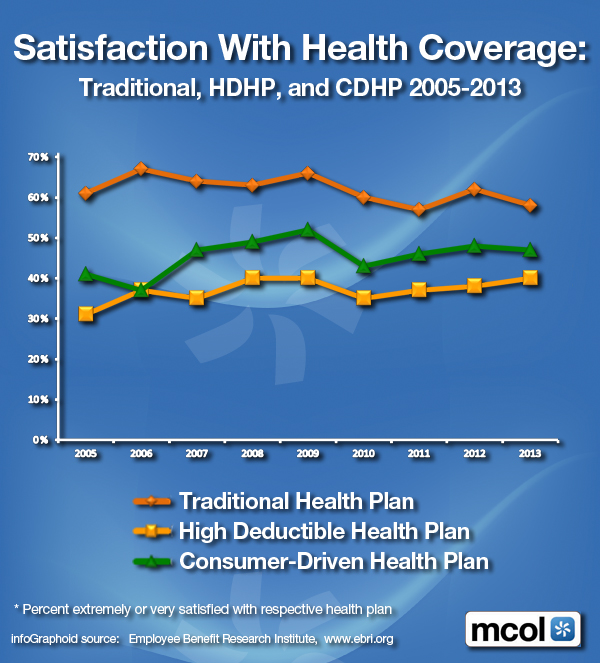

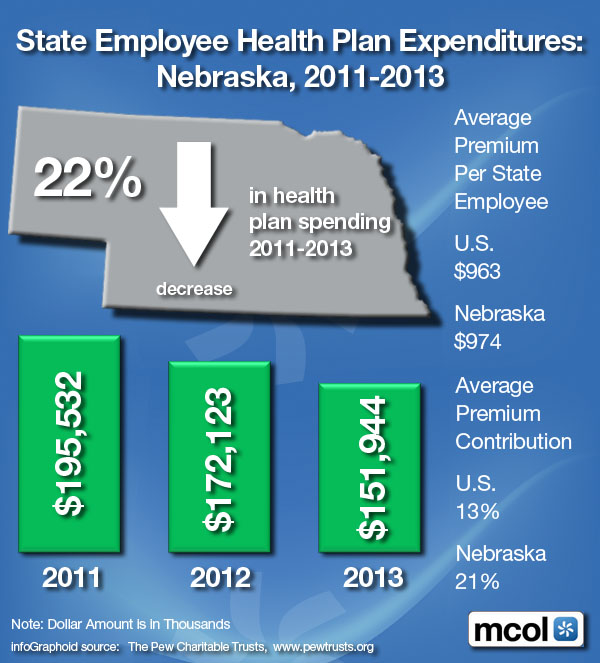

|

Share this:

Filed under: Health Economics, Health Insurance, Healthcare Finance | Tagged: ACA, Health Economics, Health Entitlements & the Deficit, Health Insurance, Nancy Chockley PhD, NIHCM.org, ObamaCare | 1 Comment »

ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

![]()

![]()

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

![]()

ePodiatryConsentForms.com

ePodiatryConsentForms.com

“Providing Management, Financial and Business Solutions for Modernity”

“Providing Management, Financial and Business Solutions for Modernity”

|

Filed under: Health Economics, Health Insurance, Healthcare Finance | Tagged: ACA, Health Economics, Health Entitlements & the Deficit, Health Insurance, Nancy Chockley PhD, NIHCM.org, ObamaCare | 1 Comment »

![]()

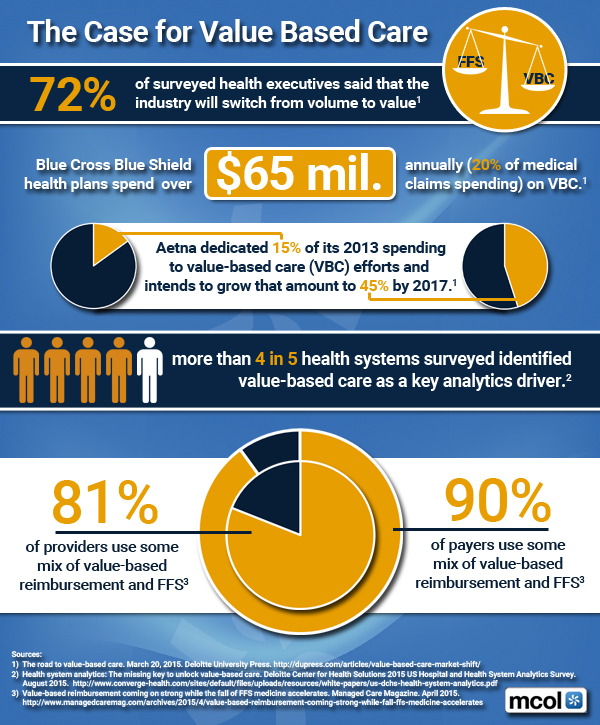

Migrating from Volume to … Value

***

***

Assessment

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

[Foreword Dr. Hashem MD PhD] *** [Foreword Dr. Silva MD MBA]

***

Filed under: Health Insurance, Quality Initiatives | Tagged: Value Based Medical Care | 5 Comments »

![]()

How do I compare my health insurance options during open enrollment?

Daniel J. Antokal MBA

[Financial Advisor]

The decisions you make during open enrollment season regarding health insurance are especially important, since you generally must stick with the options you choose until the next open enrollment season, unless you experience a “qualifying” event such as marriage or the birth of a child. As a result, you should take the time to carefully review the types of plans offered by your employer and consider all the costs associated with each plan.

With most health insurance plans, your employer will pay a portion of the premium and require you to pay the remainder through payroll deductions. When comparing different plans, keep in mind that even though a plan with a lower premium may seem like the most attractive option, it could have higher potential out-of-pocket costs.

You’ll want to review the copayments, deductibles, and coinsurance associated with each plan. This is an important step because these costs can greatly affect what you end up paying out-of-pocket.

When reviewing the costs of each plan, consider the following:

Specific features

You should also assess each plan’s coverage and specific features. For example, are there coverage exclusions or limitations that apply? Which expenses are fully or partially covered? Do you have the option to go to doctors who are outside your plan’s provider network? Does the plan offer additional types of coverage for vision, dental, or prescription drugs?

***

***

Assessment

In the end, when reviewing your options, you’ll want to balance the coverage and features offered under each plan against the plan’s overall cost to determine which plan offers you the best value for your money.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

***

Filed under: Health Insurance | Tagged: Daniel J. Antokal, Health Insurance, open enrollment | 1 Comment »

![]()

No … Really!

By Robert E.H. Khoo MD FRCS(C) FACS

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

***

Filed under: Health Insurance | Tagged: ACA, HealthCare.Gov, Robert E.H. Khoo MD | 3 Comments »

![]()

By Terri D. Wright, PhD, MPH

***

|

*** APHA’s Policy Center Creates Tools for A Healthy Future DEAR DAVID – The central challenge of the American Public Health Association is to create the healthiest nation in one generation. APHA’s Center for Public Health Policy was established almost 10 years ago to bring together analytical public health expertise and infuse the public health field with expert materials and tools in response to this challenge. The Center embraces the public health issues that threaten population health. Our work is done through national and state partnerships and by leveraging resources across multiple sectors, including government, philanthropy and non-profit. Fundamental to all that we do: strategies to ensure health equity for all. We invite you to learn about our work and stay abreast of our progress on producing resources for our members and constituents. The following priorities represent our core work to create a healthy nation:

We will keep you updated on our priority issues and encourage you to connect with our team. We invite your feedback as we embark on this journey – phpolicycenter@apha.org |

Sincerely, |

***

![]()

[Foreword Dr. Phillips MD JD MBA LLM] *** [Foreword Dr. Nash MD MBA FACP]

***

Filed under: Ethics, Health Insurance, Health Law & Policy, Research & Development | Tagged: APHA, APHA's Center for Public Health Policy, APHA’s Policy Center, Terri D. Wright PhD MPH, Tools for A Healthy Future | 1 Comment »

![]()

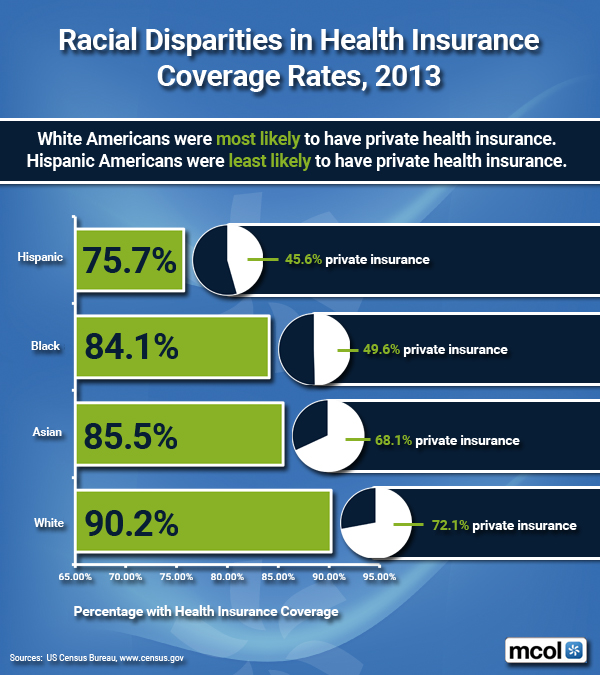

For 2013

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

[Mike Stahl PhD MBA] *** [Foreword Dr.Mata MD CIS] *** [Dr. Getzen PhD]

***

Filed under: Health Insurance, Research & Development | Tagged: health insurance coverage in minorities, health insurance minorities, racial disparities of health insurance, www.MCOL.com | Leave a comment »

![]()

A 2015 Snapshot for HSAs

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Career Development, Products and Services

“The informed voice of a new generation of fiduciary advisors for healthcare”

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Health Insurance | Tagged: Consumer Driven Healthcare Plans, health savings accounts, HSAs | 4 Comments »

![]()

By Individual State [June 30, 2015]

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

![]()

[Foreword Dr. Phillips MD JD MBA LLM] [Foreword Dr. Nash MD MBA FACP]

***

Filed under: Health Insurance, Healthcare Finance | Tagged: ACA subsidies, Health Insurance Exchanges, HIE Tax Credits Amounts, HIE's, ObamaCare, PP-ACA | 1 Comment »

![]()

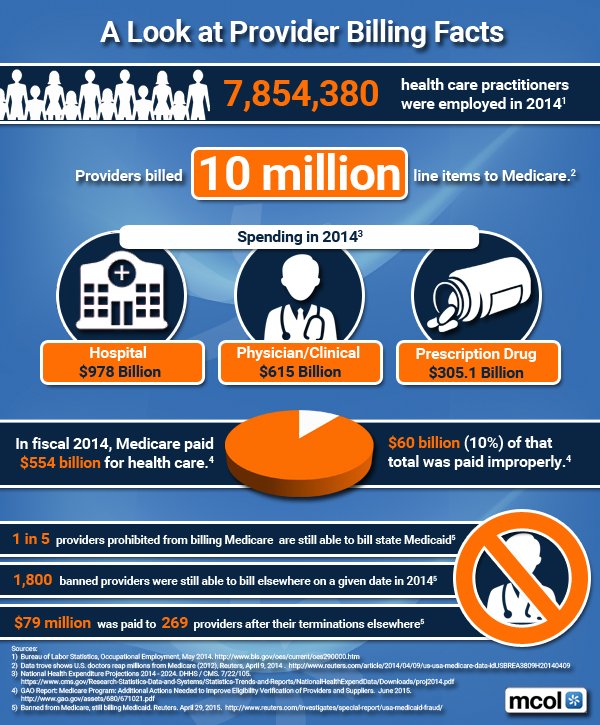

A Look at Medicare Spending

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

[Foreword Dr. Phillips MD JD MBA LLM] *** [Foreword Dr. Nash MD MBA FACP]

***

Filed under: Career Development, Ethics, Health Insurance, Risk Management | Tagged: CMS, Medical Provider Billing Facts, medicare, Medicare Provider Billing | 1 Comment »

![]()

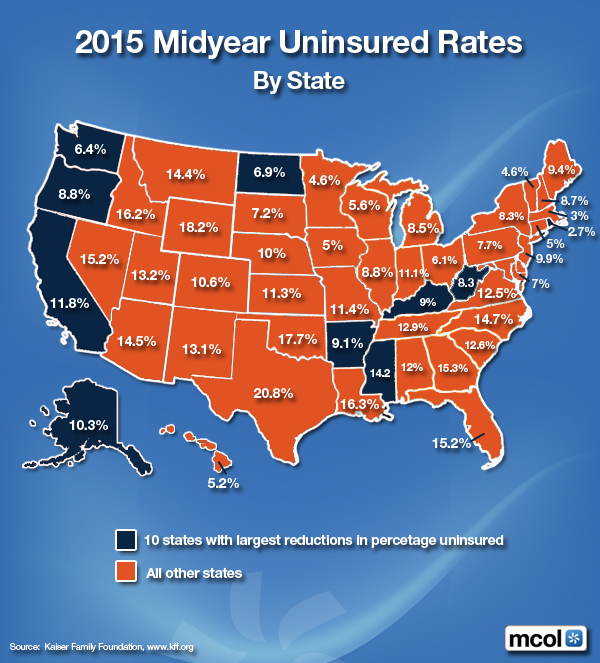

Health Insurance by US State

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

***

Filed under: Health Insurance | Tagged: 2015 Un-Insured Rates, Health Insurance | Leave a comment »

![]()

Transcripts and Slides

By Douglas B. Sherlock, CFA sherlock@sherlockco.com

By Douglas B. Sherlock, CFA sherlock@sherlockco.com

The Affordable Care Act is intended to create strong incentives to reduce the administrative costs of health insurers. The medical loss ratio rules and the new ACA-related taxes are manifestations of this policy, and the recent announced business combinations between leading national health insurers are adaptations to these incentives.

It follows that the most recent rate of increase in health plan administrative expenses, excluding the new taxes, is dramatically lower than in recent years. Sherlock Company materials summarizing the results of our surveys are found below.

Independent / Provider – Sponsored Plans

Blue Cross Blue Shield Plans

Assessment

The contents above are a very small portion of the 1,000 page Sherlock Benchmarks for each of these universes. The Sherlock Benchmarks are essential tools to manage administrative costs for your health plan.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

[Foreword Dr. Phillips MD JD MBA LLM] *** [Foreword Dr. Nash MD MBA FACP]

***

Filed under: Health Economics, Health Insurance, Healthcare Finance, Videos | Tagged: ACA, Affordable Care Act., Blue Cross Blue Shield, Douglas B. Sherlock, Medical Loss Ratio | 2 Comments »

![]()

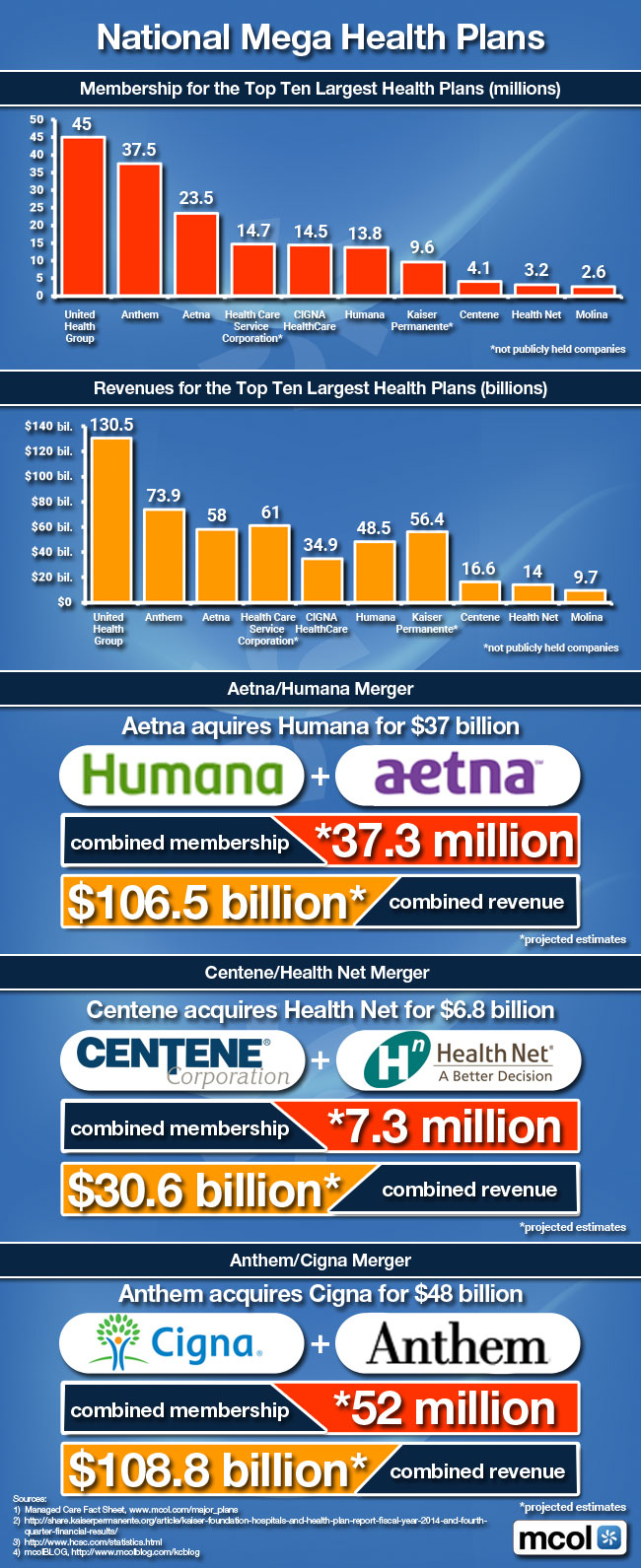

Membership Top 10 Largest Plans

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

[Mike Stahl PhD MBA] *** [Foreword Dr.Mata MD CIS] *** [Dr. Getzen PhD]

***

Filed under: Health Economics, Health Insurance, Health Law & Policy, Healthcare Finance, Information Technology | Tagged: National Mega Health Plans, Top 10 Largest Health Plans | Leave a comment »

![]()

A Site Re-Design

[By David Belk MD]

[By David Belk MD]

Here’s the new website with a whole new look that’s been redesigned by Modern Creations: http://truecostofhealthcare.org

There are three new sections:

The first is a study of the prices of brand name medications. It shows that the price pharmacies in the US pay for brand name drugs have gone up an average of 40% in 2 1/2 years. That’s about 18 times the rate of inflation.

The other two new pages examine Medicare supplemental policies as well as Part D and Advantage programs:

The page on supplemental policies is an expansion of the blog I wrote 2 years ago on the subject. It answers just about any question you might have about what Medicare covers and how much you would expect to pay if you have Medicare and need medical treatment

***

***

Assessment

Feel free to tell me what you think of it. Also, I’m sending this message from my new email address – truecostofhealthcare@gmail.com

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

“Navigating a course where sound organizational management is intertwined with financial acumen requires a strategy designed by subject-matter experts. Fortunately, Financial Management Strategies for Hospital and Healthcare Organizations: Tools, Techniques, Checklists and Case Studies provides that blueprint”

—David B. Nash MD MBA Jefferson Medical College, Thomas Jefferson University, PA

Filed under: Drugs and Pharma, Health Economics, Health Insurance, Healthcare Finance | Tagged: David B. Nash MD, David Belk MD, healthcare costs, medical inflation, medicare, truecostofhealthcare.org | 4 Comments »

![]()

Beating Medical Trends

[By William Rusteberg]

www.RiskManagers.us (click on WEBLOG)

Medical inflation continues to rise at a rate above the growth rate in the economy. Facing rate increases year after year, plan sponsors, with their financial backs to the wall, have historically resorted to cost shifting. These continued failed attempts to control costs have driven some to seek alternate means to restore pricing sanity to health care. To many, the cost of health insurance can mean the difference between profit and loss.

The Problem

Understanding the cost of health care is directly related to what we agree to pay, more and more employers are questioning managed care contracts upon which their health care costs are based. Many are discovering the truth for the first time. Secretive contracts between health care givers and third party intermediaries contain provisions that guarantee continuous and systematic cost increases. Shared savings side agreements and other schemes found in the health industry economic chain help fuel raging health insurance costs.

Known as medical trend, cost increases have proven to be consistent and predictable. The expected rise in the cost of medical services over time is expressed as an annual percentage increase and is an important element in underwriting future risk. Medical trend is a dominant cost driver in rate making. The annual compounding effect can double or triple health care costs in just a few years.

“For managed care plans, the medical care inflation part of trend is a function of the changes in provider reimbursement rates that are negotiated. To the extent that such negotiations entail factors such as outliers and provider bonuses, the trend rate may be materially more than simply the weighted average increase in fees.” Kevin Gabriel, MBA, FSA, MAAA, Chief Actuary of Sierra Berkshire Associates, Inc.

Photo of hands of businesspeople during discussing

The Solution

Moving away from managed care contracts, more and more employers are embracing a myriad of reference based pricing models. These models can vary in scope and reach; however all share certain common characteristics in conformance with prudent business practices. Price transparency and claim benchmarking are key elements.

In 2007 – 2008 we approached several of our clients to suggest something different to control costs. The concept was simple. Eschew managed care contracts in lieu of claim benchmarking off multiple data points such as Medicare reimbursement rates. Removing managed care contracts, i.e, PPO, and paying providers quickly, fairly and directly had an immediate impact on claim costs.

After 15 months we performed a study by running 100% of claims back through the prior PPO network reimbursement rates. This exercise proved a net savings of 43% above and beyond the PPO discounts we would have otherwise experienced. Instead of doing the same thing year after year, our clients did something different and it worked.

It has been seven years since our first client exited the managed care world. Subsequently more clients have embarked on the same journey, most with equally good results. None have returned to the world of managed care.

The Evidence

Skeptics may ask “How have your clients fared over time? Have they won the battle against medical trend?” The answer may be found by reviewing the experience of four of our clients who have been on a reference based pricing model for five years or more.

Our study is based on actual paid, mature medical claims through succeeding plan years starting in the first year on reference based pricing benchmarked off the prior year under a managed care plan. All claims above stop loss levels have been excluded.

This abbreviated analysis does not recognize changing demographics and plan changes. For example the leveraging effect of higher deductibles will increase trend factors. Of particular importance it should be noted that plan changes occurred in each case through improved benefits supported by claim savings. This study includes medical claims only.

One must understand that medical trend is just one of the factors used to calculate renewal rates for health plans and stop loss insurance. Each year carriers set their own trend level based on various factors, including the current health care inflation rate, analysts’ forecasts and their own experiences. However, our clients are self-funded and thus bear most risk with actual trend directly affecting costs without the benefit of pooling to any significant degree.

“Over the past several years, trend rates have consistently run 8-10% nationally, though certain regions have seen significantly higher or lower figures. Prescription drug trends (which are a component of this) have been more volatile. In the early 2000’s these trends were above 15%. They then fell back to single digit levels. But they have now returned to the teens.” – Kevin Gabriel, MBA, FSA, MAA

In comparing our client’s experience with average medical trend, we relied upon Heffernan Benefit Advisory Services – 2013 Trend Report; Historical Trend Factors. Based on this report, we are using 9.615% as average annual medical only trend factor.

Political Subdivision – 400 Employee Lives

This case has been on RBP for 7 years. They experienced poor claim years in 2010 and 2012. In 2012, for example, there were 14 large claims that approached or exceeded $125,000. Medical PEPM for 2014 and 2015 (to date) is less than 2008. Benefits have been improved; no deductible or co-insurance features with all benefits subject to co-pays only. Funding increase over seven years has been 15.6% or 2.23% per year.

Public School District – 900 Employee Lives

This case has demonstrated a consistent downward claim trend. Current PEPM (2015) is less than 2008-2009. No benefit reductions. Some benefit improvements. Plan funding has remained essentially static for the past five years.

Medical Industry – 280 Employee Lives

Plan year 2012-2013 experienced an outlier year with several large claims and 34 pregnancies. Current medical PEPM is 16% higher than under managed care plan in 2008-2009, representing a 2.66% increase per year (sans outliers). This illustrates that higher utilization and outlier claims will result in increasing cost which would occur under either managed care or RBP model. However, RBP trend factor continues below industry benchmarks.

Retail Business – 818 Employee Lives

This case has consistently been well below medical trend. Current medical PEPM is significantly lower than plan year 2008-2009. This case has not raised plan contributions in seven years.

Conclusion

Managed care has failed. Medical costs continue to soar. Providers are charging more and we continue to agree to blindly pay up through secretive contracts negotiated by vested interests. Medical trend has, and continues to be, consistently at double digits or close to it.

Cost plus insurance / reference based pricing is a proven method to maintain and even improve comprehensive coverage while at the same time keeping costs reasonable, predictable and consistent. Industry sources estimate reference based pricing plans represent 10% market share and rising. An east coast hedge fund, seeking opportunities in reference based pricing models, predicts reference based pricing will gain 60% market share within the next five years.

“What moves things is innovation. But it’s not easy to innovate in stagnant, hyper-regulated, captured sectors” – Max Borders (www.fee.org) Cost shifting under the Affordable Care Act will continue to fail to control costs.

Reference Based Pricing represents the last frontier in innovation to control health care costs in a tightly regulated and controlled market.

Plan sponsors can reasonably expect to reduce their health care costs below medical trend without benefit reductions or cost shifting of any kind.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

“Navigating a course where sound organizational management is intertwined with financial acumen requires a strategy designed by subject-matter experts. Fortunately, Financial Management Strategies for Hospital and Healthcare Organizations: Tools, Techniques, Checklists and Case Studies provides that blueprint”

—David B. Nash MD MBA Jefferson Medical College, Thomas Jefferson University, PA

Filed under: Health Economics, Health Insurance, Healthcare Finance | Tagged: healthcare costs, Managed Care vs Reference Based Pricing, medical inflation, William Rusteberg | 3 Comments »

![]()

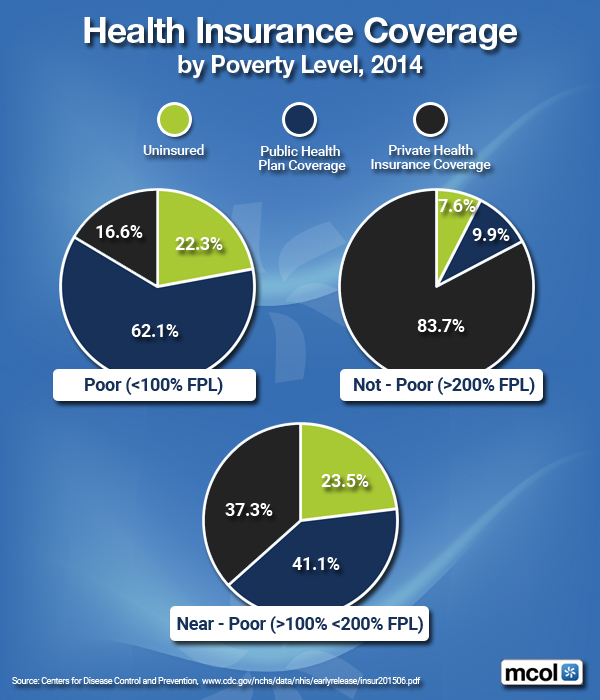

By Poverty Level in 2014

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

There is no other comprehensive book like it to help doctors, nurses, and other medical providers accumulate and preserve the wealth that their years of education and hard work have earned them.

Jason Dyken MD MBA [Dyken Wealth Strategies, Gulf Shores, Alabama]

I have read these texts and used consulting services from the Institute of Medical Business of Advisors, Inc., on several occasions.

MARSHA LEE; DO [Radiologists, Norcross, GA]

Filed under: Financial Planning, Health Insurance, Healthcare Finance, Risk Management | Tagged: Dyken Wealth Strategies, Financial planning MDs, Health Insurance Coverage, Jason Dyken MD MBA, Marcia Lee DO, Risk management MDs | 3 Comments »

![]()

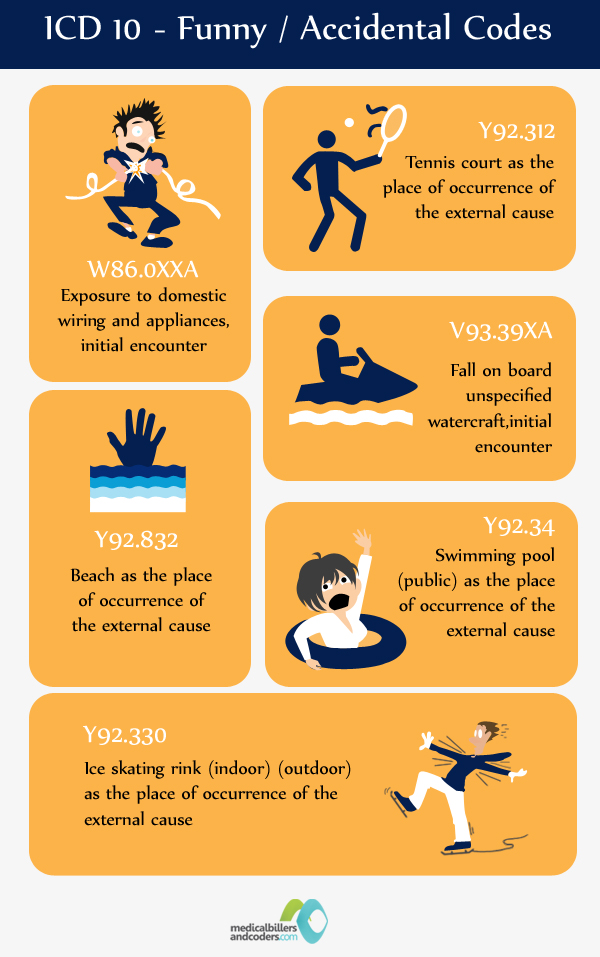

Funny … if NOT so Serious!

