BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Mensa is one of those organizations that tends to spark curiosity the moment its name comes up. People often imagine a secretive club of geniuses solving impossible puzzles in dimly lit rooms. The reality is far more grounded—and far more interesting. Mensa is, at its core, a global community built around a single criterion: high measured intelligence. But what that simple requirement has created over the decades is a surprisingly diverse network of thinkers, hobbyists, professionals, and lifelong learners who share a fascination with ideas.

Founded in 1946 in England, Mensa began with an idealistic mission: to gather the brightest minds regardless of background, politics, or profession, and to use that collective intelligence for the betterment of humanity. The founders envisioned a society where intellect could be a unifying force rather than a dividing one. Over time, Mensa expanded far beyond its origins, eventually becoming an international organization with chapters in dozens of countries and members from nearly every walk of life.

Membership is based solely on scoring within the top two percent on an approved intelligence test. That threshold is intentionally simple. Mensa does not evaluate academic degrees, professional achievements, or social status. It doesn’t matter whether someone is a scientist, a mechanic, a student, or a retiree. If they meet the cognitive requirement, they’re in. This openness is part of what makes the organization unique. It creates a space where people who might never cross paths in everyday life can connect through shared intellectual curiosity.

What draws people to Mensa varies widely. For some, it’s the appeal of belonging to a community that values quick thinking and problem‑solving. For others, it’s the social aspect—local chapters host game nights, lectures, dinners, and special interest groups that range from astronomy to cooking to science fiction. Mensa’s annual gatherings, especially in larger countries, can feel like a blend of academic conference, festival, and family reunion. Members often describe these events as energizing because they offer a rare environment where lively debate and quirky interests are not just accepted but encouraged.

Another dimension of Mensa’s identity is its commitment to intellectual enrichment. Many chapters run programs for gifted youth, offering support to children who may feel out of place in traditional school settings. Others organize scholarship competitions or community service projects. While Mensa is not a research institution, it does foster an atmosphere where learning is a lifelong pursuit. Members frequently share articles, host discussions, and create clubs centered on everything from mathematics to creative writing. The organization’s publications, both local and international, serve as platforms for essays, puzzles, humor, and commentary contributed by members themselves.

***

***

Despite its positive aspects, Mensa is not without criticism. Some argue that relying on standardized intelligence tests oversimplifies the concept of intelligence. Human cognitive ability is complex, multifaceted, and influenced by culture, environment, and opportunity. A single score cannot capture creativity, emotional intelligence, or practical problem‑solving skills. Others feel that the organization can sometimes lean toward self‑congratulation, attracting people who are more interested in the status of membership than in contributing to the community. These critiques are not new, and Mensa itself acknowledges that intelligence is only one part of a person’s identity.

Still, the organization’s longevity suggests that it fulfills a real need. Many members describe Mensa as a place where they finally feel understood. Growing up, they may have been the kid who asked too many questions, finished assignments early, or felt out of sync with peers. Mensa offers a space where intellectual intensity is normal rather than unusual. That sense of belonging can be powerful, especially for people who have spent much of their lives feeling different.

In the modern world, where information is abundant and attention is fragmented, Mensa occupies an interesting niche. It is not a think tank or a political group. It does not claim to solve global problems or dictate what intelligence should be used for. Instead, it provides a framework for connection—an invitation for people who enjoy thinking deeply to meet others who share that inclination. In a sense, Mensa’s greatest strength is not the intelligence of its members but the community that forms when people with curious minds gather.

***

***

Ultimately, Mensa is a reminder that intelligence, while often treated as a competitive metric, can also be a source of camaraderie. It shows that people with high cognitive ability are not a monolith; they are as varied in personality, interests, and life experiences as any other group. What unites them is not superiority but curiosity—a desire to explore ideas, challenge assumptions, and engage with the world in a thoughtful way.

Whether one views Mensa as an elite club, a social network, or simply a gathering of people who enjoy mental stimulation, its impact is undeniable. It has created a global space where intellect is celebrated, conversation is valued, and learning never really stops. And in a world that often rushes past nuance and depth, that kind of space is worth appreciating.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The image of the clown—painted smile, exaggerated gestures, boundless energy—has long symbolized joy, whimsy, and comic relief. Yet behind this bright façade lies one of the most enduring and poignant contradictions in human psychology: the Sad Clown Paradox. This paradox captures the tension between outward expressions of happiness and inner experiences of sadness, anxiety, or emotional struggle. It is the phenomenon of individuals who appear cheerful, supportive, and uplifting to others while privately carrying heavy emotional burdens. The paradox resonates across cultures and eras because it reflects a universal truth: people often hide their pain behind a mask of humor or positivity.

At its core, the Sad Clown Paradox is about emotional dissonance. Humans are social creatures, and we learn early in life that certain emotions are more acceptable to display than others. Joy, enthusiasm, and humor are welcomed; sadness, fear, and vulnerability can feel risky to reveal. For some, humor becomes a shield—a way to deflect attention from their internal struggles. The clown’s painted smile becomes a metaphor for the emotional masks people wear in everyday life. This mask can be protective, allowing someone to function socially or professionally even when they feel overwhelmed. But it can also become isolating, creating a gap between how a person appears and how they truly feel.

One reason the Sad Clown Paradox persists is that humor is an incredibly effective coping mechanism. Laughter can diffuse tension, create connection, and provide temporary relief from stress. Many people who gravitate toward comedic roles—whether professionally or within their social circles—develop a finely tuned ability to read the emotional needs of others. They know how to lighten a room, how to distract from discomfort, and how to make people feel at ease. Yet this sensitivity to others’ emotions often coexists with difficulty expressing their own. The person who makes everyone else laugh may struggle to ask for help, fearing that doing so would disrupt the role they’ve come to play.

***

***

Another dimension of the paradox is the pressure of expectation. When someone becomes known as “the funny one” or “the strong one,” they may feel obligated to maintain that persona even when they are hurting. This expectation can come from others, but it often becomes internalized. The sad clown tells themselves that their value lies in their ability to uplift others, not in their own emotional truth. They may worry that revealing their struggles would disappoint people or burden them. Over time, this can lead to emotional exhaustion, as the effort to maintain the mask becomes heavier than the emotions it was meant to hide.

The paradox also highlights the complexity of emotional expression. People are rarely just one thing. Someone can be genuinely joyful in one moment and deeply sad in another. The sad clown is not necessarily faking their humor; often, their ability to find lightness in dark situations is real and sincere. But sincerity does not erase struggle. The paradox reminds us that outward behavior is not always a reliable indicator of inner experience. A person who seems endlessly cheerful may be using that cheerfulness to navigate their own pain.

In a broader sense, the Sad Clown Paradox speaks to the human tendency to curate our emotional identities. Social media, workplace culture, and even casual conversation often reward positivity and discourage vulnerability. This creates an environment where people feel compelled to present a polished version of themselves. The sad clown becomes a symbol of the emotional labor involved in maintaining that façade. It raises important questions about authenticity, connection, and the ways we support one another.

***

***

Understanding the paradox invites a more compassionate view of others. It encourages us to look beyond surface impressions and recognize that everyone carries unseen struggles. It also challenges the assumption that those who seem the strongest or happiest are immune to hardship. Sometimes the people who give the most comfort are the ones who need it most. The paradox reminds us to check in on the friends who always make us laugh, the colleagues who never complain, and the loved ones who seem perpetually upbeat.

On a personal level, the Sad Clown Paradox invites reflection on the masks we wear ourselves. It encourages us to consider whether we allow others to see our full emotional range or whether we hide behind humor or competence. Acknowledging the paradox does not mean abandoning humor or positivity; rather, it means recognizing that these qualities can coexist with vulnerability. The goal is not to discard the mask entirely but to ensure it does not become a barrier to genuine connection.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Flynn Effect is one of the most intriguing and debated findings in the study of human intelligence. Named after political scientist James R. Flynn, who brought widespread attention to the phenomenon in the 1980s, it refers to the steady and substantial rise in average IQ scores across many countries throughout the twentieth century. Although intelligence tests are designed so that the average score remains 100, test publishers must periodically “renorm” them because people keep performing better than the previous generation. The scale of this rise is striking: in some nations, average scores have increased by roughly three points per decade. The Flynn Effect forces us to rethink what IQ tests measure, how societies change over time, and what “intelligence” even means.

At its core, the Flynn Effect highlights the dynamic relationship between human cognition and the environment. IQ tests do not measure intelligence in a vacuum; they measure how well individuals navigate the kinds of abstract, symbolic problems that modern societies increasingly demand. One of Flynn’s key insights was that the twentieth century brought a shift toward what he called “scientific spectacles”—a way of thinking that emphasizes classification, hypothetical reasoning, and abstraction. These cognitive habits are not innate; they are cultivated through schooling, technology, and daily life. As societies modernized, more people became accustomed to the mental tools that IQ tests reward.

Several explanations have been proposed to account for the rise in scores, and no single factor tells the whole story. One major contributor is improved education. Over the past century, schooling has become more widespread, more rigorous, and more focused on analytical reasoning. Children spend more years in school, encounter more complex curricula, and are exposed to problem‑solving tasks that mirror the structure of IQ test items. Even subtle changes—like the shift from rote memorization to conceptual understanding—can have a large cumulative effect on cognitive performance.

Another important factor is the transformation of everyday life. Modern work environments often require employees to manipulate symbols, operate technology, and adapt to rapidly changing tasks. Even leisure activities have become more cognitively demanding. Video games, digital interfaces, and information‑rich media encourage multitasking, spatial reasoning, and strategic thinking. These experiences may not directly teach the content of IQ tests, but they strengthen the underlying cognitive skills that such tests measure.

Nutrition has also been proposed as a contributor. Better prenatal care, reduced exposure to environmental toxins, and improved childhood nutrition can influence brain development. While nutrition alone cannot explain the full magnitude of the Flynn Effect, it likely plays a role, especially in countries that experienced dramatic improvements in public health during the twentieth century.

***

***

Family size and parenting practices may also matter. Smaller families allow parents to invest more time and resources in each child. Parenting has become more child‑centered, with greater emphasis on verbal interaction, exploration, and educational enrichment. These shifts create environments that nurture the kinds of cognitive abilities reflected in IQ tests.

Despite the broad upward trend, the Flynn Effect is not uniform across all domains of intelligence. Gains tend to be largest on tests that measure fluid reasoning—abstract problem‑solving and pattern recognition—rather than crystallized knowledge such as vocabulary. This pattern supports the idea that environmental complexity, rather than simple memorization, drives the effect. It also suggests that IQ gains do not necessarily mean people are “smarter” in a general sense; instead, they may be better adapted to the cognitive demands of modern life.

In recent years, some countries have reported a slowing or even reversal of the Flynn Effect. This has sparked intense debate. Some argue that the earlier gains were driven by rapid modernization, and once societies reached a certain level of development, the effect naturally plateaued. Others point to changes in education, technology use, or immigration patterns. Still others suggest that the apparent decline may reflect changes in test design rather than real cognitive shifts. The truth is likely a mix of these factors, and the debate underscores how complex and multifaceted intelligence is.

***

***

The Flynn Effect also raises philosophical questions. If IQ scores can rise so dramatically over a few generations, what does that say about the nature of intelligence? Are we measuring an innate trait, or a set of skills shaped by culture and environment? Flynn himself argued that intelligence is not a fixed quantity but a reflection of the cognitive tools that societies value and cultivate. In his view, rising IQ scores reveal not biological evolution but cultural evolution—a shift in how people think about the world.

Ultimately, the Flynn Effect challenges simplistic interpretations of IQ. It reminds us that human cognition is deeply intertwined with social, economic, and cultural forces. It shows that intelligence is not static but responsive to the world we build around ourselves. And it invites us to consider how future changes—technological, educational, or environmental—might continue to reshape the landscape of human thought.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on February 5, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

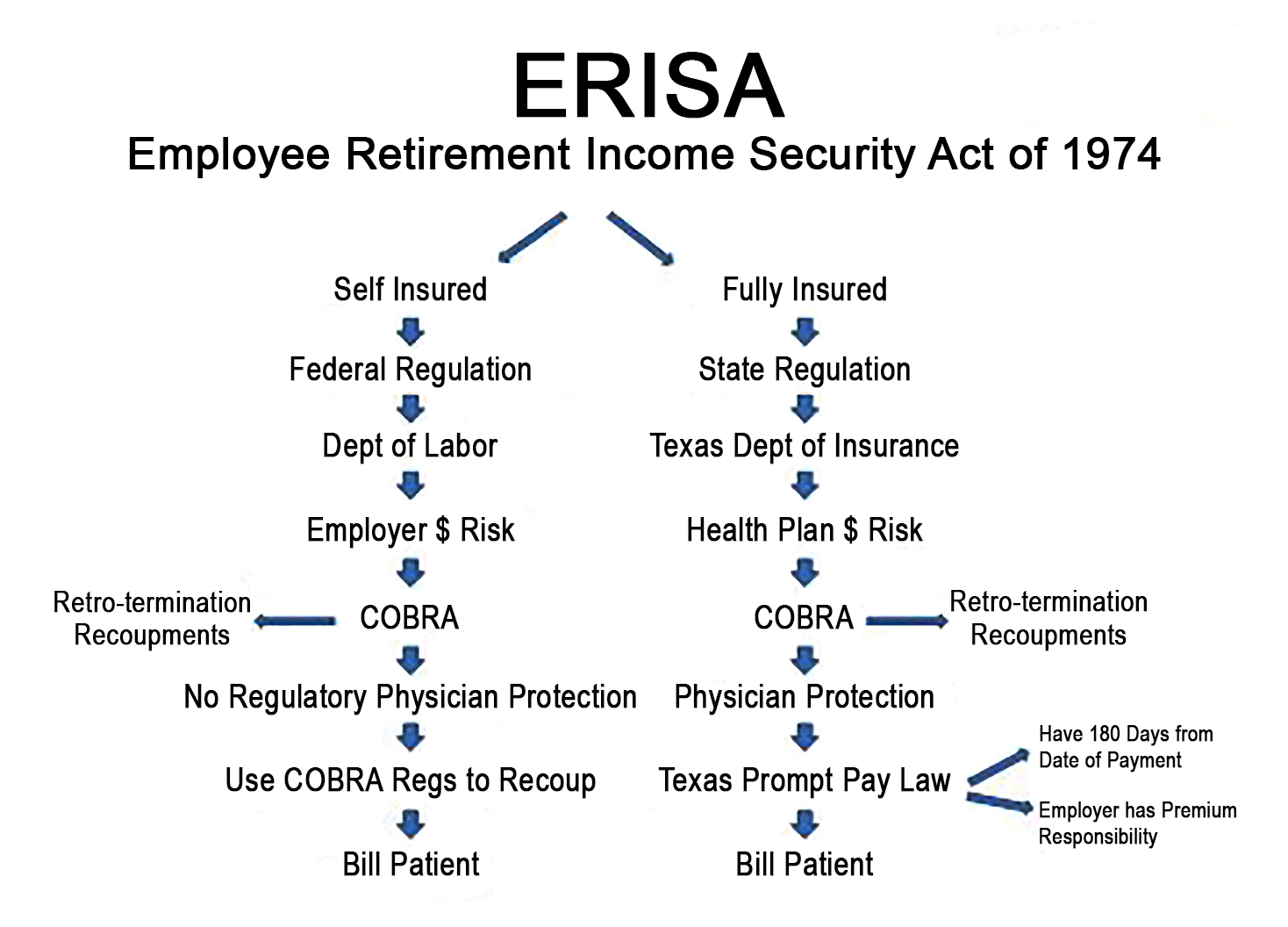

Employee Retirement Income Security Act

By Staff Reporters

***

***

The Employee Retirement Income Security Act of 1974 (ERISA) is a federal law that sets minimum standards for most voluntarily established retirement and health plans in private industry to provide protection for individuals in these plans.

ERISA requires plans to provide participants with plan information including important information about plan features and funding; provides fiduciary responsibilities for those who manage and control plan assets; requires plans to establish a grievance and appeals process for participants to get benefits from their plans; and gives participants the right to sue for benefits and breaches of fiduciary duty.

There have been a number of amendments to ERISA, expanding the protections available to health benefit plan participants and beneficiaries. One important amendment, the Consolidated Omnibus Budget Reconciliation Act (COBRA), provides some workers and their families with the right to continue their health coverage for a limited time after certain events, such as the loss of a job. Another amendment to ERISA is the Health Insurance Portability and Accountability Act which provides important protections for working Americans and their families who might otherwise suffer discrimination in health coverage based on factors that relate to an individual’s health.

Other important amendments include the Newborns’ and Mothers’ Health Protection Act, the Mental Health Parity Act, the Women’s Health and Cancer Rights Act, the Affordable Care Act and the Mental Health Parity and Addiction Equity Act.

In general, ERISA does not cover group health plans established or maintained by governmental entities, churches for their employees, or plans which are maintained solely to comply with applicable workers compensation, unemployment, or disability laws. ERISA also does not cover plans maintained outside the United States primarily for the benefit of nonresident aliens or unfunded excess benefit plans.

Posted on January 25, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

A paradox is a logically self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

Classic Definition: Artificial intelligence (AI) refers to computer systems capable of performing complex tasks that historically only a human could do, such as reasoning, making decisions, or solving problems. The term “AI” describes a wide range of technologies that power many of the services and goods we use every day – from apps that recommend TV shows to chat-bots that provide customer support in real time.

Modern Circumstance: The role of artificial intelligence in health care is becoming an increasingly topical and controversial discussion. There remains uncertainty about what is achievable regarding ongoing medical artificial intelligence research. Although there are some people who believe that artificial intelligence will be used, at best, as a tool to assist clinicians in their day-to-day activities, there are others who believe that job automation and replacement is a looming threat.

Paradox Example: Moravec’s paradox is a phenomenon observed by robotics researcher Hans Moravec, in which tasks that are easy for humans to perform (eg, motor or social skills) are difficult for machines to replicate, whereas tasks that are difficult for humans (eg, performing mathematical calculations or large-scale data analysis) are relatively easy for machines to accomplish.

***

***

For example, a computer-aided diagnostic system might be able to analyze large volumes of images quickly and accurately but might struggle to recognize clinical context or technical limitations that a human radiologist would easily identify.

Similarly, a machine learning algorithm might be able to predict a patient’s risk of a specific condition on the basis of their medical history and laboratory results but might not be able to account for the nuances of the patient’s individual case or consider the effect of social and environmental factors that a human physician would consider.

In surgery, there has been great progress in the field of robotics in health care when robotic elements are controlled by humans, but artificial intelligence-driven robotic technology has been much slower to develop.Thus far, research into clinical artificial intelligence has focused on improving diagnosis and predictive medicine.

Assessment

Moravec’s paradox also highlights the importance of maintaining a human element in the health-care system, and the need for collaboration between humans and technology to achieve the best possible outcomes.

Conclusion

In the field of medicine, it is becoming indisputable that artificial intelligence will have a role in population health analysis, predictive medicine, and personalized care.

However, for now, the job of doctors seems safe from automation.

Cite: Shuaib A: The increasing role of artificial intelligence in health care: will robots replace doctors in the future? Int J Gen Med. 2020; 13: 891-896

Today, I stand before you not just to speak about medicine, but to sound the alarm for a profession in peril. The medical field—once a beacon of hope, healing, and honor—is now grappling with a crisis that threatens its very foundation.

Across the country, doctors are burning out, hospitals are closing, and patients are waiting longer for care that’s increasingly harder to afford. This isn’t just a healthcare issue—it’s a human issue.

At the heart of this collapse is the corporatization of medicine. Physicians, once trusted decision-makers, now find themselves at the mercy of insurance companies, hospital administrators, and profit-driven systems. The art of healing has been replaced by spreadsheets and quotas. Doctors are forced to see more patients in less time, not because it’s better for care—but because it’s better for business.

And what of the next generation? Medical students face crushing debt, often exceeding $300,000. Yet even after years of study, thousands are left unmatched to residency programs due to outdated federal caps. Imagine training for a marathon, only to be told you can’t cross the finish line. That’s the reality for many aspiring physicians today.

The COVID-19 pandemic didn’t create this crisis—but it exposed it. Emergency rooms buckled under pressure. Rural hospitals shuttered. Healthcare workers risked their lives, only to face trauma, exhaustion, and in some cases, violence from the very people they sought to help.

We must also confront a cultural shift—one that undermines science, spreads misinformation, and erodes trust in medical professionals. Doctors are harassed, threatened, and doubted. This isn’t just unfair—it’s dangerous.

So what can we do?

We must advocate for reform. Expand residency slots. Reduce the cost of medical education. Protect physician autonomy. And most importantly, restore the soul of medicine—compassion, integrity, and service.

