BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelsen CFA

***

***

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way.

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way: You have to come to the office every day, work long hours, slog through countless emails, be on top of your portfolio (that is, check performance of your securities minute by minute), watch business TV and consume news continuously, and dress well and conservatively, wearing a rope around the only part of your body that lets air get to your brain. Our colleagues judge us on how early we arrive at work and how late we stay. We do these things because society expects us to, not because they make us better investors or do any good for our clients.

Somehow we let the mindless, Henry Ford–assembly-line, 8:00 a.m. to 5:00 p.m., widgets-per-hour mentality dictate how we conduct our business thinking. Though car production benefits from rigid rules, uniforms, automation and strict working hours, in investing — the business of thinking — the assembly-line culture is counterproductive. Our clients and employers would be better off if we designed our workdays to let us perform our best.

Investing is not an idea-per-hour profession; it more likely results in a few ideas per year. A traditional, structured working environment creates pressure to produce an output — an idea, even a forced idea. Warren Buffett once said at a Berkshire Hathaway annual meeting: “We don’t get paid for activity; we get paid for being right. As to how long we’ll wait, we’ll wait indefinitely.”

How you get ideas is up to you. I am not a professional writer, but as a professional money manager, I learn and think best through writing. I put on my headphones, turn on opera and stare at my computer screen for hours, pecking away at the keyboard — that is how I think. You may do better by walking in the park or sitting with your legs up on the desk, staring at the ceiling.

I do my best thinking in the morning. At 3:00 in the afternoon, my brain shuts off; that is when I read my emails. We are all different. My best friend is a brunch person; he needs to consume six cups of coffee in the morning just to get his brain going. To be most productive, he shouldn’t go to work before 11:00 a.m.

And then there’s the business news. Serious business news that lacked sensationalism, and thus ratings, has been replaced by a new genre: business entertainment (of course, investors did not get the memo). These shows do a terrific job of filling our need to have explanations for everything, even random events that require no explanation (like daily stock movements). Most information on the business entertainment channels — Bloomberg Television, CNBC, Fox Business — has as much value for investors as daily weather forecasts have for travelers who don’t intend to go anywhere for a year.

Yet many managers have CNBC, Fox or Bloomberg TV/Internet streaming on while they work.

Turning 65 is often seen as the gateway to retirement—a time to slow down, reflect, and enjoy the fruits of decades of labor. But for some, including doctors who may have faced financial setbacks, poor planning, or unexpected life events, reaching this milestone without financial security can be deeply unsettling. The image of a broke 65-year-old doctor may seem paradoxical, given the profession’s reputation for high earnings. Yet, reality paints a more nuanced picture. Fortunately, even in the face of financial hardship, retirement is not a closed door—it’s a challenge that can be met with creativity, resilience, and strategic planning.

Understanding the Situation

Before exploring solutions, it’s important to understand how a physician might arrive at retirement age without adequate savings. Medical school debt, late career starts, divorce, health issues, poor investment decisions, or supporting family members can all contribute. Some doctors work in lower-paying specialties or underserved areas, sacrificing income for impact. Others may have lived beyond their means, assuming their high salary would always be enough. Regardless of the cause, the key is to shift focus from regret to action.

Traditional retirement—ceasing work entirely—is not the only option. For a broke 65-year-old doctor, retirement may mean transitioning to a less demanding role, reducing hours, or shifting to a new field. The goal is to create a sustainable lifestyle that balances income, purpose, and well-being.

Leveraging Medical Expertise

Even if full-time clinical practice is no longer viable, a physician’s knowledge remains valuable. Here are several ways to continue earning while easing into retirement:

Telemedicine: Remote consultations are in high demand, especially in primary care, psychiatry, and chronic disease management. Telemedicine offers flexibility, reduced overhead, and the ability to work from home.

Locum Tenens: Temporary assignments can fill staffing gaps in hospitals and clinics. These roles often pay well and allow for travel or seasonal work.

Medical Writing and Reviewing: Physicians can write for journals, websites, or pharmaceutical companies. Peer reviewing, editing, and content creation are viable options.

Teaching and Mentoring: Medical schools, nursing programs, and residency programs need experienced educators. Adjunct teaching or mentoring can be fulfilling and financially helpful.

Consulting: Doctors can advise healthcare startups, legal teams, or insurance companies. Their insights are valuable in product development, litigation, and policy.

Exploring Non-Clinical Opportunities

Some physicians may wish to pivot entirely. Transferable skills—critical thinking, communication, leadership—open doors in other industries:

Health Coaching or Life Coaching: With certification, doctors can guide clients in wellness, stress management, or career transitions.

Entrepreneurship: Starting a small business, such as a tutoring service, online course, or specialty clinic, can generate income and autonomy.

Real Estate or Investing: With careful planning, investing in rental properties or learning about the stock market can create passive income.

Maximizing Government and Community Resources

At 65, individuals become eligible for Medicare, which can significantly reduce healthcare costs. Additionally, Social Security benefits may be available, depending on work history. While delaying benefits until age 70 increases monthly payments, some may need to claim earlier to meet immediate needs.

***

***

Other resources include:

Supplemental Security Income (SSI): For those with limited income and assets.

SNAP (food assistance) and LIHEAP (energy assistance): These programs help cover basic living expenses.

Community Organizations: Nonprofits and religious groups often provide support with housing, transportation, and social engagement.

Downsizing and Budgeting

Reducing expenses is a powerful way to stretch limited resources. Consider:

Relocating: Moving to a lower-cost area or state with favorable tax policies can reduce housing and living expenses.

Selling Assets: A large home, unused vehicle, or collectibles may be converted into cash.

Shared Housing: Living with family, roommates, or in co-housing communities can cut costs and reduce isolation.

Minimalist Living: Prioritizing needs over wants and embracing simplicity can lead to financial and emotional freedom.

Creating a realistic budget is essential. Track income and expenses, eliminate unnecessary costs, and prioritize essentials. Free budgeting tools and financial counseling services can help.

Financial stress can take a toll on mental health. It’s important to cultivate resilience and maintain a sense of purpose. Strategies include:

Staying Active: Physical activity improves mood and health. Walking, yoga, or swimming are low-cost options.

Volunteering: Giving back can provide structure, community, and fulfillment.

Learning New Skills: Online courses, hobbies, or certifications can reignite passion and open new doors.

Building a Support Network: Friends, family, and peer groups offer emotional support and practical advice.

Planning for the Future

Even at 65, it’s not too late to plan. Consider:

Debt Management: Negotiate payment plans, consolidate loans, or seek professional help.

Estate Planning: Create a will, designate healthcare proxies, and organize important documents.

Insurance Review: Ensure adequate coverage for health, life, and long-term care.

Financial Advising: A fee-only advisor can help create a sustainable plan without selling products.

Embracing a New Chapter

Retirement is not a destination—it’s a transition. For a broke 65-year-old doctor, it may not look like the glossy brochures, but it can still be rich in meaning. By leveraging experience, reducing expenses, accessing resources, and nurturing well-being, retirement becomes a journey of reinvention.In many ways, doctors are uniquely equipped for this challenge. They’ve faced long hours, high stakes, and complex problems. That same grit and adaptability can guide them through financial hardship and into a fulfilling retirement.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Sometimes debt is a necessary tool in building wealth

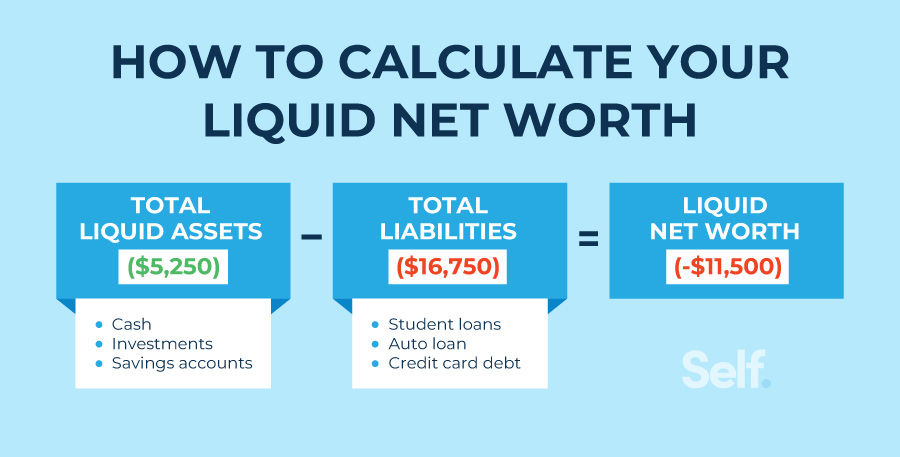

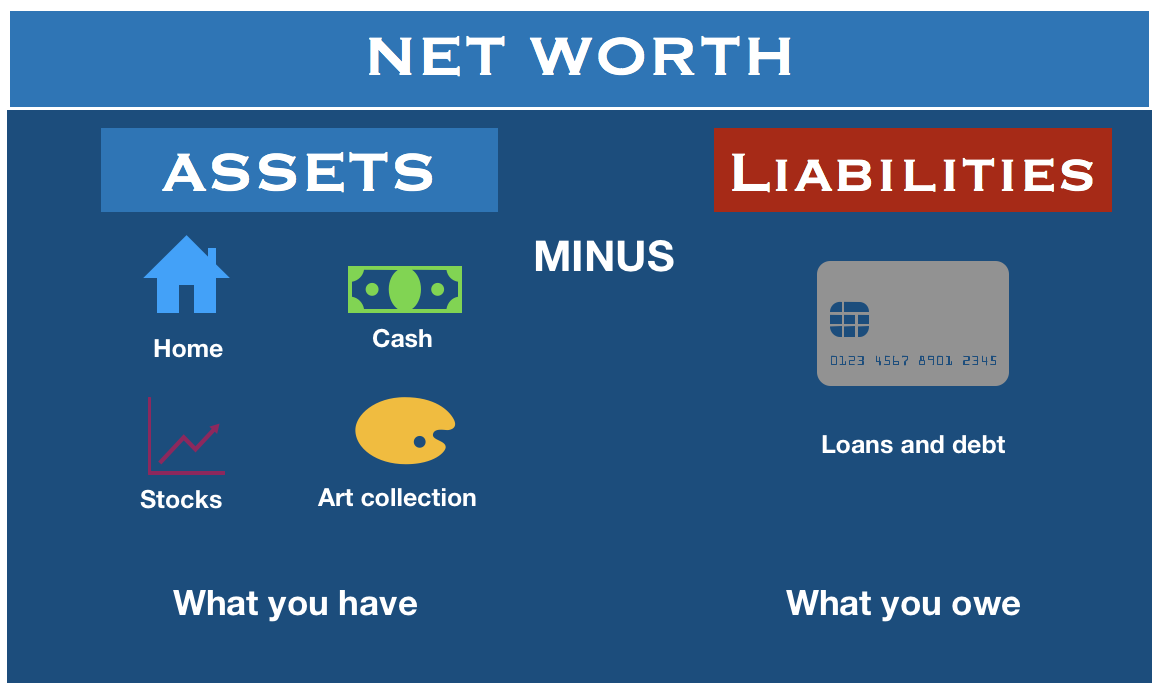

Using debt to build wealth might seem counterintuitive. After all, when you calculate your wealth, you look at what you own (assets) and subtract what you owe (debts and liabilities) to determine what your net worth (wealth) is.

It’s easy to oversimplify that debt is bad and is harmful to your wealth. Because some debt is really harmful, like credit cards, automobile, debt gets lumped into the category of “bad.”

But some types of debt can be useful and sometimes necessary to create wealth; home, education, business, etc. For folks that don’t readily have access to large sums of cash or capital, debt may be the tool that allows them to expand.

According to Medical Economics, there were 10 clinic and physician practices filing bankruptcy in 2024, making it the highest level of the last six years, according to a new analysis of cases with liabilities of at least $10 million.

Meanwhile, the Steward Health Care System bankruptcy, which was based in Massachusetts but making headlines across the nation, has become “the largest hospital sector bankruptcy by far in the last 30 years,” according to a new analysis by Gibbins Advisors, based in Nashville, Tennessee.

Health care bankruptcy filings totaled 57 last year, down from 79 in 2023, said “Healthcare Restructuring: Trends and Outlook.” The report analyzed Chapter 11 health care bankruptcy cases with liabilities of at least $10 million, since 2019.

Last year’s total was down 28% from 2023’s peak, but greater than the 2019 to 2022 average of 42 filings a year, the report said.

Bankruptcy, often considered a last financial resort, is a legal process that can help alleviate outstanding debts for individuals and businesses. Reasons to file for bankruptcy can include divorce, job loss, exorbitant medical bills or credit card debt.

There are several types of bankruptcy — six, as a matter of fact. The two most common types of bankruptcy for individuals are Chapter 7 and Chapter 13.

But there are four other types as well: Chapter 9, Chapter 11, Chapter 12 and Chapter 15. And, the type of bankruptcy filed depends on the situation.

Regardless of which type, the process is typically the same: You’ll usually retain an attorney and make your case before a judge, who will then erase some debts or set up a repayment plan.

Also note that an eligibility requirement — for all bankruptcy chapters — is that you must undergo credit counseling within the 180 days before filing.

Net worth is everything you own of significance (Assets) minus what is owed in debts (Liabilities). Assets include cash and investments, real estate, cars and anything else of value.

How is net worth calculated? Assets – Debt = Net Worth. Net worth is calculated by adding all owned assets (anything of value) and then subtracting all of your liabilities.

Is net worth yearly? No, net worth is not yearly. Net worth isn’t inherently yearly but is often tracked on an annual basis to assess financial progress year over year.

What net worth is considered wealthy, rich and upper class? In the U.S. salary average is around $59,000, and only 20% of Americans have a household income of $100,000 or more.

Is net worth the same as net income? No, net worth is not the same as net income. Net income is what you actually bring home after taxes and payroll deductions, like Social Security and 401(k) contributions.

Can one measure their net worth if they don’t have many assets or a high income? Yes. Knowing your net worth isn’t about the amount you have; it’s about understanding your financial position. It helps you track your progress, informs your financial decisions, and motivates you to improve your financial health, regardless of where you start.

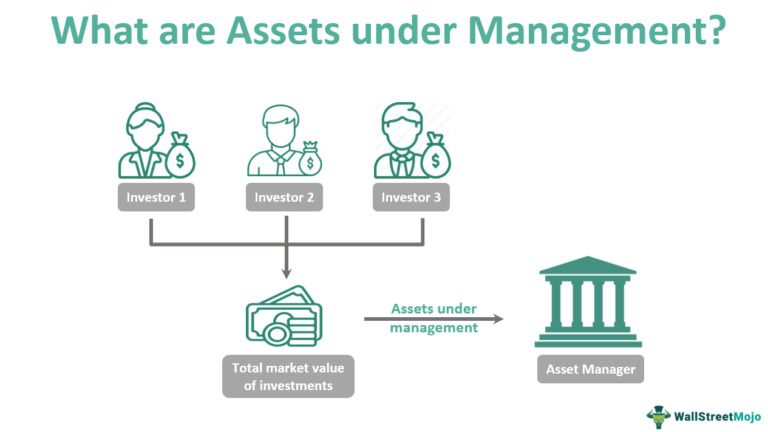

Assets under management (AUM) is a significant parameter in the financial world. It answers financial questions like – how many investments does a company manage? What is the net value of the investments that the company manages? Finally, how many investors have trusted their assets with the company? The higher the answer to these three questions, the more glory to the company.

A wealthy investor who is not concerned by higher fees but wants maximum returns of their asset will probably choose an asset manager based on its AUM. Thus, the AUM indicates the financial performance of the firm. Also, based on the funds under management, the firm collects fees from other clients.

So, what are the investments which qualify as AUM? Any liquid asset of the investor they have entrusted the asset manager with monitoring and control. For example, bank deposits, cash balances, equity shares, bonds, mutual funds, and other investments.

What are the services an asset manager provides to their clients? The most important function is decision-making. With the constant fluctuations and rapid movements in the market, an asset manager has to make decisions about holding or selling an investment. The firm communicates with the investors and advises them about the necessary action.

Once the decision is taken, the firm acts on the decision, i.e., the investor does not have to enter the field. In addition, the asset management company will buy, sell, and make any other transactions on behalf of the investor. Finally, the firm also renders services like accounting, tax reporting, proxy voting (equity shares), client reporting, and other financial services.

What are Assets Under Advisement?

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this scenario is when an adviser reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisers opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

In retirement, according to Josephine Nesbit, your economic class can be broadly categorized into four distinct groups, each defined by their net worth and financial capabilities, ranging from retirees with limited resources to the wealthy. And, according to Moneywise, here are the net worth categories of the poor, middle class (and upper-middle class) and rich:

Poor retirees: Poor retirees are in the lower 20th percentile, and may have a net worth of around $10,000. This is often without property ownership, forcing many to rely mainly on Social Security or minimal pensions.

Middle-class retirees: Making up the 50th percentile, with a median net worth of approximately $281,000, this group usually includes home equity, retirement savings and a 401(k) plan.

Upper-middle-class retirees: These retirees possess a net worth between $201,800 and $608,900. They have diversified assets and enjoy a comfortable retirement cushion.

Rich retirees: In the 90th percentile, with net worth starting at $1.9 million, this group has much more financial freedom and is able to afford luxuries and legacy planning.

Once the value of all personal assets and liabilities is known, net worth can be determined with the following formula: Net worth = assets minus liabilities. Obviously, higher is better.

In The Millionaire Next Door, Thomas H. Stanley, PhD, and William H. Danko give the following benchmark for net worth accumulation. Although conservative for physicians of a past generation, it may be more applicable in the future because of current managed care environment. Here is the guide: Multiple your age by your annual pre-tax income from all sources; except inheritances, and then divide by ten.

Example:

As an HMO pediatrician, Dr. Curtis earned $ 90,000 last year. So, if she is 35, her net worth should be at least $ 315,000.

How do you get to that point? In a word, consume less and save more. Stanley and Danko found that the typical millionaire set aside 15 percent of earned income annually and has enough invested to survive 10 years, at current income levels if he stopped working.

Question: If Dr. Curtis lost her job tomorrow, how long could she pay herself the same salary? Could you?