Posted on May 13, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

How Will COVID-19 Change Healthcare Delivery?

By Health Capital Consultants, LLC

Spurred by how unprepared the American healthcare system was for a pandemic, the current COVID-19 emergency may present the conditions necessary to commence a healthcare delivery model paradigm shift.

In response to the public health emergency, the federal government, which has a record of reducing regulatory “burdens” under the Trump Administration, has taken aggressive actions to create regulatory flexibilities for healthcare providers and suppliers.

At least some of the various actions taken to reduce provider burden as they treat COVID-19 patients are likely to stay intact following the end of this pandemic, potentially revising the fundamental tenets of U.S. healthcare delivery. (Read more…)

***

***

Assessment: Your thoughts are appreciated.

***

***

Filed under: Experts Invited, Health Economics, Health Insurance, Healthcare Finance | Tagged: Health Capital Consultants, How Will COVID-19 Change Healthcare Delivery?, LLC | Leave a comment »

Posted on May 9, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on May 8, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on May 7, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on May 6, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on May 4, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

The Law of Un-Intended [Pandemic] Health Consequences

Courtesy: http://www.CertifiedMedicalPlanner.org

By Dr. David E. Marcinko MBA

By Dr. David E. Marcinko MBA

The Cobra Effect attempts to solve a problem that makes that problem worse.

The effect comes from an Indian story about a city infested with snakes offering a bounty for every dead cobra, which caused entrepreneurs to start breeding cobras for slaughter.

***

***

***

PODCAST: https://www.bing.com/videos/search?q=cobra+effect&&view=detail&mid=591D3F7C353025BE2EEE591D3F7C353025BE2EEE&&FORM=VRDGAR&ru=%2Fvideos%2Fsearch%3Fq%3Dcobra%2Beffect%26FORM%3DHDRSC3

QUERY: Now; what about the PPP, the CARES Act, PPE and related Corona Pandemic consequences; etc?

Assessment: Your thoughts and comments are appreciated.

***

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS:

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Health Economics | Tagged: cobra effect, corona virus | Leave a comment »

Posted on May 3, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

January – March 2020

[By staff reporters]

***

***

Assessment: Your thoughts are appreciated.

***

***

Filed under: Glossary Terms, Health Insurance, LifeStyle | Tagged: cause of death, Global Deaths, Leading Cause Death | Leave a comment »

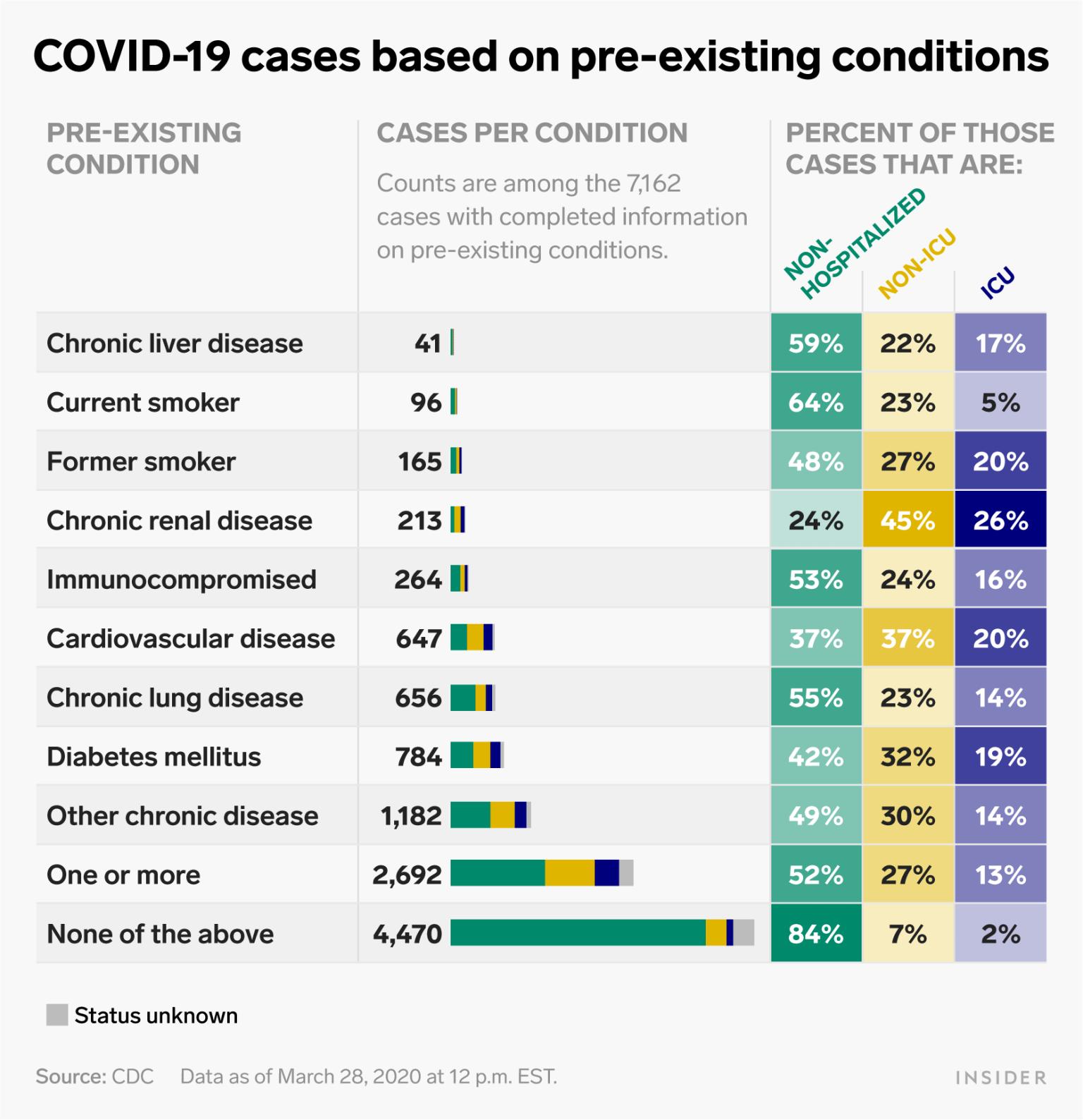

Posted on April 30, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

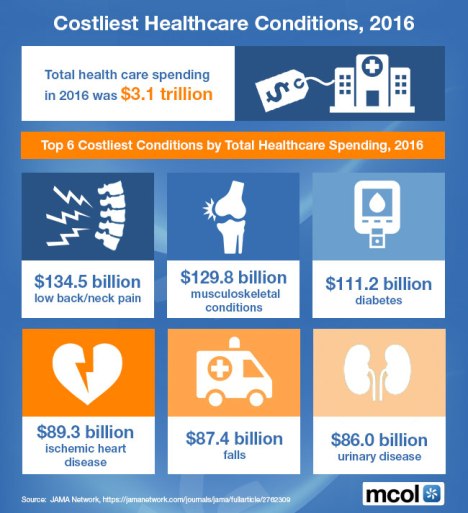

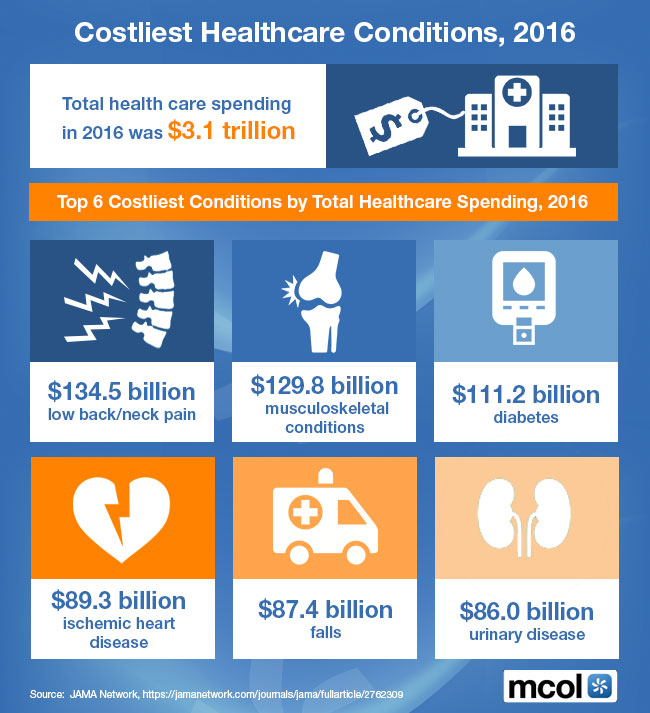

CIRCA: 2016

[By staff reporters]

http://www.MCOL.com

***

***

RECALL: These conditions represent co-morbidities for the Corona Virus pandemic; as well.

Assessment: Your thoughts are appreciated.

FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXOs:

***

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

***

***

Filed under: Health Economics, Health Insurance, Healthcare Finance | Tagged: Costliest Healthcare Conditions, www.MCOL.com | Leave a comment »

Posted on April 28, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Moral Suasion, Investing and the Corona Pandemic

Courtesy: http://www.CertifiedMedicalPlanner.org

By Dr. David E. Marcinko MBA

People will believe anything if enough people tell them it’s true.

This thought comes from a Chinese proverb that if one person tells you there’s a tiger roaming around your neighborhood, you can assume they’re lying.

LINK: https://www.springerpub.com/dictionary-of-health-economics-and-finance-9780826102546.html

If two people tell you, you begin to wonder. If three say it’s true, you’re convinced there’s a tiger in your neighborhood and you panic.

MORE: https://www.omsj.org/science/three-men-make-a-tiger

INVESTING: https://www.caseyresearch.com/daily-dispatch/three-men-make-a-tiger/

MONEY PSYCHOLOGY: https://medicalexecutivepost.com/2018/09/19/money-beliefs-and-luxury-lifestyle-tv/

INVESTING: https://medicalexecutivepost.com/2013/04/24/more-on-money-psychology/

Assessment: Your thoughts and comments related to the Corona Virus Pandemic, Money and Investing psychology are appreciated.

***

***

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

***

THANK YOU

***

Filed under: Glossary Terms, Investing, Research & Development | Tagged: corona, financial psychology, money psychology, Three men make a tiger | Leave a comment »

Posted on April 26, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Performance Increases with Anxiety and Excitement to a Point

By Dr. David E. Marcinko MBA

Courtesy: www.CertifiedMedicalPlanner.org

The Yerkes–Dodson law is an empirical relationship between arousal and performance, originally developed by psychologists Robert M. Yerkes and John Dillingham Dodson in 1908.

LINK: https://www.springerpub.com/dictionary-of-health-economics-and-finance-9780826102546.html

The law dictates that performance increases with physiological or mental arousal, but only up to a point. When levels of arousal become too high, performance decreases. The process is often illustrated graphically as a bell-shaped curve which increases and then decreases with higher levels of arousal.

LINK: https://juniperpublishers.com/gjidd/pdf/GJIDD.MS.ID.555606.pdf

MONEY: https://medicalexecutivepost.com/2018/09/19/money-beliefs-and-luxury-lifestyle-tv/

INVESTING: https://medicalexecutivepost.com/2013/04/24/more-on-money-psychology/

***

***

PODCAST: https://www.bing.com/videos/search?q=YERKES-DODSON+LAW&&view=detail&mid=6ACB86065FA362A3AC1D6ACB86065FA362A3AC1D&&FORM=VRDGAR&ru=%2Fvideos%2Fsearch%3Fq%3DYERKES-DODSON%2BLAW%26FORM%3DHDRSC3

***

***

Assessment: Your thoughts and comments related to the Corona Virus Pandemic, Investing and Money Psychology are appreciated.

***

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Glossary Terms, Investing, Research & Development | Tagged: Investing, money psychology, Yerkes-Dodson Law | 1 Comment »

Posted on April 25, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Does the Internet Promote the Same Dynamic as “Road Rage?”

Courtesy: https://lnkd.in/eBf-4vY

The best way to get an answer on the Internet is not to ask a question. It’s to post the wrong answer.

This “law” by Ward Cunningham is known to those with social media accounts. Once you’re arguing with a computer – social norms vanish! People like to fight online more than they like to help.

They’re quicker to point out flaws than to become a friendly resource.

In fact, psychologist Jonathan Haidt wrote that if you constantly express anger in your private conversations, your friends will likely find you tiresome. But, when there’s an audience, the payoffs are different and outrage can boost your status.

A study by William J. Brady at NYU measured half a million tweets and found that each moral or emotional word used in a tweet increased its virality by 20 percent.

***

***

Finally, another 2017 study, by the Pew Research Center, showed that posts exhibiting “indignant disagreement” received nearly twice as much engagement [likes and shares] as other types of content.

MORE: https://lnkd.in/emU7F5c

Assessment: Your thoughts are appreciated

TEXTS FOR PHYSICIAN-EXECUTIVES & MEDICAL CXOs:

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

Thank You

***

Filed under: Experts Invited, Glossary Terms | Tagged: WARD CUNNINGHAM'S LAW OF INTERNET INQUIRIES!, William J. Brady | 1 Comment »

Posted on April 25, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

My Fond Memories

By Dr. David E. Marcinko MBA

National Osteopathic Medicine Week takes place April 19-25, 2020. It is a special time where the osteopathic medicine profession comes together to help educate the world about what osteopathic medicine is.

At first glance, the difference between DOs and MDs is difficult to distinguish. They’re both fully licensed physicians, trained in diagnosing and treating illnesses and disorders and providing preventive care.

***

***

But, the foundation of osteopathic medicine is that people are more than just the sum of their body parts.

Learn more about National Osteopathic Medicine Week and how you can share your DO pride.

Assessment: I trained at several DO hospitals in my early career for which I am very grateful.

***

BUSINESS TEXTS FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXO:

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

***

Filed under: "Doctors Only", Quality Initiatives | Tagged: DO, National Osteopathic Medicine Week, osteopathy | 3 Comments »

Posted on April 23, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

A GLOSSARY AND GUIDE TO MEDICAL AND BIOLOGICAL STATISTICS

Courtesy: www.CertifiedMedicalPlanner.org

Biostatistics is the development and application of statistical methods to a wide range of topics in biology. It encompasses the design of biological experiments, the collection and analysis of data from those experiments and the interpretation of the results.

LINK: https://www.springerpub.com/dictionary-of-health-economics-and-finance-9780826102546.html

**

***

So, here is a white paper and glossary of important epidemiological concepts and common bio-statistical terms to help doctors, graduate students and related professionals translate medical research into everyday practice.

Link: http://www.medpagetoday.com/Medpage-Guide-to-Biostatistics.pdf

Assessment: Your thoughts are appreciated.

BUSINESS TEXTS FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXOs

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

THANK YOU

***

Filed under: Glossary Terms | Tagged: BIOLOGICAL STATISTICS | Leave a comment »

Posted on April 22, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

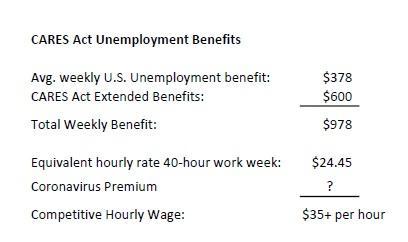

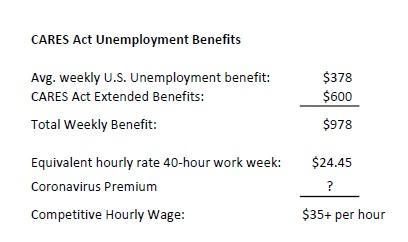

The CARES Act and HSAs, HRAs and FSAs, etc

[By Staff reporters]

The Coronavirus Aid, Relief, and Economic Security (CARES) Act, signed into law March 27, 2020, contains important updates on the use of health savings accounts (HSAs), flexible spending accounts (FSAs) and health reimbursement accounts (HRAs).

***

|

|

***

So, we wanted to inform you of the below changes that expand qualified medical expenses and access to remote care: |

| • |

Telehealth services |

|

| • |

High-deductible health plans (HDHPs) with an HSA may provide pre-deductible coverage for telehealth and other remote care services. This provision will last until December 31, 2021 (plan year must begin prior to this date). |

|

| • |

Certain over-the-counter (OTC) drugs and medications as qualified medical expenses |

|

| • |

The CARES Act restores the ability to use HSAs, FSAs and HRAs to purchase certain OTC drugs and medications, like aspirin and other pain medications, allergy medication, etc., without a doctor’s prescription. |

| • |

For the first time, menstrual care products are considered qualified medical expenses for payment or reimbursement with an HSA, FSA or HRA. |

| • |

Both provisions for OTC and menstrual products apply to amounts paid or expenses incurred on or after January 1, 2020, and are ongoing without an expiration date. |

|

|

| Important note for FSAs and HRAs: |

| You can use your account funds to purchase these products starting today. However, be sure individual merchants, like pharmacies and convenience stores, update their point of sale (POS) system to now recognize these products as qualified medical expenses for FSA and HRA. |

| Use your payment card as you normally would for these purchases, and if the sale will not process, you can pay out of pocket with the option to reimburse yourself with account funds. As a reminder, keep your itemized receipt or explanations of benefits, which are needed to verify each purchase so you can be reimbursed. |

| For HSAs, you may use your debit card as you normally would since no claim reimbursement process is required. Please retain copies of your receipts as needed for tax purposes. |

| Please visit the US Federal website for the latest developments and regulation changes related to COVID-19 and your health account(s), such as the CARES Act.

***

***

Assessment: Your thoughts are appreciated

***

|

Filed under: Health Economics, Health Insurance, Health Law & Policy | Tagged: CARES Act, HSA | 4 Comments »

Posted on April 21, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Opinion-Editorial

[By Darrell K. Pruitt DDS]

[By Darrell K. Pruitt DDS]

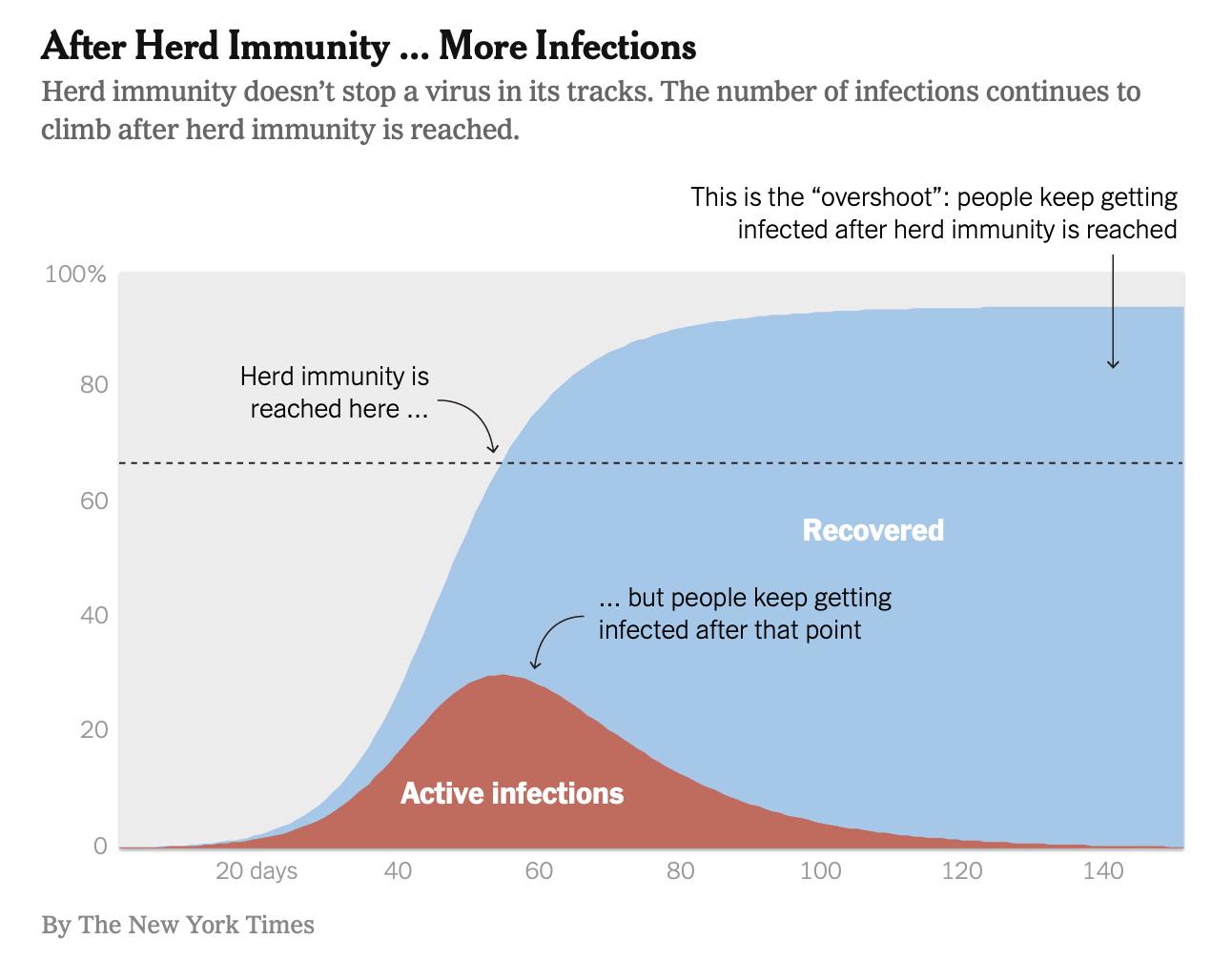

The ONLY way to protect dentists, staff, patients and their families from the risk of fatal COVID-19 infections is to keep the virus out of dental offices. (See graph from the New York Times).

***

Prediction: If quick and reliable testing is not available soon, within weeks after dental offices re-open for routine dental care – creating aerosols with high speed hand pieces, air/water syringes and ultrasonic scalers – dental offices will justifiably become known as reliable sources of COVID-19 infections, before being closed down again by the state.

Assessment: Your thoughts are appreciated.

***

Filed under: Experts Invited, LifeStyle, Op-Editorials, Pruitt's Platform | Tagged: corona, Darrell K. Pruitt, DDS, dentists | 3 Comments »

Posted on April 19, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS A MEDICAL “SENTINEL EVENT”

Courtesy: www.CertifiedMedicalPlanner.org

Terms in the Covid Virus Pandemic News

The Joint Commission suggests a Sentinel Event is any unanticipated occurrence in a healthcare setting resulting in death or serious physical or psychological injury to a patient or patients, not related to the natural course of the patient’s illness.

LINK: https://www.amazon.com/Dictionary-Health-Insurance-Managed-Care/dp/0826149944/ref=sr_1_4?ie=UTF8&s=books&qid=1275315485&sr=1-4

Sentinel Events specifically include loss of a limb or gross motor function, and any event for which a recurrence would carry a risk of a serious adverse outcome. Sentinel events are identified to help aid in root cause analysis and to assist in development of preventive measures.

TJC tracks events in a database to ensure they are adequately analyzed and undesirable trends or decreases in performance are caught early and “mitigated”.

PODCAST: https://www.bing.com/videos/search?q=Sentinel+Events+in+Hospitals&&view=detail&mid=8E346C4173EB23B5A2798E346C4173EB23B5A279&&FORM=VRDGAR&ru=%2Fvideos%2Fsearch%3Fq%3DSentinel%2BEvents%2Bin%2BHospitals%26FORM%3DVDMHRS

Deborah Leah Birx MD coordinator for the White House Corona Virus Task Force mentioned the term in the daily presidential briefings on the Covid-19 pandemic. And so, your thoughts and comments are appreciated.

Assessment: Your thoughts are appreciated.

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Glossary Terms | Tagged: sentinel events | Leave a comment »

Posted on April 18, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Medical Professionals Running Toward Corona – Hospital Administrators Running Away

[By staff reporters]

***

Right versus Left

***

Assessment: Your thoughts are appreciated.

***

***

Filed under: "Doctors Only" | Tagged: corona virus, hospital administrators, white coats | 1 Comment »

Posted on April 17, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Impact Assessment Survey

Dear David, and ME-P Readers

We are pleased to share with you the release of Research2Guidance’s “Impact Assessment Survey: How Corona Impacts the Global Digital Health Industry” whitepaper.

513 digital health experts representing a broad range of healthcare companies shared their views in our global study. Discover their opinions and 10 key takeaways.

Below are just some of the insights from the study and the first special story.

- Mixed impact assessment: 34% see positive impact of the pandemic on their business, 31% a negative. Interestingly Asian companies tend to have a more negative view on the future of their business (36%)

- Digital health companies assess the impact on their business more positively than the rest, 44%expect that the pandemic will have a positive impact on their business. Contrary, healthcare providers are very pessimistic about the future, 67% have a negative outlook on their business.

- Above all, the crisis will bring about a significant improvement in patient acceptance of digital solutions (53%)

- Telehealth solutions will benefit the most (65%) followed by remote monitoring (42%) and self-testing solutions (31%). Interestingly, tracking and tracing solutions are seen more as a short term opportunity. Only 11% of companies rate their potential as high.

- 4-6 months is the expected durationof the crisis according to the global digital health community (43%)

- The impact will be long lasting (67%), which means that changes done during the crisis will be kept and not turned back.

- and much more…

If you have any questions, please let me know. Thank you for your time.

Stay safe and healthy.

Ralf Jahns, MD

Filed under: iMBA, Inc. | 5 Comments »

Posted on April 16, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on April 15, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Employers and “Brokers”

By staff reporters

***

***

Revenue:

- Anthem Revenue $104 Billion (2019)

- Cigna Revenue $154 Billion (2019)

- United Revenue $242 Billion (2019)

- Aetna Revenues $69.6 Billion (2019)

CEO Salary:

- Cigna CEO salary $18.9 million (2018)

- United CEO salary $21.5 million (2018)

- Aetna CEO salary $18.7 million (2017)

NOTE: The total annual healthcare spending in the US is over $3.6 trillion annually. Healthcare spending on administration: 73%. Percentage of healthcare spending on physician salary: less than 8%.

Assessment: Your thoughts are appreciated.

***

***

Filed under: Health Economics, Health Insurance | Tagged: Health insurance CEO salary, healthcare costs, physician costs | 7 Comments »

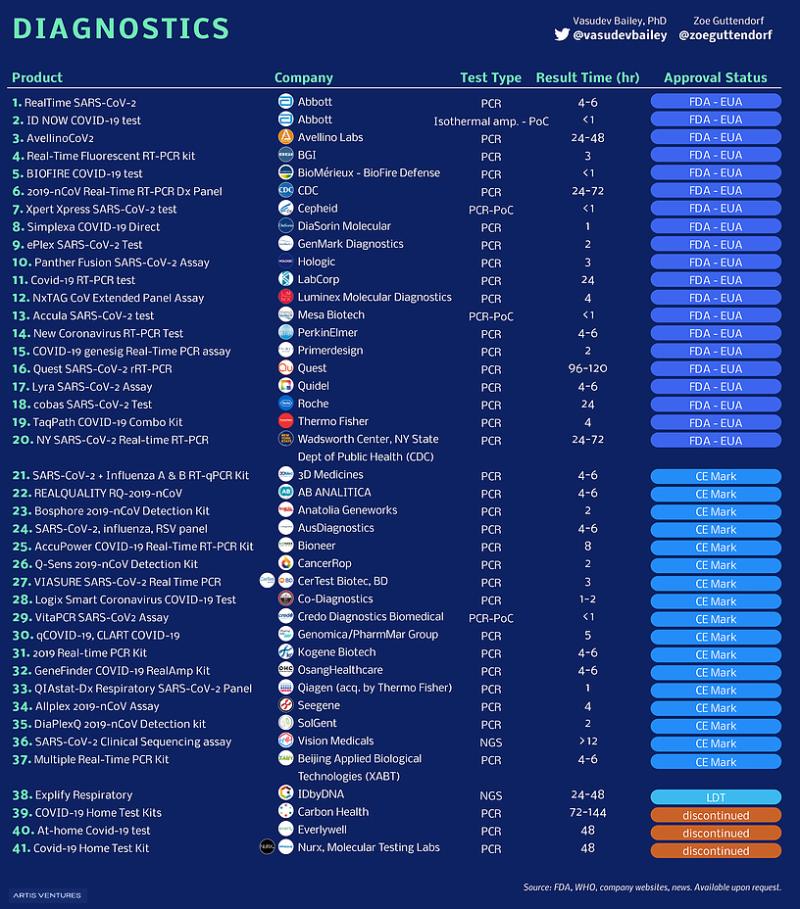

Posted on April 14, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Some Under Clinical Trials

By Igor Korolev DO, PhD

Physician / Neuroscientist – Improving Healthcare & Health Outcomes through Science & Technology

Tests developed / approved as fast as 5 minutes! Several are potential drug treatments & vaccines under evaluation in clinical trials.

There is HOPE!

***

***

Disclaimer – For informational purposes only; should not be considered medical advice; always consult a healthcare professional.

Assessment: Your thoughts are appreciated.

BUSINESS TEXTS FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXOs

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

THANK YOU

***

Filed under: "Doctors Only", Health Economics, Health Insurance | Tagged: 23 Potential COVID-19 Drugs, Corona tests, Covid-19 tests, Igor Korolev DO | 2 Comments »

Posted on April 13, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on April 11, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

KARL VON VIERORDT’S TIME LAW AND THE CORONA PANDEMIC

Courtesy: https://lnkd.in/eBf-4vY

Underestimating Long Periods AND Overestimating Short Periods

Karl Von Vierordt spent his career studying how people perceive time. His biggest finding is the opposite of what you’d assume.

LINK: https://lnkd.in/eZ-q-wN The longer something drags on the easier it is to forget the earlier moments of your experience. Five minutes can feel long because you remember everything you’ve thought about over those five minutes. An hour can feel short because your mind might have contemplated 17 different topics during that period, 15 of which you don’t recall anymore.

TIME PODCAST: https://lnkd.in/ebnXxGH

***

***

EXAMPLE: Make someone wait in a room for one minute. After a minute, ask them how long they think they’ve been waiting. They’ll likely tell you something like “three minutes.” Now put them in the room for an hour, and ask them again. They’ll likely tell you something like “40 minutes.”

QUERY: Does this relate to Corona Virus “stay-at-home” orders and patient age?

ANSWER: https://lnkd.in/eaHPhUA

Your thoughts and comments are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Ethics, LifeStyle | Tagged: corona virus, KARL VON VIERORDT, time, time law, time passage | 1 Comment »

Posted on April 10, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

SURFACE SURVIVAL

[By staff reporters]

***

***  ***

***

***

***

***

Filed under: LifeStyle | Tagged: corona, corona life span, Covid-19 lifespan | 2 Comments »

Posted on April 9, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS “CONTACT TRACING” IN PUBLIC HEALTH?

Courtesy: www.CertifiedMedicalPlanner.org

When a patient tests positive, you make a list of everyone they came in close contact with. Then, you find those people and make sure they self-isolate before infecting others.

That sounds straightforward, but contact tracing a new patient typically takes three days, which is “an insurmountable hurdle in the U.S., with its low numbers of public health workers and tens of thousands of new cases every day.”

ELSEWHERE: South Korea used high-tech contact tracing to tame its outbreak. The government compiled GPS data, credit card swipes, and other info into a public log showing where COVID-19 patients had traveled.

Some countries (including the U.S.) are trying other methods, including looking at smart-phone location data and developing Bluetooth systems that provide warnings if you’ve crossed paths with an infected person.

PROBLEMS: Despite its widespread use in places like Singapore, contact tracing has raised concerns about privacy and governments following citizens’ whereabouts.

***

***

***

PODCAST: https://www.youtube.com/watch?v=hlHCLXv2HQs

PODCAST: https://www.youtube.com/watch?v=CQBO_DHBtzw

And so, Contact Tracing is a term you’ll be hearing a lot more of in the coming weeks.

Assessment: Your thoughts and comments are appreciated.

BUSINESS TEXTS FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXO

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

THANK YOU

***

Filed under: Glossary Terms, Health Insurance, iMBA, Inc. | Tagged: contact tracing, corona virus, Covid-19, public health | 6 Comments »

Posted on April 8, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

THE 6 [Six] ANATOMIC SITES TO TAKE YOUR TEMPERATURE

Courtesy: www.CertifiedMedicalPlanner.org

Covid-19 Vital Sign Diagnostics

It is well known that a high temperature is one stigmata of the Corona Virus [88% of cases]; even higher than the seasonal flu.

But, what are the 6 gross anatomic landmarks to take a temperature and how do we adjust for standards of error?

NOTE: This information might save your life.

***

***

LINK: https://www.wikihow.com/Take-a-Temperature

PODCAST: https://www.bing.com/videos/search?q=rectal+thermometer&&view=detail&mid=D8419140B661244A970CD8419140B661244A970C&&FORM=VRDGAR&ru=%2Fvideos%2Fsearch%3Fq%3Drectal%2Bthermometer%26FORM%3DVQFRAF

Your thoughts and comments are appreciated.

BUSINESS TEXTS FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXOs:

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

THANK YOU

***

Filed under: Health Insurance, iMBA, LifeStyle | Tagged: corona virus, Covid-19, temperature, thermometer | Leave a comment »

Posted on April 7, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

iMBA Inc, NOW OFFERING FREE BUSINESS CONSULTATIONS & FINANCIAL ADVISORY OPINIONS FOR MEDICAL COLLEAGUES & ENTREPRENEURS

Courtesy: https://lnkd.in/eVGcji5

By Ann Miller RN MHA CMP®

[Executive Director]

After an overwhelming initial response, the Institute of Medical Business Advisors [iMBA, Inc] is again offering free 60 minute phone or video consultations and second opinions to doctors, nurses and medical colleagues on a limited scheduling and time basis, during the current Corona Virus outbreak 24/7.

REGULAR SERVICE: https://lnkd.in/dw7FHyP Professional fees are waved during this time of crisis. According to Professor and CEO Dr. David Edward Marcinko MBA CMP, “this is our small way to help give back to colleagues who are vital to the US public health system and wellness of the country.” Topics include a plethora of personal financial planning and / or medical practice management and entrepreneurial business issues.

TOPIC LIST: https://lnkd.in/e7WrDj9

TO SCHEDULE: MarcinkoAdvisors@msn.com B

***

***

BUSINESS, FINANCE, INVESTING & INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

PHYSICIAN-EXECUTIVES AND MEDICAL CXOs:

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

THANK YOU

***

Filed under: CMP Program, Financial Planning, iMBA, Inc., Investing | 2 Comments »

Posted on April 6, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Front Line First Medical Covid-19 Responders

[By staff reporters]

***

***

Assessment: Your thoughts are appreciated.

***

BUSINESS TEXTS FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXOs:

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

THANK YOU

***

Filed under: iMBA, Inc. | Tagged: Corona first responders, Covid-19 | Leave a comment »

Posted on April 5, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

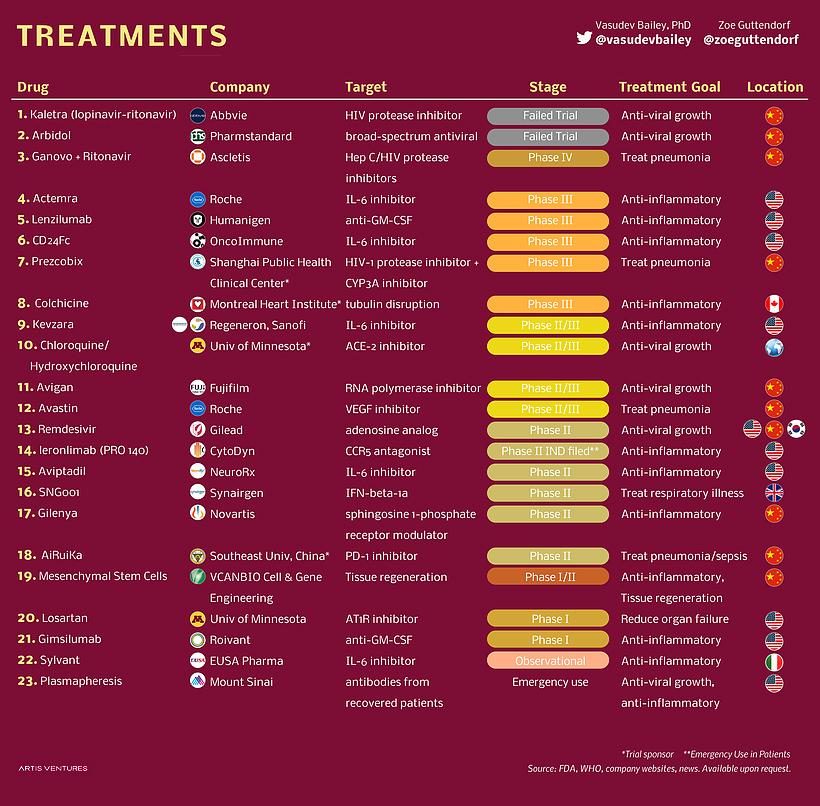

COVID-19 Drugs

[By staff reporters]

Drugs being studied in clinical trials. 30+ drug candidates in preclinical research phase.

There is HOPE!

***

***

Disclaimer – For informational purposes only; should not be considered medical advice; consult a healthcare professional. Drugs shown are not yet approved for use to treat COVID-19 but are being investigated for use in clinical trials.

***

Corona Virus Economics

***

******

******

THANK YOU

Filed under: "Doctors Only", Drugs and Pharma | Tagged: 23 Potential COVID-19 Drugs, corona virus | 1 Comment »

Posted on April 2, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

MORE Corona Virus Precautions

By Dr. David Edward Marcinko MBA

Courtesy: www.CertifiedMedicalPlanner.org

If you wear gloves because of Covid-19, and if you don’t take them off properly, you just get everything that was all over the gloves, all over yourself and everything else. As a surgeon for almost two decades, I can tell you that taking gloves off correctly isn’t a trivial thing.

***

***

HOW TO REMOVE: Briefly, you want to pinch one glove near the wrist and pull it over your hand so it ends up inside out. Then hold that in your gloved hand and carefully slip the fingers of your bare hand into the top of the other glove, let it turn inside out and cover the balled-up other glove.

***

CDC: Check out this step-by-step CDC infographic. And, if you’re not disposing of them properly, you’re just potentially contaminating more surfaces and putting yourself at a much higher risk. Finally, don’t skip hand washing after you take them off, even if you’ve removed them right.

PODCAST: https://www.bing.com/videos/search?q=how+to+removesurgicalgloves&&view=detail&mid=2607568A504FC540B18D2607568A504FC540B18D&&FORM=VRDGAR&ru=%2Fvideos%2Fsearch%3Fq%3Dhow%2Bto%2Bremovesurgicalgloves%26FORM%3DHDRSC3

Assessment: Your thoughts and comments are appreciated.

***

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Health Economics, Health Insurance, Health Law & Policy, LifeStyle, Pruitt's Platform, Touring with Marcinko | Tagged: gloves | 1 Comment »

Posted on April 1, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

R.I.P JAMES T. GOODRICH MD PhD

Courtesy: www.MedicalExecutivePost.com

By Dr. David Edward Marcinko MBA

Famed Neuro-Surgeon Succumbs to Covid19

BREAKING NEWS: Dr. James T. Goodrich was director of the Division of Pediatric Neurosurgery and Professor of Clinical Neurological Surgery, Pediatrics, Plastic and Reconstructive Surgery at the Albert Einstein College of Medicine.

LINK: https://www.beckersspine.com/spine/item/48700-new-york-neurosurgeon-who-made-medical-history-dies-of-covid-19.html

CV: https://www.drjamestgoodrich.org/

A CATASTROPHE – I knew of him; of course. But, never fortunate to meet him.

A GIANT is gone! Not much else to say.

THE END

***

Filed under: "Doctors Only", Breaking News | Tagged: JAMES T. GOODRICH MD PhD | 1 Comment »

Posted on April 1, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

National Doctors’ Day is Global

[By staff reporters]

National Doctors’ Day is a day celebrated to recognize the contributions of physicians to individual lives and communities. The date may vary from nation to nation depending on the event of commemoration used to mark the day.

In some nations the day is marked as a holiday. Although supposed to be celebrated by patients in and benefactors of the healthcare industry it is usually celebrated by health care organizations. Staff may organize a lunch for doctors to present the physicians with tokens of recognition. Historically, a card or red carnation may be sent to physicians and their spouses, along with a flower being placed on the graves of deceased physicians.

***

***

LINK: https://nationaltoday.com/doctors-day/

Assessment: Your thoughts are appreciated.

***

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: iMBA, Inc. | Tagged: National Doctors' Day | 1 Comment »

Posted on March 30, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on March 28, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

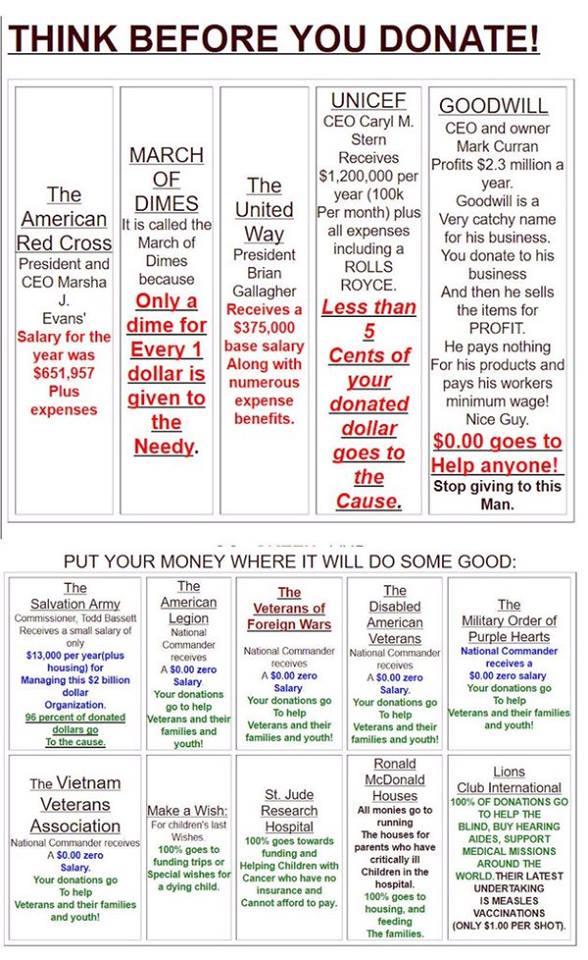

Cautious Corporate Giving?

[By staff reporters]

***  ***

***

NOTE: This chart has not been independently verified by us.

Assessment: Your thoughts are appreciated.

THANK YOU

8

***

Filed under: Risk Management | Tagged: charitable giving, charity, donors | Leave a comment »

Posted on March 27, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

A NEW I.P.O

BY HEALTH CAPITAL CONSULTANTS, LLC

***

On January 30, 2020, 1Life Healthcare, Inc. (One Medical) went public, opening at $14 per share, and closing at $22.07 per share. The innovative San Francisco-based direct primary care organization more closely resembles a technology start-up than a traditional healthcare organization.

The membership model service provides “seamless access” to primary care services at “calming offices,” 24/7 virtual care, and 21st century technology (e.g., a mobile application that allows patients to schedule appointments and message their provider).

**

HEALTH CARE DISRUPTIVE INNOVATORS

***

A new report from our colleagues over at Health Capital Consultants, LLC:

LINK: https://www.healthcapital.com/hcc/newsletter/02_20/HTML/IPO/convert_ipo_hc_topics.php#_edn4

ASSESSMENT: Your thoughts are appreciated.

***

***

Filed under: Experts Invited, Quality Initiatives, Research & Development | Tagged: Health Capital Consultants LLC, Health Care "DISRUPTORS" | 1 Comment »

Posted on March 25, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

A Per-Capita Snapshot

[By staff reporters]

***

***

***

***

***

THANK YOU

Filed under: Breaking News, Health Insurance, LifeStyle | Tagged: Covid-19, Covid-19 Testing | 2 Comments »

Posted on March 24, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on March 23, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

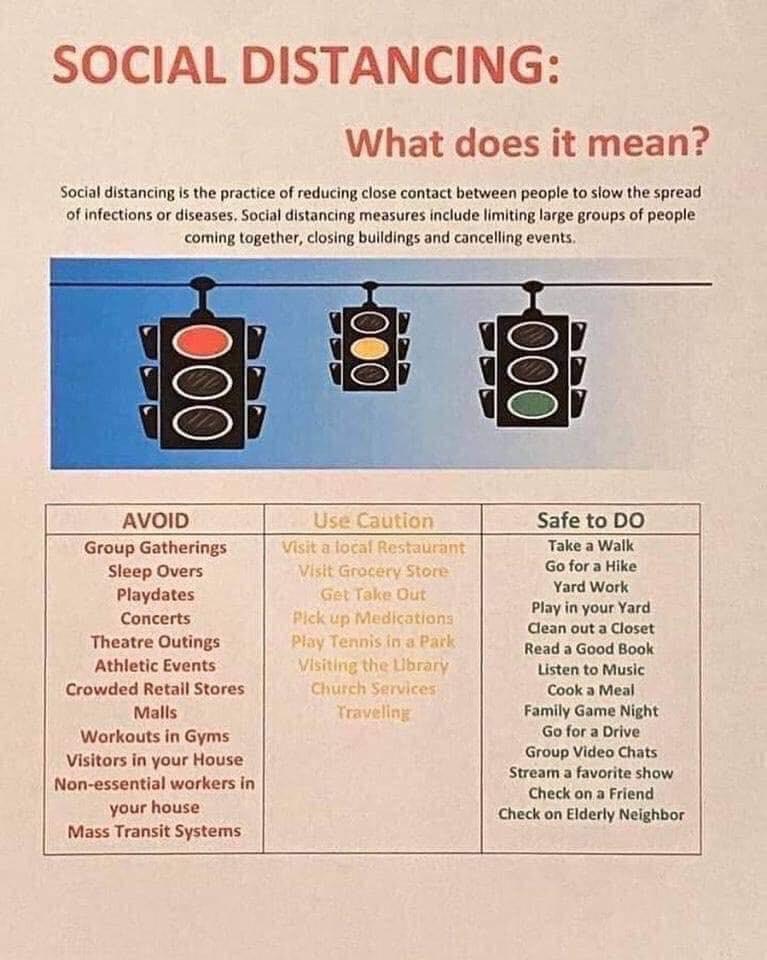

GET BACK; JACK!

GET BACK; JILL!

[By staff reporters]

With the podiums a safe social distance apart, Democratic candidates Bernie Sanders and Joe Biden debated a few days ago on how to respond to the coronavirus pandemic, the chances of a recession, and their handwashing techniques.

***

***

Social distancing is a set of nonpharmaceutical infection control actions intended to stop or slow down the spread of a contagious disease. The objective of social distancing is to reduce the probability of contact between persons carrying an infection, and others who are not infected, so as to minimize disease transmission, morbidity and ultimately, mortality.

Social distancing is most effective when an infection can be transmitted via droplet contact (coughing or sneezing); direct physical contact, including sexual contact; indirect physical contact (e.g. by touching a contaminated surface such as a fomite); or airborne transmission (if the microorganism can survive in the air for long periods).

Social distancing may be less effective in cases where an infection is transmitted primarily via contaminated water or food or by vectors such as mosquitoes or other insects, and less frequently from person to person. Drawbacks of social distancing can include loneliness, reduced productivity, and the loss of other benefits associated with human interaction.

Historically, leper colonies and lazarettos were established as a means of preventing the spread of leprosy and other contagious diseases through social distancing, until transmission was understood and effective treatments invented.

***^

***

***

Filed under: LifeStyle | Tagged: SOCIAL DISTANCING? | 5 Comments »

Posted on March 21, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

What it is – How it works?

Courtesy: http://www.CertifiedMedicalPlanner.org

In public health epidemiology, while numerators are measures of health events, the denominator is the population from which events are drawn.

LINK: https://www.amazon.com/Dictionary-Health-Economics-Finance-Marcinko/dp/0826102549/ref=sr_1_6?ie=UTF8&s=books&qid=1254413315&sr=1-6

For example, if we are measuring the incidence of Covid-19 among teens, who might comprise your denominator?

ANSWER: Any denominators used should be reflective of the population who could have been included in the numerator had they developed the condition of interest. This is the population at risk, and is often taken as the number of people who are disease-free at the start of data collection. If individuals who could not develop the condition of interest were included in the denominator, this would result in an underestimation of calculated rates.

*****

***

PODCAST: https://www.coursera.org/lecture/epidemiology-tools/denominators-jnpaa

PODCAST: https://www.healthknowledge.org.uk/public-health-textbook/research-methods/1a-epidemiology/numerators-denominators-populations

Assessment: Your thoughts and comments are appreciated.

***

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: iMBA, Inc. | Tagged: Epidemiology, public health denominator, public health numerator | Leave a comment »

Posted on March 20, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Obvious Covid-19 Implications

By Dr. David Edward Marcinko; MBA, CPHQ, CMP

We’ve discussed biologic false positives and false negatives before on this ME-P.

LINK: https://medicalexecutivepost.com/2019/09/14/what-are-false-positive-and-false-negative-tests/

Courtesy: www.CertifiedMedicalPlanner.org

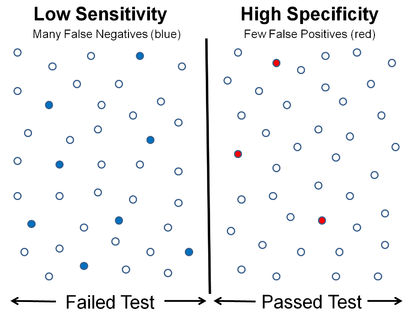

So, now is the time to discuss and conquer the medical laboratory concepts of Sensitivity and Specificity.

***

Sensitivity and specificity are statistical measures of the performance of a binary classification test, also known in statistics as a classification function, that are widely used in medicine.

LINK: https://www.amazon.com/Dictionary-Health-Insurance-Managed-Care/dp/0826149944/ref=sr_1_4?ie=UTF8&s=books&qid=1275315485&sr=1-4

- Sensitivity (also called the true positive rate, the recall, or probability of detection in some fields) measures the proportion of actual positives that are correctly identified as such (e.g., the percentage of sick people who are correctly identified as having the condition).

- Specificity (also called the true negative rate) measures the proportion of actual negatives that are correctly identified as such (e.g., the percentage of healthy people who are correctly identified as not having the condition).

LINK: https://www.differencebetween.com/difference-between-sensitivity-and-vs-specificity/

NOTE: The terms “positive” and “negative” don’t refer to the value of the condition of interest, but to its presence or absence; the condition itself could be a disease, so that “positive” might mean “diseased”, while “negative” might mean “healthy”.

***

***

And so, colleague Michael Lawrence Langan MD opines on a much deeper level.

ESSAY: https://disruptedphysician.blog/2016/11/19/diagnostic-testing-101-1-the-importance-of-sensitivity-specificity-and-diagnostic-test-accuracy-5/

Assessment: Your thoughts and comments are appreciated.

***

***

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Glossary Terms, Health Economics, Health Insurance, Quality Initiatives, Touring with Marcinko | Tagged: SENSITIVITY “versus” SPECIFICITY | 1 Comment »

Posted on March 19, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on March 19, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on March 18, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IT IS – HOW IT WORKS?

Courtesy: www.CertifiedMedicalPlanner.org

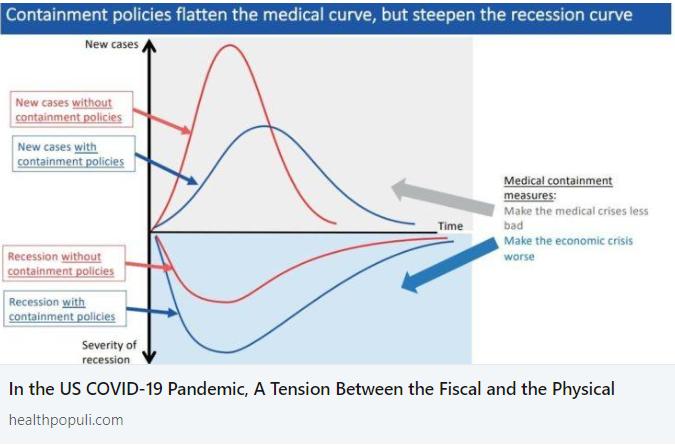

Our message on Corona Virus so far has been “don’t panic.” For the vast majority of individuals, Corona Virus is not an existential threat.

However, the rapid rate of the virus’s spread has the potential to overwhelm our health system and cause a lot of problems.

And so, colleague Aaron E. Carroll MD MS explains the infection curve, right here.

***

***

PODCAST: https://theincidentaleconomist.com/wordpress/flattening-the-curve-of-coronavirus-infections/

Assessment: Your thoughts and comments are appreciated.

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Breaking News, Experts Invited, Health Economics, Quality Initiatives | Tagged: Aaron E. Carroll MD, corona virus, Covid-19 | 1 Comment »

Posted on March 14, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

The Most Famous Number in History

[By Staff Reporters]

Pi Day is an annual celebration of the mathematical constant π. Pi Day is observed on March 14 since 3, 1, and 4 are the first three significant digits of π. In 2009, the United States House of Representatives supported the designation of Pi Day.

***

***

PODCAST: https://www.bing.com/videos/search?q=pi+day&&view=detail&mid=9C324BD69AEEC8028C129C324BD69AEEC8028C12&&FORM=VRDGAR&ru=%2Fvideos%2Fsearch%3Fq%3Dpi%2Bday%26FORM%3DHDRSC3

Assessment: Your thoughts and comments are appreciated.

BUSINESS, FINANCE AND INSURANCE TEXTS FOR DOCTORS:

1 – https://lnkd.in/ebWtzGg

2 – https://lnkd.in/ezkQMfR

3 – https://lnkd.in/ewJPTJs

THANK YOU

***

Filed under: Glossary Terms | Tagged: pi day | Leave a comment »

Posted on March 14, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Human Health Behavior and COVID-19 Thoughts

Courtesy: www.CertifiedMedicalPlanner.org

Here are 3 theories and 1 “rule” for the healthcare industrial complex that may help explain how the sector may not work correctly; from trauma, to epidemiology and to Corona; all the time.

1 – Berkson’s Paradox: Strong correlations can fall apart when combined with a larger population.

For example, among motorcycle crash victims wearing helmets are more likely to be seriously injured than those not wearing helmets. But, that’s because most crash victims saved by helmets did not need to become hospital patients, and those without helmets are more likely to die before becoming a hospital patient.

2 – Group Attribution Error: Incorrectly assuming that the views of a group member, like a physician, reflect those of the whole group in a different discipline.

3 – Baader-Meinhof Phenomenon: Noticing an idea or word every where you look as soon as it’s brought to your attention in a way that makes you overestimate its prevalence.

***

LINK:

https://www.bing.com/videos/search?q=BAADER-MEINHOF+PHENOMENON&&view=detail&mid=7DA25E95466C56098E5A7DA25E95466C56098E5A&&FORM=VRDGAR&ru=%2Fvideos%2Fsearch%3Fq%3DBAADER-MEINHOF%2BPHENOMENON%26FORM%3DHDRSC3

The 90-9-1 Rule: In social media networks, 90% of users just read content, 9% of users contribute a little content, and 1% of users contribute almost all the content.

QUERY: Does Social Media really give a false impression of what ideas are popular or “average.”

THINK: Corona Virus?

ASSESSMENT: Your thoughts and comments are appreciated.

***

TEXTS FOR PHYSICIAN EXECUTIVES:

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

THANK YOU

***

Filed under: Health Economics, Health Insurance, Healthcare Finance, iMBA, Inc., Quality Initiatives | Tagged: Baader-Meinhof Phenomenon, Berkson’s Paradox:, corona virus, Group Attribution Error, The 90-9-1 Rule | 2 Comments »

Posted on March 13, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Office Fire Drills

By Dr. David E. Marcinko MBA

Fire Drills should be performed at least annually and documented.

When first opening an office or when a new employee is brought onboard, staff need to be trained on the use of a fire extinguisher, location of the nearest fire extinguisher and location of alarm pull station (if any) on the first day. Training should be documented and placed in the employee file.

Generally speaking, a fire extinguisher is required every 75 feet in office space and be the appropriate type for the nature of business and equipment in use. Most offices use a multi-purpose ABC extinguisher that can be used on most types of fires.

The types of fires are listed below:

- Class A fires are for ordinary combustible materials such as paper, wood, cardboard, and most plastics.

- Class B fires involve flammable or combustible liquids (gasoline, kerosene, oil, and grease).

- Class C fires are those caused by electrical equipment (wiring, appliances, and outlets).

- Class D fires are chemical fires that involve combustible metals i.e. potassium, sodium, and magnesium.

EXTINGUISHERS

Carbon Dioxide (CO2) extinguishers can be used for class B and C fires. These extinguishers are highly pressurized and are best suited for electrical or computer equipment. They have an advantage over dry chemical extinguishers for this use since they do not leave damaging residue. However, they are not effective for Class A fires.

It is important to know which type of extinguisher is best for the office and equipment since using the wrong type can be critical in an emergency.

***

***

THE EMERGENCY LIST:

At a minimum, a physician office should have a safety program that addresses the following in the event of an emergency:

- Written Program

- Emergency Notification Procedures

- Warning and Evacuations Process

- Evacuation Procedures

- Facility/Department Evaluation or site review

- Means of egress clearly marked (map posted with exit route and nearest exit)

- Emergency Action Plan

- Fire Prevention Plan

- Fire extinguisher location(s), types and use (P.A.S.S. Pull, Aim, Spray & Sweep)

If you are in an area susceptible to weather emergencies such as tornadoes, the emergency plan should address these as well.

Assessment: Your thoughts are appreciated

***

***

Filed under: iMBA, Inc., Insurance Matters, Practice Management | Tagged: David Marciniko, Medical Office Fire Drills | Leave a comment »

Posted on March 12, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Understanding the 2020 Corona Virus Economic Crisis

By William Poole

Dear Dr. David E. Marcinko,

Thank you for your interest in the Merk Perspective.

Merk Senior Economic Adviser and former St. Louis Fed President William Poole shares his thoughts on how to assess the economic impact of the Corona virus, pointing out in what ways it is different from past crises.

There are several aspects of the crisis that deserve separate attention. Many will seem obvious but nonetheless need to be made explicit to yield a thorough analysis.

MORE: https://www.merkinvestments.com/insights/2020/2020-03-12.php?utm_source=merk&utm_medium=link&utm_campaign=merk-campaign®istered=yes

***

***

***

Assessment: Your thoughts are appreciated.

***

Best Wishes,

Axel Merk

President and Chief Investment Officer

Merk Investments

***

Filed under: Health Economics, Health Insurance, Quality Initiatives | Tagged: Corona Virus Economic Crisis, Covid-19, Merk, William Poole | 2 Comments »

Posted on March 11, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

CIRCA: 12/23/2019

By YAHOO Finance!

***

***

Wither the Experts?

Assessment: Your thoughts are appreciated.

***

Filed under: Investing | Tagged: finance | Leave a comment »

Posted on March 10, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

Posted on March 10, 2020 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

***

***

***

***

***

***

******

******

***

***

FOR PHYSICIAN-EXECUTIVES AND MEDICAL CXOs

1 – https://lnkd.in/eEf-xEH

2 – https://lnkd.in/e2ZmewQ

***