This is not a time for silence. It’s a time for action. Because when medicine collapses, society suffers. But if we rise together—patients, providers, policymakers—we can rebuild a system that heals not just bodies, but communities.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 15, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko; MBA MEd

***

***

Physician Drug Addiction: A Hidden Crisis in Healthcare

Physicians are often seen as the guardians of health, entrusted with the care and well-being of others. Yet behind the white coats and clinical expertise, some doctors silently struggle with substance use disorders (SUDs). Physician drug addiction is a serious and often hidden crisis that affects not only the individuals involved but also the safety of their patients and the integrity of the healthcare system.

Studies show that physicians experience substance abuse at rates comparable to or slightly lower than the general population, but the consequences are far more severe due to their professional responsibilities. According to the American Addiction Centers, approximately 10–15% of healthcare professionals will misuse drugs or alcohol at some point in their careers.

The most commonly abused substances include alcohol, opioids, benzodiazepines, and stimulants—many of which are readily accessible in medical settings.

Several factors contribute to addiction among physicians. The medical profession is notoriously stressful, with long hours, emotional strain, and high-stakes decision-making. Physicians often work in environments where trauma, suffering, and death are daily realities. This chronic stress can lead to burnout, depression, and anxiety—conditions that increase vulnerability to substance abuse. Additionally, doctors may self-medicate to cope with physical pain, insomnia, or mental health issues, believing they can manage their own treatment due to their medical knowledge.

Access to controlled substances is another risk factor. Physicians often have easier access to prescription medications, and some may rationalize their use as necessary for performance or relief. The culture of medicine, which often emphasizes perfection and stoicism, can discourage doctors from seeking help. Fear of professional repercussions, loss of license, or stigma may lead them to hide their addiction, delaying intervention until serious consequences arise.

The impact of physician addiction is profound. Impaired judgment, reduced concentration, and erratic behavior can compromise patient care and lead to medical errors. In extreme cases, addiction can result in malpractice, criminal charges, or loss of life. For the addicted physician, the personal toll includes damaged relationships, financial instability, and deteriorating health.

Fortunately, support systems exist to help physicians recover. Physician Health Programs (PHPs) offer confidential treatment, monitoring, and peer support tailored to medical professionals. These programs have high success rates, with many doctors returning to practice after rehabilitation. Early intervention is key, and colleagues are encouraged to report signs of impairment, such as unexplained absences, mood swings, or declining performance.

In conclusion, physician drug addiction is a complex and critical issue that demands attention and compassion. While the pressures of medicine can drive some doctors toward substance abuse, recovery is possible with the right support. Destigmatizing addiction, promoting mental health, and fostering a culture of openness are essential steps toward protecting both physicians and the patients they serve.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 8, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

By Professor Eugene Schmuckler PhD MBA MEd CTS

***

***

Physician gambling addiction is a growing concern that threatens both personal well-being and professional integrity. This essay explores its causes, consequences, and the urgent need for awareness and support.

Gambling addiction, or gambling disorder, is a recognized mental health condition characterized by an uncontrollable urge to gamble despite negative consequences. While it affects about 1% of the general population., its presence among physicians is particularly alarming due to the high stakes involved—both financially and ethically. Physicians are entrusted with lives, and addiction can impair judgment, compromise patient care, and lead to devastating personal and professional outcomes.

Several factors contribute to gambling addiction in physicians. The profession is inherently high-pressure, with long hours, emotional strain, and frequent exposure to trauma. These stressors can drive individuals to seek escape or excitement through gambling. Moreover, physicians often have access to substantial financial resources, making it easier to sustain gambling habits longer than others. The culture of perfectionism and stigma around mental health in medicine may also discourage seeking help, allowing addiction to fester in secrecy.

The consequences of gambling addiction for physicians are multifaceted. On a personal level, it can lead to financial ruin, strained relationships, and deteriorating mental health. Studies show that gambling activates the brain’s reward system similarly to drugs and alcohol, reinforcing compulsive behavior.

Professionally, addiction can result in medical errors, fraud, or even criminal activity—such as embezzling funds to cover gambling debts. These actions not only endanger patients but also erode public trust in the medical profession.

During the COVID-19 pandemic, gambling behavior intensified across many demographics, including healthcare workers. Increased isolation, stress, and access to online gambling platforms contributed to a surge in addiction cases. Physicians, already burdened by the pandemic’s demands, were particularly vulnerable. The rise of sports betting and fantasy leagues has further blurred the lines between entertainment and addiction, making it harder to recognize problematic behavior.

***

***

Addressing physician gambling addiction requires a multifaceted approach. First, medical institutions must foster a culture that encourages mental health support without stigma. Confidential counseling services, peer support groups, and educational programs can help physicians recognize and address addiction early. Licensing boards and hospitals should implement policies that balance accountability with rehabilitation, ensuring that affected physicians receive treatment rather than punishment alone.

Additionally, research into gambling disorder must continue to evolve. Institutions like Yale Medicine are leading efforts to understand the neurological and genetic underpinnings of addiction, which could inform more effective treatments. Public awareness campaigns can also help destigmatize gambling addiction and promote responsible behavior.

In conclusion, physician gambling addiction is a hidden crisis with far-reaching implications. It stems from a complex interplay of stress, access, and stigma, and its consequences can be catastrophic.

By promoting awareness, support, and research, the medical community can better protect its members and the patients they serve.

Posted on January 6, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

Professor Eugene Schmuckler PhD MBA MEd CTS

***

***

Navigating the Challenges of Passive-Aggressive Patients in Healthcare

In the complex landscape of healthcare, effective communication between providers and patients is essential for accurate diagnosis, treatment adherence, and overall patient satisfaction. However, passive-aggressive behavior—characterized by indirect resistance, subtle obstruction, and veiled hostility—can significantly hinder this process. Passive-aggressive patients present unique challenges that require emotional intelligence, patience, and strategic communication skills from healthcare professionals.

Passive-aggressive behavior often stems from underlying feelings of fear, resentment, or a perceived lack of control. Patients may feel overwhelmed by their diagnosis, skeptical of medical advice, or frustrated by systemic issues such as long wait times or insurance complications. Rather than expressing these concerns openly, they may resort to behaviors such as missed appointments, vague complaints, sarcasm, or noncompliance with treatment plans. These actions, though subtle, can disrupt care continuity and erode trust between patient and provider.

One of the most difficult aspects of managing passive-aggressive patients is identifying the behavior early. Unlike overt aggression, passive-aggression is cloaked in ambiguity. A patient might nod in agreement during a consultation but later ignore medical instructions. They may offer compliments laced with sarcasm or express dissatisfaction through third parties rather than directly. These indirect signals can leave providers confused and uncertain about the patient’s true feelings or intentions.

***

***

Addressing passive-aggressive behavior requires a nuanced approach. First, providers must cultivate a nonjudgmental environment where patients feel safe expressing concerns. Active listening, empathy, and validation can encourage more direct communication. For example, acknowledging a patient’s frustration with wait times or side effects can open the door to honest dialogue. Providers should also be mindful of their own reactions, avoiding defensiveness or dismissiveness, which can exacerbate the behavior.

Setting clear boundaries and expectations is another key strategy. Passive-aggressive patients often test limits subtly, so it’s important to reinforce the importance of mutual respect and accountability. Documenting interactions, treatment plans, and patient responses can help track patterns and ensure consistency. In some cases, involving mental health professionals may be beneficial, especially if the behavior is rooted in deeper psychological issues.

Ultimately, the goal is to transform passive-aggressive dynamics into constructive partnerships. This requires time, effort, and a willingness to engage with patients beyond surface-level interactions. When successful, it can lead to improved outcomes, greater patient satisfaction, and a more harmonious clinical environment.

In conclusion, passive-aggressive patients pose a unique challenge in healthcare, but they also offer an opportunity for providers to refine their communication skills and deepen their understanding of patient psychology. By fostering openness, setting boundaries, and responding with empathy, healthcare professionals can navigate these interactions effectively and promote better health outcomes for all.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on December 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Employer-sponsored healthcare benefit programs have become a cornerstone of modern employment, shaping not only the financial well-being of workers but also the overall health of society. These programs represent a partnership between employers and employees, where organizations provide access to medical coverage as part of compensation packages. While wages remain the most visible form of remuneration, healthcare benefits often carry equal or greater significance, influencing job satisfaction, retention, and productivity.

At their core, employer-sponsored healthcare programs are designed to reduce the financial burden of medical expenses for employees. Healthcare costs can be unpredictable and overwhelming, and insurance coverage provides a safety net against sudden illness or injury. By offering group plans, employers can negotiate better rates with insurers, spreading risk across a larger pool of participants. This collective approach makes healthcare more affordable than if individuals were to purchase coverage independently. For employees, the assurance of medical support fosters peace of mind, allowing them to focus on their work without the constant worry of healthcare expenses.

From the employer’s perspective, healthcare benefits serve as a strategic tool for attracting and retaining talent. In competitive labor markets, robust benefit packages can distinguish one company from another. Workers often weigh healthcare coverage heavily when deciding between job offers, and organizations that provide comprehensive plans are more likely to secure skilled professionals. Moreover, offering healthcare benefits demonstrates a company’s commitment to employee welfare, reinforcing a culture of care and responsibility. This perception can strengthen loyalty and reduce turnover, ultimately saving organizations the costs associated with recruiting and training new staff.

***

***

Beyond recruitment and retention, healthcare benefits contribute directly to workplace productivity. Employees who have access to preventive care and regular medical services are less likely to suffer from untreated conditions that impair performance. Routine checkups, vaccinations, and screenings help identify health issues early, reducing absenteeism and minimizing disruptions to workflow. In addition, healthier employees tend to be more engaged, energetic, and capable of sustaining high levels of output. Employers thus benefit from a workforce that is not only present but also performing at its best.

Employer-sponsored healthcare programs also play a role in shaping organizational culture. When companies invest in employee health, they send a message that well-being is valued. This can foster trust and strengthen relationships between management and staff. In many cases, healthcare benefits are paired with wellness initiatives such as gym memberships, mental health resources, or nutritional counseling. These programs encourage healthier lifestyles, which in turn reduce long-term medical costs and enhance overall morale. The integration of healthcare and wellness initiatives reflects a holistic approach to employee support, extending beyond the workplace into personal lives.

Despite their advantages, employer-sponsored healthcare programs are not without challenges. Rising medical costs place pressure on employers to balance affordability with coverage quality. Smaller businesses may struggle to provide comprehensive plans, limiting their competitiveness in attracting talent. Additionally, employees may face limitations in provider networks or coverage options, leading to dissatisfaction. The complexity of healthcare systems can also create confusion, requiring employers to invest in education and communication to ensure employees understand their benefits. These challenges highlight the need for ongoing innovation and adaptation in benefit design.

Looking ahead, employer-sponsored healthcare programs are likely to evolve in response to changing workforce expectations and healthcare landscapes. Remote work, diverse employee demographics, and advances in medical technology will influence how benefits are structured. Employers may increasingly emphasize flexibility, offering customizable plans that cater to individual needs. Digital health tools, telemedicine, and wellness apps are already becoming integrated into benefit packages, expanding access and convenience. As organizations continue to adapt, the central principle remains the same: supporting employee health is both a moral responsibility and a strategic advantage.

In conclusion, employer-sponsored healthcare benefit programs are more than a financial perk; they are a vital component of modern employment relationships. By reducing medical costs, attracting talent, enhancing productivity, and fostering a culture of care, these programs create value for both employees and employers. While challenges persist, the continued evolution of healthcare benefits promises to strengthen their role in shaping healthier, more resilient workplaces. Ultimately, the success of these programs lies in their ability to balance economic realities with the human need for security and well-being.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Shaping Well-being Beyond Medicine

Health is often thought of as the result of medical care, but in reality, it is deeply influenced by the conditions in which people are born, grow, live, work, and age. These conditions, known as social determinants of health, include a wide range of social, economic, and environmental factors that shape health outcomes. They are responsible for many of the differences in health status between individuals and communities. Understanding these determinants is essential for promoting fairness in health and designing policies that reduce disparities.

Economic Stability

Economic stability is one of the most powerful determinants of health. Individuals with steady income can afford nutritious food, safe housing, and preventive healthcare. Conversely, poverty increases vulnerability to chronic diseases, mental health challenges, and limited access to medical services. Families with fewer financial resources may struggle to afford medications or healthy diets, leading to higher rates of obesity, diabetes, and cardiovascular disease. Unemployment or unstable work further exacerbates stress, which itself is linked to poor health outcomes. Economic inequality directly translates into health inequality.

Education

Education shapes health both directly and indirectly. Higher educational attainment is associated with better employment opportunities, higher income, and improved health literacy. People with more education are more likely to understand medical information, adopt healthy behaviors, and navigate healthcare systems effectively. Limited education can perpetuate cycles of poverty and poor health. For instance, children who grow up in underfunded schools may face restricted opportunities, leading to lower lifetime earnings and poorer health outcomes. Education is therefore a critical lever for breaking intergenerational cycles of disadvantage.

***

***

Neighborhood and Physical Environment

The environment in which individuals live plays a crucial role in determining health. Safe neighborhoods with clean air, accessible parks, and reliable transportation promote physical activity and reduce exposure to pollutants. In contrast, communities with high crime rates, poor housing, and environmental hazards contribute to stress, injury, and illness. Food deserts—areas with limited access to affordable, healthy food—are a striking example of how environment shapes health. Residents in these areas often rely on processed foods, increasing risks of obesity and related diseases. Housing quality also matters: overcrowding, mold, or lead exposure can lead to respiratory illnesses and developmental delays.

Healthcare Access and Quality

Access to healthcare is a fundamental determinant, but it is shaped by social and economic factors. Insurance coverage, affordability, and cultural competence of providers influence whether individuals receive timely and effective care. Marginalized groups often face barriers such as discrimination, language differences, or lack of nearby facilities. Even when healthcare is available, disparities in quality persist. For example, minority populations may receive less aggressive treatment for certain conditions compared to others. Addressing these inequities requires systemic reforms that prioritize inclusivity and affordability.

Social and Community Context

Social relationships and community support networks significantly affect health. Strong social ties provide emotional support, reduce stress, and encourage healthy behaviors. Communities with high levels of trust and civic engagement often experience better health outcomes. Conversely, discrimination, racism, and social exclusion undermine health by increasing stress and limiting opportunities. Social cohesion and equity are therefore vital for fostering healthier societies.

Conclusion

The social determinants of health highlight that medicine alone cannot ensure well-being. Economic stability, education, environment, healthcare access, and social context collectively shape health outcomes and drive disparities. Addressing these determinants requires a holistic approach that integrates public health, social policy, and community action. By investing in education, reducing poverty, improving neighborhoods, and ensuring equitable healthcare, societies can move closer to achieving health equity. Ultimately, health is not just about treating illness—it is about creating conditions in which everyone has the opportunity to thrive.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

The Direct Reimbursement Payment Model allows physicians to receive payment directly from patients or employers, bypassing traditional insurance systems. This model emphasizes transparency, autonomy, and personalized care, offering an alternative to fee-for-service and managed care structures.

The Direct Reimbursement Payment Model is a healthcare financing approach in which physicians are paid directly by patients or sponsoring entities—such as employers—rather than through insurance companies or government programs. This model is gaining traction as a response to the administrative burdens, opaque billing practices, and fragmented care often associated with traditional insurance-based systems.

One prominent example of direct reimbursement is Direct Primary Care (DPC). In DPC, patients pay a recurring fee—monthly, quarterly, or annually—that covers a broad range of primary care services. These include routine checkups, preventive screenings, chronic disease management, and basic lab work. By eliminating third-party billing, DPC practices reduce overhead costs and administrative complexity, allowing physicians to spend more time with patients and focus on quality care.

***

***

Employers have also embraced direct reimbursement models to manage healthcare costs and improve employee wellness. In such arrangements, employers reimburse physicians or clinics directly for services rendered to their employees, often through a defined benefit structure. This can be part of a self-funded health plan or a supplemental offering alongside high-deductible insurance policies. The goal is to provide accessible, cost-effective care while avoiding the inefficiencies of traditional insurance networks.

Key advantages of the direct reimbursement model include:

Price transparency: Patients know upfront what services cost, reducing surprise billing and financial stress.

Improved access: Physicians often offer same-day or next-day appointments, extended visits, and direct communication via phone or email.

Lower administrative burden: Without insurance paperwork, practices can operate more efficiently and focus on patient care.

Stronger patient-physician relationships: More time per visit fosters trust, continuity, and better health outcomes.

However, the model is not without limitations. Direct reimbursement may not cover specialist care, hospitalization, or emergency services, requiring patients to maintain supplemental insurance. Additionally, the model may be less accessible to low-income populations who cannot afford recurring fees or out-of-pocket payments. Critics also argue that widespread adoption could fragment care and reduce risk pooling, undermining the broader goals of universal coverage.

Despite these concerns, the direct reimbursement model aligns with broader trends in healthcare reform, including value-based care, consumer empowerment, and decentralized service delivery. It offers a viable path for physicians seeking autonomy and for patients desiring personalized, transparent care. As healthcare continues to evolve, hybrid models that combine direct reimbursement with traditional insurance may emerge, offering flexibility and choice across diverse patient populations.

In conclusion, the Direct Reimbursement Payment Model represents a meaningful shift in how healthcare services are financed and delivered.

By prioritizing simplicity, transparency, and patient-centered care, it challenges the status quo and opens new possibilities for sustainable, high-quality medical practice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

In the competitive world of financial services, attracting and retaining clients is a constant challenge. To stand out, many financial advisors employ strategic marketing tactics known as “loss leaders”—free or discounted services designed to showcase value and build trust. These offerings serve as entry points for potential clients, allowing advisors to demonstrate expertise and initiate long-term relationships.

One of the most common loss leaders is the free initial consultation. This no-obligation meeting gives prospective clients a chance to discuss their financial goals, ask questions, and get a feel for the advisor’s approach. For the advisor, it’s an opportunity to assess the client’s needs and present tailored solutions. While no revenue is generated from this meeting, it often leads to paid engagements once the client feels confident in the advisor’s capabilities.

Another popular tactic is offering a complimentary financial plan or portfolio review. These services provide tangible insights into a client’s current financial situation and suggest improvements. By delivering real value upfront, advisors build credibility and demonstrate their analytical skills. Clients who receive actionable advice are more likely to continue working with the advisor on a paid basis.

Educational content also plays a key role in loss leader strategy. Advisors frequently host free webinars, workshops, or seminars on topics like retirement planning, tax strategies, or investment basics. These events not only educate attendees but also position the advisor as a thought leader. Attendees often leave with a better understanding of their financial needs and a desire to seek personalized guidance.

In the digital realm, advisors may offer free tools and assessments on their websites. These include retirement readiness calculators, risk tolerance quizzes, and budgeting templates. Such tools engage users and provide personalized feedback, creating a natural segue into one-on-one consultations. Additionally, offering free newsletters or eBooks helps advisors stay top-of-mind while delivering ongoing value.

Some advisors go further by waiving fees for introductory services, such as account setup or the first few months of investment management. This lowers the barrier to entry and encourages hesitant clients to try the service. Once clients experience the benefits, they’re more likely to commit long-term.

Loss leaders are not limited to high-net-worth individuals. Advisors targeting younger or less affluent clients may offer free debt management plans or budgeting assistance. These services address immediate concerns and build loyalty among clients who may become more profitable as their financial situations improve.

Ultimately, loss leaders are about building relationships. By offering something of value without immediate compensation, financial advisors demonstrate their commitment to helping clients succeed. This fosters trust, encourages engagement, and often leads to lasting partnerships. In a field where reputation and reliability are paramount, loss leaders serve as powerful tools for growth and differentiation.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic Definition: Scientific research depends on the referencing and citing of other research.

Modern Circumstance: The Google Scholar Paradox is that research which gets cited most often is whatever shows up in the top results of Google Scholar searches; regardless of its contribution to the field.

Paradox Example: The Google Scholar effect is a phenomenon when some medical and healthcare researchers pick and cite works appearing in the top results on Google Scholar regardless of their contribution to the citing publication.

Paradoxically they automatically assume these works’ credibility and believe that editors, reviewers, and readers expect to see these citations.

Posted on November 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to colleague Dan Ariely PhD, the Scitovsky Paradox and using the Kaldor–Hicks criterion, allocation A may be more efficient than allocation B, while at the same time B is more efficient than A.

Moreover, the Scitovsky paradox in welfare economics which is resolved by stating that there is no increase in social welfare by a return to the original part of the losers. It is named after the Hungarian born American economist, Tibor Scitovsky. According to Scitovsky, ther Kaldor-Hicks criterion involves contradictory and inconsistent results.

What Scitovsky demonstrated was it is possible that if an allocation A is deemed superior to another allocation B by the Kaldor compensation criteria, then by a subsequent set of moves by the same criteria, we can prove that B is also superior to A.

Posted on November 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

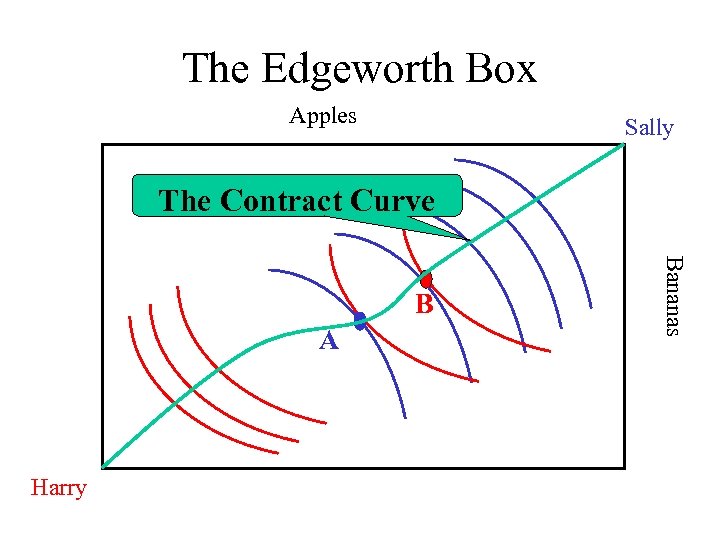

Irish economist Frances Edgeworth put forward the Edgeworth Paradox in his paper “The Pure Theory of Monopoly”, published in 1897.

It describes a situation in which two players cannot reach a state of equilibrium with pure strategies, i.e. each charging a stable price. A fact of the Edgeworth Paradox is that in some cases, even if the direct price impact is negative and exceeds the conditions, an increase in cost proportional to the quantity of an item provided may cause a decrease in all optimal prices. Due to the limited production capacity of enterprises in reality, if only one enterprise’s total production capacity can be supplied cannot meet social demand, another enterprise can charge a price that exceeds the marginal cost for the residual social need.

And so, according to colleague Dan Ariely PhD, the Edgeworth Paradox suggests that with capacity constraints, there may not be an equilibrium.

Nepo babies often go broke due to a mix of financial mismanagement, lack of resilience, and the illusion of inherited success. Their privileged upbringing can mask the need for discipline, adaptability, and long-term planning—traits essential for sustaining wealth.

The term nepo baby—short for nepotism baby—refers to children of celebrities or influential figures who benefit from family connections to launch careers, especially in entertainment, fashion, or media. While these individuals often start with significant advantages, including wealth, fame, and access, many struggle to maintain financial stability over time. The reasons are complex and rooted in both personal and systemic factors.

First, many nepo babies lack financial literacy. Growing up in environments where money flows freely, they may never learn budgeting, investing, or the value of money. Without these skills, they’re prone to overspending, poor investments, and unsustainable lifestyles. Lavish purchases—designer clothes, luxury cars, expensive homes—can quickly drain even sizable inheritances if not managed wisely.

Second, the illusion of guaranteed success can be dangerous. Nepo babies often enter industries where their family name opens doors, but that doesn’t guarantee longevity. Fame is fickle, and public interest can fade. If they don’t develop their own talents or work ethic, they may find themselves unemployable once the novelty wears off. This overreliance on family reputation can lead to complacency, making it harder to adapt when challenges arise.

Third, many nepo babies face identity crises and public scrutiny. Constant comparisons to their successful parents can erode confidence and create pressure to live up to unrealistic expectations. Some rebel by distancing themselves from their family’s legacy, while others try to prove themselves in unrelated fields. Either way, this struggle can lead to erratic career choices and unstable income streams.

Fourth, fame without privacy can fuel destructive habits. The entertainment world is rife with stories of young stars—many of them nepo babies—falling into substance abuse, reckless behavior, or toxic relationships. These issues not only affect mental health but also lead to legal troubles and financial loss. Without strong support systems or accountability, it’s easy to spiral.

Finally, inherited wealth can disappear quickly without proper estate planning. Trust funds and inheritances may be mismanaged or depleted by taxes, lawsuits, or poor financial advisors. Some nepo babies assume the money will last forever and fail to plan for long-term sustainability. Others are exploited by opportunistic friends or partners who take advantage of their naivety.

In contrast, those who succeed often do so by acknowledging their privilege, developing their own skills, and surrounding themselves with trustworthy mentors. They treat their inherited platform as a launchpad—not a safety net—and work to build something lasting.

In short, nepo babies go broke not because they lack opportunity, but because opportunity without discipline is a recipe for downfall. Wealth and fame are fleeting without the grit to sustain them. The lesson here isn’t just about celebrity—it’s a universal truth: success inherited must still be earned.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Turn Financial A-Ha Moments Into Lasting Change With Memory Re-Consolidation

By Rick Kahler MSFS CFP™

***

***

Have you ever had a light bulb moment about money?

Maybe you leave a workshop, a therapy session, or a conversation with a financial advisor, feeling as if you have finally cracked the code. You understand why you keep overspending. You see the pattern that keeps you procrastinating about saving and investing. You feel the reason you panic about money, even when you know you are okay. In that moment, it all seems so clear.

Yet a week later, you are right back at it. Swiping the credit card. Avoiding the budget. Losing sleep over the same worries you thought you had just solved. What happened to that breakthrough? Why did it not last?

I’ve experienced this myself, more times than I’d like to admit. Recently, I found a book that explains why: Unlocking the Emotional Brain by Bruce Ecker, Robin Ticic, and Laurel Hulley. The authors explain that lasting change happens through something called “memory re-consolidation.” It is the brain’s way of updating emotional patterns we have carried for years—often since childhood.

Most of us have old money stories tucked away in our emotional memory. Suppose, for example, as a child you were scolded for asking a neighbor how much money they earned. This and other similar experiences that left you feeling shamed or dismissed taught you that it was rude to talk about money.

Such early experiences are filed away as emotional truths. They shape what feels true, even years later as an adult, whether or not that “truth” is still relevant.

As an adult, you may have come to understand that talking about money is often essential for your emotional and financial well being. But when the moment comes to have a money conversation, your body still freezes up. That is not weakness. That is your brain pulling up the old file.

Here is where memory re-consolidation comes in. The brain does not update the file just because you think new thoughts. It updates when you have a new experience that feels different. Maybe someone listens without judgment, or you realize you are talking about money and still feel safe. That emotional mismatch tells the brain, “Maybe this file is not true anymore.”

But the update is not finished. To make the change stick, you have to hold both the old belief and the new experience together for a little while. It is like showing your brain two pictures: here is how it used to feel, and here is how it feels now. That moment of holding both is when the rewrite happens.

Even more interesting, the brain keeps the file open for several hours after the shift. What you do in that window can help the change settle in—or not. If you rush back into busyness or distractions, you might accidentally let the old version save itself again.

So what can we do to give those shifts a better chance of sticking? I have noticed that insights gained during a retreat or workshop, with ample time to focus and reflect, are more likely to last. Even in our everyday lives, we can slow down, even for a few minutes, to write about what we felt, check in with our bodies, or talk with someone who supports us. We can protect a little bit of quiet space before diving back into the noise.

