BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 30, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities were mixed, as the markets processed a number of events and data. Unrest in China amid protests in the region in response to its zero-tolerance COVID policy provided a source of uneasiness for the global markets, despite some optimism that the country may ease COVID-related restrictions. Meanwhile, a looming December 9th potential national strike date for rail workers added to the anxiety, all ahead of tomorrow’s comments from Fed Chairman Jerome Powell of the FOMC.

Equity news was light, with Dow member UnitedHealth Group issuing mixed 2023 guidance, while Chemours issued a full-year outlook that came in below estimates.

In economic news, home prices cooled, and the Consumer Confidence Index [CCI] fell for the second straight month.

Treasury yields were higher, and the U.S. dollar gained modest ground, while crude oil and gold prices advanced. Asia finished mostly to the upside, with mainland Chinese and Hong Kong markets leading the way amid the lingering optimism that COVID-19 restrictions may ease and as China announced further measures to support its property market.

Europe ended a choppy session mixed as the markets monitored the developments in China, as well as diverging economic data in the region.

Posted on November 29, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

More than 300 people are still dying each day on average from covid-19, most of them 65 or older, according to data from the Centers for Disease Control and Prevention. While that’s much lower than the 2,000 daily toll at the peak of the delta wave, it is still roughly two to three times the rate at which people die of the flu — renewing debate about what is an “acceptable loss.”

And, U.S. equities started off the new week with solid losses, as protests in China over its zero-tolerance COVID policy kept investors on edge. Adding to the mix, BlockFi filed for bankruptcy amid the continued fallout within the cryptocurrency markets. Equity news was in short supply on this Cyber Monday, with reports suggesting Black Friday weekend activity was solid despite the highly inflationary environment, while gaming stocks were in focus following a tentative agreement to renew casino licenses in Macau.

The economic calendar was light today, with the lone report of note showing manufacturing activity in the Dallas region unexpectedly improved but remained solidly in contraction territory.

Treasury yields were mixed, while the U.S. dollar rallied, crude oil prices were higher, and gold traded to the downside.

Markets in Asia and Europe finished lower amid the global uneasiness toward China.

Posted on November 29, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA

***

GivingTuesday, often stylized as #GivingTuesday for the purposes of hashtag activism, is the Tuesday after Thanksgiving in the United States. It is touted as a “global generosity movement unleashing the power of people and organizations to transform their communities and the world”.

Posted on November 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

All three major indexes closed higher during the Thanksgiving-shortened week, and if history is any indication, this rally has room to run through the end of the year. The Thanksgiving–New Year’s stretch has typically been a great one for stocks, with the S&P rising 71% of the time during the period since 1950. Of course, shrinking corporate profits and the FOMC’s rate hikes might play the spoiler this year.

The November jobs report will drop on Friday, and it’s expected to show the second straight monthly deceleration in US employment growth. Still, the economy is projected to have added 200,000 jobs last month, which would indicate a still-healthy labor market and keep the Fed on its rate-hiking path.

Posted on November 26, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

U.S. equities ended the day mixed, but the holiday-shortened week higher. Trading was subdued in today’s abbreviated session, and a dormant economic calendar was unable to provide any sway. Equity news was also in short supply, but shares of Activision Blizzard fell in the wake of a report that mentioned Microsoft’s $69 billion bid to acquire the video game maker could face some legal scrutiny from regulators.

Meanwhile, the retail sector was in focus, as any data on how this year’s Black Friday is shaping up was of heightened interest.

Treasury yields diverged, and the U.S. dollar nudged lower, while crude oil prices declined, and gold traded higher.

Asian and European stocks were mixed, as international markets continued to grapple with recent inflation data and its potential impact on monetary policy decisions.

Posted on November 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities accelerated to the upside to finish solidly higher amid a slew of data heading into the Thanksgiving holiday break. The move upward came following the release of the minutes from the Fed’s November monetary policy meeting which indicated some caution among Committee members. The economic calendar was robust, as durable goods orders came in much stronger than expected, along with new home sales and consumer sentiment, while mortgage applications rose for a second-straight week.

However, not all the reports were positive as weekly initial jobless claims rose and preliminary reads on manufacturing and services output both showed contraction after falling more than expected. Earnings reports continued to pour in, with Deere & Company rallying following its results, while HP and Autodesk lowered their guidance.

Treasury yields were lower, and the U.S. dollar fell, as did crude oil prices, while gold gained ground.

Asia finished mostly higher, though Japan was closed for a holiday, and Europe was mixed as the markets digested Eurozone and U.K. manufacturing and services data that also showed contraction in activity.

Posted on November 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities rose in a somewhat subdued session amid a holiday-shortened week, with the markets closed on Thursday for Thanksgiving and trading in an abbreviated session on Friday. Equity reports provided some positive earnings surprises, as Dell Technologies bested expectations, as did Dollar Tree, but the company tightened its full-year earnings outlook to the lower half of its previous guidance. Best Buy also beat forecasts, while it offered optimistic guidance and said it will resume its share repurchase program after pausing it in Q2, and Dick’s Sporting Goods rallied in the wake of its quarterly results. And, both Abercrombie & Fitch and American Eagle popped by double digits after topping earnings projections.

Today’s economic calendar was light, with the most notable report being the Richmond Fed Manufacturing Index, which remained in contraction territory.

Treasury yields were mostly lower, and the U.S. dollar declined, while crude oil prices gained ground, and gold was nearly flat.

Asian stocks ended mixed and European stocks were mostly higher, as investors focused on China’s response to its growing number of COVID cases.

Posted on November 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks declined in the first session of the holiday-shortened week, as the economic docket was void of any major releases. The economic calendar will heat up on Wednesday, with reports on durable goods orders, manufacturing and services PMIs, consumer sentiment, and new home sales, as well as the minutes from the Fed’s November monetary policy meeting.

The equity front was also quiet today, but Dow member Walt Disney Company’s announcement that Robert Iger is returning to the company as CEO boosted its shares. In other equity news, Dow component Merck & Co. Inc. announced a $1.35 billion acquisition of clinical stage biotech company Imago BioSciences Inc.

The Treasury yield curve continued to invert ahead of this week’s economic data and following recent positive inflation reports, though the U.S. dollar rallied. Crude oil prices extended a recent decline and gold was lower.

Asian stocks finished mostly lower amid lingering COVID concerns in China, and European stocks ended the day mixed as the global markets continued to assess the trajectory of monetary policies across the world.

Posted on November 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: It’ll be a short but stuffed Turkey Day week for investors. In the lead-up to Thanksgiving, when markets will close, we’ll get another batch of earnings reports and minutes from the previous Fed meeting. Traders will have to clock in on Black Friday for a half day.

Stock spotlight: The e-scooter rental company Bird is probably grateful that FTX’s implosion is stealing the spotlight from its own collapse. Last week, the company said it overstated revenue for more than two years and is warning it could go bankrupt if things don’t turn around. Currently a penny stock, Bird will be de-listed by the NYSE if its share price doesn’t rise above $1 by the end of the year.

Disney just announced that former CEO Bob Iger would return to his role atop the entertainment giant, replacing his successor Bob Chapek, who’s been CEO for less than three years.After leading the company for 15 years, Iger handed over the reins to Chapek in February 2020. It was an unexpected choice, given that streaming boss Kevin Mayer was seen as a more likely heir to the Disney throne than Chapek, who led the parks and entertainment division. But Iger had reportedly handpicked Chapek as his successor, and repeatedly said he was satisfied with being retired. “I can’t think of a better person to succeed me in this role,” Iger said in March 2020.

Elizabeth Holmes, the founder and former CEO of the doomed medical startup firm Theranos, has been sentenced to 11.25 years in prison for her role in defrauding investors and consumers about the potential of her company’s blood-testing device.

Holmes’ sentence will be followed by three years of supervised release. She will be required to self-surrender at a later date, according to NBC.

***

U.S. equities ended the day higher and the week mostly lower in a choppy trading session, as investors digested mixed corporate results and some disappointing economic data. Earnings were in focus with the season coming to a close, as Applied Materials handily beat the Street’s forecasts and upped its guidance, Gap posted a profit on the back of a tax benefit, making it unclear if it is comparable to forecasts, and Williams-Sonoma saw record earnings growth but fell short of predictions.

Economic reports were lackluster, as existing home sales slumped amid the persistent rise in interest rates, and the Leading Economic Index tumbled double what was expected.

Treasury yields rose following the economic data, as did the U.S. dollar, while crude oil and gold prices declined.

European stocks were higher despite geopolitical tensions remaining, and as the markets continued to digest the U.K. budget announcement. Markets in Asia finished out a volatile week mixed in a quiet trading session.

Posted on November 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities ended the day lower in a cautious trading session as the markets reacted to a host of economic and corporate data. Investors also weighed comments from Fed officials who signaled that the rate-hiking campaign to slow the pace of inflation is not considered sufficiently restrictive.

On the economic front, housing starts and building permits fell, jobless claims moderated slightly more than expected, while manufacturing activity in Philadelphia tumbled.

Earnings reports again offered mixed results, as Cisco Systems beat on both the top and bottom lines, but NVIDIA fell well short of estimates amid the continued problems plaguing the chip industry, and Macy’s topped forecasts amid strength in its luxury units.

Treasury yields were higher, and the U.S. dollar rose, while crude oil prices fell, and gold lost ground.

European stocks were lower for the most part, as geopolitical tensions dampened investor sentiment, and as the U.K. announced its new budget plans. Markets in Asia finished mostly lower amid weakness in technology stocks.

Posted on November 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities finished lower in choppy action amid a full slate of economic reports, including the Import Price Index, which fell at a slower pace than expected to complete October’s inflation picture. In other economic news, retail sales rose at a faster rate than anticipated, the Federal Reserve’s report on industrial production and capacity utilization marked an unexpected decline for both, and business inventories rose less than predicted. Housing data was also in focus, as the NAHB Housing Market Index indicated home builder sentiment dropped more than expected and to a fresh post-pandemic low, while mortgage applications were up for the first time in eight weeks.

Earnings reports offered varied results, as Target missed earnings expectations and delivered disappointing guidance, while Lowe’s posted a positive earnings surprise and raised its full-year outlook. In other equity news, shares of Discover Financial are rising after the company announced that it would resume its share repurchase program.

Treasury yields were lower, the U.S. dollar declined slightly, and crude oil prices fell, while gold gained modest ground. European stocks were lower following a host of inflation data in the region, and as geopolitical tensions surrounding the war in Ukraine continued to put a damper on sentiment.

Asian stocks ended the day lower in a quiet trading session, as markets in mainland China and Hong Kong were unable to continue a recent rally.

Posted on November 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Some of the biggest players in the financial industry are launching a digital dollar pilot program while the crypto sector reels from FTX’s collapse. About a dozen global giants, including Citigroup, HSBC, Mastercard and Wells Fargo, announced plans on Tuesday to test use of a digital token for 12 weeks in conjunction with the Federal Reserve Bank of New York, with the intention of examining how effective a digital currency is in speeding up payments.

U.S. equities posted gains following the release of a softer-than-expected read on wholesale price inflation. The report came in the wake of last week’s consumer price inflation release that continued to temper expectations regarding how aggressive the Fed could remain with its monetary policy tightening.

However, stocks finished well off the highs today, as geopolitics again flared following reports of Russian missiles crossing into NATO-member Poland, killing two individuals. The economic docket also offered the Empire Manufacturing Index, which showed that manufacturing activity in the New York region expanded, versus estimates calling for it to remain in contraction territory. Some retail heavyweights released earnings reports, as Dow members Walmart and Home Depot both beat estimates, with the former raising its guidance and authorizing a new share repurchase program, and the latter reaffirming its full-year outlook.

