formation, and revenue cycle enhancement. Health care leadership, governance, and compliance practices like OSHA, HIPAA, Sarbanes–Oxley, and emerging ACO model policies are included. Health 2.0 information technologies, EMRs, CPOEs, and social media collaboration are also covered, as are 5S, Six Sigma, and other logistical enhancing flow-through principles. The result is a must-have, “how-to” book for all industry participants.

Posted on July 30, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

15 Self-Funded Employers Analyzed Their Pharmacy Claims Data in Conjunction with the Commonwealth Fund and Discovered the Following Regarding their PBM FormularIES

Posted on July 22, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BOOK REVIEW

“The Dictionary of Health Insurance and Managed Care lifts the fog of confusion surrounding the most contentious topic in the health care industrial complex today. My suggestion therefore is to ‘read it, refer to it, recommend it, and reap’.”

—Michael J. Stahl, PhD, Physician Executive MBA Program [William B. Stokely Distinguished Professor of Business]

The University of Tennessee, College of Business Administration

Posted on July 21, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

TEXTBOOK RELEASE AND REVIEW

Reviews

Navigating a course where sound organizational management is intertwined with financial acumen requires a strategy designed by subject-matter experts. Fortunately, Financial Management Strategies for Hospital and Healthcare Organizations: Tools, Techniques, Checklists and Case Studiesprovides that blueprint. ―David B. Nash, MD, MBA,Jefferson Medical College, Thomas Jefferson University

It is fitting that Dr. David Edward Marcinko, MBA, CMP™ and his fellow experts have laid out a plan of action in Financial Management Strategies for Hospital and Healthcare Organizationsthat physicians, nurse-executives, administrators, institutional CEOs, CFOs, MBAs, lawyers, and healthcare accountants can follow to help move healthcare financial fitness forward in these uncharted waters. ―Neil H. Baum, MD, Tulane Medical School

Posted on July 18, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

THE SHERLOCK COMPANY

This podcast features a brief discussion by colleague Doug B. Sherlock CFA, Senior Health Care Analyst and President, Sherlock Company http://www.sherlockco.com featuring his insights into the quarterly financial reports of health plans, for the first quarter 2021.

1) The 90s HMOs: Lower Premiums, Lower Out-of-Pocket Costs, Many Many Rules Restricting Care.

2) The 2000s PPOs: High and Even Higher Premiums, Lower Out-of-Pocket Costs, Fewer Rules Restricting Care.

3) The 2010s CDHPs: Lower Premiums, HIGH Out-of-Pocket Costs, Fewer Rules Restricting Care.

The Last 30 Years Have Taught Us that Employer-Sponsored Health Plans CANNOT Have All 3–Low Premiums, Low Out-of-Pocket Costs and Few Care Restrictions.

In the 2020s, Employers Are Moving More of Their Employee Healthcare OUTSIDE of the Traditional Healthcare and Health Insurance System with On-Site Clinics, Near-Site Clinics, Virtual Urgent Care, Virtual Primary Care and Bundled-Payment Centers-of-Excellence.

Posted on July 8, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION: CRISPR is a family of DNA sequences found in the genomes of prokaryotic organisms such as bacteria and archaea. These sequences are derived from DNA fragments of bacteriophages that had previously infected the prokaryote. They are used to detect and destroy DNA from similar bacteriophages during subsequent infections

For the first time, CRISPR technology has been used to successfully treat diseasein vivo, or inside the human body.

That big medical news was announced Saturday by the biotech startup Intellia Therapeutics and its partner Regeneron, which said their gene-editing techniques reduced the amount of harmful liver protein associated with a genetic nerve disorder.

What is CRISPR? It stands for “clustered regularly interspaced short palindromic repeats,” and it’s one of those things humans found in nature and then copied. Bacteria use CRISPR to repel viruses, but humans have harnessed it to ctrl+c, ctrl+v DNA sequences, potentially leading to a revolution in treating disease. The two scientists who made that breakthrough in 2012, Jennifer Doudna and Emmanuelle Charpentier, won the Nobel Prize in Chemistry last year (Doudna is also a cofounder of Intellia).

Quote du jour: “There’s a feeling like we’re walking through a door here into all kinds of new possibilities. And there’s not many moments in medicine where you get to experience that,” Intellia CEO John Leonard said. Looking ahead…expect Intellia shares, which have gained 233% since its 2016 IPO, to pop.

Posted on July 5, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

At Least in PartACCORDING TO THESE BOOKS

BY ERIC BRICKER MD

Understandably, Many Doctors Take Issue with This Accusation and Say They Treat Their Patients with Integrity and Accountability. Both Statements May Be TRUE … How is That Possible?

Because of ‘Bad Apples.’

While the Majority of Physicians May Put Their Patients First, There Are a Minority of Physicians that Put Money, Power, Prestige and Promotions Ahead of Patients. It’s These Bad Apples That Ruin Physician Culture.

Problem: Fee-for-Service Rewards Bad Apple Physicians, While Paying the High-Integrity Doctors as Well.

Assessment: If Doctors Want to Keep Fee-for-Service, Then the Bad Apples Must Be Reduced Through 1) Increased Transparency, 2) Greater Doctor Self-Regulation, 3) More Federal Oversight and 4) Increased Employer Investigation.

A “MEME” stock isn’t as easily defined as a growth or value stock, so to give it a definitive categorization would be inappropriate. Nor would actually categorizing it alongside growth and value stocks. They won’t be found in textbooks anytime soon, but to overlook their impact could potentially be an expensive oversight.

Posted on July 2, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ELECTRIC HEALTH RECORDS

By White Hat Anonymous

Epic Systems, the country’s leading e-health record company, says an algorithm it developed can accurately flag sepsis in patients 76% of the time. The life-threatening disease, which arises from infections, is a major concern for hospitals: One-third of patients who die in hospitals have sepsis, per the CDC.

Generally, the earlier sepsis is diagnosed and treated, the better a patient’s chances of survival—and hundreds of hospitals use Epic Systems’s sepsis prediction model, The Verge reports.

The problem: According to a study published this week in JAMA Internal Medicine, Epic Systems may have gotten the success rate wrong: The model is only correct 63% of the time—“substantially worse than the performance reported by its developer,” the researchers wrote.

Part of the issue can be traced to the algorithm’s development, Stat News reports. It was trained to flag when doctors would submit bills for sepsis treatment—which doesn’t always line up with patients’ first signs of symptoms.

“It’s essentially trying to predict what physicians are already doing,” Dr. Karandeep Singh, study author.

When reached for comment, Epic Systems told us the researchers’ hypothetical scenario lacked “the required validation, analysis, and tuning that organizations need to do before deployment,” adding that the JAMA study’s findings differed from other research.

Many accountable care organizations (ACOs) received disappointing news on May 21, 2021, when the Centers for Medicare & Medicare Services (CMS) announced that it would not be extending the Next Generation ACO (NGACO) model for 2022.

After five years and a dwindling number of participating ACOs, experts were split on whether or not CMS should keep the model in place for another year. On one hand, stakeholders have argued for the NGACO model’s extension until it can be replaced with or integrated into another program; howowever, others asserted that resources could not be properly invested with only one more year left in the program. (Read more…)

Walmart, the world’s largest retailer, opened the first Walmart Health in 2019 with the main goal of helping to meet the healthcare needs of the communities they serve. After opening six locations in almost two years, Walmart is looking to operate a total of 22 standalone clinics by the end of 2021.

This Health Capital Topics article will review Walmart Health’s approach to delivering primary care, the communities into which it is expanding, its partnerships it is developing in the healthcare sector, and the competitive landscape in which it operates. (Read more…)

Nurses on General Medical and Surgical Floors Typically Have a 4:1 Patient to Nurse Ratio During the Day and an 8:1 Patient to Nurse Ratio Overnight.

Nurses in the ICU Typically Have a 2:1 or 1:1 Patient to Nurse Ratio.

Nurses on a Floor or Unit Have a ‘Charge Nurse‘ Who is the Head Nurse for the Floor for That Specific Shift.

Those Charge Nurses Then Collaborate with the Shift Coordinator Who is a Very Senior and Experience Nurse Who Coordinates All the Patient Beds for a Particular Division at a Large Hospital (e.g. All Medicine Patients vs. All Surgical Patients) or for the Entire Hospital If It Is a Smaller Hospital.

Medical Techs Provide Support Roles in Patient Rooms Such as Checking Vitals, Blood Glucose Finger-Sticks, Etc.

The Clerk Sits at the Nurses Station for the Floor and Typically Answers the Call-Button for Each of the Patient Rooms During the Day in Addition To Their Administrative Responsibilities.

There are varying opinions on how much of your total income should go toward savings and retirement goals each month. Moreover, the answer is likely to vary, depending on your full financial profile.

But if you’re looking for some basic KISS guidelines, consider applying the 50-30-20 rule, a budgeting method that allocates 50% of your income to essentials, like rent and bills, 30% to discretionary spending and 20% to savings.

Consequently, When the Supply of a Healthcare Service is Limited, then the Price Goes Up … Way Up, Since the Quantity Demanded Does Not Change.

Examples of Inelastic Demand with Limited Supply in Healthcare Are:

1) Emergencies

2) Patented Medications for Diseases That Have No Other Alternatives

3) Doctor Specialties Where the Patient Has No Choice in the Services Such As Radiologists, Anesthesiologists and Pathologists

The High-Cost Claimants with Inelastic Demand Drive the Majority of Healthcare Costs for a Group. They Generally Fall into 3 Diagnosis Categories: 1) Orthopedics, 2) Cardiovascular and 3) Cancer.

Orthopedics Should Be the 1st Priority for Lowering Healthcare Costs for a Population … While Demand May be Inelastic, Usually There is Choice and Not a Limited Supply of Orthopedic Services.

Efforts in Orthopedics Should Focus on Increasing Choice, Such as Free Travel to Centers-of-Excellence with Bundled Pricing.

Cardiovascular Care and Cancer Care Tend to Have Inelastic Demand AND Limited Supply. Therefore, the Best Way to Lower Healthcare Costs in These Areas is Through Prevention.

Posted on June 15, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BY ERIC BRICKER MD

[Book Review]

***

The Technology Adoption Lifecycle Was Explained in Geoffrey Moore’s Famous Book ‘Crossing the Chasm.‘

If You Are a Healthcare Entrepreneur or Innovator Your MUST Understand and Apply the Technology Adoption Lifecycle.

It States that Disruptive Innovation (i.e. Innovations that Require Behavior Change) Is Not Evenly Adopted Across a Population.

Rather, People Segment Themselves into Sub-Groups That Adopt the New Innovation Differently. To Whit:

**************

Early AdoptersLove Tinker and Like New Innovations Just Because They Are New. Early Adopters Tend to Not Be Price-Sensitive.

PragmatistsHave a Specific Problem that the New Innovation Will Solve and If They See Other People Using It, They Will Use It Too. Pragmatists Are Somewhat Price-Sensitive.

Conservatives Would Rather Not Adopt the New Innovation, but if it is Already Built-in to Something They Already Buy, Then They Will Be More Likely to Use It. Conservatives are Very Price Sensitive.

Skeptics Will Never Adopt the New Innovation.

**************

To Spread a New Innovation, One Must Cross the Chasm Between the Early Adopters and Pragmatists With a ‘Niche‘ and ‘Bowling Pin‘ Strategy.

Each generation of doctors and medical professionals is extraordinarily complex, bringing various skills, expertise and expectations to the modern medical work environment. Determining the best method to unite such diverse thinking is one of the many challenges faced by physician executives and healthcare leaders today.

And, as linguistic evolution occurs, the nomenclature of hospitalist was followed by that of intensivist, proceduralist and nocturnalist, etc [www.MedInnovationBlog.com and Personal communication Richard L. Reece MD].

Is it any wonder that many medical leaders and executive in the Baby Boomer generation find themselves at a loss? The days of functional leadership are gone and suddenly, no one cares about the expertise of the Baby Boomers or how they climbed the corporate ladder, in medicine or elsewhere. Leadership in the new era is no longer about command-control or dictating with intense focus on the bottom line; it is about collaboration, empowerment and communication. And, it is not about titles and nomenclature; it is about lifestyle choice.

What else drives these new-wave specialists?

The answer, of course, is the next-generation of physicians and their emerging new medical business and practice models, which include:

“Ambulists” are doctors that travel locally, have no, or only a sparse physical office presence of their own. They sporadically provide services that are additive to traditional practice models [i.e., endocrinologist in a large family medical office with many diabetics].

