![]()

Exercising Pediatric Fiscal Discipline

By Andrew D. Schwartz CPA

I’m a CPA and my wife is a CFP (Certified Financial Planner). Many ME-P readers are the same; or are doctors or nurses; or MBAs, PhD, CFAs; or other learned professionals, etc.

I’m a CPA and my wife is a CFP (Certified Financial Planner). Many ME-P readers are the same; or are doctors or nurses; or MBAs, PhD, CFAs; or other learned professionals, etc.

Even so, I think together we’ve done a lousy job teaching our two kids – Jonathan (age 15) and Lizzie (age 14) – much about personal finances. We have also done little to help them learn anything about exercising fiscal discipline.

Over the years, we’ve toyed with monthly allowances and paying our kids for doing their household chores. The problem is that we have never been consistent with doling out the promised $20 per month or with enforcing the rules they need to follow to even be eligible to receive their allowance.

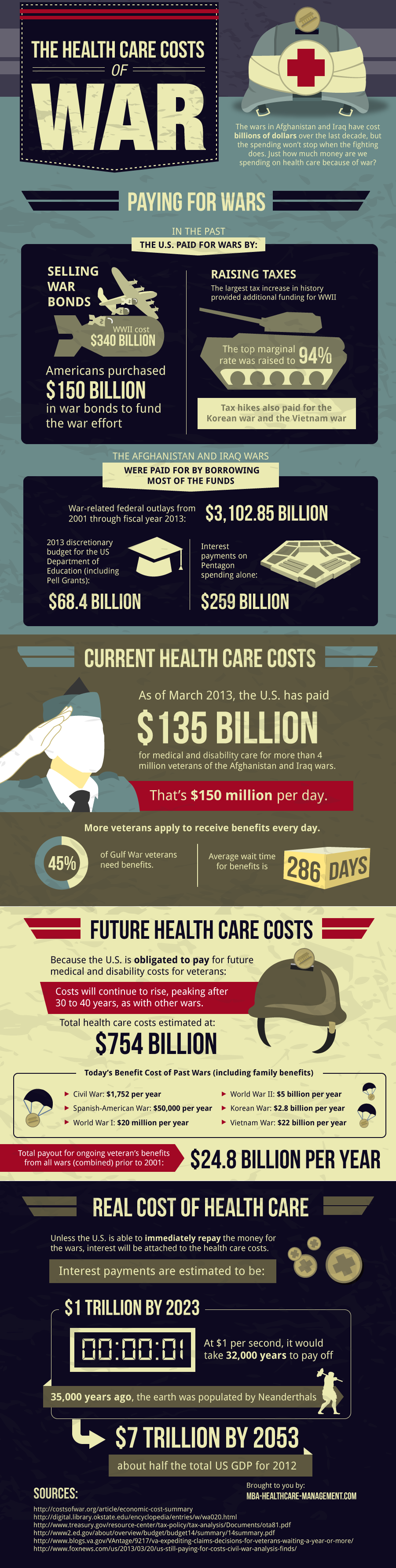

Our Allowance System

So my family’s allowance system has evolved to something like this:

Child: “Dad and/or Mom, I’m getting together with friends. Can I have some money?”

Parent: “Sure thing, Jonathan and/or Lizzie. Will $20 be sufficient?”

Well, as my kids continue to grow up, we have reached the point where this conversation happens pretty regularly. Our kids have no incentive not to ask us for money, since we have a track record of giving them money whenever they ask. And they also don’t have an incentive to try to earn any money on their own, since we have gladly been supporting 100% of their spending.

Change is Coming

That’s all about to change. Financial responsibility for the Schwartz Clan, here we come. As a parent of a teenager, you might be asking, “How will you pull this off Andrew?”

For Christmas/Chanukah last winter, we gave each child a Pass Card issued by American Express. These cards are only available to kids 13 or older.

Enter AMEX

According to American Express, “Pass is a prepaid reloadable Card parents give to teens. It’s safer than cash, and unlike a debit or credit card, teens can only spend what’s preloaded on the Card.” For my two kids, we loaded each card with $100, and then will reload the card on the tenth of each month with their $25 allowance.

Pass cardholders can spend money on the prepaid card pretty much anywhere that takes credit cards. And while parents do have the right to deny their kids access to cash from ATMs, we decided to set up the cards to allow ATM withdrawals. We can change this setting at any time, however. The first ATM transaction each month is free for each kid, and then there is a charge of $2 per withdrawal.

The Thought Process

In theory, when either kid spends all the money on the card, they are out of money until they next receive the $25 on the tenth of the month. Here is where my wife and I will need to exercise some parental discipline and not just dole out more spending money.

Instead, we need to try to use this opportunity to remind Jonathan or Lizzie that if they want to spend more than $25 per month, they can always babysit, shovel snow or rake leaves for our neighbors, work at my office during tax season, or try to find another job that hires 14 and 15 year-old kids to earn extra money.

Other Advantages

For parents, the Pass Card has a nifty web interface that allows parents the opportunity to view balance and purchase history online at any time, transfer additional funds into the card, or tweak the amount or frequency of the automatic reloads. Teens will also be able to logon to the Pass website under a separate login to monitor balances and activity.

According to the site, the Pass Card also provides your child some additional benefits similar to the benefits that come with the AMEX card, including:

- Purchase Protection if an item purchased with the Pass Card breaks within 90 days

- Roadside Assistance if your child’s car won’t start

- Global Assist Services to provide your child with emergency services while traveling

Assessment

I hope the Pass Card works out well for my family and helps my wife and I teach my kids a little about personal finances and fiscal discipline.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PHYSICIANS: www.MedicalBusinessAdvisors.com

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- BLOG: www.MedicalExecutivePost.com

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

![]()

![]()

![]()

![]()

Share this:

Filed under: Financial Planning | Tagged: AMEX, cash management, fiscal discipline, money management, Pass Card, personal finances | 1 Comment »