BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS OF NEW DEADLINE

By Staff Reporters

***

***

The Treasury Department has set a new deadline of March 21st 2025 for millions of businesses to fulfill a new reporting requirement on “beneficial ownership information,” after a court order allowed the federal agency to start enforcing the measure.

The Corporate Transparency Act, which Congress enacted in 2021, requires small businesses to disclose the identity of people who directly or indirectly own or control the company. The measure aims to prevent criminals from hiding illicit activity conducted through shell companies or opaque ownership structures, according to the Treasury.

Posted on April 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST– Today’sNewsletter

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

NEW YORK (Reuters) -The U.S. accounting watchdog on Wednesday said it has hit KPMG Netherlands with a $25 million civil penalty, a record for the regulator, in response to “egregious” and widespread exam cheating at the foreign affiliate of the major audit firm.

As millions of Americans approach age 66, they face the inevitable question, is it time to retire? The physician population is aging alongside the general population—more than 40% of physicians in the U.S. will be 65 years or older within the next decade. In the case of surgeons, there is little guidance on how to best ensure their competency throughout their career and at the same time maintain patient safety while preserving mature physician dignity.

It is a scenario playing out nationwide. From Oregon to Pennsylvania, hundreds of communities have in recent years either stopped adding fluoride to their water supplies or voted to prevent its addition. Supporters of such bans argue that people should be given the freedom of choice. The broad availability of over-the-counter dental products containing the mineral makes it no longer necessary to add to public water supplies, they say. The Centers for Disease Control and Prevention says that while store-bought products reduce tooth decay, the greatest protection comes when they are used in combination with water fluoridation.

More health systems are going to be opting out of Medicare Advantage (MA) plans, George Hill, a managing director at Deutsche Bank in Boston, predicted Monday at a “Wall Street Comes to Washington” webinar hosted by the Brookings Institution. “I think you’re going to see more large provider organizations threaten to opt out of networks, particularly as it relates to MA,” Hill said, adding that there are a number of reasons for this. “Prior authorizations are the problem, claims denials are a huge problem, delayed payments and rates are the problem — barriers in access to care in all varieties are the problem.”

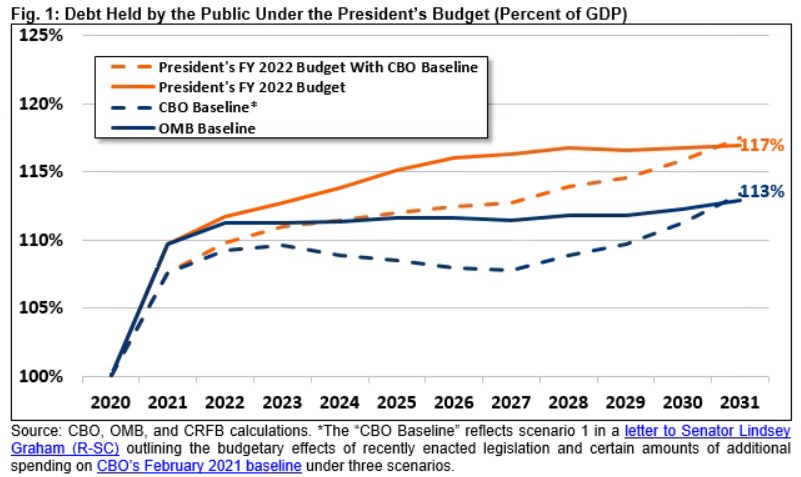

The latest budget update from the nonpartisan Congressional Budget Office (CBO) found that the federal government has spent more on paying interest on the national debt than on the military in fiscal year 2024. The CBO’s budget report for March showed that the U.S. has spent $412 billion on military programs at the Department of Defense through the first half of FY-2024, according to preliminary figures from CBO and the Treasury Department.

Consumer price increases remained high last month, boosted by gas, rents, and car insurance, the government said Wednesday in a report that will likely give pause to the Federal Reserve as it weighs when and by how much to cut interest rates this year. Prices outside the volatile food and energy categories rose 0.4% from February to March, the same accelerated pace as in the previous month. Measured from a year earlier, these core prices were up 3.8%, unchanged from the year-over-year rise in February. The Fed closely tracks core prices because they tend to provide a good read of where inflation is headed.

Here’s where the major benchmarks ended:

The S&P 500® index (SPX) dropped 49.27 points (1.0%) to 5,160.64; the Dow Jones Industrial Average lost 422.16 points (1.1%) to 38,461.51; the NASDAQ Composite® ($COMP) fell 136.28 points (0.8%) to 16,170.36.

The 10-year Treasury note yield (TNX) soared more than 18 basis points to 4.548%.

The CBOE Volatility Index® (VIX) jumped 0.82 to 15.80.

Interest-rate-sensitive sectors like banks, real estate, and utilities led Wednesday’s decliners. The KBW Regional Bank Index (KRX) tumbled 5% to its lowest point since late November. The small-cap Russell 2000® Index (RUT) lost 2.5%. Energy shares were among the few gainers as WTI Crude Oil (/CL) futures rebounded after three-straight losing sessions.

In other markets, the U.S. dollar index (DXY) jumped 1% to a five-month high amid expectations interest rates will remain elevated.

Posted on October 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The U.S. government on Friday posted a $1.695 trillion budget deficit in fiscal 2023, a 23% jump from the prior year as revenues fell and outlays for Social Security, Medicare and interest costs on the federal debt rose significantly.

The Treasury Department said the deficit was the largest since a COVID-fueled $2.78 trillion gap in 2021 and marks a major return to ballooning deficits after back-to-back declines during President Joe Biden’s first two years in office. The deficit comes as Biden is asking Congress for $100 billion in new foreign aid and security spending, including $60 billion for Ukraine and $14 billion for Israel, along with funding for U.S. border security and the Indo-Pacific region.

The S&P 500® Index was down 53.84 points (1.3%) at 4,224.16, down 2.4% for the week; the Dow Jones Industrial Average (DJI) was down 286.89 points (0.9%) at 33,127.28, down 1.6% for the week; the NASDAQ Composite was down 202.37 points (1.5%) at 12,983.81, down 3.2% for the week.

The 10-year Treasury note yield was up about 8 basis points at 4.907%.

CBOE’s Volatility Index (VIX) was up 0.26 at 21.71.

Small-cap stocks, which are considered to be more exposed to economic uncertainty, were also soft, as the Russell 2000 Index (RUT) dropped to a 12-month low and was 2.2% lower for the week.

Gold futures rose 2.3% for the week and ended near a three-month high, as the fighting in the Middle East fueled demand for assets considered to be safe havens. Volatility based on the VIX spiked to its highest level since March.

The federal government on January 19th reached its approximately $31.4 trillion debt ceiling — which legally caps how much the U.S. can borrow to pay for what tax and other revenue doesn’t cover — and the Treasury Department has since been using “extraordinary measures” along with its current cash flow to keep the government’s obligations paid.

“CBO estimates that under its baseline budget projections, the Treasury would exhaust those measures and run out of cash sometime between July and September of this year,” according to the report.

Posted on January 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

As the US just crashed into the $31.4 trillion debt ceiling as the Treasury Department began taking what it called “extraordinary measures” to prevent the government from defaulting on its debts and sparking an economic crisis.

These measures are a series of deep-cut accounting moves that allow the Treasury to continue making its payments. They include:

Suspending reinvestments into government funds for retired federal employees, such as the Civil Service Retirement and Disability Fund.

Selling existing investments in those funds to free up more outstanding debt.

And while these measures definitely aren’t ordinary…they probably aren’t so “extra,” either. The Treasury has resorted to them more than 12 times since 1985, including during the last debt-ceiling standoff in 2021.

Still, these steps amount to chugging water after eating a ghost pepper—the pain will return. Treasury Secretary Janet Yellen said her extraordinary measures will last through early June, giving lawmakers about five months to work out a deal to raise the debt ceiling.

NOTE: The US has never defaulted on its debt, but even the threat of it could be disastrous. The country’s first credit downgrade in history came during a debt-ceiling showdown in 2011.

Yesterday, Treasury Secretary Tim Geithner for the first time acknowledged the depths of the problems, but didn’t offer any new solutions. He committed to release more detailed data on how banks and other servicers are faring—a promise Treasury first made six months ago.

Geithner Speaks

“We are concerned by the wide variation in performance we see across servicers and by the countless frustrated phone calls we receive from borrowers,” Geithner testified yesterday before Congress. He added that the Treasury was “troubled” by “reports that servicers have foreclosed on potentially eligible homeowners” and frequent complaints from homeowners that servicers lose their documents. He said servicers are “not doing enough to help homeowners” and that it was not “acceptable.”

From the Treasury Department

This isn’t the first time Treasury Department officials have directed some tough talk [4] at servicers, including vague threats [5] of penalties [6]. But it remains to be seen whether, as Geithner says, the Treasury will follow through and punish servicers that break the program’s rules. Under the program, which involves paying incentives to servicers, investors and homeowners to encourage modifications, the Treasury has the power to punish servicers by withholding those payments. But Treasury has never issued any such penalties. Nor has the government outlined how much such penalties might be.

Geithner did promise to publish within a month or two more detailed information about each servicer’s performance, data that could give a much clearer picture of how servicers are treating homeowners. Treasury officials have actually been promising to release this sort of data since last year [7]. In December, Herb Allison, the official in charge of the TARP, said [8] it would be released in January. Like everything else with the government’s loan mod program, it’s taken several months longer than it was supposed to.

More Granular Data

The new, more detailed data will show how long it takes each servicer to answer calls from homeowners, how long they take to process applications, and the number of customer complaints each receives. A Treasury spokeswoman also said the reports will provide some sort of breakdown of how many people have been denied mods for which reasons, but it’s not clear yet if that data will be made available by servicer.

Up until now, the Treasury has only been releasing basic information for each of the largest servicers. And each month, we’ve transformed that data into an easy-to-digest breakdown [9].

Assessment

One major problem, the data show, has been the large volume of homeowners in limbo (376,000 as of March). A trial period under the program is supposed to last three months, but for those homeowners, it’s stretched longer, sometimes as long as ten months [6]. In total, 1.2 million homeowners have started trials since the program launched a year ago, but only 231,000 have made it to a permanent modification.

And so, your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe. It is fast, free and secure.

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on April 12, 2010 by Dr. David Edward Marcinko MBA MEd CMP™

In Financial Reform Bill

By Marian Wang, ProPublica – April 2, 2010 2:10 pm EDT

Remember how earlier this week, in a post about financial reform and liquidity requirements [1], we noted how vague [2] Treasury Secretary Tim Geithner was being with The New York Times about setting hard and fast rules about how much cash should be required to hold?

Here’s what we excerpted from the Times on Tuesday: Mr. Geithner insists that if there is one change that needs to be made to the banking system to protect it against another high-stakes bank run like the one that claimed the life of Lehman Brothers, increasing capital requirements is it.

Pinning Down Geithner

But try pinning down Mr. Geithner, or anyone else in the Beltway, on how much capital banks should be required to keep, or even how the word “capital” should be defined, and certainties disappear.

Turns out he had a lot more to say on the subject than what he told the Times. Mike Konczal [3], blogging for Ezra Klein, unearthed a letter Geithner sent to a lawmaker in January, explaining his hesitancy—really, his opposition—to setting fixed capital requirements in current financial reform proposals. From the letter [4]:

Although the Administration strongly supports imposing a simple, non-risk-based leverage constraint on banks, bank holding companies, and other major financial firms, we do not believe that codifying a specific numerical leverage requirement in statute would be appropriate.

Assessment

So when Geithner said, “We have not made a judgment yet on the number,” what he really was thinking—if this letter is any indication—is that as far as financial reform legislation itself goes, he doesn’t want a number, period. And when it comes to actually imposing tighter capital requirements on financial institutions, he wants the Treasury, the Fed or some combination of regulators to have a free hand to pick and change the number. In other words, pretty close to the way things are now.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES: