BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Stocks sank yesterday on news that Russian President Vladimir Putin lowered the threshold for using nuclear weapons, retaliation against the US for allowing Ukraine to use American-made long-range missiles. The NASDAQ and S&P 500 managed to recover, but the DJIA stayed all day in the red.

Treasury yields dropped as bonds rose.

Gold popped as traders sought safety, as the commodity benefited from the US dollar pulling back from a recent one-year high.

Bitcoin continued to climb slowly but surely, reaching another new all-time high.

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The SPX rose 5.81 points (0.10%) to 6,001.35; the Dow Jones Industrial Average® ($DJI) added 304.14 points (0.69%) to 44,293.13, a new all-time closing high; and the NASDAQ Composite®($COMP) gained 11.99 points (0.06%) to 19,298.76.

The 10-year Treasury note yield (TNX) didn’t trade today due to the Veterans Day holiday.

The CBOE Volatility Index® (VIX) inched up to 15.05.

Posted on January 18, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

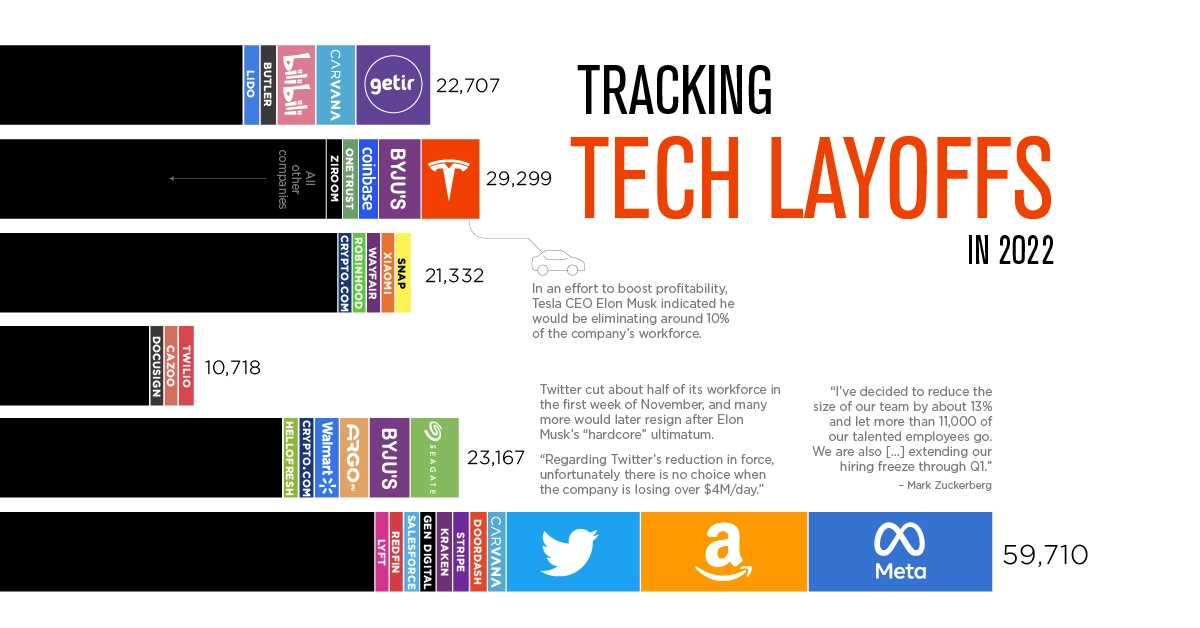

Microsoft shrank its workforce in July and October 2022 and eliminated open positions and paused hiring in various groups. While technology peers Amazon.com Inc., Meta Platforms Inc. and Salesforce Inc. have announced cuts by the thousands in the past few months, Redmond, Washington-based Microsoft has so far been taking smaller steps to deal with a worsening global economic outlook and the potential for a protracted slowdown in demand for software and services. However, Microsoft could announce wide-sweeping layoffs within the next few days. The possibility of the tech giant laying off a significant part of its workforce was first reported by Sky News and later corroborated by Bloomberg. Sky put the number of the cuts at approximately five percent of the company’s 220,000-person workforce or about 11,000 employees total. Bloomberg said it couldn’t find out the scale of the layoffs but reported they would affect “a number of engineering divisions” and that they’re set to be “significantly larger” than other rounds of job cuts undertaken by Microsoft over the last year.

***

Meanwhile, U.S. stocks ended mostly lower with the Dow Jones Industrial Average snapping a four-day win streak after Goldman Sachs reported poor earnings results. The S&P 500 also ended lower, but the NASDAQ Composite eked out a gain as investors focused on whether the early 2023 rally has legs.

The S&P 500 shed 8.12 points, or 0.2%, to end at 3,990.97

The Dow Jones Industrial Average fell 391.76 points, or 1.1%, to finish at 33,910.85

The NASDAQ Composite gained 15.96 points, or 0.1%, ending at 11,095.11

Q4 earnings season continued to heat up, with investors sifting through differing results from Dow member Goldman Sachs and Morgan Stanley, while Travelers Companies warned that its upcoming results will be lower than forecasts. The economic calendar started off a bit slow before beginning to heat up tomorrow, but today a read on New York manufacturing showed an unexpected tumble for January.

Treasury yields were mixed, and the U.S. dollar gained ground, while crude oil prices advanced, and gold traded to the downside.

Asia finished mixed, and markets in Europe also diverged, following a flood of economic data, notably out of China.

Posted on November 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks declined in the first session of the holiday-shortened week, as the economic docket was void of any major releases. The economic calendar will heat up on Wednesday, with reports on durable goods orders, manufacturing and services PMIs, consumer sentiment, and new home sales, as well as the minutes from the Fed’s November monetary policy meeting.

The equity front was also quiet today, but Dow member Walt Disney Company’s announcement that Robert Iger is returning to the company as CEO boosted its shares. In other equity news, Dow component Merck & Co. Inc. announced a $1.35 billion acquisition of clinical stage biotech company Imago BioSciences Inc.

The Treasury yield curve continued to invert ahead of this week’s economic data and following recent positive inflation reports, though the U.S. dollar rallied. Crude oil prices extended a recent decline and gold was lower.

Asian stocks finished mostly lower amid lingering COVID concerns in China, and European stocks ended the day mixed as the global markets continued to assess the trajectory of monetary policies across the world.

Posted on October 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasury market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

Posted on October 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

THE ECONOMY & RECESSION

By Staff Reporters

***

***

U.S. equities rose noticeably in the first trading session of the week following the new U.K. finance minister’s announcement that the government would abandon nearly all its tax cut plans. The moves came amid hopes of some stabilization in the global bond and currency markets which have seen increased volatility in the wake of the initial proposal.

Treasury yields traded mixed, while the U.S. dollar fell amid strength in both the British pound and the euro.

Crude oil prices nudged lower, and gold traded slightly higher.

Bank of America shares rose as the company eclipsed quarterly expectations on a jump in net interest income, while Q3 earnings season is set to kick into a higher gear this week.

***

Economy: This party may be busted by the cops. A US recession is a 100% certainty within the next 12 months, according to Bloomberg’s economic model.

Posted on October 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

Stocks initially fell, and then soared.

Treasury yields rose, particularly on the short end of the curve.

The U.S. dollar declined as the British pound rallied for a second day amid speculation that the U.K. government may reverse course on its tax cut plan.

Crude oil prices reversed higher, and gold prices were lower.

Jobless claims accelerated more than expected.

Asian stocks moved broadly lower amid the inflation uneasiness, while European stocks ended the day in the green as the markets grappled with the potential tax-cut U-turn out of the U.K.

Posted on October 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks traded noticeably lower on the heels of the September nonfarm payroll report, but was still able to post weekly gains following the strong rebound on Monday and Tuesday. The labor data showed job growth rose more than predicted, while the unemployment rate unexpectedly declined, and the labor force participation rate surprisingly dipped. The report seemed to dampen recently increased optimism that the Fed could decelerate its aggressive monetary policy tightening campaign.

In other economic news, wholesale inventories were unrevised at a solid gain, and data on consumer credit showed consumer borrowing was well above expectations.

Treasury yields rose following the labor report, and the U.S. dollar continued to rebound from a stumble earlier in the week.

Crude oil prices climbed following the decision from OPEC+ to cut oil production and gold traded lower.

Asian stocks finished out the week broadly lower, and European stocks trimmed a weekly gain as volatility remained in the currency and bond markets across the globe.

Posted on February 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

IRS: The IRS sent out a notice on February 23rd, warning taxpayers about a price hike coming in the next few months. The tax agency said that interest rates will increase for the calendar quarter starting April 1st, 2022. You can accrue interest on two types of payments: over-payment or underpayment. So starting in April, over-payments will have an interest rate of 4 percent, except for corporations which will earn a 3 percent rate and a 1.5 percent rate for the portion of a corporate over-payment that exceeds $10,000. In terms of underpayments, the interest rate will increase to 4 percent overall and 6 percent for large corporate underpayments.

“Under the Internal Revenue Code, the rate of interest is determined on a quarterly basis,” the IRS website explained. The tax agency did not change interest rates in this last quarter, which began Jan. 1, 2022. Before they get changed in April, the rates are currently 3 percent for general over-payments and 2 percent for corporation over-payments, with a 0.5 percent rate for the portion of a corporate over-payment exceeding $10,000. The underpayment interest is 3 percent right now, expect for large corporations which have a 5 percent rate.

***

***

CURRENCY INFLATION: Inflation may occur when the Federal Reserve, or another central bank, adds fiat currency into circulation at a rate that exceeds that of the economy’s growth rate. That creates a situation in which there are more dollars bidding on fewer goods and services. The result is that goods and services cost more. One reason that inflation has been a constant in the US since 1933 is that the FOMC has continually increased the money supply. In response to the 2008 financial crisis, the Fed dropped its lending rate close to zero as a way to inject more liquidity into the economy, which led to increased inflation but not hyperinflation. While those increases have usually moved in step with growth, that hasn’t always been the case.

And so, in response to the COVID-19 pandemic and subsequent lock-downs, the Federal Reserve released the equivalent of $3.8 trillion in new liquidity in 2020. That amount was equal to roughly 20% of the dollars previously in circulation. And it is one reason why many investors were watching the CPI closely in 2021.

EARNING REPORTS:

Monday: India GDP data; Earnings from Lordstown Motors, Groupon, HP, SmileDirectClub and Zoom Video

Tuesday: US and China manufacturing data; Earnings from AutoZone, Baidu, Domino’s Pizza, Hostess Brands, J.M. Smucker, Kohl’s, Target, AMC Entertainment and Salesforce

Wednesday: European inflation data; Earnings from Abercrombie & Fitch, Dine Brands, Dollar Tree, Snowflake and Victoria’s Secret

Thursday: ISM Non-Manufacturing Index; Earnings from Best Buy, Weibo, Costco and Gap

Friday: US jobs report

10-Year: Treasuries rallied to 1.902%.

Oil: The rise in oil prices is spilling over at the gas pump: The average gas price in the US has jumped 10 cents, to $3.64/gallon, in the past two weeks.

Partial SWIFT ban: Western governments put aside their hesitations and proposed banning some Russian lenders from SWIFT, the global messaging service that facilitates cross-border transactions. It’s a move that could cause turmoil across global financial markets.