HOW IT WORKS

SPONSOR: http://www.CertifiedMedicalPlanner.org

By Dr. David E. Marcinko MBA CMP®

***

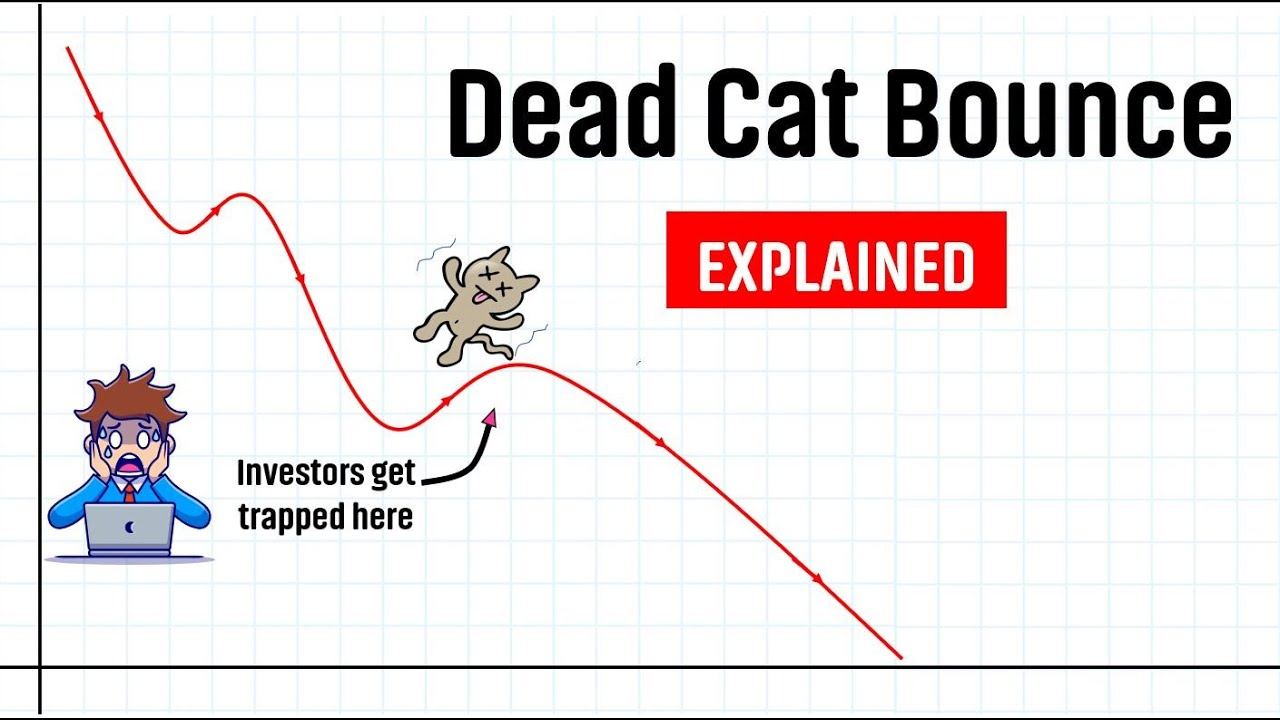

In finance, a dead cat bounce is a small, brief recovery in the price of a declining stock.

****

***

Derived from the idea that “even a dead cat will bounce if it falls from a great height”, the phrase, which originated on Wall Street, is also popularly applied to any case where a subject experiences a brief resurgence during or following a severe decline.

- The dead cat bounce is a sudden and temporary increase in stock price caused by investors erroneously believing that the stock price’s reached its lowest.

- The dead cat bounce can only be fully accurately determined with concrete data in hindsight.

- Both falsely identifying a stock price trough (i.e., falling victim to a dead cat bounce) and falsely identifying a true price trough as a dead cat bounce will result in negative financial consequences.

CITE: https://www.r2library.com/Resource/Title/0826102549

YOUR COMMENTS ARE APPRECIATED.

Thank You

***

Share this:

Filed under: "Ask-an-Advisor", CMP Program, Glossary Terms, Investing | Tagged: certified medical planner, CMP, David Edward Marcinko, dead cat bounce, financial dead cat bounce, stock bounce | Leave a comment »