***

By Michael A. Gayed, CFA

Portfolio Manager of the ATAC Rotation Funds

***

| Bob Farrell is a legendary Wall Street trader and market analyst. He’s perhaps best-known for his “10 rules” of investing that he developed based on his 50-year career in the industry. One of the more popular rules says that “when all the experts and forecasts agree, something else is going to happen.”Right now, almost everyone is expecting a recession driven by high inflation, rising interest rates and geopolitical risks. The S&P 500 is still more than 10% off of its highs, while the NASDAQ 100 is down by more than 20%. Many feel as if more downside is ahead, but what if they’re wrong? What if the bottom is already in? What if the worst is over? My take? I have no idea. I believe there’s still a bigger and more traditional classic “risk-off” period coming where stocks decline and Treasuries rally in price (which is what historically happens during periods of heightened equity volatility), but the path to get there is what drives investor sentiment. And like everyone else in this business, I can’t tell the future. All I can do is identify conditions in a rules-based fashion that favor an outcome.The important thing to remember here is that the market isn’t the economy. The financial markets are often leading indicators of where investors feel things are going. The actual data is only showing how conditions are or were. Take the 2020 COVID recession, for example. Once the government announced its multi-trillion dollar stimulus program, stock prices shot higher even though the worst of the economic pain had yet to be experienced.Today, some of the data isn’t even indicating imminent danger. |

|

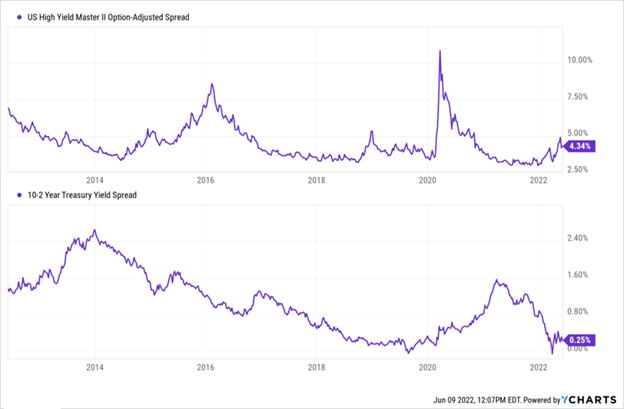

| High yield spreads tend to blow out ahead of a recession. They’re currently not at the levels reached during 2016, 2018 or 2020. Investors often view the 10-year/2-year Treasury yield spread as the “recession indicator”. This number did briefly turn negative earlier this year, but has remained in positive territory ever since. While both of these numbers have teased the idea of higher risk conditions ahead, neither has done so in convincing fashion yet.Also consider that the markets tend to be very sensitive to what the Fed does. If the central bank ever decides that recession risk is too high and it hits the pause button on the rate hiking cycle, it could be off to the races again for equity prices. Risk asset prices have the ability to react favorably to looser monetary conditions. Any pivot in that direction could give a big boost to investor sentiment. If the bear market is over, the ATAC Rotation Fund (ATACX), the ATAC U.S. Rotation ETF (RORO) and the ATAC Credit Rotation ETF (JOJO) could be primed to benefit.We believe all three funds use proven market signals to determine whether they should be positioned either offensively or defensively. Since investors often flock to safety in times of market volatility, the three funds use Treasuries as the “risk-off” or defensive asset class. Admittedly, Treasuries haven’t acted as they historically do relative to equities when in high volatility states. But that doesn’t mean things won’t revert back to historical behavior in the small sample of the here and now.When the signals suggest that conditions are more favorable, the funds can go “risk-on”. In the case of RORO and ATACX, that could include some combination of large-cap stocks, small-caps and emerging markets. JOJO remains in the fixed income markets and targets junk bonds in this scenario.RORO and ATACX also use leverage, which offers higher return potential. Why? Because leveraging equities when risk-on helps to, over time, counter the impact of being in Treasuries when stocks continue to move higher and with hindsight, risk-off positioning there wasn’t warranted. Of course this is a double-edged sword, since in a year like this year, the leveraged risk-on position in stocks earlier in the year led to a sizeable decline for both ATACX and RORO. However, over multiple roll of the die, it is that leverage which gives investors the opportunity to capture above average returns in more traditional markets when combined with occasional risk-off periods where Treasuries perform well.High volatility markets don’t need to be feared. We believe strategies that add and remove market risk based on what the market is telling us give investors the opportunity to earn superior risk-adjusted returns while lowering downside risk. If the markets are ready to begin the next leg higher, the ATAC funds stand ready to benefit while (hopefully) Treasuries get back to doing what they normally would in true risk-off periods . At some point. |

***

COMMENTS APPRECIATED

Thank You

***

***

Share this:

Filed under: Experts Invited, Investing | Tagged: Bear Market is OVER, bear markets, Bob Farrell, Michael A. Gayed |

Leave a comment