The next time you have a money breakthrough, try giving yourself that space. Consciously notice both the old belief and the new experience. Give the re-consolidation time to settle in.

Then, the next time your brain pulls up that old money story, you’ll have access to the updated, more accurate version.

Posted on October 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What’s a polymath?

The definition of “polymath” is the subject of debate. The term has its roots in Ancient Greek and was first used in the early 17th Century to mean a person with “many learnings”, but there is no easy way to decide how advanced those learnings must be and in how many disciplines. Most researchers argue that to be a true polymath you need some kind of formal acclaim in at least two apparently unrelated domains. And, one of the most detailed examinations of the subject comes from Waqas Ahmed in his book The Polymath, published earlier this year.

Now, despite his many achievements, Ahmed does not identify as a polymath. “It is too esteemed an accolade for me to refer to myself as one,” he said. When examining the lives of historical polymaths, he only considered those who had made significant contributions to at least three fields, such as Leonardo da Vinci (the artist, inventor and anatomist), Johann Wolfgang von Goethe (the great writer who also studied botany, physics and mineralogy) and Florence Nightingale (who, besides founding modern nursing, was also an accomplished statistician and theologian).

What is a savant?

Savant syndrome is an exceedingly rare condition in which individuals with a developmental disorder or an intellectual disability possess extraordinary talents, knowledge, or abilities in a specific area. Savant syndrome may be congenital at birth or acquired later in life and is commonly associated with autism spectrum disorder (ASD). It may also coexist alongside other conditions, such as brain injuries . Individuals with savant syndrome were historically referred to with the term “idiot savant,” but negative connotations of the term “idiot” resulted in its abandonment and is now solely termed “savant.”

Famous individuals with savant syndrome include Kim Peek, who was able to calculate dates for any event hundreds of years into the past or future and inspired the movie the Rain Man. Stephen Wiltshire was mute and communicated through drawings of detailed city landscapes. Approximately 10% of individuals with autistic disorder have savant abilities. Less than 1% of the non-autistic population have savant syndrome. Therefore, not all savants have ASD, and not all persons with autismare savants.

What is a genius?

There is no scientifically precise definition of genius. When used to refer to the characteristic, genius is associated with talent but several authors systematically distinguish these terms. Walter Isaacson, biographer of many well-known geniuses, explains that although high intelligence may be a prerequisite, the most common trait that actually defines a genius may be the extraordinary ability to apply creativity and imaginative thinking to almost any situation.

The plural form of genius can be either geniuses or genii, pronounced [ jee-nee-ahy ], depending on the intended meaning of the word. Geniuses is much more commonly used. The plural forms of several other singular words that end in -us are also formed in this way, such as virus/viruses, callus/calluses, and status/statuses. Irregular plurals that are formed like genii, such as radius/radii or cactus/cacti, derive directly from their original pluralization in Latin. However, the standard English plural -es is often also acceptable for these terms, as in radiuses and cactuses.

Who is Mensa material?

Mensa members range in age from 2 to 106. They include engineers, homemakers, teachers, actors, athletes, students, and CEOs, and they share only one trait — high intelligence. To qualify for Mensa, they scored in the top 2 percent of the general population on an accepted standardized intelligence test.

Note: These descriptions are presented with some thanks to Chat GPT.

Posted on October 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

Classic Definition: The Boomerang[ing] paradox is a feedback loop or cycle where events come back positively or negatively. It is an interconnection between people that looks like an ecosystem.

Modern Circumstance: When our thoughts and words energetically go out into the world, it has the same effect as the boomerang. It will go all the way out and come back around. That part of the creation model is our thinking and speaking. We’re unconscious and co-creating our reality. The Boomerang effect is everywhere: politics, business, relationships, economics, environment, marketing, psychology and healthcare, etc.

PSYCHOLOGY

Paradox Example: Research has found that teaching people and patients about psychological biases can help counteract biased behavior. On the other hand, due to the innate need for preservation of a positive self-image, it is likely that teaching people about biases they hold, may cause a boomerang paradoxical effect in cases where being associated with a specific bias implies negative social connotations

MEDICINE

Paradox Example: Recent examples of a boomerang paradoxical drug effects is withosteoporosis medications such as Actonel, Boniva and Fosamax. These all belong to a class of drugs called bisphosphonates. They are supposed to strengthen bones, but some doctors report that long-term use of these drugs may actually pose a risk of certain unusual fractures.

ECONOMICS

Paradox Example: A characteristic of advanced economies like Australia is continual growth in household income and plunging costs of electric appliances, resulting in rapid growth in peak demand. The power grid in turn requires substantial incremental generating and network capacity, which is utilized momentarily at best. The result is the Boomerang Paradox, in which the nation’s rising wealth has created the pre-conditions for fuel poverty.

***

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Population health and public health are two interrelated disciplines that strive to enhance the health outcomes of communities. While they share a common mission—to reduce health disparities and promote wellness—their approaches, target populations, and operational frameworks differ significantly.

***

***

Public health is traditionally defined as the science and art of preventing disease, prolonging life, and promoting health through organized efforts and informed choices of society, organizations, public and private sectors, communities, and individuals. It focuses on the health of the general population and emphasizes broad interventions such as vaccination programs, sanitation, health education, and policy advocacy. Public health professionals often work in government agencies, nonprofit organizations, and academic institutions to implement community-wide initiatives that prevent disease and promote healthy behaviors.

***

***

In contrast, population health takes a more targeted approach. It refers to the health outcomes of a specific group of individuals, including the distribution of such outcomes within the group. This field is particularly concerned with the social determinants of health—factors like income, education, environment, and access to care—that influence health disparities. Population health strategies often involve data-driven interventions tailored to the needs of defined groups, such as rural communities, ethnic minorities, or patients with chronic conditions.

One key distinction lies in scope and granularity. Public health initiatives are typically designed for the entire population, aiming to create systemic change. For example, anti-smoking campaigns or water fluoridation programs benefit everyone regardless of individual risk. Population health, however, might focus on reducing diabetes rates among Hispanic adults in a specific urban area, using targeted outreach and culturally sensitive care models.

Another difference is in data utilization. Population health relies heavily on health informatics and analytics to identify trends, allocate resources, and evaluate outcomes. This evidence-based approach supports precision in addressing health inequities. Public health also uses data, but often at a broader level to guide policy and monitor general health indicators like life expectancy or disease prevalence.

Despite these differences, the two fields are complementary. Public health lays the foundation for healthy societies through preventive infrastructure, while population health builds on this by addressing nuanced needs within subgroups. Together, they form a holistic framework for improving health outcomes across diverse communities.

In today’s healthcare landscape, the integration of public and population health is increasingly vital. The COVID-19 pandemic underscored the importance of both approaches: public health measures like mask mandates and vaccination campaigns were essential, while population health efforts ensured vulnerable groups received targeted support.

In conclusion, while public health and population health differ in focus and methodology, they are united by a shared goal: to foster healthier communities. Understanding their distinctions enables more effective collaboration and innovation in health policy, care delivery, and community engagement.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com