By A.I. and Staff Reporters

SPONSOR: http://www.CertifiedMedicalPlanner.org

***

***

According to Medical Economics, there were 10 clinic and physician practices filing bankruptcy in 2024, making it the highest level of the last six years, according to a new analysis of cases with liabilities of at least $10 million.

Meanwhile, the Steward Health Care System bankruptcy, which was based in Massachusetts but making headlines across the nation, has become “the largest hospital sector bankruptcy by far in the last 30 years,” according to a new analysis by Gibbins Advisors, based in Nashville, Tennessee.

Health care bankruptcy filings totaled 57 last year, down from 79 in 2023, said “Healthcare Restructuring: Trends and Outlook.” The report analyzed Chapter 11 health care bankruptcy cases with liabilities of at least $10 million, since 2019.

Last year’s total was down 28% from 2023’s peak, but greater than the 2019 to 2022 average of 42 filings a year, the report said.

BROKE DOCTORS: https://medicalexecutivepost.com/2025/08/02/doctors-going-broke-and-living-paycheck-to-paycheck/

***

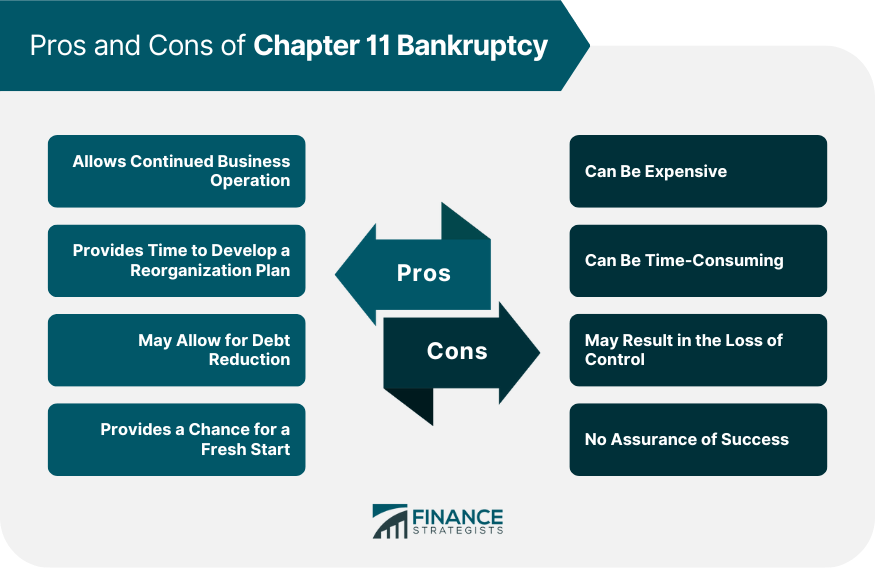

Bankruptcy, often considered a last financial resort, is a legal process that can help alleviate outstanding debts for individuals and businesses. Reasons to file for bankruptcy can include divorce, job loss, exorbitant medical bills or credit card debt.

There are several types of bankruptcy — six, as a matter of fact. The two most common types of bankruptcy for individuals are Chapter 7 and Chapter 13.

But there are four other types as well: Chapter 9, Chapter 11, Chapter 12 and Chapter 15. And, the type of bankruptcy filed depends on the situation.

Regardless of which type, the process is typically the same: You’ll usually retain an attorney and make your case before a judge, who will then erase some debts or set up a repayment plan.

Also note that an eligibility requirement — for all bankruptcy chapters — is that you must undergo credit counseling within the 180 days before filing.

DOCTORS: https://medicalexecutivepost.com/2025/07/17/doctors-and-lawyers-often-arent-millionaires/

COMMENTS APPRECIATED

Like, Subscribe and Refer

***

***

Share this:

Filed under: "Ask-an-Advisor", "Doctors Only", Career Development, CMP Program, economics, Experts Invited, finance, Glossary Terms, Health Economics, Health Insurance, Health Law & Policy, Healthcare Finance, Insurance Matters | Tagged: assets, bankruptcy, california, Chapter 11, Chapter 7, CMP, credit counseling, DMD, DPM, Gibbins Advisors, liabilities, MD, Media, medical, Medical Exonomics, Physician bankruptcy, software, Steward Health Care | Leave a comment »