“In-Situ” physicians regularly provide services that are complimentary to existing traditional practice models [i.e., dentists or podiatrists in a medical practice].

“Laborists” are obstetricians that do not wish to be on-call. First begun in Cape Cod and other Massachusetts hospitals, such obstetricians work regular shifts for the sole purpose of delivering babies.

“Locum Tenens” doctors travel around the country as itinerants [i.e., cruise ships] as temporary substitutes for another the same specialty.

“Officists” remain in their own physical practice, and rarely see patients in the hospital, nursing home, patient home, out-patient facility, etc.

Finally, “dayhawk physicians” mimic the “nighthawk physician” model where radiologists in remote locations read films in the middle of the night as cash-strapped hospitals often find it cheaper to outsource with better services and more timely interpretations in many cases.

Posted on June 11, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

OVER HEARD IN THE DOCTOR’S LOUNGE

I currently have no fewer than 10 separate insurance policies associated with my plastic surgery practice. I understand very little about the policies other than that somebody at some point told me I needed each and every one of them, and each made sense when I bought it. But, I often wonder:

Am I over-insured and thus wasting money?

Am I under-insured and thus at risk for a liability disaster?

I never really had the means of answering these questions …. Until Now!

Posted on June 9, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

AGING AND RETIREMENT

Long-term care (LTC) may not be the first thing individuals or couples think about as they approach retirement, but the costs for those who needs it can disrupt and derail retirement security. A good plan for long-term care requires many decisions over an extended period of time, and well before retirement.

In this article, Milliman consultant Robert Eaton discusses the major considerations and options for financing LTC needs in retirement.

BOOK-VALUE: Cost of capital assets minus accumulated depreciation for a healthcare [corporation], or other organization.

The net asset value of a [healthcare] companies common stock. This is calculated by dividing the net tangible assets of the company (minus the par value of any preferred stock the company has) by the number of common shares outstanding.

****

PAR VALUE: For common stock, the value on the books of the corporation. It has little to do with market value or even the original price of shares at first issuance.

The difference between par and the price at first issuance is carried on the books of a corporation as “paid-in capital” or “capital surplus.”

To keep up with the ever-changing healthcare industrial complex, we must learn new definitions and re-learn old terminology in order to correctly apply it to practice. By aggregating the most up-to-date abbreviations, acronyms, definitions and terms, the Health DictionarySeries offers a wealth of information to help understand the ever-changing terms-of-art in healthcare today.

Each 10,000 item handbook is essential for doctors, nurses, benefits managers, financial advisors/planners, and insurance agents, CPAs, and administrators; as well as graduate and under graduate students and professors. Our goal to for each dictionary to be designated as a Doody’s Core Title.

Dictionary of Health Insurance and Managed Care

With more than 10,000 definitions, 4,000 abbreviations and acronyms, and a 3,000 item oeuvre of resources, readings, and nomenclature derivatives, this dictionary covers the Medicare, managed care and Medicaid, private insurance, Veteran’s Administration and PP-ACA language of the entire health and long-term care insurance sector.

Dictionary of Health Economics and Finance

Health economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, mathematics, the actuarial sciences, stochastics and statistics, salary reimbursements, physician payments, compensation and forecasting are all commingled arenas.

Dictionary of Health Information Technology Security

There is a myth that all healthcare stakeholders understand the meaning of information technology jargon. In truth, the vernacular of contemporary systems is unique, and often misused or misunderstood. Moreover, emerging Heath Information Technology (HIT) thru the HITECG initiatives; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert in a position of maximum uncertainty and minimum productivity.

![DR. DAVID EDWARD MARCINKO FACFAS MBA CFP MBBS [Hon] [Executive Summary] - PDF Free Download](https://educationdocbox.com/docs-images/75/71938560/images/8-1.jpg)

/u-s-debt-ceiling-why-it-matters-past-crises-9ee4f4a3337c4203997fb191a9858b8c.gif)

:max_bytes(150000):strip_icc():format(webp)/the-50-30-20-rule-of-thumb-453922-final-5b61ec23c9e77c007be919e1-5ecfc51b09864e289b0ee3fa0d52422f.png)