BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The Giffen paradox describes one of the most intriguing departures from standard consumer theory: a situation in which the quantity demanded of a good rises when its price increases, violating the usual law of demand. Although rare, the paradox has played an important role in shaping how economists think about consumer behavior, income effects, and the structure of household budgets. An 800‑word exploration of the paradox benefits from looking at its theoretical foundations, the economic conditions that make it possible, the historical debates surrounding it, and its broader implications for understanding poverty and consumption.

The nature of the paradox

In standard microeconomic theory, a price increase makes a good less attractive for two reasons. The substitution effect pushes consumers toward cheaper alternatives, while the income effect reduces their overall purchasing power, causing them to buy less of normal goods. A Giffen good is an extreme case in which the income effect not only dominates the substitution effect but does so strongly enough to reverse the expected outcome. Instead of buying less of the now‑more‑expensive good, consumers buy more of it.

This outcome requires a very specific set of circumstances. The good must be inferior, meaning demand for it falls as income rises. It must also occupy a large share of the consumer’s budget, so that a price increase significantly reduces real income. Finally, there must be no close substitutes, because the substitution effect must be weak relative to the income effect. When these conditions align, the paradox emerges: the price increase makes the consumer poorer, and because the good is a staple, the household compensates by consuming more of it and cutting back on more expensive foods or goods.

Historical origins and early debates

The paradox is named after Sir Robert Giffen, a 19th‑century economist who allegedly observed that poor households in Britain consumed more bread when its price rose. The logic was that bread was a dietary staple for the poor, while meat and other higher‑quality foods were luxuries. When bread became more expensive, households could no longer afford the luxuries and instead bought even more bread to meet their caloric needs. Although the story is widely repeated, Giffen himself never published such a claim, and the historical evidence is ambiguous. Nonetheless, the idea captured economists’ imaginations because it challenged the universality of the law of demand.

For decades, the paradox remained largely theoretical. Many economists doubted that such goods existed in reality, arguing that the required conditions were too restrictive. Others believed that the paradox was important precisely because it showed that consumer theory needed to account for extreme cases. The debate pushed economists to refine the distinction between substitution and income effects and to formalize the conditions under which demand curves could slope upward.

Theoretical structure and conditions

The Giffen paradox is best understood through the lens of the Slutsky equation, which decomposes the effect of a price change into substitution and income components. For a Giffen good, the income effect must be positive and large, while the substitution effect remains negative but small. This combination produces a net positive response to a price increase.

Three conditions are essential:

Inferiority — The good must be strongly inferior, meaning that as income rises, consumers sharply reduce consumption of it.

Budget share — The good must take up a substantial portion of the household’s spending, so that a price increase meaningfully reduces real income.

Lack of substitutes — If close substitutes exist, the substitution effect will dominate, preventing the paradox.

These conditions tend to occur only among very poor households consuming staple foods such as rice, wheat, or potatoes. In wealthier contexts, consumers have more flexibility, more substitutes, and more diversified budgets, making Giffen behavior unlikely.

Modern empirical evidence

For much of the 20th century, economists lacked clear empirical examples of Giffen goods. That changed when researchers began studying consumption patterns in extremely poor regions. In some cases, households facing rising prices for staple foods increased their consumption of those staples while reducing consumption of more nutritious or desirable foods. These findings did not settle the debate entirely, but they demonstrated that the paradox is not merely theoretical.

The empirical cases share common features: severe poverty, limited dietary options, and staples that dominate the household budget. These conditions mirror the theoretical requirements and help explain why Giffen behavior is rare in modern developed economies.

Broader implications for economic theory

The Giffen paradox has implications far beyond the narrow question of whether upward‑sloping demand curves exist. It highlights the importance of income effects in shaping consumer behavior, especially among low‑income households. It also underscores the limitations of simple demand models that assume consumers always respond to price changes in predictable ways.

Finally, the paradox also has policy implications. When governments consider subsidies or price controls on staple foods, understanding how poor households adjust their consumption is crucial. A well‑intentioned policy that lowers the price of a staple might reduce consumption of that staple if it frees up income for more desirable foods. Conversely, raising the price of a staple—though undesirable—could theoretically increase consumption among the poorest households, worsening nutritional outcomes. These insights remind policymakers that consumer behavior is complex and context‑dependent.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Turning 65 is often seen as the gateway to retirement—a time to slow down, reflect, and enjoy the fruits of decades of labor. But for some, including doctors who may have faced financial setbacks, poor planning, or unexpected life events, reaching this milestone without financial security can be deeply unsettling. The image of a broke 65-year-old doctor may seem paradoxical, given the profession’s reputation for high earnings. Yet, reality paints a more nuanced picture. Fortunately, even in the face of financial hardship, retirement is not a closed door—it’s a challenge that can be met with creativity, resilience, and strategic planning.

Understanding the Situation

Before exploring solutions, it’s important to understand how a physician might arrive at retirement age without adequate savings. Medical school debt, late career starts, divorce, health issues, poor investment decisions, or supporting family members can all contribute. Some doctors work in lower-paying specialties or underserved areas, sacrificing income for impact. Others may have lived beyond their means, assuming their high salary would always be enough. Regardless of the cause, the key is to shift focus from regret to action.

Traditional retirement—ceasing work entirely—is not the only option. For a broke 65-year-old doctor, retirement may mean transitioning to a less demanding role, reducing hours, or shifting to a new field. The goal is to create a sustainable lifestyle that balances income, purpose, and well-being.

Leveraging Medical Expertise

Even if full-time clinical practice is no longer viable, a physician’s knowledge remains valuable. Here are several ways to continue earning while easing into retirement:

Telemedicine: Remote consultations are in high demand, especially in primary care, psychiatry, and chronic disease management. Telemedicine offers flexibility, reduced overhead, and the ability to work from home.

Locum Tenens: Temporary assignments can fill staffing gaps in hospitals and clinics. These roles often pay well and allow for travel or seasonal work.

Medical Writing and Reviewing: Physicians can write for journals, websites, or pharmaceutical companies. Peer reviewing, editing, and content creation are viable options.

Teaching and Mentoring: Medical schools, nursing programs, and residency programs need experienced educators. Adjunct teaching or mentoring can be fulfilling and financially helpful.

Consulting: Doctors can advise healthcare startups, legal teams, or insurance companies. Their insights are valuable in product development, litigation, and policy.

Exploring Non-Clinical Opportunities

Some physicians may wish to pivot entirely. Transferable skills—critical thinking, communication, leadership—open doors in other industries:

Health Coaching or Life Coaching: With certification, doctors can guide clients in wellness, stress management, or career transitions.

Entrepreneurship: Starting a small business, such as a tutoring service, online course, or specialty clinic, can generate income and autonomy.

Real Estate or Investing: With careful planning, investing in rental properties or learning about the stock market can create passive income.

Maximizing Government and Community Resources

At 65, individuals become eligible for Medicare, which can significantly reduce healthcare costs. Additionally, Social Security benefits may be available, depending on work history. While delaying benefits until age 70 increases monthly payments, some may need to claim earlier to meet immediate needs.

***

***

Other resources include:

Supplemental Security Income (SSI): For those with limited income and assets.

SNAP (food assistance) and LIHEAP (energy assistance): These programs help cover basic living expenses.

Community Organizations: Nonprofits and religious groups often provide support with housing, transportation, and social engagement.

Downsizing and Budgeting

Reducing expenses is a powerful way to stretch limited resources. Consider:

Relocating: Moving to a lower-cost area or state with favorable tax policies can reduce housing and living expenses.

Selling Assets: A large home, unused vehicle, or collectibles may be converted into cash.

Shared Housing: Living with family, roommates, or in co-housing communities can cut costs and reduce isolation.

Minimalist Living: Prioritizing needs over wants and embracing simplicity can lead to financial and emotional freedom.

Creating a realistic budget is essential. Track income and expenses, eliminate unnecessary costs, and prioritize essentials. Free budgeting tools and financial counseling services can help.

Financial stress can take a toll on mental health. It’s important to cultivate resilience and maintain a sense of purpose. Strategies include:

Staying Active: Physical activity improves mood and health. Walking, yoga, or swimming are low-cost options.

Volunteering: Giving back can provide structure, community, and fulfillment.

Learning New Skills: Online courses, hobbies, or certifications can reignite passion and open new doors.

Building a Support Network: Friends, family, and peer groups offer emotional support and practical advice.

Planning for the Future

Even at 65, it’s not too late to plan. Consider:

Debt Management: Negotiate payment plans, consolidate loans, or seek professional help.

Estate Planning: Create a will, designate healthcare proxies, and organize important documents.

Insurance Review: Ensure adequate coverage for health, life, and long-term care.

Financial Advising: A fee-only advisor can help create a sustainable plan without selling products.

Embracing a New Chapter

Retirement is not a destination—it’s a transition. For a broke 65-year-old doctor, it may not look like the glossy brochures, but it can still be rich in meaning. By leveraging experience, reducing expenses, accessing resources, and nurturing well-being, retirement becomes a journey of reinvention.In many ways, doctors are uniquely equipped for this challenge. They’ve faced long hours, high stakes, and complex problems. That same grit and adaptability can guide them through financial hardship and into a fulfilling retirement.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

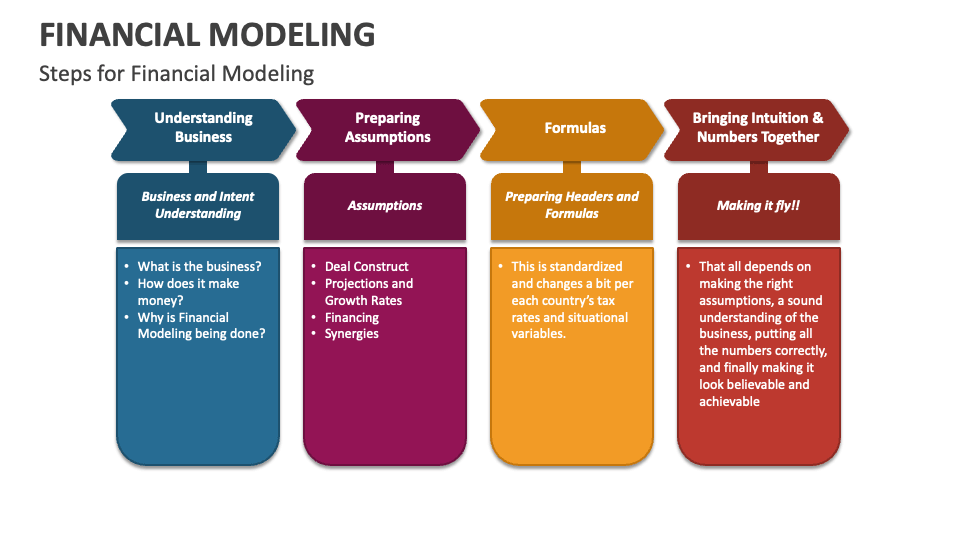

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.

What-If Analysis: Ever daydream about what would happen if you took that leap of faith with your business? This tool allows you to explore various scenarios without risking a dime. It’s like trying on outfits in a virtual dressing room before making a purchase.

Leveraged Buyout (LBO) Model: This is a bit like orchestrating a heist, but legally. It’s about acquiring a company using borrowed money, with plans to pay off the debts with the company’s own cash flows. High stakes, high rewards.

Mergers and Acquisitions (M&A) Model: Picture two puzzle pieces coming together. This model evaluates how combining companies can create a new, more valuable entity. It’s the corporate version of a matchmaker.

Three Statement Model: The holy trinity of financial modeling, linking the income statement, balance sheet, and cash flow statement. It’s like weaving a tapestry where each thread is crucial to the overall picture.

Capital Asset Pricing Model (CAPM): A formula that calculates the expected return on an investment, considering its risk compared to the market. It’s like choosing the best roller coaster in the park, balancing thrill and safety.

Cash Flow Forecasting: This is your financial weather forecast, predicting the cash flow climate of your business. It helps you plan for sunny days and save for the rainy ones.

Cost of Capital: The price of financing your business, whether through debt or equity. It’s like the interest rate on your growth engine, pushing you to maximize every dollar invested.

Debt Schedule: A timeline of your business’s debts, showing when and how much you owe. It’s your roadmap to becoming debt-free, one milestone at a time.

Equity Valuation: Determining the value of a company’s shares. It’s like assessing the worth of a rare gemstone, ensuring investors pay a fair price for a piece of the treasure.

Financial Leverage: Using debt to amplify returns on investment. It’s like using a lever to lift a heavy object, increasing force but also risk.

Forecast Model: A crystal ball for your finances, projecting future performance based on past and present data. It’s your guide through the financial wilderness, helping you navigate with confidence.

Operating Model: A detailed blueprint of how a business generates value, mapping out operational activities and their financial impact. It’s like laying out the inner workings of a clock, ensuring every gear turns smoothly.

Revenue Growth Model: This tracks potential increases in sales over time, charting a course for expansion. It’s like plotting your ascent up a mountain, anticipating the effort required to reach the summit.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

Posted on October 23, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

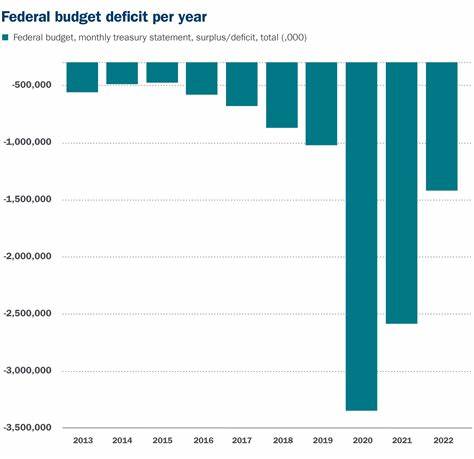

The 2023 federal budget deficitsurged by 23% to $1.7 trillion, leaving the US in its deepest yearly fiscal hole outside of the Covid era, according to the Treasury Department, which released the data on Friday.

But a closer look reveals the financial picture is even worse than the headline #s suggest.

The Treasury recorded the Biden administration’s ~$300 billion student loan forgiveness program as a cost last year, but it was struck down by the Supreme Court and never took effect, resulting in the Treasury considering it a savings this year.

That means the year over year increase effectively doubled from $1 trillion in 2022 to $2 trillion in 2023.

***

The benchmark 10-year Treasury bond yield rose above 5% and to its highest since 2007 on Monday, as a roaring U.S. economy led investors to expect interest rates to stay high for an extended period. The combination of those higher yields and risk of a wider conflict in the Middle East soured sentiment at the start of a week full of mega-cap earnings and key data, and pushed global shares down to seven-month lows.

***

Chevron said it would buy Hess in an all-stock deal worth $53 billion, the second major oil tie-up this month following Exxon Mobil’s deal to buy Pioneer Natural Resources. The U.S. energy company said buying Hess would upgrade and diversify its portfolio, marking Chevron’s entrance into an Exxon-led partnership overseeing a generational oil find in Guyana, while picking up additional U.S. shale assets largely in North Dakota. Chevron also highlighted the attraction of Hess’s assets in the Gulf of Mexico and its natural-gas business in Southeast Asia.

Posted on October 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

The stock markets ended Q3 last week with a whimper despite new data showing that the Fed’s favorite CPI inflation measure cooled in August. September was the worst month of the year for the S&P 500 and the NASDAQ. But Blue Apron soared on the news that it’s being bought by Wonder Group, a food delivery startup helmed by a former Walmart exec.

America’s debt today stands at $33 trillion, a figure some politicians, finance mavens and everyday citizens find astonishingly high.

***

Carmot Therapeutics, which is developing drugs for diabetes and weight-loss, is reportedly mulling an IPO or possible sale to a large pharmaceutical company at a valuation of at least $1B. The biotech company has two injectable GLP-1 drug candidates in Phase 2 development for type 1 and type 2 diabetes, according to the company’s website.

Carmot enlisted JP Morgan and Bank of America as underwriters on an IPO, which could come as early as this year if market conditions are favorable. The company has also received “takeover interest” from large drug makers at a valuation of over $1B, according to a Bloomberg report. Carmot had a post-money valuation of $1.25B following a $150M funding round in May, Bloomberg added.

NOTE: The US debt-ceiling bill just passed, June 1, 2023. So, here are some budgeting rules for doctors and medical professionals.

***

Budgeting is probably one of the greatest tools in building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle. This includes living in an exclusive neighborhood, driving an expensive car, wearing imported suits and a fine watch, all of which do not lend themselves to expense budgeting. Only one in ten medical professionals has a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination.

The following guidelines will assist in this microeconomic endeavor:

Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home, or in the office. Deposit it in a money market account for safety and interest.

Do not pay bills early, do not have more taxes withheld from your salary than you owe, and develop spending estimates and budget fixed expenses first. Fixed expenses are usually contractual, and may include housing, utilities, food, telephone, social security, medical, debt repayment, homeowner’ or renter’s insurance, auto, life and disability insurance, and maintenance, etc.

Make variable expenses a priority. Variable expenses are not usually contractual, and may include clothing, education, recreational, travel, vacation, gas, entertainment, gifts, furnishings, savings, investments, etc.

Trim variable expenses by 10-15 percent, and fixed expenses, when possible. Ultimately, all fixed expenses get paid and become variable in the long run.

Use carve-out or set-asides for big ticket items and differentiate “wants from needs.”

Know the difference between saving and investing. Savers tend to be risk adverse and investors understand risk and takes steps to mitigate it.

Determine shortfalls or excesses with the budget period.

Track actual expenses.

Calculate both income and expenses as a percentage of the total, and determine if there is a better way to allocate resources. Then, review the budget on a monthly basis to determine if there is a variance. Determine if the variance was avoidable, unavoidable, or a result of inaccurate assumptions, and take needed corrective action.

***

Verify Your Budget and Follow a Financial Plan

The process of establishing a budget relies heavily on guesswork, and the use of software or “apps”, that seamlessly track expenditures and help your budget and your financial plan become more of reality. Most doctors underestimate their true expenses, so lumping and best guesses on expense usually prove very inaccurate. Personal financial software and mobile phone applications make the verification of budgets easier. Once your personal accounts are setup, free apps like MINT.com will let give you a detailed report on where your money is going and the adjustments you must make. Few professions make larger contributions to the Internal Revenue Service than physicians and the medical profession. It is very important to categorize different budget categories not only to be proactive about your expenses, but also to accurately reflect the effect your different expenditures have on your real savings capability. All expense dollars are not equal.

For example, a mortgage payment, which is mostly interest expense in the early years, is likewise mostly tax deductible. Spending money on your family vacation is typically not tax deductible. Itemized deductions, which are deductions that a US taxpayer can claim on their tax return in order to reduce their Adjustable Gross Income (AGI), may include such costs as property taxes, vehicle registration fees, income taxes, mortgage expense, investment interest, charitable contributions, medical expenses (to the extent the expenses exceed 10% of the taxpayers AGI) and more.

Employing a qualifiedcertified medical planneR® that utilizes a cash-flow based financial planning software program may help the physician identify their actual after-tax projected cash flow and more accurately plan their future.

There are varying opinions on how much of your total income should go toward savings and retirement goals each month. Moreover, the answer is likely to vary, depending on your full financial profile.

But if you’re looking for some basic KISS guidelines, consider applying the 50-30-20 rule, a budgeting method that allocates 50% of your income to essentials, like rent and bills, 30% to discretionary spending and 20% to savings.

Posted on July 11, 2018 by Dr. David Edward Marcinko MBA MEd CMP™

The Essential Money Survival Skill

By Rick Kahler CFP®

Someone recently asked me to share my number-one financial tip that would make the greatest impact on a person’s financial well-being. For someone who can speak for hours on the topic, that’s a daunting task. I wanted to quote the late Dick Wagner’s advice to “Spend less, save more, and don’t do anything stupid,” but that sentence contains three tips.

I had to pick one and chose “spend less.” The greatest common denominator of financial success is not talent, IQ, career choices, income, inheritance, investment choices, being in the right place at the right time, or luck. It’s frugality.

Someone who has mastered the art of frugality has an essential survival skill. Their ability to save, to squirrel away money in times of prosperity, enables them to roll with almost any financial calamity. They tend to master their money rather than let money master them.

Frugal people find saving somewhat of a game. They get high off of building savings and finding bargains. They clip coupons, shop sales, and buy generic store brands. They buy used everything whenever possible, especially large ticket items like cars, appliances, and furniture. They do as much home maintenance themselves as is prudent. They rent things they won’t use much rather than buy. They don’t smoke, drink in excess, or do recreational drugs. They cook at home a lot. They pay off credit cards monthly, take on debt carefully, and pay down debt ahead of time, if possible. They find affordable ways to do the things they enjoy.

As frugal people accumulate wealth, they don’t give up their thrifty habits. As an example, I have a client who chose to vacation in Ireland this year. Why? It was a bargain. He got $700 roundtrip tickets by snagging a one-day sale on American Airlines.

Even though the external trappings of frugality are easy to spot, becoming frugal is really an inside job. If you aren’t naturally a saver, it’s not easy to just decide to become frugal. Changing to thrifty habits because you know you “should” doesn’t work any better than just deciding to lose 20 or 60 pounds does. Lifestyle shifts like this take something more than cognition.

To develop frugality you need to change your mindset about and your relationship with money. How do you do that? With intention, persistence, humility, patience, and curiosity.

There are many ways to begin changing your money mindset. I recommend starting with discovering the subconscious beliefs you have about money and how it works. I call these money scripts and have written about them in my books and blog.

Next, you may want to uncover the roots of those money scripts. This involves taking a look at how money was viewed in your family growing up and chronicling the positive and negative life events that have happened in your life. We help clients do this with two exercises called the Money Atom and the Money Egg. Slowly you will see themes emerge that completely explain why frugality is not your strong suit. This understanding is the foundation for change.

It is also valuable to find an accountability partner, someone who is frugal themselves, to be a mentor. This is similar to the Alcoholics Anonymous program’s recommendation to find a sponsor. It’s a tried and true model that produces results. Another option is to look for a financial coach or therapist (check at financialtherapyassociation.org) in your area or available to meet with you online.

Assessment

Becoming frugal doesn’t mean becoming a miser or depriving yourself. It means using your money thoughtfully to support the life you want to live. And it is a mindset you can learn.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

We are al aware of the student debt load crisis in this country.

But, one of the challenges at the beginning of a romantic relationship is having “the conversation” about an equally important issue for any couple: money.

Even more so for medical students, interns, residents, nurses, young doctors and medical professionals!

For example:

What is okay to ask a potential partner about money, and when?

How do you bring the subject up without seeming like a braggart, a coldhearted miser, or someone looking for a meal ticket?

There really ought to be some rules of etiquette for exploring this essential topic; something like, “by the sixth date, it’s appropriate to start undressing financially.” Unfortunately, we don’t have such guidelines.

The Money Minefield

Money is a topic fraught with emotional richness. In other words, it’s a minefield. Money is one of the top sources of conflict for couples, so if you’re dating, it’s crucial to learn a potential partner’s earnings, net worth, money habits, and financial beliefs. At the same time, talking specifically about money is so forbidden in our culture that we have no idea how to initiate a conversation about it.

Here are a few suggestions that might help:

1. Figure out your own money beliefs first. Before you even sign up with a dating site or accept your friend’s offer to set you up with her brother-in-law’s second cousin, think about what you want and need financially from a partner. Do you care if someone’s net worth is much higher or lower than yours? Is a certain level of debt a deal-breaker? What lifestyle are you comfortable with?

2. Tell before you ask. Begin with appropriate self-disclosure, in small steps, about your earnings, your long-term financial goals, or your beliefs about debt or spending. See how potential partners react. If they don’t disclose in turn, seem very uncomfortable with the conversation, or have beliefs or money habits much different from yours, you may be seeing red flags.

3. Observe. Watch how people handle money. Are there any patterns around spending or the use of credit cards that seem to indicate either overspending or excessive frugality? Do they throw cash around, or do they leave restaurant tips that Ebenezer Scrooge would be proud of?

Does someone’s home show signs of hoarding or stinginess? (A candlelight dinner of takeout Chinese at a card table is one thing for college students, but quite another for middle-aged professionals.) Do their cars or houses seem poorly maintained? Does their lifestyle seem more lavish than the typical earnings in their career field would support?

4.Listen. Despite the taboo on talking directly about money, we indirectly reveal a lot about our money beliefs by what we say. Notice how dates talk about saving or spending. Do they seem worried about money or reluctant to spend it even on basic needs? Do they seem angry about money or resentful of successful people? Do they boast about financial successes, things they own, or get-rich-quick schemes?

5. Ask. Even if everything else is all moonlight and roses. When you meet someone who seems like “the one,” don’t set aside everything that matters to you about money. Instead, remember how important this issue is to the long-term health of a relationship. Even if you can’t do it gracefully, ask the money questions. Talk frankly about debt, spending, saving for retirement, and each other’s expectations around lifestyles and careers.

Assessment

Being the one to initiate that difficult money conversation doesn’t mean you’re coldhearted, unromantic, or greedy. It simply means you recognize that money is too important a topic to ignore. When we enter into a romantic relationship, it’s tempting to think that love means not having to talk about money. In truth, love means having the courage to talk about money.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

In a previous ME-P, we looked at the first three components of a millionaire mindset: how to spend like a millionaire by living frugally, budget like a millionaire by putting essentials and savings first, and work like a millionaire by loving what you do and investing in your career.

All three of these are vital habits for anyone wanting to build financial independence and lead a satisfying life. But the millionaire mindset doesn’t stop there. Here are three more aspects of it.

4. Fail like a millionaire

The classic book, The Millionaire Next Door, by Thomas J. Stanley and William D. Danko, points out a statistic that initially seems backwards. The average millionaire makes 3.1 major financial, career, or business mishaps in a lifetime. The average non-millionaire makes 1.6 such mistakes.

Why do successful people fail so much more often? They don’t give up. They try again, and again, and again. As Steve Jobs, who had his own failures, said, “I’m convinced that about half of what separates successful entrepreneurs from the non-successful ones is pure perseverance.”

My own observation is that those who succeed also learn from their failures. A millionaire mindset means being willing to take risks, but also being smart enough not to keep making the same mistakes.

5. Network like a millionaire.

Those who succeed in starting businesses, building careers, and accumulating wealth aren’t afraid to ask for help. Millionaires know better than to rely solely on their own expertise. They are experts at building an expansive network of friends and acquaintances that they can turn to for help and advice. They understand that the more people you know, the more access you have to people you can learn from.

This, of course, is only one aspect of networking. Contrary to the projections of “greed” and “selfishness” often thrust upon them by public opinion and the media, successful people are also generous in giving back. The millionaire mindset includes an awareness that no one becomes successful in a vacuum. Millionaires are typically quick to acknowledge those who have helped them. They tend to pay it forward by mentoring, helping others to succeed, and sharing both their money and their wisdom.

6. Think like a millionaire

Having a millionaire mindset does not mean having a life goal of being rich. Millionaires think of money as a tool, not a goal. They don’t value wealth for its own sake. In fact, for many successful people, becoming rich is almost incidental. Their primary focus is succeeding at work they are passionate about.

A millionaire mindset is based on an attitude of gratitude, not one of entitlement. It includes the awareness that experiences and relationships are more valuable than things when it comes to creating sustainable happiness.

Successful millionaires understand that money itself will never give you meaning or make you happy. Yet they also understand that money is important. It is inseparable from our quest for meaning and happiness, because it touches everything we do. Financial planner Dick Wagner calls money “the most powerful and pervasive secular force on the planet.”

***

***

If you are struggling to pay the bills on a meager income, overwhelmed by debt, or living in chronic financial chaos, it’s highly unlikely that you’ll feel fulfilled and satisfied with your life. Money is an essential tool in today’s world, and learning to use that tool wisely is as important as learning the skills required for your career.

Assessment

No matter what direction your life or medical specialty takes you, developing a millionaire mindset will serve you well. It’s a crucial set of values to help you achieve your goals and realize your dreams.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on August 22, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

A Most Cruel – but Needed – Endeavor

[By Staff Reporters]

A zero-based budget means you start with the absolute essential expenses and then add-back expenses from there until you run out of money. This is an extremely effective, yet rigorous, exercise for most doctors and medical professionals; and can be used personally or at the office.

Triage and Prioritize

Your first personal financial item should be retirement plan contributions, then your mortgage and other debt payments, and then other required fixed expenses. From the office perspective, the first budget item should be salary expenses for both you and your staff. Operating assets and other big ticket items come next, followed by the more significant items on your net income statement. Some doctors even review their P&L statements quarterly, line by line, in an effort to reduce expenses. Then, you add discretionary personal or business expenses that you have some control over.

More Month than Money

Now, do you run out of money before you reach the end of the month, quarter, or year? Then you better cut back on entertainment at home or that fancy new, but unproven piece of office or medical equipment. This sounds Draconian until you remind yourself that your choice is either (1) entertainment now but no money later or; (2) living a simpler lifestyle now as you invest so you’re able to enjoy yourself at retirement.

Assessment

When you were a young doctor, budgeting may have seemed a task needed far into the future; but at midlife, you are staring retirement right in the face.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

:max_bytes(150000):strip_icc():format(webp)/the-50-30-20-rule-of-thumb-453922-final-5b61ec23c9e77c007be919e1-5ecfc51b09864e289b0ee3fa0d52422f.png)