BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on June 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

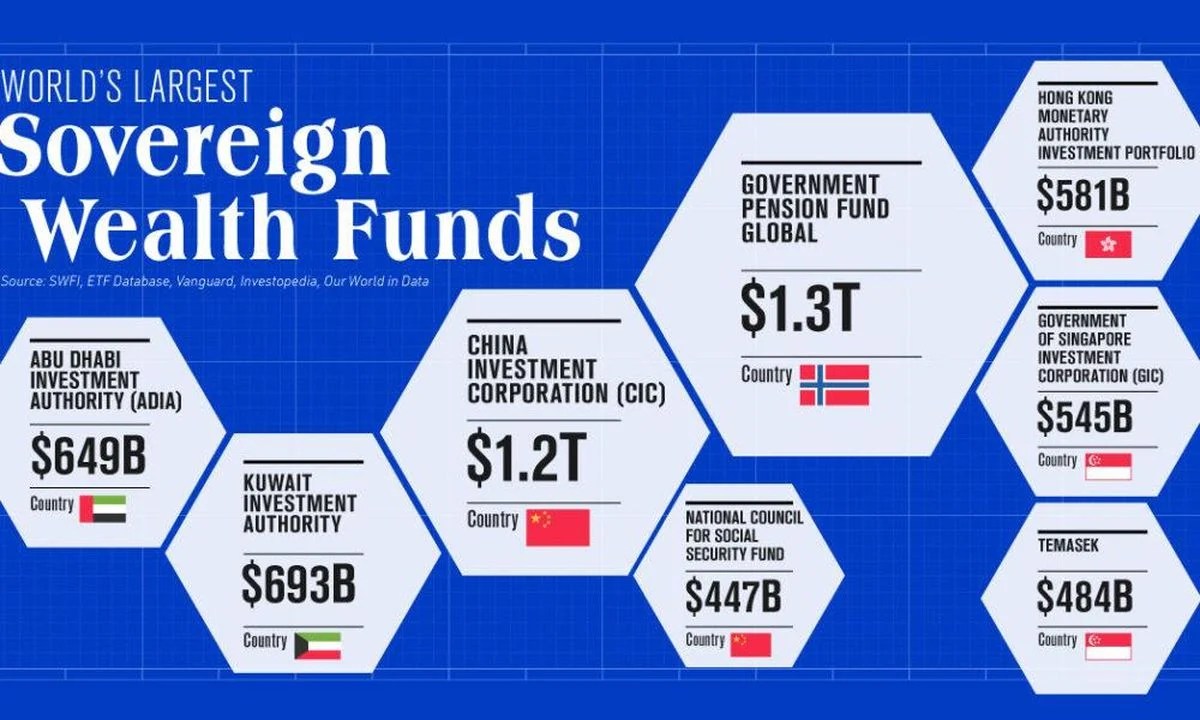

A SWF is essentially an investment fund run by the government. Similar to how a hedge fund or a private equity firm operates, the government would set aside a pot of money and invest it in assets such as stocks, bonds, startups, or real estate.

The idea of the US establishing a sovereign wealth fund akin to Norway’s or Abu Dhabi’s gained momentum recently across the political spectrum. Former President Trump endorsed the concept during a speech on his economic policy agenda for a second term, and the Biden administration has been quietly cheffing up a proposal for a wealth fund over the past several months, Bloomberg reported.

Trump and Biden officials described the fund as a key tool the country could deploy to win the global technological arms race and better compete against geopolitical rivals like China.

For example, the wealth fund could finance capital-intensive sectors such as shipbuilding, nuclear fission, and quantum cryptography that don’t offer near-term ROI for private investors.

However, disadvantages of a SWF include:

Non-Guaranteed Returns, with the Risk of Total Loss

Influence on Foreign Exchange Rates, Introducing Uncertainty

Potential Mismanagement of Funds Due to a Lack of Transparency

Dependency on Global Economic Conditions, Impacting Fund Performance

Challenges in Maintaining Accountability and Addressing Ethical Concerns

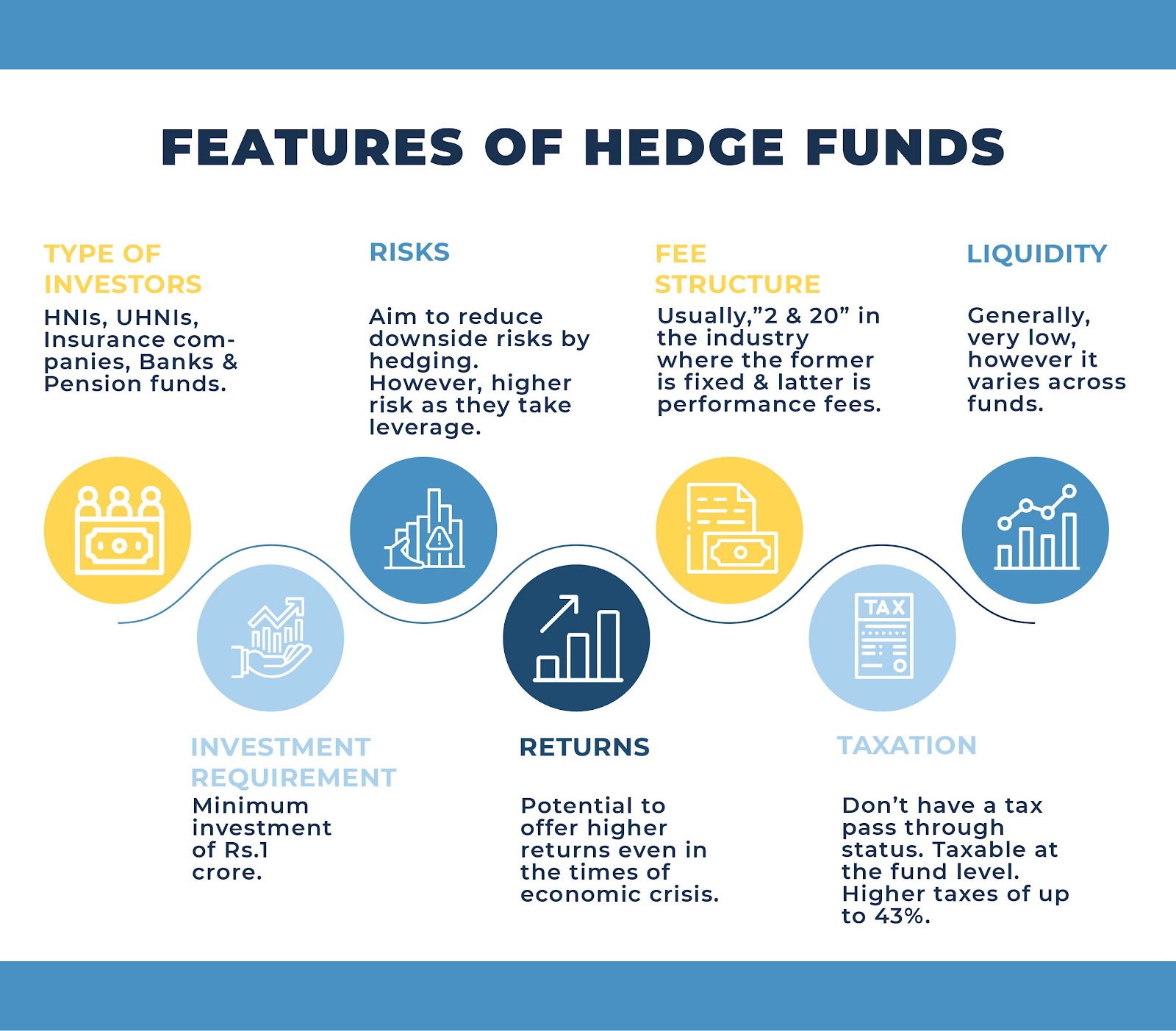

Many doctors are surprised to learn of an alternative investment known as a hedge fund, pooled investment vehicle or private investment fund. Unlike mutual funds, they can be structured in many ways. However, these funds cannot be marketed or advertised, but they are far from illegal or illicit.

In fact, physicians were among the early investors in one the most successful hedge funds. Warren Buffett got his start in 1957 running the Buffett Partnership, a hedge fund not open to the public. His first appearance as a money manager was before a group of physicians in Omaha, Nebraska. Eleven decided to invest some money with him. A few then followed into Berkshire Hathaway Inc, now among the most highly valued companies in the world.

And, more recently, Scion Asset Management® LLC, is a private investment firm founded and led by my eloquent colleague Michael J. Burry, MD and featured in the movie, The Big Short. Other hedge fund mangers of note include: George Soros, Carl Icahn, Ken Griffin, David Tepper, John Paulson and Bill Ackman.

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

The hurdle rate is part of the fund manager’s performance incentive compensation. Also known as a “benchmark,” it is the amount, expressed in percentage points an investor’s capital must appreciate before it becomes subject to a performance incentive fee. Podiatrists should view the hurdle rate as a form of protection or the fee arrangement.

The hurdle rate benchmarks a single year’s performance and may be considered mutually exclusive of any other year, or the hurdle rate may compound each year. The former case is more common. In the latter case, a portfolio manager failing to attain a hurdle rate in the first year will find the effective hurdle rate considerably higher during the second year.

Once a fund manager attains the hurdle rate, the investor’s capital account may be charged a performance incentive fee only on the performance above and beyond the hurdle rate. Alternatively, the account may be charged a performance fee for the entire level of performance, including the performance required to attain the hurdle rate. Other variations on the use of the hurdle rate exist, and are limited only by the contract signed between the fund manager and the investor. The hurdle rate is not generally a negotiating point, however.

Example: A fund charges a performance fee with a 6 percent hurdle rate, calculated in mutually exclusive manner. A podiatrist places $100,000 with the fund. The first year’s performance is 5 percent. The doctor therefore owes no performance fee during the first year because the portfolio manager did not attain the hurdle rate. During year two, the portfolio manager guides the fund to a 7 percent return. Because the hurdle rate is mutually exclusive of any other year, the portfolio manager has attained the 6 percent hurdle rate and is entitled to a performance fee.

High Water Mark

Some hedge funds feature a “high water mark” provision known as a ”loss-carry forward.” As with the hurdle rate, the high water mark is a form of protection. It is an amount equal to the greatest value of an investor’s capital account, adjusted for contributions and withdrawals. The high water mark ensures that the manager charges a performance incentive fee only on the amount of appreciation over and above the high water mark set at the time the performance fee was last charged. The current trend is for newer funds to feature this high water mark, while older, larger funds may not feature it.

Example: A fund charges a 20 percent performance fee with a high water mark but no hurdle rate. A podiatrist contributes $100,000 to the fund. During the first year, the hedge fund manager grows that capital account to $110,000 and charges a 20 percent performance fee, or $2,000. The ending capital account balance and high water mark is therefore $108,000. During year two, the account falls back to $100,000, but the high water mark remains $108,000. During year three, in order for the manager to charge a performance fee, the manager must grow the capital account to a level above $108,000.

Claw Back Provision

Rarely, a hedge fund may provide investors with a “claw back” provision. This term results in a refund to the investor of all or part of a previously charged performance fee if a certain level of performance is not attained in subsequent years. Such refunds in the face of poor or inadequate performance may not be legal in some states or under certain authorities.

ASSESSMENT

Managers of hedge funds, like colleague Dimitri Sogoloff MBA who is the CEO of Horton Point investment-technology firm, often aim to produce returns that are relatively uncorrelated with market indices and are consistent with investors’ desired level of risk.

While hedging may reduce some risks overall, they cannot all be eliminated. According to a report by the Hennessee Group, hedge funds were approximately one-third less volatile between 1993 and 2010.

For a podiatrist who already holds mutual funds and/or individual stocks and bonds, a hedge fund may provide diversification and reduce overall portfolio risk. Consider investing in them with care.

2. Burry, Michael, J: Hedge Funds [Wall Street Personified]. In, Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

4. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

WHAT YOU “MUST KNOW“ ABOUT FINANCIAL ADVISORY FEES

Investment fees still matter despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment, it’s vital to uncover all real financial advisor and stock broker costs.

1. Up-front salesperson commissions. It is easy to ask; “If I buy this investment today and want to get out tomorrow, how much money do I get back?” If the answer is not “all your money,” the difference is probably upfront fees and commissions. These fees may run as high as 30% of the money invested. If you were to earn 5% a year on the investment, it would take 8 years just to break even.

2. Ongoing advisory fees. These are monthly, quarterly, or annual fees paid to advisors for their investment advice and oversight. This includes working with you to pick the asset classes, set diversification, select a portfolio manager, optimize taxes, re-balance holdings and other periodic tasks.

These fees have many names including wrap fee or investment advisory fees. The normal “rule of thumb” is 1% of assets managed, although fees can range from 0 to 7%. Today, it can even be as low as .5%. It can be charged even if the advisor receives an upfront commission. It can be easy to see, or hidden in the fine print.

3. Additional service fees. Find out specifically what services are included financial advisory fees. Additional fees for financial planning or other services are rarely disclosed. They can range from minimal hand-holding focused on your investments to comprehensive financial planning.

4. Ongoing managerial expense ratio fees. These are incredibly well hidden that you may not see them in your statements or invoices. The only way to know is to read the prospectus or other third party analysis, like Morningstar.com. And, they can vary greatly for the same investment, depending on the class of share you buy.

For example, American Fund’s New Perspective Fund’s expense ratio ranges from 0.45% to 1.54%. The average expense ratio of a mutual fund that invests in stocks is 1.35%. Conversely, the average expense ratio of a Vanguard S&P 500 Fund is 0.10%. The difference of 1.25% is staggering over time.

5. Miscellaneous fees. Some advisors charge $50 – $100 a year per account to open or close an account, and even fees to dollar cost average your funds into the market.

6. Transaction fees. Every time you buy or sell a fund, a fee is typically paid to a custodian. These can range from $5 to hundreds of dollars per transaction.

7. Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

8. Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (or registered representatives) are simply required to sell products that are “suitable” for their clients.

A “suitable” investment is defined by FINRA as one that fits the level of risk that an investor is willing and able, as measured by personal financial circumstances, to take on. The Financial Industry Regulatory Authority is a private American corporation that acts as a Self Regulatory Organization (SRO) that regulates member stock brokerage firms and exchange markets. These criteria must be met. It is not enough to state that an investor has a risk-friendly investment profile. In addition, they must be in a financial position to take certain chances with their money. It is also necessary for them to

A hedge fund is a limited partnership of private investors whose money is managed by professional fund managers who use a wide range of strategies; including leveraging [debt] or trading of non-traditional assets [real-estate, collectible, commodities, cyrpto-currency, etc] to earn above-average returns. Hedge funds are considered a risky alternative investment and usually require a high minimum investment or net worth. This person is known as an “accredited investor” or “Regulation D” investor by the US Securities Exchange Commission and must have the following attributes:

A net worth, combined with spouse, of over $1 million, not including primary residence

An income of over $200,000 individually, or $300,000 with a spouse, in each of the past two years

Choose the fee structure. The fee structure should align with your needs. Consider the type of advice you seek, the number of times needed and the complexity of your financial situation. You can always negotiating tactics are free to ask for a better deal.

Compare fees. It is essential to research and compare different fees. Be sure to read the fine print for details or costs that are not a base fee.

Robo-advisors: For simple investment goals, with little specificity, robo-advisors may be a cost-effective option. They charge lower fees than conventional financial advisors and provide an automated, algorithmic approach to managing your investments.

Assessment

The average cost of working with a human financial advisor in 2024 was 0.5% to 2.0% of assets managed, $200 to $400 per hourly consultation, a flat fee of $1,000 to $3,000 for a one-time service, and/or a 3% to 6% commission fee on the product types sold.

When ruminating over financial advisory fees; read and understand the contract with disclosures, do not sign a confidentiality or non-disclosure agreement, and do not waive your right to a lawsuit. According to colleague Dr. Charles F. Fenton IIII JD, forced legal settlements almost always favor the advisor over the client.

2. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

The Hedge Fund manager I am considering is a Registered Investment Adviser [RIA]

QUESTION: What is a Registered Investment Advisor?

If the fund manager is an entity, then any individual you deal with will be a registered investment adviser representative. If the fund manager is an individual, then that individual is a registered investment adviser. In either case, the designation implies several steps have been taken.

In order to become a registered investment adviser, an individual must register for and pass the Series 65 Uniform Investment Adviser Law Exam, a three-hour, 130-question computer-based exam administered by the North American Securities Administrators Association. Topics covered include economics and analysis, investment vehicles, investment recommendations and strategies, and ethics and legal guidelines. A passing score is 70 percent or higher.

Once an individual has passed the Series 65, he or she must then apply via Form ADV to become a registered investment adviser. This application is made to either a state authority or to the SEC, depending on the adviser’s assets under management. If assets under management exceed $30 million, then the adviser must register with the SEC.

Form ADV consists of two parts. Part I provides general information to the regulatory authority. Part II is designed to be distributed to potential clients, and includes disclosure of a decent amount of information about the adviser. If the manager is a registered investment adviser, then you should expect to receive as part of the offering documentation either a current copy of Part II of the adviser’s Form ADV or a brochure that contains all the current information in Part II of Form ADV.

In addition to filing Form ADV and paying a small fee, the registered investment adviser becomes subject to extra administrative/regulatory burden as well as capital adequacy requirements that state the Adviser must maintain certain net worth levels.

By and large, because of the extra administrative burden as well as restrictions on certain activities, hedge fund managers attempt to avoid registering as investment advisers. Whether such managers can or cannot avoid such registration is largely dependent upon the state in which the manager operates. In California, for instance, hedge fund managers must register as investment advisers. In New York, such registration is not necessary. Not surprisingly, hedge fund managers located in California are rare, while they are quite plentiful in New York.

Absolute Return – the goal is to have a positive return, regardless of market direction. An absolute return strategy is not managed relative to a market index.

Accredited Investor – wealthy individual or well-capitalized institutions covered under Regulation D of the Securities Act of 1933.

Alpha – the return to a portfolio over and above that of an appropriate benchmark portfolio (the manager’s “value added”).

Arbitrage – any strategy that invests long in an asset, and short in a related asset, hoping the prices will converge.

Attribution – the process of “attributing” returns to their sources. For example, did the returns to a portfolio (over and above some benchmark) come from stock selection, industry/sector over- or under-weighting or factor weighting. Software programs are helpful in reporting an attribution.

Beta – a measure of systematic (i.e., non-diversifiable) risk. The goal is to quantify how much systematic risk is being taken by the fund manager vis-à-vis different risk factors, so that one can estimate the alpha or value-added on a risk-adjusted basis.

Correlation – a measure of how strategy returns move with one another, in a range of –1 to +1. A correlation of –1 implies that the strategies move in opposite directions. In constructing a portfolio of hedge funds, one usually wants to combine a number of non-correlated strategies (with decent expected returns) to be well diversified.

Drawdown – the percentage loss from a fund’s highest value to its lowest, over a particular time frame. A fund’s “maximum drawdown” is often looked at as a measure of potential risk.

Hurdle Rate – the return where the manager begins to earn incentive fees. If the hurdle rate is 5% and the fund earns 15% for the year, then incentive fees are applied to the 10% difference.

Leverage – one uses leverage if he borrows money to increase his position in a security. If one uses leverage and makes good investment decisions, leverage can magnify the gain. However, it can also magnify a loss.

Opportunistic – a general term that describes an aggressive strategy with a goal of making money (as opposed to holding on to the money one already has).

***

***

Pairs Trading – usually refers to a long/short strategy where one stock is bought long, and a similar stock is sold short, often within the same industry. Buying the stock of Home Depot and shorting Lowe’s in an equal amount would be an example.

Portfolio Simulation – involves testing an investment strategy by “simulating” it with a database and analytic software. Often referred to as “backtesting” a strategy. The simulated returns of the strategy are compared to those of a benchmark over a specific time frame to see if it can beat that benchmark.

Sharpe Ratio – a measure of risk-adjusted return, computed by dividing a fund’s return over the risk-free rate by the standard deviation of returns. The idea is to understand how much risk was undertaken to generate the alpha.

Short Rebate – if you borrow stock and then sell it short, you have cash in your account. The short rebate is the interest earned on that cash.

R-Squared – a measure of how closely a portfolio’s performance varies with the performance of a benchmark, and thus a measure of what portion of its performance can be explained by the performance of the overall market or index. Hedge fund investors want to know how much performance can be explained by market exposure versus manager skill.

Transportable Alpha – the alpha of one active strategy can be combined with another asset class. For example, an equity market-neutral strategy’s value-added can be “transported” to a fixed income asset class by simply buying a fixed income futures contract. The total return comes from both sources.

Value at Risk – a technique which uses the statistical analysis of historical market trends and volatilities to estimate the likelihood that a specific portfolio’s losses will exceed a certain amount.

“Malta has quietly leveraged the rising tide of the financial transparency imperative to attract hedge funds.“

There was a time when the quaint island sought to play on the traditional terrain, offering anonymity and a “laissez-faire regulatory regime,” not to mention very low taxes, as in no capital gains taxes and no taxes on dividends; all while English speaking and USD currency denominated.

***

***

While many leading domiciles for offshore hedge funds remain in the Caribbean – notably the Cayman Islands, the British Virgin Islands, Bermuda, and the Bahamas – the island of Malta is drawing attention, especially from European funds.

Posted on March 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

AGREE or DISAGREE?

By Staff Reporters

***

***

US Treasury Secretary Scott Bessent made waves yesterday with his comment that the American economy is facing a “detox period.”

Should we be seeing that this economy that we inherited [is] starting to roll a bit? Sure. And look, there’s going to be a natural adjustment as we move away from public spending to private spending. The market and the economy have just become hooked, and we’ve become addicted to this government spending, and there’s going to be a detox period. There’s going to be a detox” .

Bessent, a former hedge-fund manager, said during a CNBC interview.

“Employment should be from private companies, not from government. And I’m confident, if we have the right policies, it will be a very smooth transition.”

Bessent said, in an apparent reference to the layoffs of federal workers executed in large part by the entity known as the Department of Government Efficiency, which is run by Trump adviser Elon Musk.

DEFINITION: A Hedge fund is an investment partnership with freer rein to invest aggressively in a wider variety of financial products than most mutual funds. A hedge fund’s purpose is to pool funds, maximize investor returns, and eliminate risk with hedging strategies. Hedge funds are generally considered more aggressive, risky, and exclusive than mutual funds. The hedge fund industry has grown tremendously since its inception. There are trillions of dollars of assets under management, more than 8,800 hedge fund managers, and over 27,000 funds globally

Many physicians and other investors — even those that meet net worth guidelines — are surprised to learn that there exists a $500 – 999 billion, or more, alternative investment industry that is not generally marketed to the public. Such alternative investments have also been known as hedge funds or private investment funds.

Unlike mutual funds, these alternative investments can be structured in a wide variety of ways. Because of the very same regulations discussed above, these funds cannot be advertised, but they are far from illegal or illicit.

A hedge fund in the United States is generally a limited partnership providing a limited number of qualified investors with access to general partner investment decisions with little restriction in the type of investments or use of leverage. While the flexibility available to a hedge fund from a regulatory standpoint implies a high degree of potential risk, there is a wide range of investment philosophies, strategies, security types and objectives captured under the broad title of hedge fund.

Thus, generalizations regarding the characteristics of hedge funds are even less appropriate than with mutual funds, and evaluation of the investment characteristics and merits of a hedge fund strategy must be on a case-by-case basis. Likewise, the cost structure of a hedge fund often includes a base management fee to the general partner plus a performance-based fee or percentage of the profits, and must be evaluated on a case-by-case basis.

Several different investment vehicles operate under the oversight of varying regulatory bodies which provide access to an investment-managers’ discretionary decisions. While each approach generally represents ownership of an underlying pool of securities, there is usually a great deal of flexibility for the manager to deviate from a specific asset class or investment approach. Also, the fee structure of each vehicle can vary greatly and be quite large once distribution fees and sales charges are taken into account.

Thus, it is important for a medical professional to remember the following:

1. Evaluate the features and costs of an investment vehicle carefully;

2. Consider the cash flows and valuations of the securities that the manager or management approach will focus on as if the investments were being made directly, and above all;

3. Read the prospectus or agreement carefully before making any investment.

More than a few mutual, hedge and endowment fund managers have noted that they commonly compare their endowment and portfolio allocations to those of peer institutions and that as a result, allocations are often similar to the “average” as reported by one or more surveys/consulting firms.

One interviewed endowment fund manager expanded this thought by presciently noting that expecting materially different performance with substantially the same allocation is unreasonable. It is anecdotally interesting to wonder whether any “seminal” study “proving” the importance of asset allocation could have even had a substantially different conclusion. It seems likely that the pensions and funds surveyed in these types of studies have very similar allocations given the human tendency to measure one-self against peers and to use peers for guidance.

This is a truism in medicine as well as the financial services sector.

Understanding Peer Comparisons

Although peer comparisons can be useful in evaluating your portfolio, or your hospital or medical practice’s own processes, groupthink can be highly contagious and dangerous.

For historical example, in the first quarter of 2000, net flows into equity mutual funds were $140.4 billion as compared to net inflows of $187.7 billion for all of 1999. February’s equity fund inflows were a staggering $55.6 billion, the record for single month investments. For all of 1999, total net mutual fund investments were $169.8 billion[1] meaning that investors “rebalanced” out of asset classes such as bonds just in time for the market’s March 24, 2000 peak (as measured by the S&P 500).

Of course, physicians and investors are not immune to poor decision making in upward trending markets. In 2001, investors withdrew a then-record amount of $30 billion[2] in September, presumably in response to the September 11th terrorist attacks. These investors managed to skillfully “rebalance” their ways out of markets that declined approximately 11.5% during the first several trading sessions after the market reopened, only to reach September 10th levels again after only 19 trading days. In 2002, investors revealed their relentless pursuit of self-destruction when they withdrew a net $27.7 billion from equity funds[3] just before the S&P 500’s 29.9% 2003 growth.

Amateurs versus Professionals [is there such a thing?]

Although it is easy to dismiss the travails of mutual fund investors as representing only the performance of amateurs, it is important to remember that institutions are not automatically immune by virtue of being managed by investment professionals.

For example, in the 1960s and early 1970s, common wisdom stipulated that portfolios include the Nifty Fifty stocks that were viewed to be complete companies. These stocks were considered “one-decision” stocks for which the only decision was how much to buy. Even institutions got caught up in purchasing such current corporate stalwarts as Joe Schlitz Brewing, Simplicity Patterns, and Louisiana Home & Exploration. Collective market groupthink pushed these stocks to such prices that Price Earnings ratios routinely exceeded 50 [nothing in the internet age]. Subsequent disappointing performance of this strategy only revealed that common wisdom is often neither common nor wisdom.

The Bear Sterns Example

Recall that The New York Times reported on June 21, 2007, that Bear Stearns had managed to forestall the demise of the Bear Stearns High Grade Structured Credit Strategies and the related Enhanced Leveraged Fund. The two funds held mortgage-backed debt securities of almost $2 billion many of which were in the sub-prime market. To compound the problem, the funds borrowed much of the money used to purchase these securities. The firms who had provided the loans to make these purchases represented some of the smartest names on Wall Street, including JP Morgan, Goldman Sachs, Bank of America, Merrill Lynch, and Deutsche Bank.[4] Despite its efforts Bear Stearns had to inform investors less than a week later on June 27 that these two funds had collapsed. The subsequent fate of these firms, and the history of the past two years, need not be repeated to appreciate that the king surely had no clothes.

Assessment

What broader message lies in this post relative to such medical initiatives as P4P, various clinical quality improvement endeavors and benchmarks, hospital peer-review, PROs, Medicare compliance, etc?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES: