![]()

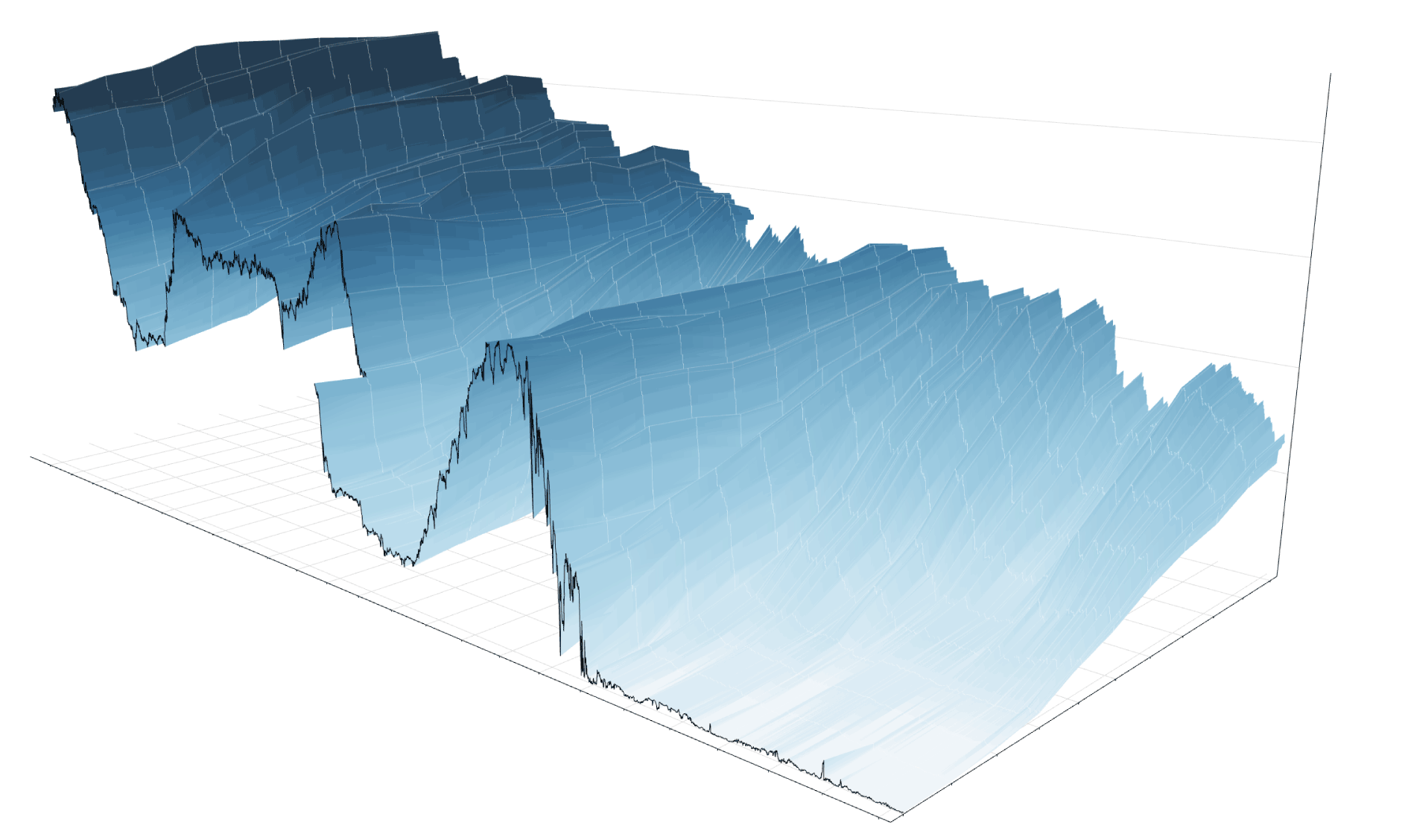

Yield Curve 101

[By GREGOR AISCH and AMANDA COX]

The yield curve shows how much it costs the federal government to borrow money for a given amount of time, revealing the relationship between long- and short-term interest rates.

It is, inherently, a forecast for what the economy holds in the future — how much inflation there will be, for example, and how healthy growth will be over the years ahead — all embodied in the price of money today, tomorrow and many years from now.

***

A 3-D View of a Chart That Predicts The Economic Future …

***

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Share this:

Filed under: Investing | Tagged: AMANDA COX, FOMC, GREGOR AISCH, inflation, long-and short-term interest rates, Yield Curve 101 |

Whither the Bear?

As a doctor, your action plan in a future bear market depends on many variables, with perhaps your age being the most important:

In your 30s:

• Pay off debts, school or practice loans.

• Invest in safe money market mutual funds, cash or CDs.

• Start retirement plan or 401-K account.

In your 40s:

• Increase your pension plan or 401-K contributions.

• Stay weighted more toward equity investments.

• Review your goals, risk tolerance and portfolio.

In your 50s:

• Position assets for ready cash instruments.

• Diversify into stock, bonds and cash.

Retirement:

• Maintain 3 years of ready cash living expenses.

• Reduce, but still maintain your exposure to equities.

Dr. David E. Marcinko MBA CMP™ MBBS [Hon]

http://www.CertifiedMedicalPlanner.org

LikeLike