BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Choice Overload is the difficulty in making a decision when faced with too many options. It’s like standing in front of an ice cream counter with 31 flavors and feeling paralyzed.

Among personal decision-makers, a prevention focus is activated and people are more satisfied with their choices after choosing among few options compared to many options, i.e. choice overload. However, individuals can also experience a reverse choice overload effect when acting as proxy decision-maker, too.

It is widely accepted that having more choices is inherently positive. When there are more available options from which to choose, an individual is more likely to be able to select the particular option that is the best fit and most likely to satisfy them. Choice is typically thought to be related to personal freedom and enhanced well-being.

Therefore, according to colleague Neal Baum MD, for most individuals the ultimate goal is to constantly maximize their choices in life to increase their overall satisfaction and well-being. The decision-making process, however, is a complex cognitive task that does not always lead to positive outcomes.

Thus, while having options is generally good, too many choices can lead to anxiety and decision fatigue. This is why curated selections and recommendations are so popular – they simplify the decision-making process’ according to another colleague Dan Ariely PhD.

So, when you’re overwhelmed by choices, narrow them down to a manageable number and make your decision easier.

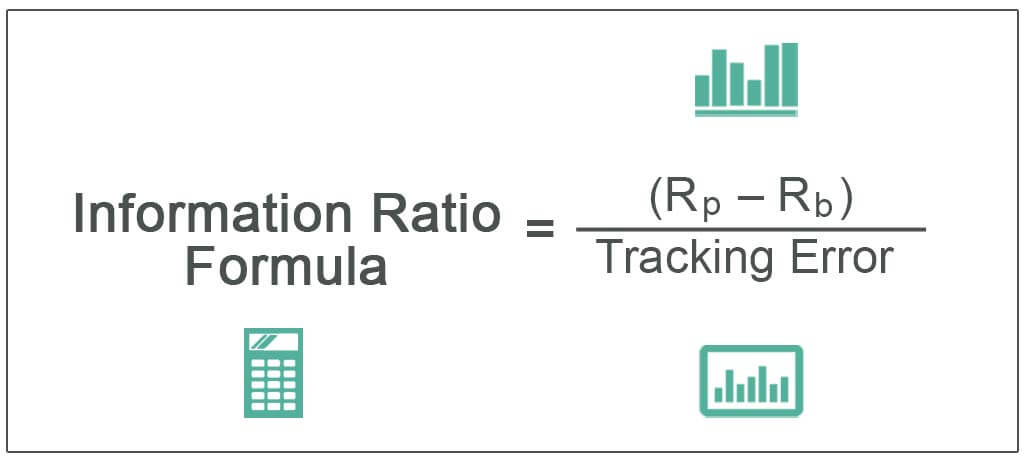

The Information Ratio (IR) is a risk-adjusted rate of return measure for comparing the performance of active investment managers over time. Its purpose is to help determine how much return an active portfolio manager has added per unit of active management risk.

Think of IR as a Sharpe Ratiofor active investment management; the IR is more focused than the Sharpe Ratio. Starting with the Sharpe Ratio’s formula, if we replace the excess return in the numerator with a portfolio’s active return (the average annualized return of an actively managed portfolio minus the average annualized return of the portfolio’s benchmark over a given period, adjusted for the portfolio’s market risk exposure), and you replace the Sharpe Ratio’s standard deviation of excess returns in the denominator with the standard deviation of a portfolio’s active returns over the period, you have the IR.

While the Sharpe Ratio expresses the amount of excess return per unit of overall risk, the IR computes only the active management-driven (alpha) returns per unit of alpha-driven risk. And while the Sharpe Ratio’s excess returns are calculated with regard to what is considered to be a relatively risk-free asset, such as a U.S. Treasury bill, the IR’s active returns are calculated with regard to each portfolio’s specific market benchmark.

The higher the IR, the better. The IR should be measured over a meaningful period of time, typically at least three to five years. The IR is not perfect–it can be influenced by external factors such as changes in market volatility. The standard deviation of active returns in the IR’s denominator is called tracking error. Tracking error will tend to increase in volatile markets for even the best active managers.

Posted on December 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

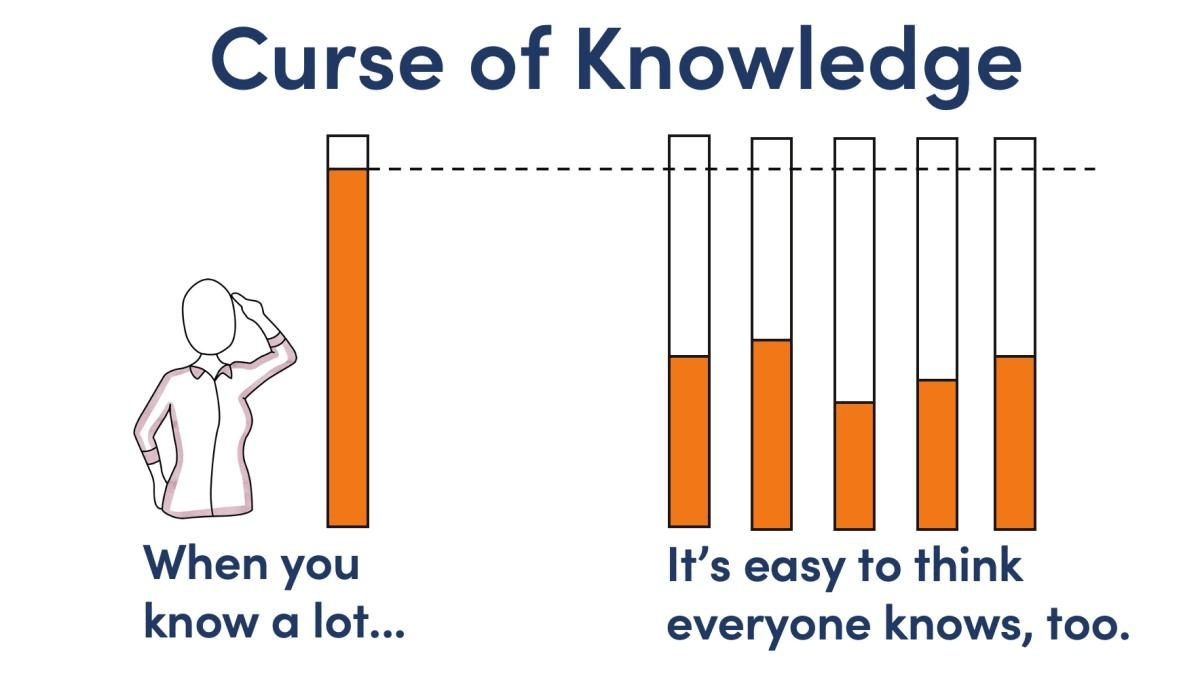

Similar to the availability heuristic (Tversky & Kahneman, 1974) and to some extent, the false consensus effect, once you really understand a new piece of information, that piece of information is now available to you and often becomes seemingly obvious. It might be easy to forget that there was ever a time you didn’t know this information and so, you assume that others, like yourself, also know this information: ie., the curse of knowledge.

However, it is often an unfair assumption that others share the same knowledge.

And so, the hindsight bias is similar to the curse of knowledge in that once we have information about an event, it then seems obvious that it was going to happen all along.

Basis Points are used in financial literature to express values that are carried out to two decimal places (hundredths of a percentage point), particularly ratios, such as yields, fees, and returns. Basis points describe values that are typically on the right side of the decimal point–one basis point equals one one-hundredth of a percentage point (0.01%). So 25 basis points equals 0.25%, and 50 basis points equals 0.50%.

Only when basis points equal or exceed 100 does the value move to the left of the decimal point–100 basis points equals 1.00%, 500 basis points equals 5.00%, etc.

Bid/Ask Spread (also known as bid/offer spread) is the difference between the National Best Bid and the National Best Offer, which represents the implied cost to trade a security.

As compensation for the risk taken, the market maker (or dealer) earns the bid/offer spread in exchange for facilitating the trade. Wider spreads generally indicate higher costs associated with trading the underlying assets in the ETF, hedging costs, inventory management costs, and general market risk.

Prepayment risk is typically used in reference to mortgage-backed securities. It refers to the risk that mortgage refinancing activity might increase when market interest rates decline, which is generally not favorable for MBS investors.

For example, when homeowners refinance their mortgages, MBS investors are “prepaid,” shortening the life of their investments and forcing investors to reinvest the proceeds under lower interest rate conditions than what were most likely prevailing at the time of the original MBS investment.

Price adjustments for prepayment risk are one factor that helps explain why MBS, despite their generally high credit quality, have higher yields than comparable-maturity Treasury securities.

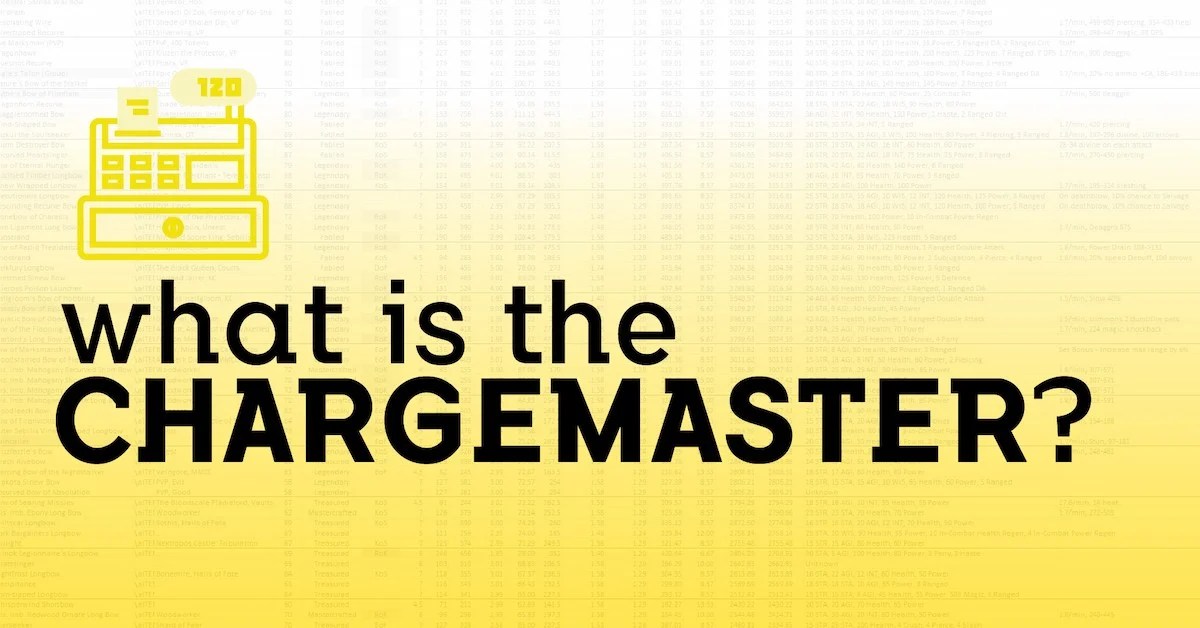

Classic Definition: A comprehensive review of a physician, clinic, facility, medical provider or hospital’s charges to ensure Medicare billing compliance through complete and accurate HCPCS/CPT and UB-92 revenue code assignments for all items including supplies and pharmaceuticals. The charge master captures the costs of each procedure, service, supply, prescription drug, and diagnostic test provided at the hospital, as well as any fees associated with services, such as equipment fees and room charges

Modern Circumstance: A charge master quizlet (charge description master [CDM]) document that contains a computer-generated list of procedures, services, and supplies with charges for each. Charge master rates are essentially the health care market equivalent of Manufacturer’s Suggested Retail Price (MSRP) in the car buying market. Poor charge master maintenance can lead to overpayments or underpayments. It can also lead to claim rejections from insurance companies, poor patient experience, or compliance violations.

Paradox Examples:

Superbills: An encounter form that is the financial record source document used by healthcare providers and other personnel to record treated diagnoses and services rendered to the patient during the current encounter. It is also called a superbill.

Payment rates: Almost no one actually pays the publicized charge master rates. The vast majority of health care consumers are represented by a payer of some kind, such as a commercial health insurance company, Medicaid, or Medicare. Commercial insurers negotiate the actual prices they pay during the process of contracting with providers. Medicare and Medicaid establish their own payment levels independent of hospitals’ charge master lists – Medicare through the federal government and Medicaid through state governments.

Cash pay: The sad irony of the charge master is that the uninsured are the most likely to be billed charge master rates because they are not represented by a third-party payer.

Problematic features: Other items also impede the ability of payers to have a comprehensive and accurate understanding of hospitals’ financial positions. For example, nonprofit hospitals are required to report charity care, bad debt expenses, community benefit initiatives, and uncompensated care. When these expenses are reported at the charge master level, expenses can be paradoxically overstated, potentially making a hospital’s financial position look worse than it actually is.

Volatility indexes are forward-looking measures of the market’s expectations of volatility (or how much a stock index’s price moves). The CBOE manages and publishes three of the most widely used volatility indexes based on three major stock indexes:

The VIX Index tracks the expected 30-day future volatility of the S&P 500 Index.

The VXN Index tracks the expected 30-day future volatility of the NASDAQ-100 Index.

The VXD Index tracks the expected 30-day future volatility of the Dow Jones Industrial Average Index.

Equity market neutral strategies seek to eliminate the risks of the equity market by holding up to 100% of net assets in long equity positions and up to 100% of net assets in short equity positions. These strategies attempt to exploit differences in stock prices by being long and short in stocks within the same sector, industry, market capitalization, etc. If successful, these strategies should generate returns independent of the equity market.

Equity market neutral portfolios have two key sources of return: 1) the Treasury Bill return (the interest on proceeds from short sales held in cash as collateral), and 2) the difference (the “spread”) between the return on the long positions and the return on the short positions. Stock picking, rather than broad market moves, should drive most of a market-neutral strategy’s total return (save for any return from the 100% cash position).

Extended Equity Strategies attempt to provide better returns than possible with long-only investments

An example of an extended equity strategy is a 130/30 portfolio, which gets its designation from taking a 130% long position and a 30% short position. In practice, this would mean $100mm invested in stocks that are viewed as attractive.

Next, the manager would borrow and sell short $30mm of unattractive stocks. Then the manager uses the proceeds from the short sale to buy an additional $30mm of attractive stocks. This results in a portfolio that has 130% long and 30% short exposure to stocks, or “extended” exposure to equities relative to a long-only, 100% stock portfolio.

Note: It’s important to point out that here is the risk of theoretical unlimited amount of loss with short selling, (i.e. the price of the short-sold stocks increases; the long position can only go down to $0).

Classic Definition: Despite rising costs, health care often is of poor quality. Evidence from a classic medical improvement outcomes study assessed care of patients with several chronic diseases. This study found that patients’ functional health status outcomes are similar to care rendered by specialists and generalists but that generalists use far fewer resources. Similar outcome at lower cost represents higher value.

Modern Circumstance: Current solutions to improving care quality may do more harm than good if they focus more on diseases than on people. Efforts to improve the parts (evidence-based care of specific diseases) may not necessarily improve the whole (the health of people and populations).

Expanding access to specialty care, for example, has been proposed as both a source of and a solution for deficiencies in quality of care. Primary care is touted as an essential building block of a high-value health care system even as it is undermined by systems attempting to improve the quality, effectiveness, and value of their health care..

Paradox Example: The above contradictions plague improvement efforts in health care systems around the world, particularly the United States The paradox is that compared with specialty care or with systems dominated by specialty medical care, primary care is associated with the following: (1) poorer quality care for individual diseases, yet (2) similar functional health status at lower cost for people with chronic disease, and (3) better quality, better health, greater health equity and lower costs for whole peoples and populations.

And so, this contradiction plagues improvement efforts in health care systems around the world, particularly the United States.

