BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Exchange‑traded funds (ETFs) have been one of the most transformative innovations in modern investing. Since the first U.S. ETF launched in the early 1990s, they have grown from a niche product to a dominant force, reshaping how individuals and institutions build portfolios. Their rise has been so dramatic that it’s fair to ask whether ETFs have already peaked. Are they past their prime, or are they simply entering a more mature—and still powerful—phase of their evolution?

To answer that, it helps to understand why ETFs became so popular in the first place. They offered something investors had long wanted: low‑cost, diversified exposure to markets without the high fees and underperformance that plagued many actively managed mutual funds. ETFs also traded like stocks, giving investors flexibility and transparency that mutual funds couldn’t match. These advantages fueled explosive growth, especially as passive investing gained cultural and academic momentum. For years, ETFs were the fresh, disruptive alternative to traditional funds.

But today, the landscape looks different. ETFs are no longer the scrappy upstarts; they are the establishment. With trillions of dollars in assets and thousands of products on the market, the ETF ecosystem is crowded, competitive, and increasingly complex. This shift has led some observers to argue that ETFs have reached saturation—that the innovation wave has crested and the industry is coasting on past success.

There is some truth to the idea that the ETF boom has matured. Many of the most useful, broad‑market ETFs already exist, and new launches often feel like variations on a theme. Investors can choose from dozens of S&P 500 ETFs, dozens more bond ETFs, and an overwhelming array of thematic funds that slice the market into ever‑narrower niches. When a market becomes this saturated, it’s natural to wonder whether the era of groundbreaking ETF innovation is behind us.

Yet maturity is not the same as decline. In fact, the very saturation that critics point to is evidence of the ETF’s enduring relevance. Investors continue to demand these products, and issuers continue to create them because ETFs remain one of the most efficient vehicles for accessing markets. Even if the pace of novelty has slowed, the core value proposition—low cost, liquidity, transparency—has not diminished.

Moreover, ETFs are still evolving in meaningful ways. One of the most significant developments in recent years has been the rise of actively managed ETFs. For decades, ETFs were synonymous with passive investing, but that boundary has blurred. Active managers have embraced the ETF structure because it offers tax advantages and lower operating costs compared to traditional mutual funds. This shift has opened the door to new strategies and has attracted investors who want the benefits of active management without the drawbacks of older fund structures. Far from being past their prime, ETFs are expanding into territory once considered off‑limits.

Another area of growth is fixed‑income ETFs. Bond markets have historically been opaque and difficult for individual investors to navigate. ETFs have changed that by offering simple, liquid access to everything from government bonds to high‑yield credit. During periods of market stress, bond ETFs have even served as price discovery tools, providing transparency when underlying bond markets were sluggish. This role suggests that ETFs are not just surviving—they are becoming integral to how modern markets function.

The rise of thematic and specialized ETFs also complicates the “past their prime” narrative. While some of these funds are gimmicky or short‑lived, others have tapped into genuine long‑term trends such as clean energy, cybersecurity, and artificial intelligence. These products allow investors to express views on specific sectors or technologies without picking individual stocks. Even if not every thematic ETF succeeds, the category reflects ongoing experimentation and investor interest.

***

***

Of course, ETFs are not without challenges. Their popularity has raised concerns about market concentration, especially in large index funds that hold significant portions of major companies. Some critics argue that passive investing distorts price signals or contributes to market bubbles. Others worry about liquidity risks in certain types of ETFs, particularly those holding less liquid assets. These debates are important, but they do not indicate that ETFs are fading. Instead, they show that ETFs have become so influential that their impact must be carefully examined.

Ultimately, the question of whether ETFs are past their prime depends on how one defines “prime.” If it means rapid, explosive growth driven by novelty, then yes—the early era of ETF disruption has passed. The industry is more mature, more crowded, and less defined by breakthrough innovation than it once was. But if “prime” refers to relevance, utility, and influence, then ETFs are arguably stronger than ever. They have become foundational tools for investors of all types, from retirees to hedge funds. Their evolution into active strategies, fixed‑income markets, and thematic investing shows that they are still adapting to new demands.

ETFs may no longer be the newest thing in finance, but they remain one of the most powerful. Rather than being past their prime, they appear to be settling into a long, stable middle age—one defined not by hype, but by enduring value.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Alternatively Weighted Exchange Traded Funds are designed to track an index that is constructed based on criteria other than market capitalization (the methodology used for most traditional indexes).

Instead, alternatively weighted indexes select and weight securities based on other factors, such as growth, valuation, and price momentum, among others. Examples include:

Invesco S&P 500 Equal Weight ETF (NYSEARCA: RSP)

SPDR Technology ETF (NYSEARCA: XNTK)

First Trust NYSE Arca Biotechnology Index Fund (NYSEARCA: FBT)

Amplify Online Retail ETF (NASDAQ: IBUY)

iShares MSCI USA Equal Weighted ETF (NYSEARCA: EUSA)

FIVE INVESTING MISTAKES OF DOCTORS; PLUS 1 VITAL TIP

As a former US Securities and Exchange Commission [SEC] Registered Investment Advisor [RIA] and business school professor of economics and finance, I’ve seen many mistakes that doctors must be aware of, and most importantly, avoid. So, here are the top 5 investing mistakes along with suggested guideline solutions.

Mistake 1: Failing to Diversify Investment but Beware Di-Worsification

A single investment may become a large portion of your portfolio as a result of solid returns lulling you into a false sense of security. The Magnificent Seven stocks are a current example:

Apple, up +5,064%% since 1/18/2008

Amazon, up +30,328% since 9/6/2002

Alphabet, up +1,200% since 7/20/2012

Tesla, up +21,713% since 11/16/2012

Meta, up +684% since 2/20/2015

Microsoft, up +22% since 12/21/2023

Nvidia, up +80,797% since 4/15/2005

Guideline: The Magnificent Seven [7] has grown from 9% of the S&P 500 at the end of 2013 to 31% at the end of 2024! That means even if you don’t own them, you’re still very exposed if you have an Index Fund [IF] or Exchange Traded Fund [ETF] that tracks the market. Accordingly, diversification is the only free lunch in investing which can reduce portfolio risk. But, remember the Wall Street insider aphorism that states: “Di-Versification Means Always Having to Say Your Sorry.”

The term “Di-Worsification” was coined by legendary investor Peter Lynch in his book, One Up On Wall Street to refer to over-diversifying an investment portfolio in such a way that it reduces your overall risk-return characteristics. In other words, the potential return rises with an increase in risk and invested money can render higher profits only if willing to accept a higher possibility of losses [1].

A podiatrist can easily fall into the trap of chasing securities or mutual funds showing the highest return. It is almost an article of faith that they should only purchase mutual funds sporting the best recent performance. But in fact, it may actually pay to shun mutual funds with strong recent performance. Unfortunately, many struggle to appreciate the benefits of their investment strategy because in jaunty markets, people tend to run after strong performance and purchase last year’s winners.

Similarly, in a market downturn, investors tend to move to lower-risk investment options, which can lead to missed opportunities during subsequent market recoveries. The extent of underperformance by individual investors has often been the most awful during bear markets. Academic studies have consistently shown that the returns achieved by the typical stock or bond fund investors have lagged substantially.

Guideline: Understand chasing performance does not work.Continually monitor your investments and don’t feel the need to invest in the hottest fund or asset category. In fact, it is much better to increase investments in poor performing categories (i.e. buy low). Also keep in remind rebalancing of assets each year is key. If stocks perform poorly and bonds do exceptionally well, then rebalance at the end of the year. In following this strategy, this will force a doctor into buying low and selling high each year.

Often doctors make their investment decisions under the belief that stocks will consistently give them solid double-digit returns. But the stock markets go through extended long-term cycles.

In examining stock market history, there have been 6 secular bull markets (market goes up for an extended period) and 5 secular bear markets (market goes down) since 1900. There have been five distinct secular bull markets in the past 100+ years. Each bull market lasted for an extended period and rewarded investors.

For example, if an investor had started investing in stocks either at the top of the markets in 1966 or 2000, future stock market returns would have been exceptionally below average for the proceeding decade. On the other hand, those investors fortunate enough to start building wealth in 1982 would have enjoyed a near two-decade period of well above average stock market returns. They key element to remember is that future historical returns in stocks are not guaranteed. If stock market returns are poor, one must consider that he or she will have to accept lower projected returns and ultimately save more money to make up for the shortfall. For example,

The May 6th, 2010, flash crash, also known as the crash of 2:45, was a United States trillion-dollar stock market plunge which started at 2:32 pm EST and lasted for approximately 36 minutes.

And, investors who have embraced the “buy the dip” strategy in 2025 have been handsomely rewarded, with the S&P 500 delivering its strongest post-pull back returns in over three decades.

According to research from Bespoke Investment Group, the S&P 500 has gained an average of 0.36% in the trading session following a down day so far in 2025. The only year with a comparable performance was 2020, which saw a 0.32% average post-dip gain [2].

The most recent example came on May 27, 2025 when the S&P 500 surged more than 2% after falling 0.7% in the final session before the holiday weekend. The rally was sparked by President Trump’s decision to scale back huge previously threatened tariffs on EU —a recurring catalyst behind many of 2025’s rebound.

Guideline: Beware of projecting forward historical returns. Doctors should realize that the stock markets are inherently volatile and that, while it is easy to rely on past historical averages, there are long periods of time where returns and risk deviate meaningfully from historical averages.

Some doctors believe they are “smarter than the market” and can time when to jump in and buy stocks or sell everything and go to cash. Wouldn’t it be nice to have the clairvoyance to be out of stocks on the market’s worst days and in on the best days?

Using the S&P 500 Index, our agile imaginary doctor-investor managed to steer clear of the worst market day each year from January 1st, 1992 to March 31st, 2012. The outcome: s/he compiled a 12.42% annualized return (including reinvestment of dividends and capital gains) during the 20+ years, sufficient to compound a $10,000 investment into $107,100.

But what about another unfortunate doctor-investor that had the mistiming to be out of the market on the best day of each year. This ill-fated investor’s portfolio returned only 4.31% annualized from January 1992 – March 2012, increasing the $10,000 portfolio value to just $23,500 during the 20 years. The design of timing markets may sound easy, but for most all investors it is a losing strategy.

More contemporaneously on December 18th 2024, the DJIA plummeted 2.5%, while the S&P 500 declined 3% and the NASDAQ tumbled 3.5%

Guideline: If it looks too good to be true, it probably is. While jumping into the market at its low and selling right at the high is appealing in theory, we should recognize the difficulties and potential opportunity and trading costs associated with trying to time the stock market in practice. In general, colleagues are be best served by matching their investment with their time horizon and looking past the peaks / valleys along the way.

Mistake 5: Failing to Recognize the Impact of Fees and Expenses

A free dinner seminar or a polished stock-broker sales pitch may hide the total underlying costs of an investment. So, fees absolutely matter.

The first costing step is determining what the fees actually are. In a mutual fund, these costs are found in the company’s obligatory “Fund Facts”. This manuscript clearly outlines all the fees paid–including up front fees (commissions and loads), deferred sales charges and any switching fees. Fund management expense ratios are also part of the overall cost. Trading costs within the fund can also impact performance.

Here is a list of the traditional mutual fund fees:

Front End Load: The commission charged to purchase a fund through a stock broker or financial advisor. The commission reduces the amount you have available to invest. Thus, if you start with $100,000 to invest, and the advisor charges up to an 8 percent front end load, you end up actually investing $92,000.

Deferred Sales Charge (DSC) or Back End Load: Imposed if you sell your position in the mutual fund within a pre-specified period of time (normally one – five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: Costs of the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing fees.

Annual Administration Fee: Many mutual fund companies also charge a fee just for administering the account – usually under $100-150 per year.

Guideline: Know and understand all fees.

For example: A 1 percent disparity in fees may not seem like much but it makes a considerable impact over a long time period.

Consider a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the investor pays a 2 percent operating fee. In comparison, if s/he opted for a fund that charged a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000!

This is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more savings over a long period of time.

One Vital Tip: Investing Time is on Your Side

Despite thousands of TV shows, podcasts, textbooks, opinions and university studies on investing, it really only has three simple components. Amount invested, rate of return and time. By far, the most important item is time! For example:

Nvidia: if you invested $1,000 in 2009, you’d have $338,103 today.

Apple: if you invested $1,000 in 2008, you’d have $48,005 today.

Netflix: if you invested $1,000 in 2004, you’d have $495,679 today.

Unfortunately, this list of investing mistakes is still being made by many doctors. Fortunately, by recognizing and acting to mitigate them, your results may be more financially fruitful and mentally quieting.

REFERENCES:

1. Lynch, Peter: One Up on Wall Street [How to Use What You Already Know to Make Money in the Market]: Simon and Shuster (2nd edition) New York, 2000.

1. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York, 2006.

3. Marcinko, DE; Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] CRC Press, New York, 2015.

BIO: As a former university Professor and Endowed Department Chair in Austrian Economics, Finance and Entrepreneurship, the author was a NYSE Registered Investment Advisor and Certified Financial Planner for a decade. Later, he was a private equity and wealth manager

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

According to wikipedia, the S&P 500 Dividend Aristocrats is a stock market index composed of the companies in the S&P 500 index that have increased their dividends in each of the past 25 consecutive years. It was launched in May 2005.

There are other indexes of dividend aristocrats that vary with respect to market cap and minimum duration of consecutive yearly dividend increases. Components are added when they reach the 25-year threshold and are removed when they fail to increase their dividend during a calendar year or are removed from the S&P 500. However, a study found that the stock performance of companies improves after they are removed from the index The index has been recommended as an alternative to bonds for investors looking to generate income.

To invest in the index, there are several exchange traded funds (ETFs), which seek to replicate the performance of the index.

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

“Phantom Tax” or “Phantom Income” for direct owners of Treasury inflation-protected securities (TIPS) TIPS adjust their principal values and interest payments for inflation. As with other directly owned Treasury securities, TIPS principal, including the inflation adjustments, is not paid back to investors until the securities mature.

However, the principal adjustments are taxed by the IRS as income in the year in which they occur, even though no actual payments are made in those years to investors who own TIPS directly. This is why this income is called “phantom income” and the tax on it is known as the “phantom tax.”

Investors can avoid the phantom income/tax issue for TIPS by holding TIPS in tax-deferred retirement accounts. Mutual funds and Exchange Traded Funds (ETFs) typically take the “phantom” factor out of TIPS ownership by distributing the principal adjustments as taxable dividends.

As with direct ownership of TIPS, the tax consequences of these distributions by mutual funds and ETFs can be reduced by holding TIPS-owning instruments in tax-deferred retirement accounts

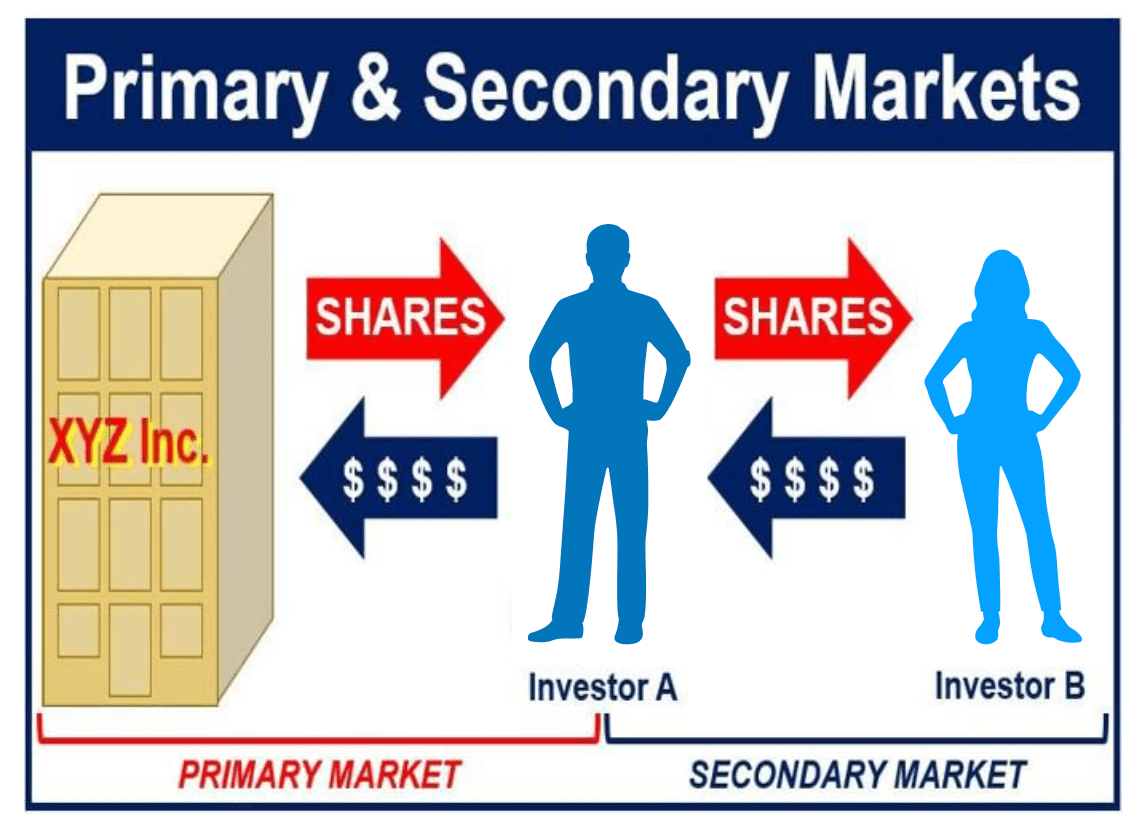

Primary Market: The primary market is also part of the stock market but differs from the secondary market because it only sells newly issued stocks.

Primary Market for Exchange Traded Funds: The primary market is where ETF shares are created and redeemed amongst ETF issuers and authorized participants. This is where the underlying basket of securities that make up an ETF is created. Shares of ETFs are made in large batches called Creation Units—usually 25,000 to 600,000 ETF shares are created at a time through this process.

Active transparent ETFs: Daily disclosure of portfolio holdings is an attribute of traditional index-based Exchange Traded Funds (ETFs).

Active transparent exchange traded funds are actively managed by a portfolio manager or team of managers. As with index-based ETFs, their portfolio holdings are disclosed daily.

Basis Points are used in financial literature to express values that are carried out to two decimal places (hundredths of a percentage point), particularly ratios, such as yields, fees, and returns. Basis points describe values that are typically on the right side of the decimal point–one basis point equals one one-hundredth of a percentage point (0.01%). So 25 basis points equals 0.25%, and 50 basis points equals 0.50%.

Only when basis points equal or exceed 100 does the value move to the left of the decimal point–100 basis points equals 1.00%, 500 basis points equals 5.00%, etc.

Bid/Ask Spread (also known as bid/offer spread) is the difference between the National Best Bid and the National Best Offer, which represents the implied cost to trade a security.

As compensation for the risk taken, the market maker (or dealer) earns the bid/offer spread in exchange for facilitating the trade. Wider spreads generally indicate higher costs associated with trading the underlying assets in the ETF, hedging costs, inventory management costs, and general market risk.

Posted on November 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Active investment management strategies are the opposite of passive investment strategies. Active portfolio managers regularly take investment positions that clearly differ from those of the portfolio’s performance benchmark, with the objective of outperforming the benchmark over time.

In addition to the upside potential of outperforming the benchmark, there’s also the downside possibility of under performing the benchmark. In an efficient market, there should be roughly the same magnitude of out performers and under performers for any given benchmark. But, markets are not always efficient.

Active non-transparent investment management strategies are Exchange Traded Funds that are actively managed by a portfolio manager or team of managers without daily disclosure of portfolio holdings. Active transparent strategies are daily disclosures of portfolio holdings as an attribute of traditional index-based Exchange Traded Funds (ETFs). Active transparent exchange traded funds are actively managed by a portfolio manager or team of managers. As with index-based ETFs, their portfolio holdings are disclosed daily.

NOTE: Absolute return as an investment vehicle seeks to make positive returns by employing investment management techniques that differ from traditional mutual funds. Absolute return investment techniques include using short selling, futures, options, derivatives, arbitrage, leverage and unconventional assets.

Posted on September 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BITCOIN MINER HALVING

By Staff Reporters

***

***

DEFINITION: After the network mines 210,000 blocks—roughly every four years—the block chain reward given to Bitcoin miners for processing transactions is cut in half. This event is called halving because it cuts the rate at which new bitcoins are released into circulation in half. This rewards system will continue until about 2140, when the proposed limit of 21 million coins is reached. At that point, miners will be rewarded with fees for processing transactions, which network users will pay. These fees ensure miners are still incentivized to participate and keep the network going.

And, so, the total value of the world’s most popular cryptocurrency surpassed $1 trillion yesterday for the first time since 2021. The overall crypto market, meanwhile, broke $2 trillion in market cap, fueled by investor confidence. If crypto were a publicly traded company, it would be the fourth-largest in the world behind Microsoft, Apple, and Saudi Aramco.

***

***

HALVING – The quadrennial event, expected to take place today or tomorrow, was built into bitcoin’s original code to cut the amount of new coins going into circulation in half every four years. The purpose is to thwart inflation and increase the currency’s value. Bitcoin’s mysterious creator, Satoshi Nakamoto, designed the crypto so that only 21 million bitcoins would ever exist. It will take about a century to hit that number, but as it approaches the cutoff, the crypto hose slowly constricts. No one’s sure what happens next

Historically, halvings have coincided with big jumps in price—the coin’s first halving in 2012 saw the price jump from $12.35 to $127 within five months, according to Time. But critics argue that the narrative around halving is much stronger than the actual event. Even bitcoin experts aren’t sure what will happen with the volatile asset. It already hit a record high of over $73,750 in March, thanks to the spot bitcoin ETF approval. And, lest we forget, the whole FTX thing happened since the last halving.

Posted on August 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

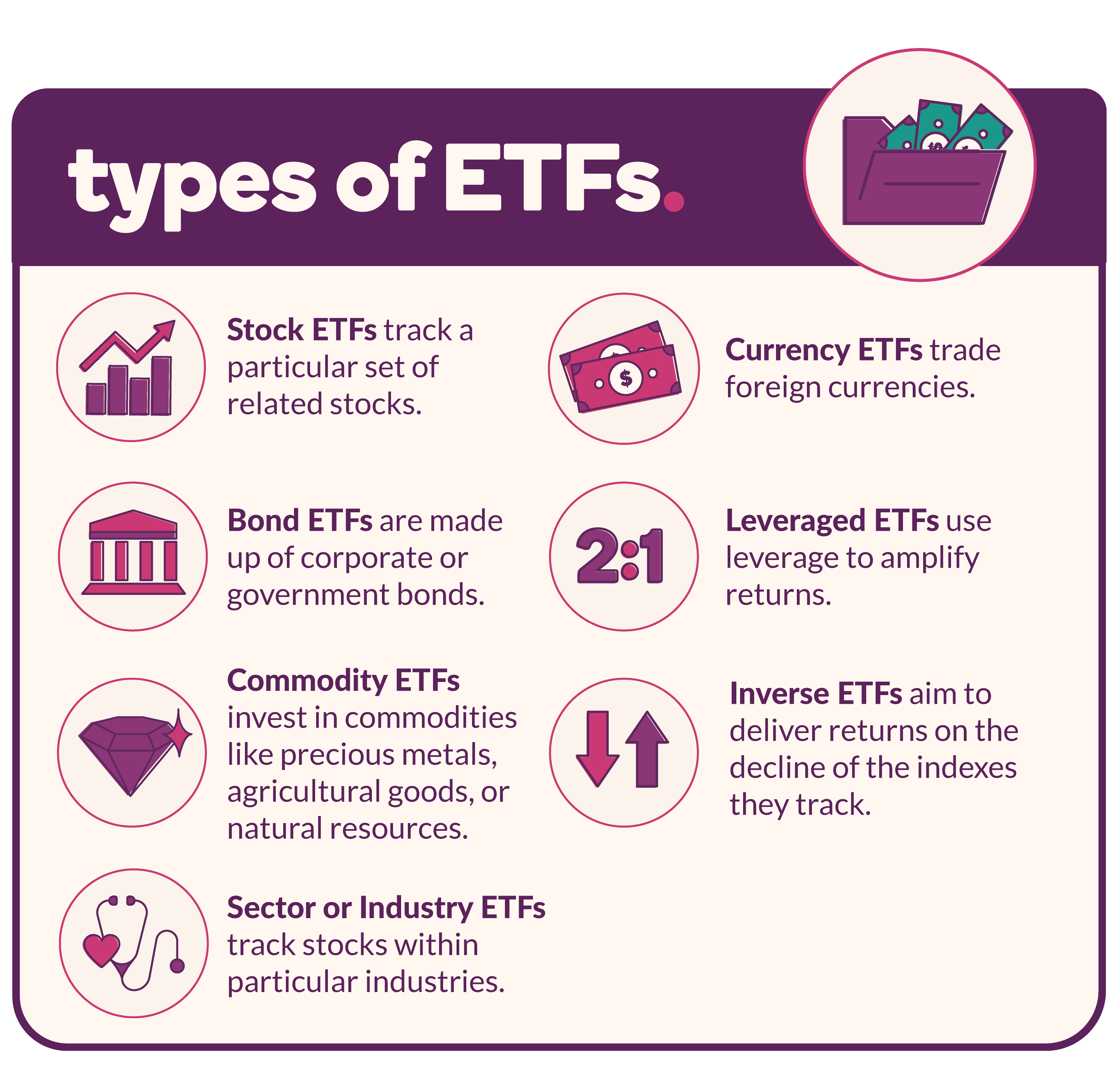

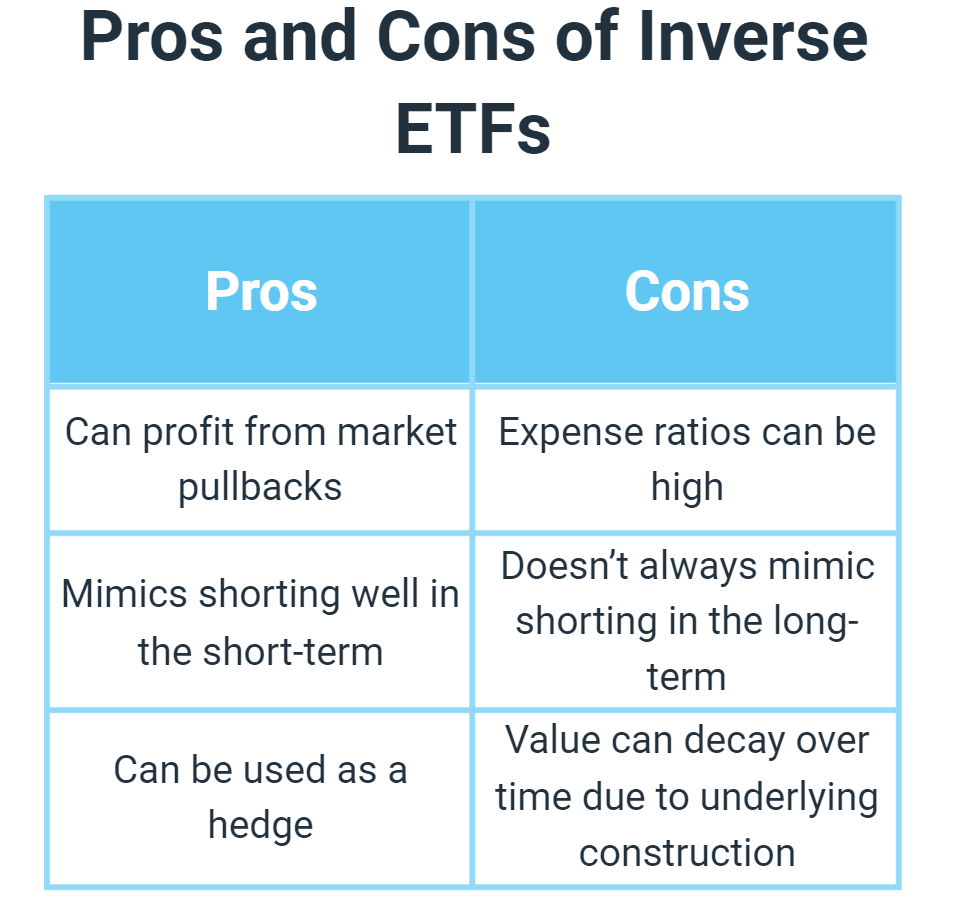

What are inverse ETFs?

An inverse ETF, often known as a bear or short ETF, is an exchange-traded fund designed to profit from a market decline. These short-term, publicly traded investments are utilized by investors who believe that a particular market or individual security will lose value in the near future. They may use inverse ETFs as a way of hedging losses during a downturn.

“Inverse ETFs are a tool to hedge a stock portfolio,” according to John DeYonker. “If the S&P 500 is your benchmark, and it goes up 1%, then your hedge will go down 1% and vice versa. Hedging with inverse ETFs can reduce volatility for investors—it’s like insurance.”

Investors may also use inverse ETFs as a way to take advantage of a predicted decline. In this way, they may be used as an alternative to short selling. For example, if an investor believes that the oil industry will have a setback in the immediate future, they may choose to purchase an inverse ETF of securities tied to energy producers. If correct in their prediction, the investor’s inverse ETF may recognize a profit. If the investor is incorrect, and the market or individual security increases in price, they may see a loss.

An investor who believes that the S&P 500 will decline, for example, may choose to purchase shares of the ProShares Short S&P 500. This inverse ETF’s value is inversely proportional to the overall S&P 500 index.

Inverse ETFs are generally considered to be highly volatile investments, as their losses typically compound daily. This makes inverse ETFs more risky than the index to which they are tied.

Thirty one years ago yesterday, the first exchange-traded fund (ETF) in the US launched. In the decades since, these once-niche investment products have become ubiquitous on Wall Street, disrupting the mutual fund industry and transforming people’s relationship with the stock market.

On January 29th, 1993, a spider decoration hanging in the American Stock Exchange heralded the arrival of the first US ETF—what’s now called the SPDR S&P 500 ETF Trust. It had a measly $6.5 million in assets and no one really paid much attention to it. The first US ETF is now the world’s biggest, with $375 billion in assets, and the ETF sector in total had amassed $6.5 trillion in assets by the end of 2022. While mutual funds still have 3x the amount of assets that ETFs have, the tide is turning: Investors poured $600 billion into US ETFs on a net basis last year, but pulled out almost $1 trillion from mutual funds.

Definition: An ETF is simply a security that tracks the performance of a particular basket of investments, like stocks. The SPDR S&P 500 ETF, for example, tracks the performance of companies in the S&P 500. Many other ETFs also track indexes, allowing people to park their money in funds that follow the ebbs and flows of the broader market.

If that sounds like a mutual fund…it’s similar. But ETFs have a few advantages over its stuffy, older cousin.

ETFs generally have lower fees than mutual funds.

They have built-in tax benefits.

They’re accessible to anyone with a brokerage account—you can buy or sell them like you would a stock.

Finally,all these advantages aside, the rise of ETFs has been also fueled by the growing recognition that trying to invest in individual stocks is foolish. Passive index funds, which aren’t designed for frequent trading, have surged to represent almost half of US fund assets, compared to less than 2% in the early ’90s.

Posted on February 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Crypto may not be back to having celebs hawk it during the Super Bowl after a series of scams and bankruptcies rocked the industry, but yesterday, the price of bitcoin rose higher than $50,000 for the first time since December 2021.

Last month’s decision by US regulators to allow spot bitcoin ETFs, which pushes the digital currency toward the mainstream by making it easier for people to access, didn’t initially significantly drive up prices, but interest in the ETFs helped spur the recent rise.

The S&P 500® index (SPX) fell 3.21 points (0.1%) to 4,780.24; the Dow Jones Industrial Average® (DJI) gained 15.29 points to 37,711.02; the NASDAQ Composite® (COMP)rose 0.55 point to 14,970.19.

The 10-year Treasury note yield dropped about 4 basis points to 3.988%.

The CBOE® Volatility Index (VIX) fell 0.25 to 12.44.

Nathan Peterson, director of derivatives analysis at the Schwab Center for Financial Research, noted that technology was one of few sectors to buck Thursday’s market weakness, as so-called mega-caps including Nvidia (NVDA) and Microsoft (MSFT) notched new record highs. Also, Amazon (AMZN), Google parent Alphabet (GOOGL), and Netflix (NFLX) each posted new 52-week highs, illustrating continued investor rotation back into that sector.

In other markets, the Securities and Exchange Commission (SEC) approved exchange-traded funds (ETF) linked to the spot bitcoin market late Wednesday. The spot market, also known as the cash market, refers to forums where commodities, securities, and other assets can be immediately exchanged between buyers and sellers. The move opens up a new crypto inroad for investors who might otherwise not want to hold actual bitcoin and looks like a potential bellwether event for individual investors and crypto itself. ETFs linked to spot bitcoin began trading today.

Bitcoin prices have nearly tripled since the start of 2023, reaching $47,000 earlier this month, partly reflecting anticipation of the SEC decision and amid hopes of easing interest rate policy.

Posted on January 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Inflation climbed from 3.1% to 3.4% in December, a sign the Federal Reserve will continue to have to wrestle consumer price growth down to its desired 2% level. Forecasts had been for a reading of 3.2%.

On a monthly basis, inflation hit 0.3%, while core inflation, which strips away the more volatile costs of food and energy, was 3.9%, down from 4% in November but ahead of forecasts for a reading of 3.8%.

***

***

The Securities and Exchange Commission (SEC) officially approved spot bitcoin ETFs yesterday for the first time. The 11 exchange-traded funds will let old-school investors and bitcoin enthusiasts alike access the world’s biggest cryptocurrency without having to keep a long password for a crypto wallet.

The long-awaited win for the beleaguered crypto industry came after a false start on Tuesday, when someone hacked the agency’s X account that…didn’t have two-factor authentication enabled…and spuriously said the ETFs had been approved.

Crypto investors have been asking for spot bitcoin ETFs since roughly 2013, but the SEC has historically grimaced at the idea of inviting such a volatile asset into the financial system, concerned that a bitcoin ETF could be easily manipulated. Trading could begin as early as today.

Posted on August 30, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Bitcoin gets a boost from landmark ETF ruling

An appeals court said the SECwas wrong to reject an application from crypto investment firm Grayscale to create a spot bitcoin exchange-traded fund (ETF), sending the price of bitcoin up about 6.5%.

The slumbering crypto industry has been eagerly anticipating a spot bitcoin ETF (as opposed to existing crypto ETFs based on futures) because it could attract a torrent of cash and interest from individual investors. The SEC said it was reviewing the decision.

Posted on July 17, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: Stocks are rolling following a week that showed our inflation emergency seems to be ending, and big banks are still raking in big profits. The Fed’s so-called “soft landing” scenario—getting inflation down without tipping the economy into a recession—is a distinct possibility, as long as corporate finances don’t end up being shockingly bad this earnings season.

Global economy: While the US economy is chugging along, the same can’t be said for China. Growth in the world’s No. 2 economy hardly budged between the first and second quarters, while youth unemployment hit a record last month. Expect President Xi Jinping to make moves to juice China’s stagnating GDP.

***

***

Curiously, Cathie Wood’s flagship exchange-traded fund has rallied more than 50% this year. Investors are using that as an opportunity to get out.

They have pulled a net $717 million from the ARK Innovation ETF over the past 12 months, according to FactSet. That exodus marks a notable shift for a fund that had consistently drawn investor cash since its 2014 inception. Once the largest actively managed ETF with nearly $30 billion in assets under management, the fund has shrunk to roughly $9 billion, mostly due to investment losses.

Known by its ticker symbol ARKK, Wood’s fund became an investor darling shortly after the onset of the Covid-19 pandemic with hugely successful bets on unprofitable and “disruptive” technology companies. It took in huge amounts of investor money, culminating with a $6.5 billion inflow in the first quarter of 2021, when its share price peaked.

Then, the Federal Reserve’s fastest interest-rate hiking campaign in decades crushed the valuations of unprofitable growth companies, which often attract investors when interest rates are low and returns on safer investments such as CDs are minimal. Shares of ARKK plunged 67% in 2022, but its investors largely held on or bought the dip.

Now, analysts say they expect some of those investors are getting out for good?

Posted on January 17, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Cathie Wood and Ark’s flagship exchange-traded fund Ark Innovation ETF (NYSE: ARKK) bought 168,989 shares of Tesla on Friday, valued at $20.68 million at the session’s closing price. The stock ended Friday’s session down 0.94% at $122.40, according to Benzinga Pro data. At one point in the session, the loss was as much as 6.4%. For the week, the stock gained 8.26%.

Investing $1,000 in META Stock: Shares of Meta Platforms traded at $332.46 on June 4, 2021. A $1,000 investment could have purchased 3 shares of META stock. The $1,000 investment would be worth $410.94 today, based on a current price of $136.98 for Meta Platforms. This represents a loss of 58.9% in 19 months.

***

European equities and US stock-index futures fell amid signs central banks will turn more hawkish and as investors focused on earnings reports from Wall Street banks.

Posted on July 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

Markets: The S&P’s drop of more than 21% was its biggest H1 plunge since 1970. Its second quarter was the worst since Q1 of 2020. And while the S&P is floundering in the bear market, the NASDAQ, which is loaded with tech stocks, has taken an even bigger licking: It’s plunged more than 30% since its peak last November. For example:

Netflix: down 71% YTD (the worst performer in the S&P)

Coinbase: down 81%

Even megacaps like Meta (-52%), Amazon (-38%), and Apple (-25%) haven’t been spared.

Ruja Ignatova promised her cryptocurrency, OneCoin, would become the next Bitcoin. The only problem: It didn’t exist. The FBI today added the Bulgarian-born Ignatova—accused of defrauding investors out of approximately $4.1 billion in a fake cryptocurrency scheme—to its most-wanted list. The 41-year-old has been on outstanding since October 2017, just days after a warrant was issued for her arrest in the U.S. In a press release, the FBI called OneCoin a “massive fraud scheme” and offered up to $100,000 for information leading to Ignatova’s arrest.

The U.S. Securities and Exchange Commission rejected a proposal from Grayscale to list a spot Bitcoin ETF on the NYSE Arca exchange, setting up a potential legal battle with the country’s biggest digital asset manager. The SEC said Grayscale’s request for an ETF listing, which it proposed as a conversion of its popular Grayscale Bitcoin Trust GBTC, didn’t meet the regulator’s standard of being “designed to prevent fraudulent and manipulative acts and practices” and “to protect investors and the public interest.” Grayscale said it would challenge the SEC’s decision in court, arguing that its approval of ETF’s that hold Bitcoin futures should “logically (make it) comfortable with ETFs that hold that same asset.”

Posted on January 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: Stocks are off to a sputtering start in 2022, and they could be in for more upheaval this week with a big inflation report due, Fed Chair Jerome Powell’s confirmation hearing on Capitol Hill, and the beginning of earnings season.

NASDAQ: Last week, the tech-heavy NASDAQ fell 4.5% for its worst week since February 2021. And the ARK Innovation ETF, which is full of high-growth tech companies, plunged 11%.

Bonds: Over in the bond market, yields (or the return you can get from buying a bond) are surging. On Friday, the yield for the 10-year Treasury note hit its highest level since January 2020. Now, While rising yields are generally a bullish sign for the economy, they also make riskier assets—like expensive tech stocks—less attractive compared to other names that may get a boost from higher interest rates. The Dow, for example, with its many financial services companies, lost just 0.29% last week.

Good News: Billionaire investor Chamath Palihapitiya said US stocks could rebound rapidly after the recent sell-off. He said there’s “a ton” of money waiting on the sidelines in products such as money market accounts.