![]()

ME-P Special Report

Share this:

Filed under: Ethics, Experts Invited, Financial Planning | Tagged: Deception in the Financial Service Industry, fiduciary advisor, fiduciary oath, Financial Planning, Lon Jefferies MBA CFP® | Leave a comment »

ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

![]()

![]()

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

![]()

ePodiatryConsentForms.com

ePodiatryConsentForms.com

“Providing Management, Financial and Business Solutions for Modernity”

“Providing Management, Financial and Business Solutions for Modernity”

![]()

Filed under: Ethics, Experts Invited, Financial Planning | Tagged: Deception in the Financial Service Industry, fiduciary advisor, fiduciary oath, Financial Planning, Lon Jefferies MBA CFP® | Leave a comment »

![]()

By Leanne Cole

***

***

Filed under: Experts Invited, LifeStyle | Tagged: Financial District New York, Leanne Cole, Wall Street | 1 Comment »

![]()

Be Ready for a Great 2016!

[By Patrick Bourbon CFA]

1. IRA – 401(k) / 403(b) retirement accounts – Are you on track for a comfortable retirement? You could increase the funding of your IRA and company retirement plan like a 401(k) or 403(b) accounts. 401(k) and 403(b) accounts allow individuals younger than 50 to contribute $18,000 each year, and individuals 50 and older to contribute $24,000. Some plans allow workers to make additional contributions of after-tax money.

For those under 50, the maximum is $53,000 for 2015. Doing so does not reduce your taxable income, but taxes are deferred on any earnings that the after-tax money makes. Later, some people roll these contributions into a Roth IRA, tax-free so the money would then grow tax-free. Traditional and Roth IRAs allow individuals younger than 50 to contribute $5,500 each year and individuals 50 and older to contribute $6,500. Even if you earn too much to contribute to a Roth IRA directly, you can open a traditional nondeductible IRA and convert it to a Roth; there is no income limit on traditional nondeductible IRAs or conversions. Returns generated in IRA and 401(k) / 403(b) accounts compound tax-free over their entire life.

2. Start tax planning! It’s not too early to think about taxes. Asset location & Tax efficiency Review your taxable and non-taxable accounts to ensure they are optimized for tax efficiency. If you have foreign bank accounts, make sure you comply with FATCA and FBAR (forms FinCEN 114, 8938, 8621…). If you have forgotten, you may look into the Offshore Voluntary Disclosure Program (OVDP) or Streamlined procedures.

3. Portfolio rebalancing Make sure you have rebalanced your portfolios to keep them in line with your goals, time horizon and risk tolerance. The market movements this summer may have thrown off your portfolio balance between stocks and bonds. David Swensen, the Chief Investment Officer at the Yale Endowment, performed an analysis that showed optimal rebalancing could add 0.4% to your annual return.

4. Harvest your capital losses Maybe it is time to sell some funds, ETF, stocks to generate some capital losses? Tax-loss harvesting is a method of reducing your taxes by selling an investment that is trading at a significant loss. Find out if you have any loss carryovers from prior years to be applied against capital gains (from sale of funds, ETF, stocks… in your taxable/brokerage accounts). If your current year’s capital losses exceed your capital gains, you have a net capital loss. You can use up to $3,000 of that loss ($1,500 if you are married filing separately) to offset other taxable income such as your salaries, wages, interest and dividends. If the capital loss is more than $3,000, you can carry over the excess and apply it against capital gains next year.

5. Emergency fund Don’t forget to establish or tune up your emergency fund. This is a good time to set aside money for next year’s cash needs. It is an account that is used to set aside funds to be used in an emergency, such as the loss of a job, an illness or a major expense.

6. Review your insurance policies Do you have a life, disability and long term care insurance? Make sure you and your loved ones are well protected if something happens to you. Your life may have changed (birth, marriage …). If you do have enough coverage it is also a good time simply to review the different types of coverage you have. Whole life or Variable Universal Life may help you reduce your taxes.

7. Health Spending Account Did you maximize your contribution to your healthcare HSA? The interest and earnings in this account are tax free! The maximum contribution for 2015 is $3,350 for an individual and $6,650 for a family ($1,000 catch-up over 55). The contributions are tax deductible and withdraws are non-taxable if they are used for medical expenses. Over the age of 65 you can withdraw funds at your ordinary tax rate (if the distribution is not used for unreimbursed medical expenses). Fidelity estimates that a 65-year-old couple retiring in 2014 will need $220,000 for health care costs in retirement, in addition to expenses covered by Medicare. The HSA can be a great source of tax-free money to pay those bills.

8. Required Minimum Distribution If you are age 70.5 or older, remember to take your required minimum distribution to avoid a potential 50% penalty.

9. 529 Plan Did you contribute to your 529 educational plan for your child/children? You can contribute $14,000 per year (annual limit) for each parent or you can pre-fund in a single instance up to five years’ worth of contributions, up to $70,000 (5 x $14,000). Together, that means a married couple can open a 529 plan with $140,000. Money saved in a 529 plan grows tax-free when used for eligible educational expenses, and some states have additional tax benefits for residents who contribute to a plan in that state.

10. Determine your net worth Add up what you own (home, car, savings, investments…) and subtract what you owe (mortgage, loans, credit cards, …). This will allow you to track your progress year to year. It may also give you some incentive to save more and create a better budget for next year.

11. Check your credit score Go to annualcreditreport.com and request a free credit report from each of the three nationwide credit reporting agencies. You’re entitled to one free report from each agency every 12 months.

12. Check your beneficiaries You can check the beneficiaries on your retirement accounts or insurance policies at any time, but it’s a good idea to do this at least annually.

13. Update your estate plan New baby? Newly married or divorced? Make sure your beneficiary designations reflect any changes. Don’t yet have an estate plan? Make that a new year’s resolution! Estate planning may include updating or establishing a “will” or trust that can help avoid public disclosure of assets in probate.

14. Spending and automated savings – You want to look ahead Did you review your budget and set up automated savings? You may have started the year with a clear budget, but did you to stick to it? Fall can be a good time of the year for your financial checkup and to reflect on your spending and develop a budget for next year. It is also a very good time to put whatever you can on automatic. Bills, recurring payments, even savings—the more you can put on auto pay now, the easier your financial life will be next year. With this year’s facts and figures in front of you, it will be easier to plan and prioritize your expenditures for next year.

Assessment

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Experts Invited, Insurance Matters, Investing, Portfolio Management | Tagged: 2015 Year-End Financial Checklist, Financial Planning, Investing, Patrick Bourbon CFA | Leave a comment »

![]()

And … Business Owners

By Robert Whirley CPA

[Alpharetta, GA 30009]

As the end of the year approaches, it is a good time to think of planning moves that will help lower your tax bill for this year and possibly the next. Factors that compound the challenge include turbulence in the stock market, overall economic uncertainty, and Congress’s failure to act on a number of important tax breaks that expired at the end of 2014. Some of these tax breaks ultimately may be retroactively reinstated and extended, as they were last year, but Congress may not decide the fate of these tax breaks until the very end of 2015 (or later). These breaks include, for individuals: the option to deduct state and local sales and use taxes instead of state and local income taxes; the above-the-line-deduction for qualified higher education expenses; tax-free IRA distributions for charitable purposes by those age 70- 1/2 or older; and the exclusion for up-to-$2 million of mortgage debt forgiveness on a principal residence. For businesses, tax breaks that expired at the end of last year and may be retroactively reinstated and extended include: 50% bonus first-year depreciation for most new machinery, equipment and software; the $500,000 annual expensing limitation; the research tax credit; and the 15-year writeoff for qualified leasehold improvements, qualified restaurant buildings and improvements, and qualified retail improvements.

Higher-income earners have unique concerns to address when mapping out year-end plans. They must be wary of the 3.8% surtax on certain unearned income and the additional 0.9% Medicare (hospital insurance, or HI) tax. The latter tax applies to individuals for whom the sum of their wages received with respect to employment and their self-employment income is in excess of an unindexed threshold amount ($250,000 for joint filers, $125,000 for married couples filing separately, and $200,000 in any other case).

The surtax is 3.8% of the lesser of: (1) net investment income (NII), or (2) the excess of modified adjusted gross income (MAGI) over an unindexed threshold amount ($250,000 for joint filers or surviving spouses, $125,000 for a married individual filing a separate return, and $200,000 in any other case). As year-end nears, a taxpayer’s approach to minimizing or eliminating the 3.8% surtax will depend on his estimated MAGI and NII for the year. Some taxpayers should consider ways to minimize (e.g., through deferral) additional NII for the balance of the year, others should try to see if they can reduce MAGI other than NII, and other individuals will need to consider ways to minimize both NII and other types of MAGI.

The 0.9% additional Medicare tax also may require year-end actions. Employers must withhold the additional Medicare tax from wages in excess of $200,000 regardless of filing status or other income. Self-employed persons must take it into account in figuring estimated tax. There could be situations where an employee may need to have more withheld toward the end of the year to cover the tax. For example, if an individual earns $200,000 from one employer during the first half of the year and a like amount from another employer during the balance of the year, he would owe the additional Medicare tax, but there would be no withholding by either employer for the additional Medicare tax since wages from each employer don’t exceed $200,000. Also, in determining whether they may need to make adjustments to avoid a penalty for underpayment of estimated tax, individuals also should be mindful that the additional Medicare tax may be overwithheld. This could occur, for example, where only one of two married spouses works and reaches the threshold for the employer to withhold, but the couple’s combined income won’t be high enough to actually cause the tax to be owed.

We have compiled a checklist of additional actions based on current tax rules that may help you save tax dollars if you act before year-end. Not all actions will apply in your particular situation, but you (or a family member) will likely benefit from many of them. We can narrow down the specific actions that you can take once we meet with you to tailor a particular plan. In the meantime, please review the following list and contact us at your earliest convenience so that we can advise you on which tax-saving moves to make.

***

***

Year-End Tax Planning Moves for Individuals

***

***

Year-End Tax-Planning Moves for Medical Practices, & Business Owners

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Front Matter with Foreword by Jason Dyken MD MBA

![]()

“BY DOCTORS – FOR DOCTORS – PEER REVIEWED – FIDUCIARY FOCUSED”

***

Filed under: Accounting, Experts Invited, Taxation | Tagged: Robert Whirley CPA, Year End Tax Planning for Physicians | 5 Comments »

![]()

By Michael Lawrence Langan, M.D.

***

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

[Foreword Dr. Phillips MD JD MBA LLM] *** [Foreword Dr. Nash MD MBA FACP]

***

Filed under: Ethics, Experts Invited, Risk Management | Tagged: physician health programs | 1 Comment »

![]()

By Vitaliy Katsenelson CFA

By Vitaliy Katsenelson CFA

So many articles have been written recently about Apple — defending it or explaining why this glorious fruit will turn into a shriveling pumpkin by midnight (with Samsung’s help) — that I really haven’t felt the need to contribute to the unending debate.

But, when Apple’s stock crashed to $450 back in January 2013, we bought a little for our clients. After receiving an outraged e-mail from one of them calling the purchase “irresponsible” and proclaiming that everyone (including his neighbor) knows that Apple is going down to $300, I decided it was time to join the discourse. Clients rarely (almost never) contact us about stocks we own in their accounts. More important, this is far from the most “radioactive” stock we own or have owned.

So, here is a column on Apple, I wrote back then. I have no intention of defending or prosecuting the company, but I would like to share some thoughts about it that many pundits have either overlooked or ignored.

***

***

The Psychlogy

What makes Apple stock difficult to own is psychology. The company’s success since 2000 is a black swan. We tend to think of Nassim Nicholas Taleb’s black swans as significant random negative events, but Apple is a positive one. When co-founder Steve Jobs came back to the company in the late ’90s, Apple was about to take its last breath. Jobs pulled off a miracle. He revived the company’s computer product line, making Macs exciting again, and then came out with three revolutionary “i” products in a row: the iPod, iPhone and iPad. You could argue that the success of each “i” product in itself was a black swan, exceeding all rational expectations and revolutionizing, transforming and in some cases creating new categories of merchandise that had never existed before.

Revenue and Market Capitalization

Apple’s revenue and market capitalization deservedly surpassed those of almighty Microsoft Corp. — the hairy monster with stinky breath that performed CPR on dying Apple in the late ’90s by injecting liquidity into the company by buying its preferred stock. We have a hard time processing this highly improbable success and an even harder time imagining that there is another black swan about to take flight from the Apple labs, especially with no Steve Jobs around to sit on the egg.

Black swans come out of nowhere, unannounced, but their impact may be long-lasting. The wildly successful “i” gadgets dug a formidable moat around Apple. They created the most valuable and still most inspirational brand in the world, funded an enormous research and development effort, enabled huge buying power (Apple locks up supply and pays much lower prices than many of its competitors for parts), filled out a mature product ecosystem and stuffed Apple’s debt-free balance sheet with $137 billion — half the market capitalization of Microsoft. The moat is wide, deep and unlikely to be breached any time soon.

***

***

High Price

One reason the psychology of owning Apple stock is so difficult: it’s high price. (Note: I am talking not about its valuation but purely about its price.) Apple has had only one stock split since the late ’90s, when it was trading in double digits, and it now changes hands at about $450 (down from $700 just a few months ago). Stock splits create zero economic value in the long run — absolutely none. Apple could split its stock ten to one and you’d have ten $45 shares, and nothing about the company or its business would change. But, I’d argue that a 3 percent “slide” of $1.35 would grab fewer headlines than a $13.50 “drop” — there is a media magnification factor that is hard to ignore.

Hardware versus Software

Is Apple a hardware or a software company? This is a very important question because Apple’s net margins of 25 percent are dangerously higher than those of Microsoft, a software monopoly that, with the minor exception of the Xbox and its new venture into tablets, sells only software, which has a 100 percent incremental margin.

Apple is either a smart hardware company or a software maker dressed in hardware company clothes. Take a look at the PC businesses of traditional “dumb” hardware companies like Dell and Hewlett-Packard Co. (I am not insulting these companies, I am just highlighting their lack of PC-directed R&D.) They buy hard drives from Western Digital Corp., graphic cards from Nvidia Corp., processors from Intel Corp. and an operating system from Microsoft, then they have contract manufacturers put together these parts in Asia and ship PCs all over the world. Dell and HP engineers design the PCs but contribute minimal R&D to their boxes; most of the R&D is done by the suppliers. Dell and HP are really asset-lite marketing and logistics companies — this explains their razor-thin margins. (Side note: Because of a lack of fixed costs, Dell and HP can remain profitable despite the ongoing decline in PC sales.)

Same Surface

On the surface, Apple’s personal computer business is not that much different from Dell’s or HP’s: It uses the same highly commoditized hardware and it also outsources manufacturing, but Apple spends much more on the R&D of its own operating system and creates distinctive, innovative products. Apple gets to keep a slice of revenue that would otherwise go to Microsoft for the operating system. Also, Apple is able to charge a premium (usually a few hundred dollars per PC) for the aesthetic appeal and perceived ease of use of its products.

However, when it comes to the “i” devices, Apple is a much smarter hardware company; its value added goes further than just basic design and software. Though there is a lot of commoditized hardware that goes into an iPhone or iPad, Apple’s skill at fitting an ever-growing number of components into ever-shrinking devices constantly increases. Add world-class touch and feel, superior battery life and durability, and you have a package that turns what would otherwise be commodity items into highly differentiated, and undeniably sexy, products. Apple has even gone a step further and is designing its own microprocessors.

But — and this is a very important “but” — as phones and tablets mature, processor speed, battery life and weight will tend to become uniform across all devices. It is arguable that the competition has already caught up with Apple in the hardware race. As the hardware premium goes away, there will be only two premiums left: Apple’s brand and its ecosystem. (I will go into detail about the “i” ecosystem and what it means for Apple’s margins and profitability in my second essay posted below).

Note that I did not mention the software premium. Unlike Microsoft, which charges for the Windows operating system installed on PCs, Google gives away Android to anyone who dares to make a phone or a tablet. Unless Apple can maintain the operating system lead against Android, that premium will go away.

Assessment

Recently, I spent a few days playing with Nexus 7, Google’s Android-powered 7-inch tablet, which retails for $200 ($130 cheaper than Apple’s iPad mini). Nexus 7 is a good product, but I kept remembering that humans and monkeys share 98 percent of their DNA, and the Android operating system is missing the 2 percent that makes Apple iOS so special.

***

Apple’s ecosystem is an important and durable competitive advantage; it creates a tangible switching cost (or, an inconvenience) after Apple has locked you into the i-ecosystem. It takes time to build an ecosystem that consists of speakers and accessories that will connect only via Apple systems: Apple TV, which easily recreates an iPhone or iPad screen on a TV set; the music collection on iTunes (competition from Spotify and Google Play lessens this advantage); a multitude of great apps (in all honesty, gaming apps have a half-life of only a few weeks, but productivity apps and my $60 TomTom GPS have a much longer half-life); and, last, the underrated Photo Stream, a feature in iOS 6 that allows you to share photos with your close friends and relatives with incredible ease. My family and friends share pictures from our daily lives (kids growing up, ski trips, get-togethers), but that, of course, only works when we’re all on Apple products. (This is why Facebook bought Instagram for $1 billion. Photo Stream is a real competitive threat to Facebook, especially if you want to share pictures with a limited group of close friends.)

The i-ecosystem makes switching from the iPhone to a competitor’s device an unpleasant undertaking, something you won’t do unless you are really significantly dissatisfied with your i-device (or you are simply very bored). How much extra are you willing to pay for your Apple goodies? Brand is more than just prestige; it is the amalgamation of intangible things like perceptions and tangible things like getting incredible phone and e-mail customer service (I’ve been blown away by how great it is!) or having your problems resolved by a genius at the Apple store.

Of course, as the phone and tablet categories mature, Apple’s hardware premium will deflate and its margins will decline. The only question is, by how much?

Let me try to answer

From 2003 to 2012, Apple’s net margins rose from 1.1 percent to 25 percent. In 2003 they were too low; today they are too high. Let’s look at why the margins went up. Gross margins increased from 27.5 percent to 44 percent: Apple is making 16.5 cents more for every dollar of product sold today than it did in 2001. Looking back at Nokia Corp. in its heyday, in 2003 the Finnish cell phone maker was able to command a 41.5 percent margin, which has gradually drifted down to 28 percent.

Today, Nokia is Microsoft’s bitch, completely dependent on the success of the Windows operating system, which is far from certain. Nokia is a sorry shell of what used to be a great company, while Apple, despite its universal hatred by growth managers, is still, well, Apple. Its gross margins will decline, but they won’t approach those of 2003 or Nokia’s current level.

For Apple to conquer emerging markets and keep what it has already won there, it will need to lower prices. The company is not doing horribly in China — its sales are running at $25 billion a year and were up 67 percent in the past quarter.

However, a significant number of the iPhones sold in China (Apple doesn’t disclose the figure) are not $650 iPhone 5’s but the cheaper 4 and 4s models. (Also, on a recent conference call, Verizon Communications mentioned that half of the iPhones it has sold were the 4 and 4s models.) Apple’s price premium over its Android brethren is not as high as everyone thinks.

What is truly astonishing is that Apple’s spending on R&D and selling, general and administrative (SG&A) expenses has fallen from 7.6 percent and 19.5 percent, respectively, in 2003 to a meager 2.2 percent and 6.4 percent today. R&D and SG&A expenses actually increased almost eightfold, but they didn’t grow nearly as fast as sales. Apple spends $3.4 billion on R&D today, compared with $471 million in 2001. This is operational leverage at its best. As long as Apple can grow sales, and R&D and SG&A increase at the same rate as sales or slower, Apple should keep its 18.5 percentage points gain in net margins through operational leverage.

***

***

Growth of sales is an assumption in itself. Apple’s annual sales are approaching $180 billion, and it is only a question of when they will run into the wall of large numbers. At this point, 20 percent-a-year growth means Apple has to sell as many i-thingies as it sold last year plus an additional $36 billion worth. Of course, this argument could have been made $100 billion ago, and the company did report 18 percent revenue growth for the past quarter, but Apple is in the last few innings of this high-growth game; otherwise its sales will exceed the GDP of some large European countries.

If you treat Apple as a pure hardware company, you’ll miss a very important element of its business model: recurrence of revenues through planned obsolescence. Apple releases a new device and a new operating system version every year. Its operating system only supports the past three or four generations of devices and limits functionality on some older devices. If you own an iPhone 3G, iOS 6 will not run on it, and thus a lot of apps will not work on it, so you will most likely be buying a new iPhone soon. In addition — and not unlike in the PC world — newer software usually requires more powerful hardware; the new software just doesn’t run fast enough on old phones. My son got a hand-me-down iPhone 3G but gave it to his cousin a few days later — it could barely run the new software.

As I wrote above, Apple’s success over the past decade is a black swan, an improbable but significant event, thanks in large part to the genius of Steve Jobs. Today investors are worried because Jobs is not there to create another revolutionary product, and they are right to be concerned. Jobs was more important to Apple’s success than Warren Buffett is to Berkshire Hathaway’s today. (Berkshire doesn’t need to innovate; it is a collection of dozens of autonomous companies run by competent managers.) Apple will be dead without continued innovation.

Jobs was the ultimate benevolent dictator, and he was the definition of a micro-manager. In his book Steve Jobs, Walter Isaacson describes how Jobs picked shades of white for Apple Store bathroom tiles and worked on the design of the iPhone box. He had to sign off on every product Apple made, down to and including the iPhone charger. His employees feared, loved and worshiped him, and they followed him into the fire. Jobs could change the direction of the company on a dime — that was what it took to deliver black i-swans. Jobs is gone, so the probability of another product achieving the success of the iPhone or iPad has declined exponentially.

***

***

What is really amazing about Apple is how underwhelming its valuation is today — it doesn’t require new black swans.

In an analysis we tried very hard to kill the company. We tanked its gross margins to a Nokia-like 28 percent and still got $30 of earnings per share (the Street’s estimate for 2013 is $45), which puts its valuation, excluding $145 a share in cash, at 10 times earnings. We killed its sales growth to 2 percent a year for ten years, discounted its cash flows and still got a $500 stock.

There is a lot of value in Apple’s enormous ability to generate cash. The company is sitting on an ever-growing pile of it — $137 billion, about one third of its market cap. Over the past 12 months, despite spending $10 billion on capital expenditures, Apple still generated $46 billion of free cash flows. If it continues to generate free cash flows at a similar rate (I am assuming no growth), by the end of 2015 it will have stockpiled $300 of cash per share. At today’s price [2013] it will be commanding a price-earnings ratio (if you exclude cash) of 4.

Of course, the market is not giving Apple credit for its cash, but I think the market is wrong. Unlike Microsoft, which does something dumber than dumb with its cash every other year, Apple has a pristine capital allocation track record. It has not made any foolish acquisitions — or, indeed, any acquisitions of size. Other than buying an Eastern European country and renaming it i-Country, Apple will not be able to acquire a technologically related company of size, nor will it want or need to. The cash it accumulates will end up in shareholders’ hands, either through dividends or share buybacks.

What is Apple worth?

After the financial acrobatics I’ve done trying to murder the valuation of Apple, it is easier to say that it is worth more than $450 than to pinpoint a price target. When I use a significantly decelerating sales growth rate and normalize margins (reducing them, but not as low as Nokia’s current margins), I get a price of about $600 to $800 a share.

Growth managers don’t want Apple to pay a large dividend, as though that would somehow transform this growing teenager into a mature adult. But I have news for them: Apple already is a mature adult. Second, when your return on capital is pushing infinity (as Apple’s is), you don’t need to retain much cash to grow. Two thirds of Apple’s cash is offshore, but that doesn’t make it worthless; it just makes it worth less — only $65 billion, maybe, not $97 billion, once the company pays its tax bill to Uncle Sam.

***

***

Assessment

In the short term none of the things I am writing about here will matter. Remember, “Everyone knows Apple is going to $300,” as a client recently e-mailed me, as everyone knew it was going to a $1,000 a few months ago when Apple’s stock was trading at $700. The company’s stock will trade on emotion, fundamentals will not matter, and growth managers will likely rotate out of Apple, because once the stock declined from $700 to $450, the label on it changed from “growth” to “value.”

But ultimately, fundamentals will prevail. Like the laws of physics, they can only be suspended for so long. And so, do these retrospective thoughts on Apple hint of future prospects?

More: Should You Buy Apple Stock Ahead of Its September Event …

ABOUT

Vitaliy N. Katsenelson CFA is Chief Investment Officer at Investment Management Associates in Denver, Colo. He is the author of Active Value Investing (Wiley 2007) and The Little Book of Sideways Markets (Wiley, 2010). His books were translated into eight languages. Forbes Magazine called him “The new Benjamin Graham”.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Front Matter with Foreword by Jason Dyken MD MBA

![]()

***

Filed under: Experts Invited, Investing | Tagged: Android, Apple Inc, behavioral economics, behavioral finance, microsoft, Nexus 7, Nokia, psychology, Steve Jobs, Vitaliy Katsenelson CFA, Warren Buffett | 3 Comments »

![]()

An Encore Presentation

[By Steve Blank]

A team of 110 researchers and clinicians, in therapeutics, diagnostics, devices and digital health in 25 teams at UCSF, has just shown us the future of translational medicine. It’s Lean, it’s fast, it works and it’s unlike anything else ever done.

It’s going to get research from the lab to the bedside cheaper and faster.

Lean LaunchPad for Life Sciences and Healthcare

Welcome to the Lean LaunchPad for Life Sciences and Healthcare (part of the National Science Foundation I-Corps).

This post is part of our series on the Lean Startup in Life Science and Health Care.

***

***

The Class

Our class talked to 2,355 customers, tested 947 hypotheses and invalidated 423 of them. They had 1,145 engagements with instructors and mentors. (We kept track of all this data by instrumenting the teams with LaunchPad Central software.)

In a packed auditorium in Genentech Hall at UCSF, the teams summarized what they learned after 10 weeks of getting out of the building. This was our version of Demo Day – we call it “Lessons Learned” Day. Each team make two presentations:

Assessment

In the next few posts I’m going to share a few of the final “Lessons Learned” presentations and videos and then summarize lessons learned from the teaching team.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

“When a practicing physician thinks about their risk exposure resulting from providing patient care, medical malpractice risk immediately comes to mind. But; malpractice and liability risk is barely the tip of the iceberg, and likely not even the biggest risk in the daily practice of medicine. There are risks from having medical records to keep private, risks related to proper billing and collections, risks from patients tripping on your office steps, risks from medical board actions, risk arising from divorce, and the list goes on and on. These liabilities put a doctor’s hard earned assets and career in a very vulnerable position.

These new books from Dr. David Marcinko and Prof. Hope Hetico show doctors the multiple types of risk they face and provides examples of steps to take to minimize them. They are written clearly and to the point, and are a valuable reference for any well-managed practice. Every doctor who wants to take preventive action against the risks coming at them from all sides needs to read these books.”

Richard Berning MD FACC [New Haven, Connecticut, USA]

***

Filed under: Career Development, Experts Invited, Information Technology, Practice Management, Videos | Tagged: evidence based medicine, Future of Translational Medicine, Lean LaunchPad for Life Sciences and Healthcare, National Science Foundation I-Corps, Steve Blank, UCSF | Leave a comment »

![]()

More on Evidence-Based Translational Medicine

By Steve Blank

We have learned a remarkable process that allow us to be highly focused, and we have learned a tool of trade we can now repeat. This has been of tremendous value to us.

Andrew Norris

Principal Investigator BCN Biosciences

Over the last three years the National Science Foundation I-Corps has taught over 700 teams of scientists how to commercialize their technology and how to fail less, increasing their odds for commercial success.

To see if this same curriculum would work for therapeutics, diagnostics, medical devices and digital health, we taught 26 teams at UCSF a life science version of the NSF curriculum. 110 researchers and clinicians, and Principal Investigators got out of the lab and hospital, and talked to 2,355 customers. (Details here)

For the last 10 weeks 19 teams in therapeutics, diagnostics and medical devices from the National Institutes of Health (from four of the largest institutes; NCI, NHBLI, NINDS, and NCATS) have gone through the I-Corps at NIH.

87 researchers and clinicians spoke to 2,120 customers, tested 695 hypotheses and pivoted 215 times. Every team spoke to over 100 customers.

Three Big Questions

The NIH teams weren’t just teams with ideas, they were fully formed companies with CEO’s and Principal Investigators who already had received a $150,000 grant from the NIH. With that SBIR-Phase 1 funding the teams were trying to establish the technical merit, feasibility, and commercial potential of their technology. Many will apply for a Phase II grant of up to $1 million to continue their R&D efforts.

Going into the class we had three questions:

Evidence-based Translational Medicine

We’ve learned that information from 100 customers is just at the edge of having sufficient data to validate/invalidate a company’s business model hypotheses. As for whether you can/should push scientists past their comfort zone, the evidence is clear – there is no other program that gets teams anywhere close to talking to 100 customers. The reason? For entrepreneurs to get out of the building at this speed and scale is an unnatural act. It’s hard, there are lots of other demands on their time, etc. But we push and cajole hard, (our phrase is we’re relentlessly direct,) knowing that while they might find it uncomfortable the first three days of the class, they come out thanking us.

The experience is demanding but time and again we have seen I-Corps teams transform their business assumptions. This direct interaction with potential users and customers is essential to commercialize science (whether to license the technology or launch a startup.) This process can’t be outsourced. These teams saved years and millions of dollars for themselves, the NIH and the U.S. taxpayer. Evidence is now in-hand that with I-Corps@NIH the NIH has the most effective program for commercializing science.

Lessons Learned Day

Every week of this 10 week class, teams present a summary of what they learned from their customers interviews. For the final presentation each team created a two minute video about their 10-week journey and a 8-minute PowerPoint presentation to tell us where they started, what they learned, how they learned it, and where they’re going. This “Lessons Learned” presentation is much different than a traditional demo day. It gives us a sense of the learning, velocity and trajectory of the teams, rather than a demo day showing us how smart they are at a single point in time.

BCN Biosciences

This video from team BCN Biosciences describes what the intensity, urgency, velocity and trajectory of an I-Corps team felt like. Like a startup it’s relentless.

BCN is developing a drug that increases anti-cancer effect of radiation in lung cancer (and/or reduces normal tissue damage by at least 40%). They were certain their customers were Radiation Oncologists, that MOA data was needed, that they needed to have Phase 1 trial data to license their product, and needed >$5 million and 6 years. After 10 weeks and 100 interviews, they learned that these hypotheses were wrong.

If you can’t see the BCN Biosciences video click here

The I-Corps experience helped the BCN Bioscience team develop an entirely new set set of business model hypotheses – this time validated by customers and partners. The “money slides” for BCN Biosciences are slides 22 and 23.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

“When a practicing physician thinks about their risk exposure resulting from providing patient care, medical malpractice risk immediately comes to mind. But; malpractice and liability risk is barely the tip of the iceberg, and likely not even the biggest risk in the daily practice of medicine. There are risks from having medical records to keep private, risks related to proper billing and collections, risks from patients tripping on your office steps, risks from medical board actions, risk arising from divorce, and the list goes on and on. These liabilities put a doctor’s hard earned assets and career in a very vulnerable position.

These new books from Dr. David Marcinko and Prof. Hope Hetico show doctors the multiple types of risk they face and provides examples of steps to take to minimize them. They are written clearly and to the point, and are a valuable reference for any well-managed practice. Every doctor who wants to take preventive action against the risks coming at them from all sides needs to read these books.”

Richard Berning MD FACC [New Haven, Connecticut, USA]

Filed under: Career Development, Experts Invited, Information Technology, Practice Management, Videos | Tagged: evidence based medicine, Evidence-Based Translational Medicine, I-Corps at the NIH, Steve Blank, Translational Medicine | Leave a comment »

![]()

A ten-point plan for aspiring software entrepreneurs

By Lynne Strang – lbstrang@gmail.com

***

***

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

8

Filed under: Experts Invited, Research & Development | Tagged: medical startups, Starting a Software Business | Leave a comment »

![]()

Devastating?

[By Austin Frakt PhD]

[By Austin Frakt PhD]

Noam Schieber’s NYT piece today is devastating.

About selecting papers to be most prominently featured at a top economics conference, David Card is quoted,

“‘I choose papers that are going to be written up’ in the mainstream press. […] ‘It’s what the people want.’”

via Non-financial conflicts of interest.

***

***

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Assessment

Has this philosophy seeped into medicine, the financial services industry and health economics; etc?

Dr. David Edward Marcinko MBA

More: Another report casts skeptical eye on patient satisfaction surveys

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Sponsors Welcomed

And, credible sponsors and like-minded advertisers are always welcomed.

Support the “Medical Executive-Post”

***

UPDATE

Conflicts of interest, the NEJM, and where we go next

Posted: 04 Jun 2015 03:20 PM PDT

If you haven’t yet, take a look at Lisa Rosenbaum’s NEJM essays (here, here, and here) calling for new thinking about researchers and financial conflicts of interest. The essays are nuanced and go against the grain of much recent writing on research ethics.

Rosenbaum’s essays have generated many responses (the Lown Institute has collected some of them here). I examine Rosenbaum’s views in an essay in the New Republic. I’m sympathetic to many of her arguments, but I think we need more transparency in science, not less (see also here). Austin explores her views here, here, and here. Rosenbaum has elicited some exceptionally harsh rejoinders, including one from two former editors-in-chief of the NEJM.

This discussion has been intense because the stakes are very high. If manipulated research data allow bad drugs to enter the market, people can die. Conversely, if unjustified prejudice against industry slows the progress of research, that could kill people too.

Filed under: Ethics, Experts Invited, Health Economics | Tagged: Austin Frakt PhD, Noam Schieber's, Non-financial conflicts of interest | Leave a comment »

Competent, Ethical and Fair Legal Representation for Doctors

Wretched creatures are compelled by the severity of the torture to confess things they have never done and so by cruel butchery innocent lives are taken; and by new alchemy, gold and silver are coined from human blood.– Father Cornelius Loos (1592)

***

[“PHP-Approved Attorneys”]

***

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

8

Filed under: Experts Invited, Health Law & Policy, Professional Liability, Risk Management | Tagged: A New Niche area for [HealthLaw] Attorneys, Competent, Ethical and Fair Legal Representation for Doctors, Michael Lawrence Langan MD | 1 Comment »

![]()

Disruptive Technologies in Medicine

[By Dr. Bertalan Meskó]

Recently, I gave a talk to medical students about what kind of trends and technologies might shape the future and I was very curious what they think about these.

The Question

I asked them to give a score between 1 and 3 about how beneficial or advantageous those can be for society; and a score between 1 and 3 about how big threats they will pose to us.

They also gave a score between 1 and 10 about how much they look forward to using a technology in action. See the full size infographics here.

The Answer

So, I just wrote about how our Disruptive Technologies in Medicine university course prepares medical students for the coming waves of change. I also recently published an infographic related to new technologies in medicine.

***

***

Assessment

Preparing them for the future is a real challenge but I remain confident that we need to to that and it is still possible.

***

***

More:

***

FUTURISTIC MEDICAL INTERFACE

Our touch screen presentations bring the future directly to your exhibition stand, shop, museum, hospital or even your tv show or movie! No prerendered elements!

It’s realtime!

LINK: https://www.behance.net/gallery/14374555/FUTURISTIC-MEDICAL-INTERFACE

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Experts Invited, Information Technology | Tagged: Bertalan Meskó, Disruptive Technologies in Medicine, health information technology, How Do Medical Students View Future Technologies? | 3 Comments »

![]()

Seriously?

[By Vitaliy N. Katsenelson, CFA]

I never thought I’d be giving writing advice. I was always the worst student in my literature class in Russia. I never received a grade higher than a C on any Russian essay I ever wrote. I have a theory that my teachers got sick of reading and grading my horrible essays, so they stopped and automatically gave me a passing grade out of pity. I don’t blame them.

I never thought I’d be giving writing advice. I was always the worst student in my literature class in Russia. I never received a grade higher than a C on any Russian essay I ever wrote. I have a theory that my teachers got sick of reading and grading my horrible essays, so they stopped and automatically gave me a passing grade out of pity. I don’t blame them.

When I came to the U.S., my grades in English class in college were not spectacular either; in fact, English was the only class I failed in college and actually had to retake my senior year.

My writing has improved slightly since then – and you, my loyal readers, get to be the judge of my scribbles. However, if the prequalification for giving writing advice was based solely on quantity – on how many words have blackened a perfectly fine white screen or besmirched innocent paper – then I am more than qualified. I have been at it for exactly a decade.

My writing “career” started in 2004 when I was hired as a writer by TheStreet.com. I was not hired because I was good – I wasn’t. But I had an investing background, and TheStreet.com was not very picky; it needed warm bodies (ideally with CFA next to their names) to comment on the markets and stocks. TheStreet.com paid almost nothing, and it was overpaying me.

I had zero experience, but I was ambitious. I took writing very seriously, and therefore my articles were serious. They were filled with big words, and, quite frankly, they were enormously boring. In addition, I was extremely self-conscious about grammar. Sentence structure and punctuation drove me nuts, and I was afraid of confusing words that were spelled similarly but had unrelated meanings (like comma and coma).

***

***

LESSONS LEARNED

This brings me to the first lesson that I want to impart about writing, and it’s one that will drive English teachers insane: Don’t worry about grammar.

Once I stopped worrying about grammar, I felt a huge weight lifted from my shoulders (as all those little punctuation marks emptied themselves from my brain). I completely gave up on a, an and the (my 12-year-old son, who was born here, does a great job fixing those for me), I stopped obsessing about commas (and comas), and I stopped trying to ferret out all the other marvelous secrets of English grammar. I let copy editors – who are very talented and oh so skilled at this – catch me out in all my little peccadilloes. Instead I channel my energy into making writing interesting and funny (if appropriate); this is Lesson No. 2.There are a lot of smart investors, and a lot of them write (just visit the web site Seeking Alpha), but only a small fraction manage to make their writing interesting (again, just visit Seeking Alpha) – and those are the ones who are read more than once.

As I mentioned, when I started writing, my articles were technical and boring. I still feel sorry for the people who read them and especially for my dear friends who felt an obligation to read them.

Then an accident happened. Six months into writing for TheStreet.com, I wrote about the digital video recorder company TiVo. In that article I dared to use a little bit of humor to describe a painful experience I had when I called TiVo’s automated telephone customer service, which did not seem to understand my “slight” Russian accent. To my embarrassment, I had to ask my three-year-old son, who by that time had already acquired a perfect “Disney” accent, to talk to the machine instead, and of course it understood him just fine.

That article was not brilliant – it contained as many or as few insights as my previous articles did – but it was not “proper,” and it was not boring. Suddenly, the feedback from readers was much different – I received a ton of e-mail. Then I understood the power of humor. But it was not just humor: I was able to deliver my otherwise boring message in an interesting way.

I realized that knowing what you want to say is not enough; you need to figure out how to say it.

To this day, I spend hours staring at the computer, trying to come up with an interesting analogy or a compelling angle on how to say something I already know. I often use analogies to tell a story, especially if the topic is complex. They help me relate complex ideas through simple examples.

Let me illustrate. I have a very smart investor friend of German ancestry. True to his roots, he is very efficient in everything he does. (I am stereotyping here, but why not?) He has written a very smart investment book. If you read the whole thing, you’d learn a lot. But that is a big if. His book is as efficient and properly structured as you would expect from a well-engineered German car or an instruction manual for that car. It doesn’t have an extra word or a superfluous sentence. But unfortunately, in the process of making it efficient, he sterilized his book. I was excited to read it but could not get past Chapter 3. I got terminally bored, and I do investments for a living.

Oh, and while we’re on the subject of boredom: Follow novelist Elmore Leonard’s advice when he said, “I try to leave out the parts that people skip.” Don’t try to be descriptive for the sake of being descriptive.

Andrew Blum in 2012 wrote a terrific book called Tubes: A Journey to the Center of the Internet . However, in his other life Andrew is a reporter who covers architecture. His job is to describe inanimate objects. In Tubes he often goes into “descriptive mode,” telling us all about things that do not need to be described. For example, at one point he falls into an exhaustive description of the hotel he stayed in near the Los Angeles International Airport. The hotel room had nothing to do with the story, but he went on and on, describing bars of soap, their colors, the plate they were on and how the sunlight bounced off each one of them.

After making it through the third chapter, I gave up and downloaded the audiobook of Tubes. So maybe Andrew succeeded after all, since I ended up buying two versions of his book. (And I do highly recommend listening to his book if you want to learn about the Internet.)

It took a while for my writing style to develop. A big part of its development came through reading great writers. The two people who had the most impact on me were John Mauldin and Cliff Asness.

John needs no introduction, as his economics newsletter (Mauldin Economics) is read by millions. He has a gift for explaining complex investment topics simply, but he also invites you into his life. He shares stories about the trips he takes and the people he meets; he talks about his kids and their travails, his lack of time for the gym and his penchant for cooking mushrooms. When you read him, you feel as if he’s writing for you – just you. This is different from fiction writing, in which the author’s fingerprints are hidden.

Cliff Asness has had a tremendous impact on me as well. Cliff is a hedge fund manager; he runs the large quant firm AQR Capital Management in Greenwich, Connecticut. Cliff has an incredible gift for being witty. Back in 2005 I read a paper by Cliff discussing the most boring topic on earth: the expensing of employee stock options. At the time, companies did not consider them an expense. Cliff argued that the companies were wrong and needed to show the options on their income statements, just like any other expense.

I had written on the same topic just a few months before, making a similar point. But after I read his paper, I sent Cliff an e-mail with the subject line “I am not worthy.” Cliff’s paper was published in the most boring finance magazine in the whole universe: Financial Analysts Journal (every article in it is full of geeky Greek symbols). To my astoundment, Cliff was able to inject humor where I thought it was not possible. I wrote a very boring, unmemorable article on stock options; Cliff wrote a great, funny article on the same topic that I still remember today.

John Mauldin showed me through his writing that it’s okay to be personal, and Cliff proved it is okay to be funny. No, Cliff proved that you must be funny when you discuss boring topics – this is how you make the reader stick with it. Lesson No. 3: Identify your favorite writers, the ones whose voices you can really relate to, and learn from them.

I could relate to John’s and Cliff’s writings because they fit my personality and my natural writing style. They liberated me from being sanitized, impersonal and boring.

A sublesson here is, Read to write. When you read, always have your writer’s hat on, and pay attention not just to content but to the quality of the writing as well. That is not something that comes automatically to most of us; we have to manually hit the “on” switch.

Lesson No. 4: Be respectful of your environment. This is not an ecological statement; I am talking about your writing environment. If you write long enough, you start to appreciate the importance of your external and internal environment. Stephen King, in his terrific book On Writing: A Memoir on the Craft , said that he listens to heavy metal band AC/DC when he writes; he feels it walls him off from the external world and helps him build his own worlds. I listen to classical music, and if I am really stuck, I start listening to opera.

And if that weren’t weird enough, I write only in italics. This little trick makes my letters look a bit friendlier to me. If you find that you like your font to be pink, go for it. We writers need any edge we can get, and you can always change back to a color and format that is acceptable to society when you are done.

The final lesson: Be prepared for pain – or maybe not. Writing is a very personal process. Some of us are great thinkers, able to puzzle through very complex ideas in our heads and lay them out logically on paper. I have tremendous respect for those lucky ones. For most of us, present company included, writing is usually a painful endeavor that involves staring at a blank screen for hours on end and writing and rewriting multiple times.

In fact, let me take it a step farther: I think through writing. A quote from George Bernard Shaw comes to mind: “Few people think more than two or three times a year; I have made an international reputation for myself by thinking once or twice a week.”

If you ask me a question about something I have not thought about before, even if you give me a minute to think about it, my answer will usually, well … suck. I have not written about that topic yet, and so I may not have thought it through, and the logical links may not have been made. That’s just how my mind operates.

Quite frankly, I am embarrassed for my brain. It’s like the dirty apartment of a confirmed bachelor, with unwashed clothes, empty pizza boxes and beer bottles all over the floor. For an idea to be developed to the point at which it can leave the room, I have to clean it up, organize it, put things in their rightful place. That is why I write – sorry, dear reader, it’s not about you; it’s about me, me and me again.

***

***

More:

ASSESSMENT

Writing is not a linear process, and when you sit down to write, your thoughts may not be quite ready to come out – it’s okay if they just haven’t come to a boil yet. Don’t blame it on writer’s block. Author Tom Clancy once said, “Writer’s block is just an official term for being lazy, and the way to get through it is work.” Just take some time off, do something fun and then get back on the writing horse.

ABOUT

Vitaliy N. Katsenelson, CFA, is Chief Investment Officer at Investment Management Associates in Denver, Colo. He is the author of The Little Book of Sideways Markets (Wiley, December 2010). To receive Vitaliy’s future articles by email or read his articles click here.

Investment Management Associates Inc. is a value investing firm based in Denver, Colorado. Its main focus is on growing and preserving wealth for private investors and institutions while adhering to a disciplined value investment process, as detailed in Vitaliy’s book Active Value Investing (Wiley, 2007).

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Filed under: Career Development, Experts Invited, iMBA, Investing, Op-Editorials | Tagged: Andrew Blum, AQR Capital Management, Elmore Leonard, TheStreet.com, Vitaliy N. Katsenelson, writing advice | 1 Comment »

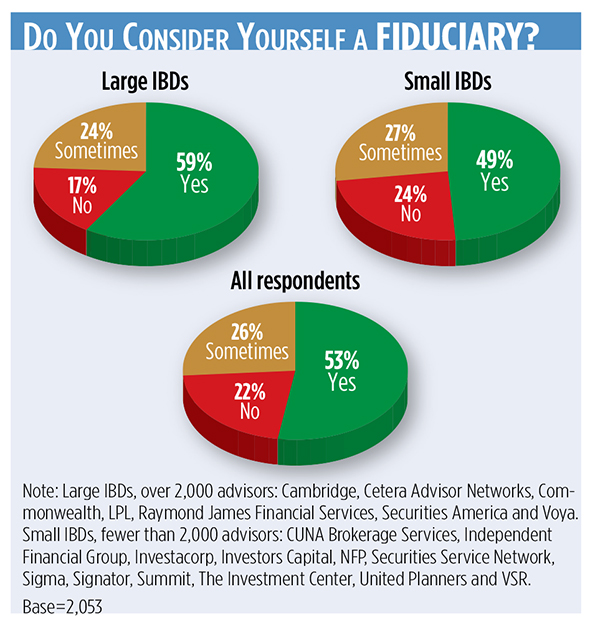

2015 IBD Report Card

By Diana Britton of WealthManagement

***

***

Link: http://wealthmanagement.com/ibd-report-card

How This Survey Was Conducted: Between Jan. 14 and Feb. 25, 2015, REP. magazine emailed invitations to participate in an online survey to print subscribers and advisors in the Meridian-IQ database at over 80 independent broker/dealers. By Feb. 25, a total of 2,069 completed responses were received. Brokers rated their current employers on several items related to their satisfaction. Ratings are based on a 1-to-10 scale, with 10 representing the highest satisfaction level.

Note: Large IBDs, over 2,000 advisors: Cambridge, Cetera Advisor Networks, Commonwealth, LPL, Raymond James Financial Services, Securities America and Voya. Small IBDs, fewer than 2,000 advisors: CUNA Brokerage Services, Independent Financial Group, Investacorp, Investors Capital, NFP, Securities Service Network, Sigma, Signator, Summit, The Investment Center, United Planners and VSR.

More:

Read even more:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

***

***

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Filed under: Experts Invited | Tagged: "The Wall Street Casino", Diana Britton., fiduciary | Leave a comment »

![]()

Filed under: Experts Invited, iMBA, Practice Management | Tagged: experts invited, MEDICAL PRACTICE ADVERTISING, medical practice management, medical practice marketing, Practice Management | Leave a comment »

![]()

[By Edward Bukstel]

***

***

***

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Experts Invited, Information Technology | Tagged: Edward Bukstel, mHealth; mobile Health, Mobile-Health or Global Economy? | 4 Comments »

![]()

The Elephant in the Room

[By Michael Lawrence Langan MD]

***

***

[Courtesy SplitShire]

***

More:

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

* 8

Filed under: Ethics, Experts Invited | Tagged: Michael Lawrence Langan MD, physician suicide | 7 Comments »

![]()

***

***

***

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

Filed under: Experts Invited, Health Economics, Practice Management, Research & Development, Risk Management | Tagged: Edward Bukstel, The Wharton School of Business, Why Healthcare is F@#Ked ! | Leave a comment »

![]()

Our Newest Text Book-in-Production

http://www.CertifiedMedicalPlanner.org

[By Ann Miller RN MHA]

![]()

***

***

***

Skills Needed

If you are a physician, nurse, accountant, attorney, medical risk manager or healthcare executive, we need you.

Form below or contact us for details to peer-review, etc. MarcinkoAdvisors@msn.com

Assessment

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

[Companion Text Book]

Filed under: CMP Program, Experts Invited, Insurance Matters, Professional Liability, Risk Management | Tagged: CMP Program, malpractice, malpractice insurance, medical liability, medical risk management, www.CertifiedfMedicalPlanner.org | 2 Comments »

![]()

Who needs it … What for?

[By Ann Miller RN MHA]

What’s the point of publishing your essays, thoughts, comments and articles on this ME-P?

Today, many physicians, FAs and health economic experts still don’t have the potential to express themselves to a large audience. By adding articles to their own blogs, with poor attendance, they deprive a wide audience of the opportunity to familiarize themselves with their works.

That’s why material from our ME-P website is available to all English-speaking inhabitants of the world. Some website owners even visit our web portal to pick up or re-post the best articles to place on their own websites.

Why publish with the ME-P?

All this is interesting, but what is the use of the website to an author? So, here is what you get by publishing with us:

• A unique method of promoting your website, self, financial advisory or medical practice; or ideas. If your essay is really interesting – many others will want to read our related books, white-papers and texts; so you will become well-known among our readers.

• The content of our website is automatically placed on other main web sources via RSS feeds. By this you can attract a wide range of readers – and with little effort. The readers will get acquainted with your thoughts, articles and the personal data you share in your included profile.

• Our website is a great launching pad for new doctors, starting academics, medical practitioners, FAs, CPAs, health economists and fledgling writers. By publishing your articles here, you will be able to raise your prestige among colleagues and ME-P readers.

• You may use any free articles from our website to fulfill your own web project (you must add a link to our original material) via RSS feeds. The probability that someone will be interested in you is increased many times.

• Everyday our website is visited by many people, and their numbers are growing constantly. By adding articles the number of your readers will grow in geometric sequence.

• Once placed on the ME-P, your essay will stay on our website [almost] forever. All published materials [probably] will not be deleted with the lapse of time. This means that many years later – your articles will be still available to everyone.

Assessment

The number of ME-P subscribers and regular visitors is growing rapidly. And, the traffic to our authors’ web sources are growing too. Join us – we welcome all authors who are willing to cooperate with our vision and mission!

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

![]()

* 8

Filed under: Experts Invited, iMBA, Inc. | Tagged: ME-P, medical executive post | 1 Comment »

![]()

By Eugene Schmuckler PhD MBA MEd CTS [Academic Provost]

About the Medical Executive-Post

We are an emerging online and onground community that connects medical professionals with financial advisors and management consultants.

We participate in a variety of insightful educational seminars, teaching conferences and national workshops. We produce journals, textbooks and handbooks, white-papers, CDs and award-winning dictionaries. And, our didactic heritage includes innovative R&D, litigation support, opinions for engaged private clients and media sourcing in the sectors we passionately serve.

Through the balanced collaboration of this rich-media sharing and ranking forum, we have become a leading network at the intersection of healthcare administration, practice management, medical economics, business strategy and financial planning for doctors and their consulting advisors. Even if not seeking our products or services, we hope this knowledge silo is useful to you.

In the Health 2.0 era of political reform, our goal is to: “bridge the gap between practice mission and financial solidarity for all medical professionals.”

More: Letterhead.iMBA_Inc.

***

***

Enter the Certified Medical Planners™

There is no certification program, course of study or professional designation for FAs who wish to enter the lucrative financial planning space serving physicians and healthcare professionals.

That’s why the R&D efforts of our governing board of physician-directors, accountants, financial advisors, academics and health economists identified the need for integrated personal financial planning and medical practice management as an effective first step in the survival and wealth building life-cycle for physicians, nurses, healthcare executives, administrators and all medical professionals.

Now – more than ever – desperate doctors of all ages are turning to knowledge able financial advisors and medical management consultants for help. Symbiotically too, generalist advisors are finding that the mutual need for extreme niche synergy is obvious.

But, there was no established curriculum or educational program; no corpus of knowledge or codifying terms-of-art; no academic gravitas or fiduciary accountability; and certainly no identifying professional designation that demonstrated integrated subject matter expertise for the increasingly unique healthcare focused financial advisory niche … Until Now!

Enter the Certified Medical Planner™ charter professional designation. And, CMPs™ are FIDUCIARIES, 24/7.

Video: http://vimeo.com/84247360

An Interview with Bennett Aikin AIF®

Physician-Investors and the “F” Word

More:

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES: