|

||||

|

Share this:

Filed under: Health Economics, iMBA, Inc., Investing, Practice Management, Recommended Books | Tagged: FOMC, interest rates, IRS, Michael A. Gayed CFA | 5 Comments »

ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

![]()

![]()

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

![]()

ePodiatryConsentForms.com

ePodiatryConsentForms.com

“Providing Management, Financial and Business Solutions for Modernity”

“Providing Management, Financial and Business Solutions for Modernity”

|

||||

|

Filed under: Health Economics, iMBA, Inc., Investing, Practice Management, Recommended Books | Tagged: FOMC, interest rates, IRS, Michael A. Gayed CFA | 5 Comments »

![]()

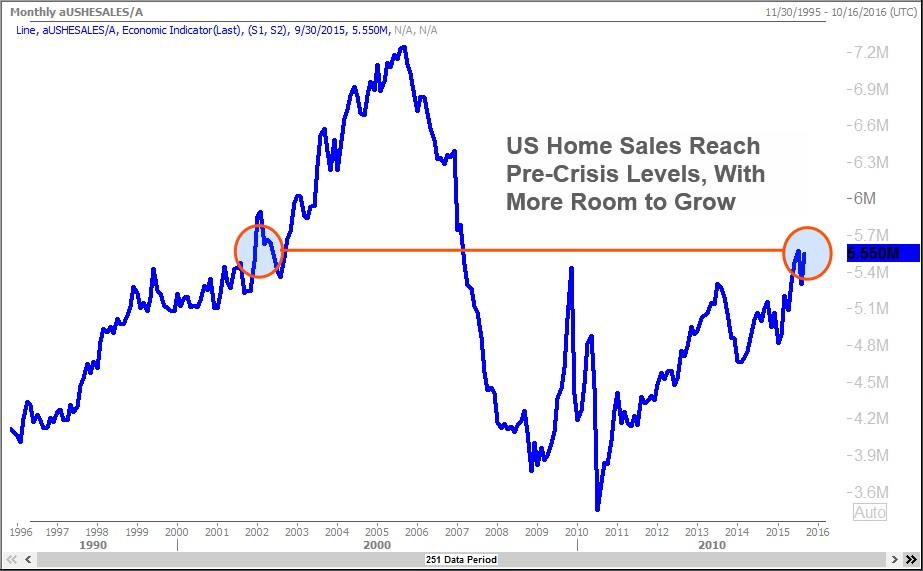

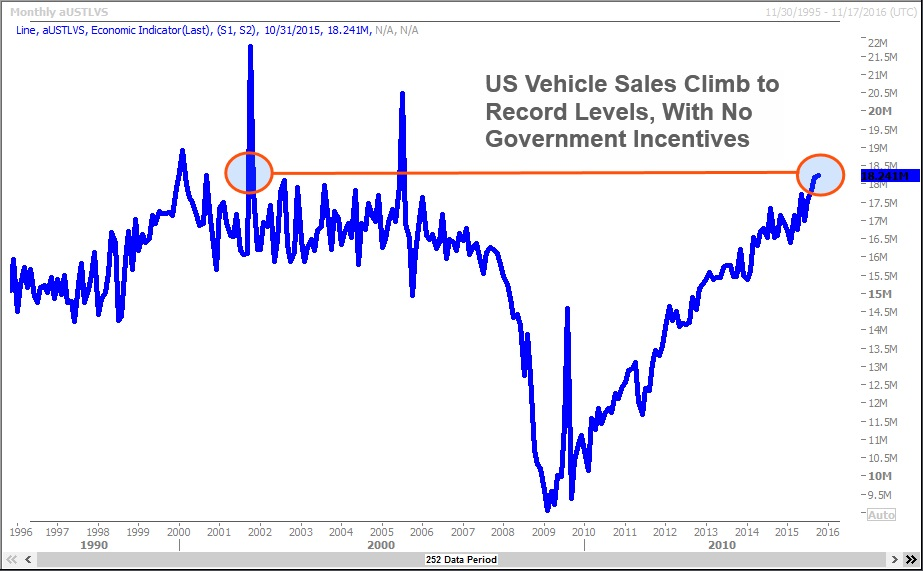

On cars and houses

[By Josh Velazquez CMPS]

[By Josh Velazquez CMPS]

jvelazquez@bankingunusual.com

The US economy is roaring back to life as measured by the two largest purchases that people make: cars and houses. The interesting thing is that the uptick in sales is not being driven by artificial government incentives.

Instead, consumer demand is the main driver. It’s also interesting to note the impact of housing on your local economy.

***

***

According to data compiled by the Bureau of Economic Analysis (BEA) and the National Association of Realtors (NAR), the value of construction as well as real estate and rental and leasing represents approximately 16.8% of the US economy, but the impact is much larger in some states.

Click here to check out the impact of housing in your state.

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

***

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Filed under: Alternative Investments, Investing, Op-Editorials, Research & Development | Tagged: Bureau of Economic Analysis, Josh Velazquez, National Association of Realtors, US economy | 3 Comments »

![]()

Be Ready for a Great 2016!

[By Patrick Bourbon CFA]

1. IRA – 401(k) / 403(b) retirement accounts – Are you on track for a comfortable retirement? You could increase the funding of your IRA and company retirement plan like a 401(k) or 403(b) accounts. 401(k) and 403(b) accounts allow individuals younger than 50 to contribute $18,000 each year, and individuals 50 and older to contribute $24,000. Some plans allow workers to make additional contributions of after-tax money.

For those under 50, the maximum is $53,000 for 2015. Doing so does not reduce your taxable income, but taxes are deferred on any earnings that the after-tax money makes. Later, some people roll these contributions into a Roth IRA, tax-free so the money would then grow tax-free. Traditional and Roth IRAs allow individuals younger than 50 to contribute $5,500 each year and individuals 50 and older to contribute $6,500. Even if you earn too much to contribute to a Roth IRA directly, you can open a traditional nondeductible IRA and convert it to a Roth; there is no income limit on traditional nondeductible IRAs or conversions. Returns generated in IRA and 401(k) / 403(b) accounts compound tax-free over their entire life.

2. Start tax planning! It’s not too early to think about taxes. Asset location & Tax efficiency Review your taxable and non-taxable accounts to ensure they are optimized for tax efficiency. If you have foreign bank accounts, make sure you comply with FATCA and FBAR (forms FinCEN 114, 8938, 8621…). If you have forgotten, you may look into the Offshore Voluntary Disclosure Program (OVDP) or Streamlined procedures.

3. Portfolio rebalancing Make sure you have rebalanced your portfolios to keep them in line with your goals, time horizon and risk tolerance. The market movements this summer may have thrown off your portfolio balance between stocks and bonds. David Swensen, the Chief Investment Officer at the Yale Endowment, performed an analysis that showed optimal rebalancing could add 0.4% to your annual return.

4. Harvest your capital losses Maybe it is time to sell some funds, ETF, stocks to generate some capital losses? Tax-loss harvesting is a method of reducing your taxes by selling an investment that is trading at a significant loss. Find out if you have any loss carryovers from prior years to be applied against capital gains (from sale of funds, ETF, stocks… in your taxable/brokerage accounts). If your current year’s capital losses exceed your capital gains, you have a net capital loss. You can use up to $3,000 of that loss ($1,500 if you are married filing separately) to offset other taxable income such as your salaries, wages, interest and dividends. If the capital loss is more than $3,000, you can carry over the excess and apply it against capital gains next year.

5. Emergency fund Don’t forget to establish or tune up your emergency fund. This is a good time to set aside money for next year’s cash needs. It is an account that is used to set aside funds to be used in an emergency, such as the loss of a job, an illness or a major expense.

6. Review your insurance policies Do you have a life, disability and long term care insurance? Make sure you and your loved ones are well protected if something happens to you. Your life may have changed (birth, marriage …). If you do have enough coverage it is also a good time simply to review the different types of coverage you have. Whole life or Variable Universal Life may help you reduce your taxes.

7. Health Spending Account Did you maximize your contribution to your healthcare HSA? The interest and earnings in this account are tax free! The maximum contribution for 2015 is $3,350 for an individual and $6,650 for a family ($1,000 catch-up over 55). The contributions are tax deductible and withdraws are non-taxable if they are used for medical expenses. Over the age of 65 you can withdraw funds at your ordinary tax rate (if the distribution is not used for unreimbursed medical expenses). Fidelity estimates that a 65-year-old couple retiring in 2014 will need $220,000 for health care costs in retirement, in addition to expenses covered by Medicare. The HSA can be a great source of tax-free money to pay those bills.

8. Required Minimum Distribution If you are age 70.5 or older, remember to take your required minimum distribution to avoid a potential 50% penalty.

9. 529 Plan Did you contribute to your 529 educational plan for your child/children? You can contribute $14,000 per year (annual limit) for each parent or you can pre-fund in a single instance up to five years’ worth of contributions, up to $70,000 (5 x $14,000). Together, that means a married couple can open a 529 plan with $140,000. Money saved in a 529 plan grows tax-free when used for eligible educational expenses, and some states have additional tax benefits for residents who contribute to a plan in that state.

10. Determine your net worth Add up what you own (home, car, savings, investments…) and subtract what you owe (mortgage, loans, credit cards, …). This will allow you to track your progress year to year. It may also give you some incentive to save more and create a better budget for next year.

11. Check your credit score Go to annualcreditreport.com and request a free credit report from each of the three nationwide credit reporting agencies. You’re entitled to one free report from each agency every 12 months.

12. Check your beneficiaries You can check the beneficiaries on your retirement accounts or insurance policies at any time, but it’s a good idea to do this at least annually.

13. Update your estate plan New baby? Newly married or divorced? Make sure your beneficiary designations reflect any changes. Don’t yet have an estate plan? Make that a new year’s resolution! Estate planning may include updating or establishing a “will” or trust that can help avoid public disclosure of assets in probate.

14. Spending and automated savings – You want to look ahead Did you review your budget and set up automated savings? You may have started the year with a clear budget, but did you to stick to it? Fall can be a good time of the year for your financial checkup and to reflect on your spending and develop a budget for next year. It is also a very good time to put whatever you can on automatic. Bills, recurring payments, even savings—the more you can put on auto pay now, the easier your financial life will be next year. With this year’s facts and figures in front of you, it will be easier to plan and prioritize your expenditures for next year.

Assessment

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Experts Invited, Insurance Matters, Investing, Portfolio Management | Tagged: 2015 Year-End Financial Checklist, Financial Planning, Investing, Patrick Bourbon CFA | Leave a comment »

![]()

And, the Bureau of Labor Statistics (BLS) said …

By Arthur Chalekian GEPC

[Financial Consultant]

U.S. job growth surpassed expectations in October. About 271,000 jobs were created across diverse industries: professional and business services, health care, retail, construction, and others. That was a significantly higher number than predicted by economists who participated in a survey conducted by The Wall Street Journal. They expected to see 183,000 new jobs for October.

BLS revised

The BLS revised August and September jobs numbers higher overall and reported improvement on the wage front, too. Average hourly earnings increased by nine cents during October. For the year, hourly earnings are up 2.5 percent. Rising wages and a 5 percent unemployment rate “appear to indicate the labor market has reached full employment,” reported Barron’s.

Strong employment data supports the idea the Fed will begin to lift the Fed funds rate this year. On Friday, former Chairman of the Federal Reserve Ben Bernanke wrote in his blog:

“Wednesday was something of a trifecta for Fed watchers: Chair Yellen, Board Vice-Chair Stanley Fischer, and Federal Reserve Bank of New York president Bill Dudley (who is also the vice chair of the Federal Open Market Committee) all made public appearances. Moreover, the comments by all three members of the Fed’s leadership explicitly or implicitly supported the idea that a December rate increase by the FOMC is a distinct possibility. (The possibility of a rate increase is even more distinct with this morning’s strong job market report.)”

Markets responded swiftly, according to The Wall Street Journal, as investors repositioned their portfolios in anticipation of a rate hike. While stock market indices remained relatively steady, there was considerable volatility within certain sectors. An expert cited by the publication commented:

“…one of the big rotation trades on Friday was investors taking money out of companies such as utilities and real-estate-investment trusts, and putting it into those that are expected to benefit from higher rates, such as financial companies.”

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

***

Filed under: Health Economics, Investing | Tagged: Arthur Chalekian, Ben Bernanke, Bill Dudley, BLS, Bureau of Labor Statistics, Federal Open Market Committee, FOMC, interest rates, Stanley Fischer | 2 Comments »

***

![]()

[Foreword Dr. Phillips MD JD MBA LLM] *** [Foreword Dr. Nash MD MBA FACP]

![]()

![]()

[Mike Stahl PhD MBA] *** [Foreword Dr.Mata MD CIS] *** [Dr. Getzen PhD]

***

***

Dr. David Edward Marcinko, editor-in-chief, is a next-generation apostle of Nobel Laureate Kenneth Joseph Arrow, PhD, as a health-care economist, insurance advisor, financial advisor, risk manager, and board-certified surgeon from Temple University in Philadelphia. In the past, he edited eight practice-management books, three medical textbooks and manuals in four languages, five financial planning yearbooks, dozens of interactive CD-ROMs, and three comprehensive health-care administration dictionaries. Internationally recognized for his clinical work, he is a distinguished visiting professor of surgery and a recipient of an honorary Bachelor of Medicine–Bachelor of Surgery (MBBS) degree from Marien Hospital in Aachen, Germany. He provides litigation support and expert witness testimony in state and federal court, with medical publications archived in the Library of Congress and the Library of Medicine at the National Institutes of Health.

***

Filed under: Book Reviews, Financial Planning, Health Economics, Health Insurance, Health Law & Policy, Healthcare Finance, iMBA, Information Technology, Insurance Matters, Investing, Portfolio Management, Practice Management, Retirement and Benefits, Taxation | Tagged: david marcinko, Financial Planning, Health Economics, Health Insurance, physician investing, Portfolio Management | 1 Comment »

![]()

Qualitatively and quantitatively intensive!

By Vitaliy N. Katsenelson CFA

Our investment process at IMA is both qualitatively and quantitatively intensive. Throughout the course of a year we look at hundreds of companies. Most of them receive only a cursory look – we don’t like the business, the valuation is too stretched, or we simply have no insight into the business. We usually glance at them and move on.

Our investment process at IMA is both qualitatively and quantitatively intensive. Throughout the course of a year we look at hundreds of companies. Most of them receive only a cursory look – we don’t like the business, the valuation is too stretched, or we simply have no insight into the business. We usually glance at them and move on.

But, if we really like the business and/or its valuation, we build a model. Often, just from a cursory look we know that the stock is not cheap enough, but if we really (really!) like the business we’ll invest the time to model it so we can understand it better and set a price at which we want to buy it (and then wait).

***

We build models

***

We build a lot of models. We built over a hundred models last year (we bought only a handful of stocks). Building models is important for us. Models help us to understand businesses better. They provide insights as to which metrics matter and which don’t. They allow us stress test the business: we don’t just look at the upside but spend a lot of times looking at the downside – we try to “kill” the business. We usually try to drill down to essential operating metrics. If it is a convenience store retailer, we’ll look into gallons of gas sold and profit per gallon. If it is a driller (see our Helmerich & Payne analysis), we look at utilization rates, rigs in service, average revenue per rig per day, etc.

***

In the past, when we owned Joseph A. Banks, a model helped us understand the impact maturation of its new stores had on same-store sales (PDF, see slide 49). Half of Joseph A. Banks stores were less than five years old, and their maturation drove significant same-store sales increase for years.

***

We looked at American Express before the crisis, which gave us insight into inflated profit margins of the financial sector, and thus we avoided for the most part the carnage in the financials. We thought American Express stock was not cheap enough at the time, but we learned that Amex’s high swipe-fee revenue provided an important buffer to help the company absorb significant loan losses. Amex could have withstood over 10% loan losses on its credit card portfolio and still have remained profitable. This insight gave us the confidence to buy Amex during the crisis.

***

***

Models are important because they help us remain rational. It is only the matter of time before a stock we own will “blow up” (or, in layman’s terms, decline). We can go back to our model and assess whether the decline is warranted. The model then gives us the confidence to make a rational (very key word) decision: buy more, do nothing, or sell.

***

Assessment

***

Models are frameworks that help us think about the businesses we analyze. We are always aware of John Maynard Keynes’ expression, “I’d rather be vaguely right than precisely wrong.” Models are not a panacea, but they are an important and often invaluable tool. However, models are only as good as their builders and the inputs to them.

***

ABOUT

Vitaliy N. Katsenelson, CFA, is Chief Investment Officer at Investment Management Associates in Denver, Colo. He is the author of Active Value Investing (Wiley 2007) and The Little Book of Sideways Markets (Wiley, 2010). His books have been translated into eight languages. Forbes called him – the new Benjamin Graham.

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Investing, Portfolio Management | Tagged: Helmerich & Payne analysis, Investing, Investment Management Associates, investment models, Vitaliy N. Katsenelson CFA | 1 Comment »

![]()

“Altitude Sickness,” or Value Asphyxiation?

[By Vitaliy N. Katsenelson CFA]

“Asphyxiation is a condition in which the body doesn’t receive enough oxygen.”

That’s how I started another column awhile back , in which I explained how the recent U.S. equity market highs have been creating “altitude sickness,” or value asphyxiation, for investors. If you look down from 30,000 feet, the market is trading at a significant premium to its average long-term valuation, especially if you normalize earnings for sky-high profit margins.

The Trench View

The view from the trenches is not much different. I spend a lot of time looking for new stocks, either by screen or by reading or talking to other value investors. We are all having a hard time finding many stocks of interest. In fact, we’ve been doing a lot more selling than buying.

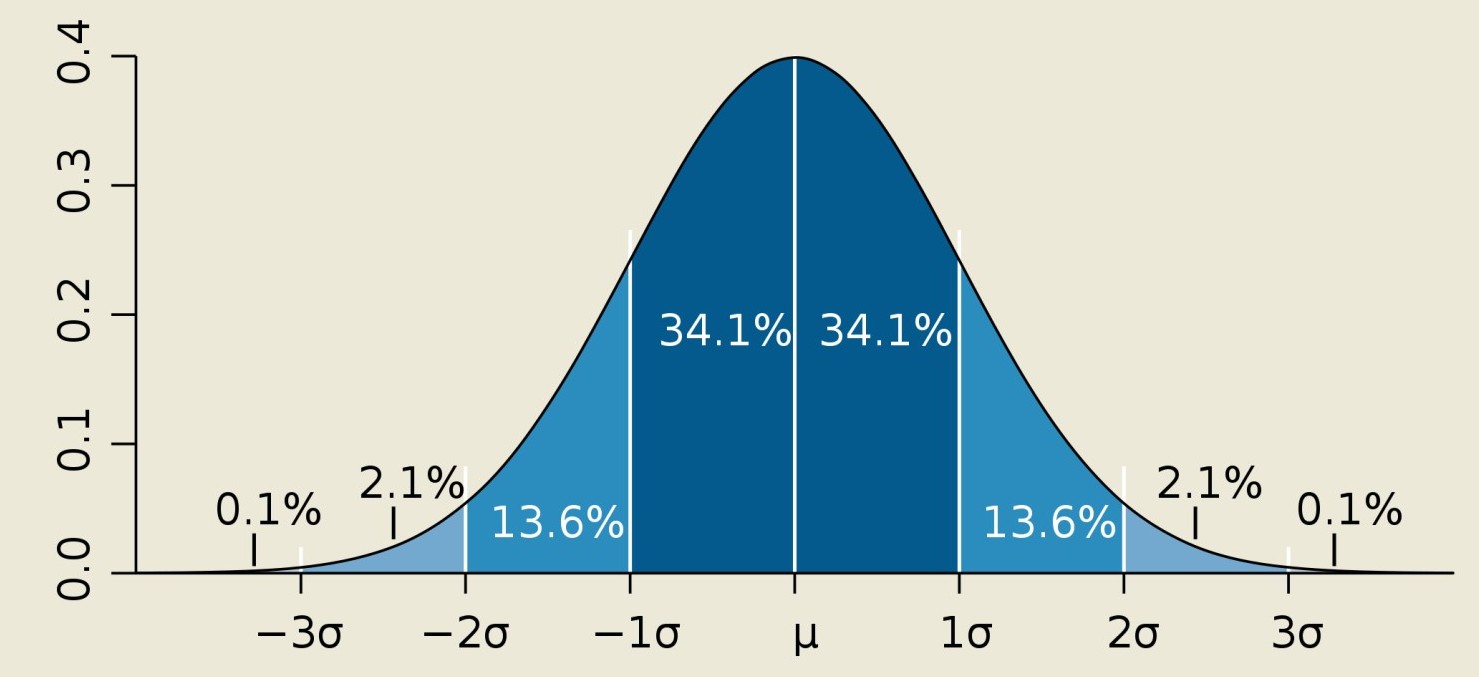

I often get asked a question: Are we in a bubble? Bubble is a word that has been thrown around a lot lately. There may be an academic definition of what a bubble is — probably something to do with valuations at least a few standard deviations from the mean — but I don’t really care what it is. (Only academics believe in normal distributions.)

The Practitioner’s View

From the practitioner’s perspective, a bubbly valuation occurs when the price-earnings ratio of a company is so high that its earnings will have a hard time growing into investors’ expectations. In other words, the stock is so expensive that investors holding it will find it difficult to realize a positive return for a long time (think of Cisco Systems, Microsoft and Sun Microsystems in 2000). There are some bubbly stocks in the market today. Most years you see some, but today there are probably a few more than usual.

We see a lot of overvalued or fully valued stocks. Expectations (valuations) of those stocks have already more than priced in rosy earnings growth scenarios. If these scenarios play out, investors will likely make very little money, as earnings growth will merely offset P/E compression. But here is where it gets interesting: The line between overvalued and bubbly stocks is often very murky. If the economy’s growth is lower than expected or corporate profit margins revert toward the mean (or, in the situation we have today, decline), the return profiles of these stocks will not be substantially different from those of the bubbly ones. Unfortunately for the value-asphyxiated investor, there are a lot of stocks that fall into this overvalued bucket.

It is very hard for investors to remain disciplined and stick to an investment process. Selling overvalued stocks is hard, because every sell decision brings consequent pain as overvalued stocks that are not aware you’ve sold them keep on marching higher. Just as Pavlov’s dog responded to a bell, the pain of selling teaches us not to sell.

More Pain

If that pain were not enough, cash keeps burning a hole in our portfolios. Cash doesn’t rise in value when everything else is rising; thus investors feel forced to buy. When you are forced into a buy or sell decision, the outcome will usually not be good. Forced buy decisions are usually bad buy decisions. Just because a stock looks less bad than the rest of the market doesn’t make it a good stock. Maybe its peer is trading at 23 times earnings and your pick is trading at “only” 19. Such relative logic is dangerous today, because it anchors you to a transitory environment that may or may not be there for you in the future (most likely not).

***

***

An Annoying Phase

We are in the most annoying phase of the investing calendar: the month when every market strategist and his dog have to make a prediction as to what the market will do next year. To be right in forecasting, you have to predict often. And market strategists do. In fact, they predict so often that no one remembers how often their predictions worked out. I am not knocking the prognosticators: That is their job. They predict and sound smart doing it — just like it’s the barber’s job to cut your hair and pretend he is concentrating on not cutting off your ear.

It is your job, however, not to pay attention to the predictors. They simply don’t know. They may have a gut feeling, but that feeling is worth as much as you pay for it — very little. To time the market, you have to forecast what the economy will do, which is also very difficult. The Fed has 450 economists working full time on that (half of them are Ph.D.s, but I am not going to hold it against them), and they have an amazingly poor track record. Then you have to figure out how other market participants will respond to the economics news — and that is incredibly difficult. Let’s say you nailed both of these tasks. You still need to predict the multitude of random events — a few of which may be very large black swans — that will show up in the next 12 months. There is a reason why they are called “random.”

Assessment

Though it is dangerous to drink the market’s Kool-Aid and celebrate, it is not time to be gloomy either. There is good news for all of us: Cyclical bull markets are here to absolve us from our “buy” sins. Not every stock in your portfolio is marching in rhythm to its fundamentals. Indeed, this market has lifted many stocks while divorcing them from their weak fundamentals. This absolution is temporary: Take advantage of it.

ABOUT

Vitaliy N. Katsenelson, CFA, is Chief Investment Officer at Investment Management Associates in Denver, Colo. He is the author of Active Value Investing (Wiley 2007) and The Little Book of Sideways Markets (Wiley, 2010). His books have been translated into eight languages. Forbes called him – the new Benjamin Graham.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Filed under: Investing, Portfolio Management | Tagged: Investing, market bubbles, value investors, Vitaliy N. Katsenelson | Leave a comment »

![]()

By Daniel J. Antokal MBA

By Daniel J. Antokal MBA

[Financial Advisor]

As the year draws to a close, there might be a slew of tasks on your to-do list. One task to consider is setting up a meeting with your financial professional to review your investments. If you take the time to get organized now, it may help you accomplish your long-term goals more efficiently.

Here are some steps that might help:

During the meeting with your financial professional, review how your overall investment portfolio fared over the past year and determine whether adjustments are needed to keep it on track.

Here are some questions to consider:

Addressing these issues might help you determine whether your investment strategy needs to change in the coming year.

During the portfolio review process, look at your current asset allocation among stocks, bonds, and cash alternatives. You might determine that one asset class has outperformed the others and now represents a larger proportion of your portfolio than desired. In this situation, you might want to rebalance your portfolio.

The process of rebalancing typically involves buying and selling securities to restore your portfolio to your targeted asset allocation based on your risk tolerance, investment objectives, and time frame. For example, you might sell some securities in an overweighted asset class and use the proceeds to purchase assets in an underweighted asset class; of course, this could result in a tax liability.

***

***

Tax losses

If you own taxable investments that have lost money, consider selling shares of losing securities before the end of the year to recognize a tax loss on your tax return. Tax losses, in turn, could be used to offset any tax gains. When attempting to realize a tax loss, remember the wash sale rule, which applies when you sell a security at a loss and repurchase the same security within 30 days of the sale. When this happens, the loss is disallowed for tax purposes.

If you don’t want to sell any of your current investments but want to change your asset allocation over time, you might adjust future investment contributions so that more money is directed to the asset class you want to grow. Once your portfolio’s asset allocation reaches your desired balance, you can revert back to your previous strategy, if desired. Keep in mind that asset allocation and diversification do not guarantee a profit or protect against loss; they are methods used to help manage investment risk.

Your financial professional can help you understand how your investments may be affected by capital gains and other taxes. You can learn more about current tax laws and rates by visiting www.irs.gov.

After your year-end investment review, you might resolve to increase contributions to an IRA, an employer-sponsored retirement plan, or a college fund next year. With a fresh perspective on where you stand, you may be able to make better choices next year, which could potentially benefit your investment portfolio over the long term.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

***

Filed under: Financial Planning, iMBA, Investing | Tagged: By Daniel J. Antokal MBA, Year-End Investment Planning | 1 Comment »

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

***

Filed under: Funding Basics, Investing, Portfolio Management | Tagged: Arthur Chalekian, Elite Financial Partners, European Central Bank, Mario Draghi, People's Bank of China | 2 Comments »

![]()

Our default brain operating system is programmed to make poor financial decisions?

By Rick Kahler MS CFP® http://www.KahlerFinancial.com

By Rick Kahler MS CFP® http://www.KahlerFinancial.com

If you’ve ever struggled to learn new software or unravel a computer problem, you know that part of the frustration of dealing with technology is its logic. Computers respond according to their default operating systems. If we want them to do something different, they need to be reprogrammed.

In the same way, the default operating systems of our brains are actually programmed to make poor financial decisions. This is normal. Making good financial decisions actually takes a deliberate reprogramming of your internal operating system. Here is why.

Our brains are divided into three sections: the reptilian brain, the mammalian brain, and the prefrontal cortex.

The reptilian brain is the oldest, most primitive part. In a talk at the Financial Therapy Association’s annual conference in July 2015 in San Jose del Cabo, Mexico, Dr. Ted Klontz explained that the reptilian brain continually scans for threats. It is waiting for death to come walking through the doorway, so it lives in anxiety. Since anything positive is not a threat, it’s oblivious to the positive. It also doesn’t understand the concept of the future, but lives only in this moment.

Left to its own programming, then, of course the reptilian brain might have a problem making monthly contributions to a retirement account. Saving for the future isn’t a concept it even understands. Further, it sees taking money out of the checkbook as a threat because that leaves fewer resources to battle death when it comes through the doorway. Making things even worse, the reptilian brain is nearly impossible to change. The best most of us can do is manage it.

***

***

This brings us to the mammalian brain, whose only job is to manage the anxiety of the reptilian brain. It does so in three ways:

Most of us favor one of these three responses to threats, and according to Dr. Klontz we select our preferred response by the age of six. When the mammalian brain responds, it processes exponentially faster than the thinking part of our brain, the prefrontal cortex. Because of the ease with which the mammalian brain responds to threats, 90% of all decisions—including financial ones—are made here.

With the mammalian brain managing the anxiety of the reptilian brain, we have a more sophisticated response to our potential retirement plan contribution. Some of us will verbally fight and defeat any messenger (article, employer, financial advisor, spouse) that suggests we drain our current resources to send money into a black hole. Others will simply flee the messenger by diverting our attention to the Monday night football game or any task at hand. A portion of us will just freeze into a glassy-eyed stare. Nobody is home.

That leaves us with our only hope, the understanding and thinking part of the brain, the prefrontal cortex. This part of our brain doesn’t fully come on line until the mid-twenties. It functions as the parent of the other two brains, but unfortunately it processes information very slowly and with great effort.

***

***

More:

Assessment

Fortunately, this is the brain that is easiest to change. By training it to become aware when the lower parts of the brain are about to make a hair-trigger decision, we can stop the ensuing action long enough to add logic as well as emotion to the process.

More:

Reprogramming the brain takes time, practice, and using resources like education, mentors, advisors, and counseling. Eventually, wise financial choices like saving for retirement can become the new default programming, even in spite of the reptilian brain.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

***

Filed under: Investing, LifeStyle | Tagged: behavioral economics, behavioral finance, Emotional Intelligence, EQ, IQ, Rick Kahler CFP®, Ted Klontz | 1 Comment »

|

||||||||

|

Filed under: Book Reviews, Investing, Portfolio Management, Videos | Tagged: Buffett, CFA Institute, Dr. David Marcinko, Education of a Value Investor, Guy Spier, Mohnish Pabrai, Munger, value investing, Vitaliy N. Katsenelson CFA | 1 Comment »

![]()

A Motley Fool Interview

ABOUT

Vitaliy N. Katsenelson CFA is Chief Investment Officer at Investment Management Associates in Denver, Colo. He is the author of Active Value Investing (Wiley 2007) and The Little Book of Sideways Markets (Wiley, 2010). His books were translated into eight languages. Forbes Magazine called him “The new Benjamin Graham”.

|

Filed under: Investing | Tagged: Forbes, James Early, Motley Fool, stock price, value investing, Vitaliy N. Katsenelson | 1 Comment »

It’s already priced into the markets … according to some experts!

By Arthur Chalekian GEPC [Elite Financial Partners]

The Markets UPDATE

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Filed under: Investing | Tagged: Arthur Chalekian GEPC, Barron's, contrarian investors, Elite Financial Partners, market emotions | 2 Comments »

![]()

[Staff reporters]

According to NEIL IRWIN; it is the 82-Year-Old Banking Law That Stirred a Debate!

What is the Glass-Steagall Act [Banking Act of 1933]?

When people talk about banking, they are talking about two broad classes of activities.

Commercial banking is what happens at your neighborhood branch: You deposit money in a checking or savings account, and the bank uses those deposits to make loans to consumers or small businesses.

Investment banking refers to the kind of banking activity more common on Wall Street, like helping large companies issue stock or bonds in order to fund themselves, and trading securities in hope of making a profit.

The government’s response was the Banking Act of 1933, commonly known as the Glass-Steagall Act (for the bill’s sponsors, Senator Carter Glass of Virginia and Representative Henry Steagall of Alabama), which required that commercial banking and securities activities be separated, not to take place within the same financial institution.

More: The Three Types of Banks

***

***

More:

Assessment

So, here is a look at why the Democratic presidential candidates Bernie Sanders and Martin O’Malley want to reinstate it.

TERMS: Investment Banking DR. MARCINKO

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

***

Filed under: Investing | Tagged: Banking Act of 1933, Commercial banking, Glass Steagall Act, INVESTMENT BANKING | 1 Comment »

By Arthur Chalekian GEPC

[Financial Consultant]

***

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

8

***

Filed under: Investing | Tagged: Arthur Chalekian, Investing | 1 Comment »

By Arthur Chalekian GEPC

[Financial Consultant]

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Investing, Portfolio Management | Tagged: Arthur Chalekian, Business Standard, FOMC, Investing, Portfolio Management, Shenzhen Stock Exchange Composite Index | 3 Comments »

![]()

Linear thinking is dangerous

[By Vitaliy Katsenelson, CFA]

Linear thinking is dangerous. It is the easiest form of reasoning, lying on the path of least resistance. The simpler the path, the more readily people will march along it. Linear arguments are easy to make, as they require the least amount of evidence — past data points with a straight line drawn through them.However, the larger the crowd that follows the wrong line of reasoning, the more people pile in, and the greater the consequences if they are proved wrong.

A lot of things in nature, and thus in investing, are not linear. A past trend may or may not persist into the future. Events don’t happen in a vacuum; they are observed, studied and capitalized on — which in the case of investing may preclude a company’s future from resembling its past. As I write this, I think of successful companies whose achievements attracted competition, which then marginalized them.

Some things are inherently nonlinear, their behavior reminiscent of a pendulum’s: The further they swing in one direction, the harder they’ll go in the opposite direction. It is very dangerous to default to linearity with such nonlinear phenomena, as the more confident we become in the swing (the more linearity we observe), the closer we are to the pendulum’s reversing course.

Price-earnings ratios often follow a pendulum behavior. If you look at high-quality dividend-paying stocks — the Coca-Colas and Procter & Gambles of the world — they are now changing hands at more than 20 times earnings. Their recent performance has driven linear thinkers to pile into them, expecting more of the same in the future. Don’t! These stocks were beneficiaries of a swing in the P/E pendulum as it went from low to average and then to above-average levels.

Pattern recognition is an important contributor to success in investing. Mark Twain once said that history doesn’t repeat itself, but it rhymes. If you can identify a rhyme (that is, see a pattern) relating to the current situation, then you can develop a framework to analyze and forecast it. But what if the current situation is very different — if it doesn’t rhyme with anything in the past? This is where the ability to draw parallels becomes helpful. It allows you to overlay rhymes (patterns) from other companies, industries or even fields. Building analogous frameworks is a cure for linear thinking; it helps us see nonlinearity and facilitates the creation of nonlinear mental models.

Then there is pseudolinearity: things that seem to be linear but are forced into linearity by extrinsic factors. This was a subtopic of my presentation at the Valuex Vail investing conference in June. I drew a parallel between two entities that suddenly looked analogous: Jos. A. Bank Clothiers, a Hampstead, Maryland–based retailer of men’s apparel, and the Federal Reserve.

***

***

Jos. A. Bank

Jos. A. Bank has always been a very promotional retailer. It would jack up prices, then run sales for consumers happy to be deceived — a typical American retail tale. But sometime in 2008, Jos. A. Bank went promotional on steroids. You could not watch CNBC for an hour without seeing one of its ads. The company started out by encouraging you to buy one suit and get one free. Then you got two free suits. Finally, it started giving away Android phones with suit purchases. For a while this past March, Jos. A. Bank offered consumers the opportunity to buy one suit and get three free.

There are several problems with the strategy: It does not emphasize the quality of the suits or the company’s great service, and the ads aren’t helping to build a brand but are intended just to pimp sales at Jos. A. Bank, as if it were a grocery store with USDA choice beef on sale.

This brings us to the latest quarter. Jos. A. Bank’s same-store sales dropped 8 percent, but what really piqued my interest was this explanation by its CEO, R. Neal Black, during its earnings call in June: “Since 2008, at the beginning of the financial crisis and the recession, the overall sales picture has been one of volatility, and strong promotional activity has been consistently and effectively driving our sales increases. This strategy was designed with 18 to 24 months of effectiveness in mind, and we stuck with it for more than 60 months since — as the economy remained weak. Now the strategy has become less effective.”

What Jos. A. Bank has really been doing since the financial crisis is running its own version of quantitative easing. The company had a temporary strategy that was supposed to get people into its stores during the recession — much like the Fed’s original QE, which was designed to provide liquidity in a time of crisis — but the recovery that ensued was not to Jos. A. Bank’s liking. So just as the Fed implemented QE2, and then QE3 when the economy did not improve to its satisfaction, the retailer followed with more QE.

It is understandable why Jos. A. Bank’s management did what it did. The company was being responsible to its employees — it didn’t want to close stores or have layoffs — and it had to report quarterly to shareholders. The focus shifted from building a long-term sustainable franchise to using short-term measures to grow earnings the next quarter and the quarter after that.

There are many lessons that one can draw from the parallels between Jos. A. Bank’s behavior and the Fed’s handling of our economy. First, it is very hard to challenge someone who has a linear argument. Let’s say that a year ago you talked to Jos. A. Bank’s management and raised the question of the sustainability of their advertising strategy. They’d have pointed to four years of success, and they’d have been right, at least up to that moment. They would have had four years of data points and a bulletproof linear argument, and you would have had your common sense and little else.

***

***

Ben Bernanke

Right now Ben Bernanke looks like a genius. He can show you all the data points in the recovery, but so could Jos. A. Bank, and this leads us to a second lesson: Pain is postponable, but it is cumulative. During Jos. A. Bank’s quarterly call, its CEO also said: “The decline in traffic is because existing customers are returning slightly less frequently. . . . It makes sense when you consider the saturating effect of our intense promotional activity over the past several years.”

With every sale Jos. A. Bank stole its future purchases, because when you buy one suit and get three for free, you may not need to buy another one for a while.But there is also a snowball effect that you cannot ignore: Every ad chipped away at the company’s brand. Now when you show someone that you wear a Jos. A. Bank suit, they don’t think about its quality, just that you have two or three more suits in your closet.

There is a cost to our recovery — a bloated Federal Reserve balance sheet and our addiction to low interest rates. Of course, we spread that addiction globally.

According to Hugh Hendry, founding partner and CIO of London-based hedge fund firm Eclectica Asset Management, rising U.S. bond yields have driven global yields higher. “In Brazil for instance, the biggest emerging debt market, no company has been able to raise debt abroad since mid-May as borrowing costs soared to a four-year high in June, at 7.1 percent,” he wrote in a recent investment letter.

The Fed is betting on George Soros’ theory of reflexivity, in which people’s biases and actions can change the economy: Instead of the wagon being towed by the horse, the wagon, in expectation that it will be towed by the horse, starts moving on its own, thereby motivating the horse to start towing the wagon.Lower interest rates drive people to riskier assets, and as asset values go up, people feel confident and spend money, and the economy grows. But this policy puts us on very shaky ground, because reflexivity cuts both ways: If asset prices start to decline, confidence declines — and so will the economy. Now there are a lot more savers owning riskier assets than they otherwise would have, and their wealth is at risk of getting wiped out.

The third lesson from the parallels between the Fed and Jos. A. Bank: We are in the midst of a game of musical chairs, and when the music stops, no one wants to be left standing around holding risky assets. Everyone is focused on the Fed’s tapering, and they are right to do so. Just as we saw with Jos. A. Bank, economic promotions cannot go on forever. With every sale the company had to increase the ante, giving away more and more to get people to come into its stores. The Fed may continue to buy Treasuries and mortgage securities, but the purchases will be less and less effective. And the music may stop on its own, without the Fed doing anything about it.

Last, pseudolinearity eventually leads to high uncertainty and thus lower valuations. Put yourself in the shoes of an investor analyzing Jos. A. Bank today. Before buying the stock, you’d have to answer the following questions: What is the company’s earnings power? How much did its promotional strategy damage the brand? And how much in future sales did that strategy steal?

Assessment

In the wake of Jos. A. Bank’s own five-year, nonstop version of QE, it is difficult to answer these questions with confidence. The company’s earnings power is uncertain, and investors will be willing to pay less for a dollar of uncertain earnings, thus resulting in a lower P/E. At some point, when U.S. economic activity weakens, investors will have to answer similar questions about the U.S. and global economies. And as they look for answers, they’ll be putting a lower P/E on U.S. stocks.

ABOUT

Vitaliy N. Katsenelson CFA is Chief Investment Officer at Investment Management Associates in Denver, Colo. He is the author of Active Value Investing (Wiley 2007) and The Little Book of Sideways Markets (Wiley, 2010). His books were translated into eight languages. Forbes Magazine called him “The new Benjamin Graham”.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

“The informed voice of a new generation of fiduciary advisors for healthcare”

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Alternative Investments, Investing, Op-Editorials | Tagged: Ben Bernanke, Federal Reserve, FOMC, George Soros, Jos. A. Bank, Linear thinking, Quantitative Easing, R. Neal Black, Vitaliy Katsenelson | 1 Comment »

![]()

Balancing profits, people and the planet

By Rick Kahler MS CFP® http://www.KahlerFinancial.com

Balancing profits, people, and the planet can be tricky. Many physicians and other investors prefer to put their funds into companies that not only make money, but that also reflect the investors’ values. Some take this concept, often described as “socially conscious” or “socially responsible” investing, very seriously. There are also financial advisors who specialize in this niche.

Yet investing in companies whose values align with your own is not as simple as it may seem.

Business owners and corporate executives

In my experience with business owners and corporate executives, most of them take an interest in bettering the people who work with them, the planet, and their own lives. They run their companies with integrity. They don’t break the law. They respect their customers and don’t take advantage of them, but give them fair value in exchange for their money. They offer compensation and working conditions that will attract and retain good employees. Ultimately, they understand that ethical business practices are not only the right thing to do, but the best way to run profitable businesses.

But, how do you as an investor know whether a company is bettering people and the planet while it is making a profit? One method is to choose companies in which to invest by using some type of socially responsible screening. Such screening looks to exclude companies producing products that harm people or the earth, or companies judged to have poor corporate cultures.

The challenges

One challenge with using such screens is that we don’t all have the same definitions of what may be socially or morally offensive. Investor A may not want to own stock in oil or mining companies. Investor B may be concerned about goods produced in unsafe working conditions. Investor C may not want to support companies that sell tobacco or alcohol.

A second challenge is that companies change. They may expand, diversify, or merge with other companies until it’s difficult to pinpoint their values, products, and company culture. A company may sell a lot of great products that do a lot of good for people, but have one division that produces a product some investors may find offensive. And it’s even harder to screen for companies that have good cultures—especially since there’s no clear definition of a “good” culture.

Choices

Investors can choose mutual funds that include only socially responsible companies, but any such fund is almost guaranteed to include companies that you would otherwise exclude.

If you are serious about investing only in companies that support your values, it’s essential to research them before you invest and monitor them regularly to ensure their practices or products don’t change. You also may find it necessary to give companies or SRI funds a little leeway—settling for perhaps 95% compliance with your values rather than insisting on 100%.

But sadly, even if you could invest your money in the shares of companies that totally support your values, doing so may not have much impact on that company, its people, or the planet. One reason for this is that your investment is likely to be a miniscule fraction of the company’s stock.

In addition, most often when we invest in stocks, we do not buy shares directly from the company. We buy shares, through a stock exchange, that are being sold by other investors. The profits or losses involved in trading those stocks accrue to the third-party buyers and sellers. They don’t directly affect the company’s bottom line.

***

***

Assessment

For most small investors, making a difference through socially responsible investing may be an illusory goal. Its only real impact may be to help us feel better about ourselves.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

“The informed voice of a new generation of fiduciary advisors for healthcare”

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Ethics, Investing | Tagged: rick kahler, Socially Responsible Investing | 3 Comments »

DJIA: 16,330.47 -179.72 -1.09% What to watch The Federal Reserve [FOMC] announced last week that it will leave the federal funds rate unchanged. Unease concerning the domestic implications of international weakness, particularly with regard to inflation, contributed to the Fed’s decision to delay changing its policy right now. Why it’s important The Fed’s decision to stay put indicates that policymakers are not as “reasonably confident” that inflation is heading towards their target of 2% as they’d like to be. For example, Core Inflation [CI], one key economic measure the Fed is watching, is heading into a third year of running below the Fed’s long-run 2% target rate. While the labor market portion of the Fed’s dual mandate appears in good shape, in part indicated by an unemployment rate within their estimate of full employment, policymakers decided to postpone a decision to raise their policy rate for the first time in nearly a decade, citing concerns around the impact that global economic and financial developments could have on domestic conditions. ****

**** Assessment According to the Vanguard Group, despite the attention given to the timing of when the Fed starts raising rate, some believe the more important questions are how quickly rates will go up and where they stop. Whether liftoff happens in the coming months or even next year, we expect the Fed to make more measured, staggered rate increases than in previous tightening cycles, especially given the fragility in global economic growth. This “dovish tightening” will gradually normalize policy in a global environment not yet ready for a positive real fed funds rate. |

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: iMBA, Investing, Portfolio Management | Tagged: Core Inflation, Federal Reserve, global economic environment, US economy, Vanguard’s Investment Strategy Group | 12 Comments »

![]()

On changing monetary policy

By Arthur Chalekian, GEPC

[Financial Consultant – Elite Financial Partners]

Economic Growth

It’s safe to say many people – like doctors ad medical professionals – are worried about whether economic growth – in the United States and abroad – will be stifled by changing monetary policy in the United States. As a result, all eyes have been on the Federal Reserve, which is expected to begin raising the Fed funds rates sometime soon. But, it didn’t happen on 9/17/15.

However, the Federal Reserve’s monetary policy isn’t the only game in town. Fiscal policy – the actions taken by our government – can also have a profound effect on economic growth. A July Brookings’ blog post ‘Fiscal Headwinds are Abating,’ reported:

“Tight fiscal policy by local, state, and federal governments held down economic growth for more than four years, but that restraint finally appears to be over….Fiscal policy is no longer a source of contraction for the economy, but neither is it a source of strength.”

The blog post discusses the reasons that government spending has held back economic growth. At the federal level, contraction was attributed to “… tight caps on annually appropriated spending and the automatic spending cuts known as sequestration.” The organization’s Federal Impact Measure (FIM), which estimates the effect of federal, state, and local spending (and taxes) on gross domestic product growth, suggests federal spending caused economic growth to be 0.35 percentage points lower per year, on average, between 2011 and 2013.

There is talk of a government shutdown at the end of September. If it happens, it could have an effect on economic growth. The last time the government shut down was in 2013. Experts cited by the BBC reported the 2013 shutdown cost the U.S. economy about $24 billion and reduced quarterly economic growth by 0.6 percent. That shutdown lasted 16 days.

***

***

Assessment

It is possible economic growth may slow for some period of time. It’s also possible monetary policy, fiscal policy, and other factors may be responsible.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Investing | Tagged: Arthur Chalekian, Federal Impact Measure, monetary policy | 1 Comment »

|

|

“Asphyxiation is a condition in which the body doesn’t receive enough oxygen.”

That’s how I started a column a while back, in which I explained how the recent U.S. equity market highs have been creating “altitude sickness,” or value asphyxiation, for investors. If you look down from 30,000 feet, the market is trading at a significant premium to its average long-term valuation, especially if you normalize earnings for sky-high profit margins.

The view from the trenches is not much different. I spend a lot of time looking for new stocks, either by screen or by reading or talking to other value investors. We are all having a hard time finding many stocks of interest. In fact, we’ve been doing a lot more selling than buying.

A Bubble?

I often get asked a question: Are we in a bubble? Bubble is a word that has been thrown around a lot lately. There may be an academic definition of what a bubble is — probably something to do with valuations at least a few standard deviations from the mean — but I don’t really care what it is. (Only academics believe in normal distributions.)

From the practitioner’s perspective, a bubbly valuation occurs when the price-earnings ratio of a company is so high that its earnings will have a hard time growing into investors’ expectations. In other words, the stock is so expensive that investors holding it will find it difficult to realize a positive return for a long time (think of Cisco Systems, Microsoft and Sun Microsystems in 2000). There are some bubbly stocks in the market today. Most years you see some, but today there are probably a few more than usual.

A murky line

We see a lot of overvalued or fully valued stocks. Expectations (valuations) of those stocks have already more than priced in rosy earnings growth scenarios. If these scenarios play out, investors will likely make very little money, as earnings growth will merely offset P/E compression. But, here is where it gets interesting: The line between overvalued and bubbly stocks is often very murky. If the economy’s growth is lower than expected or corporate profit margins revert toward the mean (or, in the situation we have today, decline), the return profiles of these stocks will not be substantially different from those of the bubbly ones. Unfortunately for the value-asphyxiated investor, there are a lot of stocks that fall into this overvalued bucket.

It is very hard for investors to remain disciplined and stick to an investment process. Selling overvalued stocks is hard, because every sell decision brings consequent pain as overvalued stocks that are not aware you’ve sold them keep on marching higher. Just as Pavlov’s dog responded to a bell, the pain of selling teaches us not to sell.

***

More pain

If that pain were not enough, cash keeps burning a hole in our portfolios. Cash doesn’t rise in value when everything else is rising; thus investors feel forced to buy. When you are forced into a buy or sell decision, the outcome will usually not be good. Forced buy decisions are usually bad buy decisions. Just because a stock looks less bad than the rest of the market doesn’t make it a good stock. Maybe its peer is trading at 23 times earnings and your pick is trading at “only” 19. Such relative logic is dangerous today, because it anchors you to a transitory environment that may or may not be there for you in the future (most likely not).

An annoying phase

We are in the most annoying phase of the investing calendar: the month when every market strategist and his dog have to make a prediction as to what the market will do next year. To be right in forecasting, you have to predict often. And market strategists do. In fact, they predict so often that no one remembers how often their predictions worked out. I am not knocking the prognosticators: That is their job. They predict and sound smart doing it — just like it’s the barber’s job to cut your hair and pretend he is concentrating on not cutting off your ear.

It is your job, however, not to pay attention to the predictors. They simply don’t know. They may have a gut feeling, but that feeling is worth as much as you pay for it — very little. To time the market, you have to forecast what the economy will do, which is also very difficult. The Fed has 450 economists working full time on that (half of them are Ph.D.s, but I am not going to hold it against them), and they have an amazingly poor track record. Then you have to figure out how other market participants will respond to the economics news — and that is incredibly difficult. Let’s say you nailed both of these tasks. You still need to predict the multitude of random events — a few of which may be very large black swans — that will show up in the next 12 months. There is a reason why they are called “random.”

Assessment

Though it is dangerous to drink the market’s Kool-Aid and celebrate, it is not time to be gloomy either. There is good news for all of us: Cyclical bull markets are here to absolve us from our “buy” sins. Not every stock in your portfolio is marching in rhythm to its fundamentals. Indeed, this market has lifted many stocks while divorcing them from their weak fundamentals. This absolution is temporary: Take advantage of it.

ABOUT

Vitaliy N. Katsenelson CFA is Chief Investment Officer at Investment Management Associates in Denver, Colo. He is the author of Active Value Investing (Wiley 2007) and The Little Book of Sideways Markets (Wiley, 2010). His books were translated into eight languages. Forbes Magazine called him “The new Benjamin Graham”.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Investing, Portfolio Management | Tagged: Cyclical bull markets, equity market highs, stock valuations, Vitaliy N. Katsenelson CFA | 1 Comment »

![]()

The Wall Street Journal Called

By Rick Kahler CFP® CLU MS http://www.KahlerFinancial.com

[FOMC Holds Steady Today]

A few weeks ago, when the US markets started dropping dramatically, a reporter for The Wall Street Journal called. He asked me if I had received any calls from worried clients. I told him I had heard from 5% of my clients. “What changes in their portfolios are you making?” he asked.

“I’m not making any changes to my investment strategy.”

He expressed amazement that I was not “doing something.” Most investors and their advisors he was speaking with were making “adjustments” to their portfolios. He told me I must have a “stomach of steel.”

Hardly. My gut is certainly not immune to those fearful sinking feelings that go along with market plunges. What I do have is enough experience to trust my long-term investment strategy.

The time most investors and advisors decide an investment strategy doesn’t work is when their portfolios lose value, usually due to a decline in US stocks. This confuses me.

Here’s why:

First, I’m confused that so many investors believe it’s possible to move in and out of markets in such a way that their portfolios will rarely, if ever, suffer a negative return.

This is magical or delusional thinking. The only investor I’m aware of who consistently produced positive returns, year after year, was a fellow by the name of Bernie Madoff. If you have never heard of this investment wizard, he’s the one who is now serving a life sentence in a federal prison for propagating a Ponzi scheme that robbed billions of dollars from investors.

Short-term or moderate-term losses are inevitable in any portfolio that seeks to earn returns above those offered by a bank Certificate of Deposit. Usually, in the long run, markets recover and so does your portfolio.

Sadly, too many investors turn short-term losses into long-term losses by abandoning their investment strategy when the US markets turn down. This locks in their losses, never to be recovered.

If your portfolio is widely diversified among many markets—like bonds, emerging markets, commodities, real estate, TIPs, and various investment strategies—you will almost always have an asset class losing money. You will also almost always have an asset class making money. If not, you probably don’t have a diversified portfolio.

Here’s the second reason I’m confused.

Most investment strategies assume that the US market will decline, and they have a strategy in place for dealing with those declines. For a buy-and-hold investor, the strategy is to do absolutely nothing. For a strategic asset allocator like myself, it’s to rebalance frequently by selling appreciating asset classes and buying into those in decline. By not making changes to clients’ portfolios during a market decline, I am not “doing nothing;” I am simply continuing to follow an investment strategy.

Because most of my clients have learned over time to trust this strategy, relatively few of them make panicky calls to my office during downturns. Yet I have noticed a direct correlation between US stock market declines and my daily phone call volume. Many of the calls are from reporters wanting to know what I am doing and am telling clients. My response—that I’m not doing anything different—is the same thing I told them when the markets last declined in 2011 and before that in 2009, 2008, 2002, 2001, 2000, 1997, etc.

***

***

Assessment

This isn’t the response an anxious client or a concerned reporter wants to hear. When the emotional center of the brain is overcome with panic and fear, taking action helps relieve anxiety. If that short-term action is selling into volatile stock markets, however, it often turns out to be a long-term mistake.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Investing, Portfolio Management | Tagged: rick kahler, Stock Market Volatility, The Wall Street Journal, volatile stock markets | 2 Comments »

![]()

By the Economic Policy Institute

EPI’s Family Budget Calculator measures the income a family needs in order to attain a secure yet modest standard of living in 618 areas across the country.

Compared with the federal poverty line, EPI’s family budgets provide a more accurate and complete measure of economic security in America.

These factsheets offer a full picture of what it costs to live in a given area and how family size affects these costs.

Assessment

So doctor – how does your budget rate relative to the above for this Labor Day Weekend?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Sponsors Welcomed: Credible sponsors and like-minded advertisers are always welcomed.

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

Filed under: Career Development, Investing | Tagged: Family Budgets | 1 Comment »

![]()

Why Invest … At all!

DJIA plummets 470 today!

By Lon Jefferies CFP MBA lon@networthadvice.com | http://www.networthadvice.com

Why do we invest in the stock market? To make money so we can improve our standard of living, right?

Why do we invest in the stock market? To make money so we can improve our standard of living, right?

Notice that we aren’t investing just to get our money back. If we simply wanted our money back, we would place the money in a savings account at a bank where we would likely be able to access it any time and know that we could redeem it at full value.

However, making money is better than simply getting our invested dollars back, so there has to be a trade off for receiving that additional benefit.

Market Corrections

Of course, the trade off is that investing in the market involves more risk than simply depositing money in a bank account. The additional return that is required by investors for investing in an asset that could potentially lose money is called the equity risk premium. There must be a potential downside in exchange for the larger reward that can be obtained by investing in the stock market. Otherwise, no one would ever deposit money into the more secure bank accounts and people would always invest in the stock market generating superior returns. Unfortunately, this would make things too easy, and as we have learned our whole lives, the easier a goal is the less reward we get for achieving that goal. That is why positions that can only be filled by a select few individuals with rare talents (CEOs, doctors, Lebron James) are handsomely compensated.

By now, most people know that over a sufficiently lengthy period of time, the stock market has historically produced returns of approximately 10% per year. This seems like a simple and easy way to make money, so why don’t all investors buy stocks and hold them for extended periods of time? The fact that we aren’t all rich suggests that buying stocks and allowing the market time to do its thing isn’t easy. This is because enduring risk and suffering losses creates negative emotions that get the best of many investors, causing them to sell at the wrong time and stop investing new dollars.

Yet, when we refer back to the concept that the tougher the task the greater the reward, we should be happy that buying and holding stocks isn’t easy because it makes the strategy more profitable.

For this reason, the next time the market goes through a correction or even a crash, wise investors should be grateful. Market volatility causes unsuccessful investors to sell when prices are down and increases the rewards for those who can stick with their investment strategy by holding their assets or even buying new positions.

***

***

Supply and Demand

Supply and demand suggests that when the markets are decreasing in value, more people are selling assets than buying. The people who are selling their investments at a loss create an equity risk premium for those who can endure market volatility. This increases the reward for successful investors by both providing an opportunity to buy assets when they are inexpensive, and reminding the marketplace that investing in volatile positions is unpleasant. Of course, things that are unpleasant aren’t easy to accomplish, which means there is a large benefit for achieving those things.

Thus, market corrections are great for successful investors because it is volatility and easily-rattled buy-and-sell investors that enable buy-and-hold investors to make significant profits over the long term. In fact, it wouldn’t be possible for stock market investors to make money without periodic intervals of unpleasantness as it is this discomfort which causes some investors to sell and creates an equity risk premium for the rest of us.

***

***

Great Fall of China

Until the Great Fall of China recently, it has been easy for investors to buy and hold for the last six years as the market has been nothing but accommodating since early 2009.

However, when things get too easy, it reduces our reward for being a long-term investor because everyone can do it. For this reason, we need the market to experience a correction at some point to shake out the unsuccessful investors, causing them to sell assets and create an equity risk premium once more.

Assessment

When the next correction occurs, you can either sell assets and create a risk premium for others, or you can stay invested and take advantage of the money unsuccessful investors leave on the table. Successful investors with a sufficiently lengthy investment time horizon remind themselves of this concept frequently so that when the market experiences a decline they aren’t overcome by fear but grateful for the opportunity provided by the short-sighted.