Treasury yields declined following the inflation data, and the U.S. dollar finished lower. Crude oil prices rose, and gold also traded to the upside.

Stocks in Asia finished mostly higher, led by mainland Chinese and Hong Kong stocks, amid moves to ease China’s COVID restrictions. European stocks were also higher for the most part as investors continued to digest recent monetary policy actions as a result of inflationary concerns.

Posted on November 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

U.S. equities declined in a choppy and cautious trading session as investors await a host of notable economic reports later this week. The economic docket, while empty today, will round out the inflation picture with release of the Producer Price Index (PPI), as well as the Import Price Index on Wednesday. The releases will follow last week’s cooler-than-expected Consumer Price Index (CPI), which appeared to soothe concerns about how aggressive the Fed will need to remain as FOMC Vice Chair Lael Brainard said it will “probably be appropriate soon” to slow down the pace of interest rate hikes. And Hasbro was the S&P 500’s biggest loser of the day as Bank of America downgraded the stock.

Treasury yields were mostly higher, and the U.S. dollar rose, paring some of last week’s tumble.

Crude oil prices were lower, while gold reversed to the upside following losses earlier in the day.

Equity news was light, with Tyson Foods missing on the bottom line, but reporting record sales for the year and upping its quarterly dividend.

Stocks in Asia were mixed, with Hong Kong leading the region in gains following a jump in property stocks, while European stocks ended the day mostly higher in cautious trading.

Cryptocurrency lender BlockFi just admitted it has significant exposure to Sam Bankman-Fried’s crypto exchange FTX, and associated entities, that last week filed for bankruptcy.

Finally, although it’s become more difficult to find qualified healthcare professionals, it’s proving just as difficult to retain staff, especially when working with fewer resources. At the recent HR Healthcare conference in Austin, much of the retention conversation focused on improving the quality of work life and flexibility. But we want to hear how you’re solving retention and staffing problems: Share your insights right here on the ME-P.

Posted on November 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Elizabeth Holmes will find out how much time she’s spending in prison. The Theranos founder will be sentenced on Friday after being found guilty of fraud for lying to investors about her blood-testing startup. Prosecutors want 15 years.

Meanwhile, beaten-down tech stocks were the stars of last week’s rally, staging their biggest two-day pop since the financial crisis after inflation numbers came in cooler than expected. Investors still caution that this might be a classic case of a “bear market rally,” or a brief glimpse of the sun before the storm clouds return. Corporations haven’t exactly been lighting it up with profits right now.

Posted on November 12, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities ended the day and week higher following Thursday’s trading session, which posted the largest daily gain since 2020.

Yesterday’s sharp rise came in the wake of a cooler-than-expected October consumer price inflation report, which seems to be curbing expectations regarding how aggressive the Fed could remain with its monetary policy tightening. The ongoing turmoil in the cryptocurrency markets kept sentiment in check after crypto exchange FTX.com voluntarily began Chapter 11 bankruptcy procedures.

The bond markets were closed today in observance of the Veteran’s Day holiday, giving Treasuries a breather after yesterday’s plunge, while the U.S. dollar continued its fall.

Crude oil prices were sharply higher, and gold gained modest ground. News on the equity front was focused on some tertiary earnings reports, with Toast Inc. posting a wider loss that expected, and Doximity beating on both the top and bottom lines, as well as announcing a new share repurchase program.

The lone economic report for today showed that consumer sentiment for November deteriorated more than expected. Stocks in Asia rallied following yesterday’s gains in the U.S and amid news that China will relax travel restrictions, while European stocks ended the day mixed, tempering the previous trading session’s solid gains.

Posted on November 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Unlike banks, the New York Stock Exchange doesn’t close on Veterans Day. Wall Street will have a full day of trading, and operate as usual on Veteran’s Day. Bond markets, which work with the federal government, will also be closed.

***

***

U.S. stocks closed sharply higher yesterday, with all three major indexes posting their best day of gains since 2020 as investors cheered signs that U.S. inflation finally might be headed lower.

For example, the Dow Jones Industrial Average shot up about 1,198 points, or 3.7%, ending near 33,712, marking its highest level since August and its best daily percentage gain since May 2020, according to Dow Jones Market Data. The S&P 500 index gained 5.5% and the NASDAQ Composite Index closed up 7.4%, their best daily percentage increases since 2020. The sharp rally on Wall Street was led by gains in technology and communication shares, segments of the S&P 500 that booked massive gains of about 8.3% and 6.3%, respectively, according to FactSet.

Buyers came out in force after the release of October’s consumer-price index showed a 7.7% annual rate of inflation, down from 9.1% this summer, while spurring hopes that the Federal Reserve might be making headway in its fight to bring inflation down to its 2% target.

That took some of the attention off the ongoing woes at crypto exchange FTX, with bitcoin down near a 2-year low. The 10-year Treasury rate also dropped to about 3.8% Thursday, down from a 4.2% high in October ahead of the three-day weekend for the U.S. bond market, which will remain closed on Friday for Veterans Day. U.S. stock exchanges, however, will remain open Friday.

The S&P 500 (^GSPC) shed over 2%, while the Dow Jones Industrial Average (^DJI) fell by nearly 650 points, or roughly 2%. The technology-heavy Nasdaq Composite (^IXIC) dragged down by almost 2.5%, or 260 points.

Meanwhile, volatility in the cryptocurrency markets continued as Binance Holdings ditched its plans of acquiring FTX.com, which has experienced some liquidity issues. Earnings reports continued to trickle in, with Dow member Walt Disney Company missing Q4 expectations. In other equity news, Meta Platforms announced large-scale layoffs as the company tries to become a more leaner communication services firm.

Treasuries were mixed, and the U.S. dollar was solidly higher, while crude oil prices fell, and gold saw some pressure. Economic news was light, with mortgage applications falling for a seventh-straight week.

Asia finished mixed following some Chinese inflation data, and Europe also diverged.

Posted on November 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities finished higher, but well off the highs of the day, as some caution may have set in ahead of the results of today’s midterm elections. The economic docket was relatively light, with the most notable report being the Small Business Optimism Index, which declined in line with expectations versus the prior month.

However, later this week, we will get a key read on October’s Consumer Price Inflation (CPI), along with commentary from FOMC officials after last week’s rate hike. Treasury yields were lower, and the U.S. dollar lost ground, while crude oil prices fell, and gold jumped.

Earnings reports offered varied results, as Lyft posted a larger-than-expected loss, while Activision Blizzard and DuPont beat earnings estimates, with the latter announcing a new share repurchase program. Asian stocks ended mixed ahead of a busy conclusion to the week, while European stocks were higher, as the international markets grapple with economic data and recent monetary policy actions.

Posted on November 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

The outcome of today’s midterm elections could be influenced by something the government has little control over: the cost of filling up your car with gas. Since the 1970s, presidential approval ratings have tended to sag when gas prices rise. And that correlation has been especially pronounced this year as inflation has run rampant and gas prices have spiked.

The Washington Post found that the share of Americans who said the country was on the right track has moved remarkably in sync with gas prices.

Since gas prices peaked in June, the correlation between Democratic generic-ballot polling and the price of gas clocked in at minus-.91, nearly a perfect inverse correlation (which is minus-1).

NOTE: Recall that correlation is NOT causation!

Why are gas prices so powerful?

Gas prices are the only consumer good whose price we’re reminded of virtually every time we leave the house, experts say. Unlike salmon fish or outdoor patio furniture, ties, shirts or sneakers, the price of gas is advertised in size-500 font on huge signs that you can’t help but notice. In fact, gas prices have been so beaten into us that they can change our behavior over decades. Researchers at the University of Pennsylvania discovered that people who experienced raging gas prices in their formative driving years in the 1970s seemed less likely to drive to work 20 years later than other age cohorts.

The curious part about the link between voter sentiment and gas prices is that gas prices have very little to do with the White House. Gas prices are largely influenced by the price of crude oil, which is a globally traded commodity. That commodity has been dealt a shock this year by Russia’s invasion of Ukraine, technical snags with refineries in the US, and OPEC+’s production cuts.

Still, President Biden’s team is fully aware of the importance of gas prices, which explains his incessant attacks on oil companies’ windfall profits, his releasing of crude from the Strategic Petroleum Reserve, and his visit to Saudi Arabia, a major oil producer.

Price check?

The current national average for a gallon of unleaded gas is $3.80, per AAA. That’s roughly the same as a month ago, down significantly from the record of more than $5, but about 38 cents more than a year ago.

Posted on November 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks ended the day higher as the markets await some key data later this week and amid some likely caution ahead of tomorrow’s mid-term election. In the final hour of trading, the economic calendar released data on consumer credit for September, which showed that consumers borrowed less than expected. The economic docket will heat up later this week, headlined by the first read on consumer price inflation in the form of the Consumer Price Index, which will be accompanied by some commentary by Fed officials. Treasury yields rose, and the U.S. dollar saw pressure.

Crude oil prices declined, while gold nudged higher.

In equity news, Dow member Apple said iPhone shipments will be hampered by the impact of the COVID lock-downs in China, Meta Platforms is reportedly set to announce large-scale layoffs, and Dow component Walgreens Boots Alliance announced that a company it controls has agreed to acquire Summit Health-CityMD.

Asian stocks rallied, led by Hong Kong markets, while European stocks were mixed to begin the week, as the international markets continued to digest recent global monetary policy decisions.

Posted on November 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

The American Hospital Association (AHA) is advocating for the creation of a new hospital designation for certain urban safety net hospitals.

In a report released in mid-October 2022, as well as in an accompanying fact sheet and letter sent to congressional leaders, the AHA defines these so-called Metropolitan Anchor Hospitals (MAHs), outlines their importance to the communities they serve, and explains why MAHs deserve supplemental financial support from the government.

Posted on November 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reportersand BLS

***

***

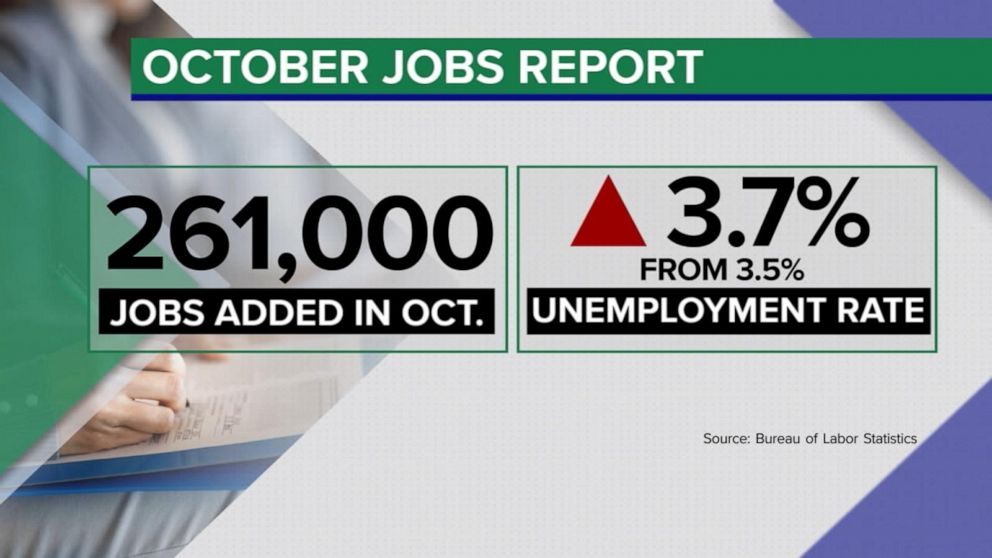

U.S. equities posted a weekly loss, despite ending the day higher in a choppy trading session, following a larger-than-expected increase in non-farm payrolls for October, 2022. The choppiness came amid an increase in the unemployment rate that was also above estimates, and in the wake of FOMC Chair Powell’s comments earlier this week, in which he reiterated the central bank’s aim at cooling the robust labor market.

Earnings surprises were mostly positive, as Amgen bested expectations and upped its guidance, Starbucks also exceeded estimates despite a tumble in sales in China, and PayPal posted upbeat results and announced a collaboration with Apple, while DoorDash rose despite posting a wider-than-expected loss.

Treasury yields were mixed, and the U.S dollar erased all of yesterday’s rally, while crude oil and gold prices surged.

Overseas, Asian stocks were higher for the most part, led by a rally in the Hong Kong markets. European stocks ended the volatile week on a positive note, as the international markets continued to digest the implications of monetary policy actions from central banks all over the world.

Posted on November 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities extended yesterday’s sharp drop that followed the Federal Reserve’s fourth-straight 75-basis point rate hike and some hawkish comments. As a result of the Fed’s monetary policy decision, Treasury yields and the U.S. dollar climbed noticeably higher. The Fed’s rate hike was trailed by today’s announcement from the Bank of England to hike its benchmark interest rate by 75 bps, though it tried to suppress expectations of future aggressiveness of that magnitude. The U.S. dollar’s rally came as the British pound fell, along with the euro, as the markets digested the monetary policy actions and comments.

Crude oil prices fell, and gold traded lower. In economic news, jobless claims dipped, the trade balance widened more than expected, Q3 productivity rebounded less than fore-casted and labor costs moderated more than projected. Additionally, factory orders figures were mixed, along with October reads on services sector output. Earnings season continues to roll on, with Qualcomm cutting its guidance, though eBay topped estimates and issued a positive outlook. Moreover, Booking Holdings topped expectations and Marriott decreased despite exceeding profit projections.

Asian stocks declined, though markets in Japan were closed for a holiday, and European stocks were mostly lower as the markets digested the decisions from the Fed and Bank of England.

U.S. equities finished lower with the Dow whipsawing within a more than 900-point range following the Fed’s monetary policy decision. The Central Bank raised rates by 75 basis points for a fourth-straight meeting, but opened the door to slowing within its statement. However, in his presser following the announcement, Chairman Powell reiterated that any notion of a pause was premature.

Treasury yields were mixed and the U.S. dollar traded to the upside, while crude oil prices gained ground, and gold saw a modest loss. In economic news, mortgage applications fell for a sixth-straight week even as mortgage rates snapped a string of increases, and ADP’s private sector employment report came in above estimates ahead of Friday’s key labor report.

Earnings season continued to roll on, with Advanced Micro Devices missing earnings forecasts, and CVS Health exceeding profit projections and raising its guidance. Ford Motor Company reported October sales that showed a year-over-year decline, but EV sales grew.

Asia finished mixed with mainland Chinese markets and Hong Kong continuing rallies, while Europe also diverged amid some likely trepidation ahead of the Fed decision.

Posted on November 2, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities were modestly lower, as investors awaited tomorrow’s conclusion of the Federal Open Market Committee (FOMC) meeting. The Fed is widely expected to hike the target for its fed funds rate by another 75-basis points. On the economic front, the Job Openings and Labor Turnover Survey (JOLTS) posted an unexpected rebound—indicating a still-tight labor market—which seems to be enhancing monetary policy tightening concerns. Reports on manufacturing showed that activity remained in expansion territory, while construction spending unexpectedly rose month-over-month.

In equity news, pharmaceutical companies Eli Lilly and Pfizer both topped earnings estimates, while the former lowered its full-year guidance, and the latter raised its outlook.

Treasury yields were mixed, while the U.S. dollar ended little changed in choppy action. Crude oil prices gained ground, and gold was higher.

And, Asian stocks finished to the upside amid a host of mixed economic news, and after the Reserve Bank of Australia hiked rates by 25-basis points for a second-straight meeting. European markets were mostly higher in the wake of mixed manufacturing data, and ahead of today’s decision by the FOMC.

Posted on November 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities ended the day in the red, failing to continue last week’s positive momentum. The moves came amid a quiet day on the economic and earnings fronts, but both are set to heat up as the week progresses.

In earnings news, Global Payments bested estimates and reaffirmed its guidance, and Emerson Electric also beat the Street, while also announcing the sale of a majority stake in its climate unit to Blackstone.

Meanwhile, a couple of reads on regional manufacturing showed activity continued to contract. Treasury yields traded higher and the U.S. dollar gained ground, continuing to rebound from a recent drop, while gold and crude oil prices were lower.

Stocks in Asia were mixed amid a slew of economic data in the region, and Europe ended higher as investors continued to digest last week’s 75 basis point rate hike by the European Central Bank.

Posted on October 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The New York Stock Exchange will suspend Twitter shares today as Elon Musk closes in on a takeover. Musk just bought the social media company for $44 billion after trying to walk away from the deal.

***

Stocks Ended Mixed in Volatile Day Full of Reports

U.S. stocks finished mixed in a choppy trading session, as a host of earnings and economic news were released. The markets digested a second-straight 75 basis point rate hike by the European Central Bank (ECB).

Shares of Meta Platforms tumbled after missing earnings estimates and forecasting much higher-than-expected capital expenditures, while Dow members Caterpillar, McDonald’s, Honeywell, and Merck all rallied after beating earnings expectations.

The economic calendar is full as Q3 GDP growth came in stronger than expected, and weekly initial jobless claims were lower than anticipated, but durable goods orders missed forecasts. Treasury yields fell following the data, and the U.S. dollar rebounded from a recent drop amid the ECB rate hike.

Crude oil prices were higher, and gold dipped. Asia diverged as the markets remained choppy, while Europe ended higher following the ECB’s monetary policy decision and amid the flood of earnings reports.

Posted on October 27, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities closed out a volatile session mixed as the markets digested a host of quarterly results with earnings season kicking into high gear. Information Technology and Communications Services sectors were the biggest laggards in the wake of disappointing reports from Google’s parent Alphabet, as well as Dow member Microsoft.

Meanwhile, Dow component Boeing was lower despite optimism about its free-cash flow performance, but Dow member Visa rallied following its results.

Housing data dominated the economic front today, with mortgage applications falling for a fifth-straight week, and new home sales dropping amid the spike in interest rates in September.

Treasury yields were lower and the U.S. dollar tumbled to alleviate some uneasiness in the markets, while a smaller-than-expected rate hike out of Canada appeared to also soothe some nerves.

Crude oil prices were sharply higher, and gold traded to the upside.

Asia finished higher though choppiness remained, while Europe saw widespread gains amid cautious trading ahead of tomorrow’s monetary policy decision from the European Central Bank.

October is National Financial Planning Month—an ideal time to plan your financial future. The end of the year is approaching and a new one will soon begin, so this is the right time to think about what you have done in 2022 and what you could do in 2023. You might want to do something new; you may want to do some things differently.

***

***

GREAT NEWS: But what about financial planning specificity for physicians, nurses and all medical professionals?

Posted on October 26, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks Extend Rally as U.S. Dollar and Bond Yields Cool Off

U.S. stocks traded higher as Treasury yields and the U.S. dollar pulled back, while investors digested a host of corporate results.

Earnings reports painted a mixed picture, as Dow member Coca-Cola beat earnings estimates and raised its guidance, while Dow member 3M also announced a positive earnings surprise, but lowered its full-year outlook. Additionally, General Electric missed earnings expectations and lowered guidance, and General Motors topped profit projections. In economic news, home prices declined more than expected in August, consumer confidence decreased, and regional manufacturing fell more than fore-casted.

Crude oil and gold prices gained ground.

Markets in Asia finished mixed as economic uncertainty continued to weigh on conviction, while European stocks finished mostly higher following economic reports and the political situation in the U.K.

Posted on October 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks ended the day higher, adding to last week’s rally, which was the biggest advance since June. The three major stock averages climbed for the second straight trading day, but this rally will face a big test in the upcoming earnings season. Left out in the cold were Chinese tech stocks like Alibaba, which plunged as markets reacted (rather negatively) to China’s President Xi Jinping securing an unprecedented third term and packing the country’s leadership with loyalists.

Treasury yields were mixed, as longer-term rates reversed to the upside and seemingly weighed on growth sectors.

The markets awaited this week’s flood of earnings reports amid a day light in equity news, headlined by Tesla’s decision to cut prices for some of its vehicles in China. Political developments out of China and the U.K. were also in focus, along with a flood of Manufacturing and Services PMIs in the U.S. and abroad, which mostly showed a slowdown in activity.

The U.S. dollar was unchanged, while crude oil and gold prices edged lower.

Asian stocks finished mixed with mainland Chinese and Hong Kong equities tumbling, while Europe ended higher despite some

Posted on October 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

HAPPY DIWALI

By Staff Reporters

***

***

Happy Diwali! Hindus, Sikhs, Jains, and Buddhists around the world will celebrate India’s “festival of lights” today. In a sign of growing recognition of the festival, New York City announced last week that Diwali will become an official school holiday.

Earnings: If earnings season were a music festival, the headliners are about to come onstage. Corporate titans Amazon, Microsoft, Apple, Alphabet, and Meta are among the ~150 S&P companies that will give financial updates this week.

Economic data: The US economy shrank during the first two quarters of the year. We’ll find out whether it grew again in Q3 when fresh GDP numbers drop on Thursday (it’s expected to have). Plus, the Fed’s preferred measure of inflation will be released on Friday.

Posted on October 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Forecasts Cognitive [Mental] Dissonance?

By Staff Reporters

***

***

A Bloomberg economic model forecast a 100% chance of a US recession within 12 months

Jeff Bezos warned companies to “batten down the hatches” in response to Goldman Sachs’s CEO saying there’s a good chance we’ll have a recession.

Elon Musk guesstimated that we’re going to be in a recession “probably until spring of ’24.”

Gwyneth Paltrow said, “The economy sucks.”

BUT, Bank of America CEO Brian Moynihan (the one with the epic vocabulary) said that while analysts are warning of recession and slower spending, “We just don’t see [that] here at Bank of America.” Transaction volumes for its customers jumped 10% in September and the first half of October over a year earlier.

And, American Express’s CEO said, “We’re not seeing any changes in consumer spending” and predicted a strong holiday quarter for retail and travel.

United Airlines’s CEO is “so optimistic about 2023.”

Many business leaders are forecasting an economic downturn. But the execs who run travel and credit card companies say that shoppers aren’t pulling back spending at all.

It’s like Americans are watching the forecast call for thunderstorms but, seeing that it’s still sunny outside, are heading out to the waves to surf anyway.

Big picture: Recession fears are rising as the Fed raises interest rates to tame inflation that’s soaring at 40-year highs. While the definition of a recession is pretty broad, a slowdown in consumer spending would certainly be an indicator of one: It accounts for about 70% of the US economy.

Posted on October 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Stocks Ended Noticeably Higher Amid Wall Street Journal Report

U.S. equities rose sharply in a choppy trading session as investors sifted through a host of earnings releases, and reassessed the outlook for future Fed rate hikes. This follows the release of a Wall Street Journal (WSJ) report that said some Fed officials are concerned about over-tightening monetary policy. Investors also eyed events overseas, particularly the abrupt resignation of U.K. Prime Minister Liz Truss, as today’s domestic economic calendar was void of any major releases. Q3 earnings season continued in earnest, as Dow member American Express eclipsed analysts’ expectations but an increase in reserves for potential defaults seemed to hamper conviction.

Fellow Dow component Verizon Communications beat forecasts, Tenet Healthcare’s disappointing guidance overshadowed its earnings beat, and social media company Snap was able to post an adjusted profit, but warned of lower ad revenues in the future. Pfizer was among the standout companies after revealing plans to start charging more for Covid vaccines.

Treasury yields were mixed in the wake of the Wall Street Journal reporting, while the Fed is likely to go for another big rate hike in November, it’ll probably start slowing down thereafter.

The U.S. dollar dropped amid a rally in the British pound and the Euro, while crude oil and gold prices increased.

Stocks in Europe ended the day mostly lower, with the political chaos surrounding the U.K. in focus, while markets in Asia were mixed, as economic uncertainty continues to weigh on sentiment.

Posted on October 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities ended the day lower in a choppy trading session as the markets sifted through a host of earnings results, as well as news of the sudden resignation of the U.K.’s prime minister.

Q3 earnings season has shifted into a higher gear, as IBM beat the Street’s forecasts and upped its guidance, Tesla also exceeded estimates and offered upbeat commentary, and American Airlines far surpassed estimates on record revenue. Meta fell 1.28%. Microsoft Corp. fell 0.14% to $236.15, Alphabet Inc. Cl A rose 0.34% to $99.97, and Twitter Inc. rose 1.18% to $52.44. Trading volume (24.4 M) remained 3.5 million below its 50-day average volume of 27.8 M.

The economic calendar for the day came in heavy, with jobless claims moderating and manufacturing activity out of the Philadelphia region improving slightly, but remaining contractionary. Additionally, existing homes sales fell for an eighth-straight month, and the Leading Economic Index has now declined for six of the past seven months.

Treasury yields gained ground, but the U.S. dollar paired some of its recent run, while crude oil and gold prices nudged lower. Stocks in Europe were mostly higher with investors absorbing the events transpiring in the U.K. and more hot inflation data, and Asian markets were lower, as economic uncertainty continues to weigh on conviction.

Posted on October 20, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities snapped a two-day winning streak, finishing lower as investors weighed a host of earnings and economic reports and eyed a noticeable rise in Treasury yields.

Housing data was in focus today, as mortgage applications declined last week, while housing starts fell more than anticipated, and building permits unexpectedly rose.

Equity news was headlined by positive earnings surprises, as Netflix and Dow member Proctor & Gamble both bested earnings expectations, despite citing the impacts of foreign exchange headwinds.

United Airlines also topped earnings estimates and expects the strong COVID-19 recovery trends to continue to overcome recessionary pressures.

Meanwhile, the U.S. dollar rallied amid weakness in the euro and British pound, while crude oil prices gained ground, and gold fell.

European stocks traded lower following hot inflation data out of the region. And, Asian markets closed out mixed in a quiet day as the markets continued to grapple with global monetary policy tightening concerns.

Posted on October 19, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities finished higher, adding to yesterday’s rally that came amid the U.K.’s decision to abandon nearly all of its tax cut plans. The moves came amid some stabilization in the global bond and currency markets which had seen increased volatility after the initial release of the proposal.

In economic news, the Federal Reserve’s industrial production and capacity utilization report showed both rose more than expected, while homebuilder sentiment declined more than anticipated.

In earnings news, Dow members Goldman Sachs and Johnson & Johnson both bested earnings estimates. Lockheed Martin also beat earnings expectations, reaffirmed full-year guidance, and announced an anticipated $4 billion in accelerated share repurchasing during Q4.

Treasury yields and the U.S. dollar were nearly unchanged in choppy action, while crude oil and gold prices declined.

Asian stocks were mostly higher after yesterday’s market rally in the U.S., and as Australia’s central bank released the minutes from its October monetary policy meeting.

European stocks rose as markets in the region continued to digest the U.K.’s tax-cut reversal.

Posted on October 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

THE ECONOMY & RECESSION

By Staff Reporters

***

***

U.S. equities rose noticeably in the first trading session of the week following the new U.K. finance minister’s announcement that the government would abandon nearly all its tax cut plans. The moves came amid hopes of some stabilization in the global bond and currency markets which have seen increased volatility in the wake of the initial proposal.

Treasury yields traded mixed, while the U.S. dollar fell amid strength in both the British pound and the euro.

Crude oil prices nudged lower, and gold traded slightly higher.

Bank of America shares rose as the company eclipsed quarterly expectations on a jump in net interest income, while Q3 earnings season is set to kick into a higher gear this week.

***

Economy: This party may be busted by the cops. A US recession is a 100% certainty within the next 12 months, according to Bloomberg’s economic model.

Posted on October 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Earnings: Earnings season goes from a trot to a canter this week when some heavy-hitters will give business updates, including Netflix, Tesla, IBM, Goldman Sachs, and P&G.

In their reports last week, bank execs said that consumers were still in pretty good shape, despite the gloomy economic outlook.

Posted on October 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

This week the stock market was the opposite of a snoozefest, as economic data sent markets swinging wildly in both directions. The Dow closed higher for the week, but the S&P and NASDAQ closed in the red.

After another bad day as Tesla shares have now fallen 50% below their peak.

The Fedis investigating trades made by Atlanta Fed President Raphael Bostic during restricted periods, rekindling a controversy that has dogged the central bank. Bostic said that the trades were made by third-party managers and were not directed by him.

Trevor Milton, the founder and former CEO of electric automaker Nikola, was found guilty of fraud for lying to investors about the business.

Beyond Meatis cutting about 20% of its workforce, and its COO is leaving the company.

Decentraland, a metaverse company that sells virtual real estate, has just 8,000 daily users despite being valued at $1.2 billion.

Posted on October 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

Stocks initially fell, and then soared.

Treasury yields rose, particularly on the short end of the curve.

The U.S. dollar declined as the British pound rallied for a second day amid speculation that the U.K. government may reverse course on its tax cut plan.

Crude oil prices reversed higher, and gold prices were lower.

Jobless claims accelerated more than expected.

Asian stocks moved broadly lower amid the inflation uneasiness, while European stocks ended the day in the green as the markets grappled with the potential tax-cut U-turn out of the U.K.

Posted on October 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: The S&P 500 extended its losing streak to six days yesterday, notching its worst day since November 2020. But, Moderna did not contribute to the decline after news broke it will develop a cancer vaccine with Merck.

***

***

The Social Security Administration is expected to announce a cost of living adjustment, or COLA, of at least 8% today amid a rising inflation rate that has been punishing for Americans on fixed incomes.

The annual adjustment is forecast to be the largest one-time increase since 1981, and the largest experienced by beneficiaries alive today. The nonprofit Senior Citizens League predicts an adjustment coming in at 8.7%, implying that Social Security recipients could see an increase of about $144 starting Jan. 1, 2023. The increase that took effect this year was 5.9%.

Posted on October 12, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. equities finished mixed after turning to the downside following news that the Bank of England set a three-day deadline to end its bond buying initiative and for pension funds within the U.K. to rebalance. Action was choppy most of the day, as investors awaited tomorrow’s first look at the highly anticipated September inflation data.

Now, according to the Schwab Center for Financial Research, the markets appeared to be on edge at the prospect of further monetary policy tightening, which could be enhanced by the inflation reports. In light economic news, small business optimism unexpectedly increased but remained below the 48-year average for a ninth-consecutive month.

On the equity front, Leggett & Platt lowered its full-year guidance, KLA Corporation ceased some of its business with China-based customers following export restrictions, while a proposal from the Labor Department is pressuring ride-hailing and food-delivery companies. Treasury yields were mixed after a return to action following yesterday’s holiday.

The U.S. dollar finished modestly higher in its own whipsaw session, crude oil prices fell, and gold was also lower.

Asian markets were mostly lower following new export rules on semiconductor chips from the U.S., while European stocks were lower as the Bank of England announced further intervention to try to ensure financial stability.

The global markets continue to grapple with the possibility of future global rate hikes as inflationary concerns remain.

Posted on October 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Investors are eyeing this week’s Consumer Price Index report and sifting through corporate earnings reports, which could both bring bearish news to the market.

Morgan Stanley’s Mike Wilson just told CNBC he believed earnings would be a mixed bag, and JPMorgan warned investors that stocks could see another 5% sell-off on Thursday if September inflation clocks in above 8.3%.

Posted on October 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

It’s a regular day of business for the U.S. stock market in 2022, as equity exchanges stay open for Columbus Day, a federal holiday that also has been recognized as Indigenous Peoples’ Day.

Bond markets, however, take the day off, which means a long weekend for the Treasury market, corporate bonds and other forms of tradable debt.

Stocks have endured a brutal selloff in the first nine months of the year as the Federal Reserve has worked to fight inflation that’s been stuck near it highest levels since the early 1980s. The central bank’s main tool to battle inflation has been to dramatically increase interest rates, while also shrinking its balance sheet, in an effort to tighten financial conditions and squelch demand for goods and services, while also bringing down stubbornly high costs of living, including food, shelter and energy prices.

The jobs report for September pegged the unemployment rate as matching a prepandemic low of 3.5%, dashing hopes for now of a significant trend toward a pullback in the labor market.

Posted on October 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Markets: Stocks nose-dived as the September 2022 jobs report delivered a nasty gut-punch. What did it show? That the labor market cooled off last month, but not enough for the Fed to ease up on its interest rate hikes. Expect a fourth-straight 75 basis point increase at the central bank’s meeting next month.

Stock spotlight: While nearly 95% of S&P stocks were in the red computer chip makers have to be singled out for their dire warnings about the economy. AMD and Samsung both revealed that demand for their chips has plunged recently—a bad omen for the entire tech sector.

Posted on October 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks traded noticeably lower on the heels of the September nonfarm payroll report, but was still able to post weekly gains following the strong rebound on Monday and Tuesday. The labor data showed job growth rose more than predicted, while the unemployment rate unexpectedly declined, and the labor force participation rate surprisingly dipped. The report seemed to dampen recently increased optimism that the Fed could decelerate its aggressive monetary policy tightening campaign.

In other economic news, wholesale inventories were unrevised at a solid gain, and data on consumer credit showed consumer borrowing was well above expectations.

Treasury yields rose following the labor report, and the U.S. dollar continued to rebound from a stumble earlier in the week.

Crude oil prices climbed following the decision from OPEC+ to cut oil production and gold traded lower.

Asian stocks finished out the week broadly lower, and European stocks trimmed a weekly gain as volatility remained in the currency and bond markets across the globe.

Posted on October 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: Stocks closed lower for the second straight day, but that was a sideshow to this morning’s September jobs report. For investors, it’ll likely be a case of bad news is good news—a drop in new jobs added to the economy would be a signal that the Fed’s campaign to curb inflation is working, and that it could potentially ease its foot off the brake pedal in the future.

Stock spotlight: Cannabis companies like Tilray surged after President Biden signaled a major shift in federal marijuana policy.

Posted on October 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Federal Reserve just put out an update saying that debit-card issuers such as Visa Inc. will have to enable at least two payment-card networks for debit-card processing, including for online and other “card-not-present” transactions. The rules are “substantially similar” to a proposal from last year, the Fed announced.

The final deadline for implementation will be July 1, 2023.