[By Staff Reporters]

Greater Coverage with ICD 10 Codes

***

***

Injury, Venue, Situation

Assessment:

You’ve got yourself covered.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance, Information Technology, Jokes and Puns | Tagged: ICD 10 Codes | 4 Comments »

![]()

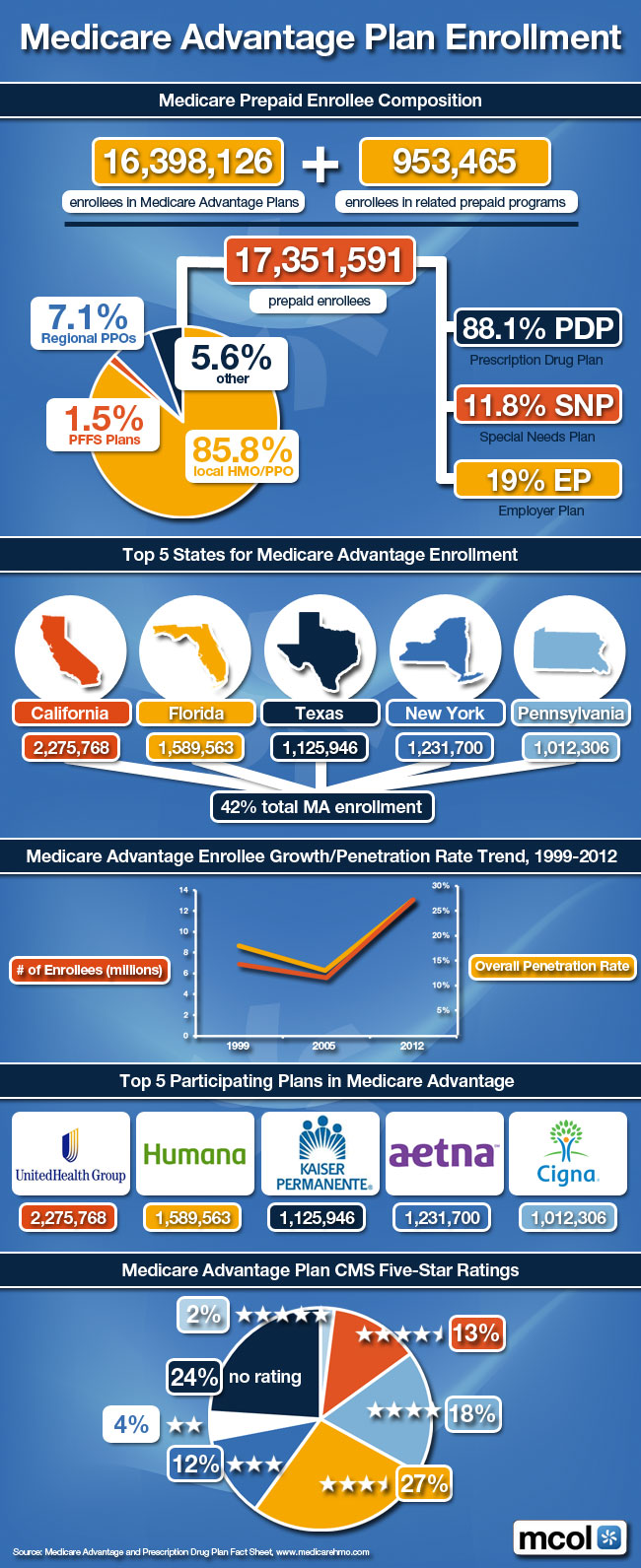

Medicare Pre-Paid Enrollee Composition

***

***

NOTE: CMS Releases 2013 Hospital, Physician Data

***

Source: Joseph Goedert, Health Data Management [6/2/15]

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance | Tagged: medicare, Medicare Advantage, Medicare Advantage Plan, Medicare HMOs | 10 Comments »

![]()

[By Staff reporters]

We are an emerging online and onground community that connects medical professionals with financial advisors and management consultants. We participate in a variety of insightful educational seminars, teaching conferences and national workshops. We produce journals, textbooks and handbooks, white-papers, CDs and award-winning dictionaries. And, our didactic heritage includes innovative R&D, litigation support, opinions for engaged private clients and media sourcing in the sectors we passionately serve.

Through the balanced collaboration of this rich-media sharing and ranking forum, we have become a leading network at the intersection of healthcare administration, practice management, medical economics, business strategy and financial planning for doctors and their consulting advisors. Even if not seeking our products or services, we hope this knowledge silo is useful to you.

In the Health 2.0 era of political reform, our goal is to: “bridge the gap between practice mission and financial solidarity for all medical professionals.”

***

***

![]()

![]()

![]()

8

***

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Book Reviews, Financial Planning, Health Economics, Health Insurance, Healthcare Finance, iMBA, Managed Care, Professional Liability, Recommended Books, Risk Management | Tagged: Financial Planning, Institute Medical Business Advisors, Medical Executve-Post, textbooks | 3 Comments »

![]()

Time for a Change?

By Miriam J. Laugesen PhD

[Assistant Professor, Department of Health Policy and Management, Mailman School of Public Health, Columbia University]

via: NIHCM Foundation | 1225 19th Street, NW | Suite 710 | Washington | DC | 20036 www.nihcm.org

The Government Accountability Office (GAO) just released an important review of the way the Relative Value Scale Update Committee (RUC) and CMS value physician services for Medicare. The report finds significant flaws in the data and processes used, echoing a recent Expert Voices essay by RUC researcher Miriam Laugesen.

***

***

Assessment

In this essay, Dr. Laugesen illustrates inaccuracies with work time estimates and the shortcomings of specialty society surveys. She also highlights ways to introduce greater precision and transparency to the process of updating Medicare physician fees. Read more…

EVEN MORE:

Gail Wilensky

The Outlook for Reforming Payments to Graduate Medical Education

John Iglehart

Meeting the Demand for Primary Care: Nurse Practitioners Answer the Call

David Dranove

Federal Antitrust Enforcement in Health Care

Michael L. Millenson

Paradigm, Not Pill: The New Role of Patient-Centered Care

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Economics, Health Insurance, Healthcare Finance | Tagged: Expert Voices, Mailman School of Public Health, Miriam J. Laugesen PhD, NIHCM Foundation, Valuing Physician Work in Medicare | 3 Comments »

![]()

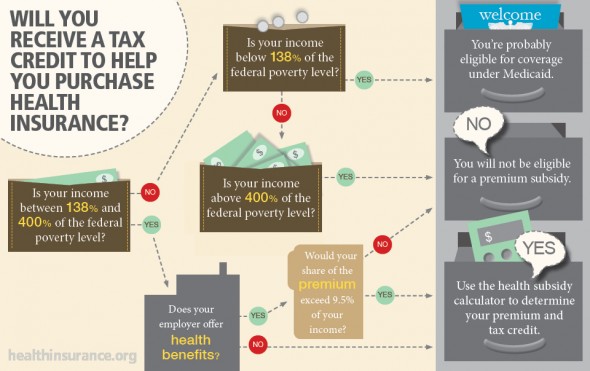

An Infographic

This infographic helps Americans determine whether they will be eligible for a health insurance premium subsidy under the Affordable Care Act aka Obamacare.

The infographic accompanies a story by blogger Maggie Mahar, who explains not only how eligibility for health insurance tax credits is determined, but also how much recipients should expect to receive.

The article also includes a chart with federal poverty level (FPL) numbers and links to a Kaiser Family Foundation premium subsidy calculator

Link: Healthinsurance.org

The graphic was created by Mahar, HIO editor Steve Anderson, and designer Barb Etzkorn. It was posted on the Blog of the Health Insurance Resource Center, one of the longest running sources of consumer health insurance information on the Web.

***

[Click to Enlarge]

Assessment

All healthcare and medical professionals should be aware of the information in this info-graphic; all FAs, too!

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance, Health Law & Policy | Tagged: ACA, ACA eligibility, ACA premiums, Healthinsurance.org, Kaiser Family Foundation, Maggie Mahar, Steve Anderson | 2 Comments »

![]()

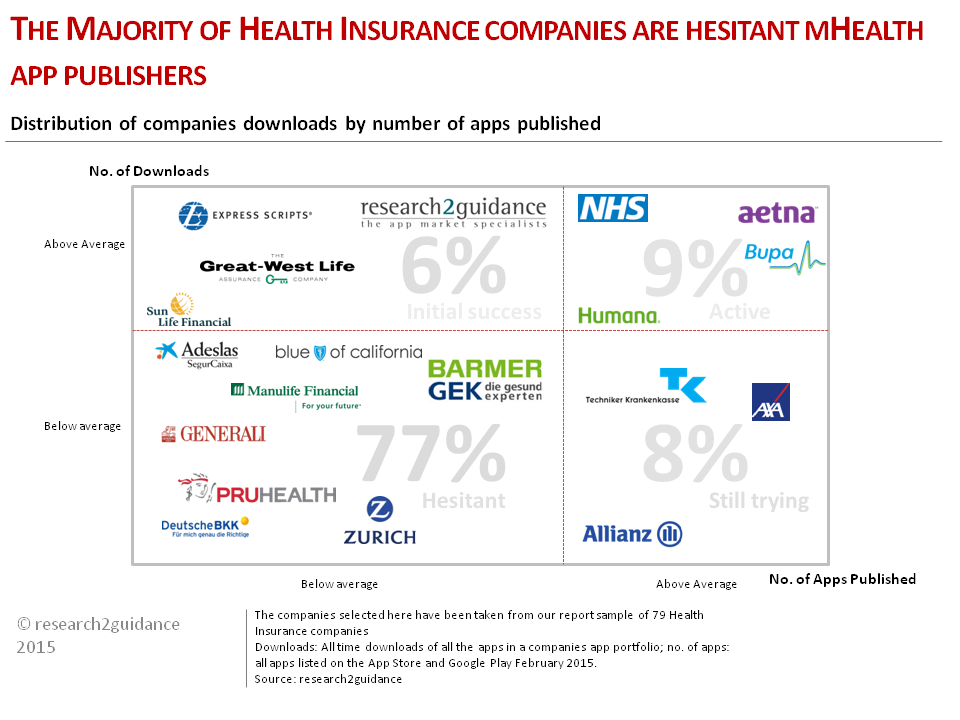

***

The majority of health insurance companies can be described as hesitant in their app publishing activities, even those that have a larger app portfolio fail to have a significant impact. A new report from research2guidance analyses global app publishing activities of the leading health insurance companies.

***

Some of the reasons are that health insurance companies are not leveraging their assets, their apps are not compliant with state-of-the-art app publishing rules and missing cross promotion.

The vast majority of health insurance companies have failed to generate a significant reach with their app portfolio, with 67% of health insurance companies having achieved less than 100,000 downloads. The majority of apps in the portfolio of healthcare payers belong to the long-tail:

AETNA

Aetna is the one health insurance company that stands out. Having published 28 apps across both iOS and Android Aetna have achieved more than 14million downloads, significantly more than any other health insurance company. That being said 85% of those download come from just on app within their app portfolio, iTriage. This is not uncommon amongst those health insurance companies that have generated a large number of downloads.

For example, 7 of the top 10 biggest health insurance companiesapp portfolios generate more than 50% of downloads from the top performing app. What are the reasons for the little impact the traditional payers of the healthcare systems have in the app economy?

RESULTS

These are some findings from research2guidance’s latest report “Health Insurance App Benchmarking 2015”. The report provides information on app categories health insurance companies concentrate on, the number of apps they have published, target user groups and the organization of their app business model.

***

***

The study results indicate that:

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance, Information Technology | Tagged: Aetna, Android Aetna, Health Insurance App, Ralf-Gordon Jahns, research2guidance.com | Leave a comment »

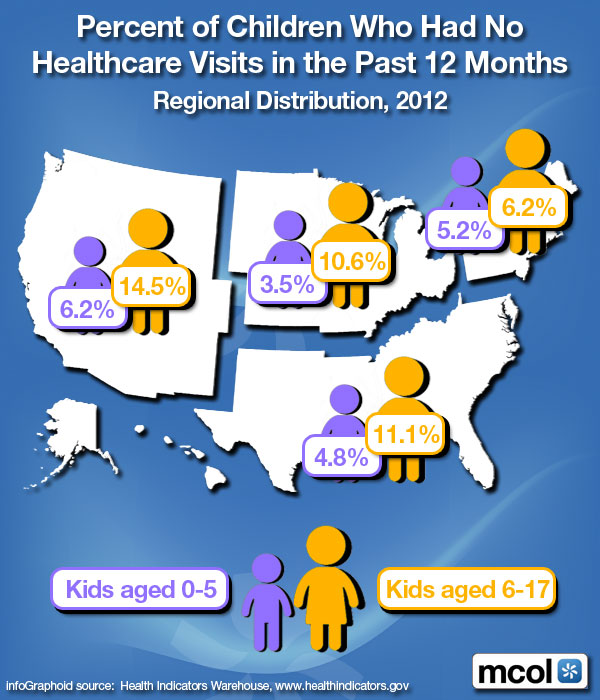

![]()

Regional Distribution 2012

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Breaking News, Health Insurance, iMBA | Tagged: American Academy of Pediatrics, pediatric healthcare, www.MCOL.com | 4 Comments »

![]()

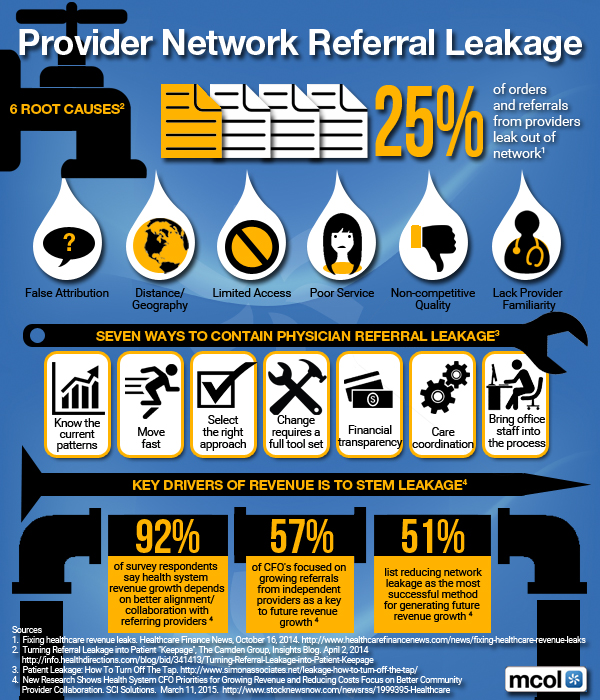

Understanding the Referral Relationship

[By Dr. David Edward Marcinko MBA]

Developing and cultivating a steady stream of referrals involves good planning, an investment of time and energy in the referral relationship, and a keen understanding of referring physicians’ needs and priorities.

Developing and cultivating a steady stream of referrals involves good planning, an investment of time and energy in the referral relationship, and a keen understanding of referring physicians’ needs and priorities.

Enhancing the referral relationship is a step-by-step process, not unlike the clinical process, that begins by identifying target physicians and their needs, prioritizing the list of referral contacts and then determining the best way to reach them.

A physician may routinely refer patients to a particular specialist because he or she has an outstanding reputation for medical expertise and competence, is more accessible than comparable practitioners or has a convenient location for the referring physician’s patients. The physician may have a relationship with the specialist because of marketing by a local hospital or the specialist’s own practice. And, in some cases the two physicians have a social relationship. Once again, there are many ways to create and maintain the relationship. Physicians should choose the approach that works best for them, put together a plan and stay consistent. Look for ways to make the relationship a win-win for both practices or for the referring hospital or outpatient facility.

If you are not comfortable with developing referral relationships for your practice, seek out partners, office staff or hospital partners who can appropriately assist, train or support you in this effort. Many hospitals have staff focused on physician sales and service.

The Society for Healthcare Strategy and Market Development (SHSMD) recently reported that 41% of hospitals had dedicated sales staff support, with more than half of those using their sales staff to support cardiology and radiology.[i] Often, hospitals are seeking physician speakers for community seminars, wellness programs and other outreach efforts. Ask about participating in these venues. Offer to write articles for newsletters, the Web site or local media outlets. All of these expose the physician and the practice to referral sources as well as the public.

Six Root Causes of Leakage

***

***

Communication is Key

It really comes down to the age-old golden rule of doing unto others as you would want them to do unto you. Not surprisingly, referral relationships are built on mutual respect, trust and courtesy. Focusing on the needs of the referring physician is the best way for both relationships to thrive.

Communication is especially important in not only nurturing the referral relationship, but also improving the quality of care.

A recent study that examines the attitudes primary care physicians have regarding communication with hospitalists found that 3% of primary care physicians reported being involved in discussions about discharge and 17% to 20% reported always being notified about discharges.[ii]

The study suggests that delayed or inaccurate communication at discharge may negatively effect continuity of care and contribute to adverse events. Communication tools such as computer-generated summaries and standardized formats may result in a more timely transfer of information, making discharge summaries more consistently available during follow-up care.

Many physicians indicate a preference for quick voice mail updates on patients they’ve referred supported by the electronic or faxed record. This type of proactive communication is the basis of a strong and lasting referral relationship. In fact, the relationship can be further strengthened by tailoring communication to individual primary care doctors, according to their preferences.

Indeed, the most responsive specialists ask the referring physician how best to stay in touch because one size does not fit all. Some physicians prefer face-to-face contact, others phone or facsimile and still others e-mail. The use of electronic medical records and other electronic communication devices can help the physician enhance the consistency, speed and real time level of their physician-to-physician communication.

Primary care doctors want to work with specialists who recognize their role in treating the patient on an ongoing basis. Many want frequent communication about the plan of care and status. At the very least, tertiary specialists should always pay the courtesy of discharge communication—a phone call, e-mail, timely letter or fax when they return the patient to the community physician. The specialist should include the diagnosis, any issues that he or she may have identified; any changes in treatment and medication, follow-up recommendations and a phone or pager number if the referring physician has questions or concerns.

Both sides should keep each other informed of changes within their respective practice including new partnerships, expanded services, staff changes and insurance plan participation. Paying close attention to these relationship and communication basics builds trust and respect among colleagues and improves care to patients.

***

***

Systems Can Help With Communication

A cardiac surgeon in the Northeast with a very busy practice dictates immediately following each case, and then at the end of the day calls to update the referring physician even if he just leaves a voice mail with his pager number. The referring physician has 24/7 access to the cardiac surgeon, who, two weeks later, has his practice administrator send a thank-you note for the referral. At a conference of specialists who were questioning their own ability to commit to this level of time, he simply stated “how can you not afford to pay attention to this part of your practice?”

Another example involves a large specialty practice that was challenged with communication back to the referring physician. They hired a clinician to support them as patient/practice case manager, with a primary job focus on communicating about the patient, ensuring discharge information was forwarded and conducting a personal office call with the referring physician. This ensured it was received, understood and if not, helping the referring physician to gain quick access to the specialist.

Citations:

[i] “By the Numbers, 2008.” Society for Healthcare Strategy and Market Development of the American Hospital Association.

[ii] Sunil Kripalani, M.D., et al., “Deficits in Communication and Information Transfer Between Hospital-Based and Primary Care Physicians,” The Journal of the American Medical Association, Feb. 28 2007, 297; 831-841.

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

![]()

Filed under: Health Insurance, Practice Management | Tagged: david marcinko, Doctor Referrals, Medical Provider Network Referral Leakage, patient referrals, SHSMD, Society for Healthcare Strategy and Market Development | 2 Comments »

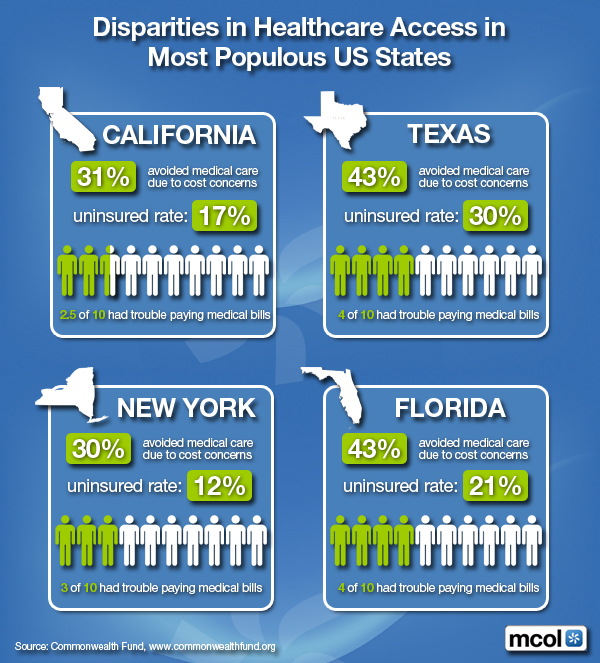

![]()

Most Populous US States

***

***

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Ethics, Health Insurance | Tagged: Healthcare Access Disparities, Healthcare Disparities | 2 Comments »

![]()

A Former Teacher Engages Reality

[By Jeffrey M. Hartman]

In late 2014, I did something many teachers never have to consider doing. I sought my own health insurance. After leaving my teaching career, I opted to work for myself. My plan was to live off my savings while getting started. This meant I was going to have to buy insurance rather than rely on a school to provide it. The misadventure that unfolded provided unsurprising but unsettling insights.

In late 2014, I did something many teachers never have to consider doing. I sought my own health insurance. After leaving my teaching career, I opted to work for myself. My plan was to live off my savings while getting started. This meant I was going to have to buy insurance rather than rely on a school to provide it. The misadventure that unfolded provided unsurprising but unsettling insights.

Bubble-Boy

I lived in a bubble during my teaching career. The comforts my job afforded me affected my perspective. How did people in other fields work so late each day? Why did anyone agree to work during the summer? I had a salary that kept me more than comfortable and health insurance that most people would have envied. Although I frequently reminded myself how fortunate I was, I still took too much of my situation for granted. When I decided to up and leave, reality poured into my bubble.

Great Coverage

Health insurance had never concerned me. Working in schools my entire adult life, I didn’t fret over having coverage. It was a given; an amount taken out of each check. If anything, I felt guilty for having such great coverage. I rarely used it. I happened to be a healthy person and I infrequently visited my doctor. Being so cavalier about my coverage while other people suffered without it made me feel like some kind of heel. My wife used it occasionally, so it wasn’t completely wasted.

A Career Abandoned

By abandoning my career, I forced myself to face a sudden and real need for coverage. I’ll admit resenting the need to have something I wasn’t likely to use, but I accepted the situation and proceeded. I had left other teaching jobs. After each departure, I replaced the job quickly, moving to a better job each time. This was another example of my chosen field distorting reality. Not many people enjoy that kind of mobility. Benefits had come along with each new job. With no intention of taking a new job last fall and no immediate income from working for myself, I was on deck to try HealthCare.gov.

****

****

Enter HealthCare.gov

Prior to any of this, most of my experience in dealing with health insurance involved my mother. I helped her get Supplemental Security Income and Medical Assistance. The process was arduous, but after an appeal, she got what she needed. More recently, I assisted my grandmother in connecting with a home health care aide through her insurance. This was tricky as well, but perseverance paid off. Having to deal with these systems gave me a notion of what to expect when navigating a massive health insurance bureaucracy.

Experienced as I was, working through HealthCare.gov tested my patience. The site achieved infamy in early 2014 following its beleaguered launch. I expected the site administrators to have fixed most of the bugs for the second year. Perhaps they had. What I found was convoluted, nonetheless. I managed, but not without incident.

Registration

The first hiccup came during registration. I followed the directions on the screen and provided the requested information, but the site couldn’t verify my identification. I’d never had a problem like this registering for anything else. It prompted me to upload registration documents, but I found no way to do this. I called customer service and a helpful but disaffected person verified my identification simply by asking for my address and Social Security number.

I completed the application and was eager to see my results. Before I registered, I had investigated what coverage might be available. I expected to be eligible for one of several seemingly suitable plans. Upon seeing my results, I was shocked to find my wife and I only qualified for Medicaid. Nothing else was available. I knew Medicaid had a resource limit in my state. I also knew my savings were approximately thirty times that limit. The site never asked about resources. It only asked for income, which was zero at the time. My wife’s income didn’t put us over the Medicaid income limit, but this was irrelevant.

I realized my situation was an anomaly. Most people don’t go from my former income to nothing by choice while not having any solid replacement. At the time, I was paying a high premium for continuing coverage from my former employer. I was determined to get something less costly through the Marketplace for the start of 2015. My state was going to deny me Medicaid. I had to appeal.

Non-Appeals

I couldn’t find a way to appeal online, at least not in my state. I had to mail the completed appeal form. After several weeks, I got no response. The deadline approached for having coverage by the first of the year. I called customer service. The representative told me I’d have to apply for Medicaid and get rejected before appealing. This was going to take too long. I called my state Department of Health and Welfare. A representative confirmed I’d be denied. He urged me to call HealthCare.gov again and simply state I’d been denied instead of going through the process. I did. I handled the appeal over the phone. An hour later, I had new insurance. I had even paid my first premium, which definitely stung.

Over the next month, HealthCare.gov sent me three letters and called me twice to remind me my identification had yet to be verified and my appeal had been denied. I politely informed them I had handled each issue. No one I spoke with could tell that I had, nor could they tell I’d selected and paid for coverage, even though I had.

****

****

New Coverage

Dealing with the new coverage was almost comical. I’d selected the same provider I had while teaching, but a different plan. My wife and I selected the same physicians we had seen for years. Despite our history with each, making appointments or filling prescriptions required us to provide detailed proof of our existence and needs through phone calls, faxes, and emails. This was necessary for the first several interactions. Inquiries and referrals were much more tedious than what we had known. Over four months, the provider sent us a total of ten new insurance cards. All the inefficiency with both systems prompted some reflection.

One could expect such confusion within large systems. However, I’ve thought of what difficulty others users might face. I’d like to think I’m relatively literate, tech-savvy, and patient. I have family members who would have been stumped after the first few screens of the on-line HealthCare.gov site. The parents of some of the students I taught would have had similar difficulty. People in such situations might have the greatest need for coverage. The complicated and buggy nature of Healthcare.gov requires a small army of customer service operators to help befuddled applicants through problems. I shiver thinking about the resources spent maintaining this backup system in lieu of having a more functional interface, but I guess this creates jobs. Similarly, my actual provider requires a maddening degree of redundancy that might strain the coping skills of needy clients. I wonder how many people just give up when pursing complicated but necessary claims.

Assessment

Perhaps by 2016 HealthCare.gov will be streamlined and smart enough to not confound its users. My provider might be as streamlined and smart as it’s going to get. I’ve rarely seen such bloated systems. Maybe I’ve been ignorant to what other people endure. Having outstanding coverage handed to me while teaching and being healthy my whole life kept me out of touch. My new experiences were mild inconveniences, but I fear how similar complications could stifle those really needing help. I suppose I’ve emerged from my bubble.

More:

ABOUT

Jeffrey M. Hartman is a former teacher who blogs at http://jeffreymhartman.com/

Conclusion

Your thoughts and comments on this ME-P are appreciated. Tell us YOUR story. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Filed under: Health Insurance, Health Law & Policy, Op-Editorials | Tagged: Getting Health Care, Health Insurance, Jeffrey Hartman | Leave a comment »

![]()

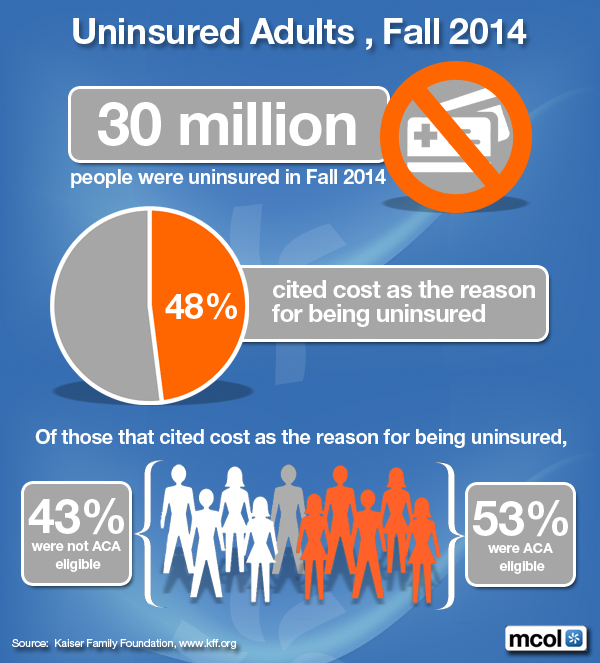

Fall 2014

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance | Tagged: ACA, PP-ACA, Un-Insured Adults in the USA | Leave a comment »

![]()

More on Healthcare Fraud and Abuse with Video

***

***

***

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

More: Submitted by Perry D’Alessio CPA

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Economics, Health Insurance, Healthcare Finance, Risk Management, Videos | Tagged: Edward Bukstel, health 2.0, medical fraud abuse, Medicare Fraud 2.0 Prediction. | 1 Comment »

![]()

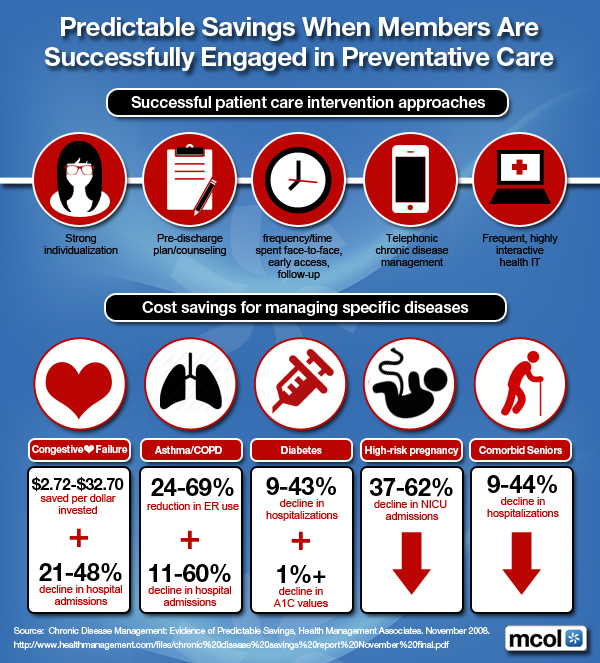

For … Successfully Engaged Members

More:

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Health Economics, Health Insurance | Tagged: Disease Management, Preventative Health Savings | 1 Comment »

![]()

Top Five Investment Priorities

By http://www.MCOL.com

***

***

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Health Economics, Health Insurance | Tagged: Digital Health Startups, Health 2.0 Innovators to Know, Physician Entrepreneurs, State Health Innovation Plans | 3 Comments »

![]()

Tax-free benefits provided to employees

[By Perry D’alessio CPA]

More and more physicians are employees; not employers.

More and more physicians are employees; not employers.

So, here are the most common types of tax-free benefits provided to employees.

They include payments for health care insurance, payment to a fund that provides accident and health benefit directly to the employee, company direct reimbursements for employee medical expenses and contributions to an Archer MSA (medical savings account).

The IRS definition of employee, for health care benefit purposes, is very broad

Health benefits are exempt from income, FICA and FUTA (Federal Unemployment Tax). This saves the employer 7.65% that would otherwise be the “matching” 6.2% Social Security tax and the 1.45% Medicare Tax components due if these were true wages. The employer also saves the 0.8% FUTA tax, but since FUTA taxes only the first $7,000 of calendar year wages, per employee, this usually doesn’t factor in.

Calculation:

If you pay the full state unemployment tax, then your FUTA tax = Gross Salary * .08% – The maximum amount is $56 per employee:

The hospital employee saves federal income taxes on health benefits received, at their marginal tax rate, and, their components of FICA taxes. Depending on the coverage provided, these plans, when fully funded by the employer, can save the employee thousands of dollars in taxes each year.

IRS restrictions include:

Example 1: Let’s say the annual cost of providing medical coverage for an employee, age 50, with a spouse and two minor children is $7,500. An employee in the 30% tax bracket who received this amount in cash each year and then paid for his or her own medical coverage would be liable for as much as $2,250 in income taxes. In addition, FICA taxes save another 7.65% or $574, for a total savings to the employee of $2,824. The employer saves $574 in FICA taxes.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Filed under: Accounting, Health Insurance, Taxation | Tagged: Accident and Health Benefits, MSA, Perry D'alessio, Taxation of Accident and Health Benefits | 2 Comments »

![]()

February 2015 Edition of Plan Management

[By Douglas B. Sherlock CFA] Sherlock@sherlockco.com

Please find attached, the February 2015 Edition of Plan Management Navigator.

In this issue, we highlight characteristics among Independent/Provider-Sponsored plans in the lowest 25th percentile in costs, which we consider Best-in-Class health plans. We found that Best-in-Class plans operated with administrative costs that were lower by $10.99 PMPM, excluding Sales and Marketing and Medical Management.

A lower Staffing Ratio was mainly responsible for low costs, while low Staffing Costs also contributed. Non-Labor Costs, however, were actually higher in the Best-in-Class plans. Almost every functional area was lower for the Best-in-Class plans with IS, Claims, and Corporate Services most responsible for overall low costs. Finance and Accounting was the exception in that its costs were higher.

The Analysis

To perform this analysis, we endeavor to quantify and eliminate the effect of factors largely beyond management control. We then isolate and measure the specific contributing factors that are more susceptible to management.

In addition, we are building the universes for the Sherlock Benchmarks. For the Independent/Provider-Sponsored universe we have 23 plans committed to participate in this year’s study. This is up by 44% from last year and collectively, the committed plans serve 10.5 million people with comprehensive products.

***

***

Participation Solicitation

We are meeting to finalize the survey form in about one month, will distribute the survey forms in late March, collect the completed surveys in May and publish results beginning in July. Participation entails notable efforts on your part since useful outputs require relatively granular inputs. However, the cost is relatively modest.

Link: Navigator – February 2015

Assessment

Please contact me if you are interested in participating. You will be among good company.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance, Healthcare Finance | Tagged: America's Health Insurance Plans, Douglas B. Sherlock CFA, health insurance plans, Plan Management Navigator | 1 Comment »

![]()

Update on the Medicare prescription drug benefit program

[By Staff Reporters]

![]()

Medicare Part D, also called the Medicare prescription drug benefit, is a United States federal-government program to subsidize the costs of prescription drugs and prescription drug insurance premiums for Medicare beneficiaries. It was enacted as part of the Medicare Modernization Act of 2003 (which also made changes to the public Part C Medicare health plan program) and went into effect on January 1, 2006.

Medicare Part D Premiums

The monthly Medicare Part D base premium is set to pay 25.5 percent of the cost of standard coverage, established by bids submitted annually by Part D plans. CMS releases the Medicare Part D base premium in early August each year. Actual premiums are based on this set premium, but can vary greatly. The premium for 2014 was $32.42.

As of 2011, beneficiaries with higher incomes must pay a premium adjustment based on their income. This premium adjustment is called the Income-Related Monthly Adjustment Amount (IRMAA), and is paid directly to the Federal government (deducted from Social Security, Railroad Retirement Board, or Office of Personnel Management benefits).

Medicare Part D Deductible

The annual deductible for the standard Medicare Part D benefit was $310 in 2014, which is a decrease of $10 from the 2013 deductible. No Medicare drug plan may have a deductible more than $310 in 2014, although some plans may have a lower deductible or no deductible at all.

***

|

*** CMS Part D 2015 Standard Benefit Model Plan Details Here are the highlights for the CMS defined Standard Benefit Plan changes from 2014 to 2015. The chart below shows the Standard Benefit design changes for plan years 2011, 2012, 2013, 2014 and 2015. This “Standard Benefit Plan” is the minimum allowable plan to be offered.

******

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

* 8

Filed under: Health Insurance, iMBA, Inc. | Tagged: Medicare Part D, Medicare prescription drug benefits | 7 Comments »

![]()

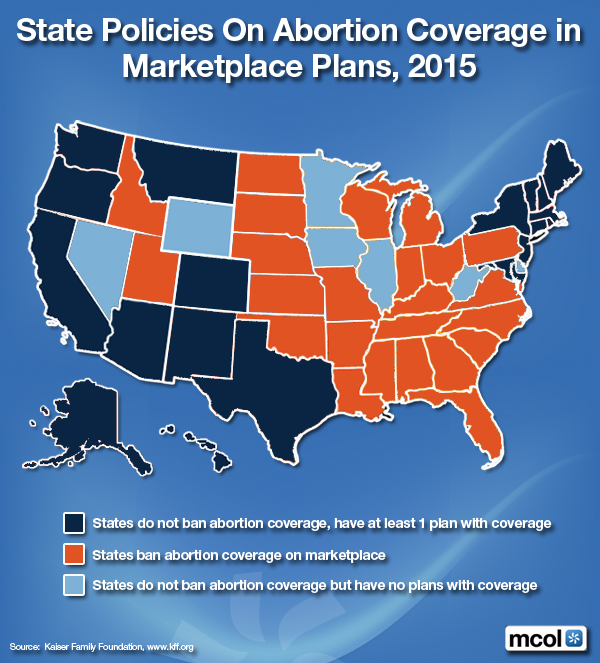

Market-Place Plans 2015

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Ethics, Health Economics, Health Insurance | Tagged: HIE abortion coverage, HIE's, PP-ACA, State Abortion Coverage | 3 Comments »

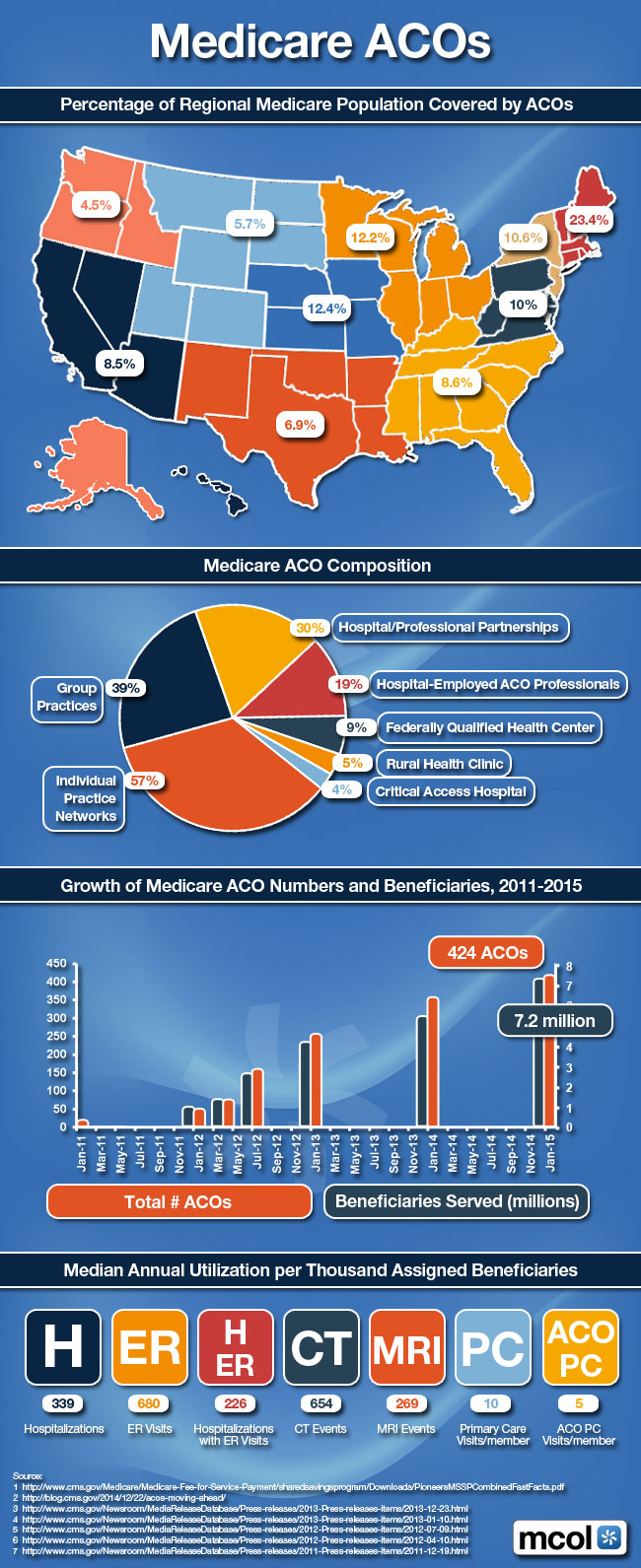

![]()

Percent of Regionally Covered Populations

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

More Articles on Accountable Care Organizations:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance | Tagged: ACA, ACOs, Medicare ACOs | 6 Comments »

![]()

About

***

The Institute of Medical Business Advisors, Inc provides a team of experienced, senior level consultants led by iMBA Chief Executive Officer Dr. David Edward Marcinko MBA CMP™ MBBS [Hon] and President Hope Rachel Hetico RN MHA CMP™ to provide going contact with our clients throughout all phases of each project, with most of the communications between iMBA and the key client participants flowing through this Senior Team.

iMBA Inc., and its skilled staff of certified professionals have many years of significant experience, enjoy a national reputation in the healthcare consulting field, and are supported by an unsurpassed research and support staff of CPAs, MBAs, MPHs, PhDs, CMPs™, CFPs® and JDs to maintain a thorough and extensive knowledge of the healthcare environment.

![]()

The iMBA team approach emphasizes providing superior service in a timely, cost-effective manner to our clients by working together to focus on identifying and presenting solutions for our clients’ unique, individual needs.

The iMBA Inc project team’s exclusive focus on the healthcare industry provides a unique advantage for our clients. Over the years, our industry specialization has allowed iMBA to maintain instantaneous access to a comprehensive collection of healthcare industry-focused data comprised of both historically-significant resources as well as the most recent information available. iMBA Inc’s specific, in-depth knowledge and understanding of the “value drivers” in various healthcare markets, in addition to the transaction marketplace for healthcare entities, will provide you with a level of confidence unsurpassed in the public health, health economics, management, administration, and financial planning and consulting fields.

![]()

![]()

iMBA Inc’s information resources and network of healthcare industry textbook resources enhanced by our professional consultants and research staff, ensure that the iMBA project team will maintain the highest level of knowledge regarding the current and future trends of the specific specialty market related to the project, as well as the healthcare industry overall, which serves as the “foundation” for each of our client engagements.

![]()

![]()

Ann Miller RN MHA

www.MedicalBusinessAdvisors.com

Financial Advisor Education Letterhead CMP™

Solicitation Letterhead.iMBA, Inc

***

***

Filed under: Career Development, Financial Planning, Health Economics, Health Insurance, Healthcare Finance, iMBA, Inc., Investing, Portfolio Management, Professional Liability, Recommended Books, Retirement and Benefits, Risk Management | Tagged: career planning, David Edward Marcinko, Financial Planning, Health Economics, Investing, Portfolio Management, practice administration, Practice Management, practice valuation | 1 Comment »

![]()

Detailing “Out-Of-Pocket” Expenses not included in Federal NHE Calculations

More:

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Economics, Health Insurance | Tagged: Expenses not in Federal NHE Calculations, Out-Of-Pocket Expenses | 4 Comments »

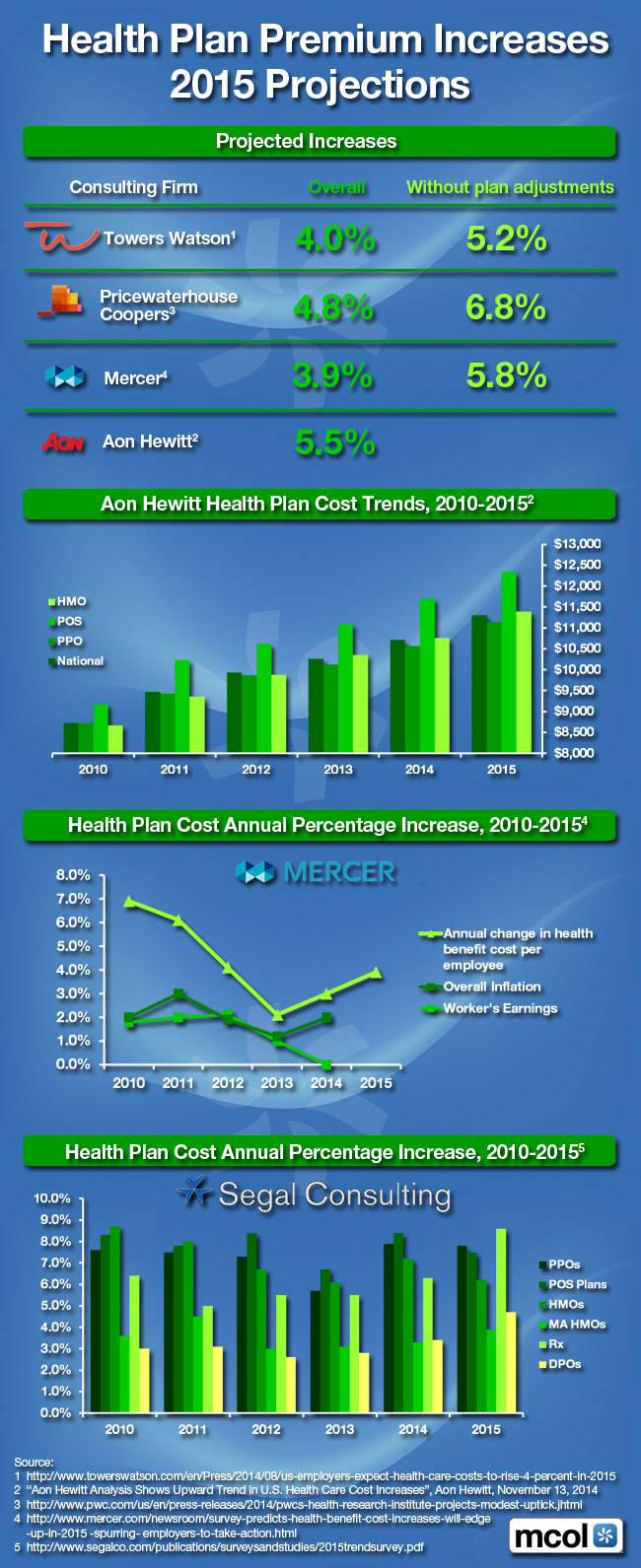

![]()

Projections

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance, Healthcare Finance | Tagged: 2015 Health Plan Premium Increases, ACA, health insurance premiums, healthcare premiums | Leave a comment »

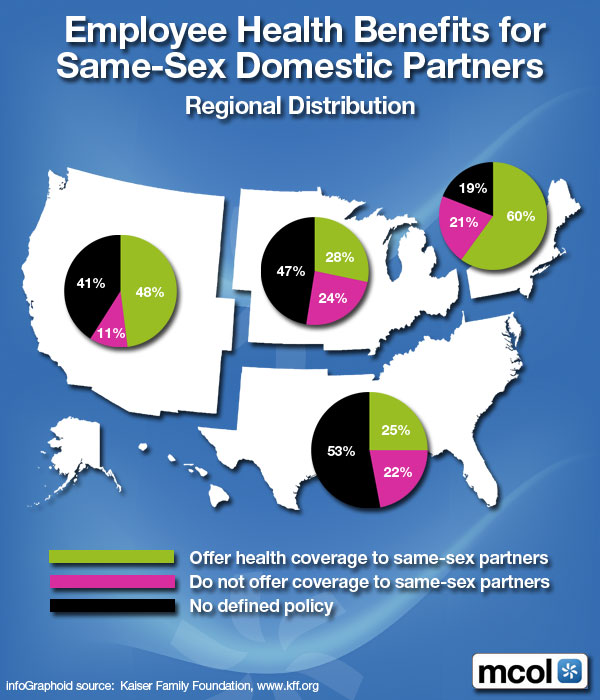

![]()

Regional Distribution

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Ethics, Health Insurance, Risk Management | Tagged: gay doctors, homosexual doctors, Same Sex Domestic Partners | Leave a comment »

![]()

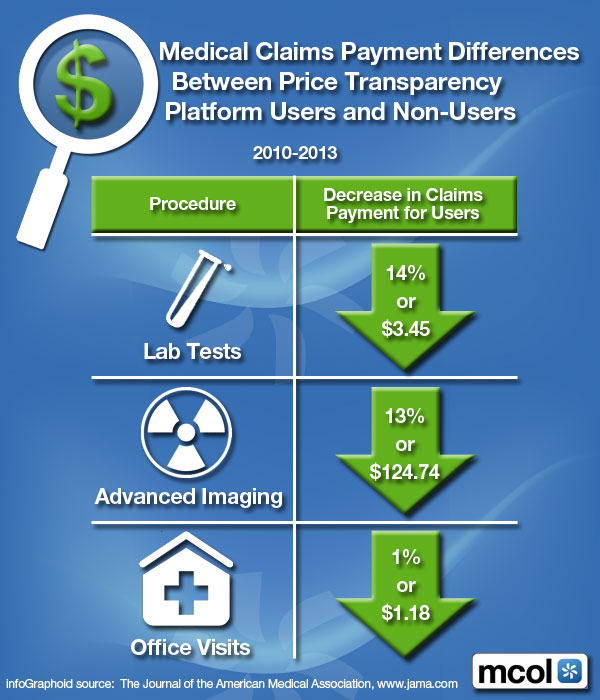

Between Price Transparency Platform Users and Non-Users

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Health Insurance | Tagged: Medical Claims Payment Differences | Leave a comment »

![]()

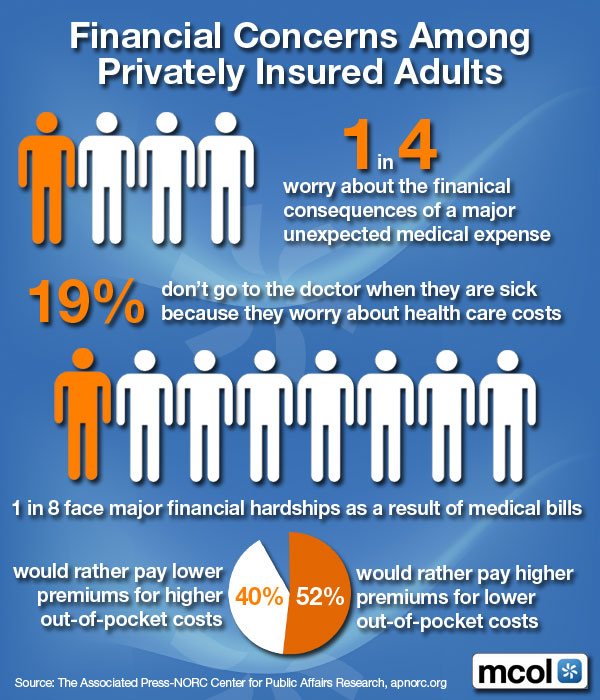

Privately Insured

***

***

Assessment

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Ethics, Funding Basics, Health Insurance | Tagged: ACA, Financial Hardship Concerns, private health insurance | 4 Comments »

![]()

The fuel which fires the self-funded engine of employee health and welfare plans

[By William Rusteberg]

Introduction