BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Marcinko & Associates is financial guide. We help answer your questions in an empowering way. We educate and guide medical colleagues to understand their financial picture and to make better financial decisions. We strive to simplify everything, clear up confusion, and address specific needs and goals.

Simply put, we’re a financial services company on a mission to empower financial freedom for all healthcare professionals; only. We work with doctors, nurses, medical providers, individuals and all sizes of organizations to offer investment, wealth management and retirement solutions so everyone can have a clear and simple understanding of where their finances and career is today and where it is headed tomorrow.

Whatever your financial situation, we do not shame, criticize, or sell. We enrich, educate and empower. We work only with medical colleagues at every stage of their financial journey [students, interns, residents, practitioners, mid-career and mature physicians], through big life personal changes to annual employment reviews, in order to help them understand, invest, and protect their money and lifestyle.

Assess, develop, and align financial retirement and estate planning goals

Risk Management: Malpractice, home, life, medical, auto and personal indemnity

Life Insurance Need Reviews: whole, universal and term

Business, operations, HR, employment negotiations and medical practice management

Annuity Need Reviews: Indexed and Fixed [Pros and Cons].

***

***

At Marcinko & Associates we discuss specific needs and answer specific questions. We educate and make personalized recommendations that you are free to use, incorporate or disregard. Referrals to trusted specialists and strategic alliance partners then occur if – and as – needed [pro re nata].

Posted on September 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

The Medical Executive-Post Educational Resource

[By Ann Miller RN MHA]

We are an emerging online and onground community that connects medical professionals with financial advisors and management consultants. We participate in a variety of insightful educational seminars, teaching conferences and national workshops. We produce journals, textbooks and handbooks, white-papers, CDs and award-winning dictionaries. And, our didactic heritage includes innovative R&D, litigation support, opinions for engaged private clients and media sourcing in the sectors we passionately serve.

Through the balanced collaboration of this rich-media sharing and ranking forum, we have become a leading network at the intersection of healthcare administration, practice management, medical economics, business strategy and financial planning for doctors and their consulting advisors. Even if not seeking our products or services, we hope this knowledge silo is useful to you. Our content creation—including speaking topics, articles and course development—is client-driven.

In the Health 2.0 era of political reform, our goal is to: “bridge the gap between practice mission and financial solidarity for all medical professionals.”

THE CHALLENGE

Join the ME-P Nation today … and tell us what you think!

***

8

BOOK REVIEW

Am I over-insured and thus wasting money? Am I under-insured and thus at risk for a liability or other disaster? I never really had the means of answering these questions; until now.

Did you know that at MARCINKO & Associates, all medical colleagues throughout the United States may contact us when they are considering the sale, purchase, strategic operating improvement, merger, acquisition and/or other financial business or related personal financial planning transaction?

Our difference is “hard” knowledge and insider financial guidance that helps medical colleagues, nurses, private practitioners, clinics, ambulatory surgery, radiology and outpatient wound care centers realize their ultimate economic goals. This typically includes managerial and cost accounting, financial ratio analysis, fair market valuation business appraisals, business plan creation and personal financial planning.

Our “expert witness” business litigation support service and divorce mediation, arbitration, asset division, settlement and second opinion offerings are always available, as well.

And, our “soft” skill professional career guidance and mentoring center includes executive coaching, consulting and mentoring advisory programs for stressed, conflicted or burned-out physicians and medical practitioners.

Most importantly, our professional fees are reasonable and always transparent.

MARCINKO & Associates also serves universities, medical, business, graduate and nursing schools; physicians, dentists, podiatrists, optometrists and legal societies. This includes accountants, financial service providers, wealth and hedge fund managers, emerging entities, hospitals, CEOs and their BODs, the press, media and related organizations.

Financial advisors don’t ascribe to the Hippocratic Oath. People don’t go to work on “Wall Street” for the same reasons other people become firemen and teachers. There are no essays where they attempt to come up with a new way to say, “I just want to help people.”

Financial Advisor’s are Not Doctors

Some financial advisors and insurance agents like to compare themselves to CPAs, attorneys and physicians who spend years in training and pass difficult tests to get advanced degrees and certifications. We call these steps: barriers-to-entry. Most agents, financial product representatives and advisors, if they took a test at all, take one that requires little training and even less experience. There are few BTEs in the financial services industry.

For example, most insurance agent licensing tests are thirty minutes in length. The Series #7 exam for stock brokers is about 2 hours; and the formerly exalted CFP® test is about only about six [and now recently abbreviated]. All are multiple-choice [guess] and computerized. An aptitude for psychometric savvy is often as important as real knowledge; and the most rigorous of these examinations can best be compared to a college freshman biology or chemistry test in difficulty.

Yet, financial product salesman, advisors and stock-brokers still use lines such as; “You wouldn’t let just anyone operate on you, would you?” or “I’m like your family physician for your finances. I might send you to a specialist for a few things, but I’m the one coordinating it all.” These lines are designed to make us feel good about trusting them with our hard-earned dollars and, more importantly, to think of personal finance and investing as something that “only a professional can do.”

Unfortunately, believing those lines can cost you hundreds of thousands of dollars and years of retirement.

***

***

Suitability Rule

A National Association of Securities Dealers [NASD] / Financial Industry Regulatory Authority [FINRA] guideline that require stock-brokers, financial product salesman and brokerages to have reasonable grounds for believing a recommendation fits the investment needs of a client. This is a low standard of care for commissioned transactions without relationships; and for those “financial advisors” not interested in engaging clients with advice on a continuous and ongoing basis. It is governed by rules in as much as a Series #7 licensee is a Registered Representative [RR] of a broker-dealer. S/he represents best-interests of the firm; not the client.

And, a year or so ago there we two pieces of legislation for independent broker-dealers-Rule 2111 on suitability guidelines and Rule 408(b)2 on ERISA. These required a change in processes and procedures, as well as mindset change.

Note: ERISA = The Employee Retirement Income Security Act of 1974 (ERISA) codified in part a federal law that established minimum standards for pension plans in private industry and provides for extensive rules on the federal income tax effects of transactions associated with employee benefit plans. ERISA was enacted to protect the interests of employee benefit plan participants and their beneficiaries by:

Requiring the disclosure of financial and other information concerning the plan to beneficiaries;

Establishing standards of conduct for plan fiduciaries ;

Providing for appropriate remedies and access to the federal courts.

ERISA is sometimes used to refer to the full body of laws regulating employee benefit plans, which are found mainly in the Internal Revenue Code and ERISA itself. Responsibility for the interpretation and enforcement of ERISA is divided among the Department Labor, Treasury, IRS and the Pension Benefit Guarantee Corporation.

Yet, there is still room for commissioned based FAs. For example, some smaller physician clients might have limited funds [say under $100,000-$250,000], but still need some counsel, insight or advice.

Or, they may need some investing start up service from time to time; rather than ongoing advice on an annual basis. Thus, for new doctors, a commission based financial advisor may make some sense.

Prudent Man Rule

This is a federal and state regulation requiring trustees, financial advisors and portfolio managers to make decisions in the manner of a prudent man – that is – with intelligence and discretion. The prudent man rule requires care in the selection of investments but does not limit investment alternatives. This standard of care is a bit higher than mere suitability for one who wants to broaden and deepen client relationships.

***

***

Prudent Investor Rule

The Uniform Prudent Investor Act (UPIA), adopted in 1992 by the American Law Institute’s Third Restatement of the Law of Trusts, reflects a modern portfolio theory [MPT] and total investment return approach to the exercise of fiduciary investment discretion. This approach allows fiduciary advisors to utilize modern portfolio theory to guide investment decisions and requires risk versus return analysis. Therefore, a fiduciary’s performance is measured on the performance of the entire portfolio, rather than individual investments

Fiduciary Rule

The legal duty of a fiduciary is to act in the best interests of the client or beneficiary. A fiduciary is governed by regulations and is expected to judge wisely and objectively. This is true for Investment Advisors [IAs] and RIAs; but not necessarily stock-brokers, commission salesmen, agents or even most financial advisors. Doctors, lawyers, and the clergy are prototypical fiduciaries.

***

***

More formally, a financial advisor who is a fiduciary is legally bound and authorized to put the client’s interests above his or her own at all times. The Investment Advisors Act of 1940 and the laws of most states contain anti-fraud provisions that require financial advisors to act as fiduciaries in working with their clients. However, following the 2008 financial crisis, there has been substantial debate regarding the fiduciary standard and to which advisors it should apply. In July of 2010, The Dodd-Frank Wall Street Reform and Consumer Protection Act mandated increased consumer protection measures (including enhanced disclosures) and authorized the SEC to extend the fiduciary duty to include brokers rather than only advisors, as prescribed in the 1940 Act. However, as of 2014, the SEC has yet to extend a meaningful fiduciary duty to all brokers and advisors, regardless of their designation.

Ultimately, physician focused and holistic “financial lifestyle planning” is about helping some very smart people change their behavior for the better. But, one can’t help doctors choose which opportunities to take advantage of along the way unless there is a sound base of technical knowledge to apply the best skills, tools, and techniques to achieve goals in the first place.

Most of the harms inflicted on consumers by “financial advisors” or “financial planners” occur not due to malice or greed but ignorance; as a result, better consumer protections require not only a fiduciary standard for advice, but a higher standard for competency.

The CFP® practitioner fiduciary should be the minimum standard for financial planning for retail consumers, but there is room for post CFP® studies, certifications and designations; especially those that support real medical niches and deep healthcare specialization like the Certified Medical Planner™ course of study [Michael E. Kitces; MSFS, MTax, CLU, CFP®, personal communication].

Being a financial planner entails Life-Long-Learning [LLL]. One should not be allowed to hold themselves out as an advisor, consultant, or planner unless they are held to a fiduciary standard, period. Corollary – there’s nothing wrong with a suitability standard, but those in sales should be required to hold themselves out as a salesperson, not an advisor.

The real distinction is between advisors and salespeople. And, fiduciary standards can accommodate both fee and commission compensation mechanisms. However; there must be clear standards and a process to which advisors can be held accountable to affirm that a recommendation met the fiduciary obligation despite the compensation involved.

Ultimately, being a fiduciary is about process, not compensation.

As a medical practitioner, Dr. Marcinko is a fiduciary at all times. He earned Series #7 (general securities), Series #63 (uniform securities state law), and Series #65 (investment advisory) licenses from the National Association of Securities Dealers (NASD-FINRA), and the Securities Exchange Commission [SEC] with a life, health, disability, variable annuity, and property-casualty license from the State of Georgia.

Dr.Marcinko was a licensee of the CERTIFIED FINANCIAL PLANNER™ Board of Standards (Denver) for a decade; now reformed, and holds the Certified Medical Planner™ designation (CMP™). He is CEO of iMBA Inc and the Founding President of: http://www.CertifiedMedicalPlanner.org

[Two Newest Books by Marcinko annd the iMBA, Inc Team]

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on September 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

And … How to Prevent It

By Staff Reporter Ashley

We’ve written about medical workplace violence and sexual harassment before on the ME-P and in our handbooks and texts. It is an increasingly important issue around the blog-o-sphere and in the real world.

This harassment in the workplace Infographic explains through images what sexual harassment is and how to prevent sexual harassment from happening at your small business or [medical practice, clinic or healthcare entity].

The authors’ research shows that your business [practice] is more at risk than you think and that you need to act now in proactively protecting that business.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Financial ratio analysis typically involves the calculation of ratios that are financial and operational measures representative of the financial status of a clinic or medical practice enterprise. These ratios are evaluated in terms of their relative comparison to generally established industry norms, which may be expressed as positive or negative trends for that industry sector. The ratios selected may function as several different measures of operating performance or financial condition of the subject entity.

Common types of financial indicators that are measured by ratio analysis include:

Liquidity. Liquidity ratios measure the ability of an organization to meet cash obligations as they become due, i.e., to support operational goals. Ratios above the industry mean generally indicate that the organization is in an advantageous position to better support immediate goals. The current ratio, which quantifies the relationship between assets and liabilities, is an indicator of an organization’s ability to meet short-term obligations. Managers use this measure to determine how quickly assets are converted into cash.

Activity. Activity ratios, also called efficiency ratios, indicate how efficiently the organization utilizes its resources or assets, including cash, accounts receivable, salaries, inventory, property, plant, and equipment. Lower ratios may indicate an inefficient use of those assets.

Leverage.Leverage ratios, measured as the ratio of long-term debt to net fixed assets, are used to illustrate the proportion of funds, or capital, provided by shareholders (owners) and creditors to aid analysts in assessing the appropriateness of an organization’s current level of debt. When this ratio falls equal to or below the industry norm, the organization is typically not considered to be at significant risk.

Profitability. Indicates the overall net effect of managerial efficiency of the enterprise. To determine the profitability of the enterprise for bench marking purposes, the analyst should first review and make adjustments to the owner(s) compensation, if appropriate. Adjustments for the market value of the “replacement cost” of the professional services provided by the owner are particularly important in the valuation of professional medical practices for the purpose of arriving at an ”economic level” of profit.

The selection of financial ratios for analysis and comparison to the organization’s performance requires careful attention to the homogeneity of data. Bench marking of intra-organizational data (i.e., internal bench marking) typically proves to be less variable across several different measurement periods.

However, the use of data from external facilities for comparison may introduce variation in measurement methodology and procedure. In the latter case, use of a standard chart of accounts for the organization or recasting the organization’s data to a standard format can effectively facilitate an appropriate comparison of the organization’s operating performance and financial status data to survey results.

Posted on August 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Customizable Medical Practice Example

[By Staff Reporters]

The undersigned acknowledges that Hamilton Family Clinic (HFC) has furnished to the undersigned potential Investor (“Investor”) certain proprietary data (“Confidential Information”) relating to the business affairs and operations of Hamilton Family Clinic (HFC) for study and evaluation by Investor for possibly investing in Hamilton Family Clinic (HFC).

It is acknowledged by Investor that the information provided by Hamilton Family Clinic (HFC) is confidential; therefore, Investor agrees not to disclose it and not to disclose that any discussions or contracts with Hamilton Family Clinic (HFC) have occurred or are intended, other than as provided for in the following paragraph.

It is acknowledged by Investor that information to be furnished is in all respects confidential in nature, other than information which is in the public domain through other means and that any disclosure or use of same by Investor, except as provided in this agreement, may cause serious harm or damage to Hamilton Family Clinic (HFC), and its owners and officers.

Therefore, Investor agrees that Investor will not use the information furnished for any purpose other than as stated above, and agrees that Investor will not either directly or indirectly by agent, employee, or representative, disclose this information, either in whole or in part, to any third party; provided, however that (a) information furnished may be disclosed only to those directors, officers and employees of Investor and to Investor’s advisors or their representatives who need such information for the purpose of evaluating any possible transaction (it being understood that those directors, officers, employees, advisors and representatives shall be informed by Investor of the confidential nature of such information and shall be directed by Investor to treat such information confidentially), and (b) any disclosure of information may be made to which Hamilton Family Clinic (HFC) consents in writing. At the close of negotiations, Investor will return to Hamilton Family Clinic (HFC) all records, reports, documents, and memoranda furnished and will not make or retain any copy thereof.

No intent to practice law; sample customizable template only. Always consult an attorney or competent consultant familiar with your individual circumstances before use.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

At least 5 people are dead and multiple people are injured following a shooting at the Natalie Building at St. Francis Hospital in Tulsa, Oklahoma.

***

The impact of medical workplace violence became widely exposed on November 6, 2009 when 39 year old Army psychiatrist Maj. Nidal M. Hasan MD, a 1997 graduate of Virginia Tech University who received a medical doctorate in psychiatry from the Uniformed Services University of the Health Sciences in Bethesda, Maryland, and served as an intern, resident and fellow at the Walter Reed Army Medical Center in the District of Columbia, went on a savage 100 round shooting spree and rampage that killed 13 people and injured 32 others. In April 2010 he was transferred to Bell County Jail in Belton, Texas awaiting trial.

Federal Government Guidelines

The federal government and some states have developed guidelines to assist employers with workplace violence prevention. For instance, one of the earliest sets of guidelines for a comprehensive workplace violence prevention program was published in 1993 by California OSHA. This resulted from the murder of a state employee. In 1996, Guidelines for Preventing Workplace Violence for Healthcare and Social Service Workers was published by OSHA.

OSHA Guidelines

In its guidelines, OSHA sets forth the following essential elements for developing a violence prevention program:

Management commitment — as seen by high-level management involvement and support for a written workplace violence prevention policy and its implementation.

Meaningful employee involvement — in policy development, joint management-worker violence prevention committees, post-assault counseling and debriefing, and follow-up are all critical program components.

Worksite analysis — includes regular walk-through surveys of all patient care areas and the collection and review of all reports of worker assault. A successful job hazard analysis must include strategies and policies for encouraging the reporting of all incidents of workplace violence, including verbal threats that do not result in physical injury.

Hazard prevention and control — includes the installation and maintenance of alarm systems in high-risk areas. It may also include the training and posting of security personnel in emergency departments. Adequate staffing is an essential hazard prevention measure, as is adequate lighting and control of access to staff offices and secluded work areas.

Pre-placement and periodic training and education — must include educationally appropriate information regarding the risk factors for violence in the healthcare environment and control measures available to prevent violent incidents. Training should include skills in aggressive behavior identification and management, especially for staff working in the mental health and emergency departments.

On May 17, 1999, Governor Gary Locke signed the New Workplace Violence Prevention Act for the state of Washington. This act mandates that each healthcare setting in the state implement a plan to reasonably prevent and protect employees from violence.

New Washington Workplace Violence Prevention Act

According to this act, prevention plans need to address security considerations related to:

physical attributes of the healthcare setting;

staffing, including security staffing;

personnel policies;

first aid and emergency procedures;

reporting of violent acts; and

employee education and training.

Prior to the development of an actual plan, a security and safety assessment needs to be conducted to identify existing or potential hazards. The training component of the plan must include the following topics:

general safety procedures;

personal safety procedures;

the violence escalation cycle;

violence-predicting factors;

means of obtaining a patient history form from a patient with violent behavior;

strategies to avoid physical harm;

restraining techniques;

appropriate use of medications as chemical restraints;

documenting and reporting incidents;

the process whereby employees affected by a violent act may debrief;

any resources available to employee for coping with violence; and

the healthcare setting’s workplace violence prevention plan.

Assessment

The act further mandates that any hospital operated and maintained by the State of Washington for the care of the mentally ill is required to provide violence prevention training to affected employees identified in the plan on a regular basis and prior.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What is anAccountable Care Organization?

DEFINITION: ACOs are groups of doctors, hospitals, and other health care providers, who come together voluntarily to give coordinated high-quality care to their patients. The goal of coordinated care is to ensure that patients get the right care at the right time, while avoiding unnecessary duplication of services and preventing medical errors. When an ACO succeeds both in delivering high-quality care and spending health care dollars more wisely, the ACO will share in the savings.

Thankfully, Anish Koka is vigilant and explains the blatant obfuscations and manipulations that the central planners engage in to have their way.

***

And so, In this video, Anish and colleague Michel Accad, MD, will reveal the machinations, take the culprits to task, and discuss pertinent questions regarding health care organization:

Does “capitation” reduce costs?

Do employed physicians necessarily utilize fewer resources?

What happens when a HMO and a traditional fee-for-service health system operate side-by-side in a community?

Posted on July 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

Because of the federal government’s preference for, and reliance on the success of, accountable care organizations (ACOs), some ACOs assume their legal status shields the organization from legal scrutiny on all issues.

However, since the 2010 advent of ACOs, the law has adapted uniquely to these organizations. This fourth installment of a five-part series on the valuation of ACOs will discuss this unique regulatory environment in which ACOs operate. (Read more…)

Posted on July 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By NIHCM

***

***

Private equity acquisition of physician practices continues to grow nationwide. New research focused on specialists in dermatology, gastroenterology, and ophthalmology shows the impact of the trend.

Novel evidence by NIHCM grantee Jane Zhu, MD, and her team, reveals shifts in workforce composition and hiring patterns after private equity firms obtain physician practices. The researchers’ findings are particularly important for policymakers and practices considering selling to private equity firms. Highlights include:

A significant yearly increase in the number of advanced practice providers at private equity-acquired practices, specifically nurse practitioners and physician assistants.

In acquired practices, entering clinicians replaced exiting clinicians at a higher rate than at non-private equity-acquired practices.

This work adds to the research team’s previous findings, including the geographic variations in private equity ownership across six medical specialties, and the impact of private equity on health care costs and utilization.

Posted on July 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Significance Often Under Appreciated

By Dr. David Edward Marcinko; MBA, MEd, CMP™

[Publisher-in-Chief]

As some MedicalExecutive-Post readers and subscribers are aware, hospitals that filed bankruptcy a decade ago include: a two-hospital system in Honolulu; one in Pontiac, MI; Trinity Hospital in Erin, Tennessee; Century City Doctors Hospital in Beverly Hills, and four hospital system Hospital Partners of America, in Charlotte. Today,

one can only wonder about the impact of Incurred But Not Reported claims on their plight?

IBNR Definition

According to the www.CertifiedMedicalPlanner.org, an IBNR claim is a concept that signifies healthcare services have been rendered but not invoiced or recorded by the healthcare provider, clinic, hospital, or organization.

Cause and Affect

IBNRs are usually the result of a commercial prospective payment risk contract between managed care organizations and healthcare providers, an IBNR claim refers to the estimated cost of medical services for which a claim has not been filed, or monitored by an IBNR collection systems or control sheet.

IBNR Types

More formally, IBNRs are a financial accounting of all services that have been performed but, as a result of a short period of time or “lag,” have not been invoiced or recorded. The medical services that will not be collected should be accounted for using the following accrued but not recorded (ABNR) entry:

Debit — accrued payments to medical providers or healthcare entity

Credit — IBNR accrual account

Example:

An example of an IBNR is hospital Coronary Artery Bypass Graft [CABG] surgery for a managed care plan member. Out of the capitated or prospective payment funds, the surgeon and/or healthcare organization has to pay for all related physical and respirator therapy, and rehabilitation services, as well as ancillary providers, drugs, and durable medical equipment [DME], as contractually obligated. This may also include complication diagnosis and extensive follow-up treatment.

Accordingly, the health plan will not be completely billed until several weeks, months, or quarters later or even further downstream in the reporting year after the patient is discharged. In order to accurately project the health plan’s financial liability, however, the health plan and hospital must estimate the cost of care based on past expenses.

Accounting Cost Controls

Since the identification and control of costs are paramount in financial healthcare management, an IBNR reserve fund (an interest bearing account) must be set up for claims that reflect services already delivered but, for whatever reason, not yet reimbursed.

From the accounting perspective, IBNR is accrued as an expense and is related as a short-term liability each fiscal month or accounting period.

Otherwise, the organization may not be able to pay the claim, if the associated revenue has already been spent. The proper handling of these “bills in the pipeline” is crucial for proactive providers and health organizations that are exploring arrangements that put them in the role of adjudicating claims or operating in a sub-capitated system.

###

###

Assessment

IBNRs are especially important with newer patients who may be sicker than prior norms.

Recoverables that hospitals post as part of their large reserve charges are also, in many cases, IBNR losses. They may be recorded as IBNR claims on their balance sheets. Once these losses start becoming actual losses, the hospital may look to the insurer to pay a part of the claim. This causes disputes between the payor, provider, and/or healthcare organization.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

There are a myriad of reasons for obtaining a Fair Market Value [FMV], Venture Capital [VC} and/or Investment Banking [IB] funding appraisal engagement:

Outright Selling-Buying

Partnership and Associate buy-in / buy-out

Mergers and Acquisitions

Organic growth tracking

Hospital integrations

Private and public reporting

Financing and Venture Capital

Estate and Tax Planning

And, there are many cautions, too. On July 19, 2023, the Federal Trade Commission (FTC) and the Department of Justice (DOJ) released a draft update of its Merger Guidelines, which guides the regulatory agencies in their review of both mergers and acquisitions in evaluating compliance with federal antitrust laws.

The new Guidelines replace, amend, and consolidate the Vertical Merger Guidelines and Horizontal Merger Guidelines, which were published in 2020 and 2010, respectively.

Vicki Rackner MD, author, speaker, ME-P thought-leader and President of Targeting Doctors, helps financial advisors accelerate their practice growth by acquiring more physician clients. She calls on her experience as a practicing surgeon, clinical faculty at the University of Washington School of Medicine and nationally-noted expert in physician engagement to offer a bridge between the world of medicine and the world of business.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

It has been argued that physicians have abdicated the “moral high ground” in health care by their interest in seeking protection for their high incomes, their highly publicized self-referral arrangements, and their historical opposition toward reform efforts that jeopardized their clinical autonomy.

Experts Speak

In his book Medicine at the Crossroads, colleague and Emory University professor Melvin Konnor, MD noted that “throughout its history, organized medicine has represented, first and foremost, the pecuniary interests of doctors.” He lays significant blame for the present problems in health care at the doorstep of both insurers and doctors, stating that “the system’s ills are pervasive and all its participants are responsible.”

In order to reclaim their once esteemed moral position, physicians must actively reaffirm their commitment to the highest standards of the medical profession and call on other participants in the health care delivery system also to elevate their values and standards to the highest level.

Evolution

In the evolutionary shifts in models for care, physicians have been asked to embrace business values of efficiency and cost effectiveness, sometimes at the expense of their professional judgment and personal values. While some of these changes have been inevitable as our society sought to rein in out-of-control costs, it is not unreasonable for physicians to call on payers, regulators and other parties to the health care delivery system to raise their ethical bar.

Harvard University physician-ethicist Linda Emmanuel noted that “health professionals are now accountable to business values (such as efficiency and cost effectiveness), so business persons should be accountable to professional values including kindness and compassion.”

Within the framework of ethical principles, John La Puma, M.D., wrote in Managed Care Ethics, that “business’s ethical obligations are integrity and honesty. Medicine’s are those plus altruism, beneficence, non-maleficence, respect, and fairness.”

Incumbent in these activities is the expectation that the forces that control our health care delivery system, the payers, the regulators, and the providers will reach out to the larger community, working to eliminate the inequities that have left so many Americans with limited access to even basic health care.

Charles Dougherty clarified this obligation in Back to Reform, when he noted that “behind the daunting social reality stands a simple moral value that motivates the entire enterprise”.

ASSESSMENT

Health care is indeed grounded in caring. And, managing risk is a component of caring. It arises from a sympathetic response to the suffering of others.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

“Collectively the healthcare industry spends over $350 Billion to submit and process claims while still working with cumbersome workflows, inefficient processes, and a changing landscape marked by increasing out-of-pocket cost for patients as well as increasing operating costs.”

The Norm Continues Downhill

For many years hospitals and healthcare organizations have struggled to maintain and improve their operating margins. They continue to face a widening gap between their operating costs and the revenues required to cover not only current costs, but also to finance strategic growth initiatives and investments.

Faced with increased operational costs and associated declines in rates of reimbursement, many healthcare hospital executives and leaders are concerned that they will not achieve margin targets. To stabilize the internal financial issue, some hospital have focused on lowering expenses in order to save costs – an area they control and an area that will show an immediate impact; however, that is not the best solution.

Beware Cost Reductions

Hospital executives are concerned with the effect that these reductions may have on patient quality and service. Finding ways to maximize workflow to lower operating costs is vital. Every dollar not collected negatively impacts short- and long term capital projects, lowers patient satisfaction scores and possibly affects quality of patient care.

Status Today

Hospitals, healthcare organizations and all medical providers are under great pressure to collect revenue in order to remain solvent. And so, here are some of the issues impacting the modern hospital revenue cycle as Obama-Care, or the PP-ACA of 2010, as launched last decade?

Issues Impacting the Revenue Cycle

Several of the major leading issues facing the revenue cycle are:

Impact of Consumer-driven Health – This process has emerged as a new approach to the traditional managed care system, shifting payment flows and introducing new “non-traditional” parties into the claims processing workflow. As market adoption enters the mainstream, consumer-driven health stands to alter the healthcare landscape more dramatically than anything we have seen since the advent of managed care. This process places more financial responsibility on the consumer to encourage value-drive healthcare spending decisions.

Competing high-priority projects –Hospitals are feeling pressured to maximize collections primarily because they know changes are coming down the pike due to healthcare reform and they know they will need to juggle these major initiatives along with the day-to-day revenue cycle operations.

Lack of skilled resources in several areas – Hospital have struggled to find the right personnel with sufficient knowledge of project management, clinical documentation improvement, coding and other revenue cycle functions, resulting in inefficient operations.

Narrowing margins – Declines in reimbursement are forcing hospitals to look at their organization to determine if they can increase efficiencies and automate to save money. Hospitals are faced with the potential of increased cost to upgrade and adapt clinical software while not meeting budget projections. There are a number of factors contributing to the financial pressure including inefficient administrative processes such as redundant data collection, manual processes, and repetitive rework of claims submissions. Also included are organizations using outdated processes and legacy technologies.

Significant market changes – Regardless of what happens with the Patient Protection and Affordable Care Act, hospitals will have to deal with fluctuating amounts of insured and uninsured patients and variable payments.

Limited access to capital – With the trend towards more complex and expensive systems, industry may not have the internal resources and funding to build and manage these systems that keep pace with the trends.

Need to optimize revenue – There are five core areas hospitals have to examine carefully and they are:

ICD-10 – This is an entirely new coding and health information technology issue but is also a revenue issues

System integration – Hospitals need to look at integrating software and hardware systems that can combine patient account billing, collections and electronic health records.

Clinical documentation – Meaningful use will require detailed documentation in order for payment to be made and this is another revenue issue.

Billing and claims management – Reducing denials and reject claims, training staff, improving point-of-service collections and decreasing delays in patient billing can improve the revenue cycle productivity,

Contract analysis– Hospitals need to focus more on negotiating rates with insurers in order to increase revenue.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

When You May Need a Business, Management or Financial Second Opinion?

The Marcinko & Associates second opinion service is a physician-to-advisor telephone or e-mail portal that connects independent financial and business management professionals and consultants, with doctors or healthcare executives desiring affordable and unbiased financial or business advice on an as-needed, pay-per-use basis.

Medical professionals and healthcare executives can now receive direct access to us in the areas of Practice Enhancement, Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Practice Management, Information Technology, Human Resources and Employee Benefits.

This Marcinko & Associates service is designed to fill a growing need for medically focused financial or managerial advice that traditional consultants have not been able to serve. For example, situations in which you could benefit from a personal financial planning second opinion include:

Approximately 250 hospitals across the U.S. are completely or partially physician owned. These physician-owned hospitals (POHs) can offer a variety of services, from general care to specialty services, such as cardiovascular or orthopedic care, known as “focused factories.”

Over the past several decades, healthcare providers and policymakers have claimed that POHs have a negative impact on the healthcare industry, suggesting that: (1) POHs “cherry-pick” the most profitable patients; (2) the quality of care provided at POHs is substandard; and, (3) conflicts of interest exist due to the financial incentive for physician owners to refer patients to their POHs. (Read more…)

Posted on June 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On April 10th, 2024, the Centers for Medicare & Medicaid Services (CMS) released its proposed rules for the payment and policy updates for the Medicare inpatient prospective payment system (IPPS) and long-term care hospital prospective payment system (LTCH PPS) for fiscal year (FY) 2025.

Posted on May 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS THE “MEDICARE COST CONTROL EFFICIENCY” PARADOX?

The 800 Pound Gorilla in the Medical Treatment Room

By Staff Reporters

Blogger Ezra Klein opined more than a decade ago that one of the dirty little secrets of the health-care system is that Medicare has done a much better job controlling costs than private health insurers. It is a paradox!

DEFINITION: A paradox is a seemingly absurd or self-contradictory statement or proposition that when investigated may prove to be well founded or true.

***

***

QUERY:But, what about Medicare, cost control efficiency, today?

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world. All in a Corona safe environment.

MARCINKO in the METAVERSE

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, end-note lectures at city and statewide financial coalitions, and annual lectures for a variety of internal yearly meetings.

Posted on May 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A Non-Traditional Accounting System

[By Dr. David Marcinko MBA MEd CMP]

Sooner or later you will want to ascertain and then demonstrate the cost effectiveness of your medical care. By using the process of Activity Based Cost (ABC) management, you will be able to do so. But, if you’re using a traditional accounting system, you won’t know a thing about your activity costs. Here’s how.

Traditional Cost Accounting Methods

In a traditional medical practice cost accounting system, costs are assigned to different procedures and services based on volume. In others words, office costs are spread over the entire office’s product line and you may not know the true profitability of any single medical activity. So, if the office is doing more “procedures” than general medicine, for example, more indirect office overhead costs will be allocated to the procedural portion of the practice.

ABC management, on the other hand, determines the actual costs of the resources that each service consumes. Because general medicine requires more human resources than “technical procedures,” ABC management will assign more costs to the general medical portion of the practice.

Accordingly, most physicians, office managers, and their accountants are surprised that a prior notion of office profitability is different than previously thought. ABC management is just more accurate in measuring medical service profitability than traditional accounting methods.

Medical Activity Cost Drivers

Examples of medical activities that are office cost drivers include such items as monitoring vital signs, taking radiographic images, removing dressings or casts, performing laboratory tests or veni-punctures, surgical set-ups or operative procedures; etc.

However, in the office setting, the most economically important activities are listed as specific CPT codes for each medical specialty. The most important end result of ABC management is the shift of general overhead costs to low volume services from high volume services. These effects are not symmetrical as there is a bigger dollar effect on the per-unit costs of the low volume service.

ABC Managerial Accounting Improvements

ABC management improves office managerial cost accounting systems in three ways:

It increases the number of cost pools used to accumulate general overhead office costs. Rather than accumulate overhead costs in a single office-wide pool, costs are accumulated by activity, service or procedure.

It changes the base used to assign general overhead costs to services or patients. Rather than assigning costs on the basis of a measure of volume (employee or doctor hours), costs are assigned on the basis of medical services or activities that generated those costs.

It changes the nature of many overhead costs in that those formerly considered indirect, are now traced to specific activities or services. The office service mix may then be adjusted accordingly, for additional profit.

Methodology

In order to perform an ABC analysis for your medical office, calculate the cost of delivering a single unit of medical or surgical activity using only the work component of the resource based relative value scale (RBRVS).

Do this by adding up your office’s average variable expenses for the prior 1-3 years. Now, count the number of work resource based relative value units (RBRVUs) delivered for each CPT code for the same time period, using the latest edition of the Federal Register to obtain the latest list of RVUs by CPT code. Then divide total variable expenses by the total number of work RVUs in order to arrive at the marginal cost of a single unit of service for the time period being evaluated.

For example, if your office had variable expenses of $480,000, and produced 80,000 work RVUs last year, it cost $6, on top of the office’s fixed expenses, to deliver one unit of work product. So, if an HMO plan offers to reimburse you at a rate of $11 per member, per month, and you can expect to reasonably deliver on average of one RVU pm/pm, you’ll earn enough on the contract to cover your marginal costs and some of your fixed and direct expenses.

Remember, this method assumes that you have the excess operating capacity and time slots, available and unused, to see the additional patients of the new plan without adding extra overhead expenses to service the contract.

If not, or if you plan for capitation to become a major portion of your practice, you might want the capitated contract(s) to cover all your office expenses, so be sure to include both the fixed and other direct costs to your variable cost calculations. ABC determines the actual costs of resources rendered for each activity and represents a real measure of practice profitability. Office service mix can then be changed to either maximize revenues or better suit your practice personality.

A Caveat

Suppose however, that a medical service is competitively priced but still shows that the CPT code is unprofitable. For example, the costs of special requests can adversely affect office profits. Yet, special patient requests are one of the biggest reasons that a CPT code or procedure isn’t profitable.

In this case, look closely at activity costs and determine which ones are being performed inefficiently. Improving the efficiency of those kinds of medical services, or referring them out or abandoning them all together, will increase office profitability.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

It goes without saying that it takes a special kind of person to become a doctor, and an entrepreneur.

Driven, motivated, innovative – these are just a few of the many ways to describe individuals who risk everything to transform their vision into reality; or to save lives.

We created this infographic to celebrate the entrepreneur, not only for their individual, quirky styles, but also for their contributions to the global economy.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

****

BY DR. ERIC BRICKER MD

***

Value-Based Care Happened 40 Years

Why Was Medicare Able to Bring About So Much Value-Based Payment Change in 3 Years (’83-’86) Compared to the Relatively Little Change That Has Occurred in the 11 Years Since the Affordable Care Act?

Posted on May 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

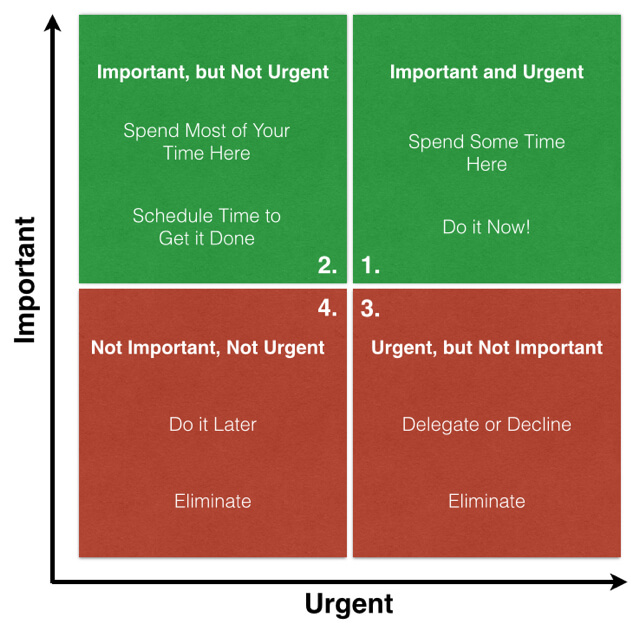

What is the Eisenhower Matrix?

[By staff reporters]

The Eisenhower Matrix is a business management and strategic planning productivity tool that helps to sort tasks and spread them reasonably over time.

The sort out is based on the principals of urgency and importance. When assigned to each task, those two factors place the task to the relevant quadrant of the matrix.

After this routine is done, it’s enough to take a look at the matrix to visually estimate what you should start with.

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Today’s electronic media makes physician-patient communication possible; yet there is another kind of intimacy. ICTs—information and communication technologies—enable 24/7 monitoring of basic information such as blood pressure, glucose levels, pulse, and respiration, etc.

Example:

In one study, an ICT not only made it easier for patients to stay in touch with their doctors, the outcomes were also significantly better.[i] Today, Hippocrates is no longer trailing patients around the house to keep track of their snacks and moods. But Hippocrates has gone digital in the form of a wearable device that records subtle changes in biological markers and communicates them instantaneously to a health provider.

While this is obviously a great advance, we suggest you pause for a moment before plugging in.

Why?

ICTs and social media tools can make a difference to one of the most important dimensions—physiological outcomes. But you can have the latest interactive technology at your disposal and still fail to be connected.

Example:

A story that a friend told me shows how.

***

One morning, her elderly father was touching up the paint on his sailboat. Nearby, another boat-owner, who happened to be an emergency medical technician, noticed her father was struggling to breathe and that his lips had turned purple. A trip to the local community hospital led to a barrage of high-tech tests and procedures, a diagnosis of emphysema, later complications with cerebral hematomas, and hospitalizations and re-hospitalizations that brought him into contact with a neurologist, a neurosurgeon, a cardiologist, and a pulmonologist.

Throughout her father’s medical ordeal, the team of specialists stayed in touch with each other and the primary care physician via various electronic media. But one person remained out of the loop—her father. One day, six months into the experience, the primary care physician phoned our friend’s mother to check on his patient. Her father recalls thinking, “Why was he calling her?”

The physician was communicating, but he was emotionally disconnected.

***

The Moral

The moral of the story: communication needs to be patient-centered in both electronic and psychological terms. That means understanding how someone likes to communicate and making sure the medium fits the message. Electronic media are just part of the equation. The other is the doctor-patient relationship. Once a relationship is established, it may be fine to use e-mail to send information about dosage.

But, delivering a new diagnosis may require the extra effort of scheduling a phone call or a face-to-face visit. Today, since you have so many Health 2.0 choices, it takes some effort to select the right way to communicate in a particular situation.

Use the Right Relationship Strategy

A colleague recently shared another story about an encounter with a specialist.

Example:

***

After an examination for a minor ailment, he was told that there might be a medicated lotion that could ameliorate his condition. The doctor thought for a moment, then swiveled around to the computer on his desk. As our colleague watched the screen, his physician typed a few words into a search engine. Up popped a list and he wrote out a script. “Try this,” his doctor concluded. “I think it will help.”

It did, almost overnight.

***

The Moral

Even though his physical problem had disappeared completely, our colleague felt there was something missing in the interaction. “It bothered me that my doctor turned to the Web for help at that moment. He found a cure, but I felt he wasn’t paying attention to me.”

The physician is supposed to be an authority who has a special relationship to the patient. “Anybody can Google,” our colleague complained. Was he being unreasonable? Maybe.

But; this story tells us something important about technology—it cuts both ways.

***

***

Assessment

Everyone has their own preferences when it comes to how they want to interact with each other and with technology. If these preferences are explicit and aligned, the chances for a productive partnership are high. The preferences, however, are many and complex. You can easily get lost in the tangled thicket of interpersonal styles and virtual mediums.

In the Web 2.0 environment, it helps to narrow down the endless choices to just a few options.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Financial benchmarking can assist healthcare managers and professional financial advisors in understanding the operational and financial status of their organization or practice.

The general process of financial benchmarking analysis may include three elements: (1) Historical subject benchmarking; (2) Benchmarking to industry norms; and, (3) Financial ratio analysis.

History

Historical subject benchmarking compares a healthcare organization’s most recent performance with its reported performance in the past in order to: examine performance over time; identify changes in performance within the organization (e.g., extraordinary and non-recurring events); and, to predict future performance.

As a form of internal benchmarking, historical subject benchmarking avoids issues such as: differences in data collection and use of measurement tools; and, benchmarking metrics that often cause problems in comparing two different organizations.

However, it is necessary to common size data in order to account for company differences over time that may skew results.

Benchmarking

Benchmarking to industry norms, analogous to Fong and colleagues’ concept of industry benchmarking, involves comparing internal company-specific data to survey data from other organizations within the same industry. This method of benchmarking provides the basis for comparing the subject entity to similar entities, with the purpose of identifying its relative strengths, weaknesses, and related measures of risk.

***

***

Financial Ratio Analysis

The process of benchmarking against industry averages or norms will typically involve the following steps:

Identification and selection of appropriate surveys to use as a benchmark, i.e., to compare with data from the organization of interest. This involves answering the question, “In which survey would this organization most likely be included?”;

If appropriate, re-categorization and adjustment of the organization’s revenue and expense accounts to optimize data compatibility with the selected survey’s structure and definitions (e.g., common sizing); and,

Calculation and articulation of observed differences of organization from the industry averages and norms, expressed either in terms of variance in ratio, dollar unit amounts, or percentages of variation.

Trends

Financial ratio analysis typically involves the calculation of ratios that are financial and operational measures representative of the financial status of an enterprise. These ratios are evaluated in terms of their relative comparison to generally established industry norms, which may be expressed as positive or negative trends for that industry sector. The ratios selected may function as several different measures of operating performance or financial condition of the subject entity.

The Selected Ratios

Common types of financial indicators that are measured by ratio analysis include:

Liquidity. Liquidity ratios measure the ability of an organization to meet cash obligations as they become due, i.e., to support operational goals. Ratios above the industry mean generally indicate that the organization is in an advantageous position to better support immediate goals. The current ratio, which quantifies the relationship between assets and liabilities, is an indicator of an organization’s ability to meet short-term obligations. Managers use this measure to determine how quickly assets are converted into cash.

Activity. Activity ratios, also called efficiency ratios, indicate how efficiently the organization utilizes its resources or assets, including cash, accounts receivable, salaries, inventory, property, plant, and equipment. Lower ratios may indicate an inefficient use of those assets.

Leverage.Leverage ratios, measured as the ratio of long-term debt to net fixed assets, are used to illustrate the proportion of funds, or capital, provided by shareholders (owners) and creditors to aid analysts in assessing the appropriateness of an organization’s current level of debt. When this ratio falls equal to or below the industry norm, the organization is typically not considered to be at significant risk.

Profitability. Indicates the overall net effect of managerial efficiency of the enterprise. To determine the profitability of the enterprise for benchmarking purposes, the analyst should first review and make adjustments to the owner(s) compensation, if appropriate. Adjustments for the market value of the “replacement cost” of the professional services provided by the owner are particularly important in the valuation of professional medical practices for the purpose of arriving at an ”economic level” of profit.

Data Homogeneity

The selection of financial ratios for analysis and comparison to the organization’s performance requires careful attention to the homogeneity of data. Benchmarking of intra-organizational data (i.e., internal benchmarking) typically proves to be less variable across several different measurement periods.

However, the use of data from external facilities for comparison may introduce variation in measurement methodology and procedure. In the latter case, use of a standard chart of accounts for the organization or recasting the organization’s data to a standard format can effectively facilitate an appropriate comparison of the organization’s operating performance and financial status data to survey results.

Operational benchmarking is used to target non-central work or business processes for improvement. It is conceptually similar to both process and performance benchmarking, but is generally classified by the application of the results, as opposed to what is being compared. Operational benchmarking studies tend to be smaller in scope than other types of benchmarking, but, like many other types of benchmarking, are limited by the degree to which the definitions and performance measures used by comparing entities differ. Common sizing is a technique used to reduce the variations in measures caused by differences (e.g., definition issues) between the organizations or processes being compared.

Common Sizing

Common sizing is a technique used to alter financial operating data prior to certain types of benchmarking analysis and may be useful for any type of benchmarking that requires the comparison of entities that differ on some level (e.g., scope of respective benchmarking measurements, definitions, business processes). This is done by expressing the data for differing entities in relative (i.e., comparable) terms.

Example:

For example, common sizing is often used to compare financial statements of the same company over different periods of time (e.g., historical subject benchmarking), or of several companies of differing sizes (e.g., benchmarking to industry norms). The latter type may be used for benchmarking an organization to another in its industry, to industry averages, or to the best performing agency in its industry. Some examples of common size measures utilized in healthcare include:

Percent of revenue or per unit produced, e.g., relative value unit (RVU);

Per provider, e.g., physician;

Per capacity measurement, e.g., per square foot; or,

Other standard units of comparison.

Assessment

As with any data, differences in how data is collected, stored, and analyzed over time or between different organizations may complicate the use of it at a later time. Accordingly, appropriate adjustments must be made to account for such differences and provide an accurate and reliable dataset for benchmarking.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By National Council on Disability

The origins of managed care can be traced back to at least 1929, when Michael Shadid, a physician in Elk City, Oklahoma, established a health cooperative for farmers in a small community without medical specialists or a nearby general hospital. He sold shares to raise money to establish a local hospital and created an annual fee schedule to cover the costs of providing care. By 1934, 600 family memberships were supporting a staff that included Dr. Shadid, four newly recruited specialists, and a dentist. That same year, two Los Angeles physicians, Donald Ross and Clifford Loos, entered into a prepaid contract to provide comprehensive health services to 2,000 employees of a local water company

Development of Prepaid Health Plans

Other major prepaid group practice plans were initiated between 1930 and 1960, including the Group Health Association in Washington, DC, in 1937, the Kaiser-Permanente Medical Program in 1942, the Health Cooperative of Puget Sound in Seattle in 1947, the Health Insurance Plan of Greater New York in New York City in 1947, and the Group Health Plan of Minneapolis in 1957. These plans encountered strong opposition from the medical establishment, but they also attracted a large number of enrollees.

Today, such prepaid health plans are commonly referred to as health maintenance organizations (HMOs). The term “health maintenance organization,” however, was not coined until 1970, with the aim of highlighting the importance that prepaid health plans assign to health promotion and prevention of illness. HMOs are what most Americans think of when the term “managed care” is used, even though other managed care models have emerged over the past 40 years.

Public Managed Care Plans

The enactment of the Health Maintenance Organization Act of 1973 (P. L. 93-222) provided a major impetus to the expansion of managed health care. The legislation was proposed by the Nixon Administration in an attempt to restrain the growth of health care costs and also to preempt efforts by congressional Democrats to enact a universal health care plan. P. L. 93-222 authorized $375 million to assist in establishing and expanding HMOs, overrode state laws restricting the establishment of prepaid health plans, and required employers with 25 or more employees to offer an HMO option if they furnished health insurance coverage to their workers. The purpose of the legislation was to stimulate greater competition within health care markets by developing outpatient alternatives to expensive hospital-based treatment. Passage of this legislation also marked an important turning point in the U.S. health care industry because it introduced the concept of for-profit health care corporations to an industry long dominated by a not-for-profit business model.

In the decade following the passage of P. L. 93-222, enrollment in HMOs grew slowly. Stiff opposition from the medical profession led to the imposition of regulatory restrictions on HMO operations. But the continued, rapid growth in health care outlays forced government officials to look for new solutions. National health expenditures grew as a proportion of the overall gross national product (GNP) from 5.3 percent in 1960 to 9.5 percent in 1980. In response, Congress in 1972 authorized Medicare payments to free-standing ambulatory care clinics providing kidney dialysis to beneficiaries with end-stage renal disease. Over the following decade, the Federal Government authorized payments for more than 2,400 Medicare procedures performed on an outpatient basis.

Responding to the relaxed regulatory environment, physicians began to form group practices and open outpatient centers specializing in diagnostic imaging, wellness and fitness, rehabilitation, surgery, birthing, and other services previously provided exclusively in hospital settings. As a result, the number of outpatient clinics skyrocketed from 200 in 1983 to more than 1,500 in 1991, and the percentage of surgeries performed in hospitals was halved between 1980 (83.7%) and 1992.

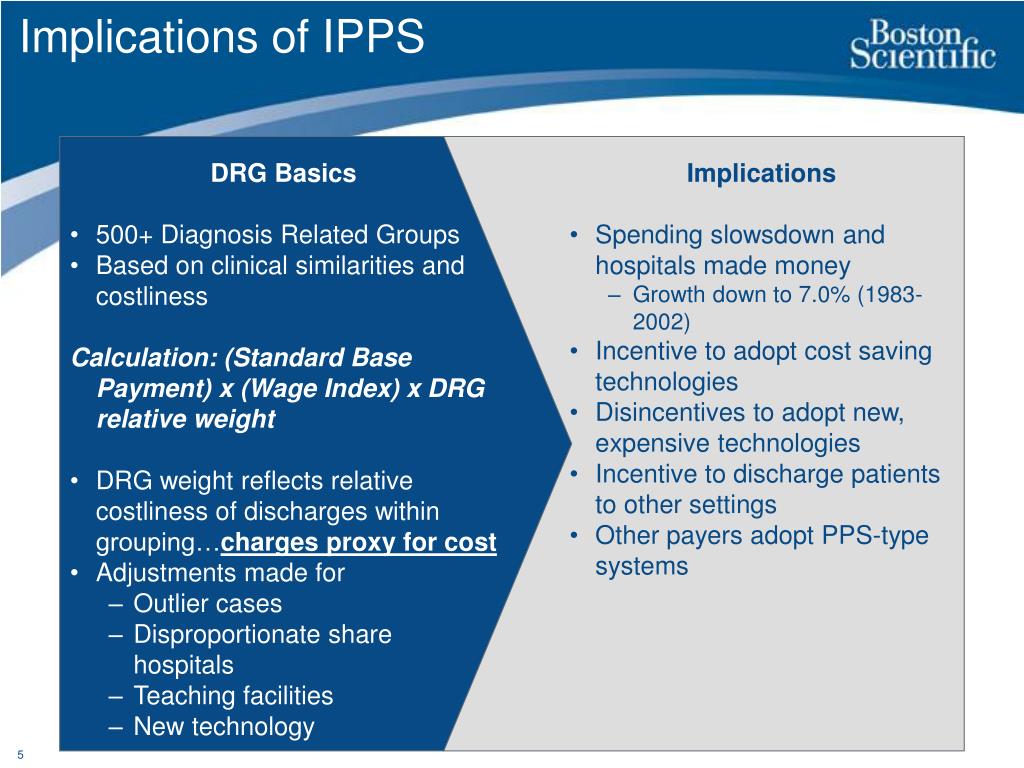

The Influence of Medicare Prospective Payments

Health care costs, however, continued to spiral upward, consuming 10.8 percent of GNP by 1983. In an attempt to slow the growth rate, Congress in 1982 capped hospital reimbursement rates under the Medicare program and directed the secretary of HHS to develop a case mix methodology for reimbursing hospitals based on diagnosis-related groups (DRGs). As an incentive to the hospital industry, the legislation (the Tax Equity and Fiscal Responsibility Act (P. L. 97-248)) included a provision allowing hospitals to avoid a Medicare spending cap by reaching an agreement with HHS on implementing a prospective payment system (PPS) to replace the existing FFS system. Following months of intense negotiations involving federal officials and representatives of the hospital industry, the Reagan Administration unveiled a Medicare PPS. Under the new system, health conditions were divided into 468 DRGs, with a fixed hospital payment rate assigned to each group.

Once the DRG system was fully phased in, Medicare payments to hospitals stabilized. However, since DRGs applied to inpatient hospital services only, many hospitals, like many group medical practices, began to expand their outpatient services in order to offset revenues lost as a result of shorter hospital stays. Between 1983 and 1991, the percentage of hospitals with outpatient care departments grew from 50 percent to 87 percent. Hospital revenues derived from outpatient services doubled over the period, reaching 25 percent of all revenues by 1992

Since DRGs were applied exclusively to Medicare payments, hospitals began to shift unreimbursed costs to private health insurance plans. As a result, average per employee health plan premiums doubled between 1984 and 1991, rising from $1,645 to $3,605. With health insurance costs eroding profits, many employers took aggressive steps to control health care expenditures. Plan benefits were reduced. Employees were required to pay a larger share of health insurance premiums. More and more employers—especially large corporations—decided to pay employee health costs directly rather than purchase health insurance. And a steadily increasing number of large and small businesses turned to managed health care plans in an attempt to rein in spiraling health care outlays.

Managed Long-Term Services and Supports

Arizona became the first state to apply managed care principles to the delivery and financing of Medicaid-funded LTSS in 1987, when the federal Health Care Financing Administration (later renamed the Centers for Medicare and Medicaid Services) approved the state’s request to expand its existing Medicaid managed care program. Medicaid recipients with physical and developmental disabilities became eligible to participate in the Arizona Long-Term Care System as a result of this program expansion. Over the following two decades, a number of other states joined Arizona in providing managed LTSS, and by the summer of 2012, 16 states were operating Medicaid managed LTSS programs

Growth of Commercial Managed Care Plans