BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Correlation measures the relationship between two investments–the higher the correlation, the more likely they are to move in the same direction for a given set of economic or market events. Correlation, in the finance and investment industries, is a statistic that measures the degree to which two securities move in relation to each other. Correlations are used in advanced portfolio management, computed as the correlation coefficient which has a value that must fall between -1.0 and +1.0.

So if two securities are highly positively correlated, they will move in the same direction the vast majority of the time. Negatively correlated investments do the opposite–as one security rises, the other falls, and vice versa. No correlation means there is no relationship between the movement of two securities–the performance of one security has no bearing on the performance of the other.

Correlation is an important concept for portfolio diversification--combining assets with low or negative correlations can improve risk-adjusted performance over time by providing a diversity of payouts under the same financial conditions.

Posted on April 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS – MARKET VOLATILITY

By Staff Reporters

***

***

US stocks nosedived on Thursday, with the Dow tumbling more than 1,200 points as President Trump’s surprisingly steep “Liberation Day” tariffs sent shock waves through markets worldwide. The tech-heavy NASDAQ Composite (IXIC) led the sell-off, plummeting over 4%. The S&P 500 (GSPC) dove 3.7%, while the Dow Jones Industrial Average (^DJI) tumbled roughly 3%. [ongoing story].

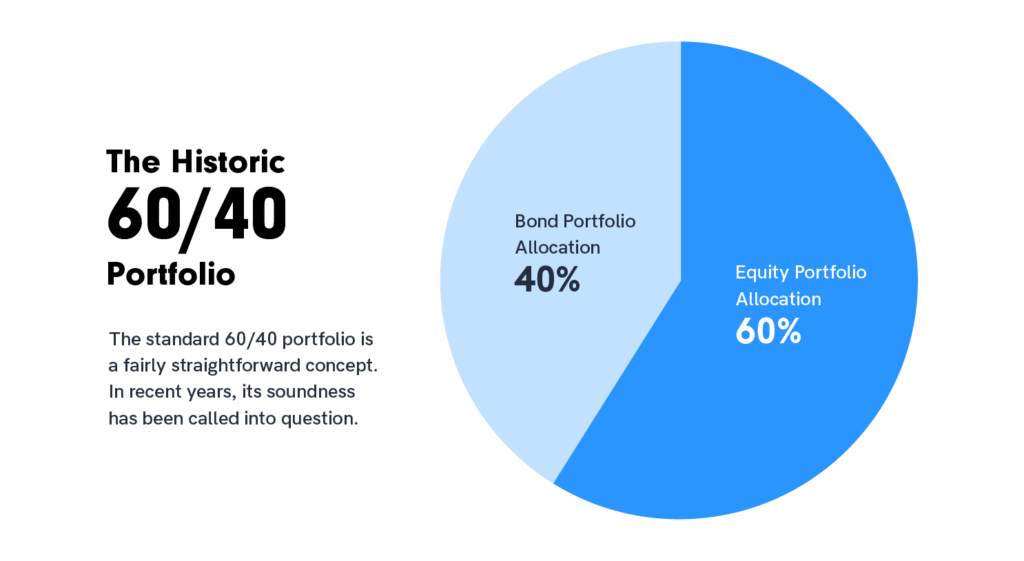

So, does the traditional 60 stock / 40 bond strategy still work or do we need another portfolio model?

***

The 60/40 strategy evolved out of American economist Harry Markowitz’s groundbreaking 1950s work on modern portfolio theory, which holds that investors should diversify their holdings with a mix of high-risk, high-return assets and low-risk, low-return assets based on their individual circumstances.

While a portfolio with a mix of 40% bonds and 60% equities may bring lower returns than all-stock holdings, the diversification generally brings lower variance in the returns—meaning more reliability—as long as there isn’t a strong correlation between stock and bond returns (ideally the correlation is negative, with bond returns rising while stock returns fall).

For 60/40 to work, bonds must be less volatile than stocks and economic growth and inflation have to move up and down in tandem. Typically, the same economic growth that powers rallies in equities also pushes up inflation—and bond returns down. Conversely, in a recession stocks drop and inflation is low, pushing up bond prices.

***

But, the traditional 60/40 portfolio may “no longer fully represent true diversification,” BlackRock CEO Larry Fink writes in a new letter to investors.

Instead, the “future standard portfolio” may move toward 50/30/20 with stocks, bonds and private assets like real estate, infrastructure and private credit, Fink writes.

Here’s what experts say individual investors may want to consider before dabbling in private investments.

It may be time to rethink the traditional 60/40 investment portfolio, according to BlackRock CEO Larry Fink. In a new letter to investors, Fink writes the traditional allocation comprised of 60% stocks and 40% bonds that dates back to the 1950s “may no longer fully represent true diversification.“

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on November 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

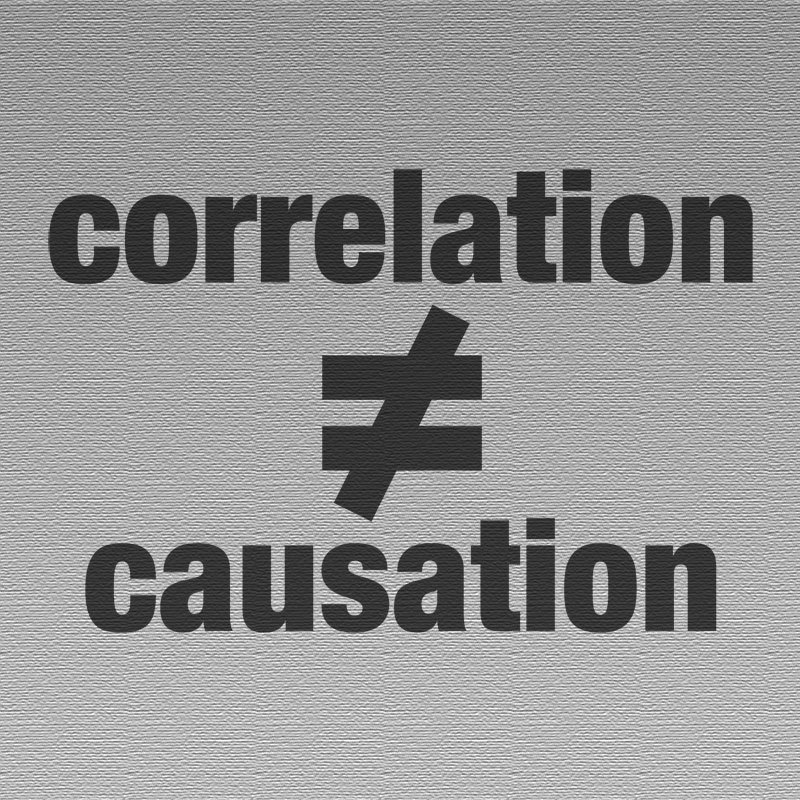

CORRELATION IS NOT CAUSATION

By Staff Reporters

***

***

According to colleague Dan Ariely PhD,Illusory Correlation is the perception of a relationship between variables when none exists. It’s like thinking that carrying an umbrella causes it to rain. Our brains are pattern-seeking machines, often connecting dots that aren’t actually connected. This bias can lead to superstitions and incorrect beliefs.

The illusory correlation occurs when someone believes that there is a relationship between two people, events, or behaviors, even though there is no logical way to connect them. The illusory correlation fools us into believing stereotypes, superstitions, old wives’ tales, and other silly ideas. Sometimes, the perceived connection between two events is harmless. It’s silly to think that a certain number always brings you luck. But forming these connections is completely normal. To avoid illusory correlations, rely on data and evidence rather than anecdotal observations.

So always remember: correlation does not imply causation, no matter how convincing it seems.

Posted on June 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

“Correlation” has been used over the past twenty years by institutions, [physician] investors and financial advisors to assemble portfolios of moderate INVESTMENT risk

Modern Portfolio Theory approaches investing by examining the complete market and the full economy. MPT places a great emphasis on the correlation between investments.

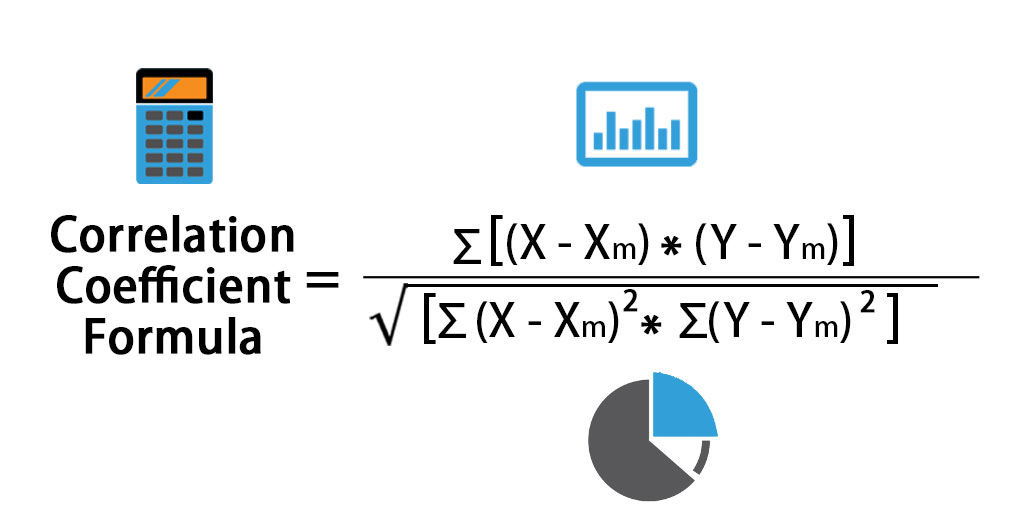

DEFINITION: Correlation is a measure of how frequently one event tends to happen when another event happens. High positive correlation means two events usually happen together – high SAT scores and getting through college for instance. High negative correlation means two events tend not to happen together – high SATs and a poor grade record. No correlation means the two events are independent of one another.

In statistical terms two events that are perfectly correlated have a “correlation coefficient” of 1; two events that are perfectly negatively correlated have a correlation coefficient of -1; and two events that have zero correlation have a coefficient of 0.

In calculating correlation, a statistician would examine the possibility of two events happening together, namely:

If the probability of A happening is 1/X;

And the probability of B happening is 1/Y; then

The probability of A and B happening together is (1/X) times (1/Y), or 1/(X times Y).

There are several laws of correlation including;

Combining assets with a perfect positive correlation offers no reduction in portfolio risk. These two assets will simply move in tandem with each other.

Combining assets with zero correlation (statistically independent) reduces the risk of the portfolio. If more assets with uncorrelated returns are added to the portfolio, significant risk reduction can be achieved.

Combing assets with a perfect negative correlation could eliminate risk entirely. This is the principle with “hedging strategies”. These strategies are discussed later in the book.

In the real world, negative correlations are very rare. Most assets maintain a positive correlation with each other. The goal of a prudent investor is to assemble a portfolio that contains uncorrelated assets. When a portfolio contains assets that possess low correlations, the upward movement of one asset class will help offset the downward movement of another. This is especially important when economic and market conditions change.

As a result, including assets in your portfolio that are not highly correlated will reduce the overall volatility (as measured by standard deviation) and may also increase long-term investment returns. This is the primary argument for including dissimilar asset classes in your portfolio. Keep in mind that this type of diversification does not guarantee you will avoid a loss. It simply minimizes the chance of loss.

In this table provided by Ibbotson, the average correlation between the five major asset classes is displayed. The lowest correlation is between the U.S. Treasury Bonds and the EAFE (international stocks). The highest correlation is between the S&P 500 and the EAFE; 0.77 or 77 percent. This signifies a prominent level of correlation that has grown even larger during this decade. Low correlations within the table appear most with U.S. Treasury Bills.

Posted on June 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

“CORRELATION DOES NOT IMPLY CAUSATION” Repeat After Me!

DEFINITION: The phrase “correlation does not imply causation” refers to the inability to legitimately deduce a cause-and-effect relationship between two events or variables solely on the basis of an observed association between them. CITE: https://www.r2library.com/Resource/Title/082610254

***

***

LOGIC FALLACY: The idea that “correlation implies causation” is an example of a questionable-cause logical fallacy, in which two events occurring together are taken to have established a cause-and-effect relationship.

This fallacy is also known by the Latin phrase cum hoc ergo propter hoc (‘with this, therefore because of this‘). This differs from the fallacy known as post hoc ergo propter hoc (“after this, therefore because of this”), in which an event following another is seen as a necessary consequence of the former event, and from conflation, the errant merging of two events, ideas, databases, etc., into one.

CORRELATION: The degree and relationship between two variables which vary together over time. Correlation can vary from +1 to -1. Values close to +1 indicate a high-degree of positive correlation, and values close to -1 indicate a high degree of negative correlation.

CAUSATION: The”causal relationship between conduct and result”. It connects conduct with effect. Causation, often confused with correlation, indicates the extent to which two variables increase or decrease in parallel. However, correlation by itself does not imply causation. There may be a third factor, for example, responsible for the fluctuations in both variables. LINK: https://lnkd.in/eJNz355

***

***

Assessment: Now, “correlation does not imply causation” is a phrase to emphasize that correlation between two variables does not imply that one causes the other. But – what about evidence and applications in medicine? Colleague Steve Novella explains.