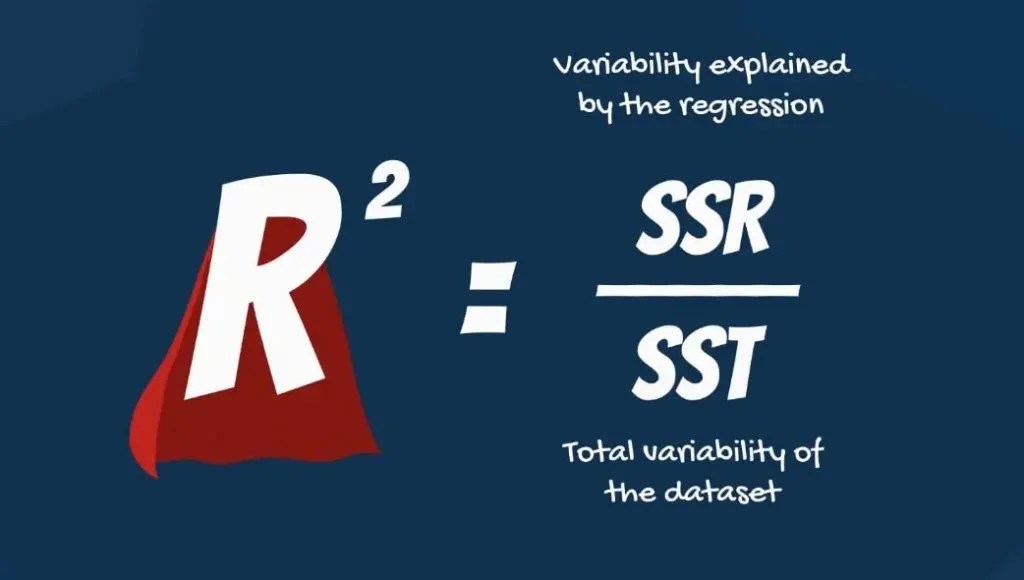

R-squared is an investment portfolio performance and risk measure that indicates how much of a portfolio’s performance fluctuations were attributable to movements in the portfolio’s benchmark index. R-squared can range from 0-100%.

IOW: R Squared, also known as the coefficient of determination, is a statistical measure used in the context of regression analysis. It represents the proportion of the variance in the dependent variable that is predictable from the independent variable(s). Essentially, it provides a measure of how well the observed outcomes are replicated by the model, based on the proportion of total variation of outcomes explained by the mode

For example, an R-squared of 100% indicates that all portfolio performance movements were attributable to movements in the benchmark index—they correlate perfectly to the benchmark.

Conversely, an r-squared of 0% indicates that there is no correlation between the performance movements of the portfolio and the benchmark.

Classic Definition: Employers write checks that cover most health insurance premiums for employees and their dependents. But as the late Princeton health economist Uwe Reinhardt PhD once explained, employer-sponsored insurance is like a pickpocket taking money out of your wallet at a bar and buying you a drink. You appreciate the cocktail until you realize you paid for it yourself.

Modern Circumstance: With health coverage, employers write the check to the insurer, but employees bear the cost of the premium — the entire premium, not just the portion listed as their contribution on their pay stub. The premium money that goes to the insurance company is cash that employers would otherwise deposit in employees’ accounts like the rest of their salary.

Paradox Example: The fallacy paradox is in thinking an employer’s contribution comes out of profits. In fact, higher health insurance premiums mean lower wages for workers. Since 1999, health insurance premiums have increased 147 percent and employer profits have increased 148 percent. But in that time, average wages have hardly moved, increasing just 7 percent. Clearly workers’ wages, not corporate profits, have been paying for higher health insurance premiums. Health care costs are one — though not the only — reason wages have stagnated over the last few decades. With health insurance costs rising faster than growth in the economy, more labor costs go to benefits like health insurance and less to take-home pay. Yet the paradox that employees don’t pay for their own health insurance is widespread:

The first reason is that individuals cannot be sure what causes their wages to change or remain stagnant for decades.

The second reason is that employers want Americans to believe that they pay for their workers’ health insurance.

The third reason is that there are those who profit from the employment-based system: drug companies, device manufacturers, specialty physicians and high-income individuals.

And so, they all want you to believe companies are being magnanimous in giving you insurance, but they are not!

Investors waited for the Magnificent 7 stock reports to begin rolling last evening. The NASDAQ rose to a new high on optimism while the Dow Jones fell, and the S&P 500 split the difference.

Alphabet announced earnings after the bell yesterday, Microsoft and MetaPlatforms reveal their latest quarters today, Amazon and Apple on Thursday afternoon.

The 10-year Treasury yield hit a 4-month high this afternoon before paring back a bit as traders struggle to find a signal in all the market noise.

Oil rebounded a bit from yesterday’s terrible day, though it still ended the trading session lower.

Ever tried making a decision when you’re angry or excited? According to colleague Dan Ariely PhD, that’s a hot state – when emotions run high and logic takes a backseat. It’s like trying to think clearly in the middle of a storm.

Be you a doctor, CPA, attorney, engineer, husband, wife, parent, teacher or all others. In a hot state, we’re impulsive, making choices we might regret later. It’s why cooling off before making big decisions is always a good idea.

So, when your emotions are boiling over, take a step back, breathe, and wait for the storm to pass. You’ll make better choices when you’re in a calm, cool state.

Posted on October 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Trump Media & Technology Group rocketed higher at the opening bell, prompting the Nasdaq to halt trading on what has quickly become the meme stock du jour. Shares ended the day 8.76% higher.

23andMe clawed 1.86% higher after introducing three new board members about a month after the entire board resigned.

VF Corp, parent company of clothing brands JanSport, Vans, and North Face, surged 27.01% thanks to an impeccable earnings report that revealed its turnaround plans are coming to fruition.

Trex, the stuff your dad built an awesome deck out of, saw sales fall last quarter but still managed to beat earnings expectations. Shares popped 6.19%.

STOCKS DOWN

JetBlue Airways sank 17.08% in spite of reporting a smaller loss than analysts expected. The problem is all the turbulence that lies ahead.

D.R. Horton is the largest homebuilder by market cap, so when it says that 2025 will be a bad year, investors should listen. Shares dropped 7.29% on the news.

Crocs stumbled 19.17% after beating earnings but announcing that its fiscal year would be bogged down by poor sales of its HeyDude shoe brand.

Stanley Black & Decker fell 8.77% after missing on both profits and sales, citing weaker consumer spending.

Xerox plummeted 17.41% after the company that can’t make a printer that works for longer than 3 months without needing a new ink cartridge announced weaker sales than expected.

The S&P 500® index (SPX) rose 9.40(0.16%) to 5,832.92; the Dow Jones Industrial Average® ($DJI) fell 154.52 points (–0.36%) to 42,233.05; and the $COMP added points 145.55 (0.78%) to 18,712.75.

The 10-year Treasury note yield (TNX) finished unchanged at 4.27% after reaching nearly 4.34% earlier today.

It is a multi-factor model measures the overall risk associated with a security relative to the market. And, it incorporates over 40 data metrics, including earnings growth, share turnover and senior debt rating.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

401(k) vs. pension: There’s pros and cons to both. While pension plans guarantee a steady income stream, payments sometimes aren’t indexed by inflation, which can erode their value over time. On the flip side, 401(k)s are subject to market fluctuations and require financial literacy.

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By: Christian Hernandez MBA – Apple Health Care Services

Richard Melnyck MBA MS

Mark Friedman PhD Department of Accounting

Howard Gitlow PhD Department of Management Science University Miami

***

BACKGROUND

***

Homecare has long been one the most cost-effective methods of treating patients. Yet today, homecare providers face significant challenges: reimbursement cuts, mandatory accreditation, and influencing policy changes. So, how can homecare managers efficiently sustain a cutting edge, consistent and quality focused practice amidst this changing landscape?

***

It is time the homecare industry tap into the high-tech tools and proven management theories that together make up “Six sigma” management. This article will provide a solid point of reference for managers interested in adopting “Six Sigma” management. In today’s stiff economic climate, organizations are once again turning to “Six Sigma”strategies as a means to reduce their bottom lines.

***

However, its cost cutting aspect is technically more of a by product than the core of its theory. “Six Sigma” management is practiced in many organizations across all sectors of the global economy. Companies such as drug giant Merck, Cadbury, and Dunkin’ Brands are increasingly turning to Six Sigma to lift their bottom lines.

***

The term “Lean Management” is an old buzz word that still excites managers. Lean Management stems from the term Lean Manufacturing, which was a derivative of Total Quality Management (TQM) —considered one of the earlier versions of “Six Sigma”.

***

Over the years, “Six Sigma” has evolved from a ground-breaking management system to one of the most proven methods for instituting change, reducing errors and eliminating inefficiencies. These management utilities run through the entire spectrum of organizational applications, from confronting the serious issues mentioned above to routine business functions.

***

The resurgence of Japan’s economy in the 70’s and 80’s is largely attributed to TQM. “In the auto industry, manufacturers such as Toyota and Honda became major players. In the consumer goods market, companies such as Toshiba and Sony led the way. These foreign competitors were producing lower-priced products with considerably higher quality.”

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A young clinician representative advising to consider the cost versus value of medicine. Health care concept for economic cost-effectiveness analysis, driving down medical costs, improved access.

***

Value Based CareClassic Definition: Value-based care is a type of payment model that pays doctors and hospitals for treating patients in the right place, at the right time and with just the right amount of care. You can look at it as a financial incentive to motivate healthcare providers to meet specific performance measures related to the quality and efficiency of the process. The same way, it penalizes weaker experiences, such as medical errors. The concept is often counter-intuitive.

Modern Circumstance: As healthcare costs continue to rise, value-based care has been growing in popularity compared to the traditional fee-for-service method.

Think: HMOs, PPOs, capitation payments and Medicare Advantage [Part C].

Paradox Examples:

Payment: A physician paid through fee-for-service compensation might like to see a packed medical office waiting room. More patients and services equate to higher pay. But, the same doctor paid through a VBC contract might wish to see an emptier waiting room as s/he will get the exact same daily pay for seeing fewer patients and working much less.

Prospectivity: Traditional Fee-for-Service medicine treats sick patients. VBC medicine seeks to keep patients healthy and out of the doctor’s office.

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Applications to MBA programs are up 12% in 2024 after declining for two years, according to the Graduate Management Admission Council, which surveys business school admissions offices.

Apple and Goldman Sachs were ordered to pay $89 million by the Consumer Financial Protection Bureau for failing to address thousands of consumer disputes of Apple Card transactions.

Apple is cutting production of Vision Pro due to slow sales. The tech giant is scaling down production of its $3,500 Vision Pro VR headset and might halt assembly of new ones next month,

UPS delivered a strong earnings report, with revenue beating analyst expectations for the first time in two years. Shares popped 5.28%.

ServiceNow rose 5.41% to a new all-time high thanks to a beat-and-raise third-quarter earnings report powered by higher AI demand for the enterprise software company.

Whirlpool climbed 11.20% after announcing solid earnings and reiterating guidance for the rest of the fiscal year, reassuring worried shareholders.

Molina Healthcare soared 17.67% after beating both top and bottom line estimates in the third quarter, thanks to the health insurer reaping the rewards of higher Medicaid payouts.

STOCKS DOWN

IBM dropped 6.17% on disappointing third-quarter results, missing on both top and bottom line forecasts thanks to lower consulting and infrastructure revenue.

Peloton pedaled higher yesterday after Greenlight Capital’s David Einhorn declared that the company was undervalued while he was pedaling on a Peloton. The stunt only worked for a quick sprint, though, with shares back down 2.07% today.

TKO Group Holdings got hit with a piledriver after the owner of the WWE and UFC announced it is acquiring several entertainment companies, including Professional Bull Riders. Investors bucked shares off 8.69%.

Keurig Dr. Pepper fizzled 4.80% thanks to lower sales last quarter, though the company is trying to bolster revenue by acquiring energy drink maker Ghost.

Air taxi startup Lilium crashed 61.50% on the news that its main subsidiaries have run out of cash and are filing for insolvency.

The S&P 500® index (SPX) rose 12.44 points (0.21%) to 5,809.86; the $DJI fell 140.59 points (–0.33%) to 42,374.36; and the NASDAQ Composite® ($COMP) added 138.83 points (0.76%) to 18,415.49.

The 10-year Treasury note yield fell four basis points to 4.20%.

The CBOE Volatility Index® (VIX) was about flat at 19.18.

Posted on October 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX) fell10.69points (–0.18%) to 5,853.98; the Dow Jones Industrial Average® ($DJI) lost 344.31 points (–0.80%) to 42,931.60; and the NASDAQ Composite®($COMP) rose 50.45 points (0.27%) to 18,540.01.

The 10-year Treasury note yield (TNX) climbed 11 basis points to 4.18%, outpacing a 7 basis-point rise for the 2-year Treasury note yield.

The CBOE Volatility Index®(VIX) climbed to 18.6 but remains below recent peaks.

Boeing popped 3.11% on the news that it has reached a tentative deal with the machinists union that has been on strike for over a month now. With Boeing’s earnings announcement coming Wednesday, shareholders are definitely breathing a sigh of relief.

Activist investor Starboard Value has taken a sizable stake in Tylenol-maker Kenvue, which was spun off of Johnson & Johnson just last year. Kenvue shares rose 5.52% on the news.

Warby Parker climbed 9.84% thanks to an upgrade from Goldman Sachs analysts, who like the company’s strong margin growth and improved operational efficiency.

Cigna will once again attempt to acquire fellow health insurerHumana. Shareholders on both sides didn’t like the idea: Shares of Cigna sank 4.69%, and Humana fell 2.51%.

UPS dropped 3.38% on a downgrade from Barclays analysts citing pressures on the company’s margins, including higher competition and weaker demand. Management will have a chance to respond when earnings drop on Thursday.

Southwest Airlines fell 1.74% after Bloomberg reported that the beleaguered airline wants to call a truce with activist investor Elliott Investment Management.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Yep – Even the Smart Folks!

By Lon Jefferies MBA CMP® CFP®

Dr. David Edward Marcinko MBA MEd CMP®

In the Business Insider, Mandi Woodruff describes nine mental blocks that cause smart people to do dumb things. Review the list and itemize the factors that have negatively impacted your finances.

The Factors

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia (or nearsightedness) makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Confirmation bias causes us to place more emphasis on information that supports the opinion we already have. Consequently, we tend to ignore or downplay opinions that don’t mirror our own, leading us to make uninformed decisions.

NOTE: An interesting example of the confirmation bias is the case of David Rosenberg, who is one of the most well-known perpetual bears on Wall Street. In October, Mr. Rosenberg’s analysis forced him to warm to the current investment environment. His fans and followers, rather than appreciating his research and ability to adjust to new information, criticized him for changing his opinion.

As it turned out Mr. Rosenberg had fans not because of his expert analysis, but because he added intellectual heft to his followers pessimism and quasi-political desire for the system to collapse. Their view was that things were in permanent decline and his analysis, charts, and voice added respectability to their pre-existing bias. Mr. Rosenberg has now lost his fan base not because he was wrong for the last four years, but because he changed his mind.

Loss aversion affected many investors during the crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often underperform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Assessment

The good news is that being aware of these tendencies can help us avoid mistakes. We’ll never be perfect, but avoiding detrimental decisions based on mental prejudices can give us an advantage in our financial and retirement planning efforts.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Gambler’s Fallacy occurs when we subconsciously believe we can use past events to predict the future. It is also called the Monte Carlo Fallacy, after the Casino de Monte-Carlo in Monaco where it was observed in 1913

For example, it is common for the hottest sector during one calendar year to attract the most investors the following year.

Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Goldman Sachs’ profit jumped 45% in monster quarter. The investment bank made $3 billion of profit on revenue of nearly $13 billion in Q3, it reported yesterday, surpassing even the rosiest of expectations. Bloomberg reported that it was the best quarter ever for Goldman’s stock trading unit, putting the group on track for a record year.

Walgreenssaid it will close 1,200 US stores, about one in seven locations, by 2027. The retailer will shutter 500 stores by the end of next year.

Trump Media & Technology Group has had a wild week, falling nearly 10% yesterday before trading of the stock was halted, then popping 15.52% today. Election hype, a Trump-sponsored cryptocurrency, and Truth+, a new streaming service, are keeping shareholders on their toes.

Abbott Laboratories rose 1.53% thanks to a stronger-than-expected earnings report powered by the company’s impressive medical device sales.

Aspen Aerogels makes insulating material for batteries, which sounds boring to everyone but the Department of Energy. The DOE signed a conditional commitment to loan the company up to $670 million, sending shares 13.24% higher.

DOWN STOCKS

Novavax plummeted 19.44% after the FDA put a hold on the pharma company’s flu and Covid vaccine combination.

Interactive Brokers enjoyed higher revenue and more trading from its user base last quarter, but earnings per share came in under expectations, and shares sank 4.05%.

The SPX rose27.21points (0.47%) to 5,842.47; the Dow Jones Industrial Average® ($DJI) added 337.28 points (0.79%) to 43,077.70; and the NASDAQ Composite®($COMP) increased 51.49 points (0.28%) to 18.367.08.

The 10-year Treasury note yield (TNX) fell two basis points to just below 4.02%, the lowest close since October 4.

The CBOE Volatility Index® (VIX) dropped moderately to 19.58, still elevated considering stock market strength.

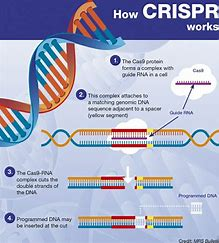

CRISPR is a family of DNA sequences found in the genomes of prokaryotic organisms such as bacteria and archaea. These sequences are derived from DNA fragments of bacteriophages that had previously infected the prokaryote. They are used to detect and destroy DNA from similar bacteriophages during subsequent infections

Posted on October 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Maximum lifespans. The upper limit of human life expectancy is leveling out, according to a new study published in the journal Nature Aging. Back in 1990, life-extending tech and health measures were increasing the average global lifespan by about 2.5 years per decade, but that dropped to 1.5 years per decade in the 2010s and closer to zero in the US, where there are more drug overdoses, shootings, and medical care inequities.

Sphere Entertainment popped 6.33% on the news that a second Sphere will be built in Abu Dhabi. London was originally supposed to be the location of a second venue, but they’ve already got the Eye, and didn’t need more circular tourist attractions.

Oklo, a Sam Altman-backed nuclear energy startup, rose another 16.04% on the news that Google will purchase nuclear power to turbocharge its AI infrastructure.

Charles Schwab climbed 6.10% after the bank announced a top and bottom line beat last quarter, as well as higher revenue projections for the full fiscal year.

Boeing somehow gained 2.26% after announcing it is raising $35 billion to support its struggling finances as the machinist union strike enters its second month.

Wolfspeed, which sounds like a super power in a YA novel, soared 21.27% on the news that the US government will provide the chipmaker with up to $750 million in government grants.

STOCKS DOWN

Semiconductor stocks got a double whammy in the last 48 hours. First, Bloomberg revealed that US officials are considering limiting the sale of AI chips outside the country. Then, ASMLmissed its Q3 sales estimates (more on that below). Nvidia shares slid 4.52%, AMD fell 5.22%, and Intel dropped 3.33%.

Citigroup beat earnings estimates this quarter, but shareholders punished the bank for setting aside more money in case of higher loan losses ahead. Shares dropped 5.11%.

Coty, parent company of numerous beauty brands like CoverGirl, fell 10.74% to a new 52-week low after it warned of a sales slowdown in the coming quarters.

Enphase Energy tumbled 9.29% after RBC analysts downgraded the solar power stock, citing growing competition from the likes of Tesla as well as slowing demand for solar batteries.

Speaking of energy, oil stocks plummeted on news of Israel’s targeting of Iranian military assets rather than crude production facilities. ExxonMobil fell 3.01%, Chevron dropped 2.67%, and ValeroEnergy sank 4.62%.

Here’s where the major benchmarks ended yesterday:

The S&P 500® index (SPX) fell 44.59 points (–0.76%) to 5,815.26; the Dow Jones Industrial Average® ($DJI) dropped 324.80 points (–0.75%) to 42,740.42; and the NASDAQ Composite®($COMP) lost 187.09 points (–1.01%) to 18,315.59.

The 10-year Treasury note yield (TNX) fell three basis points to 4.04%, the lowest close in a week.

The CBOE Volatility Index® (VIX) climbed to 20.72, an elevated level.

Millions of seniors will lose access to their Medicare Advantage plans after major insurer cuts in the aftermath of the Inflation Reduction Act. Experts spoke with Newsweek about what’s going on and what steps seniors can take to get the coverage they need.

Posted on October 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters &The Medicare Team

Medicare open enrollment—which runs from October 15th through December 7th this year—is your chance to check in on your Medicare plan and, if needed, change it.

***

***

Mark your calendars — Medicare Open Enrollment starts October 15th! Did you know new benefits are coming to Medicare drug coverage next year?

Also starting next year, you can choose to participate in a program that spreads your out-of-pocket drug costs across the calendar year, instead of paying all at once at the pharmacy. It’s called the Medicare Prescription Payment Plan — and you can opt in with your plan throughout the 2025 plan year. Contact your plan for more details.

Remember, Medicare plans can change from one year to the next, and so can your health needs. Preview and compare all your health and drug options and see if you can save!

The modern medical practice is both similar, and unlike, other businesses today. This disparity often adds to confusion for the private practitioner. And so, the experts at iMBA Inc, list the top 25 most urgent questions in practice financial management, asked by clients to date.

Assessment

Since inception in 2000, the Institute of Medical Business Advisors Inc., has become one of North America’s leading professional health consulting and valuation firms; and focused provider of textbooks, CDs, tools, templates, onsite and distance education for the health economics, administration and financial management policy space. As competition and litigation support activities increase and the cognitive demands of the global marketplace change, iMBA Inc is well positioned with offices in five states and Europe, to meet the needs of medical colleagues, related advisory clients and corporate customers today; and into the future.

And so, your thoughts and comments on this Medical Executive-Post are appreciated. Tell us what you think. Send in your own questions. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed

And, credible sponsors and like-minded advertisers are always welcomed.

Posted on September 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

The Medical Executive-Post Educational Resource

[By Ann Miller RN MHA]

We are an emerging online and onground community that connects medical professionals with financial advisors and management consultants. We participate in a variety of insightful educational seminars, teaching conferences and national workshops. We produce journals, textbooks and handbooks, white-papers, CDs and award-winning dictionaries. And, our didactic heritage includes innovative R&D, litigation support, opinions for engaged private clients and media sourcing in the sectors we passionately serve.

Through the balanced collaboration of this rich-media sharing and ranking forum, we have become a leading network at the intersection of healthcare administration, practice management, medical economics, business strategy and financial planning for doctors and their consulting advisors. Even if not seeking our products or services, we hope this knowledge silo is useful to you. Our content creation—including speaking topics, articles and course development—is client-driven.

In the Health 2.0 era of political reform, our goal is to: “bridge the gap between practice mission and financial solidarity for all medical professionals.”

THE CHALLENGE

Join the ME-P Nation today … and tell us what you think!

***

8

BOOK REVIEW

Am I over-insured and thus wasting money? Am I under-insured and thus at risk for a liability or other disaster? I never really had the means of answering these questions; until now.

It’s been a while since you’ve connected with us. Are you still interested in emerging financial planning, investing, medical practice management and health information technology insights from the Institute ofMedical Business, Advisors, Inc?

If so, please email us if you want to continue receiving daily updates about cutting-edge news and trends or if you’d like to be removed from our e-mailing list.

Your own related posts, comments and personal referrals are appreciated as well.

Thank You Dr. David Edward Marcinko MBA MEd CMP Editor-in-Chief MarcinkoAdvisors@msn.com

Posted on June 1, 2015 by Dr. David Edward Marcinko MBA MEd CMP™

[By Staff reporters]

An Educational Resource Supporting Doctors, Universities and Consulting Advisors

We are an emerging online and onground community that connects medical professionals with financial advisors and management consultants. We participate in a variety of insightful educational seminars, teaching conferences and national workshops. We produce journals, textbooks and handbooks, white-papers, CDs and award-winning dictionaries. And, our didactic heritage includes innovative R&D, litigation support, opinions for engaged private clients and media sourcing in the sectors we passionately serve.

Through the balanced collaboration of this rich-media sharing and ranking forum, we have become a leading network at the intersection of healthcare administration, practice management, medical economics, business strategy and financial planning for doctors and their consulting advisors. Even if not seeking our products or services, we hope this knowledge silo is useful to you.

In the Health 2.0 era of political reform, our goal is to: “bridge the gap between practice mission and financial solidarity for all medical professionals.”

Join the ME-P Nation today … and tell us what you think!

***

***

OUR BOOKS, TEXTS AND DICTIONARIES ARE VITAL SURVIVAL TOOLS FOR ALL PHYSICIANS … AND THEIR CONSULTING ADVISORS

***

8

***

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

We are an emerging online and onground community that connects medical professionals with financial advisors and management consultants.

We participate in a variety of insightful educational seminars, teaching conferences and national workshops. We produce journals, textbooks and handbooks, white-papers, CDs and award-winning dictionaries. And, our didactic heritage includes innovative R&D, litigation support, opinions for engaged private clients and media sourcing in the sectors we passionately serve.

Through the balanced collaboration of this rich-media sharing and ranking forum, we have become a leading network at the intersection of healthcare administration, practice management, medical economics, business strategy and financial planning for doctors and their consulting advisors. Even if not seeking our products or services, we hope this knowledge silo is useful to you.

In the Health 2.0 era of political reform, our goal is to: “bridge the gap between practice mission and financial solidarity for all medical professionals.”

There is no certification program, course of study or professional designation for FAs who wish to enter the lucrative financial planning space serving physicians and healthcare professionals.

That’s why the R&D efforts of our governing board of physician-directors, accountants, financial advisors, academics and health economists identified the need for integrated personal financial planning and medical practice management as an effective first step in the survival and wealth building life-cycle for physicians, nurses, healthcare executives, administrators and all medical professionals.

Now – more than ever – desperate doctors of all ages are turning to knowledge able financial advisors and medical management consultants for help. Symbiotically too, generalist advisors are finding that the mutual need for extreme niche synergy is obvious.

But, there was no established curriculum or educational program; no corpus of knowledge or codifying terms-of-art; no academic gravitas or fiduciary accountability; and certainly no identifying professional designation that demonstrated integrated subject matter expertise for the increasingly unique healthcare focused financial advisory niche … Until Now!

Enter the Certified Medical Planner™ charter professional designation. And, CMPs™ are FIDUCIARIES, 24/7.

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES: