BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Many financial planning websites mention fees, as required, but still remain opaque to potential clients because the advisor wants to control the discussion and understandably wishes to avoid the website shopper phenomenon.

But, physicians and all investors can still control the discussion, and still provide transparency, because posting up front pricing information doesn’t mean presenting information in a vacuum!

For example, a 1%/year fee doesn’t have to just be 1%; it can be 1%, compared to an industry average cost of X%, where the average cost of an actively managed mutual fund is Y%.

***

***

Similarly, it doesn’t have to be a retainer fee of $1,000/year; it can be a retainer fee for less than the cost of a monthly cable bill! And, a financial plan doesn’t cost $1,500; it costs 8-12 hours of staff time to craft extensive, customized solutions; but saves the doctor-client so much more!

And, if services have a range of potential prices, they might be provided with some insight into the factors that impact the price. Modern young and internet savvy doctors expect this sort of information.

Posted on April 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: The Office of the National Coordinator for Health Information Technology (ONC) is a staff division of the Office of the Secretary, within the U.S. Department of Health and Human Services. ONC leads national health IT efforts, charged as the principal federal entity to coordinate nationwide efforts to implement and use the most advanced health information technology [HIT] and the electronic exchange of health information.

Posted on April 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Medial Office Equipment Interest Rate Costs

Dr. David E. Marcinko; MBA, MEd, CMP™

[Publisher in Chief]

Physicians, administrators and healthcare entrepreneurs are aware of the compounding effect of interest.However, since interest is deductible as a medical office business expense, many seem to forget about it despite the fact that it must be continually paid until the asset is either purchased or otherwise disposed.

So, what are the various types of interest rates important to the medical practitioner and commodity – money?

[1] Simple Interest

Simple interest is merely the pro rata interest on a loan or deposit and represents the most basic interest rate type.

For example, for every $100 Dr. Bill borrows at 12 percent annual interest, he pays twelve dollars per year. The interest is calculated by multiplying the principal or original amount, by the interest rate in decimal form (100 x .12).

[2] Add-On Interest

Add on interest immediately attaches the annual interest amount, to the principal amount, at the beginning of the payment period. Payments are then made according to the number of years required.

The following formula is useful:

Add-on-Interest minus Payment = Total Interest on Balance/Number of Payments

For example, if Dr. William Needy borrows $10,000 at 8 percent add-on interest, he will repay $10,000 plus $ 800 ($10,000 x 8%) or $10,800, divided by twelve months, for a total of $900 per month, since $ 900/month x 12 months equals $10,800.

[3] Discounted Interest

When using the discounted interest method, the interest amount is deducted from the principal right up front. Notice that this is the opposite of add-on-interest that is applied up front.

For example, if Dr. Bill borrows the same $ 10,000 at a discounted interest rate of 8 percent, he will only receive a $9,200 loan, since $10,000 – $800 is $9,200.

Obviously, the discount method is the most expense way to borrow money.

[4] Annual Percentage Rate

Most financial institutions advertise an annual percentage rates (APR) for loans, deposits and investments. The APR is the periodic interest rate multiplied by the number of periods a year. If the APR is 12 percent, and interest is compounded monthly, you receive (or pay) 1 percent of your balance each month, and the balance shifts with each compounding.

For example, if Dr. Bill deposits $ 100 dollars at 12 percent APR compounded monthly, he receives $ 1 interest the first month (1% of $100), $1.10 the second month (1% of $101), and so forth. If compounding is daily, the interest accumulates at the rate of 1/365 of the APR each day.

Unless interest is compounded annually, the APR will be lower than the effective annual interest rate, discussed below.

[5] Effective Interest Rate

It is important to differentiate between the effective interest rate and the APR, which is often the most prominent figure in advertisements for medical business equipment, consumer goods and financial services (loans, annuities, IRAs, CDs, investment analysis, college funding or retirement planning). Although the APR is the periodic interest rate multiplied by the number of periods per year, the effective annual interest rate is the periodic rate, compounded.

In our case, if the APR is 12 percent, compounded monthly, the monthly interest rate is 1 percent and the effective annual rate is the monthly rate compounded for 12 periods.

Therefore, if your calculation is for a single year, you can treat the effective rate as simple interest. If you deposit (or borrow) $1,000 at 12 percent APR, the effective rate is 12.68 percent, and interest for the first year is about $126.80 (12.68% of $1,000).

For longer periods, you can use the effective interest rate as the periodic interest rate, compounded annually.

[a] “Rule of 72” (Double your Money)

The number of periods required to double a lump sum of money can be quickly estimated by using what is known as the “Rule of 72”. To get the number of periods, usually years, just divide 72 by the periodic interest rate, expressed as a whole number (not a decimal).

For example, if the annual interest rate is 10 percent, it will take about 7.2 years (72/10) to double any lump cache of money. Conversely, you can also calculate the interest rate required to double your money in a given period by dividing 72 by the term.

Thus, to double your money in ten years, you need to earn about 7.2 percent annual interest (72/10) = 7.2%).

[b] “Rule of 78”

According to this method, interest is front end loaded like a home mortgage, or office condominium, to discourage prepayment of a loan and consequently preserve the lender’s profit. In other words, it is a method of calculating installment loan interest rebates.

The number 78 comes from an approved method of accelerated tax depreciation, known as the “Sum of the Years Digits” (SOYD) method (i.e., 12 + 11 + 10 + 9 . . . = 78). This fact is important because, throughout the period of a loan, even though the payments are all the same, the portions that are interest and principal are very different.

Using this method for a one year loan shows that, in the first payment, 15.38 percent of the interest due is paid off, and by the sixth month, 73.08 percent of the interest is paid off. This means, that if a physician makes a one year equipment loan with a total interest charge of $ 100 and pays the loan off in full with the sixth payments, he or she will not get an interest rebate of $ 50, but only $ 26.92, since $ 73.08 of the interest has already been prepaid.

Most ethical lenders use simple interest rates for loan rebates, and the Rule of 78 is unfair according to many authorities.

[c] “Rule of 116”

A derivative of the Rule of 72 is the Rule of 116. This determines the number of years it takes for a principal amount to be tripled and is calculated by dividing the annual interest rate into 116.

The Rules of 72 and 78 are very handy for figuring the amount of interest payments made or growth of funds invested. They can also be used in reverse to calculate at what rate of interest money must be invested to double or triple in a certain number of years.

[6] Medical Equipment Payback Cost Analysis

The payback period, expressed in years, is the length of time that it takes for the medical equipment investment to recoup its initial cost out of the cash receipts it generates. The basic premise is that the quicker the cost of an investment can be recovered, the better the investment is. It is most often used when considering equipment whose useful life is short and unpredictable.

When the same cash flow occurs every year, the formula is as follows:

Investment Required / Net Annual Cash Inflow = Payback Period

Thus, in today’s tightening medical reimbursement atmosphere, practice cost control and expense reduction is the easiest method to increase medical office profitability. Keeping the cost of the commodity money in the form of interest rate charges, as low as possible, will assist in this endeavor

Assessment

And so, how have these rules affected your medical office borrowing costs; if at all? Does these principles apply to the medical student loan crisis, today?

Posted on April 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Essay on the Eight-Hundred Pound Gorilla in the Medical Treatment Room

By Dr. David E. Marcinko MBA MEd CMP

[Editor-in-Chief]

According to economist Austin Frakt PhD, and others, there is a school of thought that says Congress is incapable of controlling costs in the Medicare and Medicaid System [CMS].

And, then there is the reality known by all practicing medical professionals regardless of specialty orientation or degree designation. That is to say, CMS really can control healthcare costs and with great ferocity and efficiency, and to non-public sectors as well …. PARADOXICAL?

On Getting What You Wish For

Blogger Ezra Klein opines that one of the dirty little secrets of the health-care system is that Medicare has done a much better job controlling costs than private health insurers.

Of course, we doctors know that the real problem is that Medicare seemingly [think Seinfeld’s character George Costanza] controls costs all too well; but not really. It is just that CMS pays doctors too little and thus it appears costs are controlled. What really is happening is that physician fees are being reduced carte’ blanche.

Nevertheless, and regardless of semantics, CMS will never control costs much more efficiently than private insurance companies or doctors will simply abandon Medicare for related payment models like direct reimbursement or concierge medicine. This is happening right now. Physicians, osteopaths and podiatrists etc, are opting out of Medicare in increasingly large numbers. In a world where there’s only Medicare and Medicare to control costs, doctors can either take the pay cut or stop seeing patients, and stop being doctors. “Taking what they are given – because they’re working for a livin.”

So sorry that this seems like a forehead-palm moment for Ezra, but not for healthcare practitioners or the ME-P!

Too Much Demand Elsewhere

And, as we see from other countries, many young bright folks want to be doctors, even if being a doctor doesn’t make one particularly wealthy [high demand and high eventual supply produces lower provider costs in the long term?]. Think medical tourism.

Not so much the case anymore in this country [lower demand and lower eventual supply produces higher reimbursement costs to the doctor survivors in the very long term?].

Our Domestic World

But, we are not elsewhere. In fact, in our present domestic healthcare ecosystem, when Medicare decides to control costs, many doctors can simply stop accepting Medicare patients, and the politicians will lose their jobs. One political party then declares that Medicare is rationing and will hurt senior citizens. The other party capitulates and pays MDs more [SGR]. Then, the federal budget looks bad as it does now. The circle is complete when one party asserts that Medicare actually can’t contain costs but the private insurance companies will. It all fails, in an unending circular Boolean-like loop of illogic.

Listen Up!

So, listen up AARP, politicians, CMS and seniors as I admonish you to be careful what you wish for [medical cost controls]. It might just come true. As Ezra rightly says; rinse, repeat – rinse, repeat – ad nausea. You simply can’t have it both ways. You either choose to spend less and offend certain cohorts, or spend more and offend different factions. Either way, you’re going to piss someone off. A good healthcare reimbursement system would try to make that decision rationally [a-politically]. But, at least it would make an economics driven decision; wouldn’t it?

Assessment

Is CMS really the eight hundred pound cost-controlled gorilla in the increasingly large Medicare treatment room? Why or why not? Now, relative to the ACA of 2010, please read: The Case for Public Plan Choice in National Health Reform [Key to Cost Control and Quality Coverage], by Jacob S. Hacker, PhD. Link:Jacob Hacker Public Plan Choice

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Do we have a Medicare cost control efficiency paradox? Or, are the economists just reveling in the publication banal? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed: And, credible sponsors and like-minded advertisers are always welcomed.

Posted on April 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Paradox of Prosperity

“A paradox of prosperity is revealed and shown to be stable in the cycles of economic advancement between generations. I would put the matter this way: If one accepts, for example, that Mr. Brokaw’s ‘Greatest Generation’ were characterized by prudence, diligence, and patriotism in deed rather than word, that very generation produced its opposite in the generation that followed it. That is to say, I have found it repeated across the ages and across cultures, that the more diligent a previous generation, as a natural propensity, the more licentious the generation that follows. Invariably therefore, the generation that exhibits the more cogent properties of character for the best sort of citizenship fails to produce a generation of the same or similar characteristics.”

***

***

“Paradox of Prosperity” was applied as a term of analysis in the recent New York Times, Wall Street Journal bestseller Rescue America: Our best America is only one generation away (published October 2011), which Professor Morris co-authored with Chris Salamone. There the inter-generational breakdown is given a fuller exposition. Morris, who has been a careful reader of Thorstein Veblen, particularly Veblen’s masterpiece The Theory of the Leisure Class, says his own advancement of this inter-generational thesis was influenced by Veblen. “I think”, says Morris, “Veblen gave some insight as to what is produced in the generation which follows one such as Tom Brokaw described. The Greatest Generations – if by that we mean a generation characterized by prudence and sacrifice – nearly always produces a generation which can be characterized as a leisure class. They consume without manufacturing. They project feelings over principles. In general terms, they lack a spirit of sacrifice because they abhor the notion of “Objective Values” and so lack the will to re-create or advance the social ethos created by their parent’s generation.” In cultural terms, the generation that followed the “Greatest Generation” were the baby boomers (essentially, the children of the Greatest Generation between 1945–1965). The “Boomers” fit the classic definition of a “leisure class”, which Veblen described as being characterized by Conspicuous Consumption. To quote their description of their leisure class “they move values toward behavior, rather than behavior toward values”.

Posted on April 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Medical Ethics – Ever on Guard

***

ByAaron Carroll MD, MS

***

I’m a doctor. My father is a doctor. My colleagues are doctors, the people I train are doctors, lots and lots of my friends are doctors.

***

But, that doesn’t meant that doctors sometimes aren’t blind to certain issues like their own financial conflicts of interest. Sometimes we have to poke doctors with a stick. That’s how we show our love.

***

Conflicts of interest are the topic of this Healthcare Triage video.

Dr. Carroll has published some of the seminal work on various types of health care reform, and continues to be a sought after speaker on cost, quality and access-and the Affordable Care Act and its implications for our future. Considered one of the leading pediatric informaticists in the U.S. he has received millions of dollars in grants to explore the use of information technology in health care. Dr. Carroll was the Primary Investigator on a grant from the Agency for Healthcare Research and Quality to study the true impact of malpractice claims on the practice of medicine.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Physicians Received $12 Billion from Drug & Device Makers in Less Than 10 Years

A review of the federal Open Payments database found that the pharmaceutical and medical device industry paid physicians $12.1 billion over nearly a decade. Almost two thirds of eligible physicians — 826,313 doctors — received a payment from a drug or device maker from 2013 to 2022, according to a study published online in JAMA on March 28th. Overall, the median payment was $48 per physician.

Orthopedists received the largest amount of payments in aggregate, $1.3 billion, followed by neurologists and psychiatrists at $1.2 billion, and cardiologists at $1.29 billion. To find out what any physician was paid, click here.

On August 14, 2023, the Centers for Medicare and Medicaid Services (CMS) announced updates to their Accountable Care Organization Realizing Equity, Access, and Community Health (ACO REACH) model.

In response to feedback from stakeholders, starting in performance year (PY) 2024, the agency expects to increase the predictability for the model and further advance health equity. Only in its first PY, ACO REACH is a revision and replacement of the Global and Professional Direct Contracting (GPDC) model and the Geographic Direct Contracting (Geo Model) model, a subset of the GPDC model. This Health Capital Topics article will discuss the updates to the ACO REACH model and its implications for existing accountable care organizations (ACOs). (Read more…)

In a recent survey by Edelman Financial Engines, 57% of respondents said they’d feel wealthy if they had $1 million in the bank. But for many people, like doctors, that may not be enough.

Among those with $500,000 and $3 million in assets, 53% said it would take over $3 million in the bank for them to feel wealthy, and 33% said it would take over $5 million. Given that these are amounts some people will never even come close to amassing in their lifetimes, it may be hard to wrap your head around these answers.

Posted on April 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

THE AMA A.U.I. REPORT

***

By Staff Reporters

Doctors are excited—yet cautious—about the role augmented intelligence (AUI) could play in the future of healthcare. That’s the takeaway from an American Medical Association (AMA) survey released last month.

About two-thirds (65%) of 1,000+ physicians that the AMA surveyed in August 2023 agreed that there was at least some advantage to using AUI-powered tools, particularly when it comes to diagnostic ability (72%), work efficiency (69%), and clinical outcomes (61%). More than half (56%) of doctors said AUI tools could best help address administrative burdens.

Posted on April 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

On March 5th, 2024, the Department of Justice’s (DOJ’s) Antitrust Division, the Federal Trade Commission (FTC), and the Department of Health and Human Services (HHS), announced the launch of a multi-agency inquiry – in the form of a request for information (RFI) and public workshop – focusing on the increasing control of private equity (PE) and other corporations over the healthcare industry.

This Health Capital Topics article discusses the agencies recent actions and how it appears to be in line with the government’s recent moves to crack down on anti-competitive actions in healthcare. (Read more…)

The Institute of Medical Business Advisors Inc identified several reasons based on observations working with medical professional and physician clients over the years.

A late start

By the time doctors finish medical school and residency they’re typically in their middle or late thirties. Many have families to feed, and substantial student loans to pay off. It will be years before they can even start accumulating wealth. Consider that physicians typically enter careers at later ages, often with larger debts from training. Some specialties may not lead a case until 10 years of practice, and many specialties have limited longevity. Peak earning years may also be shorter for health care providers than other professionals. Financial survival skills are paramount for converting the limited earnings time period to personal financial security.

Challenging socio-political environment

It is increasingly challenging to practice medicine. With the Medicare Trust Fund slated to go bust in 2019, the Center for Medicare and Medicare Service (CMS) is increasingly resorting to cutting physician reimbursements and implementing capitation and bundled value based medical payments models. The medical reimbursement effects of the PP-ACA are not yet fully discerned; but appear to continue the decline in compensation. And to illustrate this potential governmental control, in what other industry can participants debate the simple question, “who is the customer?”

Lifestyle expectations

Society expects a doctor to live like a doctor, dress like a doctor, and drive like a doctor. Meeting social expectations can be quite expensive.

Time and energy

A doctor can’t be just a doctor any more. S/he also has to deal with ever increasing regulatory mandates, paperwork requirements by state and federal agencies and capricious insurance companies. It is estimated that for every hour spent on patient care, and additional half-hour is spent on paperwork. To-date, the use of electronic medical records has exacerbated; not ameliorated this problem. The demand on their time is mind-boggling. A typical doctor works a ten- to twelve-hour day. After work and family, they simply don’t have time and energy left to do comprehensive financial planning.

Financially naïve

Doctors are smart. They’re highly trained in their area of expertise. But, that doesn’t translate into understanding about finance or economics. Because they are smart, it’s easy for them to think they can easily master and execute concepts of personal financial planning, as well. Often, they don’t.

Lack of trust and delegation

Many doctors don’t trust financial advisors working for major Wall Street banks. They have the good instinct to realize that their interests are not aligned. Not knowing there are independent advisors out there who observe a strict fiduciary standard, they tend to do everything by themselves.

In fact, Paul Larson CFP®, President-CEO of the firm LARSON Financial Group LLC, noted a disquieting trend among physician client in his firm [personal communication]. Almost 90% of them fail to take care of their own family finances in a comprehensive manner; while only 10% are succeeding. The strategies in this chapter and book are common to their success.

Too Trusting

Another aspect of naivety, many physicians do not realize that the financial advisory industry lacks the same discipline and regulation that the average physician operates in. A primary care doctor would never even attempt a complicated surgery on a patient, but is trained to refer such patients to a specialist in the field with the proper training and experience. Financial Advisors often come from a sales background and are trained to keep a client in house even if the advisor is lacking in expertise. Also, many physicians are not trained to discern a qualified financial advisor from a sales person dressed up like a financial advisor. It is illegal to call yourself a physician in the United States unless you have the credentials to back it up; yet, anyone in the US can legally call themselves a financial advisor or a financial planner.

Posted on April 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Bertalan Meskó, MDPhD

***

***

What are you going to do 10-20 years from now? We toyed with the idea and came up with a list of healthcare jobs we think will be born in the coming decades. In case you want to become an organ designer or an end-of-life therapist. OR telesurgery VR planner.

And before you say I’m looking too far into the future, let me remind you that researchers are experimenting with a computer made of DNA-coated microbeads, with wireless charging of electronic implants, an Osaka hospital uses smart glasses to connect remote teams, while the FDA cleared an A.I. software automatically flagging cases of pneumothorax.

I hope you will find the newsletter useful!

Best regards, Bertalan Meskó, MD PhD The Medical Futurist

Posted on April 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

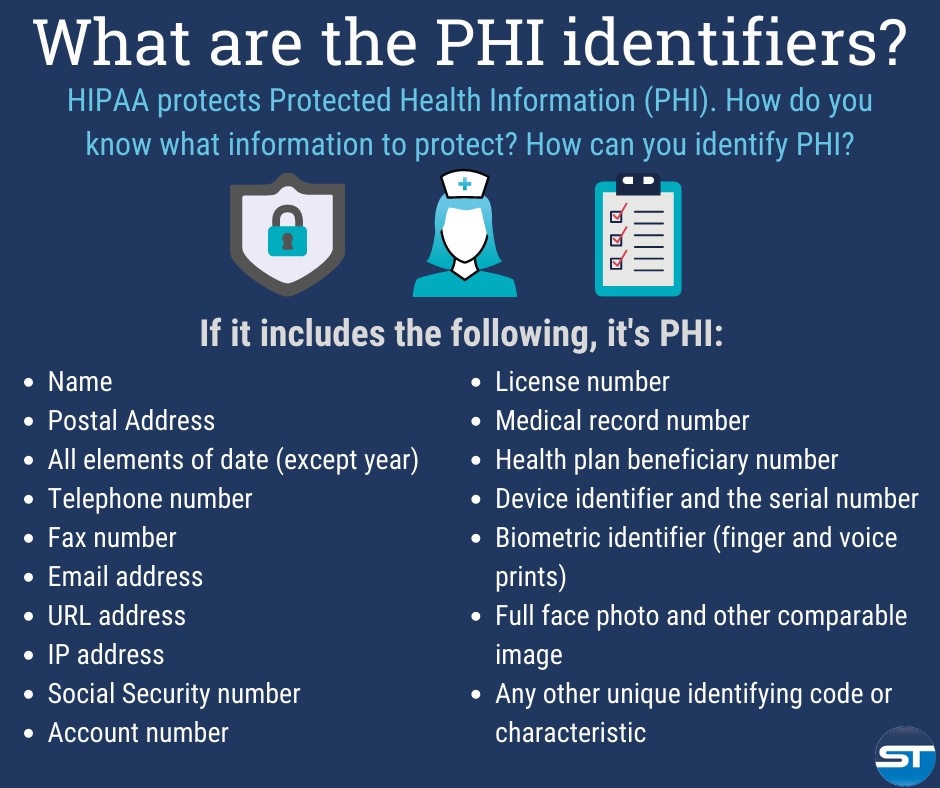

The Designated Medical Record Set [DMRS]: Contains medical and billing records and any other records that a physician, hospital, clinic and/or medical practice utilizes for making decisions about a patient; a hospital, emerging healthcare organization, or other healthcare organization. It serves to define which set of information comprises “protected health information” and which set does not; or contains medical or mixed billing records, and any other information that a physician and/or medical practice utilizes for making decisions about a patient.

It is up to the hospital or healthcare organization to define which set of information comprises “protected health information” and which does not though logically this should not differ from locale to locale. The patient has the right to know who in the lengthy data chain has seen their Protected Health Information. This sets up an audit challenge for the medical organization, especially if the accountability is programmed, and other examiners view the document without cause.

Posted on April 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What’s Your Back-up Plan – Doctor?

As per a recent study, 32% of data is lost by human errors. However hardware, software, hacks and smack-downs are responsible for remaining 68% data loss.

Data protection gains major importance in data loss. It can be achieved by implementing data management successfully.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On March 9th, 2024, President Biden signed into law a $460 billion spending package to continue funding the federal government for the remainder of the 2024 fiscal year. Contained within the spending package was legislation to cut in half the 2024 Medicare physician payment update of approximately -3.4%.

This Health Capital Topics article discusses the payment update, other healthcare provisions contained in the bipartisan spending bills, and responses from stakeholders. (Read more…)

Posted on March 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

NOBEL PRIZE WINNER AND FATHER OF BEHAVIORAL ECONOMICS

By Staff Reporters

DEFINITION: According to Wikipedia, behavioral economics is the study of the psychological, cognitive, emotional, cultural and social factors involved in the decisions of individuals or institutions, and how these decisions deviate from those implied by classical economic theory.

Behavioral economics is primarily concerned with the bounds of rationality of economic agents. Behavioral models typically integrate insights from psychology, neuroscience and microeconomic theory. The study of behavioral economics includes how market decisions are made and the mechanisms that drive public opinion.

Behavioral economics began as a distinct field of study in the 1970s and ’80s, but can be traced back to 18th-century economists, such as Adam Smith, who deliberated how the economic behavior of individuals could be influenced by their desires.

The status of behavioral economics as a subfield of economics is a fairly recent development; the breakthroughs that laid the foundation for it were published through the last three decades of the 20th century. Behavioral economics is still growing as a field, being used increasingly in research and in teaching.

***

***

Daniel Kahneman PhD, the father of behavioral economics, died yesterday at age 90 years old. He’s best known for applying psychology to economics and uncovering biases and mental shortcuts that make people act irrationally, as he chronicled in his best-selling book Thinking, Fast and Slow.

Kahneman, along with his long-time collaborator and friend Amos Tversky PhD, developed “prospect theory,” or loss-aversion theory, which earned him the Nobel Prize in Economics in 2002 (which he shared with fellow economist Vernon Smith). The idea is that people value losses and gains differently, so we feel more bad about losing $100 than we feel good about making the same amount. He applied this theory to investors, who had previously been considered rational decision-makers. It shows up elsewhere, too—for example, golfers putt better when they’re facing the loss of a stroke than when they might gain one.

Two other biases he identified include:

The “peak-end rule” that people remember an experience primarily based on how they felt at its most intense moment and the final part of it. It’s why you consider a whole vacation good if the last day was good—or the opposite.

The conjunction fallacy where people erroneously think the probability of two things being true is more likely than just one thing, which the famous “Linda the Bank Teller” problem illustrates.

A young concierge medical practice is a business with challenges in these Customer [Patient] Relationship Management’s [CRM] areas that are critical for success.

Areas of Most Challenge

Maturity of Processes:

Processes are often associated with bureaucracy or stuffy hierarchical healthcare systems that are anathema to emerging concierge medical practices. At small practices, doctors are often owners who fiercely pride themselves on flat structures, autonomy and flexibility. However, processes are imperative to conduct a streamlined practice that can be woven around a CM culture that still ensures practice business is conducted in a systematic manner.

Organization Structure:

Young concierge medical practices have challenges managing growth while grappling to incorporate an organization structure that promotes the elite private practice culture.

Multi-tasking, rapidly growing work places:

Young CM practices are often characterized by employees who multi-task and assume several roles to make their resources stretch farther. Especially in the current healthcare reform climate, young practice employees take up a broader set of responsibilities. In addition, as young private CM practices grow, they may become anguished with a growing office workplace that may not be equipped with an evolving infrastructure to cope. They have a fierce need to carefully control growth with tightly managed resources.

Changing business needs and strategy:

In an era after the golden age of traditional medicine, profitability is critical for emerging concierge practices. It is imperative to be nimble and change marketing strategies as socio-political and competitive climates dictate. A good C[P] RM system is tightly integrated, but loosely coupled, to allow CM practices to communicate appropriately with patients.

Little room for Slack:

Small concierge medical practices do not have as much established name-brand equity as larger, established practices of any model type, and patients are less willing to tolerate mistakes. Concierge practices have to run a much tighter ship and build impeccable patient experiences.

Fierce Competition:

The cash or retainer medicine landscape today looks very different from just five years ago. Competition is becoming fierce and practices are fighting for mindshare and patients. Young practices are competing with older concierge practices – large traditional practices, micro-practices, behemoth healthcare systems, enterprise-wide medical corporations and every other practice model in-between – to attract and retain patients with private resources.

Assessment

The above characteristics form the basis of a compelling strategy to embrace C[P]RM and streamline patient relationships and cash revenue opportunities. Concierge practices still need to build scalable marketing programs that can easily ramp up and down effortlessly as needs and economic environments demand. But, they do need to establish marketing metrics and processes that can demonstrate the Return on Investment (ROI) on their CRM, and marketing programs, and for getting critical cash-paying patient buy-in.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The fact that every physician in private medical practice, without a business education, leaves approximately a million dollars on the table and is unaware of it is well known to business experts who work with medical doctors experiencing financial difficulties.

Business experts such as Dan S. Kennedy, Peter Drucker, Michael Gerber, Maxwell Maltz, Neil Baum, William Hanson,Huss and Coleman, Steven Hacker, Thomas Stanley, Chris Hurn, Napoleon Hill, and Dave Ramsey, among others, understand the financial problems faced by medical practices and how to solve them.

Posted on March 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Colin Hung

***

Small- and medium-sized medical practices are struggling. The uncertain economic environment, staffing challenges, and the increasing complexity of providing care is putting practice owners under tremendous stress. EverHealth, providers of end-to-end solutions for healthcare providers, believes that these practices need support from partners that can take on some of the administrative, operational, and financial tasks so they can continue to deliver care to patients.

Healthcare IT Today sat down with Adam Laskey, General Manager of EverHealth at EverCommerce, to find out more about the company’s work, their vision for medical practices, and how the acquisitions of DrChrono and Updox is progressing.

Posted on March 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Financial hardship has led dozens of operators of senior facilities to file for bankruptcy over the past three years, with 13 companies filing petitions in 2021, 12 debtors filing in 2022 and 15 more in 2023, according to Gibbins Advisors.

***

***

Notable Chapter 11 filings over the past year have included Evangelical Retirement Homes of Greater Chicago, which filed Chapter 11 in the U.S. Bankruptcy Court for the Northern District of Illinois in June 2023 to sell its assets at auction. Also, Windsor Terrace Health, an operator of 32 nursing homes in California and three in Arizona, filed its petition in the U.S. Bankruptcy Court for the Central District of California in August 2023 listing $1 million to $10 million in assets and liabilities and unable to pay its debts.

More recently, Magnolia Senior Living, an operator of four facilities in Georgia, filed for Chapter 11 protection on March. 19 in the U.S. Bankruptcy Court for the Northern District of Georgia.

***

The Great Recession of 2008 had a lot of downsides: People lost homes, jobs, and retirement savings, had their careers derailed, and were forced to learn what the heck synthetic collateralized debt obligations are. But according to recent research, it also made people in the US live longer.

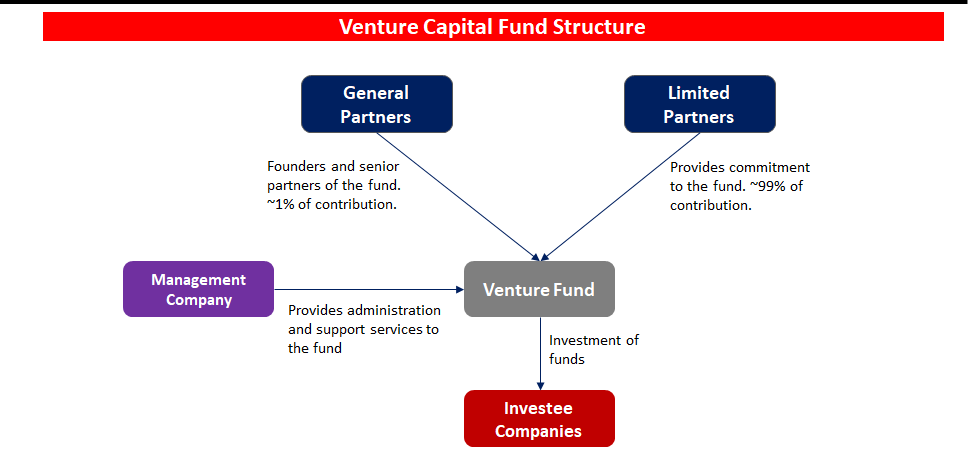

Venture capital funding in the digital health space cooled a bit in 2022 following a red-hot 2021. Overall, digital health companies raised $15.3 billion last year, down from the $29.1 billion raised in 2021—but still above the $14.1 billion raised in 2020, according to Rock Health a seed fund that supports digital health startups.

Nevertheless, analysts predict VC investors and bankers will still put a good amount of money into digital health in 2024 and 2025, especially in alternative care, drug development, health information technology technology, EMRs and software that reduces physician workload.

Of course. an essential first part of attracting VC interest and money is the crafting and presentation of your formal business plan [“elevator pitch”]; as well as the needed technical and managerial experience. This is crucial for success and exactly where we can assist.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

Almost every medical profession has its fair share of grossness and unbelievable moments. But, when it comes to podiatrists, you could argue that they have it extra bad for the simple reason that they specialize in feet. Most people would probably agree feet can be one of the human body’s most disgusting parts. People often neglect or ignore their feet, which can suffer badly from some common diseases and become a hotbed for unsanitary practices.

But, is a podiatrist really a physician?

You bet! Now, while the American Podiatric Medical Association [APMA] defines Doctor of Podiatric Medicine, or podiatrist, as “a physician and surgeon of the foot and ankle,” the The Social Security Administration’s Program Operations Manual System (POMS) legally defines a podiatrist as the following:

A podiatrist is a “physician” with respect to those functions which the podiatrist is legally authorized to perform in the State in which the individual performs them. Furthermore, the POMS states: A podiatrist is considered a “physician” for any of the following purposes: 1. for making the required physician certification and re-certifications of the medical necessity for Part A and Part B provider services. 2. for the purpose of establishing and periodically reviewing a home health plan of treatment; and for purposes of constituting a member of a Utilization Review (UR) committee but only if: a. the performance of these functions is consistent with the policy of the institution or agency with respect to which the podiatrist performs them; b. the podiatrist is legally authorized by the State to perform such functions; and c. at least two of the physicians on the Utilization Review committee are doctors of medicine or osteopathy.

In the United States, podiatrists are educated and licensed as Doctors of Podiatric Medicine (DPM). After a 4-year bachelor’s degree, the preparatory education of most podiatric physicians — similar to the paths of traditional physicians (MD or DO) — includes four years of undergraduate work, followed by four years in an accredited podiatric medical school, followed by a three or four year hospital-based residency program.

Optional one to two-year fellowships in foot and ankle reconstruction, surgical limb salvage, sports medicine, plastic surgery, pediatric foot and ankle surgery, and wound care is also available. Podiatric medical residencies and/ or fellowships are accredited by the Council on Podiatric Medical Education (CPME). The overall scope of podiatric practice varies from state to state with a common focus on foot and ankle surgery. Podiatrists work in hospitals, private practices and clinics, university medical centers and/or specialized practices.

Generally podiatrists can:

Perform physical examinations and study medical histories

Order and interpret X-rays and also other imaging studies like MRIs, and CAT scans.

Giving podiatric advice, second opinions and diagnosis

Administer drugs, narcotics, anesthetics and also sedation

Perform surgery related to the foot, ankle and legs

Perform plastic, macro and micro-surgeries and reconstructive bone surgeries

Prescribe medications such as narcotic pain killers, sleep aides and antibiotics

Perform certain physical and occupational therapies

Be on hospital staffs and take Emergency Room hospital call

Be on health insurance plans for covered physicians and medical providers

Prescribe, order, and fit prosthetics, casts, insoles, and orthotic devices

Attest to physical disability, write a doctor’s medical, treatment or absentee note, etc

In fact, the American Board of Podiatric Medicine [ABPM] offers a comprehensive qualification and certification process in podiatric medicine and orthopedics. Sub-specialties of podiatry include:

Did you know that the American Medical Association is calling on medical schools and residency programs to include specific information about healthcare economics and financing in their curricula.

But, is health economics heterodoxic, or not? And; what about demand-derived economics in medicine?

Posted on March 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Indications for 2024

By Health Capital Consultants, LLC

***

***

After healthcare mergers and acquisitions (M&A) activity began to regain momentum in 2022, following the slowing of deals in the wake of the COVID-19 pandemic, transactional activity continued to accelerate in 2023. While the healthcare sector continued to be impacted by factors such as valuation gaps, higher-for-longer interest rates, general macroeconomic risks, and increased state and federal regulatory concerns in 2023, the outlook for 2024 remains cautiously optimistic.

This Health Capital Topics article reviews the U.S. healthcare industry’s 2023 M&A activity and discusses what these trends may mean for 2024. (Read more…)

As fellow doctors, we understand better than most the more complex financial challenges physicians can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

And you may be misled by unscrupulous “advisors”.

For example:

Question: Do you know the difference between a “Fee-Only” and a “Fee-Based financial advisor? Not knowing may cost you tens of thousands of dollars, or more, in excessive advisory fees.

Posted on March 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Spiked in 2023

By Staff Reporters

***

***

Healthcare company bankruptcies spiked in 2023 amid high interest rates, rising labor and supply costs, and an uptick in denials from payers, according to a January report from healthcare restructuring firm Gibbins Advisors.

For example, Seventy-nine healthcare companies filed for bankruptcy in 2023—the highest number since 2019, which saw 51 bankruptcies, according to the report. The volume of bankruptcies last year was nearly 2x as high as 2022 and over 3x the level seen in 2021.

“We saw a dramatic increase in healthcare bankruptcy filings in 2023, continuing the trend which began in mid-2022,” Clare Moylan, co-founder and principal at Gibbins Advisors, said in a statement. “Key observations from 2023 are the return of large bankruptcy cases with over $100 million in liabilities, and a spike in hospital filings, both of which appear to primarily be a result of Covid-19 pandemic-related protections ending.”

Our virtual consulting model at DE MARCINKO & ASSOCIATES offer services to their clients primarily or entirely online, by phone or video-conference.

This means that no matter where you are or choose to live, you’re always just an email, telephone call or Zoom® conference away from a face-to-face meeting.

THE CONSULTATION IS VIRTUAL – THE INFORMATIONAL ADVICE IS REAL !

In a January 24th letter, AHA and other national hospital organizations voiced support for the Safety from Violence for Healthcare Employees (SAVE) Act (H.R. 2584/S. 2768), bipartisan legislation that would provide federal protections for health care workers similar to those that apply to aircraft and airport workers.

“Although our members have for many years had protocols in place designed to protect their employees and promote a safe environment for patient care, the number of violent attacks against health care workers has increased markedly in recent years,” the letters to House and Senate sponsors note. “Recent studies indicate that 44% of nurses have reported being subjected to physical violence and 68% have reported verbal abuse. These experiences affect the individual provider, who may suffer from both physical and psychological trauma, and they can also interfere with care delivery when providers fear for their personal safety, are distracted by disruptive patients or family members, or are traumatized from prior violent interactions. These types of incidents also consume scarce hospital and health system resources, which in turn could impact the care available for other patients.”

Did you know that desperate doctors of all ages are turning to knowledgeable financial advisors and medical management consultants for help? Symbiotically too, generalist advisors are finding that the mutual need for knowledge and extreme niche synergy is obvious.

***

***

But, there was no established curriculum or educational program; no corpus of knowledge or codifying terms-of-art; no academic gravitas or fiduciary accountability; and certainly no identifying professional designation that demonstrated integrated subject matter expertise for the increasingly unique healthcare focused financial advisory niche … Until Now!

So, if you are looking to supplement your knowledge, income and designations; and find other qualified professionals you may want to consider the CMP® program.

Enter the Certified Medical Planner™ charter professional designation. And, CMPs™ are FIDUCIARIES, 24/7.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

***

***

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The giant accounting firm Grant Thornton LLP is laying off 200 people, its second round of layoffs in the past six months and an indication that the major players in the professional consulting, accounting and advisory business are preparing for an economic slowdown that could squeeze profits across corporate America.

***

Statistics: 7.4%. That’s the percentage drop in students who graduated with a degree in accounting in the 2021–2022 school year than the year before. Low starting salaries, heavy workloads, and uncertainty around AI are driving the exodus of students from choosing accounting degrees. (the Wall Street Journal).

Informational essays of most current interest to healthcare professionals. Check back periodically for practical updates. Our catalogue library of major books, texts, case models and dictionaries is suggested for additional financial, economic, business and medical practice management information and education.

Posted on February 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Get ’em … While They are Hot!

By Ann Miller RN MHA

[ME-P Executive Director]

Just click on the book icon to order; get any one or all three! You’ll be glad you did.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Running a business involves a constant learning curve. And that applies whether you’re a rookie entrepreneur just starting out with a great idea for a new business or a more established small business owner with a quickly growing business that needs to expand. You should always be learning as a business owner, no matter where you are in your career—there’s always a new tool to master, new problems to solve, and new vocabulary to understand.

In order to not get totally overwhelmed, it’s helpful to take things one segment at a time. For instance, feeling confident when discussing the business’s financial needs should be a priority for every small business owner. After all, you represent the heart and soul of your business in the marketplace. So knowing the “language” of business finance is an integral part of your job as the owner.

The good news is that you don’t have to be an accountant or a financial planner to negotiate in the world of business finance. Here are some business terms and finance terms that will help you find your way to successful small business funding. https://www.youtube.com/embed/0kD4X2fgxGs

Business and Finance Terms to Know

From accounting, to business loans, to general business financial operations, here’s the ultimate list to all the business finance terms and definitions you need to know:

1. Accounts Payable

Accounts payable is a business finance 101 term. This represents your small business’s obligations to pay debts owed to lenders, suppliers, and creditors. Sometimes referred to as A/P or AP for short, accounts payable can be short or long term depending upon the type of credit provided to the business by the lender.

2. Accounts Receivable

Also known as A/R (or AR, good guess), accounts receivables is another business finance 101 term that means the money owed to your small business by others for goods or services rendered. These accounts are labeled as assets because they represent a legal obligation for the customer to pay you cash for their short-term debt.

3. Accrual Basis

The accrual basis of accounting is an accounting method of recording income when it’s actually earned and expenses when they actually occur. Accrual basis accounting is the most common approach used by larger businesses to record and maintain financial transactions.

4. Accruals

A business finance term and definition referring to expenses that have been incurred but haven’t yet been recorded in the business books. Wages and payroll taxes are common examples.

5. Asset

This business finance key term is anything that has value—whether tangible or intangible—and is owned by the business is considered an asset. Typical items listed as business assets are cash on hand, accounts receivable, buildings, equipment, inventory, and anything else that can be turned into cash.

6. Balance Sheet

Along with three other reports relating to the financial health of your small business, the balance sheet is essential information that gives a “snapshot” of the company’s net worth at any given time. The report is a summary of the business assets and liabilities.

7. Bookkeeping

A method of accounting that involves the timely recording of all financial transactions for the business.

8. Capital

Refers to the overall wealth of a business as demonstrated by its cash accounts, assets, and investments. Often called “fixed capital,” it refers to the long-term worth of the business. Capital can be tangible, like durable goods, buildings, and equipment, or intangible such as intellectual property.

9. Working Capital

Not to be confused with fixed capital, working capital is another business finance 101 term. It consists of the financial resources necessary for maintaining the day-to-day operation of the business. Working capital, by definition, is the business’s cash on hand or instruments that you can convert to cash quickly.

10. Cash Flow

Every business needs cash to operate. The business finance term and definition cash flow refers to the amount of operating cash that “flows” through the business and affects the business’s liquidity. Cash flow reports reflect activity for a specified period of time, usually one accounting period or one month. Maintaining tight control of cash flow is especially important if your small business is new, since ready cash can be limited until the business begins to grow and produce more working capital.

11. Cash Flow Projections

Future business decisions will depend on your educated cash flow projections. To plan ahead for upcoming expenditures and working capital, you need to depend on previous cash flow patterns. These patterns will give you a comprehensive look at how and when you receive and spend your cash. This info is the key to unlock informed, accurate cash flow projections.

12. Depreciation

The value of any asset can be said to depreciate when it loses some of that value in increments over time. Depreciation occurs due to wear and tear. Various methods of depreciation are used by businesses to decrease the recorded value of assets.

13. Fixed Asset

A tangible, long-term asset used for the business and not expected to be sold or otherwise converted into cash during the current or upcoming fiscal year is called a fixed asset. Fixed assets are items like furniture, computer equipment, equipment, and real estate.

14. Gross Profit

This business finance term and definition can be calculated as total sales (income) less the costs (expenses) directly related to those sales. Raw materials, manufacturing expenses, labor costs, marketing, and transportation of goods are all included in expenses.

15. Income Statement

Here is one of the four most important reports lenders and investors want to see when evaluating the viability of your small business. It is also called a profit and loss statement, and it addresses the business’s bottom line, reporting how much the business has earned and spent over a given period of time. The result will be either a net gain or a net loss.

16. Intangible Asset

A business asset that is non-physical is considered intangible. These assets can be items like patents, goodwill, and intellectual property.

17. Liability

This business finance key term is a legal obligation to repay or otherwise settle a debt. Liabilities are considered either current (payable within one year or less) or long-term (payable after one year) and are listed on a business’s balance sheet. A business’s accounts payable, wages, taxes, and accrued expenses are all considered liabilities.

18. Liquidity

Liquidity is an indicator of how quickly an asset can be turned into cash for full market value. The more liquid your assets, the more financial flexibility you have.

19. Profit & Loss Statement

See “Income Statement” above.

20. Statement of Cash Flow

One of the important documents required by lenders and investors that shows a summary of the actual collection of revenue and payment of expenses for your business. The statement of cash flow should reflect activity in the areas of operating, investing, and financing and should be an integral part of your financial statement package.

21. Statement of Shareholders’ Equity

If you have chosen to fund your small business with equity financing and you have established shares and shareholders as part of the controlling interests, you are obligated to provide a financial report that shows changes in the equity section of your balance sheet.

22. Annual Percentage Rate

The business finance term and definition APR represents the yearly real cost of a loan including all interest and fees. The total amount of interest to be paid is based on the original amount loaned, or the principal, and is represented in percentage form. When shopping for the right loan for your small business, you should know the APR for the loan in question. This figure can be very helpful in comparing one financial tool with another since it represents the actual cost of borrowing.

23. Appraisal

Just like your real estate appraisal when buying a house, an appraisal is a professional opinion of market value. When closing a loan for your small business, you will probably need one or more of the three types of appraisals: real estate, equipment, and business value.

24. Balloon Loan

A loan that is structured so that the small business owner makes regular repayments on a predetermined schedule and one much larger payment, or balloon payment, at the end. These can be attractive to new businesses because the payments are smaller at the outset when the business is more likely to be facing strict financial constraints. However, be sure that your business will be capable of making that last balloon payment since it will be a large one.

25. Bankruptcy

This federal law is used as a tool for businesses or individuals who are having severe financial challenges. It provides a plan for reduction and repayment of debts over time or an opportunity to completely eliminate the majority of the outstanding debts. Turning to bankruptcy should be given careful thought because it will have a negative effect on the business credit score.

26. Bootstrapping

Using your own money to finance the start-up and growth of your small business. Think of it as being your own investor. Once the business is up and running successfully, the business finance term and definition bootstrapping refers to the use of profits earned to reinvest in the business.

27. Business Credit Report

Just like you have a personal credit report that lenders look at to determine risk factors for making personal loans, businesses also generate credit reports. These are maintained by credit bureaus that record information about a business’s financial history.

Items like how large the company is, how long has it been in business, amount and type of credit issued to the business, how credit has been managed, and any legal filings (i.e., bankruptcy) are all questions addressed by the business credit report. Lenders, investors, and insurance companies use these reports to evaluate risk exposure and financial health of a business.

28. Business Credit Score

A business credit score is calculated based on the information found in the business credit report. Using a specialized algorithm, business credit scoring companies take into account all the information found on your credit report and give your small business a credit score. Also called a commercial credit score, this number is used by various lenders and suppliers to evaluate your creditworthiness.

29. Collateral

Any asset that you pledge as security for a loan instrument is called collateral. Lenders often require collateral as a way to make sure they won’t lose money if your business defaults on the loan. When you pledge an asset for collateral, it becomes subject to seizure by the lender if you fail to meet the requirements of the loan documents.

30. Credit Limit

When a lender offers a business line of credit it usually comes with a credit limit, or a maximum amount that you can use at any given time. It is said that you reach your credit limit or “max out” your credit when you borrow up to or exceed that number. A business line of credit can be especially useful if your business is seasonal or if the income is extremely unpredictable. It is one of the fastest ways to access cash for emergencies.

31. Debt Consolidation

If your small business has several loans with various payments, you might want to consider a business debt consolidation loan. It is a process that lets you combine multiple loans into a single loan. The advantages are possibly reducing the interest rates on the borrowed funds as well as lowering the total amount you repay each month. Businesses use this tool to help improve cash flow.

32. Debt Service Coverage Ratio

The business finance term and definition debt service coverage ratio (DSCR) is the ratio of cash your small business has available for paying or servicing its debt. Debt payments include making principal and interest payments on the loan you are requesting. Generally speaking, if your DSCR is above 1, your business has enough income to meet its debt requirements.

33. Debt Financing

When you borrow money from a lender and agree to repay the principal with interest in regular payments for a specified period of time, you’re using debt financing. Traditionally, it has been the most common form of funding for small businesses.

Debt financing can include borrowing from banks, business credit cards, lines of credit, personal loans, merchant cash advances, and invoice financing. This method creates a debt that must be repaid but lets you maintain sole control of your business.

34. Equity Financing

The act of using investor funds in exchange for a piece or ”share” of your business is another way to raise capital. These funds can come from friends, family, angel investors, or venture capitalists.

Before deciding to use equity financing to raise the cash necessary for your business, decide how much control you are willing to share when it comes to decision-making and philosophy. Some investors will also want voting rights.

35. FICO Score

A FICO score is another type of credit score used by potential lenders for evaluating the wisdom of entering a contract with you and your business. FICO scores comprise a substantial part of the credit report that lenders use to assess credit risk. It was created by the Fair Isaac Corporation, hence the name FICO.

36. Financial Statements

An integral part of the loan application process is furnishing information that shows your business is a good credit risk. The standard financial statement packet includes four main reports: the income statement, the balance sheet, the statement of cash flow, and the statement of shareholders’ equity, if you have shareholders.

Lenders and investors want to see that your business is well-balanced with assets and liabilities, has positive cash flow, and will have capital to make expected repayments.

37. Fixed Interest Rate

The interest rate on a loan that is established in the beginning and does not change for the lifetime of the loan is said to be fixed. Loans with fixed interest rates are appealing to small business owners because the repayment amounts are consistent and easier to budget for in the future.

38. Floating Interest Rate

In contrast to the business finance term and definition fixed rate, the floating interest rate will change with market fluctuations. Also referred to as variable rates or adjustable rates, these amounts may often start out lower than the fixed rate percentages. This makes them more appealing in the short term if the market is trending down.

39. Guarantor

When starting a new small business, lenders might want you to provide a guarantor. This is an individual who guarantees to cover the balance owed on a debt if you or your business cannot meet the repayment obligation.

40. Interest Rate

All loans and other lending instruments are assigned the business finance key term interest rates. This is a percentage of the principal amount charged by the lender for the use of its money. Interest rates represent the current cost of borrowing.

41. Invoice Factoring or Financing

If your business has a significant amount of open invoices outstanding, you may contact a factoring company and have them purchase the invoices at a discount. By raising capital this way, there is no debt, and the factoring company assumes the financial responsibility for collecting the invoice debts.

42. Lien

This business finance term and definition is a creditor’s legal claim to the collateral pledged as security for a loan is called a lien.

43. Line of Credit

A lender may offer you an unsecured amount of funds available for your business to draw on when capital is needed. This line of credit is considered a short-term funding option, with a maximum amount available. This pre-approved pool of money is appealing because it gives you quick access to the cash.

44. Loan-to-Value

The LTV comparison is a ratio of the fair-market value of an asset compared to the amount of the loan that will fund it. This is another important number for lenders who need to know if the value of the asset will cover the loan repayment if your business defaults and fails to pay.

45. Long-Term Debt

Any loan product with a total repayment schedule lasting longer than one year is considered a long-term debt.

46. Merchant Cash Advance

A merchant may offer a funding method through a loan based on the business’s monthly sales volume. Repayment is made with a percentage of the daily or weekly sales. These tend to be short-term loans and are one of the costliest ways to fund your small business.

47. Microloan

Microloans are loans made through nonprofit, community-based organizations and they are most often for amounts under $50,000.

48. Personal Guarantee

If you’re seeking financing for a very new business and don’t have a high value asset to offer as collateral, you may be asked by the lender to sign a statement of personal guarantee. In effect, this statement affirms that you as an individual will act as guarantor for the business’s debt, making you personally liable for the balance of the loan even in the event that your business fails.

49. Principal

Any loan instrument is made of three parts—the principal, the interest, and the fees. The principal is a business finance key term and is the original amount that is borrowed or the outstanding balance to be repaid less interest. It is used to calculate the total interest and fees charged.

50. Revolving Line of Credit

This business finance term and definition is a funding option is similar to a standard line of credit. However, the agreement is to lend a specific amount of money, and once that sum is repaid, it can be borrowed again.

51. Secured Loan

Many lenders will require some form of security when loaning money. When this happens, this business finance term and definition is a secured loan. The asset being used as collateral for the loan is said to be “securing” the loan. In the event that your small business defaults on the loan, the lender can then claim the collateral and use its fair-market value to offset the unpaid balance.

52. Term Loan

These are debt financing tools used to raise needed funds for your small business. Term loans provide the business with a lump sum of cash up front in exchange for a promise to repay the principal and interest at specified intervals over a set period of time. These are typically longer term, one-time loans for start-up expenses or costs for established business expansion.

53. Unsecured Loans

Loans that are not backed by collateral are called unsecured loans. These types of loans represent a higher risk for the lender, so you can expect to pay higher interest rates and have shorter repayment time frames. Credit cards are an excellent example of unsecured loans that are a good option for small business funding when combined with other financing options.

54. Articles of Incorporation

This is legal documentation of the business’s creation, including name, type of business, and type of business structure or incorporation. This paperwork is one of the first tasks you will complete when you officially start your business. Once submitted, your articles of incorporation are kept on file with the appropriate governmental agencies.

55. Business Plan

Here is your tool for demonstrating how you want to establish your small business and how you plan to grow it into good financial health. When writing a business plan, it should include financial, operational, and marketing goals as well as how you plan to get there. The more specific you are with your business plan, the better prepared you will be in the long run.

56. Employer Identification Number (EIN) Certificate

In order to be more easily identified by the Internal Revenue Service, every business entity is assigned a unique number called an EIN. When you start your small business, an EIN will be assigned and mailed to the business address. This number never changes, and you will be asked to furnish it for many reasons.

57. Franchise Agreement

For a small business entrepreneur, entering into a franchise agreement with a larger company can be a way to enter the marketplace. The agreement made between you and the larger company gives you the right to operate as a satellite of the larger company in a certain territory for a given period of time. This lets you, the business owner, take advantage of a brand name that’s already familiar in the marketplace and a process or operation that has already been tested.

58. Net Worth

This business finance term and definition is an expression of your business’s total value, as determined by your total current assets less the total liabilities currently owed by the business. With your business’s most recent balance sheet in hand, you can calculate the net worth using a simple formula: Assets – Liabilities = Net Worth.

59. Retained Earnings

Just like it sounds, this term represents any profits earned that are retained in the business. This can also be referred to as bootstrapping.

60. Tax Lien

If your business fails to pay taxes owed to the designated government entity, namely the IRS, you may find your assets seized by the claim of a tax lien. The government can not only seize your assets for liquidation to resolve the tax debt, but they can also charge you penalties on the amount you owe.

Don’t Be Overwhelmed by Health Economics, Business and Finance Terms

As a small business owner, physicians are required to wear many different hats—often including that of chief financial officer or bookkeeper. Before you let yourself get intimidated by all the business terms and definitions, just remember that knowledge is power.

You can serve your small practice business, clinic, out-patient center or hospital most effectively by becoming familiar with terms used in business and finance and how they will affect your financial health. Armed with a basic understanding of business finance key terms, you will be prepared to face the financial challenges that go along with being a modern doctor, today!

Posted on February 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Beneficial Ownership Information Report

IMPORTANT FOR DOCTORS, CONSULTANTS AND ADVISORS

By Staff Reporters

***

***

The BOI E-Filing System supports the electronic filing of the Beneficial Ownership Information Report (BOIR) under the Corporate Transparency Act (CTA). The CTA requires certain types of U.S. and foreign entities to report beneficial ownership information to the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury.