BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on January 6, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

Professor Eugene Schmuckler PhD MBA MEd CTS

***

***

Navigating the Challenges of Passive-Aggressive Patients in Healthcare

In the complex landscape of healthcare, effective communication between providers and patients is essential for accurate diagnosis, treatment adherence, and overall patient satisfaction. However, passive-aggressive behavior—characterized by indirect resistance, subtle obstruction, and veiled hostility—can significantly hinder this process. Passive-aggressive patients present unique challenges that require emotional intelligence, patience, and strategic communication skills from healthcare professionals.

Passive-aggressive behavior often stems from underlying feelings of fear, resentment, or a perceived lack of control. Patients may feel overwhelmed by their diagnosis, skeptical of medical advice, or frustrated by systemic issues such as long wait times or insurance complications. Rather than expressing these concerns openly, they may resort to behaviors such as missed appointments, vague complaints, sarcasm, or noncompliance with treatment plans. These actions, though subtle, can disrupt care continuity and erode trust between patient and provider.

One of the most difficult aspects of managing passive-aggressive patients is identifying the behavior early. Unlike overt aggression, passive-aggression is cloaked in ambiguity. A patient might nod in agreement during a consultation but later ignore medical instructions. They may offer compliments laced with sarcasm or express dissatisfaction through third parties rather than directly. These indirect signals can leave providers confused and uncertain about the patient’s true feelings or intentions.

***

***

Addressing passive-aggressive behavior requires a nuanced approach. First, providers must cultivate a nonjudgmental environment where patients feel safe expressing concerns. Active listening, empathy, and validation can encourage more direct communication. For example, acknowledging a patient’s frustration with wait times or side effects can open the door to honest dialogue. Providers should also be mindful of their own reactions, avoiding defensiveness or dismissiveness, which can exacerbate the behavior.

Setting clear boundaries and expectations is another key strategy. Passive-aggressive patients often test limits subtly, so it’s important to reinforce the importance of mutual respect and accountability. Documenting interactions, treatment plans, and patient responses can help track patterns and ensure consistency. In some cases, involving mental health professionals may be beneficial, especially if the behavior is rooted in deeper psychological issues.

Ultimately, the goal is to transform passive-aggressive dynamics into constructive partnerships. This requires time, effort, and a willingness to engage with patients beyond surface-level interactions. When successful, it can lead to improved outcomes, greater patient satisfaction, and a more harmonious clinical environment.

In conclusion, passive-aggressive patients pose a unique challenge in healthcare, but they also offer an opportunity for providers to refine their communication skills and deepen their understanding of patient psychology. By fostering openness, setting boundaries, and responding with empathy, healthcare professionals can navigate these interactions effectively and promote better health outcomes for all.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

In the competitive world of financial services, attracting and retaining clients is a constant challenge. To stand out, many financial advisors employ strategic marketing tactics known as “loss leaders”—free or discounted services designed to showcase value and build trust. These offerings serve as entry points for potential clients, allowing advisors to demonstrate expertise and initiate long-term relationships.

One of the most common loss leaders is the free initial consultation. This no-obligation meeting gives prospective clients a chance to discuss their financial goals, ask questions, and get a feel for the advisor’s approach. For the advisor, it’s an opportunity to assess the client’s needs and present tailored solutions. While no revenue is generated from this meeting, it often leads to paid engagements once the client feels confident in the advisor’s capabilities.

Another popular tactic is offering a complimentary financial plan or portfolio review. These services provide tangible insights into a client’s current financial situation and suggest improvements. By delivering real value upfront, advisors build credibility and demonstrate their analytical skills. Clients who receive actionable advice are more likely to continue working with the advisor on a paid basis.

Educational content also plays a key role in loss leader strategy. Advisors frequently host free webinars, workshops, or seminars on topics like retirement planning, tax strategies, or investment basics. These events not only educate attendees but also position the advisor as a thought leader. Attendees often leave with a better understanding of their financial needs and a desire to seek personalized guidance.

In the digital realm, advisors may offer free tools and assessments on their websites. These include retirement readiness calculators, risk tolerance quizzes, and budgeting templates. Such tools engage users and provide personalized feedback, creating a natural segue into one-on-one consultations. Additionally, offering free newsletters or eBooks helps advisors stay top-of-mind while delivering ongoing value.

Some advisors go further by waiving fees for introductory services, such as account setup or the first few months of investment management. This lowers the barrier to entry and encourages hesitant clients to try the service. Once clients experience the benefits, they’re more likely to commit long-term.

Loss leaders are not limited to high-net-worth individuals. Advisors targeting younger or less affluent clients may offer free debt management plans or budgeting assistance. These services address immediate concerns and build loyalty among clients who may become more profitable as their financial situations improve.

Ultimately, loss leaders are about building relationships. By offering something of value without immediate compensation, financial advisors demonstrate their commitment to helping clients succeed. This fosters trust, encourages engagement, and often leads to lasting partnerships. In a field where reputation and reliability are paramount, loss leaders serve as powerful tools for growth and differentiation.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

Classic Definition: The Boomerang[ing] paradox is a feedback loop or cycle where events come back positively or negatively. It is an interconnection between people that looks like an ecosystem.

Modern Circumstance: When our thoughts and words energetically go out into the world, it has the same effect as the boomerang. It will go all the way out and come back around. That part of the creation model is our thinking and speaking. We’re unconscious and co-creating our reality. The Boomerang effect is everywhere: politics, business, relationships, economics, environment, marketing, psychology and healthcare, etc.

PSYCHOLOGY

Paradox Example: Research has found that teaching people and patients about psychological biases can help counteract biased behavior. On the other hand, due to the innate need for preservation of a positive self-image, it is likely that teaching people about biases they hold, may cause a boomerang paradoxical effect in cases where being associated with a specific bias implies negative social connotations

MEDICINE

Paradox Example: Recent examples of a boomerang paradoxical drug effects is withosteoporosis medications such as Actonel, Boniva and Fosamax. These all belong to a class of drugs called bisphosphonates. They are supposed to strengthen bones, but some doctors report that long-term use of these drugs may actually pose a risk of certain unusual fractures.

ECONOMICS

Paradox Example: A characteristic of advanced economies like Australia is continual growth in household income and plunging costs of electric appliances, resulting in rapid growth in peak demand. The power grid in turn requires substantial incremental generating and network capacity, which is utilized momentarily at best. The result is the Boomerang Paradox, in which the nation’s rising wealth has created the pre-conditions for fuel poverty.

***

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on October 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

ByAI and Staff Reporters

***

***

Alpha Male and Beta Male are terms for men derived from the designations of alpha and beta animals in ethology. They may also be used with other genders, such as women, or additionally use other letters of the Greek alphabet (such as sigma. The popularization of these terms to describe humans has been widely criticized by scientists. Both terms have been frequently used in internet memes.

The term beta is used as a pejorative self-identifier among some members of the manosphere, particularly incels, who do not believe they are assertive and/or traditionally masculine, and feel overlooked by women. It is also used to negatively describe other men who are not deemed to be assertive, particularly with women. In internet culture, the term sigma male is also frequently used, gaining popularity in the late 2010s, but has since been used jokingly, often being used with incel.

Note: Incel is a portmateau of “involuntary celibate”) is a term associated with an online subculture of mostly male and heterosexual people who define themselves as unable to find a romantic or sexual despite desiring one. They often blame, objectify and denigrate women and girls as a result.

Delta Males are very responsible and keep the world moving. Highly adaptable, deltas are known for their competence and work ethic rather than their leadership and ambition. Delta Males love learning new skills for the sake of improving themselves, not for power or extrinsic successes. Because of this, they often have a very healthy work-life balance. They’re dependable and unpretentious. Common personality traits: hardworking, loyal and responsible. Careers they excel at are accountant, dentist, engineer and firefighter. If you’re a delta male, your work often speaks for itself. People trust you, so consider being more proactive and taking initiative at work; you’ll be rewarded for it and won’t necessarily need to be in the spotlight.

Gammas Males tend to be insecure about status and may overestimate their status. They’re unhappy with their position, so they try to convince themselves that they’re Sigmas. A Gamma Male is described as intelligent, romantic, and empathetic. While he has some female traits, he has difficulty understanding and dating women. But, unlike alphas, gammas avoid conflict at all costs and care deeply about what other people think of them. They lack the leadership skills and confidence to be on top.

Omega Males are skilled introverts who don’t need external validation. Pop culture portrays them as the shyer, more reserved yin to the zeta male’s yang. They’re independent and very comfortable in their own company. They’d rather spend time coming up with (usually brilliant) new ideas and inventions of their own instead of socializing with others. They have uncouth but delightful senses of humor and their theories often change the world for the better. Common personality traits are self-motivated, strategic and quiet. Careers they excel at are chemist, composer, inventor and mathematician. If you’re an omega male, your ideas are likely ingenious.

Sigma Males are rebellious leaders with lots of life experience while delta males are responsible companions who you want by your side.Common personality traits are nurturing and wise. Careers they excel at areentrepreneur, philosopher, professor, or therapist.

Zeta Males are one-of-a-kind progressives. There’s a reason the zeta male is the least talked about personality type in pop culture. They’re rare nonconformists who don’t care what other people think. They know themselves and refuse to change to fit into the rigid social standards of society. Zeta males are fierce creatives who blaze new paths for themselves and others. Zeta Males are nonconformist creatives, gamma males are charismatic nomads, and omega males are sharp intellectuals with boundless ideas. Careers they excel at are actor, artist, musician or writer. Common personality traits are creative, independent and self-aware.

QUESTION: Doctors, Agents, Accountants and Financial Advisors: What is your male personality type?

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

The study of behavioral economics has revealed much about how different biases can affect our finances—often for the worse.

Take loss aversion: Because we feel a financial setback more acutely than a commensurate gain, we often cling to failed investments to avoid realizing the loss. Another potential hazard is present bias, or the tendency to prefer instant gratification over long-term reward, even if the latter gain is greater.

When it comes to money, sometimes it’s difficult to make rational decisions. Here, are three behavioral financial biases that could be impeding financial goals.

ANCHORING BIAS

Anchoring Bias happens when we place too much emphasis on the first piece of information we receive regarding a given subject. Anchoring is the mental trick your brain plays when it latches onto the first piece of information it gets, no matter how irrelevant. You might know this as a ‘first impression’ when someone relies on their own first idea of a person or situation.

Example: When shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this financial advice, even though the guideline provided may cause us to spend more than we can afford.

Example: Imagine you’re buying a car, and the salesperson starts with a high price. That number sticks in your mind and influences all your subsequent negotiations. Anchoring can skew our decisions and perceptions, making us think the first offer is more important than it is. Or, subsequent offers lower than they really are.

Example: Imagine an investor named Jane who purchased 100 shares of XYZ Corporation at $100 per share several years ago. Over time, the stock price declined to $60 per share. Jane is anchored to her initial price of $100 and is reluctant to sell at a loss because she keeps hoping the stock will return to her original purchase price. She continues to hold onto the stock, even as it declines, due to her anchoring bias. Eventually, the stock price drops to $40 per share, resulting in significant losses for Jane.

In this example, Jane’s nchoring bias to the original purchase price of $100 prevents her from rationalizing to sell the stock and cut her losses, even though market conditions have changed. So, the next time you’re haggling for your self, a potential customer or client, or making another big financial decision, be aware of that initial anchor dragging you down.

HERD MENTALITY BIAS

Herd Mentality Bias makes it very hard for humans to not take action when everyone around us does.

Example: We may hear stories of people making significant monetary profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Example: During the dotcom bubble of the late 1990’s many investors exhibited a herd mentality. As technology stocks soared to astronomical valuations, investors rushed to buy these stocks driven by the fear of missing out on the gains others were enjoying. Even though some of these stocks had questionable fundamentals, the herd mentality led investors to follow the crowd.

In this example, the herd mentality contributed to the overvaluation of technology stocks. Eventually, it led to the dot-com bubble’s burst, causing significant losses for those who had unthinkingly followed the crowd without conducting proper research or analysis.

OVERCONFIDENT INVESTING BIAS

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

ASSESSMENT

Finally, questions remain after consuming this cognitive bias review.

Question: Can behavioral cognitive biases be eliminated by financial advisors in prospecting and client sales endeavors?

A: Indeed they can significantly reduce their impact by appreciating and understanding the above and following a disciplined and rational decision-making sales process.

Question: What is the role of financial advisors in helping clients and prospects address behavioral biases?

A: Financial advisors can provide an objective perspective and help investors recognize and address their biases. They can assist in creating well-structured investment and financial plans, setting realistic goals, and offering guidance to ensure investment decisions align with long-term objectives.

Question:How important is self-discipline in overcoming behavioral biases?

A; Self-discipline is crucial in overcoming behavioral biases. It helps investors and advisors adhere to their investment plans, avoid impulsive decisions, and stay focused on long-term goals reducing the influence of emotional and cognitive biases.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological biases to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

REFERENCES:

Marcinko, DE; Dictionary of Health Insurance and Managed Care. Springer Publishing Company, New York, 2007.

Marcinko, DE: Comprehensive Financial Planning Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2016.

Marcinko, DE: Risk Management, Liability and Insurance Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2017.

Nofsinger, JR: The Psychology of Investing. Rutledge Publishing, 2022

Winters, Scott: The 10X Financial Advisor: Your Blueprint for Massive and Sustainable Growth. Absolute Author Publishing House, 2020.

Ikea Effect Bias describes the tendency of people to place a higher value on products they have partially created or assembled themselves. This phenomenon is named after the Swedish furniture retailer Ikea, known for selling furniture in flat-pack kits that customers must assemble at home.

he IKEA effect was identified and named by Michael Norton of Harvard Business School, Daniel Mochon of Yale University and colleague Dan Ariely PhD of Duke University, who published the results of three studies in 2011. They described the IKEA effect as “labor alone can be sufficient to induce greater liking for the fruits of one’s labor: even constructing a standardized bureau, an arduous, solitary task, can lead people to overvalue their (often poorly constructed) creations.”

Example: A prospect is more likely to pursue his/her own financial plan than that one from an informed financial planner, CPA or professional advisor.

2011 study found that subjects were willing to pay 63% more for furniture they had assembled themselves than for equivalent pre-assembled items.

IN FINANCE AND INVESTING

The IKEA effect can contribute to reducing panic selling. Investors typically reduce their stock market exposure after a financial crash which often results in “buy high, sell low” strategy that is detrimental to long-run wealth accumulation.

Ashtiani et al.’s study proposes a nudge utilizing the IKEA effect to counteract this phenomenon: “actively involving investors in the selection process of the risky investments, while restricting their selections in a way that preserves a large degree of diversification.”

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

A paradox is a self-contradictory statement. And, the ancient Greeks were well aware that a paradox can take us outside our usual way of thinking. They combined the prefix para – (“beyond” or “outside of”) with the verb dokein (“to think”), forming paradoxos, an adjective meaning “contrary to expectation.” Latin speakers used that word as the basis for a noun paradoxum, which English speakers borrowed during the 1500s to create paradox.

***

***

Paradox of Education: Cumulative Advantage and Disadvantage

Classic Definition: Social status snowballs in either direction because people like associating with successful people, so doors are opened for them. And, folks avoid associating with unsuccessful people, for whom doors are closed.

Modern Circumstance: Education’s positive effect on health gets larger as people age. The large socioeconomic differences in health among older Americans mostly accrue earlier in adulthood on gradients set by educational attainment. Education develops abilities that help individuals gain control of their own lives, encouraging and enabling a healthy life.

Paradox Example: The health-related consequences of education cumulate on many levels, from the socioeconomic (including work and income) and behavioral (including health behaviors like exercising) to the physiological and intra-cellular. Some accumulations even influence each other.

In particular, a low sense of control over one’s own life accelerates physical impairment, which in turn decreases the sense of control. That feedback progressively concentrates good physical functioning and a firm sense of personal control together in the better educated while concentrating physical impairment and a sense of powerlessness together in the less well educated, creating large differences in health in old age.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

In the early 1980s, Daniel Kahneman and Amos Tverskey proved in numerous experiments that the reality of decision making differed greatly from the assumptions held by economists. They published their findings in Prospect Theory: An analysis of decision making under risk, which quickly became one of the most cited papers in all of economics.

To understand the importance of their breakthrough, we first need to take a step back and explain a few things. Up until that point, economists were working under a normative model of decision making. A normative model is a prescriptive approach that concerns itself with how people should make optimal decisions. Basically, if everyone was rational, this is how they should act.

Amanda, an RN client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her Financial Advisor know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

According to colleague Eugene Schmuckler PhD MBA MEd CTS, Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page.

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

CITE: Jaan E. Sidorov MD [Harrisburg, PA]

Assessment

Much like in healthcare today, the current mass-customized approaches to the financial services industry fall short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

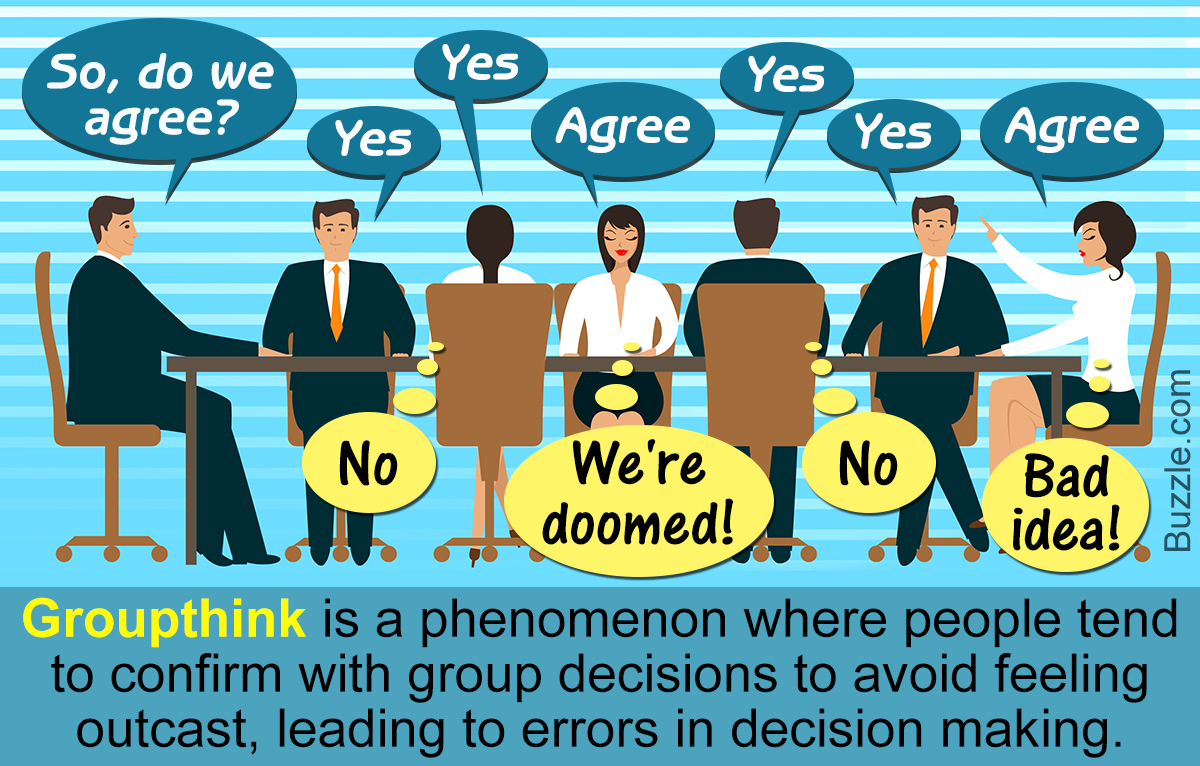

“lemming effect” or “group-think”

By Staff Reporters

***

***

According to psychologist and colleague Dan Ariely PhD, human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks.

In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”.

Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake. It is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect.

Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

The terms “psychologist” and “psychiatrist” are often used interchangeably to describe anyone who provides therapy services, but the two professions and the services they provide differ in terms of content and scope. A major difference between the two types of experts is that psychiatrists can prescribe medication [Rx].

As physicians [MD/DO] psychiatrists are trained to recognize the ways biological processes affect mental functioning.

Psychologists are oriented to how thoughts, feelings, and social factors influence mental functioning.

PSYCHIATRIST

Psychiatrists are medical or osteopathic doctors who are able to prescribe psychotropic medications, which they do in conjunction with providing psychotherapy though medical and pharmacological interventions are often their focus.

PSYCHOLOGIST

Though many psychologists hold doctorate degrees, they are not medical doctors, and most cannot prescribe medications. Rather, they solely provide psycho-therapy, which may involve cognitive and behavioral interventions, psycho-dynamic or psycho-analytic approaches.

NOTEPROTECTED TITLE: The title of “psychologist” can only be used by an individual who has completed the required education, training, and state license requirements. Informal titles, such as “counselor” or “therapist,” are often used as well. Other mental health care professionals, such as licensed social workers, can claim those titles, but not the title of “psychologist.”

According to Leslie Kernisan MD MPH, these are the basic self-care tasks that we initially learn as very young children. These are the self-care tasks we then learn as teenagers. They require more complex thinking skills, including organizational skills. They include:

Managing finances, such as paying bills and managing financial assets.

Managing transportation, either via driving or by organizing other means of transport.

Shopping and meal preparation. This covers everything required to get a meal on the table. It also covers shopping for clothing and other items required for daily life.

Housecleaning and home maintenance. This means cleaning kitchens after eating, keeping one’s living space reasonably clean and tidy, and keeping up with home maintenance.

Managing communication, such as the telephone and mail.

Managing medications, which covers obtaining medications and taking them as directed.

Because managing IADLs requires a fair amount of cognitive skill, it’s common for IADLs to be affected when an older person is having difficulty with memory or thinking. For those older adults who develop Alzheimer’s disease or a related dementia, IADLs will usually be affected before ADLs are.

***

***

IADLs were defined about ten years after ADLs, by a psychologist named M.P. Lawton. Dr. Lawton felt there were more skills required to maintain independence than were listed on the original Katz ADL index, and hence created the “Lawton Instrumental Activities of Daily Living Scale.”

Posted on June 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to BetterHealth.com, billions of people worldwide use social media platforms today. While social media can be a helpful tool for connection in the digital age, it also has the power to contribute to loneliness and isolation. This is the essence of the social media paradox.

***

What is the social media paradox?

The Merriam-Webster dictionary defines a paradox as “a statement that is seemingly contradictory or opposed to common sense and yet is perhaps true.” The social media paradox is a term coined to point out how, despite “social” being in the very name of it, social media has the potential to make people feel disconnected and lonely.

As a Public Health Post article published by Boston University puts it, “The more time people spend actively engaging on social media—whether through posting, commenting, or messaging—the lonelier they may feel,” calling it “a double-edged sword.” This simple statement summarizes the core of the social media paradox.

So how could something “social” be so closely tied to isolation?

The effects of social media are complex. On the one hand, it has brought many positives to the lives of many people. It can help individuals stay connected, learn about themselves, and receive important information.

On the other hand, excessive social media use in particular also has the potential to separate and contribute to negative mental health outcomes.

Posted on June 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and AI

***

***

Consistency and Commitment Tendency: Human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks.

In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”.

Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake.

According to colleague Dan Ariely PhD, it is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect. Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

Posted on May 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

GENDER

Gender is a subclass within a grammatical class (such as noun, pronoun, adjective, or verb) of a language that is partly arbitrary but also partly based on distinguishable characteristics (such as shape, social rank, manner of existence, or sex) and that determines agreement with and selection of other words or grammatical forms.

Gender paradox: Women conform more closely than men to socio-linguistics norms that are overtly prescribed, but conform less than men when they are not.

Gender-equality paradox: Countries which promote gender equality tend to have less gender balance in some fields.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Cognitive science is the interdisciplinary study of the mind and cognition. According to linguistics Professor Mackenzie H. Marcinko PhD, it combines various aspects from neuroscience, computer science, psychology, philosophy, linguistics, anthropology, and other fields, into a comprehensive study on the nature of intelligence.

Linguistics is the scientific study of language and its structure, including the study of morphology, syntax, phonetics, and semantics. Specific branches of linguistics include sociolinguistics, dialectology, psycholinguistics, computational linguistics, historical-comparative linguistics and applied linguistics.

Now, language and linguistics are closely related fields of study but they have distinct focuses.

Language refers to the system of communication used by humans, encompassing spoken, written, and signed forms. It is a means of expressing thoughts, ideas, and emotions.

On the other hand, linguistics is the scientific study of language itself. It examines the structure, sounds, meaning, and evolution of languages, as well as how they are acquired and used by individuals and communities.

While language is a broader concept that encompasses various forms of communication, linguistics delves into the intricate details and mechanics of language, aiming to understand its underlying principles and patterns.

Posted on April 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A thought experiment is an imaginary scenario that is meant to elucidate or test an argument or theory. It is often an experiment that would be hard, impossible, or unethical to actually perform. It can also be an abstract hypothetical that is meant to test our intuitions about morality or other fundamental philosophical questions. The German term Gedankenexperiment was utilized by physicist Ernst Mach

***

Mary is a brilliant scientist who is, for whatever reason, forced to investigate the world from a black and white room via a black and white television monitor. She specializes in the neuro-physiology of vision and acquires, let us suppose, all the physical information there is to obtain about what goes on when we see ripe tomatoes, or the sky, and use terms like ‘red’, ‘blue’, and so on.

Question: What will happen when Mary is released from her black and white room or is given a color television monitor? Will she learn anything or not?

***

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on April 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to colleague Dan Ariely PhD, Bereavement Sex is one of those coping mechanisms that sounds strange but makes sense when you think about it. In the face of loss, our brains crave connection and comfort.

Engaging in sex after a significant loss can be a way to feel alive and regain a sense of control. It’s a testament to our complex emotional wiring, where grief and intimacy intertwine.

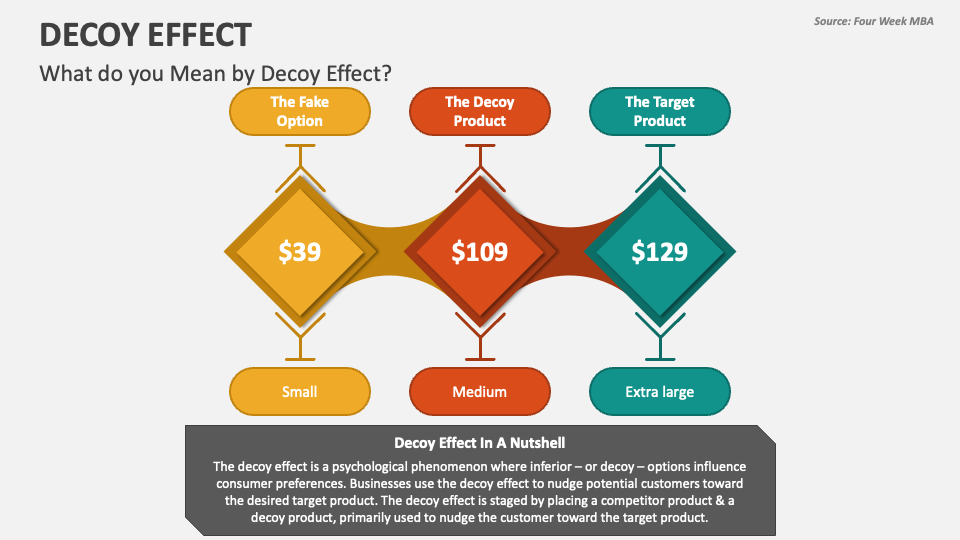

Decoy Bias Effect is a dubious phenomenon in decision-making where the introduction of a third, less attractive option (the “decoy”) influences individuals to change their preference between two other options.

The decoy bias effect describes how, when we are choosing between two alternatives, the addition of a third, less attractive option (the decoy) can influence our perception of the original two choices. Decoys are “asymmetrically dominated:” they are completely inferior to one option (the target) but only partially inferior to the other (the competitor). For this reason, the decoy effect is sometimes called the “asymmetric dominance effect.”

EXAMPLE: This bias is commonly used in financial planning sales; as well as marketing and mutual fund, ETF, REIT, stock broker, insurance agent and financial advisor pricing strategies to manipulate investor choices.

Classic: It’s no surprise that people are more honest when they know that they’re being watched. But what about just reminding them of the idea of being watched, without them actually being watched?

Modern: Researchers at the University of Newcastle’s Division of Psychology have an honor (or trust) system where they are requested to deposit payment for coffee in an “honesty box.” There was a note saying how much they should pay.

In 2006, Dr. Melissa Bateson and colleagues decided to do a little experiment: they placed an image above the note. They alternate between two pictures: one week they would use a picture of alleged human eyes and the other week, flowers. After 10 weeks, they plotted the amount of money received versus drinks consumed and found that people paid nearly three times as much for their drinks when eyes were displayed.

“There’s an argument that if nobody is watching us it is in our interests to behave selfishly. But when we think we’re being watched we should behave better, so people see us as co-operative and behave the same way towards us,” — Dr Bateson said

EXAMPLE:

Tax: This has great exemplar potential in things like federal, state and local income tax preparation, etc.

Insight: “It’s a definite that you’re all going to screw up, but it’s not a definite that any of you will learn from that,” declared one of our medical school instructors, years ago. “Cultivate the attitude that allows you to own your mistakes, and then, not repeat them” — reported Monique Tello MD MPH.

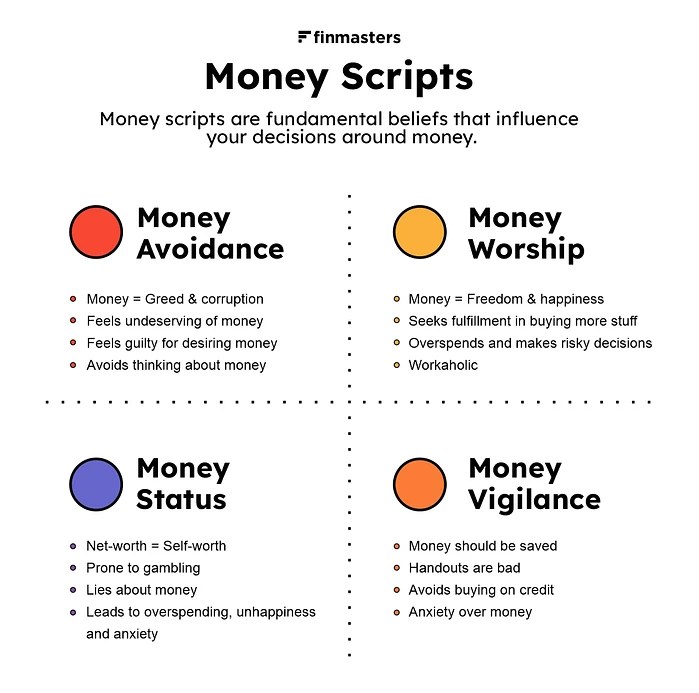

Stocks were decimated yesterday in the first full trading day following President Trump’s tariff announcement. It was the biggest single-day decline since the start of the Covid-19 pandemic in March 2020. Every Magnificent Seven stock was battered—Apple worst of all. And so perhaps it is a good time to discuss the concept of “Money Scripts”.

***

Money Scripts are unconscious beliefs about money that are typically only partially true, are developed in childhood, and drive adult financial behaviors. Money scripts may be the result of “financial flashpoints,” which are salient early experiences around money that have a lasting impact in adulthood. Money scripts are often passed down through the generations and social groups often share similar money scripts. And so, we argue that Money scripts are at the root of all illogical, ill-advised, self-destructive, or self-limiting financial behaviors.

In research at Kansas State University [KSU], researchers identified four distinct Money script patterns, which are associated with financial health and predict financial behaviors. These include: (a) money avoidance, (b) money worship, (c) money status, and (d) money vigilance [personal communication Brad Klontz, PsyD, CFP®, Kenneth Shubin-Stein, MD, MPH, MS, CFA and Sonya Britt, PhD, CFP®].

And so, we all like to think our financial decisions are fully rational, but the truth is that our subconscious beliefs have a dramatic impact on our money and financial decisions. These money scripts are important to know and understand. A summary is below:

Money Avoidance

Money avoidance scripts are illustrated by beliefs such as “Rich people are greedy,”“It is not okay to have more than you need,” and “I do not deserve a lot of money when others have less than me.” Money avoiders believe that money is bad or that they do not deserve money. They believe that wealthy people are corrupt and there is virtue in living with less money. They may sabotage their financial success or give money away even though they cannot afford to do so. Money avoidance scripts may be associated with lower income and lower net worth and predict financial behaviors including ignoring bank statements, overspending, financial dependence on others, financial enabling of others, and having trouble sticking to a budget.

Money Worship

Money worship is typified by beliefs such as “More money will make you happier,” “You can never have enough money,” and “Money would solve all my problems.” Money worshipers are convinced that money is the key to happiness. At the same time, they believe that one can never have enough. Money worships have lower income, lower net worth, and higher credit card debt. They are more likely to be hoarders, spend compulsively, and put work ahead of family.

Money Status

Money status scripts include “I will not buy something unless it is new,” “Your self-worth equals you net worth,” and “If something isn’t considered the ‘best’ it is not worth buying.” Money status seekers see net worth and self-worth as being synonymous. They pretend to have more money than they do and tend to overspend as a result. They often grew up in poorer families and believe that the universe should take care of their financial needs if they live a virtuous life. Money status scripts are associated with compulsive gambling, overspending, being financially dependent on others, and lying to one’s spouse about spending.

Money Vigilance

Money vigilant beliefs include “It is important to save for a rainy day,” “You should always look for the best deal, even if it takes more time,” and “I would be a nervous wreck if I did not have an emergency fund.” The money vigilants are alert, watchful and concerned about their financial welfare. They are more likely to save and less likely to buy on credit. As a result, they tend to have higher income and higher net worth. They also have a tendency to be anxious about money and are secretive about their financial status outside of their household. While money vigilance is associated with frugality and saving, excessive anxiety can keep someone from enjoying the benefits that money can provide.

Identification

When money scripts are identified, it is helpful to examine where they came from. A simple behavioral finance technique involves reflecting on the following questions:

What three lessons did you learn about money from your mother?

What three lessons did you learn about money from your father?

What is your first memory around money?

What is your most painful money memory?

What is your most joyful money memory?

What money scripts emerged for you from this experience?

How have they helped you?

How have they hurt you?

What money scripts do you need to change?

Conclusion

Ideally, from a balanced middle ground, we can see past the limitations of money scripts, our self and others who are polarized. Those who believe “Money is meant to be spent” or “Money is meant to be saved” have a world view that results in extreme positions. Labeling them as “correct” or “wrong” is not a useful way to try to shift anyone’s polarized money script beliefs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Negativity bias is not totally separate from pessimism bias, but it is subtly and importantly distinct. In fact, it works according to similar mechanics as the sunk cost fallacy in that it reflects our profound aversion to losing. We like to win, but we hate to lose even more.

And so, according to cognitive scientist Mackenzie Marcinko PhD, when we make a decision, we generally think in terms of outcomes—either positive or negative. The bias comes into play when we irrationally weigh the potential for a negative outcome as more important than that of a positive outcome.

***

***

Pessimism bias on the other hand, is a cognitive bias that causes people to overestimate the likelihood of negative things and underestimate the likelihood of positive things, especially when it comes to assuming that future events will have a bad outcome.

For example, the pessimism bias could cause someone to believe that they’re going to fail an exam, even though they’re well-prepared and are likely to get a good grade.

According to colleague Dan Ariely PhD, The pessimism bias can distort people’s thinking, including your own, in a way that leads to irrational decision-making, as well as to various issues with your mental health and emotional well being.

Avram Noam Chomsky is an American professor known for his traditional work in linguistics and political activism. Sometimes called “the father of modern linguistics”, Chomsky is also one of the founders of the field of cognitive science. He is a laureate professor of linguistics at the University of Arizona and an professor emeritus at MIT.

And so, modern linguists today approach their work with scientific rigor and perspective [STEM], although they use methods that were once thought to be solely an academic discipline of the humanities.

Contrary to this humanitarian belief, according to Professor Mackenzie Hope Marcinko PhD of the University of Delaware, linguistics is now multidisciplinary. It overlaps each of the human sciences including psychology, neurology, anthropology, and sociology. Linguists conduct formal studies of sound structure, grammar and meaning, but also investigate the history of language families, and research language acquisition.

Posted on March 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Inattentional Blindness: Is a psychological phenomenon where individuals fail to notice unexpected stimuli in their visual field when their attention is focused on a specific task or object.

This occurs because the brain prioritizes processing information relevant to the task at hand, leading to a temporary inability to perceive other, potentially significant details in the environment. Experiments, such as the famous “invisible gorilla” study, illustrate how people can completely miss prominent objects or events when their attention is directed elsewhere.

And, according to colleague Dan Ariely PhD, inattentional blindness highlights the limitations of human perception and attention, emphasizing that what we see is often influenced by where we focus our cognitive resources.

Posted on February 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

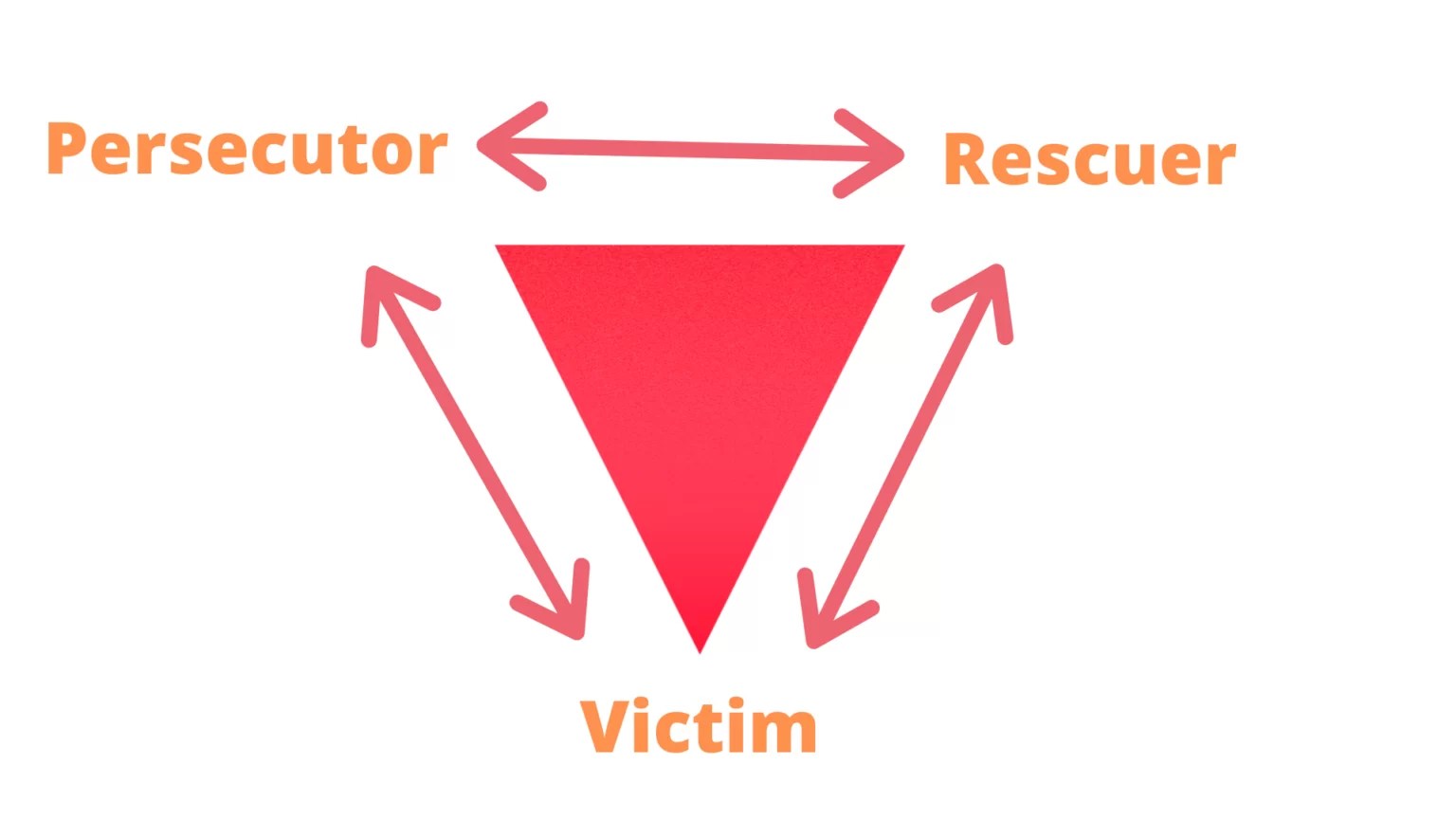

The Karpman drama triangle is a social model of human interaction proposed by San Francisco psychiatrist, Stephen B. Karpman in 1968. The triangle maps a type of destructive interaction that can occur among people in conflict. The drama triangle model is a tool used in psychotherapy, specifically transactional analysis. The triangle of actors in the drama are persecutors, victims and rescuers.

Karpman described how in some cases these roles were not undertaken in an honest manner to resolve the presenting problem, but rather were used fluidly and switched between by the actors in a way that achieved unconscious goals and agendas.

The outcome in such cases was that the actors would be left feeling justified and entrenched, but there would often be little or no change to the presenting problem, and other more fundamental problems giving rise to the situation remaining unaddressed.

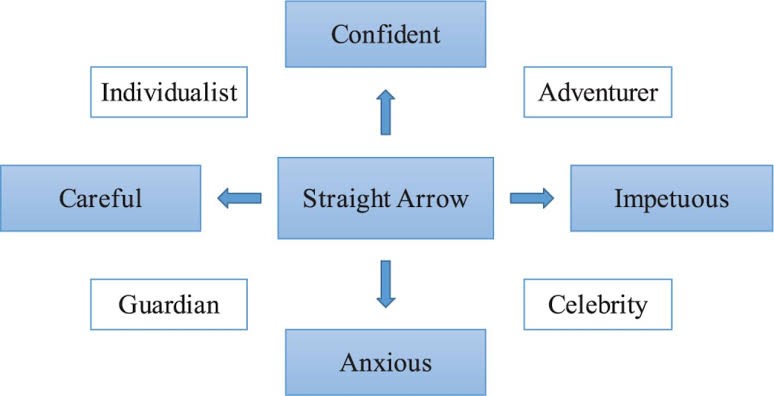

Fund managers Tom Bailard, Larry Biehl and Ron Kaiser identified five types of investors, each type characterized by their investment preferences and actions. These 5 types are: Individualists, Adventurers, Celebrities, Guardians and Straight Arrows. Key to the different categories is their different attitude to seeking professional financial advice. Defined below:

Individualists have faith in their own investment abilities so do not approach a financial adviser. But they are also cautious.

Adventurers are what may be called high rollers, in that they like big bets, tend not to diversify and are happy to put all their eggs in one basket. They, too, are unlikely to seek financial advice.

Celebrities tend to follow the crowd in investment terms but are aware of their lack of expertise so frequently consult advisers.

Guardians are fearful of losing money, thus prefer rock-solid investments such as government bonds. They, too, are likely to seek professional investment advice.

Straight Arrows exhibit some of the characteristics of individualists and some of adventurers.

Posted on January 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Ego-Protection refers to psychological strategies individuals use to defend their self-esteem and sense of self-worth against threats or failures. This can include attributing failures to external factors, minimizing the importance of negative feedback, or comparing oneself to others in ways that maintain a positive self-image.

According to colleague Dan Ariely PhD, ego-protective mechanisms help people cope with setbacks and maintain mental well-being, although they can sometimes prevent individuals from learning from mistakes or accepting constructive criticism.

Posted on January 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to colleague Dan Ariely PhD,Pre-Procurement Ownership is when you start to feel ownership over something before you actually have it. It’s like mentally moving into a house or car before you’ve signed the papers and moved in or driven away

This psychological quirk makes us more likely to commit to purchases because we’ve already imagined them as ours. Marketers exploit this by encouraging us to “try before you buy.”

So, next time you’re trying on a new men’s suit or woman’s skirt, be aware: your brain might already be claiming ownership.

Posted on January 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

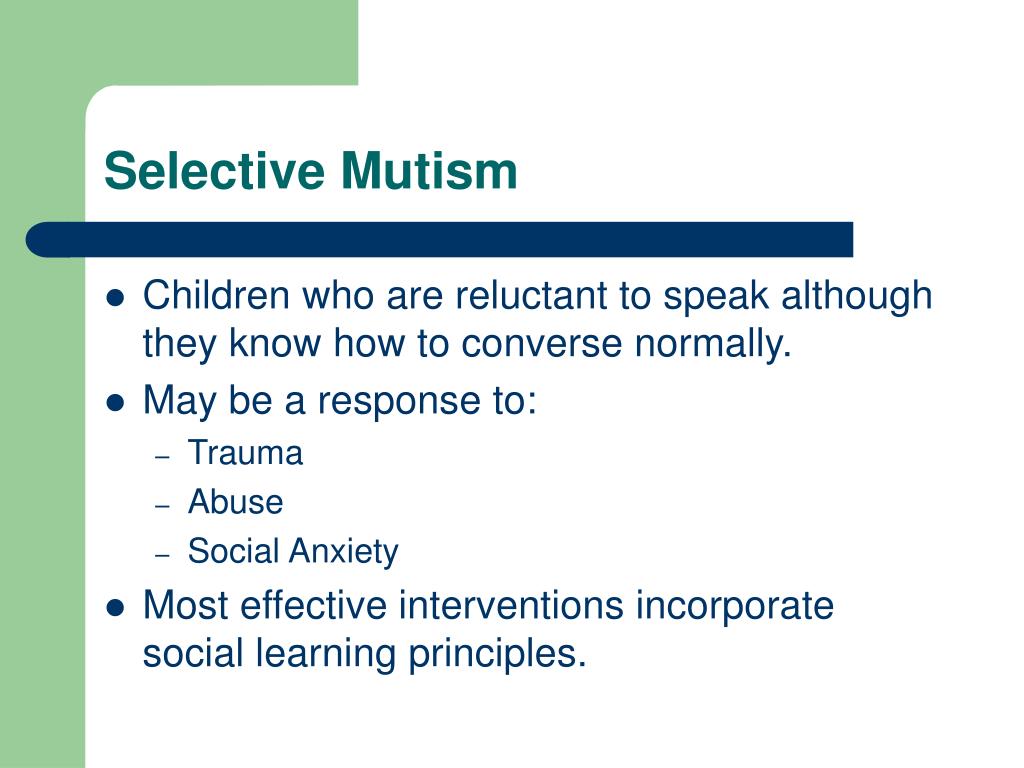

Selective Mutism: Some people experience selective mutism, a condition where intense trauma or anxiety leaves them temporarily unable to speak. It’s a defense mechanism that shields them from emotional overwhelm. It is characterized by:

A person’s inability to speak in certain social settings, even though they are otherwise capable of speech.

Triggers for selective mutism can include specific situations, places, or people.

People with SM can speak comfortably and communicate well in other settings, such as at home with family.

For many, according to colleague Dan Ariely PhD, this silence is involuntary, reflecting how deeply emotions affect speech.

Posted on January 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Reporters

***

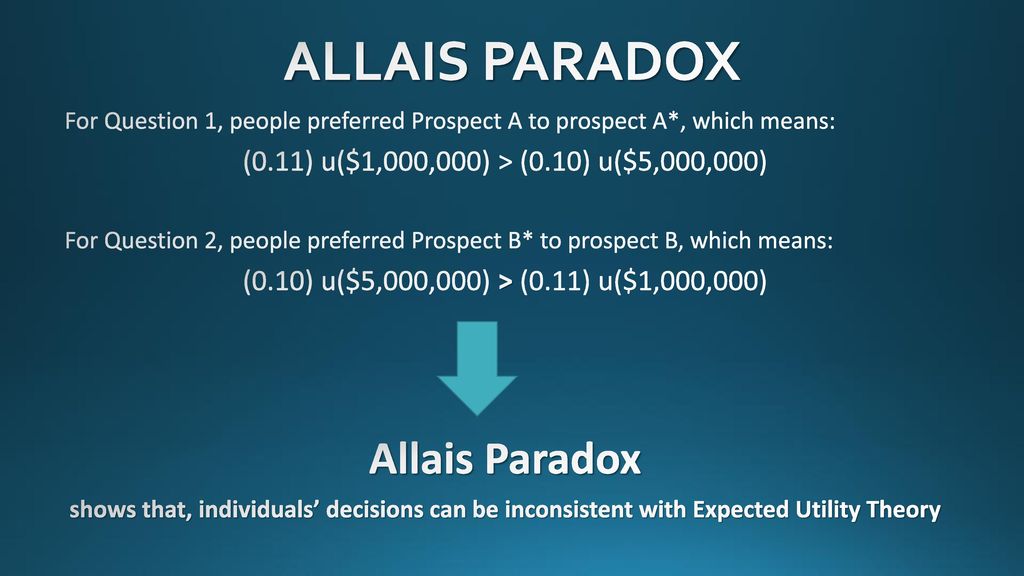

For Question 1, people preferred Prospect A to prospect A , which means: (0.11) u( 1,000,000) > (0.10) u( 5,000,000) For Question 2, people preferred Prospect B to prospect B, which means: (0.10) u( 5,000,000) > (0.11) u( 1,000,000) Allais Paradox. shows that, individuals’ decisions can be inconsistent with Expected Utility Theory.

***

Allais Paradox is a change in a possible outcome that is shared by different alternatives affects people’s choices among those alternatives, in contradiction with expected utility theory.

The Allais paradox is a choice problem designed by Maurice Allais 1953 to show an inconsistency of actual observed choices with the predictions of expected utility theory theory.

According to colleague Dan Ariely PhD, the Allais paradox demonstrates that individuals rarely make rational decisions consistently when required to do so immediately. The independence axiom of expected utility theory, which requires that the preferences of an individual should not change when altering two lotteries by equal proportions, was proven to be violated by the paradox.

Posted on January 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

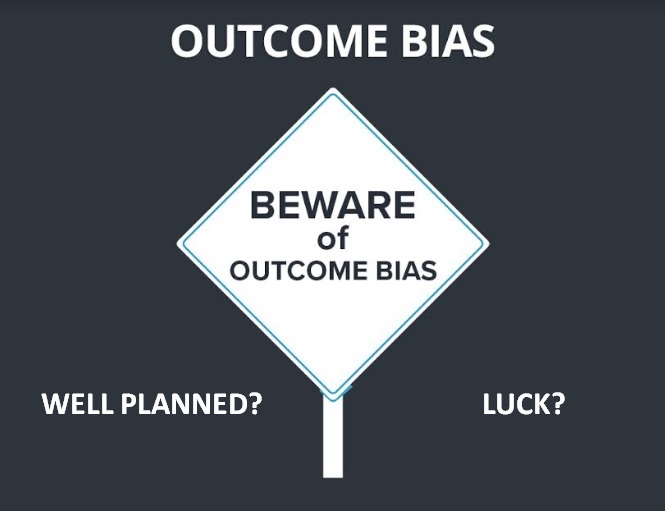

Outcome bias is judging a decision based on its result rather than the quality of the decision at the time it was made.

It’s like saying a bad poker play was smart because you won the hand. Or, a bad stock picker or financial advisor was good because the price went up!

According to psychologist and colleague Dan Ariely PhD, this bias ignores the process and focuses solely on the outcome. It’s why we celebrate lucky breaks and criticize thoughtful risks that didn’t pan out.

So, the next time you’re evaluating a decision, focus on the reasoning behind it, not just the end result.

Posted on December 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

QUESTION: Ever tried convincing someone by arguing against your own point?

If so, that’s paradoxical persuasion. It’s like reverse psychology’s sophisticated cousin. By presenting the opposite argument, you make people defend your original point. It’s a mental judo move, using their own momentum against them. Next time you want someone to agree with you, try saying, “You’re right, maybe we shouldn’t get pizza.”

So, according to Dan Ariely PhD, watch as they passionately argue why pizza is, in fact, the best choice for dinner.

Posted on December 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The proportionality bias, also known as major event/major cause heuristic, is the tendency to assume that big events have big causes. It is a type of cognitive bias and plays an important role in people’s tendency to accept conspiracy theories. Academic psychologist Rob Brotherton summarized it as “When something big happens, we tend to assume that something big must have caused it”.

IOW:Proportionality Bias is the inclination to believe that the magnitude of an event’s cause must be proportional to the event’s outcome. It’s like thinking a huge disaster must have a huge cause. This bias simplifies our understanding of complex situations but often leads to misconceptions. In reality, small causes can have large effects, and vice versa.

And so, to overcome proportionality bias according to colleague Dan Ariely Phd, consider all possible explanations, regardless of their size. Remember: sometimes big things happen for small reasons.

Posted on December 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Feeling the Pressure to “Give”

By Rick Kahler MS CFP®

Are you feeling any pressure this Christmas season to give, give, give? Keeping up with the Joneses all year is hard enough. It gets even worse during the holidays, when we feel pressured to keep up, not just with the Joneses, but also with the expectations others, and ourselves, put on Santa Claus.

Some Christmas shoppers overspend on gifts and end up paying off credit card bills for months. Others drive themselves crazy trying to find exactly the right gifts for the right people. Others hate the whole idea of shopping so much that they find it hard to enjoy the season.

If you fit into any of these categories, the cause may be your money scripts. The unconscious beliefs about money that we all hold are especially likely to kick in this time of year. We are surrounded by expectations and pressures about “ideal” holiday celebrations with the perfect gifts, the perfect decorations, and the perfect foods. As a result, we are especially vulnerable to making money decisions blindly in response to beliefs we don’t even realize we hold.

You may be one of those who regularly end up spending significantly more on gifts than you intended to. You may impulsively buy additional, unbudgeted gifts for people you’ve already bought presents for. You may not even try to set holiday spending limits. You may overspend on things for yourself while you’re Christmas shopping.

If any of these are true for you, you may have some unconscious beliefs about money that drive you to overspend. See whether any of the following money scripts might fit for you:

“The more you spend, the more love you show.”

“It takes the joy out of giving if you pinch pennies.”

“It’s the season for giving lavishly, not for being a Scrooge.”

“If I don’t buy just the right gifts, people won’t like or respect me.”

“I need to give my kids more than I got when I was a child.”

“More gifts and more spending will make the holidays okay (and make my guilt go away).”

“It’s tradition. Everyone expects (whatever) from me.”

“I do so much for everyone else; I deserve something for myself, too.”

It’s also possible you may go to the opposite extreme and be a Grinch when it comes to the holidays. If you hate Christmas shopping, grumble about the holiday being so commercialized, and look forward to January, it’s possible you may hold some money scripts that drive you to underspend. Your beliefs may be similar to the following:

“It’s wrong to spend money except on necessities.”

“You aren’t a spiritual or religious person if you spend too much money.”

“Christmas shouldn’t be about money.”

“It’s wrong to spend money on luxuries when poor people are suffering.”

“It isn’t good for kids to get too much.”

“My kids shouldn’t have more than I had when I was a child.”

If you’d like to change some aspects of what you do and how you feel about holiday spending, you may find it useful to take a closer look at your own beliefs about the season. One way to begin this is to quickly write answers (short statements are best) to the following questions: What do I believe about money and each of the following? Christmas? Family celebrations? Presents? Giving? Spending? Receiving?

Assessment

You may uncover some money scripts similar to the ones listed above. Learning why you tend to overspend or under spend this time of year won’t instantly change what you do. Yet understanding what is behind your pattern of holiday spending is an important way to start becoming a more conscious Christmas shopper.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Choice Overload is the difficulty in making a decision when faced with too many options. It’s like standing in front of an ice cream counter with 31 flavors and feeling paralyzed.

Among personal decision-makers, a prevention focus is activated and people are more satisfied with their choices after choosing among few options compared to many options, i.e. choice overload. However, individuals can also experience a reverse choice overload effect when acting as proxy decision-maker, too.

It is widely accepted that having more choices is inherently positive. When there are more available options from which to choose, an individual is more likely to be able to select the particular option that is the best fit and most likely to satisfy them. Choice is typically thought to be related to personal freedom and enhanced well-being.

Therefore, according to colleague Neal Baum MD, for most individuals the ultimate goal is to constantly maximize their choices in life to increase their overall satisfaction and well-being. The decision-making process, however, is a complex cognitive task that does not always lead to positive outcomes.

Thus, while having options is generally good, too many choices can lead to anxiety and decision fatigue. This is why curated selections and recommendations are so popular – they simplify the decision-making process’ according to another colleague Dan Ariely PhD.

So, when you’re overwhelmed by choices, narrow them down to a manageable number and make your decision easier.

Posted on December 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Theory of Linguistic Sciences

Avram Noam Chomsky is an American professor known for his work in linguistics and political activism. Sometimes called “the father of modern linguistics”, Chomsky is also one of the founders of the field of cognitive science. He is a laureate professor of linguistics at the University of Arizona and an professor emeritus at MIT.

And so, modern linguists today approach their work with scientific rigor and perspective [STEM], although they use methods that were once thought to be solely an academic discipline of the humanities.

Contrary to this belief, linguistics is multidisciplinary. It overlaps each of the human sciences including psychology, neurology, anthropology, and sociology. Linguists conduct formal studies of sound structure, grammar and meaning, but also investigates the history of language families, and research language acquisition.

And, as with other scientists according to linguistical engineer and Professor Mackenzie Hope Marcinko PhD from the University of Delaware [UD], they formulate hypotheses, catalog observations, and work to support explanatory theories, etc.

Posted on December 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

Sympathy Mining is the act of exaggerating personal problems to gain sympathy or attention. While it may fulfill a need for validation, it can strain genuine connections.

Someone who deliberately entices others into showing sympathy by utilizing social media with non-descriptive &/or ambiguous statements designed to invite further questioning and therefore garnering sympathy with their reported issue.

According to colleague Dan Ariely PhD, over time, onground or online sympathy mining can erode trust, especially if it’s clear that issues are exaggerated.

Incentives: It is broadly accepted that incenting someone to do something is effective, whether it be paying office staff a commissions to sell more healthcare products, or giving bonuses to office employees if they work efficiently to see more HMO patients. Some experts even suggest there are five specific components1 that should be built into an overall physician incentive program:

Appropriate financial incentives.

Managed-care efficiency incentives.

Group citizenship.

Patient satisfaction.

Group profitability.

What is not well understood is that the incentives cause a sub-conscious distortion of decision-making ability in the incented person. This distortion causes the affected person – whether it is yourself or someone else – to truly believe in a certain decision, even if it is the wrong choice when viewed objectively. Service professionals, including financial advisors and lawyers, are affected by this bias, and it causes them to honestly offer recommendations that may be inappropriate, and that they would recognize as being inappropriate if they did not have this bias.

According to colleague Dan Ariely PhD, the existence of this bias makes it important for each one of us to examine our incentive biases and take extra care when advising physician clients, or to make sure we are appropriately considering non-incented alternatives.

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

MODERN DAY SOCIAL INFLUENCERS

***

***

Mob Mentality can occur in unfamiliar groups, social cues disappear, and behavior becomes influenced by the crowd. Mob mentality shows how people sometimes act in ways they wouldn’t alone, following the group’s lead. According to colleague Dan Ariely PhD, this effect can create a loss of personal accountability, leading to behavior that may not align with personal values.

Herd mentality is the tendency for people’s behavior or beliefs to conform to those of the group they belong to. The concept of herd mentality has been studied and analyzed from different perspectives, including biology, psychology and sociology. This psychological phenomenon can have profound impacts on human behavior.

QUESTION: What about social media sites and modern influencers today! So-called celebrity endorsements and political elections, too?

Posted on December 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BEWARE THE PSYCHOLOGY OF HOLIDAY SHOPPING!

[Online -OR- Onground]

By Staff Reporters

***

***

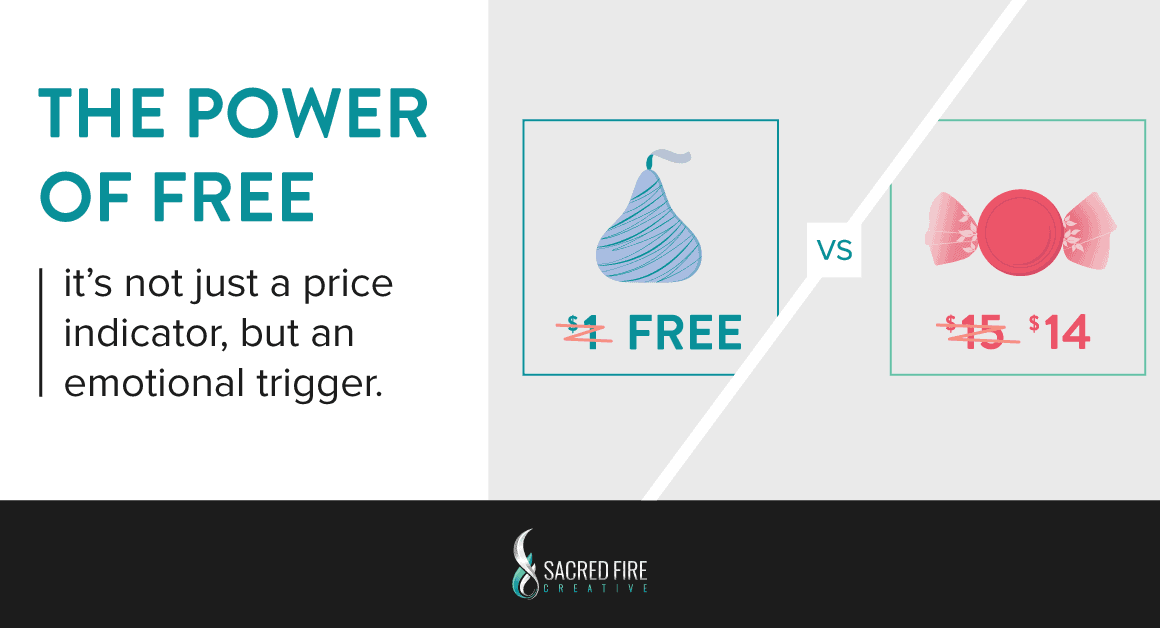

Power of Free

Who doesn’t love free stuff? The word “free” is like a magic spell that makes our rational minds go on vacation.

According to colleague Dan Ariely PhD, the power of free compels us to grab things we don’t need and make questionable choices. Why buy one and get one free when you can get two for the price of one? It’s the same deal, but free feels better.