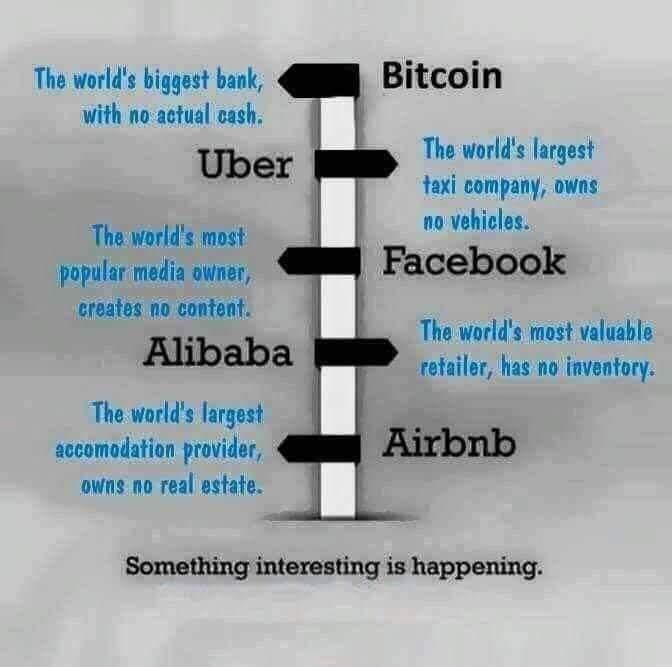

Supply Chain Service Management?

[By staff reporters]

***

***

8

8

Share this:

Filed under: Investing | Tagged: Asset Lite Companies | Leave a comment »

ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

![]()

![]()

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

![]()

ePodiatryConsentForms.com

ePodiatryConsentForms.com

“Providing Management, Financial and Business Solutions for Modernity”

“Providing Management, Financial and Business Solutions for Modernity”

Supply Chain Service Management?

[By staff reporters]

***

***

8

Filed under: Investing | Tagged: Asset Lite Companies | Leave a comment »

Investing in Financial Counseling

By Rick Kahker MSFS CFP By Rick Kahker MSFS CFP

As a long-time advocate of blending financial planning with counseling, I’ve had years of seeing the benefit for clients. I have come to see financial counseling as an investment: one that can pay greater dividends than investments in a home, retirement account, or college education.

|

Filed under: Experts Invited, Investing, Op-Editorials | Tagged: Financial Counseling | Leave a comment »

My Interview with Danielle Town

By Vitaliy Katsenelson, CFA

Today I’d like to share with you an interview I did with my friend Danielle Town. Danielle is coauthor of Invested and runs the Rule #1 Finance blog with her father, Phil Town.

Danielle put me on the proverbial podcast couch; and though originally we were going to talk about investing, well, we talked about everything but investing. We ended up delving into many personal topics I rarely discuss. I went down memory lane about growing up in Soviet Russia, my family’s immigration to the US in 1991 and our first years in the US, my parents’ attitude towards money, budgeting, creativity, sleep, writing, a book I am working on, and more.

This interview ran so long it was broken up into two parts (Listen to Part 1 here and Part 2 here). I don’t think I could have done this interview talking to a stranger. It turned into a conversation between friends.

We decided that we are going to go back and talk about investing next time. Maybe we’ll do another interview when I see her in Switzerland in January, where we’ll both attend VALUEx Klosters.

Assessment: Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

THANK YOU

Filed under: Investing, Videos | Tagged: Danielle Town, Vitaliy Katsenelson CFA | Leave a comment »

Not Really a Safe – SAFE?

By Rick Kahler CFP®

I have routinely recommended that people use a bank safe deposit box to store valuable papers and small assets. These include documents like wills, trust documents, ethical wills, and unrecorded deeds. Valuable assets would include diamonds, gemstones, jewelry, bullion, and small collectables like rare coins, stamps, and trading cards.

The physical protection of a bank vault, plus a system of access requiring two keys kept by the customer and the bank, would seem to provide a great deal of security. Yet several recent news articles suggest safe deposit boxes may not be as safe as they seem.

Report

An article in the New York Times reported 44 robberies in the last five years related to safe deposit boxes. Even worse were numerous bank errors in which boxes were moved, misplaced, drilled open, or closed by mistake. A large Maryland bank closed several branches and lost hundreds of safe deposit boxes. One customer lost $500,000 worth of gold and gems.

In each case, banks vigorously fought any requirement to make their customers whole. Even more shocking, no provision of federal banking law regulates safe deposit boxes.

Nor do banks insure the belongings of customers who trustingly store their most precious valuables in safe deposit boxes. The risks fall on the renter. Wells Fargo’s safe deposit box contract caps the bank’s liability at $500. Citigroup limits it to 500 times the box’s annual rent. JPMorgan Chase has a $25,000 ceiling on its liability.

***

***

My Story

Decades ago, I placed some rare coins in a safe deposit box with a local bank. A few years ago I went to retrieve my valuables, only to find the bank had drilled open the box and sent the contents to the state as abandoned property. I learned that when I relocated my office, the change of address notification failed to carry through to the annual billing notice for the safe deposit box fee. After three years of non-payment, the bank chose to go through the effort of drilling open the box and shipping the contents to the State Treasurer’s office. It would have been simpler to spend a few minutes looking up my information and contacting me.

Eventually I was able to retrieve the contents of the box. I was lucky.

An international expert in rare watches stored 92 watches plus rare coins, worth millions, in a safe deposit box at a Wells Fargo bank branch. Wells Fargo had evicted another customer for non-payment and drilled open the wrong safe deposit box. The customer found his “safe” deposit box empty. Wells Fargo executives could only find 85 of his watches.

The customer sued. Wells Fargo admitted in court that its employees had mistakenly drilled into and terminated the box. The unrecovered items included gold coins and a watch estimated to be worth nearly a million dollars. After years of litigation and appeals, Wells Fargo has offered no restitution.

If a “safe” deposit box isn’t really safe, what can you do instead?

Here are a few suggestions.

1. Consider investing in a high-quality home safe for small valuables and important documents.

2. Scan all important documents and save copies in a secure online “vault.” Many financial planners provide such online backup storage.

3. If you do use a safe deposit box, choose one at the bank you use regularly and open it at least once a year.

4. No matter where you keep your valuables, insure them adequately. Standard homeowner coverage is probably not enough.

5. Share passwords and access codes with another trusted person.

Finally, ask before you store. Understand a bank’s policies and coverage limits before you trust it with your valuables.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

8

8

***

Filed under: Investing, Risk Management | Tagged: banks, safety deposit box | 2 Comments »

HOW I EARN – AND YOU PROFIT!

By Dr. David E. Marcinko MBA

My fee is $250 per hour prorated, so you only pay for the time used. This fee covers almost any medical practice management, insurance and risk management, personal financial planning or investment-related topic, including document review, phone consultation, research, and written investment strategies.

I also offer a special program for first-time potential clients called a Physician Practice-Portfolio Second Opinion™. This all-inclusive $450 program takes about two hours in total and includes a pre-call document review, 60-minute phone consultation, and summary with observations and recommendations.

Docotor colleagues find this to to be a good value because their questions are answered under one fee.

So, it does not matter if you are a new, mid-career or mature practitioner, or where your money is invested or how much you have invested. Simply, I serve along side you as a fiduciary by upholding a duty of loyalty, fairness and good faith in all decision making.

At your professional service!

THANK YOU

Dr. David Edward Marcinko MBA MEd CMP™

Certified Medical Planner™

phone: 770-448-0769

MarcinkoAdvisors@msn.com

***

8

***

Filed under: Financial Planning, Investing | Leave a comment »

By Dr. David E. Marcinko MBA

Courtesy: www.CertifiedMedicalPlanner.org

Evaluating “Sham” Risk Aversion Determination Methodologies

BACK STORY: You visit a local financial advisor as a prospective client. S/he gives you a form to complete that purports to discern your investing risk tolerance?

FORM: It says: “Please indicate by ranking the items below from 1 to 4, with 1 being the most descriptive and 4 being the least descriptive”.

LINK: https://medicalexecutivepost.com/2009/12/28/risk-aversion-and-investment-alternatives/

EPIPHANY: After reviewing the form, you realize it is a superfluous one-size-fits-all risk reduction mechanism for the advisor. You identify the sheer malarkey of the exercise and leave in disgust. You ruminate to yourself – “there must be a better way,”

MORE: https://medicalexecutivepost.com/2017/10/24/on-investing-risk-tolerance/

And so, colleague Rick Kahler MSFS CFP® suggests alternative methods.

MORE: https://medicalexecutivepost.com/2017/10/18/on-retirement-planning-risks/

Your thoughts are appreciated.

***

***

***

BUSINESS, FINANCE AND ECONOMICS TEXTBOOKS FOR DOCTORS:

THANK YOU

8

***

Filed under: Investing, Op-Editorials | Tagged: financial metrics, financial shenanigans | 1 Comment »

Bonds an Investment Class Worth Some Excitement, Today?

By Rick Kahler CFP®

| “One thing I definitely don’t want in my portfolio is bonds,” a prospective client told me a few weeks ago. “Bonds are boring and don’t give good returns.”

Her confidence in her money script that bonds had no place in her portfolio was palpable. However, her understanding of the role bonds play in a portfolio was incomplete. I restrained myself from launching into a lecture on the importance of bonds and simply replied, “While it is true bonds can be boring, sometimes they can be phenomenally exciting.” Certainly stocks, commodities, and real estate investments are generally much more exciting. They are many times more volatile than bonds; in just a year it’s possible they might even gain or decline 50% in value. Meanwhile, individually held bonds and their mutual funds can crank out predictable coupon yields quarter after quarter after quarter, with one-third of the volatility of stocks. The cost of the lower volatility is that the long-term returns on bonds tend to be half to a third that of stocks. However, the bond market right now is anything but boring. So far this year, while stocks are back to prices roughly where they were in early 2018, a sharp fall in interest rates has caused bond investors to reap some significant capital gains. Bonds have an inverse relationship with interest rates. The value of most bonds increases when interest rates decline and go down when interest rates rise. ***

*** How significant are the gains in bonds? Since the beginning of 2019, investors in the 30-year Treasury bond have seen gains (interest plus price appreciation) of 26.4%. That would be an outstanding full year’s return for stocks. According to the Bloomberg Barclay’s U.S. Aggregate Bond Index, long-term bonds overall have generated a 23.5% return. Investment grade corporate bonds have returned 14.1%, while the 10-year Treasury note has gained 12.6%. Market observers have predicted for the last decade or so that bond rates have nowhere to go but up. What we’re seeing currently is a yield on the ten-year Treasury note of just under 1.47%. At the end of 2018 it was more than 3%. Will we see more of the same? It’s very hard to imagine that same 10-year Treasury falling another 1.5%—to zero yield. So the smart money says that most of the gains have already been taken, and anybody looking for 20-plus percent returns in long bonds going forward is just chasing them after the fact when returns are dropping. But how smart is smart? Just in case you agree and think interest rates have nowhere to go but up, consider that many countries in Europe actually have negative interest rates, where the investor or depositor pays to loan their money to organizations or banks. Another 1.5% fall to 0% interest rates could deliver similar 20% bond returns. Lessons Learned The lesson here is that even if you think of bonds as the boring part of your portfolio, there are times when they can add a little more kick to your returns than you might have expected. And in times of falling equity markets, they are an invaluable buffer against big losses. Still, with the long term probability that bonds produce a return half that of equities, there is a significant chance that they won’t sustain the 20-plus percent returns as rates stabilize and increase at some point in the future. Unlike the misinformed prospect I visited with, most investors over the age of 40 can benefit by having a substantial slice of their investment portfolio in bonds. Whether their returns are typically boring or occasionally exciting, bonds are an important asset class for diversified investors. Assessment: Your thoughts are appreciated. ***

*** |

Filed under: Investing | Tagged: bonds, Rick Kahler CFP | 1 Comment »

By staff reporters

***

READ HERE

***

***

8

***

Filed under: Investing, LifeStyle | Leave a comment »

Vitaliy Katsenelson, CFA

Student of Life

These pharnacy stocks are good businesses. In general they have solid balance sheets, above-average returns on capital, and they generate a lot of cash, which is used to pay dividends and buy back stock.

But, these defensive features have not mattered much lately, as we are entering the 10th year of uninterrupted economic expansion.

Accordingly, these companies are significantly undervalued. How under valued? Let’s answer that question by examining two stocks in our portfolio in closer detail.

***

Prescription Pill Bottles

***

***

***

Filed under: Drugs and Pharma, Investing | Tagged: By Vitaliy Katsenelson CFA, Drug-Distribution Stocks, Drugs, PBMs, Pharmacy Stocks | 1 Comment »

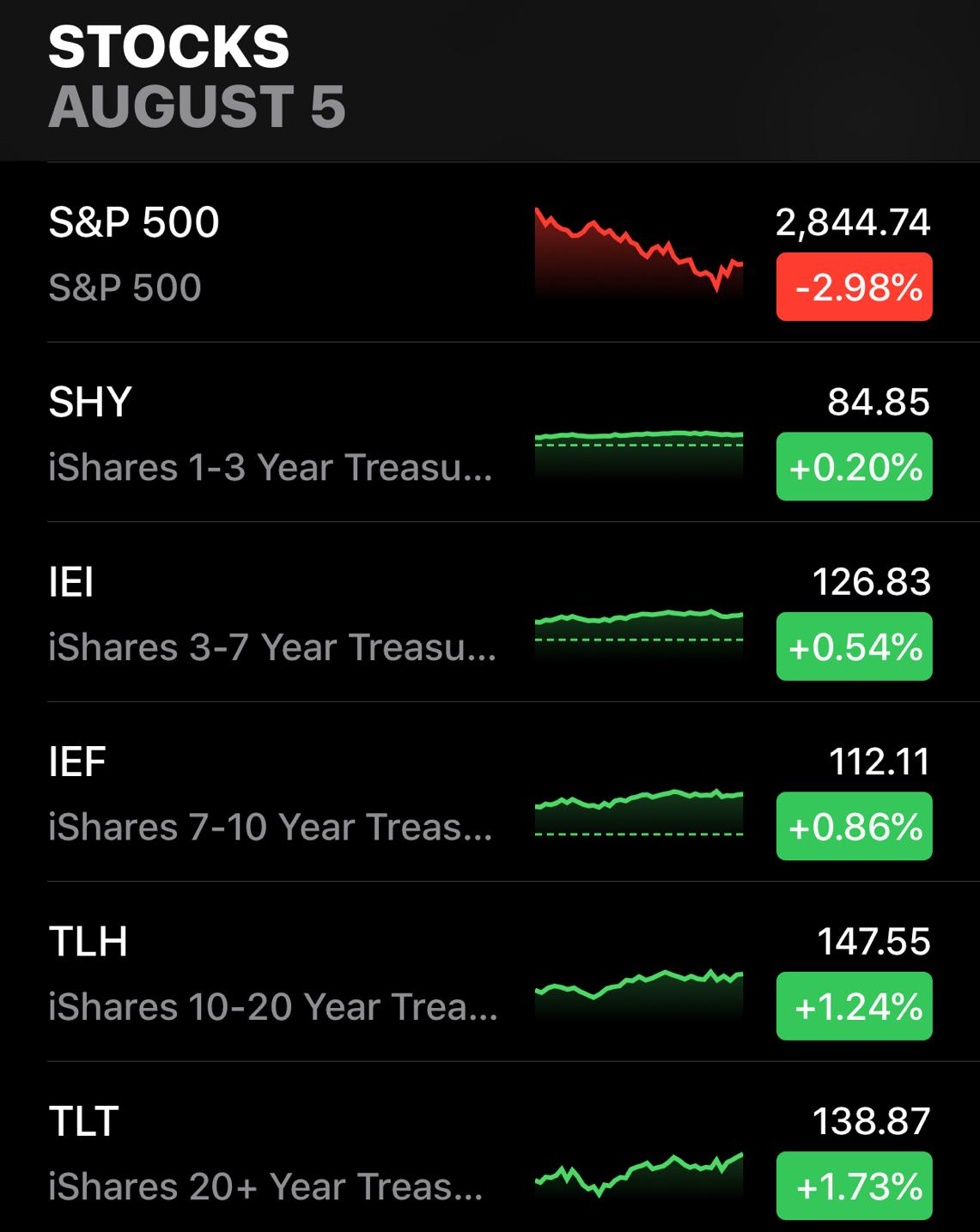

A Round-Up with “Sick” Infographic

***

***

***

8

***

***

Filed under: Investing | Tagged: August 5th 2019 Stocks | Leave a comment »

“Money is supposed to be spent!” “Money is supposed to be saved!”

By Rick Kahler CFP®

We may not hear talk-show participants shouting these opposing views at each other with the same level of anger that characterizes some of our political rhetoric. Yet the core polarization that pervades so much of today’s society also shows up in people’s beliefs about money.

I saw this polarization recently in a conversation with a group of friends in Europe. The topic of money came up, as it usually does when people find out one of my specialties as a financial advisor is financial therapy. The thinking of my friends was that money is meant to be spent, not saved. They felt that people who saved money were faithless and greedy hoarders who by their saving threatened the economic system.

At the other extreme, I know other people who strongly believe a person’s first duty is to save and invest. According to them, those who don’t save as much as possible for emergencies and retirement are foolish, deluded, irresponsible, and destined to live out their last days in poverty.

My friends who embrace the money script that “money is to be spent, not saved” are likely to also hold a money script that “the universe will provide.” They tend to fall into a category we label Money Avoiders. Those who embrace the money scripts that “money is to be saved and not spent,” who also believe “one can never really have enough money,” are in the category of Money Worshipers.

Like most other forms of polarized thinking, neither of these extremes is right. Nor is either belief wrong.

Money does need to be spent. The health of our economic system depends on transactions. It’s important that money flows through the selling and buying of goods and services. When a significant number of consumers stop spending, economic activity grinds to a halt. We saw the effect of this in the financial crises of 2008. It’s also important to spend money to take care of ourselves and our families. Saving or investing money to a point that we go without adequate food, shelter, health care, or similar necessities is not healthy.

***

Money also needs to be saved to provide a cushion against emergencies and to provide for our needs in retirement. My European friends enjoy a higher certainty of adequate income in retirement. For them, this is the universe providing, a strong government security net. However, those that live in many Asian countries are assured very little, if anything, in the way of retirement income. For them, the universe comes up short and depends upon the generosity of family to provide. Saving in an Asian culture is therefore much more important than if you live in a Scandinavian country.

Saving and investing for retirement is important for those of us in the US, as well. Without it, we face two dubious prospects: we can depend on family to provide or we can eke out a meager living on a Social Security payment of around $2,000 a month in retirement.

Those who are not polarized around money understand that both spending and saving are important for financial health. They can balance their spending and saving, applying both when necessary in their own lives.

Assessment

Ideally, from this balanced middle ground, someone can also see past the limitations of others who are polarized. Those who believe “Money is meant to be spent” or “Money is meant to be saved” have a world view that results in such an extreme position. Labeling them as “wrong” is not a useful way to try to shift anyone’s polarized beliefs.

Conclusion: Your thoughts are appreciated.

***

8

***

Filed under: Experts Invited, Investing | Tagged: Prioriting Money Beliefs, Rick Kahler CFP | Leave a comment »

[By Rick Kahler CFP]

“What do you think of the FIRE movement?” a reporter asked me recently. I told her I was ambivalent about it.

The FIRE acronym in this context stands for “Financial Independence, Retire Early.” While a Harris poll done in late 2018 found most people over 45 had never heard of the FIRE movement, it apparently has caught fire among millennials.

The focus of FIRE adherents is lifestyle more than finances. Two books are the foundation of the FIRE movement: Your Money or Your Life, written in 1992 by Vicki Robin and Joe Dominguez, and Early Retirement Extreme, written in 2010 by Jacob Lund Fisker. The concept was popularized in 2011 by blogger Peter Adeney (Mr. Money Mustache), who lives in Longmont, CO. At the age of 30, Adeney and his wife retired with a retirement fund of $600,000 and a paid-for home.

According to the reporter who interviewed me, many advisors have strong opinions against the FIRE movement. This may seem odd. After all, financial independence and retiring early is often a goal of those seeking financial planning. That was certainly one of my goals when I was the age of today’s millennials.

I find very little to criticize about adopting a frugal lifestyle and saving as much as possible. For decades I have suggested living on half of what you make, with a goal of reaching financial freedom as soon as possible. Some FIRE proponents do save up to 50% of their income, which is five times more than their peers, according to a January 21, 2019, InvestmentNews article by Greg Iacurci, “Advisors throw cold water on FIRE Movement.”

What makes many financial planners uncomfortable is the definition of “early.” In my day, early was age 50, not 30. In terms of FIRE, Adeney promotes a lifestyle of aggressive frugality with the goal of retiring as soon as possible, using a 4% withdrawal rate as a guideline to determine the nest egg you need to accumulate.

***

***

This raises two obvious issues that need clarification.

First, you need to earn enough to be able to live on 50 percent of your income. Relatively few young adults make that much. There is no magic income number, since the cost of living varies so much across the country.

One’s definition of frugality is also important. To some that may mean setting the thermostat at 68 all winter or driving a small fuel-efficient vehicle. For others it may mean chopping your own wood to heat your living space only with a wood-burning stove or doing without a car altogether. As with many things, the wisdom is knowing when frugality crosses the line to dangerous deprivation.

Finally, the earlier you retires the longer your retirement nest egg must last. With a 4% withdrawal rate, someone retiring at age 70 has a much higher probability of seeing their investment portfolio last for their lifetime than someone retiring at age 30. Also, the rate of return on the portfolio is critical. The higher the rate of return the longer the funds will last. If there is any potential problem with the FIRE formula it’s probably this.

Since the average 30 year old may live another 60 years, and assuming a 4% return net of mutual fund and advisor fees, I would make a strong argument for a 2 percent withdrawal rate. Someone age 50 could reasonably withdraw 3%, while someone age 60 or above could probably be safe at 4%.

Assessment:

As with any conflagration, playing with FIRE irresponsibly can end up burning down the house. But used wisely, it can sustain life and make living much more rewarding.

8

***

Filed under: Investing, Retirement and Benefits | Tagged: 4% rule, FIRE movement, retirement | Leave a comment »

Vitaliy Katsenelson CFA

***

***

8

***

Filed under: Investing | Tagged: value investing, Vitaliy Katsenelson CFA | 1 Comment »

The “Rules”

[By Rick Kahler CFP®]

In the business of selling financial products, the “good deal exemption” may be one of the most widely used “rules” most people have never heard of. You can’t find it in any rule book or statute. Even Google has never heard of it. Yet it is used on a daily basis.

The rules and laws surrounding the sale of financial products are complex and voluminous. Even with the best of intentions, it isn’t hard to run afoul of a rule.

Under the good deal exemption, however, a licensee can violate any rule or statute as long as the investment sold to the customer turns out to be a “good deal.” This is a tongue-in-cheek way of saying you can violate any rule you want as long as the customer doesn’t file a complaint or sue you. Which they will rarely do if the deal turns out to make them loads of money.

It’s when investments go bad that customers often complain or sue, not because they were aware of any securities violations, but because they lost money. It’s the ensuing investigation by the regulating body and the customer’s attorney that uncovers any violations.

Example:

Recently, I came across a perfect example of the good deal exemption. A married couple I knew, Arnie and Audrey, invested with Bernie (not his real name) 30 years ago as they neared retirement. He put their entire savings of about $310,000 into mutual funds that invested in common stocks. Because of a pension and Social Security, they didn’t need any income from their investments.

At the same time, Arnie put his investments into a revocable living trust, naming Audrey as the trustee and beneficiary. Eleven years later, when Audrey was 80, Arnie died.

Losing her husband’s pension income and one Social Security check, Audrey needed to start drawing $2,000 a month from the portfolio. While most advisors would have recommended reducing the risk and volatility of the portfolio by investing less in stocks and more in bonds, Bernie kept Audrey invested 100% in stocks. This is aggressive for any 80-year-old needing income from a portfolio. He made no changes as the years went by.

At 85, Audrey started showing signs of dementia. Bernie rightly suggested appointing someone other than herself as trustee. But rather than naming one of her three children (who didn’t trust Bernie and may have transferred the accounts), he convinced her to appoint his wife, who also worked in his office, as trustee. In any broker’s books, this was a serious ethics violation.

In the great recession of 2008-2009, when Audrey was 89, her portfolio lost just under half of its value, falling from $832,507 to $478,820. Had Bernie reallocated the portfolio before the crash to a mix of 50% stocks and 50% bonds, the loss would have been cut in half. To his credit, Bernie told her to stay the course and not sell out.

Recently, at age 99, Audrey died. Her account had done phenomenally well, being 100% invested in US stocks, which for the last 10 years was the best investment class on the planet. Her $478,820 had grown to $1,300,000, providing her a $2000 monthly income and a substantial estate that she left to her children.

Assessment

Despite the inappropriately risky investments and the ethics violations, Bernie and his wife are probably protected by the good deal exemption. Given their substantial inheritance, Audrey’s children are unlikely to sue.

This happy ending was due primarily to luck. Audrey lived long enough and at the right time so her portfolio recovered. However, if luck were a sound investment strategy, Las Vegas would be full of millionaires happily retired on their winnings.

Conclusion

Your thoughts are appreciated.

***

8

***

Filed under: Health Law & Policy, Investing | Tagged: "Good Deal Exemption", invve, Rick Kahler CFP, SEC | Leave a comment »

How can this possibly be fair?

By Rick Kahler MS CFP®

An April 29th headline in The New York Times got my attention: “Profitable Giants Like Amazon pay $0 in Corporate Taxes. Some Voters Are Sick of It.” My immediate reaction was outrage. Amazon had a 0% tax rate. My company’s overall tax rate was 24%, and its net profit was less than 0.000025% of Amazon’s. How can this possibly be fair?

The Times article, by Stephanie Saul and Patricia Cohen, gave few specifics but left the impression that Amazon simply gets out of paying taxes on its profits because of a legal, but unfair, manipulation of the tax code afforded only to wealthy corporations, leaving the heavy lifting to the rest of us poor saps.

I wanted to know how Amazon did it, so I did some research

First, let’s put the $11.1 billion profit into perspective. The past 18 months are the first time Amazon has shown any meaningful profit since 2011. Many of those years saw them losing billions of dollars.

The total value (market capitalization) that shareholders have invested in Amazon is $954 billion as of April 29, 2019. That means the 2018 profit of $11.1 billion represents an earnings yield of 1.16% return on investors’ money. The average earnings yield on a large US company is 4.5%, significantly higher than Amazon’s. While $11.1 billion sounds like a lot of money in dollar terms, when viewed in the amount of money it takes to generate those profits, Amazon’s financials are significantly subpar.

Amazon reduced their taxes to zero by primarily doing four things:

The article cited a carpet layer who had a profit of $18,000 and paid more in taxes than Amazon. He was so upset at this injustice that he joined the Socialist Party.

The article failed to mention that many of the same write-offs used by Amazon were available to him, too. If his business was incorporated, the tax bill on his profits was probably 21%, or $3,780. If he had reinvested his profit in a new carpet cleaning machine, had losses from previous years to carry forward, spent money on developing a new type of carpet cleaner, or paid his employees in stock, he would have paid nothing in taxes.

***

***

Assessment

Critics of big corporations might say such strategies would not be realistic for a one-person company. Yet I have seen many small business owners use them, particularly carrying forward losses that result from the essential start-up costs. The corporate tax code generally applies equally to all businesses and is meant to encourage small companies as well as large ones to take the risks necessary to create new jobs.

Conclusion

Your thoughts are appreciated.

***

8

***

Filed under: Experts Invited, Investing, Taxation | Tagged: Amazon, New York Times, Rick Kahler MS CFP® | Leave a comment »

By Vitaliy Katsenelson CFA

***

8

***

Filed under: Interviews, Investing, Videos | Tagged: Investing, Vitaliy Katsenelson CFA, Warren Buffet | Leave a comment »

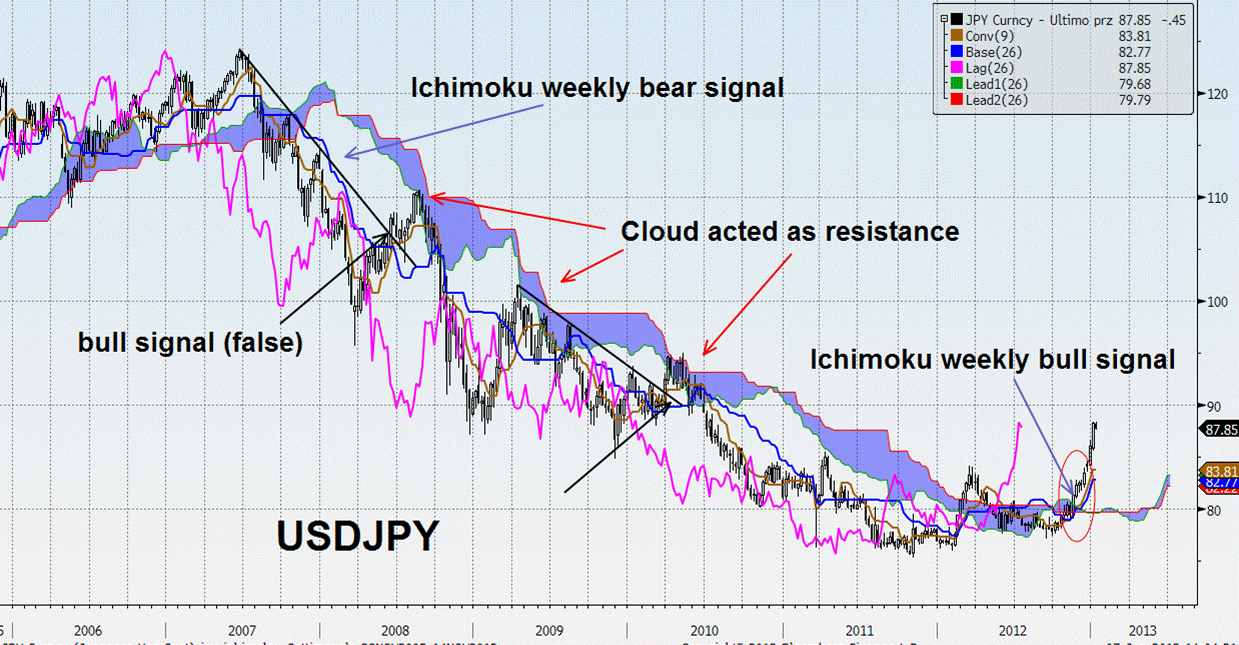

No More “Candle Stick” Technical Stock Charts

[By Staff reporters]

The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on the chart. It also uses these figures to compute a “cloud” which attempts to forecast where the price may find support or resistance in the future.

***

8

[Dr. Cappiello PhD MBA] *** [Foreword Dr. Krieger MD MBA]

Front Matter with Foreword by Jason Dyken MD MBA

***

***

Filed under: Investing | Tagged: Ichimoku Cloud?, Technical analysis | Leave a comment »

|

|

|

|

|

|

Filed under: Investing | Tagged: Investing, stocks, Vitaliy Katsenelson CFA | Leave a comment »

The Beginners Guide

By Forbes Wealth

***

***

***

***

Filed under: Investing | Tagged: Bitcoin, cryptocurrency | 4 Comments »

![]()

SEC Failed to Rein in Investment Banks [April Fool’s Day – 2015]

By Ben Protess, ProPublica – October 1, 2008 5:01 pm EDT

Editor’s Note: This investigative report was first published ten years ago. And so, we ask you to consider – on this April Fool’s Day 2019 – how [if] things have changed since then?

***

***

The Securities and Exchange Commission [SEC] last week abolished the special regulatory program that it applied to Wall Street’s largest investment banks. Known as the “consolidated supervised entities” program, it relaxed the minimum capital requirements for firms that submitted to the commission’s oversight, and thus, in the view of some experts, helped create the current global financial crisis.

But, the SEC’s decision to ax the program currently affects no one, since three of the five firms that voluntarily joined the program previously collapsed and the other two reorganized.

The Decision – 18 Months Ago

The decision came last Friday, one day after the commission’s inspector general released a report [1] (PDF) detailing the program’s failed oversight of Bear Stearns before the firm collapsed in March. The commission’s chairman, Christopher Cox, a longtime opponent of industry regulation, said in a statement [2] that the report “validates and echoes the concerns” he had about the program, which had been voluntary for the five Wall Street titans since 2004.

The report found that the SEC division that oversees trading and markets was “not fulfilling its obligations. “These reports are another indictment of failed leadership,” said Sen. Charles Grassley (R-Iowa) who requested the inspector general’s investigation.

The SEC program, approved by the commission in 2004 under Cox’s predecessor, William Donaldson, allowed investment banks to increase their amount of leveraged debt. But, there was a tradeoff: Banks that participated allowed their broker-dealer operations and holding companies to be subject to SEC oversight. Previous to 2004, the SEC only had authority to oversee the banks’ broker dealers.

Longstanding SEC rules required the broker dealers to limit their debt-to-net-capital ratio and issue an early warning if they began to approach the limit. The limit was about 15-to-1, according to the inspector general report, meaning that for every $15 of debt, the banks were required to have $1 of equity.

But the 2004 “consolidated supervised entities” program revoked these limits. The new program also eliminated the requirement that firms keep a certain amount of capital as a cushion in case an asset defaults.

Bear Sterns

As a result, the oversight program created the conditions that helped cause the collapse of Bear Stearns. Bear had a gross debt ratio of about 33-to-1 prior to its demise, the inspector general found. The inspector general also found that Bear was fully compliant with the programs’ requirements when it collapsed, which raised “serious questions about whether the capital requirement amounts were adequate,” the report said.

The report quoted Lee Pickard, a former SEC official who helped write the original debt-limit requirements in 1975 and now argues the 2004 program is largely to blame for the current Wall Street crisis.

“The SEC gave up the very protections that caused these firms to go under,” Pickard said in an interview with ProPublica. “The SEC in 2004 thought it gained something in oversight, but in turn it gave up too much public protection. You don’t bargain in a way that causes you to give up serious protections.”

Pickard, now a senior partner at a Washington, D.C.-based law firm, estimated that prior to the 2004 program most firms never exceeded an 8-to-1 debt-to-net capital ratio.

The previous program “had an excellent track record in preserving the securities markets’ financial integrity and protecting customer assets,” Pickard wrote [3] in American Banker this August. The new program required “substantial SEC resources for complex oversight, which apparently are not always available.”

Asked if he believes the 2004 program was a direct cause of the current crisis, Pickard told ProPublica, “I’m afraid I do.”

The New York Times reported Saturday that the SEC created the program after “heavy lobbying” for the plan from the investment banks. The banks favored the SEC as their regulator, the Times reported, because that let them avoid regulation of their fast-growing European operations by the European Union, which has been threatening to impose its own rules since 2002.

SEC Spokesman

A SEC spokesman declined to comment for this article, referring inquires to Chairman Cox’s statement. In the statement, Cox admitted the program “was fundamentally flawed from the beginning.” But Cox, a former Republican congressman from California, offered mild support for the program as recently as July when he testified before the House Committee on Financial Services. The program, among other oversight efforts, Cox said, had “gone far to adapt the existing regulatory structure to today’s exigencies.” He added that legislative improvements were necessary as well, and has since told Congress that the program failed.

More Questions

So why did the commission not end the program sooner? Some say that the program’s flaws only recently became apparent. “As late as 2005, the program seemed to make a lot of sense,” said Charles Morris, a former banker who predicted the current financial crisis in his book written last year, The Trillion Dollar Meltdown [4]. The SEC “didn’t know it didn’t work until we had this stress.”

And leverage does not always spell trouble. In a strong economy, leverage can also be attractive because it can increase the profitability of banks through lending.

In his recent statement, Cox said the inspector general’s findings reflect a deeper problem: “the lack of specific legal authority for the SEC or any other agency to act as the regulator of these large investment bank holding companies.”

Secretary of the Treasury Henry Paulson has called for a refining of the regulatory structure to reflect the global and interconnected nature of today’s financial system. In any case, the program’s failure can be seen in the disappearance of the participating banks: Bear Stearns, Lehman Brothers, Merrill Lynch, Morgan Stanley and Goldman Sachs.

***

Assessment

Merrill Lynch’s leverage ratio was possibly as high as 40-to-1 this year and Lehman Brothers faced a ratio of about 30-to-1, according to Bloomberg [5].

The Fed and Treasury Department forced Bear Stearns into a merger with JPMorgan Chase in March. And the last two months, Lehman Brothers went bankrupt and sold their core U.S. business to British bank Barclays PLC, and Merrill Lynch was acquired by Bank of America. Morgan Stanley and Goldman Sachs, the two remaining large independent investment banks, changed their corporate structures to become bank holding companies, which are regulated by the Federal Reserve.

As these banks have folded or reorganized over the last several months, the Federal Reserve has largely assumed the SEC’s oversight responsibilities, though the commission will still have the power to regulate broker dealers.

Original Essay: http://www.propublica.org/article/flawed-sec-program-failed-to-rein-in-investment-banks-101

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Ethics, Investing | Tagged: American Banker, April Fool's Day, Bank of America, Bear Stearns, Ben Protess, Charles Grassley, Charles Morris, Christopher Cox, FDIC, Federal Reserve, Goldman Sachs, Henry Paulson, JPMorgan Chase, Lee Pickard, Lehman Brothers, Merrill Lynch, Morgan Stanley, SEC, Securities and Exchange Commission, Wall Street, William Donaldson | 10 Comments »

Based on Tax Considerations?

By Dr. David Edward Marcinko MBA

LINK: https://medicalexecutivepost.com/schedule-a-consultation/

One personal investing strategy is to place more conservative investments (those with lower expected returns) in a tax-deferred traditional IRA, 401-k, 403-b or similar, and more aggressive (higher-earning) assets in a taxable brokerage account or Roth IRA.

WHY? Each account is thus working hard but in very different ways.

HOW? The conservative funds in the traditional IRA or retirement accounts would fill any needs for safety as they grow more slowly – and the higher tax rate won’t take out as big of a bite.

Meanwhile, the more aggressive funds in a taxable brokerage accounts would grow more quickly, but be taxed at a lower rate.

Assessment: Any thoughts?

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

MORE FOR DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

***

Filed under: Investing, Retirement and Benefits, Taxation | Tagged: david marcinko, IRA, retirement planning, Roth IRA | Leave a comment »

Random Drivel?

[By Vitaly Katsenelson CFA]

What I am about to share with you is somewhat random drivel about a topic that has been very important to me in 2018 – time.

I am anything but an expert on it; and in fact, as you’ll see, this is something I fail in and am trying to fail less.

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

Filed under: Experts Invited, Information Technology, Investing | Tagged: Resetting Defaults for 2019, Vitaliy Katsenelson CFA | Leave a comment »

THE VANGUARD GROUP FOUNDER

[By Dr. David Edward Marcinko MBA]

John Bogle, who founded Vanguard and revolutionized retirement savings, dies at age 89.

***

http://www.philly.com/business/john-bogle-dead-vanguard-obituary-20190116.html

***

The Vanguard Group is an American registered investment advisor based in Malvern, Pennsylvania with over $5.1 trillion in assets under management. It is the largest provider of mutual funds and the second-largest provider of exchange-traded funds in the world after BlackRock’s iShares.

In addition to mutual funds and ETFs, Vanguard offers brokerage services, variable and fixed annuities, educational account services, financial planning, asset management, and trust services.

Assessment

I attended medical school in Philadelphia back in the day, which was not far from Malvern; PA. My girl friend at the time was at the Wharton School. So, we were thrilled to have the occasion to actually visit and tour Vanguard Headquarters. We were not able to meet Mr. Bogle but I am very grateful to him.

***

8

***

Filed under: Investing | Tagged: John C. Bogle, Vanguard | 4 Comments »

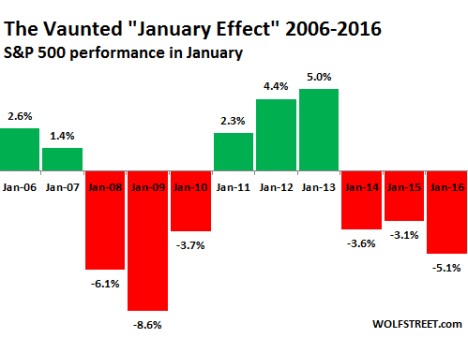

[By Dr. David E. Marcinko MBA]

The January effect is a hypothesis that there is a seasonal anomaly in the financial market where securities’ prices increase in the month of January more than in any other month.

***

***

This calendar effect would create an opportunity for investors to buy stocks for lower prices before January and sell them after their value increases.

“Santa Clause Effect” or “Rally: https://medicalexecutivepost.com/2018/12/24/will-there-be-a-santa-clause-rally-this-year/

NOTE: Also known as the “Turn-of-the-Year Effect” and “Calendar Effect.”

Assessment

Your thoughts are appreciated.

RESOURCES:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

THANK YOU

8

Filed under: iMBA, Inc., Investing | Tagged: Calendar Effect, January Effect, Turn-of-the-Year Effect | 2 Comments »

For Physician-Investors to Know

[By staff reporters]

***

***

***

***

Your thoughts are appreciated.

RESOURCES:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

THANK YOU

8

Filed under: Health Economics, Investing | Tagged: Economists of Note, fama, french, Harry Markowitz, Novy-Marx, Sharpe | Leave a comment »

***

***

Book Dr. David Edward Marcinko CMP®, MBA, MBBS for your Next Medical, Pharma or Financial Services Seminar or Personal and Corporate Coaching Sessions

Dr. Dave Marcinko enjoys personal coaching and public speaking and gives as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These have included lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

Topics Link: toc_ho

***

***

![]()

[Foreword Dr. Phillips MD JD MBA LLM] *** [Foreword Dr. Nash MD MBA FACP]

***

Filed under: Financial Planning, Health Economics, iMBA, Investing, Managed Care, Portfolio Management, Practice Management, Practice Worth, Risk Management, Touring with Marcinko | Tagged: David E. Marcinko, Financial Planning, Investing, medical practice management, Portfolio Management | Leave a comment »

What it is – How it works

[By staff reporters]

A fat-finger error is a keyboard input error or mouse misclick in the financial markets such as the stock market or foreign exchange market whereby an order to buy or sell is placed of far greater size than intended, for the wrong stock or contract, at the wrong price, or with any number of other input errors.

Automated systems within trading houses may catch fat-finger errors before they reach the market or such orders may be cancelled before they can be fulfilled. The larger the order, the more likely it is to be cancelled, as it may be an order larger than the amount of stock available in the market.

Fat-finger errors are a product of the electronic processing of orders which requires details to be input using keyboards. Before trading was computerised, erroneous orders were known as “out-trades” which could be cancelled before proceeding. Erroneous orders placed using computers may be harder or impossible to cancel.

***

***

MORE: https://en.wikipedia.org/wiki/Fat-finger_error

RELATED: https://medicalexecutivepost.com/2017/06/06/peering-at-a-high-frequency-stock-trading-algorithm/

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

Filed under: Investing | Tagged: Fat Finger | Leave a comment »

By Vitaliy Katsenelson CFA

Dear ME-P Readers,

You might want to listen to some great interviews by Roben on investment topics (his shows cover a wide variety of themes).

I am just scratching the surface here. You can listen to hundreds of other shows with Roben here, or look for Full Disclosure with Roben Farzad on your podcast app – just be careful, they are very addicting.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

Filed under: Interviews, Investing, Videos | Tagged: investing podcasts, Vitaliy Katsenelson CFA | Leave a comment »

By Vitaliy Katsenelson CFA

***

I was interviewed by my friend Dan Ferris on the Stansberry Investor Hour show. My segment of the interview starts at the 22:22 mark (click here to listen).

If you’d like to dig deeper into some of the concepts I discussed, you can read the following articles:

1 – What quality means to us.

2 – Why we sold of ETFs and bought Treasuries

3 – How and why we are hedging our portfolios with options

4 – Why Amazon will not run McKesson out of business and why we like the stock and here is one more.

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***8

Filed under: Experts Invited, Investing, Videos | Tagged: Stansberry Investor Hour Interview, Vitaliy Katsenelson CFA | Leave a comment »

|

Filed under: Experts Invited, Investing | Tagged: Vitaliy Katsenelson CFA | 1 Comment »

By Vitaliy Katsenelson CFA

***

Today I am going to share with you an article I wrote after the January 2018 stock market volatility index run-up. It’s as relevant today as it was then.

***

https://contrarianedge.com/how-a-volatile-stock-market-turns-investors-into-gamblers/

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

Filed under: Experts Invited, Investing, Videos | Tagged: A Stock Market Top?, Optimal Living Daily, Vitaliy Katsenelson CFA | 1 Comment »

By Vitaliy Katsenelson CFA

***

|

Filed under: Experts Invited, Investing | Tagged: Vitaliy Katsenelson CFA | Leave a comment »

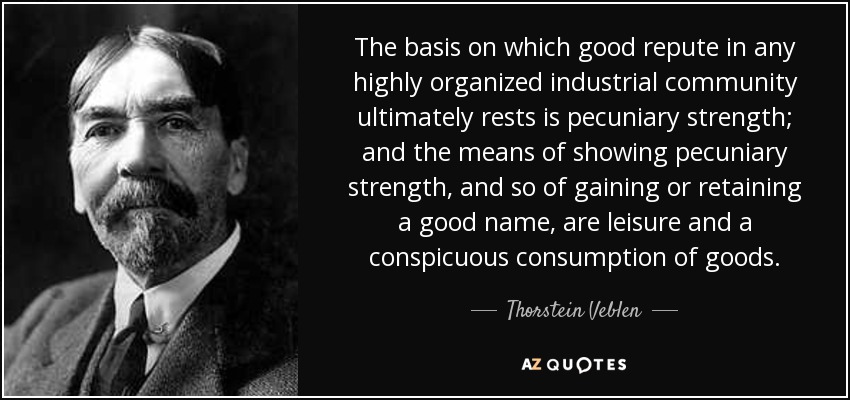

Conspicuous Consumption by Definition

[By Dr. David Marcinko MBA and staff reporters]

Conspicuous consumption is a term introduced by the Norwegian-American economist and sociologist Thorstein Veblen in his book “The Theory of the Leisure Class” published in 1899.

***

***

The term refers to consumers who buy expensive items to display wealth and income rather than to cover the real needs of the consumer. www.HealthDictionarySeries.org

A flashy consumer uses such behavior to maintain or gain higher social status. Most classes have a flashy consumer affect and influence over other classes, seeking to emulate the behavior.

***

The result, according to Veblen, is a society characterized by wasted time and money.

***

***

Assessment

Are doctors today, or yesterday, practitioners of this theory?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

MORE FOR DOCTORS AND NURES:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

8

***

Filed under: Ethics, Investing | Tagged: Conspicuous Consumption, Thorstein Veblen | 2 Comments »

| To my valued connections,

By Alan Yong I have serious concerns about the current state of ICO’s and their future potential could be in jeopardy, if the current trend continues. Please take a moment to read the following articles before investing in, participating with, giving legal advice on, or launching your own ICO. Personally, I believe that ICOs are the best tools for capital formation if properly regulated.

Investopedia report finds 80% of all ICO’s to be scams – 92% never reach exchange Alan Yong Provides Long Term Viability Solution for ICO’s ***

|

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

MORE FOR DOCTORS AND NURES:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

Filed under: Investing | Tagged: Alan Yong, Bitcoin, crypto-currency, ICO's | Leave a comment »

Investors Have Misdiagnosed Amazon’s Push Into The Pharmacy Business |

By Vitaliy Katsenelson CFA

|

*** Companies everywhere, in every business, are paranoid about Amazon.com. This sort of paranoia is healthy for the long-term well-being of our investment portfolio, as it is creating interesting buying opportunities. A case in point: My firm spent a lot of time thinking about pharmacies when we were analyzing investments in McKesson and other drug distributors. We struggled with a question: How will the retail pharmaceutical industry look in the future? Or more precisely, how will Amazon’s entrance into the retail pharmacy business change this industry? Our inability to answer this question kept us away from retail pharmacies. Then we had a small but important insight that shifted our thinking on Walgreens Boots Alliance. The preponderance of drugs in the U.S. is consumed by an older population, whose habits change slowly or not at all. Accordingly, it’s likely that Amazon’s online pharmacy will not significantly impact the existing drug industry. Here’s why: Americans currently spend $450 billion a year on drugs. Walmart is the fourth-largest pharmacy in the U.S., with sales of $21 billion, or 4.6% of the company’s total sales. Let’s say that over the next five years Amazon gets to Walmart’s sales level of $21 billion. If the U.S. pharmaceutical industry grows 2% a year over that time, total drug sales will have increased by $45 billion, or the equivalent of two Walmarts (we are ignoring compounding here), to $495 billion. Walgreens, with its pharmacy selling about $70 billion a year, would barely notice Amazon’s presence. I’ve made this point before, but it is important to repeat: 10 years ago Amazon was not taken too seriously. Giants like Google, now Alphabet, and Microsoft ignored Amazon’s entry into cloud hosting, thinking “What does a bookseller know about the cloud?” They have regretted it ever since. Nowadays everyone is taking Amazon too seriously, bestowing CEO Jeff Bezos with walk-on-water-like superpowers. Boardrooms today are filled to overflowing with chatter about Amazon. There‘s admittedly a lot Corporate America can learn from Bezos (for instance, about ignoring short-term results), but Bezos is not superhuman and Amazon cannot bend the laws of economic gravity. Walgreens’ U.S. business, which is about 75% of its total sales, is impressive. A single stand-alone store produces revenues of about $10 million a year — $7 million in the pharmacy and $3 million in front-end sales (milk, candy bars, T-shirts, etc.) A single store fills about 121,000 scripts a year (up from 97,000 four years ago). Walgreens has one of the highest sales-per-square-foot numbers in the retail industry, at around $1,000 per-square-foot (compared to Walmart’s $450, Kroger’s $550, and Target’s $300). (Note that Tesco’s U.K. stores have sales per square foot of $1,100 — this is why we like the U.K. grocery business more than ones in the US). Walgreens also has an underutilized asset: the front end of the store. Think about it: The pharmacy takes up 20% of the floor space but generates 70% of revenue. In other words 80% of the store (the front end) brings in only 30% of revenue. Walgreens is experimenting with different ways to optimize this underutilized asset — it’s opening medical clinics and bringing LabCorp into its stores, for instance. In 2018 Walgreens bought 1,900 stores from Rite Aid, bringing its total U.S. store count up to around 10,000. Store-count growth days are behind Walgreens, but the scripts-per-store-growth will continue, since baby boomers are not getting any younger. Accordingly, total sales growth will continue at a level of at least 2%-3% a year. When retailers mature and cannot open new stores, their free cash flows explode. Which begs the question, what will Walgreens do with its cash? Already Walgreens is taking a quite different approach than its largest counterpart, CVS Health Corp. CVS owns one of the largest pharmacy benefit management (PBM) companies (a business that has a lot of political risk, as it’s ridden with conflicts of interest), and CVS is doubling down on complexity and buying Aetna , a health insurance company. CVS is trying to become an integrated healthcare provider. We don’t know if CVS will be successful in this endeavor, but the historical odds of success with acquisitions of this complexity clearly do not favor CVS. Walgreens is run by Stefano Pessina, who owns 13% of the company; and thus 13 cents of every dollar spent is his. Walgreens has therefore been deleveraging its business, buying back stock, and paying a dividend. Walgreens is expected to earn $6 a share in 2018. My estimate is that earnings, helped by the Rite Aid acquisition, same-store sales growth, and share buybacks (WBA repurchased 8% of its shares in 2018 and has an authorization to buy another 13%), will exceed $8 per share in 2021. ***

*** Assessment If Walgreens shares trade at 13 times its $8 earnings per share in three years, then the upside from here is about 70%; if it trades at 15 times then it’s a double (Walmart trades currently at 18 times estimated 2018 earnings, while Target is at 15 times). We bought Walgreens at a little over 10 times estimated 2018 earnings in July 2018. Walgreens is a better business than Target and at least as good a business as Walmart. At this valuation, heads we win, tails we win — the only question is by how much. |

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

MORE FOR DOCTORS AND NURES:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

Filed under: Drugs and Pharma, Investing | Tagged: Amazon’s Push Into The Pharmacy Business, Vitaliy Katsenelson CFA | 1 Comment »

Top Ten Money Truisms

By Rick Kahler CFP®

Jonathan Clements is a longtime former columnist for the Wall Street Journal, editor of the HumbleDollar blog, and author whose latest book, From Here to Financial Happiness, comes out in September. I’ve long been a fan of his, and I appreciate his list of 41 Twitter-length truisms that pack a lot of wisdom into a few words.

Here are what I think are the top ten:

1. “We get just one shot at making the journey from birth to retirement. Flirting with financial disaster is not advisable.” I would add that flirting with financial disaster can come as much from being afraid to take action as from taking the wrong action.

2. “We are voracious acquirers of financial information, but mostly to buttress opinions we already hold.” I find very few people have open minds about money. Most hold on tightly to their money scripts because they are too frightened to entertain the notion that they don’t know.

3. “Picking superior investments is a crowded trade. Saving more is an easy win.” One of the least dramatic but most important components to creating wealth is frugality, whether it takes the form of choosing lower-fee investments or living below one’s means.

4. “What’s the difference between an equity-indexed annuity and an index fund? One needs an army of salespeople. The other sells itself.” I have never, ever had a client who purchased an annuity of any kind on their own accord. I have had scores who purchased index funds. Avoiding “investments” being aggressively pushed by salespeople can save you thousands and potentially make you millions.

5. “Cash value life insurance isn’t an investment, it’s a religion—and you’ll never meet a more prickly group of disciples.” I absolutely agree, and the proof is in the nasty comments that fill my email inbox every time I write about this topic.

6. “Draw up a list of your greatest pleasures in life. Then ask yourself: Do you need great wealth to enjoy any of them?” Of course you don’t need great wealth to spend time with those you love, drink in a gorgeous sunset, or do something nice for someone else. You do, however, need some financial well-being to make meaningful pleasures happen.

7. “When you’re ill, you realize how great it is to feel healthy. Money’s similar: When you’re broke, you realize how great it is to be solvent.” The flip side of this truism is the gratitude many of my clients feel for having financial security.

8. “A boat is not your financial friend, but a friend with a boat is.” Buying toys, tools, or other big-ticket items you rarely use and can barely afford is a common money mistake.

9. “Trying to beat the market is a game for the rich. Only they can afford the inevitable disappointing results.” Timing markets doesn’t work whether you are poor or rich; even the rich can only afford to be wrong for a while.

10. “The big financial risk isn’t dying early in retirement but, rather, living longer than we ever imagined.” Most people significantly underestimate how long they will live. That is why 48% start Social Security benefits at age 62 and another 48% start them at age 66. Only 4% wait until age 70, despite statistics showing the odds are this choice will net more lifetime income.

Assessment

I know that’s ten, but one more seems appropriate to end with: “Our only earthly immortality will be the recollection of others. Make sure those memories are good.” One of the ways we can be remembered fondly is through giving back to our communities with both our money and our time.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

***

Filed under: Investing | Tagged: Rick Kahler CFP®, Top Ten Money Truisms | Leave a comment »

By Vitaliy Katsenelson, CFA

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

Filed under: Experts Invited, Investing | 1 Comment »

Questions I’d be Asking If I Owned Tesla Stock

By Vitaliy Katsenelson CFA

What happened to 345,000 reservations?

When Tesla’s Model 3 was released, it was supposed to be a $35,000 car. Four hundred thousand people, including yours truly, put down a $1,000 deposit to reserve their spots in line so they could get their hands on that marvel as soon as it became available. It was a brilliant move by Tesla, as it provided the company $400 million of interest-free financing — the biggest crowdfunding project ever.

Today, after some delays, the Model 3 is being produced. However, $35,000 seems to have been a fiction of CEO Elon Musk’s imagination. Though the car is getting great reviews from auto critics, the price for a bare-bones Model 3 starts at $49,000, and the tax incentives are fading away.

But something interesting happened recently. I received an email from Tesla that said: Model 3 is available to order, and no reservation is required in the U.S. We’re now offering all our best options — including our Long Range and Performance configurations with dual motor all-wheel drive. You can design and order yours today for delivery in approximately 2–4 months.

On the surface this sounds like great news, except that it begs a question: What happened to 345,000 orders? Let me explain. According to Bloomberg, which has been tracking Tesla’s production, to date (as of July 28, 2018) Tesla has produced 55,000 Model 3 cars. Since a $1,000 deposit was supposed to secure buyers a place in line, any car ordered today will only be delivered after orders that were placed years ago are fulfilled — after all, 400,000 people paid Tesla $1,000 to hold their places.

Thus there are only three possible explanations for the email I received. One is that Model 3 production is expected to accelerate at an exponential rate to 40,000 cars a week, starting now. However, Bloomberg estimates that Tesla’s normal production cadence of the Model 3 is closer to 2,825 cars a week, so this is a highly unlikely scenario.

Or two, maybe Tesla has been extremely liberal with its statement of a two-to-four month delivery schedule because it still has 345,000 cars to produce before it can start fulfilling new orders, and the company is using that email to raise additional funds from new customers making deposits. (The required deposit is now $2,500.)

There is a third explanation: The bulk of the original 400,000 orders were for a $35,000 car. When it came time to actually buy the car, consumers may have realized that the out-of-pocket expense was much more than expected and simply canceled their orders, draining Tesla’s balance sheet of $345 million.

How sound is Tesla’s balance sheet?

What Musk has achieved with Tesla and SpaceX is truly astounding. I have incredible respect for him, but he is also a magician playing a confidence game. If Musk can continue to convince the market that Tesla has a bright future, then the market will continue to finance Tesla’s losses, and maybe Musk will figure out how to produce the Model 3 more cheaply and then Tesla will sell hundreds of thousands of Model 3s and the future will be as bright as Musk paints it.

For that to happen, Tesla needs to maintain its high stock price, and investors have to believe that Musk is the Iron Man. Investors have to suspend belief, ignore current problems, and focus on the future. However, if the market loses confidence in Tesla and Musk, Tesla is done. This company is losing billions of dollars a year; it has an over-levered balance sheet. This is where Musk’s confidence game comes in.

If you believe in magic stop reading right now. Okay, you’ve been warned.

There is no magic. Magic is just the art of misdirection. The magician gets you to focus on the shiny object he holds in his left hand and you don’t see what he is doing with his right hand.

Musk has been showing us a lot of shiny objects. Some are real, like the success of SpaceX; some are superfluous, like sending a Tesla Roadster into space, and some are future promises on which Musk may or may not be able to deliver, like his futuristic underground railroad for cars (the hyperloop) and the Tesla truck, which is unlikely to be produced on time and at the promised price. The list is long in this category and never-ending; Musk’s futuristic thinking knows no bounds.

But importantly, these promises are the shiny objects that keep Tesla’s stock price high.

If I was a Tesla investor I’d be seriously worried about the company’s balance sheet. There are some ominous signs that Tesla’s financial situation is deteriorating rapidly. Tesla reportedly recently sent an email to its suppliers asking them to give some money back to help the company with its profitability.

Such requests are made by companies looking for Hail Mary solutions to significant financial problems. If suppliers start questioning Tesla’s financial viability, they’ll start shortening their accounts receivables periods and start requesting letters of credit. This would escalate the company’s problems. Hail Marys are acts of desperation. Putting this in the context of the likely Model 3 cancellations, — Tesla’s cash burn has likely gotten a lot worse.

How effective is Musk at running Tesla?

Tesla is Elon Musk. He has achieved more than many of us will achieve in a thousand lifetimes. But today Musk is running half a dozen companies (Tesla, SpaceX, Solar City, Boring, OpenAI, Hyperloop). To make matters worse, he is also an incredible micromanager. I read that he interviews (or at least used to) every new employee who joins Tesla and SpaceX.

It is clear that Musk is quite exhausted, and his behavior is becoming more erratic. In a conference call snafu in April, he called the British diver who saved the Thai cave kids a “pedo” on Twitter. This sort of thing undermines Musk’s Iron Man image — if he loses that, the confidence game is lost and Tesla is done.

Another red flag went up recently: Musk started to attack short sellers. A short seller who went under the name of Montana Sceptic posted negative research on Tesla on Twitter and SeekingAlpha. Elon Musk personally called the man’s employer and threatened a lawsuit if the employer didn’t silence Montana Sceptic. Historically, companies that have gone after short sellers have had something to hide or were playing a confidence game. (The short sellers were interfering with the misdirection to shiny objects.)

Assessment

Tesla investors are still fascinated by the shiny objects, but I note that CDS insurance on Tesla’s bonds prices in a 24% risk of default by 2025. I am not long or short the stock. But if I were long Tesla’s shares I’d be asking myself these questions. After all, you’re paying $50 billion for a company that trades completely on the spoils of future dreams.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

Filed under: Experts Invited, Investing | Tagged: Tesla, Vitaliy Katsenelson CFA | 15 Comments »

Avoid These 2 Mistakes

By Rick Kahler CFP®

Investing through an IRA is a foundational method of retirement saving. Opening and contributing to an individual retirement account is not hard. That doesn’t mean IRAs are simple and easy to understand.

National Association of Personal Financial Advisors

I was reminded of this at the 2018 spring conference of the National Association of Personal Financial Advisors, where I attended a workshop by Jeff Levine of Fully Vested Advice, Inc., on “10 Critical IRA Mistakes.”

Top on his list of mistakes was failing to make charitable contributions out of your IRA when you are over 70½. These are called Qualified Charitable Distributions (QCDs). Here is why giving to charity directly from your IRA is a good idea.